(Members of the NSE since 1954) 10th Floor, Pension Towers, Loita Street P.O. Box 45396-00100 Nairobi, Kenya Tel: +254-20-3240000 Fax: +254-20-218633 Website: www.dyerandblair.com

CEMENT INDUSTRY OVERVIEW

Kenya’s building and construction sector is amongst the most rapidly growing, experiencing an average growth rate of 14.2% for the period 2006 –

2011. Over the same period, Kenya’s economic growth, as measured by the real Gross Domestic Product rate (GDP) averaged only 4.3% declining to

4.38% in 2011 from 6.33% in 2006.

Difficult global macro conditions (effects of high oil prices and the August 2007 commencement of the financial crisis) and Kenya’s 2008 post election

violence in the midst of a high inflation environment (inflation averaged 9.0%) resulted in the country’s subdued economic performance during the

period.

Figure 1: Growth in Construction Output vs. GDP Growth, %

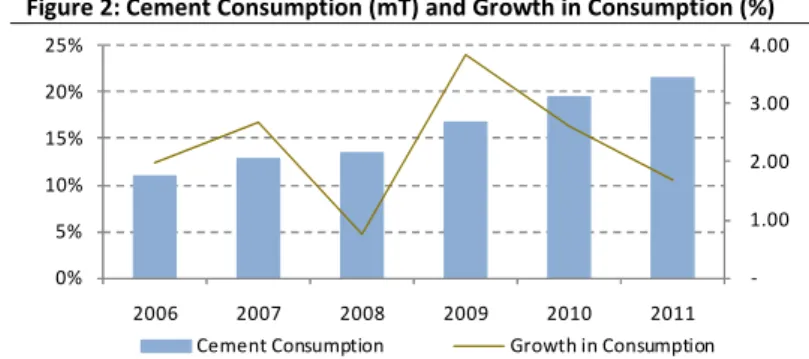

Figure 2: Cement Consumption (mT) and Growth in Consumption (%)

Source: World Economic Outlook (WEO) Database (October 2012), Kenya National Bureau of Statistics (KNBS) Economic Survey (2009 and 2012)

Source: KNBS Economic Survey (2009 and 2012)

Cement Demand

While the cement industry, cement consumption in particular is highly correlated to a country’s economic performance, cement consumption

experienced superior growth that was more than twice the rate of GDP growth during the period. Growing in tandem with the construction sector,

cement consumption increased at an average rate of 14.1% for the period 2006 – 2011, with consumption reaching 3.43 million tonnes (mT) in 2011,

up from 1.57mT in 2006.

The key drivers of this growth in consumption included rising demand for housing (which triggered an upsurge in private sector funded housing

developments), the commercial construction boom fuelled by increased foreign investment, and extensive government and donor-funded spending on

the country’s mega infrastructure projects. As a result, per capita consumption (PCC) of cement increased at an average rate of 10.7% for the period to

83.9 kilograms (Kg) in 2011 from 50.0Kg in 2006 despite relative stagnation in annual population growth.

Figure 3: Population Growth vs. Cement PCC Growth, %

Figure 4: Cement Consumption vs. Production, mT

Source: WEO Database (October 2012), KNBS Economic Survey (2009 and 2012) Source: KNBS Economic Survey (2009 and 2012)

0% 5% 10% 15% 20% 2006 2007 2008 2009 2010 2011

Real GDP growth Construction Output

-1.00 2.00 3.00 4.00 0% 5% 10% 15% 20% 25% 2006 2007 2008 2009 2010 2011

Cement Consumption Growth in Consumption

0% 5% 10% 15% 20% 2006 2007 2008 2009 2010 2011

Population Per capita Cement Consumption

1,000 1,500 2,000 2,500 3,000 3,500 4,000 4,500 2006 2007 2008 2009 2010 2011

Cement Consumption Cement Production

Kenya Cement industry

Brief Overview

21

St

December 2012

Research Department

Dealing Department

+254-20-3240130/128/166

+254-20-3240124/115

Dyer & Blair may do business with companies covered in its research reports. Although the views expressed in this document are solely those of the Research Department and are subject to change without notice, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

22

2

2

Cement Production and Supply

Cement production expanded at an average rate of 11.6% for the period 2006 – 2011 to 4.09mT in 2011 from 2.41mT in 2006. This rise in production

was driven by the entry of new cement producers and extensive capacity expansion by existing players in response to increasing competition.

