Before a Board of Inquiry

Ruakura Development Plan Change

IN THE MATTER of the Resource Management Act 1991

AND

IN THE MATTER of a Board of Inquiry appointed under section 149J of the Resource Management Act 1991 to consider a Plan Change requested by Tainui Group Holdings Limited and Chedworth Properties Limited

Statement of Evidence in Chief of Philip James

McDermott on behalf of Tainui Group Holdings Ltd and

Chedworth Properties Ltd

24

thFEBRUARY 2014

Summary

1. The Proposed Hamilton City District Plan (PDP) provides for Neighbourhood Centres in the Knowledge Zone and the Medium Density Residential Zone in the Ruakura Structure Plan. My review of local demand (Technical Document, Retail Review Report, Request for a Ruakura Private Plan Change) presented the results of an analysis of likely demand for retail and related services and an assessment of contingencies that might influence the outcome. It indicated a retail land requirement of around 3.8 ha and floorspace demand of between 15,900sqm GFA and 22,700sqm GFA, the lower figure dependent on achieving relatively high sales per square metre across the board.

2. Contributing in large part to this demand will be the activities required to service a large commuter population (employees) as well as residential demand. A commercial centre in Ruakura will also attract business related professional and support services that I have not quantified.

3. I conclude that the provisions in the Ruakura Development Plan Change Request (the “Plan Change”) for a 15,000sqm Suburban Centre in the Knowledge Area and 3,500sqm Integrated Retail Centre in the Medium Density Residential Area are consistent with the likely scale of demand, if a little conservative.

4. I also consider issues raised by submissions to the Board of Inquiry.

5. I also conclude:

Demand: The provisions for a Suburban Centre in the Knowledge Area and an Integrated retail Centre in the Medium Density Residential Area are related to incremental demand associated with the growth of activity at Ruakura, which includes plans for 1,800 households, capacity for around 9,150 employees on-site, and a range of businesses and other organisations in logistics, innovation and technology, and associated service industries. The centre does not depend on attracting custom from other centres in the vicinity.

A Suburban Main Street Centre: Neighbourhood Centres are generally established in existing Residential areas with little capacity to expand, which is not the case with the Ruakura Main Street. Providing for park and ride facilities as required by the Structure Plan is inconsistent with a Neighbourhood Centre under the PDP where parking is treated as non-complying. In addition, a transport hub will add to the need for convenience retailing.

A new centre incorporating park and ride and transit facilities at Ruakura provides an opportunity to redress a demonstrable lack of supermarket capacity in southeast Hamilton where it is currently deficient.

Planning Provisions: Objecting to the use of the Operative District Plan Suburban Centre provisions ignores the range of activities required to service businesses and employees and the greater flexibility they provide for a centre subject to diverse and often unpredictable demands.

Threat to other centres: The difference in floorspace provided for in the Plan Change and the Proposed District Plan (PDP) is 2,500sqm for the Integrated Retail Centre and 10,000sqm for the Main Street Centre. This increment represents just 2.4% of Hamilton City’s current retail floorspace according to Quotable Value NZ figures and is less than the average annual gain between 2000 and 2012 (13,000sqm). I conclude that this increment is insignificant relative to current and future retail developments.

Threat to the CBD: The risk posed to the Central City is considered minimal on several grounds. First, a 10,000sqm difference between provision for a Neighbourhood Centre under the PDP and a Suburban Centre under the Plan Change is around 5.3% of retail floorspace in the CBD, a relatively small portion so that the effect (if any) of allowing the increment will be minor.

Second, the nature of retail activities likely to be provided at the Suburban Centre differ from those associated with the CBD.

Much of the focus of the Suburban Centre proposed for Ruakura will be to provide for the retail and service requirements of local employees and businesses

Third, no evidence is provided in support of the inference that the performance of the CBD is determined by the performance of Suburban Centres and that no evidence to this effect has been provided in the PDP process.

Fourth, an assessment of indicators of economic activity in the central city points to a CBD undergoing substantial structural change and changes in the way it is used, but that is not necessarily in decline. Following under-investment between 2000 and 2010, the redevelopment of Centre Place as a large integrated mall and recent new office development indicate a resurgence which may bring about changes in the nature of retailing and the distribution of activity within the CBD (form) and between the CBD and the rest of the city (function) and changes in how it is used by the wider population (amenity).

