Principal and Agent Relationships

in the Financial Crisis in 2008

Authors

Preface

The topic of the work deals with the consequences of the principal-agent relationships in the financial crisis of the year 2008, particularly the one of relationships in the AIG. The following questions are dealt with: What kind of relationships are there? Which characteristics do these relations have? Which possible solutions there are to defuse the problems in these relation-ships?

This scientific work was made in the context of the module Business Science. The module is part of the Master of Science of Business Information Systems course of the University of Applied Sciences Northwestern Switzerland (www.fhnw.ch/msc-bis). The work was carried out as teamwork. For the co-ordination of the group the service "Google Sites" was used (sites.google.com/site/bsrgwaig).

We would like to thank all persons and organization who have made for this work a contribu-tion. We thank the authors for their engagement at the search for literature and writing the contributions. We also thank the company Google for the provisioning of the services which has made a smooth cooperation possible.

Olten in December 2008

Table of Contents

Preface... I Executive Summary...II Table of Contents...III List of Figures and Tables...V List of Abbreviations...VI

1 The American International Group...1

1.1 History...1

1.2 Products...1

1.3 Vision & Values...2

1.4 Corporate Governance...2

2 Situation of the AIG Today...4

2.1 Chain of the events leading to the call for help at the FED...4

2.2 Situation at the Stock Exchange...6

2.3 Income Situation...7

3 Research Approach and Related Theory...9

3.1 Research Approach...9

3.1.1 Research Question...9

3.1.2 Hypothesis...9

3.1.3 Specific Aim...9

3.1.4 Related Theory for the Principal – Agent Relationships at the AIG...10

4 Principal – Agent Relationships...12

4.1 Relationship “AIG Financial Products – Insurance Customer (Banks)“ (Michael)...12

4.1.1 Characteristics of the Relationships...12

4.1.2 Problematic Nature of the Relationships...12

4.1.3 Solutions to Improve the Relationship...12

4.2 Relationship “AIG Holding – AIG Financial Products (Joseph J. Cassano)“ (Steffi)...13

4.2.1 Characteristics of the Relationships...13

4.2.2 Problematic Nature of the Relationships...13

4.3 Relationship “AIG Financial Products (Joseph J. Cassano) – Rating

Agen-cies“ (Simon L.)...14

4.3.1 Characteristics of the Relationships...14

4.3.2 Problematic Nature of the Relationships...14

4.3.3 Solutions to Improve the Relationship...14

4.4 Relationship “AIG Financial Products (Joseph J. Cassano) – Consultatnt (Gary Gorton)” (Simon N.)...15

4.4.1 Characteristics of the Relationships...15

4.4.2 Problematic Nature of the Relationships...15

4.4.3 Solutions to Improve the Relationship...15

5 Conclusion...16

List of Literature...17

List of Figures and Tables

Figure 1-1: AIG Situation: A tiny unit at American International Group... (The New York Times 2008)...4 Figure 1-2: AIG Situation: ...was well compensated for generating a significant share of

revenue... (The New York Times 2008)...5 Figure 1-3: AIG Situation: ... from selling contracts that protected clients from losses on

debt (The New York Times 2008)...5 Figure 1-4: AIG Situation: Punished by rating agencies into a downward spiral (The

New York Times 2008)...6 Figure 1-5: AIG (Common Stock) Chart from November 15, 2007 to November 14,

2008 compared to the DowJones Index (BigCharts 2008)...6 Figure 1-6: Overview on the quarterly income since 2003 (NYTimes X)...8

List of Abbreviations

AIG American International Group, Inc. CDO Collateralized Debt Obligation

1

The American International Group

The American International Group, Inc. (AIG) is a world leader in insurance and financial ser-vices. It is an international insurance organization with operations in more than 130 countries (AIG 2008c).

The AIG holding companies serve commercial, institutional and individual customers through a worldwide property-casualty and life insurance networks of any insurer. AIG companies are providers of retirement services, financial services and asset management.

AIG's common stock is listed at the New York Stock Exchange, and at the stock exchanges in Ireland and Tokyo.

1.1 History

According AIG (AIGx), the company history of AIG started in 1919, when Cornelius Vander Starr founded an insurance agency named American Asiatic Underwriters in Shanghai, fol-lowed by decades of expansion. Despite some difficulties in wartimes, Vander Starr estab-lished several companies like Asia Life Insurance Company, American International Under-writers, The Philippine American Life and General Insurance Company and American Inter-national Assurance Company, Ltd, represented in about 75 countries by the end of the 1960s. The firm American International Group, Inc. (AIG) was formed in 1967 and went pub-lic two years later with Maurice R. Greenberg as President and CEO.