This rise in production led to the consistent oversupply of cement during this period. Given an estimated industry capacity utilisation rate of about

72%

1, this glut supply could be much higher were installed capacity fully utilised.

As at end-2011, the local cement industry included six cement companies with mines concentrated in three sites across the country.

Cement Company Mines Cement Brand

Bamburi Cement Limited (BMBC) Mombasa Nguvu

Athi River Mining Limited (ARML) Athi River Rhino

East African Portland Cement Company Limited (EAPC) Athi River Blue Triangle

National Cement Company Limited (NCC) Lukenya Simba

Mombasa Cement Limited (MCL) Athi River Nyumba

Savannah Cement Company (SCC) Athi River Savannah

Figure 5: Cement Production (mT) and Growth in Production (%)

Figure 6: Cement Imports vs. Exports, mT

Source: KNBS Economic Survey (2009 and 2012) Source: KNBS Economic Survey (2009 and 2012)

Cement exports averaged 21.1% of total cement production over the period 2006 – 2011. Key export markets included Uganda, Tanzania, the

Democratic Republic of Congo (DRC) and other East and Central African countries.

Imported cement accounted for a marginal 2% of total cement consumed during the period indicating the country’s overall reliance on locally

produced cement. In 2011, cement import duty under the East African Community Common External Tariff was lowered by 10% to 25% despite stiff

opposition from industry players. Should the suspension of the 10% import duty remain, the quantum of cheap cement imports particularly from

low-cost producers such as Egypt, India, China and Pakistan could increase considerably, further widening the demand-supply mismatch.

COMPANY OVERVIEWS

Bamburi Cement Limited

BMBC was started in 1951 with its first plant located in Mombasa beginning production in 1954. BMBC, which was listed on the Nairobi Securities

Exchange (NSE) in September 1970, is the largest cement manufacturer in Kenya, enjoying local dominance both in terms of production and market

share.

Through Fincem Holding Limited and Kencem Holding Limited, Lafarge Group (the world largest cement manufacturer) owns 58.6% of BMBC with key

local institutions such as the National Social Security Fund (NSSF), Old Mutual Life Assurance Company and Kenya Reinsurance Corporation also holding

sizable shares in the company.

BMBC is also a producer of cement and related products including precast concrete paving blocks and ready-mix concrete through its subsidiary

Bamburi Special Products Limited. The company also has operations in Uganda through wholly-owned Hima Cement Limited, Uganda’s second largest

cement manufacturer.

1

According to the 2011 Annual Report for Bamburi Cement Limited, Kenya’s total installed cement capacity is estimated at 5.65mT which against a consumption level of 4.09mT implies industry capacity utilisation of 72.36%.

-1.00 2.00 3.00 4.00 5.00 0% 5% 10% 15% 20% 25% 2006 2007 2008 2009 2010 2011

Cement Production Growth in Production

0 200 400 600 800 2006 2007 2008 2009 2010 2011 Imports Exports

Athi River Mining Limited

ARML was established in 1974 and listed on the NSE in July 1997. ARML is currently the third leading cement manufacturer in Kenya (in terms of

market share) and has subsidiaries in Kenya, Tanzania, South Africa and Rwanda.

The company is 46% held by the family of the late founder, H. J. Paunrana. Amanat Investments Limited, the family’s investments’ holding company,

owns 28% while Pradeep H. Paunrana, the Managing Director owns 18%. ARML’s top ten shareholders largely comprise institutions which have a

combined shareholding of 64%.

ARML also manufactures sodium silicate, lime, industrial minerals, fertilizer and special building products. In 2011, these non-cement products

accounted for 32.4% of the company’s total income.

East Africa Portland Cement Company Limited

EAPC is the oldest cement manufacturer in Kenya having been incorporated in 1933. EAPC started as a trading company, importing cement for early

construction work in East Africa and in 1956 constructed its first factory in Athi River.

EAPC’s shareholding structure is largely institutionally, with the company’s top ten shareholders owning a combined 96.1% stake in the company. NSSF

and the Treasury are the company’s top shareholders holding 27.0% and 25.3% respectively.

EAPC also produces custom-made cement products for the construction industry. The company does not have subsidiaries.

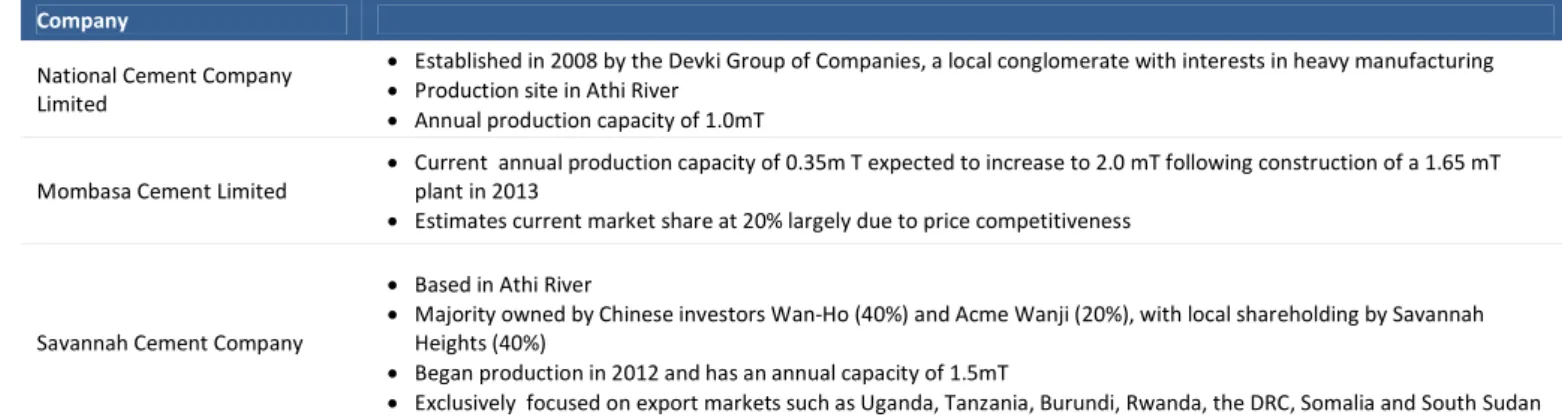

Other Companies

2Company

National Cement Company Limited

• Established in 2008 by the Devki Group of Companies, a local conglomerate with interests in heavy manufacturing

• Production site in Athi River

• Annual production capacity of 1.0mT

Mombasa Cement Limited

• Current annual production capacity of 0.35m T expected to increase to 2.0 mT following construction of a 1.65 mT plant in 2013

• Estimates current market share at 20% largely due to price competitiveness

Savannah Cement Company

• Based in Athi River

• Majority owned by Chinese investors Wan-Ho (40%) and Acme Wanji (20%), with local shareholding by Savannah Heights (40%)

• Began production in 2012 and has an annual capacity of 1.5mT

• Exclusively focused on export markets such as Uganda, Tanzania, Burundi, Rwanda, the DRC, Somalia and South Sudan

Source: Company websites, Press filings and Dyer and Blair websites

COMPETITIVE POSITIONING

Figure 7: Estimated 2011 Production Capacity (%)

Figure 8: Estimated Market Share (%)

Source: Company filings, Press reports and Dyer and Blair estimates Source: EAPC Annual Report 2012 and Dyer and Blair estimates

2

Information regarding the smaller cement companies was not widely available in the public domain.

BMBC 33% EAPC 20% ARML 15% NCC 5% MCL 5% SCC 22% BMBC 40% EAPC 24% ARML 16% NCC 7% MCL 13%

Dyer & Blair may do business with companies covered in its research reports. Although the views expressed in this document are solely those of the Research Department and are subject to change without notice, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

44

4

4

COMPARATIVE ANALYSIS OF LISTED CEMENT COMPANIES

Using the audited annual reports for ARML, BMBC and EAPC, we compare their financial performances for the period 2007 – 2011, with the aim of

understanding their competitiveness and relative comparability.

