WIRELESS INNOVATION: BRIDGING THE MOBILITY GAP

INDUSTRY OVERVIEW FROM A VENTURE CAPITAL PERSPECTIVE

Information has been obtained from sources believed to be reliable but Fairview Capital does not warrant its

completeness or accuracy. Opinions expressed in this report constitute our judgment as of the date of this material and are subject to change without notice. Past performance is not indicative of future results. The recipients of this report must make their own decisions regarding any securities or investment ideas mentioned herein.

1

Table of Contents

Introduction ... 2 Industry Overview ... 2 Infrastructure ... 3 Devices ... 4 Operating Systems ... 4 Software ... 5 Investment Themes ... 7 Advertising ... 7 Gaming ... 8Mobile Payment Services ... 9

Venture Activity... 9

Notable Exits ... 10

2

Introduction

Advances in wireless technology have transformed the way we communicate, gather information and operate in our daily lives. Consumers have become increasingly dependent on this technology. Consider the use of the smartphone – these phones have increased access to data and have simplified communication. We can access unlimited information and stay constantly connected with mobile phones. As a result, landline replacement in homes is accelerating as consumers shift to wireless usage, resulting in the acceleration of growth in the wireless ecosystem. New, faster networks are being built to handle significant volumes of data. Advertisers are beginning to find innovative methods to brand themselves on mobile media. All of the aforementioned phenomena are driven by our increased reliance on wireless connectivity for messaging, social networking, and access to content. Wireless is becoming an essential part of our culture and daily living, and the necessity for innovation continues to grow.

As the wireless evolution becomes more about simplifying people’s lives and giving greater access to new technology, consumer demand continues to rapidly increase. This rising demand has created more opportunities for venture capital and private equity investors to make attractive investments in new technology. Additionally, investment in the development of wireless devices and technology will help to expand market opportunities. Venture capital and private equity investment in the wireless industry can help the industry rapidly progress towards any device, any application, anytime for all consumers.

Industry Overview

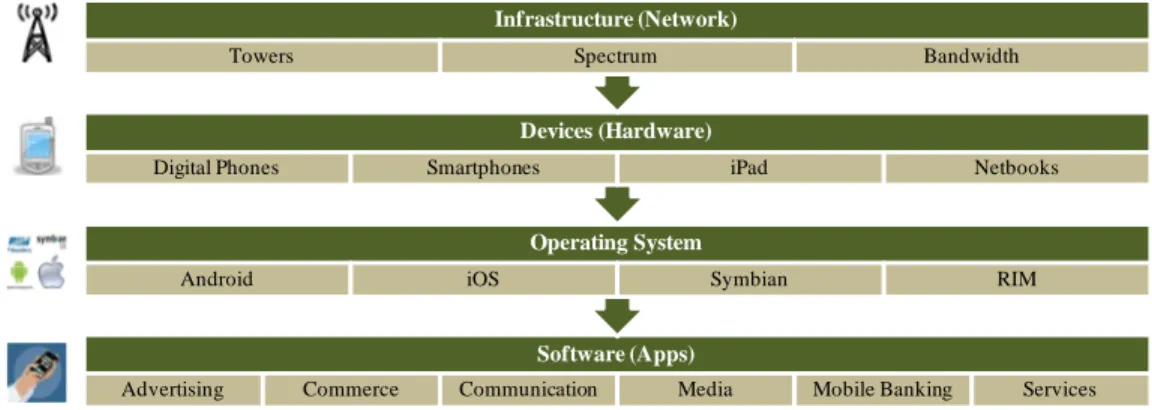

The wireless ecosystem is composed of the following: infrastructure, devices, operating systems, and software.

Figure 1 – The Wireless Ecosystem

Source: FCC; Fairview Capital

The entire ecosystem enables the delivery of different types of mobile media (e.g. apps, content, and mobile commerce), which become easier to access as the ecosystem evolves.

Software (Apps)

Advertising Commerce Communication Media Mobile Banking Services

Operating System

Android iOS Symbian RIM

Devices (Hardware)

Digital Phones Smartphones iPad Netbooks

Infrastructure (Network)

3 The wireless industry is primarily consumer-driven. As consumers expect more from devices (e.g. more information, increased communication, and faster access), wireless technology will improve to meet demands. The wireless industry increases profitability based on the ability to meet consumer expectations, and the pace of innovation has been directly tied to consumerism and consumer spending on devices.