However, the scale and diversity of activity in the City Centre and its regional role compared with the scale, focus and likely function of the proposed Ruakura Main Street centre mean that the latter will not pose a threat to the former, particularly as Ruakura Main Street functions will reflect its location, first, in an industrial environment and, second, in a suburban locality.

6. In conclusion, a Suburban Centre in the Knowledge Area provides for the scale of retailing and related services and the flexibility required to support the development of the Ruakura Structure Plan Area. By contributing to the development of Ruakura as a whole, the Main Street Centre will make a positive contribution to the Hamilton economy as whole. As an important part of the commercial infrastructure of Ruakura, and hence Hamilton, the centre will indirectly support the CBD as it benefits from the income flowing from Ruakura, some of which will be reflected in intermediate and final demand expenditure in the City Centre.

Introduction

7. My name is Philip James McDermott. I am a consultant in development planning. I am a member of the New Zealand Planning Institute and a Fellow of the Chartered Institute of Logistics and Transport. I have a Masters Degree in Geography from the University of Auckland and a PhD from the University of Cambridge.

8. I established consultants McDermott Associates Ltd in 1977 (later McDermott Miller Group and McDermott Fairgray Group) and market research business Forsyte Research in 1986. In 1994 I took up a five year contract as Professor and Head of the Department of Resource and Environmental Planning at Massey University. In 1999 I became General Manager and Senior Consultant at the Centre for Asia Pacific Aviation in Sydney.

9. Since returning to New Zealand in 2004 I have practiced as an independent consultant. I attach a list of project experience relevant to this statement of evidence.

Background

10. In February 2013 I was retained by Tainui Group Holdings Ltd (TGH) to review the provisions for retailing and commercial centres within the Proposed Hamilton City District Plan (PDP and the underlying research and planning documents. These included Future Proof and its source documents dealing with retailing and commercial land use, the Proposed Regional Policy Statement and the Proposed District Plan and associated documents, including section 32 analyses.

11. I also analysed the development of retailing in Hamilton since 2000 in terms of employment structure, building consents, land and capital values, expenditure, and distribution relative to population and employment. I analysed the drivers of change in retailing and considered evidence from elsewhere with respect to retail trends, prospects, and planning in urban areas.

12. On the basis of my findings I agreed in March 2013 to support the TGH submissions on the PDP and, I submitted a final report in June 2013 (Retail Planning and Development in Hamilton: a Review).

13. My subsequent report into the need for retail capacity in Ruakura was submitted by letter to Mr Philip Stickney, Associate Director of Planning at Boffa Miskell, dated 14 June 2013 (Ruakura Retail Centres) and together with my review of Hamilton retailing comprises the Technical Document, Retail Review Report in the Request for a Ruakura Private Plan Change (the Plan Change).

Code of Conduct

14. I confirm that I have read the Code of Conduct for Expert Witnesses as contained in the Environment Court Practice Note 2011. I agree to comply with this Code of Conduct. In particular, unless I state otherwise, this evidence is within my sphere of expertise and I have not omitted to consider material facts known to me that might alter or detract from the opinions I express.

Scope of Evidence

15. The PDP provides for two Neighbourhood Centres in the Ruakura Area. In this statement I address the provision in the Plan Change for the one in the Knowledge Area to be zoned a Suburban Centre (“Ruakura Main Street”) as defined by Schedule 25H, of the Plan Change and the appropriate size of both this centre and the Integrated Retail Centre provided for in the Medium Density Residential Area in the Plan Change. I also consider the submissions made in response to the Plan Change.

16. In particular, I offer evidence in support of the Plan Change Section 25H7.1(d):

“the Knowledge Area also needs to provide supporting retail and commercial activities which act as the focal point and increase the attractiveness for innovation and research activities to establish here. The area is centred on a “Main Street” precinct with a large public Plaza. This area makes provision for a passenger transport hub to provide connectivity to the Central City”

17. This statement commences with an outline of the relationship between the Plan Change and the provisions anticipated for retailing in the Ruakura Structure Plan in the Proposed District Plan. Having identified the issues I then review my June 2013 Ruakura Retail Centres report in which I outlined the appropriate scale and scope of the two centres proposed for Ruakura when the area is fully developed.

