US stock market regimes and oil price shocks

Full text

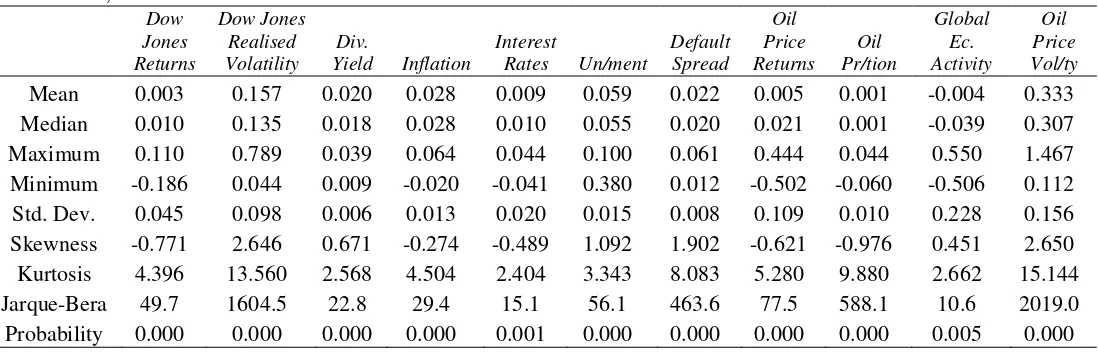

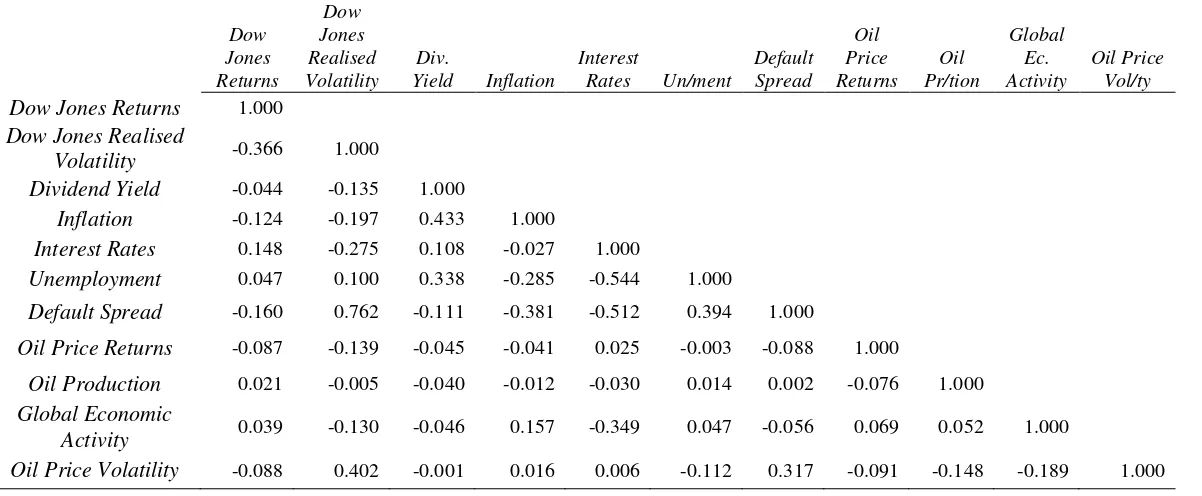

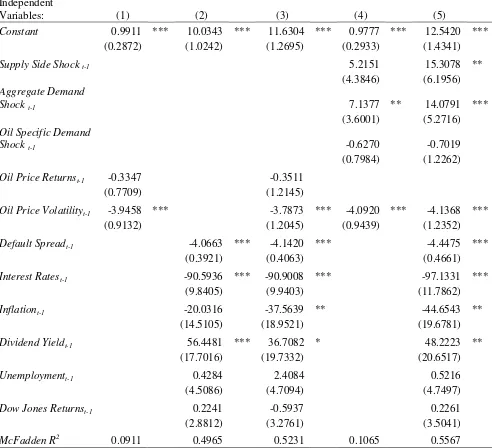

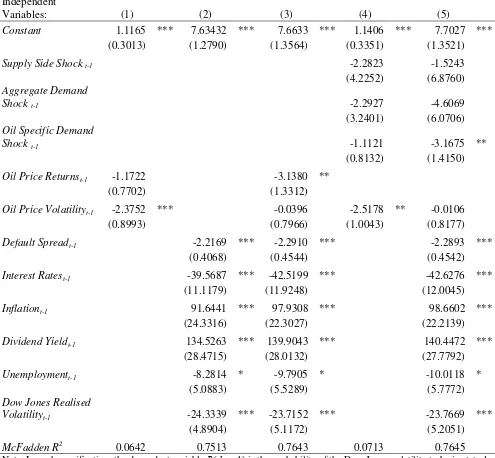

Figure

Related documents

The acronym names of the methods are as follows: QIM – Quadratic interpolation method (Shimko (1993)); HPM – Hermite polynomials method (Madan and Milne (1994)); JDM –

The research was based on 160 Latino immigrants and the researchers used a framework that took consideration of the roles of both one’s cultural and social circumstances to better

Abstract - This study investigated the trend of ground and surface water quality for drinking and irrigation purposes in Minna Metropolis.. Geologically, the

See how Head Start and Early Head Start programs look when staff, governing body, and Policy Council members have been brought on board and have embraced the use of data... 18

84 neostrata skin active matrix support reviews 85 neostrata bionic face..

The results of MMP-2 secretion assays also showed that increased CAS expression enhanced MMP-2 secretion, and reduced CAS expression decreased MMP-2 secretion of B16-F10 melanoma

- The Blue Book should be made available to the Penn Police or other emergency responders (Philadelphia Fire Department) to ensure that vital information about the building's

Pure Mathematics courses provide the insights and understanding required by those using mathematics, leading to mastery of the fundamental processes of mathematical science and