Advances in wireless technology have had non-traditional growth that has outpaced most other industries. Mobile content and applications have taken on a life of their own. For example, consider the iPhone and how it has transformed smartphones. The demand for data through mobile devices is 10 times greater for iPhone users compared to other smartphones users. As consumers demand more access to data, Apple has created devices that have superior technological capabilities to meet consumer needs. Google and Research in Motion (RIM) have subsequently developed and released smartphones to compete directly with the iPhone.

The proliferation of smartphones and the development of new, attractive features are driving more consumers to smartphones. Today’s networks allow consumers to send and receive data faster than ever before. The capabilities of wireless technology coupled with strong consumer demands, make this an increasingly attractive industry.

Infrastructure (Network)

The 1960s ushered in a new era of communication. The initial purpose of cellular communication was to connect mobile users in cars to a fixed public network. These connections were transmitted over an analog cellular network, and would eventually become known as 1G, the first generation of wireless telephone technology. 1G wireless networks allowed users to only make voice calls over the network. First generation (1G) networks were eventually replaced by second generation (2G) networks.

Developed in the 1980s, 2G networks are all digital and based on low-band digital data. The most popular 2G wireless technology is known as Global Systems for Mobile Communications (GSM). GSM, a commonly available international network, is still used by over four billion people across more than 200 countries for cellular phone calls. Compared to 1G, 2G systems provided better quality and higher capacity at lower costs to consumers. 2G wireless technology can handle data capabilities such as fax and short message service (SMS) data, while 1G was not capable of handling these types of data. Third generation, or 3G, networks were deployed in 2001 as a result of advancements in wireless radio technology. The network can handle large volumes of data due to its increased bandwidth. 3G networks allow for faster data transfer speeds, increased voice performance and the addition of other key network capabilities, such as the ability to send images and video over the cellular network. 3G has enabled consumers to access multimedia entertainment, location-based services via GPS, and highly interactive services such as video on demand through mobile devices. While there are tremendous benefits of 3G networks, they only allow for data downloading at speeds up to approximately 14 megabytes/second, which is slow relative to most fixed connections.

4 Operators have recognized that consumers now demand wireless capabilities at higher speeds. Therefore, operators have acknowledged the need for a more robust infrastructure, which can now be supported by the advanced technology of 4G. 4G networks are planned to have transmission rates 10 times faster than current 3G networks, and will exhibit the latest advances in wireless technology, allowing consumers to send and receive more data than ever before. These networks are expected to provide broadband, large capacity, and high speed data transmission, providing users with high quality color video, images, lower costs, and increased mobility.

Devices (Hardware)

The evolution of the mobile phone has been synchronous with the development of the wireless infrastructure. Each evolution of the wireless infrastructure brought about changes in mobile phones. Phones quickly went from large, clunky devices in the 1980s that were limited to phone calls, to very small, compact devices capable of using enhanced voice services, sending and receiving text and pictures, being able to surf the internet, and allowing users to consume other forms of media. The evolution of mobile devices is strongly tied to consumers’ growing desire to always be connected.

In 1993, IBM released Simon, the first smartphone. This device was the first attempt to converge critical business applications such as a pager, calendar, note pad, and address book into one handheld device. Over the ensuing years, other smartphone devices came to the market, utilizing the wireless infrastructure of the time. Since 2007, several companies have released smartphones that utilize touchscreens, enable multimedia, and have become the mobile device of choice to access the internet. These devices are regarded as one of the fastest growing consumer electronic segments.

While smartphones account for 44% of total handset sales, there is one clear leader for consumer smartphone preference: Apple’s iPhone. The iPhone’s introduction in 2007 signified a new era in mobile usage. The iPhone sold over 6.1 million units over a period of five quarters, and was one of the first smartphones with touchscreen capability. The device’s ability to connect to the internet over Wi-Fi or the 3G network has allowed users to consume media in ways they were never able to do before. With the iPhone, users can easily browse web pages similar to the experience on a PC. Users can also read documents, access email, consume media such as music, pictures and movies, and even browse and download applications for a host of uses. It can be argued that the iPhone is not really a phone, but a computer that makes phone calls. Smartphones with Google’s Android operating system appear to be pursuing a similar strategy, and RIM’s Blackberry devices seem to be progressing in the same direction.