18. Next I outline the issues raised by submissions to this Board of Inquiry relative to the centres proposed in in the Plan Change. I consequently address these issues in turn, dealing first with the likely magnitude and nature of retail demand in the Ruakura Structure Plan Area to be met at the centres provided for in the Plan Change. I then consider the appropriateness of a Suburban Centre under the provisions of the Operative District Plan rather than a Neighbourhood Centre under the PDP. I next assess the significance of the retail capacity provided for in the Plan Change relative to retailing in Hamilton City generally, before assessing in more detail the possible impact on the central city. Finally, I consider provisions for an Integrated Retail Centre and service station in the Medium Density Residential Area held by Chedworth Properties Ltd (CPL).

Methodology and Limitations

19. No single source provides a definitive view of the state of or outlook for retailing in Hamilton generally or in Ruakura in particular. I have therefore analysed various data sources on likely future demand for, and the effect of, retailing and related land uses in Ruakura.

20. As well as the planning source documents identified in paragraph 10, above, I have drawn on:

(a) Annual employment data from the Statistics New Zealand (SNZ) Business Directory and compiled using the Table Builder facilities on the SNZ website;

(b) Detailed building permit data sourced from SNZ;

(d) Quotable Value New Zealand property valuation data sourced from Property IQ;

(e) CBD pedestrian counts published by the Waikato Branch of the Property Institute;

(f) Academic or professional papers dealing with retailing and centres development;

(g) Information on zoned areas sourced from the Hamilton City Council and compiled by Boffa Miskell; and

(h) The evidence of other experts as acknowledged in the text.

Relationship with the Plan Change

21. A Suburban Centre Zone of up to 4ha is proposed within the Knowledge Area (Plan Change 25H.7.3.2, 25H.12.3(a)). This is to include a building footprint of 15,000sqm and provision for a park and ride facility. An additional 0.576ha is provided for a Neighbourhood Centre (with a GFA of 3,500sqm) in the Medium Density Residential area. This gives a total land area of around 4.6ha committed to commercial centres, including parking and public transport facilities. This compares with 9.5ha provided for the Rototuna growth cell in the PDP, 7.1ha for Rotokauri and, in due course, 3.2ha for Peacocke.

22. The PDP proposes a Neighbourhood Centre only for the Knowledge Zone (PDP 8.1.e, p.8-1). The differences between Neighbourhood and Suburban Centres in the PDP are reflected in differences between Business Zones 5 and 7. The PDP objective for Suburban Centres is:

6.22 A distribution of suburban centres that provide goods, services and employment at a scale appropriate to suburban catchments, while not undermining the primacy, vitality or viability of the Central City.

23. The objective for Neighbourhood Centres is:

6.2.3 A distribution of locally-based centres that provide services and community facilities capable of meeting the day-to-day needs of their immediate neighbourhoods.

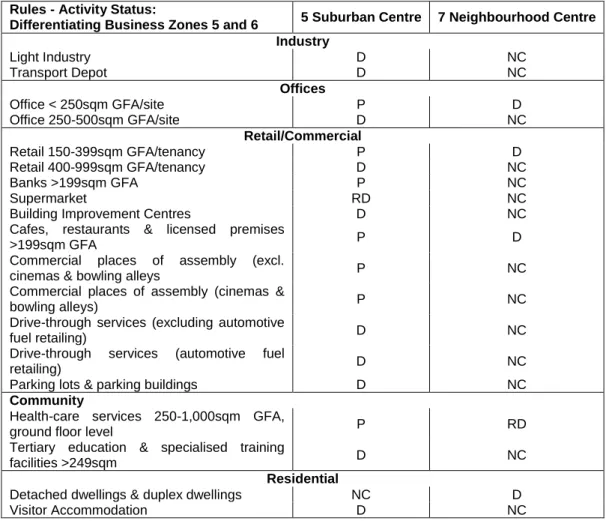

24. Table 1, below, lists those rules (and only those rules) in the PDP that distinguish between the two zones. Through them strict limits are placed on office and light industry in neighbourhood zones. Supermarkets, larger shops, offices, and banks, commercial places of assembly, community services, and accommodation are non-complying and the potential size of permitted activities more constrained in neighbourhood than suburban centres.