Greenberg "was the chairman of the American International Group from 1968 to 2005, during which time he built the small insurance company into what became the world’s largest insur-ance and financial services corporation" (nytimes x).

Considering the context of today’s financial crisis and AIG's tarnished position, a very impor-tant step in AIG's history may be what AIG entitles with "Expanding into Financial Services" (AIGx): In 1987, AIG Financial Products Corp. was formed in 1987 to specialize in complex derivative product transactions later followed by other AIG company foundations including leasing, banking and real estate.

Concerning the company leadership, the past years brought more changes than the previous decades: Greenberg "was succeeded by Martin J. Sullivan and President and CEO […]" who "[…] resigned from AIG in 2008, and was succeeded as CEO by Robert B. Willumstad. […] Mr. Willumstad now holds both the CEO and Chairman positions" (AIGx).

1.2 Products

AIG offers product in four principal business segments (AIG 2008c):

Life Insurance & Retirement Services: AIG has the most extensive global network of any life insurer, a leading U.S. life insurance organization and a premier retirement services franchise with a leadership position in the U.S. fixed annuities market as well as a grow-ing international network.

Financial Services: AIG has a major presence in aircraft finance, capital markets, con-sumer finance and insurance premium finance.

Asset Management: AIG provides institutional and individual assets, retail funds and pri-vate banking through a growing global network.

1.3 Vision & Values

The vision which has given itself the AIG:

“To be the world’s first choice provider of insurance and financial services. We will create un-matched value for our customers, colleagues, business partners, and shareholders, as we contribute to the growth of sustainable, prosperous communities.” (AIG 2008b)

The values which has given itself the AIG:

“Our mission at AIG is to provide our customers all over the world with exceptional products and exemplary service; however, this goal can only be realized if we are consistently guided by our shared beliefs - our values.” (AIG 2008b)

1.4 Corporate Governance

The AIG’s Board of Directors has established the AIG Corporate Governance Guidelines to promote the effective functioning of the Board and its committees, to promote the interests of shareholders and to establish a common set of expectations for the governance of the orga-nization.

The Corporate Governance Guidelines contains:

Director Independence Standards

Charters of Audit

Compensation and Management Resources

Finance

Nominating and Corporate Governance

Public Policy and Social Responsibility

Regulatory, Compliance and Legal Committees

Director, Executive Officer and Senior Financial Officer Code of Business Conduct and Ethics

2

Situation of the AIG Today

Today, AIG is in a very uncomfortable situation due to the financial crisis. Being the chain of the events represented briefly in the following as it has come to the FED to the call for help. And as the AIG share has developed at the stock exchange in the recent year.