Operating Systems

Each mobile device is linked to an operating system (OS) platform. As mobile phones become more like miniature computers, the OS gives access to a variety of features and functionality such as built-in cameras, gyroscopes and GPS. Figure 2 shows the market share of various smartphone devices by operating system.

5 Figure 2 – Smartphone Device Market Share by Operating System

Source: Gartner (May 2010)

Nokia’s Symbian and RIM have the largest market share of smartphone sales to consumers by operating system. Symbian is very popular in under-developed countries due to the low cost of the mobile phones that still utilize 2G networks while RIM, through its early technology lead with the Blackberry, captures a large segment of the business market. In the past year, Symbian and RIM have lost ground to other smartphones as their relative advantages have been assailed by competitors. Symbian’s market share decreased 4.5%, and RIM decreased 1.2%. In contrast, Apple’s iPhone’s market share increased 4.9%, and Google’s Android increased 8%.

Each iteration of smartphone devices and operating systems has given way to new possibilities for data usage and access. Smartphones have evolved into devices that we increasingly rely on for data access and communication, and there is excitement around the future possibilities for usage and applications. This enthusiasm has created a high level of interest in developing applications, content and media specific for mobile devices. For venture capital and private equity investors, this enthusiasm presents a unique opportunity to invest in a rapidly growing market segment.

Software (Apps)

The average US mobile phone user spends 70% of their time on voice calls and 30% using data. Conversely, iPhone users, only spend 45% of their time on voice, while the majority of time is spent on data consumption. The consumption of larger amounts of data can be attributed to the availability and use of mobile applications - software programs specifically developed for mobile devices that have become widely known as “Apps”. Nokia Symbian 44% RIM 19% Apple iPhone OS 15% Google Android 10% Microsoft Windows Mobile 7% Linux 4% Other OS 1%

6 Figure 3 - Daily Usage Breakdown

Source: Morgan Stanley (June 2010)

The increased use of data by iPhone users may be partially due to how Apple changed the dynamics of application distribution. In the early days of mobile application development, wireless carriers were the only ones able to distribute mobile applications to consumers. In the last few years, driven by Apple’s launch of the App Store, wireless companies have relaxed their policies and have allowed subscribers to access and use applications developed and distributed by third parties. Developers now have a direct-to-consumer approach to reach end users and are less reliant on carriers.

The iPhone has experienced significant traffic in its App Store where consumers download applications. As Figure 4 shows, the iPhone has more than 200,000 Apps available, and users have downloaded more than four billion Apps since the device launched. These statistics surpass any other mobile smartphone currently on the market. The average number of Apps downloaded per user to the iPhone is more than double its closest competitor. Comparatively, 50,000 Apps have been downloaded to Android devices and 5,000 to Blackberry devices.

Cell Phone iPhone

Other Music E-mail SMS Voice 40 Minutes Average Use per Day 60 Minutes Average Use per Day 70% 15% 9% 2% 4% 19% 10% 12% 14% 45%

7 Figure 4 - Apps Downloads by Device

Source: Morgan Stanley (June 2010)

More consumers are using applications on the mobile device to access data and content via the internet. Several applications available today allow users to search for data on mobile devices using 3G technology without reliance on conventional internet connectivity found through PCs or laptops. comScore reported that 30% of mobile owners now browse the mobile internet, with more than one million additional mobile users starting to browse the mobile internet each month since January 2009. Social networking is also driving much of this data consumption as individuals share pictures, videos and messages on the internet via their smartphones. Mobile social networking users are showing the highest gain at 80% year over year growth from 2009 to 2010.

Investment Themes

Investment is happening across the entire wireless ecosystem. The Apps subsegment has experienced a significant amount of investment, but other areas of focus include

advertising, gaming, and mobile payment services.

Advertising

As advertisers better appreciate the tremendous effect that the mobile web has on consumers, mobile advertising has become a fast growing sector. Mobile advertising is appealing because it can connect advertisers with millions of consumers in a non-intrusive manner. Advertising has become integrated into applications in a fashion that will not compromise the user experience and has become a new revenue model for application developers. Often times, developers allow consumers to use their

8 applications without charge; they then monetize the applications by selling advertising through the application. Companies are now able to send branded messaging to targeted demographics based on the type of content the user is consuming.