25. Applying the Neighbourhood Centre rules proposed for the PDP to the Ruakura Main Street Centre will reduce the potential for employees to purchase day-to-day household supplies (thereby combining work and shopping trips). In addition, it largely excludes non-retail consumer and business services of the sorts that might be expected in a centre servicing a substantial area of business and employment. Such limits and exclusions are inconsistent with the likely level and diversity of demand for retail and associated services in a large mixed use area.

Table 1 Differences between Business Zones 5 and 6 Rules in PDP

Rules - Activity Status:

Differentiating Business Zones 5 and 6 5 Suburban Centre 7 Neighbourhood Centre Industry Light Industry D NC Transport Depot D NC Offices Office < 250sqm GFA/site P D Office 250-500sqm GFA/site D NC Retail/Commercial Retail 150-399sqm GFA/tenancy P D Retail 400-999sqm GFA/tenancy D NC Banks >199sqm GFA P NC Supermarket RD NC

Building Improvement Centres D NC Cafes, restaurants & licensed premises

>199sqm GFA P D

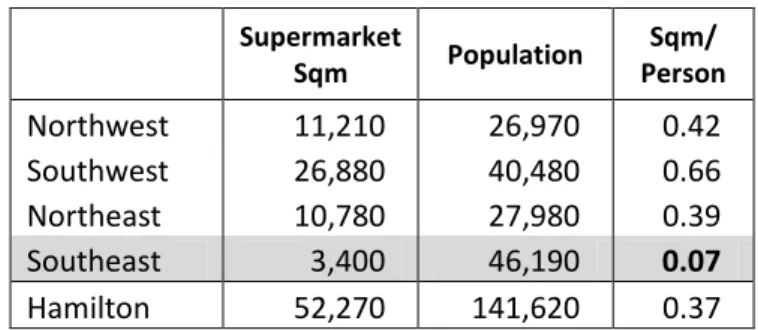

Commercial places of assembly (excl.

cinemas & bowling alleys P NC Commercial places of assembly (cinemas &

bowling alleys) P NC

Drive-through services (excluding automotive

fuel retailing) D NC

Drive-through services (automotive fuel

retailing) D NC

Parking lots & parking buildings D NC

Community

Health-care services 250-1,000sqm GFA,

ground floor level P RD

Tertiary education & specialised training

facilities >249sqm D NC

Residential

Detached dwellings & duplex dwellings NC D

Visitor Accommodation D NC

Source: Hamilton City Proposed District Plan, Section 42A Hearing Report, Chapter 6 Business Zones

26. A Main Street centre in Ruakura needs to offer the scope, scale and flexibility of commercial activity appropriate to a modern business and employment environment, as well as meeting the retail needs of residents. At 4.0ha Ruakura Main Street Centre would be just below the mean for current and planned Suburban Centres in Hamilton (4.1ha1) and above the median (3.2ha; Table 1, p.6, Ruakura Retail

Centres report). In comparison, Hamilton East covers around 4.5ha and Five Cross Roads 2.6ha. It is modest in comparison with the provisions made for the Rotokauri and Rototuna Growth Cells (7.1ha and 9.5ha respectively).

27. The 3,500sqm provided for the Integrated Retail Development in the Medium Density Residential area (Plan Change 25H.9.6.10 a) is above the 1,500sqm provided for in the PDP (Rule 4.8.1.a) ii, p.4-32) but also close to the mean (3,400sqm) of the 63 neighbourhood centres identified in the Review of Retail Development and Planning (pp17-18). It is well below the maximum of 5,000sqm provided for in the PDP (Explanation, Objective 6.2.3).