2.1 Chain of the events leading to the call for help at the FED

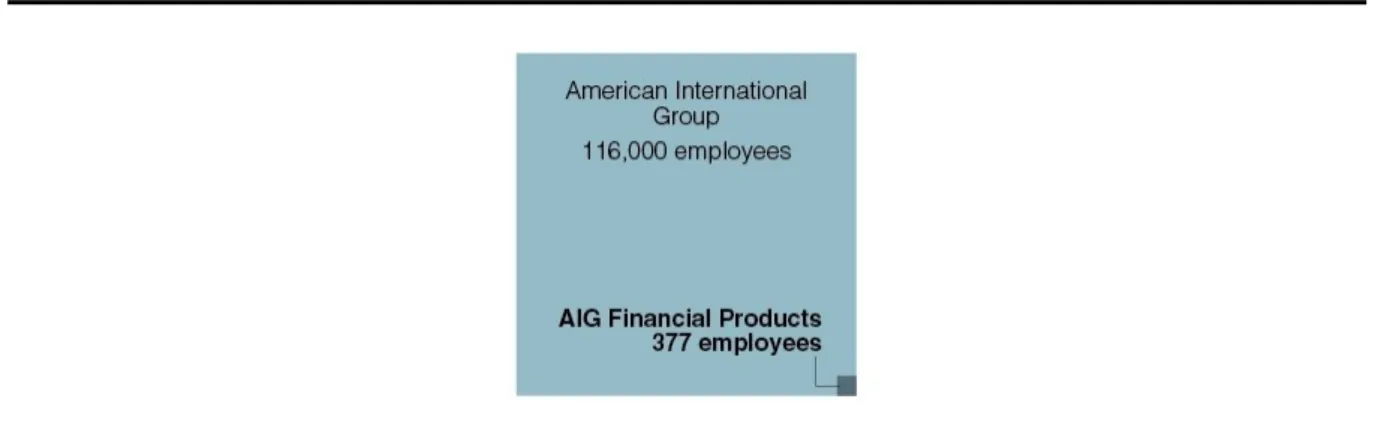

The New York Times has illustrated what happened that brought AIG in this difficult situation today, with a short sequence of text and charts. The interesting fact is that all information published in this sequence was found in reports of the AIG itself. The New York Times (2008) has the opinion that a tiny unit at American International Group brought the giant to the edge of bankruptcy: The London unit AIG Financial Products which sold complex finan-cial contracts called credit derivatives.

Figure 2-1: AIG Situation: A tiny unit at American International Group... (The New York Times 2008)

Compensation: Revenues:

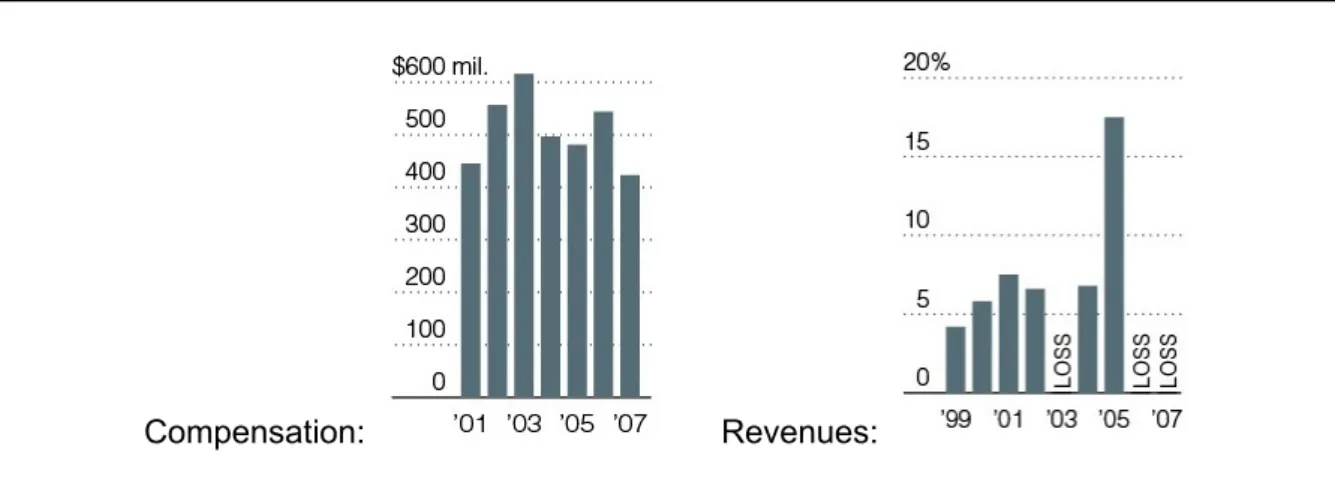

Figure 2-2: AIG Situation: ...was well compensated for generating a significant share of rev-enue... (The New York Times 2008)

The Financial Products unit generated these revenues from selling contracts that protected clients from losses on debt. They insured $513 billion of debt against default using credit-de-fault swaps. $78 billion worth of insured debt was affected by the decline in the U.S. housing market. But as certain debt losses increased, A.I.G. was forced to enlarge its own financial reserves and lower the value of some of its own holdings. Ratings agencies punished the company, ultimately forcing it into a downward spiral.