A study released by Petsky Prunier showed that in Q1 2010 the most active M&A subsegment in advertising was mobile advertising with 18 transactions for a total of $590 million. This represents 32% of interactive advertising deals and 37% of deal value in this segment. Two recent acquisitions reflect this growth: AdMob and Quattro Wireless, by Google and Apple, respectively.

AdMob, whose investors included Sequoia Capital, Accel and the DFJ Growth Fund, is one of the largest mobile advertising networks that offers solutions for discovery, branding and monetization of the mobile web. AdMob was one of the first companies to serve ads inside mobile applications across multiple platforms. In September 2009, AdMob received 2.6 billion ad requests from iPhone and iPod touch devices alone. In total, it received 10 billion requests that month. In November 2009, Google acquired AdMob for $750 million, but government regulators held up the purchase for review. In May 2010, the government finally approved the acquisition.

Quattro Wireless, a Globespan Capital Partners investment and a close competitor to AdMob, was acquired by Apple in January 2010 for $275 million. Apple made the strategic purchase as a way to further monetize its App platform. Apple is using the Quattro Wireless platform to launch iAd, a rich media ad platform that will allow users to interact with advertising without leaving the App. Apple sells and serves the ads, and developers receive 60% of the advertising revenue.

The acquisition of these two companies illustrates a very competitive advertising marketplace. Google has indicated that they expect to spend more money to acquire companies in the mobile advertising sector, and others will likely follow. As these companies become more acquisitive, exit opportunities will be created for venture-backed mobile advertising companies.

Gaming

Americans spend over $20 billion annually on the video game market, which has become increasingly mobile. In fact, 5% of gaming industry revenue now comes from mobile devices. Advances in smartphones with bigger screens, better graphics, and improved interfaces have created a new medium through which consumers can play games.

Apple has grown the mobile gaming marketplace with the App Store. Games make up 58% of Apps. While some of the games charge nominal fees to obtain the game, many games are offered for free. The “free” games are supported by advertising and in-game purchases, also known as virtual goods. Some free games also offer premium versions for a price, the so-called “freemium” model. Those who succeed in this space will be able to offer a low cost product to the consumer that can either be monetized through advertising support, in-game purchases, volume of downloads, or a combination thereof.

9 The large gaming companies currently do not have a strong presence in the mobile gaming sector, but opportunities abound for them to enter organically or by acquisition. Mobile game development is low cost, and the potential for high revenues and returns make this an interesting subsector of wireless for investment. While there have been exits in the mobile gaming space, there remain several opportunities for acquisition and consolidation. For example, Ngmoco, a mobile game developer and publisher, recently raised $25 million from IVP, Kleiner Perkins, Norwest and Maples to acquire Freeverse, the developer for several top games in the Apple App Store.

Mobile Payment Services

Since the second quarter of 2009, there has been a significant increase in mobile payment services investment. These payment services are transactions made on mobile devices that can include online banking, shopping, and other point-of-sale uses. In fact, mobile payments are progressing toward point-of-sale scenarios such as taxis and other forms of public transportation.

Recently, a mobile payment company, Square, has received attention from the press. Square, backed by Khosla Ventures, is bringing new meaning to the term point-of-sale. Square allows users to accept payments via an iPhone, iPad or Android device. The payments are made using a small device that attaches to the mobile device and is capable of processing credit card payments. Square’s goal is to enable people to accept payments immediately, everywhere.

Venture Activity

Many people tend to think of wireless as its own industry. However, wireless is really the convergence of a few industries: communications and equipment, internet software and services, and wireless telecommunications services. Wireless usage on mobile devices is becoming an extension of the internet and another platform by which consumers can access and consume data. As shown in Figure 5, the number of deals declined from 2008 to 2009, but has now stabilized and shown a slight upward trend recently, consistent with the broader venture capital market trends.