Key Findings from Retail Review Report

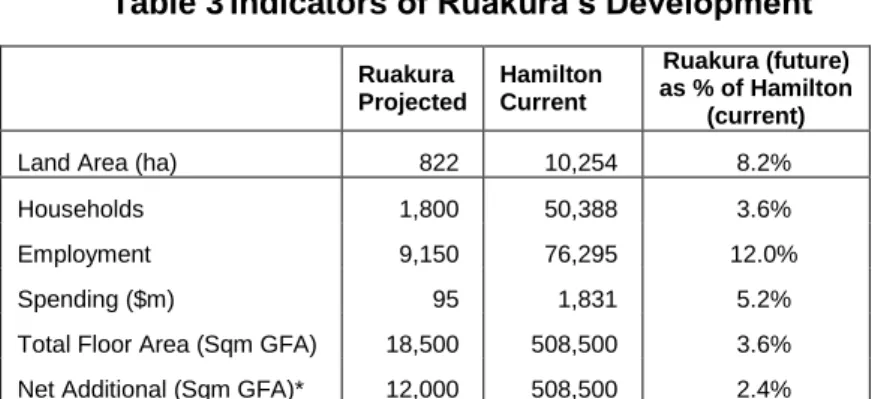

28. Ruakura Retail Centres reports an assessment of the likely demand for retail capacity based on projecting demand at full development of Ruakura. The structure of the model, data sources and assumptions are those set out in my report Retail Planning and Development in Hamilton: a Review (pp.65-68) which, incidentally, yielded much the same estimate of total expenditure in Hamilton as estimated by Property Economics in 20102. The application of the same assumptions to Ruakura confirms the need for substantially more retail land than proposed in the PDP to meet the anticipated growth of the night-time (residential) and daytime (employment and business) populations provided for in the Plan Change.

29. Depending on the productivity of sales achieved (defined in terms of dollars of expenditure per square metre of gross floor area – sqm GFA)

1 Incorrectly recorded as 3.1ha in the Ruakura Retail Centres report. 2 Property Economics (2010) Future Proof Business Land Data Assessment

this exercise indicates the need for between 15,900sqm and 22,700sqm of retail capacity (including food services) to cater for the additional local demand. If a relatively high building 42% footprint is achieved, this would suggest a need for 3.8ha.

30. The scale of retail development I have estimated clearly supports Suburban Centre (Business 5) rather than Neighbourhood Centre (Business 7) zoning within the Knowledge Area, as well justifying a substantial Neighbourhood Centre (Integrated Retail Centre in the Plan Change) in the Medium Density Residential area.

31. Having said that, I acknowledge considerable uncertainty around planning for retailing and associated uses. Unforeseeable changes in the drivers of demand and supply will influence the detail of how and where retailing develops. I therefore assessed the contingencies that might alter my projections of demand. This led me to conclude the demand for retail capacity from developing Ruakura is more likely to be above than below my estimate (Ruakura Retail Centres, pp10-12).

32. To the extent that the Ruakura Main Street building footprint allowed in the Plan Change is less than my estimate of future retail demand some activities, particularly services, may need to be accommodated in first floor premises. In addition, some of the additional retail demand will need to be satisfied by other centres outside Ruakura.

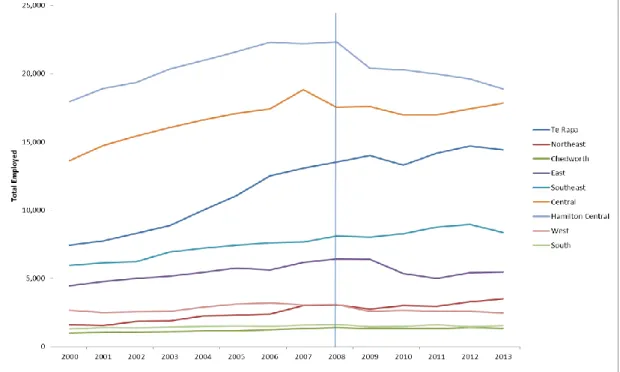

33. On the grounds that the additional demand that I have estimated is less than provided for in the Plan Change, it is unlikely that the provision for a Suburban Centre and integrated retail centre in Ruakura will have an adverse effect on nearby retail centres. There are a number of reasons for this conclusion. First, the capacity proposed is intended to cater primarily for Ruakura’s local growth; second nearby centres (such as Five Crossroads, Clyde St, and Hamilton East) should secure a share of the increased expenditure (as well as any increases arising from residential intensification in the nearby suburbs east of the river); and third, these centres are generally well tenanted and have little if any capacity for expanding their footprints.