Figure 9: Net Revenue Growth (%)

Figure 10: Net Income Growth (%)

Source: ARML, BMBC & EAPC Annual Reports and Dyer & Blair estimates Source: ARML, BMBC & EAPC Annual Reports and Dyer & Blair estimates

Additional cement capacity arising from new entrants and capacity increments by existing players resulted in excessive supply, eroding the gains in

cement consumption growth by pushing down prices considerably. The 14.3% drop in the price of a 50Kg cement bag to KES 660 in June 2011 from KES

770 in December 2010 is an indication of these competitive pricing dynamics that resulted in the three companies experiencing erratic revenue growth.

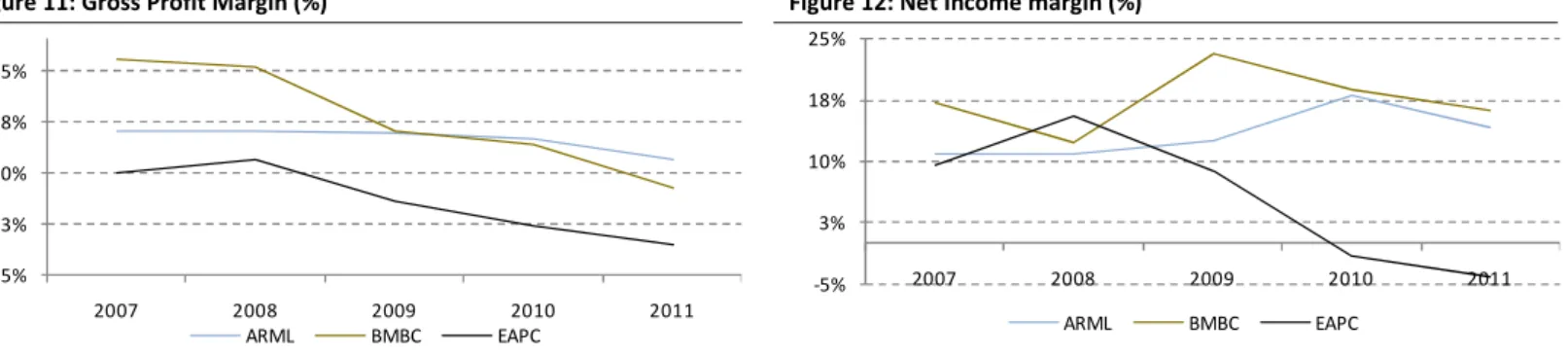

Figure 11: Gross Profit Margin (%)

Figure 12: Net Income margin (%)

Source: ARML, BMBC & EAPC Annual Reports and Dyer & Blair estimates Source: ARML, BMBC & EAPC Annual Reports and Dyer & Blair estimates

The effects of rising competition and high production costs (electricity and fuel) were compounded by a difficult macroeconomic environment, pushing

up cost-to-income ratios significantly and dampening net income growth and the profitability margins. ARML and EAPC had considerable debt on their

balance sheets although ARML’s higher leverage could constrain future debt carry capacity.

Figure 13: Cost to Income Ratio (%)

Figure 14: Debt / Equity Ratio (x)

Source: ARML, BMBC & EAPC Annual Reports and Dyer & Blair estimates Source: ARML, BMBC & EAPC Annual Reports and Dyer & Blair estimates

-10% 0% 10% 20% 30% 40% 50% 2007 2008 2009 2010 2011 ARML BMBC EAPC -150% -75% 0% 75% 150% 225% 2007 2008 2009 2010 2011 ARML BMBC EAPC 15% 23% 30% 38% 45% 2007 2008 2009 2010 2011 ARML BMBC EAPC -5% 3% 10% 18% 25% 2007 2008 2009 2010 2011 ARML BMBC EAPC 50% 58% 65% 73% 80% 2007 2008 2009 2010 2011 ARML BMBC EAPC 0.00x 0.45x 0.90x 1.35x 1.80x 2007 2008 2009 2010 2011 ARML BMBC EAPC

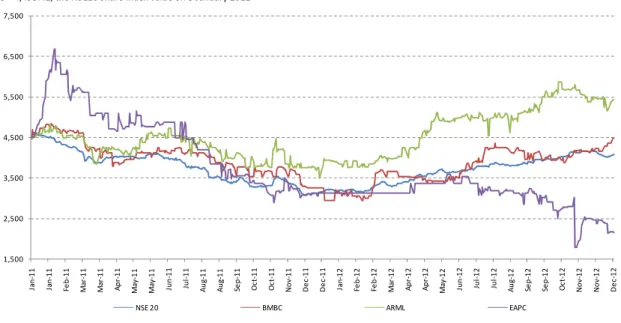

SHARE PRICE PERFORMANCE

BMBC and ARML displayed relatively good performance from January 2011 to-date. While BMBC largely tracked the NSE20 Share index (NSE20), ARML,

which is currently undertaking a five-for-one share split

3consistently, outperformed the general market’s performance since March 2011.