Figure 5 – Venture Backed Investments in Wireless Related Industries

Source: PricewaterhouseCoopers/National Venture Capital Association MoneyTree™ Report 0 50 100 150 200 250 300 350 0 200 400 600 800 1000 1200 1400 1600 1800 2000 Q1 08 Q2 08 Q3 08 Q4 08 Q1 09 Q2 09 Q3 09 Q4 09 Q1 10 N u m b er o f D ea ls Inv es te d C a pi ta l

Telecommunications Software Deals

10 Several venture investors have raised funds specifically to focus on investing in companies that develop Apps and the wireless ecosystem. In April 2008, Kleiner Perkins Caufield & Byers raised a $100 million fund called the iFund to invest in developers making applications and other software for the iPhone. In April 2010, the firm doubled the iFund to $200 million to invest in other mobile tools that can be used by Apple products including the iPod touch and the iPad, another Apple product that is a mix between a smartphone and a laptop. Similarly, JLA Ventures, the Royal Bank of Canada, and RIM gathered $150 million for the BlackBerry Partners fund to develop applications for Blackberry devices. Many of the funds that invest in applications are looking for companies whose plan is to sell direct to the consumer. Other investors have invested in Apps as part of their broader portfolio. Menlo and Morgenthaler invested in Siri, a personal assistant that aggregates search content. Zynga, a developer of online games for play on social networks, has several venture capital investors that include IVP, Foundry Group, and Kleiner Perkins Caufield & Byers.

At the end of the Q1 2010, the five largest technology companies (Apple, Google, Microsoft, IBM, and Cisco) had an average of $8 billion in cash on their balance sheets. If these companies begin to use more of their cash to make acquisitions that add significant value to their current portfolios and product offerings, the liquidity options for venture-capital backed companies will improve, which could spur increased investment in the wireless sector.

Notable Exits

There have been several notable exits from the Fairview portfolio in the wireless industry. These investments include:

• Asurion is a provider of insurance for mobile devices. Asurion, an investment by TA Associates, merged with DST lock/line in 2006, which has resulted in an 11.9x return.

• CCTV Wireless I, an investment by Highland Capital Partners, is the owner of a wireless spectrum. CCTV Wireless was acquired by TerreStar Corporation in 2008 for a 2.8x return. The acquisition allowed TerreStar to enhance its nationwide spectrum footprint.

• MetroPCS, provider of mobile phones and wireless service, was an investment by Accel, Battery Ventures, M/C Ventures, and TA Associates. The $1.2 billion IPO resulted in an aggregate distribution of 20.6x for the funds.

11

• MicroPower Electronics, an investment by Sierra Ventures, is the leading developer of custom portable power systems for use in mobile devices. The company was acquired by Weston Presidio in 2007 for a 7.3x return.

• Quattro Wireless, an investment by Globespan Capital Partners, combines its diverse global network of publishers with exclusive advertising inventory to form the mobile industry's premier advertising marketplace. Quattro Wireless was acquired by Apple in 2010, which resulted in a 4.8x return. The Quattro Wireless technology will be used by Apple as the basis for their iAd campaign, which will seamlessly embed advertising into Apps for a unique user experience.

• Siri, an investment by Menlo Ventures and Morgenthaler Ventures, was sold to Apple for $200 in April 2010. Siri provides voice recognition search and personal assistant capability on iPhones.

Summary

The desire to meet consumer demand, and ultimately increase profitability, is driving investment in the wireless industry, and the smartphone evolution will continue rapidly as users consume larger volumes of data over the mobile internet. Smartphones and other wireless connectivity devices are becoming all-in-one tools designed to meet the social and occupational needs of many. New and innovative technological advances continue to give users greater access to the things they enjoy, and have now grown dependent on. The delivery of content through mobile applications will continue to drive advertising spend. Additionally, the development of novel ways to deliver advertising to the consumer will continue to advance. This will fundamentally change the advertising landscape, shifting more of the dollars from television and print to mobile devices. Given the state of the current wireless industry and all of the technological advances in 4G, smartphone capabilities and availability of data, we believe several subsectors of wireless will experience significant changes over the next few years and create opportunities for investment. Potential areas of interest include infrastructure development, updates/launch of the 4G networks, improving overall power efficiency of the devices, converging messaging and social networking with location-based services, mobile enterprise, and SaaS solutions. We view these opportunities with eager anticipation for the innovation they will generate.