34. In addition, the major centres in Hamilton (the CBD, The Base, and Chartwell) have distinctive functions which they will sustain and no doubt expand as the City continues to grow.

35. These matters are considered further in response to submissions received by the Board of Inquiry.

Submissions

36. The following submissions raise objections to the Plan Change provisions for a Suburban Centre.

37. Submission References 103661 Letford F., 106528 Centre for Redefining Progress:, 106887 Ellis J., 106624 West J: A number of submissions have been received that express concern about the scope and scale of retailing that might invest in the Ruakura Main Street centre, including concerns that it will be similar to The Base (Centre for Redefining Progress, West) and that it will pre-empt recovery of the CBD, relegating it to “small mall” status (Letford).

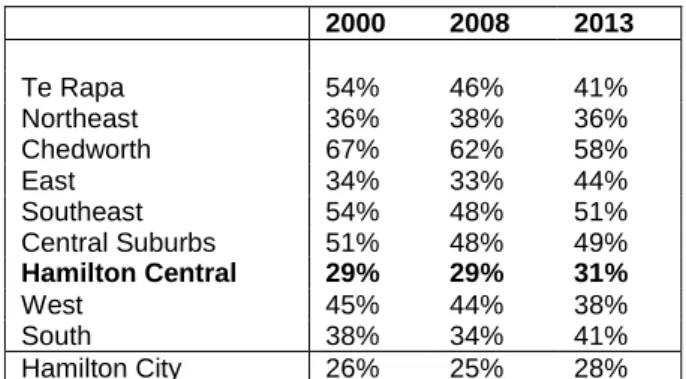

38. Submission Reference 106894 Waikato Regional Council: The Waikato Regional Council does not oppose the Suburban Centre zoning, but seeks recognition of the primacy of the central city:

Waikato Regional Council notes that the Knowledge Area (25H.7 of the plan change) provides for retail and commercial activities in a ‘suburban centre’. Waikato Regional Council does not oppose the concept of a suburban centre in this location, and understands the rationale for supporting the industrial area with limited commercial activity. However Waikato Regional Council is concerned that the plan change provisions do not adequately reflect the need to maintain the hierarchy of commercial centres throughout greater Hamilton. In particular, the plan change does not recognise the Central Business District (‘CBD’) of Hamilton as the primary commercial centre of Hamilton, and the need to maintain its vitality and viability. (Para 3.11, Pp8-9)

39. The Regional Council consequently seeks a new objective and policies recognising the primacy of the CBD and avoiding development that might undermine it (Attachment Two, Table 2).

40. Ref 106901 Future Proof Implementation Committee: The Future Proof Implementation Committee submission adopts the same position as the HCC in promoting a neighbourhood centre “which is significantly smaller in scale (generally no larger than 5,000m2 gfa) and function (to serve a residential neighbourhood)”. The grounds for this are that:

“supporting the primacy, vitality and viability of the Central City is fundamental to achieving the strategic approach of the Future Proof Strategy … The Hamilton Central City has to be able to support the wider region by fulfilling its function as the primary centre for the Waikato. The Central City cannot fulfil these functions if we continue with a decentralised model of retail and commercial activity. The sub-regional centre (sic) proposed in the Ruakura Plan Change runs a real risk of competing with and potentially undermining the Central City”. 41. Consequently it seeks “the reclassification of the proposed centre to be

a Neighbourhood Centre as defined in the Business Centres hierarchy in the PDP” or else “a full assessment of the impacts that a proposed suburban centre will have on the retail network and business hierarchy within Hamilton City in accordance with the Centres Viability Assessment Report as described in the PDP Volume 2, Section 1.5.20”.

42. Ref 106914 Hamilton City Council: The Hamilton City Council submission claims that objectives and policies in the Plan Change:

Have selectively sought to limit or exclude from consideration the future viability, function, vibrancy and amenity of the Central City when considering all types of future development within the Plan Change area. The Primacy of the Central City in the PDP is not acknowledged in the Planned Change. Similarly, there is no recognition of the hierarchy of business centres presented in chapter 2 of the PDP" (Part B, para.30, p8).