EAPC’s price movement has been relatively volatile, significantly exceeding market performance between January and October 2011 then dipping

considerably thereafter. The announcement of a KES 821.5m loss in October last year pushed down EAPC’s price with the onset of corporate

governance battles and the ensuing litigation further accelerating the price decline between mid-2012 and today.

Figure 15: Share Price Performance of Listed Kenyan Cement Companies

Base = 4,495.41, the NSE20 share index value on 3 January 2011

Source: Bloomberg and NSE, Dyer & Blair estimates

SUMMARY VALUATION

We relied on the trading multiples approach to compare the relative values of the three companies i.e. Price to Equity (P/E), Price to Book (P/B) and

Enterprise Value to EBITDA

4(EV/EBITDA) valuation techniques. This methodology provides a reasonable indication of the value that investors would

place on a company, based on values of comparable peer companies.

Our high level analysis indicates that relative to the average cement company multiples:

•

ARML is overvalued on all three multiples

•

BMBC is undervalued on a P/E and EV/EBITDA basis

Table 1: Market Capitalisation & Trading Multiples of Cement Companies

5Source: NSE (share prices as at 19 December 2012), Company filings and Dyer & Blair estimates

3

Today (21st December) is the last day of ARML’s pre-split trading. 4 Earnings before interest, tax, depreciation and amortisation.

5EAPC’s made a loss in 2011 rendering the P/E valuation not meaningful (n.m.)

1,500 2,500 3,500 4,500 5,500 6,500 7,500 Ja n -1 1 Ja n -1 1 Fe b -1 1 M a r-1 1 M a r-1 1 A p r-1 1 M a y-1 1 M a y-1 1 Ju n -1 1 Ju l-1 1 A u g -1 1 A u g -1 1 Se p -1 1 O c t-1 1 O c t-1 1 N o v -1 1 D e c -1 1 D e c -1 1 Ja n -1 2 Fe b -1 2 Fe b -1 2 M a r-1 2 A p r-1 2 A p r-1 2 M a y-1 2 Ju n -1 2 Ju l-1 2 Ju l-1 2 A u g -1 2 Se p -1 2 Se p -1 2 O c t-1 2 N o v -1 2 N o v -1 2 D e c -1 2

NSE 20 BMBC ARML EAPC

Bloomberg Ticker Share price (KES)

Market Cap

(KES m) P/E:2011C P/B:2011C EV/EBITDA:2011C ARML 222.00 21,990 19.11x 3.60x 15.93x BMBC 189.00 68,599 11.71x 2.84x 7.85x EAPC 39.00 3,510 n.m. 0.62x 12.73x

Dyer & Blair may do business with companies covered in its research reports. Although the views expressed in this document are solely those of the Research Department and are subject to change without notice, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

66

6

6

APPENDIX

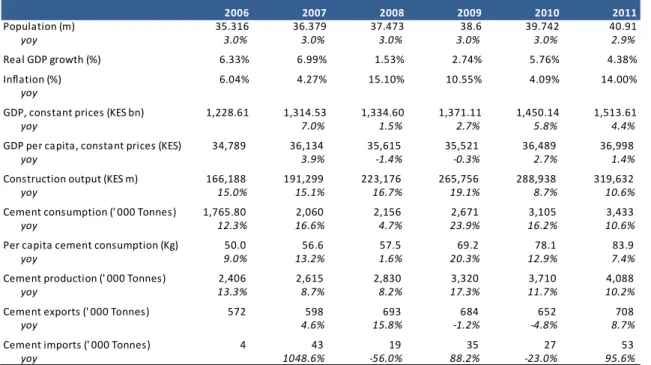

Table 2: Cement Statistics and Macroeconomic Indicators

Source: WEO Database (October 2012), KNBS Economic Survey (2009 and 2012)

2006 2007 2008 2009 2010 2011 Population (m) 35.316 36.379 37.473 38.6 39.742 40.91 yoy 3.0% 3.0% 3.0% 3.0% 3.0% 2.9% Real GDP growth (%) 6.33% 6.99% 1.53% 2.74% 5.76% 4.38% Inflation (%) 6.04% 4.27% 15.10% 10.55% 4.09% 14.00% yoy

GDP, constant prices (KES bn) 1,228.61 1,314.53 1,334.60 1,371.11 1,450.14 1,513.61

yoy 7.0% 1.5% 2.7% 5.8% 4.4%

GDP per capita, constant prices (KES) 34,789 36,134 35,615 35,521 36,489 36,998

yoy 3.9% -1.4% -0.3% 2.7% 1.4%

Construction output (KES m) 166,188 191,299 223,176 265,756 288,938 319,632

yoy 15.0% 15.1% 16.7% 19.1% 8.7% 10.6%

Cement consumption (' 000 Tonnes) 1,765.80 2,060 2,156 2,671 3,105 3,433

yoy 12.3% 16.6% 4.7% 23.9% 16.2% 10.6%

Per capita cement consumption (Kg) 50.0 56.6 57.5 69.2 78.1 83.9

yoy 9.0% 13.2% 1.6% 20.3% 12.9% 7.4%

Cement production (' 000 Tonnes) 2,406 2,615 2,830 3,320 3,710 4,088

yoy 13.3% 8.7% 8.2% 17.3% 11.7% 10.2%

Cement exports (' 000 Tonnes) 572 598 693 684 652 708

yoy 4.6% 15.8% -1.2% -4.8% 8.7%

Cement imports (' 000 Tonnes) 4 43 19 35 27 53

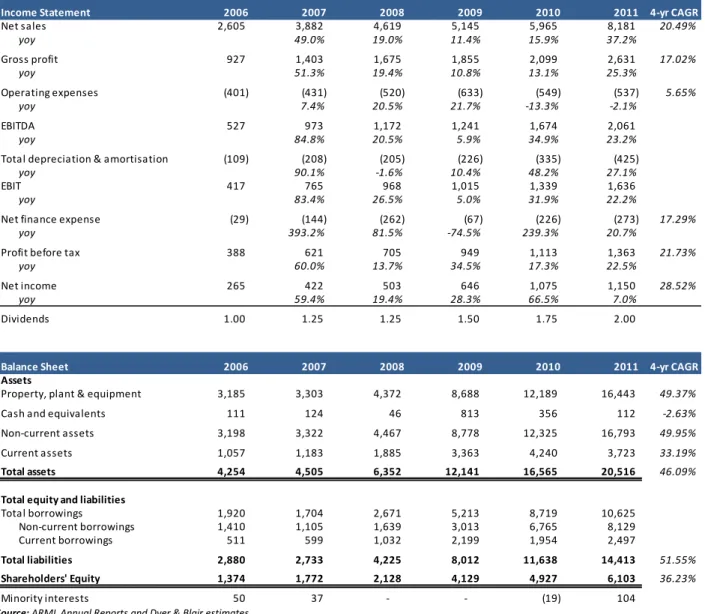

Table 3: ARML’s Summarised Financials in KESm (Year ended 31 December)

Source: ARML Annual Reports and Dyer & Blair estimates

Income Statement 2006 2007 2008 2009 2010 2011 4-yr CAGR

Net sales 2,605 3,882 4,619 5,145 5,965 8,181 20.49% yoy 49.0% 19.0% 11.4% 15.9% 37.2% Gross profit 927 1,403 1,675 1,855 2,099 2,631 17.02% yoy 51.3% 19.4% 10.8% 13.1% 25.3% Operating expenses (401) (431) (520) (633) (549) (537) 5.65% yoy 7.4% 20.5% 21.7% -13.3% -2.1% EBITDA 527 973 1,172 1,241 1,674 2,061 yoy 84.8% 20.5% 5.9% 34.9% 23.2%

Total depreciation & amortisation (109) (208) (205) (226) (335) (425)

yoy 90.1% -1.6% 10.4% 48.2% 27.1%

EBIT 417 765 968 1,015 1,339 1,636

yoy 83.4% 26.5% 5.0% 31.9% 22.2%

Net finance expense (29) (144) (262) (67) (226) (273) 17.29%

yoy 393.2% 81.5% -74.5% 239.3% 20.7%

Profit before tax 388 621 705 949 1,113 1,363 21.73%

yoy 60.0% 13.7% 34.5% 17.3% 22.5%

Net income 265 422 503 646 1,075 1,150 28.52%

yoy 59.4% 19.4% 28.3% 66.5% 7.0%

Dividends 1.00 1.25 1.25 1.50 1.75 2.00

Balance Sheet 2006 2007 2008 2009 2010 2011 4-yr CAGR

Assets

Property, plant & equipment 3,185 3,303 4,372 8,688 12,189 16,443 49.37%

Cash and equivalents 111 124 46 813 356 112 -2.63%

Non-current assets 3,198 3,322 4,467 8,778 12,325 16,793 49.95%

Current assets 1,057 1,183 1,885 3,363 4,240 3,723 33.19% Total assets 4,254 4,505 6,352 12,141 16,565 20,516 46.09%

Total equity and liabilities

Total borrowings 1,920 1,704 2,671 5,213 8,719 10,625 Non-current borrowings 1,410 1,105 1,639 3,013 6,765 8,129 Current borrowings 511 599 1,032 2,199 1,954 2,497 Total liabilities 2,880 2,733 4,225 8,012 11,638 14,413 51.55% Shareholders' Equity 1,374 1,772 2,128 4,129 4,927 6,103 36.23% Minority interests 50 37 - - (19) 104

Dyer & Blair may do business with companies covered in its research reports. Although the views expressed in this document are solely those of the Research Department and are subject to change without notice, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

88

8

8

Table 4: BMBC’s Summarised Financials in KESm (Year ended 31 December)

Source: BMBC Annual Reports and Dyer & Blair estimates

Income Statement 2006 2007 2008 2009 2010 2011 4-yr CAGR

Net sales 16,488 22,111 27,467 29,994 28,075 35,884 12.87% yoy 34.1% 24.2% 9.2% -6.4% 27.8% Gross profit 8,059 10,343 12,552 10,815 9,618 9,964 -0.93% yoy 28.3% 21.4% -13.8% -11.1% 3.6% Operating expenses (3,634) (4,714) (6,907) (2,247) (1,321) (749) -36.86% yoy 29.7% 46.5% -67.5% -41.2% -43.3% EBITDA 4,660 6,168 5,648 10,446 8,670 10,101 yoy 32.4% -8.4% 85.0% -17.0% 16.5%

Total depreciation & amortisation (673) (655) (685) (836) (1,015) (1,261)

yoy -2.7% 4.6% 22.0% 21.4% 24.2%

EBIT 3,987 5,513 4,963 9,610 7,655 8,840

yoy 38.3% -10.0% 93.6% -20.3% 15.5%

Net finance expense (149) (70) (74) (14) (91) (374) 52.03%

yoy -53.0% 5.7% -81.1% 550.0% 311.0%

Profit before tax 3,838 5,443 4,889 9,596 7,564 8,466 11.68%

yoy 41.8% -10.2% 96.3% -21.2% 11.9%

Net income 2,799 3,810 3,412 6,970 5,299 5,859 11.36%

yoy 36.1% -10.4% 104.3% -24.0% 10.6%

Dividends 5.50 6.00 6.00 11.00 8.50 10.00

Balance Sheet 2006 2007 2008 2009 2010 2011 4-yr CAGR

Assets

Property, plant & equipment 9,395 9,030 10,267 11,847 17,833 16,939 17.03%

Cash and equivalents 2,057 371 1,818 6,427 7,616 7,136 109.42%

Non-current assets 12,931 13,631 18,179 19,339 20,443 20,146 10.26%

Current assets 5,582 7,089 10,036 12,773 12,863 13,356 17.16% Total assets 18,513 20,720 28,215 32,112 33,306 33,502 12.76%

Total equity and liabilities

Total borrowings - 112 4,572 3,571 2,953 1,391 Non-current borrowings - - 3,408 3,201 1,067 619 Current borrowings - 112 1,164 370 1,886 772 Total liabilities 4,777 5,645 11,613 11,171 11,680 9,328 13.38% Shareholders' Equity 13,736 15,075 16,602 20,941 21,626 24,174 12.53% Minority interests 719 846 1,106 1,444 1,461 2,146

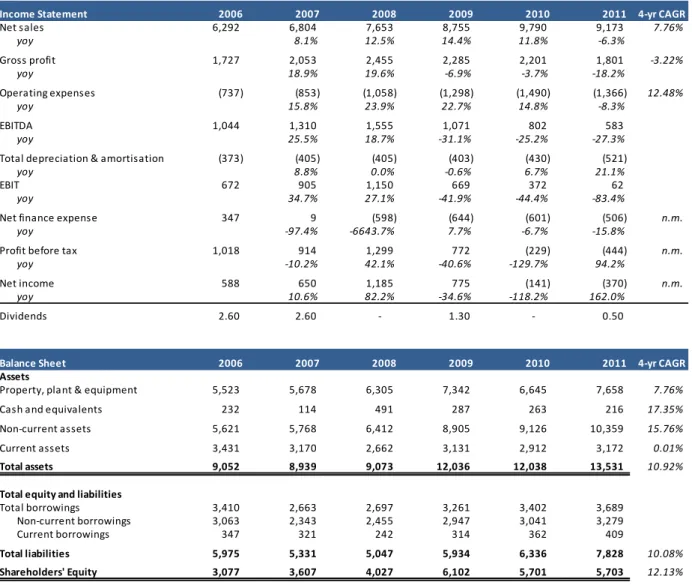

Table 5: EAPC’s Summarised Financials in KESm (Year ended 31 December)

Source: EAPC Annual Reports and Dyer & Blair estimates

Income Statement 2006 2007 2008 2009 2010 2011 4-yr CAGR

Net sales 6,292 6,804 7,653 8,755 9,790 9,173 7.76% yoy 8.1% 12.5% 14.4% 11.8% -6.3% Gross profit 1,727 2,053 2,455 2,285 2,201 1,801 -3.22% yoy 18.9% 19.6% -6.9% -3.7% -18.2% Operating expenses (737) (853) (1,058) (1,298) (1,490) (1,366) 12.48% yoy 15.8% 23.9% 22.7% 14.8% -8.3% EBITDA 1,044 1,310 1,555 1,071 802 583 yoy 25.5% 18.7% -31.1% -25.2% -27.3%

Total depreciation & amortisation (373) (405) (405) (403) (430) (521)

yoy 8.8% 0.0% -0.6% 6.7% 21.1%

EBIT 672 905 1,150 669 372 62

yoy 34.7% 27.1% -41.9% -44.4% -83.4%

Net finance expense 347 9 (598) (644) (601) (506) n.m.

yoy -97.4% -6643.7% 7.7% -6.7% -15.8%

Profit before tax 1,018 914 1,299 772 (229) (444) n.m.

yoy -10.2% 42.1% -40.6% -129.7% 94.2%

Net income 588 650 1,185 775 (141) (370) n.m.

yoy 10.6% 82.2% -34.6% -118.2% 162.0%

Dividends 2.60 2.60 - 1.30 - 0.50

Balance Sheet 2006 2007 2008 2009 2010 2011 4-yr CAGR

Assets

Property, plant & equipment 5,523 5,678 6,305 7,342 6,645 7,658 7.76%

Cash and equivalents 232 114 491 287 263 216 17.35%

Non-current assets 5,621 5,768 6,412 8,905 9,126 10,359 15.76%

Current assets 3,431 3,170 2,662 3,131 2,912 3,172 0.01% Total assets 9,052 8,939 9,073 12,036 12,038 13,531 10.92%

Total equity and liabilities

Total borrowings 3,410 2,663 2,697 3,261 3,402 3,689 Non-current borrowings 3,063 2,343 2,455 2,947 3,041 3,279 Current borrowings 347 321 242 314 362 409 Total liabilities 5,975 5,331 5,047 5,934 6,336 7,828 10.08% Shareholders' Equity 3,077 3,607 4,027 6,102 5,701 5,703 12.13% Minority interests