Figure 2-3: AIG Situation: ... from selling contracts that protected clients from losses on debt (The New York Times 2008)

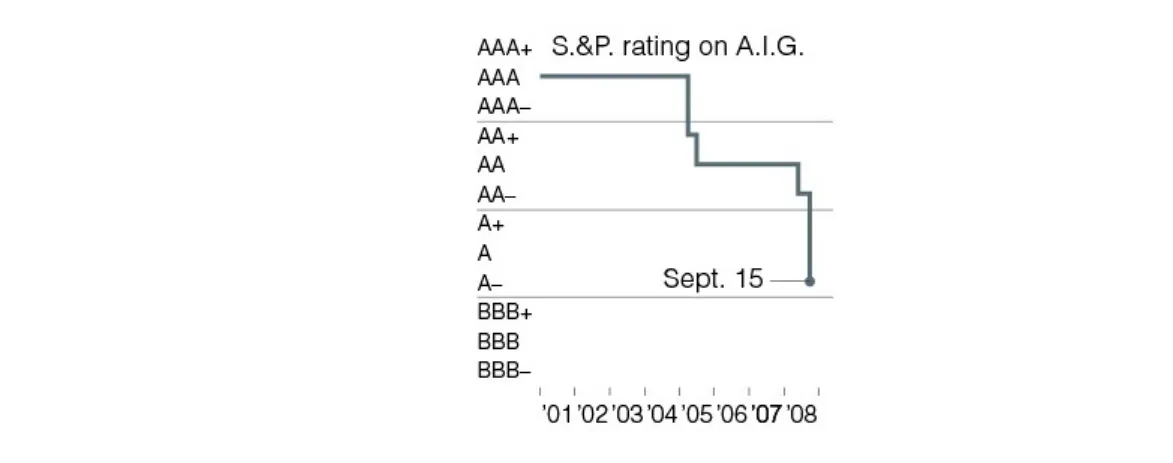

Figure 2-4: AIG Situation: Punished by rating agencies into a downward spiral (The New York Times 2008)

2.2 Situation at the Stock Exchange

As capital concerns and potential mortgage-related losses continue to bother AIG the share prices drop substantially. During the peaks of the crisis nervous investors continued to sell their shares and hammered AIG stocks. The behavior of rating agencies and customers could also begin to punish the company.

Shares in AIG fell more than 60 percent on Monday 15th of September and the company’s

potential write-offs were mounting and reached 60 to 70 billion dollars.

There is a basic pattern: the lower the stock price, the harder it can be for the firm to raise capital. The lower the capital the bigger the concerns, and so on. If this goes on for a while the firm finds itself close to bankruptcy and there is no other possibility than governmental help. This is exactly what happened to AIG.

Table 2-1: AIG (Common Stock) November 14, 2008 (BigCharts 2008)

Price 2.08 Change + 0.02

52 Week High 62.30 52 Week Low 1.25

Currency US Dollar Exchange NYSE

2.3 Income Situation

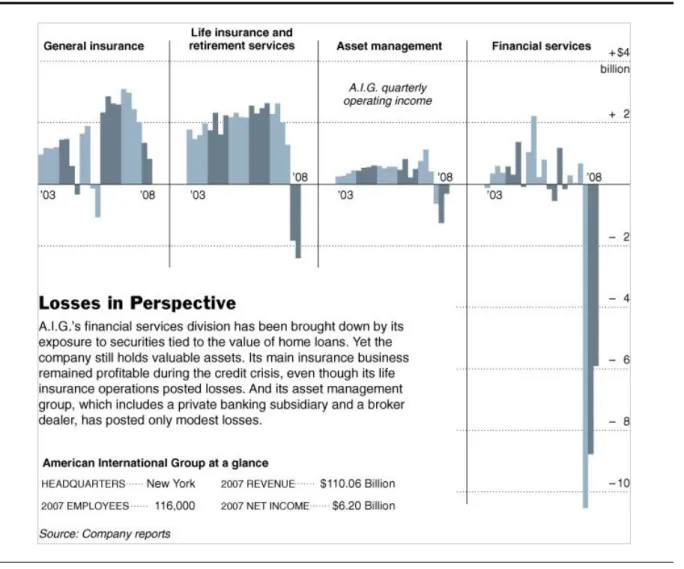

The consolidated financial results are structured according the main operating segments which are described in chapter 1.2. The following chart shows the development of AIG's fi-nancial results in the past 5 years. In particular the disproportional losses are conspicuous. Whilst the losses of other units (life insurance or asset management) are in the range of their profits in previous years, the financial services segment shows enormous losses since the last quarter of 2007. Concretely financial services accounted a loss of 10'523 million dollars in the third quarter of 2007 (AIGXY). The financial report of 2007 (AIG-z) declares a loss of $ 9'515 million, noting, that this "includes an unrealized market valuation loss of $11.5 billion on AIGFP’s super senior credit default swap portfolio".

What is not shown in the chart: In the third quarter of 2008, actually the unit general insur-ance had a loss of $2,5 billion, life insurinsur-ances even $15,3 billion and financial services $ 8,2 billion leading to a total net income of $ -37,6 billion for the first 9 month of this year (AIG XZ).

Even though AIG's balance sheet contains a total assets value of more than 1 trillion dollars (AIG-z) and (AIG xz), AIG was apparently not able to comply with its short term liabilities any-more. According Reuters, AIG asked the Fed for financial support on September 15 2008 (Reuters 1). On October 9, New York Fed promises $ 37,8 billion to AIG (Reuters 2). Since then, the US government agreed multiple bailout strategies for AIG, by now reaching support of up to $ 150 billions (Reuters 3).

Reuters 3: http://www.reuters.com/article/ousiv/idUSTRE4A92FM20081110 Reuters 2: http://de.reuters.com/article/topNews/idDEBEE49800S20081009 Reuters 1: http://de.reuters.com/article/topNews/idDEMIG52008220080915 AIGXY: Press release 6 2008

http://media.corporate-ir.net/media_files/irol/76/76115/releases/Q407_Press_Release_fi-AIG XZ: Press release 9 2008

http://media.corporate-ir.net/media_files/irol/76/76115/releases/AIG%203Q08%20Press %20Release.pdf

AIG-z

http://www.ezodproxy.com/AIG/2008/AR2007/images/AIG_AR2007.pdf

3

Research Approach and Related Theory

In this chapter the research approach and the theory used about principal – agent relation-ships are explained. Approach and theory are valid for all four examined relationrelation-ships.

3.1 Research Approach

The research approach includes the research question, the hypothesis derived from it and the specific aim on which one has worked towards for results.

3.1.1 Research Question

As it is represented chapters above in detail, there were some events at the AIG which indi-cate the existence of hidden information in principal – agent relationships. Hidden information often is the reason that risks are not recognized correctly or assessed wrongly. Or that den information is used of one party for the better of one's own. It also can happen that hid-den information is not analyzed at all since two parties trust themselves very strongly. The examination question therefore is:

Were too high risk aversion, moral hazard and blind confidence responsible for the fi-nancial crisis of AIG and how is it possible to prevent these situations in their princi-pal-agent relationship in the future?

3.1.2 Hypothesis

From the research question the hypothesis can directly be derived. The parties in the princi-pal – agent relationships must be stirred up that they have less hidden information and are willing on a common objective regarding reduction of risks. The hypotheses therefore are:

The risk of hidden information must be shared up equally between principal and agent. One result from the spread of the risk will be lesser moral hazard.

With risk guidelines it can be prevented that in financial transactions a too high risk is taken even if there exists apparently not the slightest risk in the financial transactions.

3.1.3 Specific Aim

With pursuing of the specific aim the hypotheses made has to be proved. In the chapter 4 were four specific principal – agent relationships situations of the AIG explained. On these relationships it is shown that the claims made can be fulfilled. The specific aim therefore is:

3.1.4 Related Theory for the Principal – Agent Relationships at the AIG

In the following chapter we will comment on the theory regarding the principal – agent rela-tionship in AIG. A principal-agent model is first developed to formulate the asymmetry of in-formation in knowledge sharing.

A principal-agent relationship has arisen between two or more parties when one, designated as the agent, acts for, on behalf of, or as representative for the other, designated the princi-pal, in a particular domain of decision problems. The agent is empowered to act for the prin-cipal because the prinprin-cipal chooses to hire the agent or because there is an implicit contract between principal and agent. The Principal agent problem lies in the fact that differences of interest and information between the two parties mean that the agent may not always act in the interests of the principal.

The principle agent problem describes the effect of the agent’s motivation or incentive in exe-cuting their task, and how it satisfies the desired objectives of a task. In mortgage lending, the agents of the lenders functioned with their own compensation in mind: They originated mortgages and helped people obtain mortgages, regardless of whether it seemed like they could afford it of if they were even being truthful in their application, as they were paid their fee by origination. They operated, as most everyone does, with their self-interest in mind. Agency problems can be classified in three big categories: Moral Hazard describes situa-tions, in which the agent uses information not observable by the principal which is than called hidden information or performs actions not observable by the principal hidden action) in order to increase his own utility against the principal’s best interest.