43. The table that references differences between the PDP and the proposed Plan Change in the HCC submission (Part B, pp 9-10) notes that Paragraph 25 H.4.13 is inconsistent with the PDP policy that identifies the centre as serving a neighbourhood. This is elaborated in paragraphs 36 to 39 of the submission (part B, pp 10-11) which confirm that a Neighbourhood Centre would be significantly smaller and more limited in function than a Suburban Centre. The rationale is as follows:

Retail economics advice relied on by HCC supports a business centres hierarchy for the City, including provision for a neighbourhood centre in the general location of the Knowledge Area. The level of trading that could be achieved through a suburban centre would adversely affect adjacent (sic) established suburban and neighbourhood centres in south eastern Hamilton such as Hillcrest, Hamilton East and Five Cross Roads for example, and would be contrary to the business centres hierarchy outlined in Chapter 2 Strategic Framework and Chapter 7 Business 1 to 7 Zones of the PDP. (Part B, Para 37, p.11)

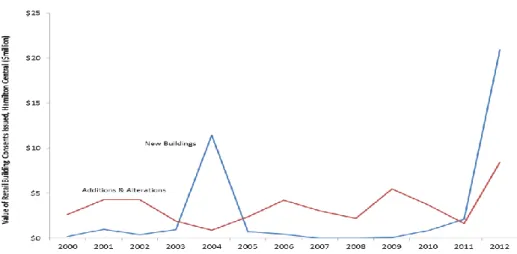

44. The Council rejects the application of the Operative Suburban Centre Zone provisions as they are “permissive with respect to the establishment of office and retail activities and would directly undermine the new business centres hierarchy promoted in the PDP” (Para 38, p.11).

45. It also seeks to replace the provision for an integrated retail centre in the Medium-Density Residential Area (25.H.9) with Rule 4 of the PDP “including the objectives, policies, assessment criteria and notification rule provisions” in which retail activity (except as a home-based occupation) is Non-Complying (4.3, p4.12).

46. Ref 107038 Kiwi Property Holdings Ltd and Kiwi Property Management Ltd (Kiwi). Kiwi submits that its interests in the CBD have “been adversely affected by a decline in the vitality, amenity function and role of the CBD” over the past ten years, a decline that “has generated significant consequential adverse effects in the social, economic and cultural wellbeing of residents and visitors to Hamilton City“ (para. 3(c), p2). The submission holds that these “adverse effects

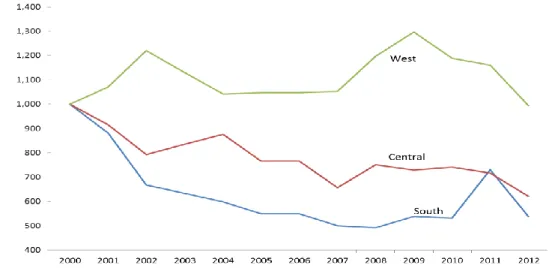

activity including offices throughout the business zoned areas of the city and in particular to former light industrial areas in the northern part of the city” (Para 3(d)). Consequently, the submitters consider that “the extent and nature of activities that could be established under the Knowledge Area and Suburban Centre provisions are such that they are likely to generate significant cumulative adverse effects on the vitality, amenity, function and role of the CBD”

47. Among other things the submission requests that the Suburban Centre zone “be reduced in scope so as to cater for the local retail and service requirements generated by the adjacent commercial and industrial area but without posing a risk in terms of potential cumulative effects on the CBD and other centres” (para 4(c)(i), p5).

48. Refs 107129 Parkway Gateway Holdings Ltd and 107132 Portland Park Ltd: These submissions dispute provisions for a Neighbourhood Centre and service station in the Medium Density Residential area owned by CPL.

49. Parkwood Gateway Holdings Ltd was granted resource consent to develop a hotel (450sqm), retail building (300sqm) and food hall (400sqm) on its 1.06ha site in June 2012. That development lies on the north-eastern side of the planned Wairere Drive intersection. Portland Park Ltd was granted consent to develop a mixed use centre incorporating a child care facility, garden, medical, and education centres, a café, and 22 apartments at 370 Tramway Rd sited on the south-eastern side of the intersection in October 2013. Both sites are zoned Suburban Centre under the Operative District Plan. