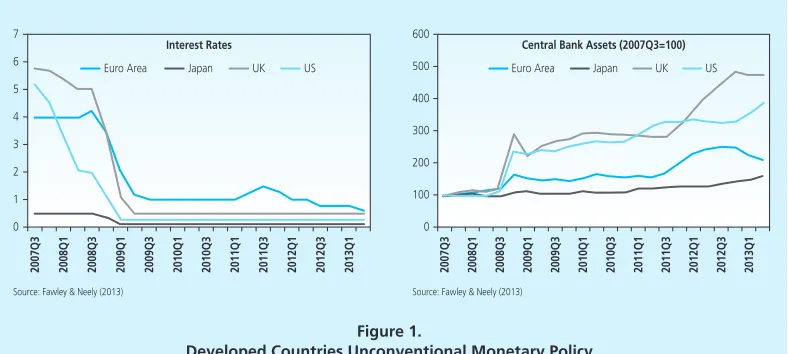

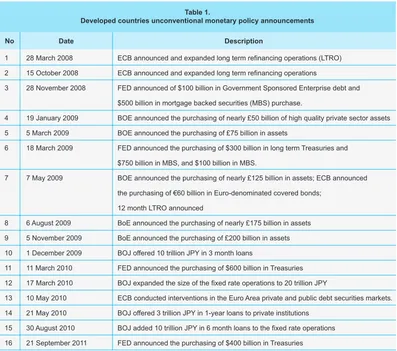

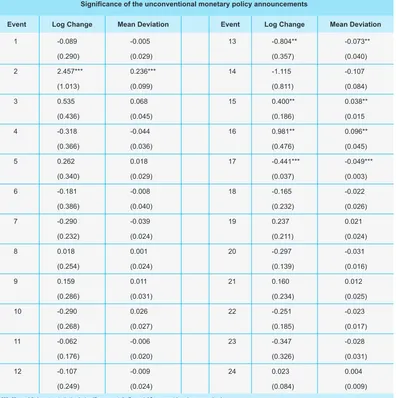

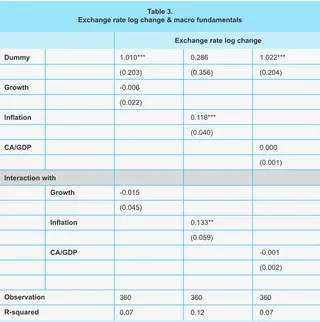

WHAT PROTECT EMERGING MARKETS FROM DEVELOPED COUNTRIES UNCONVENTIONAL MONETARY POLICY SPILLOVER?

Full text

Figure

Related documents

The purpose of this study is to determine the benefit of enzalutamide versus placebo as assessed by overall survival and pro- gression-free survival in patients with

While large-scale land acquisitions do not always result in local communities losing their land or having their livelihoods subverted, many recent acquisitions have, in fact,

Further to these Resolutions, at the Information Session of the seventh meeting of the Ad Hoc Advisory Committee on the Funding Strategy of the Treaty (the Committee, or ACFS), a

To develop the completed research methodology, process of data collecting, method of data analysis, writing draft of the dissertation and be able to present the

D.Ed 2007/ may No No No No NO No No No B Ped 2017 Physical education Anatomy School managem No NO No No No DEd and BSC No No No No No NO No No No Hindi. language 2011 Regular NA

Another term which holds negative connotations in popular discourse is ‘stalking’. Young people demonstrated that this concept took on new meaning for them in the context of

Section 6.10 contains details about the semismooth Newton (SSN) method and the primal dual active set method, respectively, which are applied to discretized problems with

Nesse sentido, sabendo que os custos de transporte representam mais da metade dos custos logísticos de uma organização, esse trabalho tem o objetivo de propor uma