The second category Holdup describes situations in which the agent systematically uses gaps in incomplete contracts, in which not every future state is specified, in his favor After the closing of the contract and after specific investments have been made and sunk costs have been incurred by the principal, the agent reveals his previously hidden intentions openly in-terpreting the fulfillment of his commitments in his favor and forcing the principal into renego-tiations

The third category Adverse Selection is a problem that appears in markets where one party cannot discriminate between good and bad quality of the other party, i.e. the other party has hidden characteristics. The orientation of the price at an average quality can induce good quality suppliers to leave the market and can ultimately cause a market breakdown. Even though this is not clearly a hierarchical relationship it is often summarized as an agency prob-lem.

The principle agent problem plays a key role in the current financial crisis 2007 / 2008 also called the subprime mortgage crisis. The global financial crisis really started to show its ef-fects in the middle of 2008. Around the world stock markets have fallen, large financial insti-tutions have collapsed or been bought out, and governments in even the wealthiest nations have had to come up with rescue packages to bail out their financial systems.

in other cases, the governments of the wealthiest nations in the world have resorted to exten-sive bail-out and rescue packages for the remaining large banks and financial institutions. While explaining the cause of this crisis seems complicated to even the best of minds, it seems a proximate cause for bankruptcies like AIG was excessive investment in instruments like credit default swaps that insured the debt of other institutions like Goldman and then sent AIG down-under once the housing bubble decided to burst.

4

Principal – Agent Relationships

Michael: Each team has to analyze the situation regarding principal/agent-relationships:

4.1 Relationship “AIG Financial Products – Insurance Customer (Banks)“ (Michael)

General description of the Relationship Who is agent and who is principal? Why? Hypothesis and Sub-Hypothesis

4.1.1 Characteristics of the Relationships

What are the objectives / interests of the agent? What are the objectives / goals of the principal? What are current measures in this relationship? Where are possible hidden information?

What are possible hidden actions?

4.1.2 Problematic Nature of the Relationships

Are there cases of adverse selection (Risk Aversion)? Why? What are the consequences of this adverse selection? Are there situations of moral hazard / unequal risk? What are the consequences of this moral hazard?

4.1.3 Solutions to Improve the Relationship

Explicit Contract Implicit Contracts Regulations

Each team has to work out regarding the relationship:

How could we align the agent’s interests to the principal’s objectives?

How could we write explicit incentive contracts / regulations / effective measures for this relationship?

Each team has:

to propose a concept how to motivate the agent to apply this proposal.

to analyze possible side-effects of their proposal.

4.2 Relationship “AIG Holding – AIG Financial Products (Joseph J. Cassano)“ (Steffi)

General description of the Relationship Who is agent and who is principal? Why? Hypothesis and Sub-Hypothesis

4.2.1 Characteristics of the Relationships

What are the objectives / interests of the agent? What are the objectives / goals of the principal? What are current measures in this relationship? Where are possible hidden information?

What are possible hidden actions?

4.2.2 Problematic Nature of the Relationships

Are there cases of adverse selection (Risk Aversion)? Why? What are the consequences of this adverse selection? Are there situations of moral hazard / unequal risk? What are the consequences of this moral hazard?

4.2.3 Solutions to Improve the Relationship

Explicit Contract Implicit Contracts Regulations

Each team has to work out regarding the relationship:

How could we align the agent’s interests to the principal’s objectives?

How could we write explicit incentive contracts / regulations / effective measures for this relationship?

Each team has:

to analyze possible side-effects of their proposal.

4.3 Relationship “AIG Financial Products (Joseph J. Cassano) – Rating Agencies“ (Simon L.)

General description of the Relationship Who is agent and who is principal? Why? Hypothesis and Sub-Hypothesis

4.3.1 Characteristics of the Relationships

What are the objectives / interests of the agent? What are the objectives / goals of the principal? What are current measures in this relationship? Where are possible hidden information?

What are possible hidden actions?

4.3.2 Problematic Nature of the Relationships

Are there cases of adverse selection (Risk Aversion)? Why? What are the consequences of this adverse selection? Are there situations of moral hazard / unequal risk? What are the consequences of this moral hazard?

4.3.3 Solutions to Improve the Relationship

Explicit Contract Implicit Contracts Regulations

Each team has to work out regarding the relationship:

How could we align the agent’s interests to the principal’s objectives?

How could we write explicit incentive contracts / regulations / effective measures for this relationship?

Each team has:

to prove why their proposal to align the interests will work!

to propose a concept how to motivate the agent to apply this proposal.

4.4 Relationship “AIG Financial Products (Joseph J. Cassano) – Consultatnt (Gary Gorton)” (Simon N.)

General description of the Relationship Who is agent and who is principal? Why? Hypothesis and Sub-Hypothesis

4.4.1 Characteristics of the Relationships

What are the objectives / interests of the agent? What are the objectives / goals of the principal? What are current measures in this relationship? Where are possible hidden information?

What are possible hidden actions?

4.4.2 Problematic Nature of the Relationships

Are there cases of adverse selection (Risk Aversion)? Why? What are the consequences of this adverse selection? Are there situations of moral hazard / unequal risk? What are the consequences of this moral hazard?

4.4.3 Solutions to Improve the Relationship

Explicit Contract Implizit Contracts Regulations

Each team has to work out regarding the relationship:

How could we align the agent’s interests to the principal’s objectives?

How could we write explicit incentive contracts / regulations / effective measures for this relationship?

Each team has:

to prove why their proposal to align the interests will work!

to propose a concept how to motivate the agent to apply this proposal.

List of Literature

AIG: Riesenverlust und neue Hilfe, (2008, November 10). AIG: Riesenverlust und neue Hilfe. baz.online. Retrieved November 11, 2008, from http://www.bazonline.ch/wirtschaft/un-ternehmen-und-konjunktur/AIG-Riesenverlust-und-neue-Hilfe/story/22372795

AIG used billions from Fed but hasn't said for what; International Herald Tribune; By Mary Williams Walsh

American International Group, Inc., (2008, November 4). Information about AIG. Retrieved November 6, 2008, from http://www.aig.com/About-aig_20_19308.html

American International Group, Inc. (June 15, 2008). Corporate Governance Guidelines. Re-trieved November 14, 2008, from http://library.corporate-ir.net/library/76/761/76115/ items/300256/Corporate_Governance_Guidelines_061508.pdf

A principal-agent model for incentive design in knowledge sharing, Ning Nan

Asset Securitisation: Die Geschäftsmodelle von Ratingagenturen im Spannungsfeld einer Principal-Agent-Betrachtung; Zeitschrift für das gesamte Kreditwesen 9/2008, S. 393-396; von Stefan Morkötter und Dr. Simone Westerfeld

Dr. David Garson, (2006) Key Concepts and Terms of the Principal-Agent Theory

Drucker, Jesse, (2008). AIG's Tax Dispute With U.S. Has Twist of Irony. The Wall Street Jounal Online. Retrieved November 14, 2008, form http://online.wsj.com/article/ SB122662579362126965.html?mod=MKTW&ru=MKTW

Haubrich, Joseph, (1994). Risk aversion, performance pay, and the principal-agent problem [Electronic version]. Journal of Political Economy 102, 258-276.

Lauchlan T. Munro (2001) A Principal-Agent Analysis of the Family: Implications for the Wel-fare State - Focus on Economic Sociology

Moral Hazard and Observability, Bengt Holmstrom

Morgenson, Gretchen, (September 27, 2008). The Reckoning: Behind Insurer’s Crisis, Blind Eye to a Web of Risk. The New York Times. Retrieved November 14, 2008, from http:// www.nytimes.com/2008/09/28/business/28melt.html?_r=1&oref=slogin

Nilesh Fernando (2008) Principal, Agents and Bailouts

Principal-Agent Problems in Venture Capital; WWZ/Department of Finance, Working Paper No. 11/03; Stefan Duffner

Sappington, David E M, (1991). Incentives in Principal-Agent Relationships [Electronic ver-sion]. Journal of Economic Perspectives, American Economic Association, vol. 5(2), 45-66. Spring.

THE DEVELOPMENT OF PRINCIPAL–AGENT, CONTRACTING AND ACCOUNTABILITY RELATIONSHIPS IN THE PUBLIC SECTOR: CONCEPTUAL AND CULTURAL PROBLEMS, Jane Broadbenta,Michael Dietricha and Richard Laughlin

The New York Times, (2008). An Insurance Giant, Brought Down, Retrieved November 14, 2008, from http://www.nytimes.com/imagepages/2008/09/27/business/

20080928_MELT_GRAPHIC.html

Wikipedia, (2008, November 5). American International Group. Retrieved November 6, 2008, from http://en.wikipedia.org/wiki/AIG

Wikipedia, (2008, November 10). APA style. Retrieved November 11, 2008, from http:// en.wikipedia.org/wiki/APA_style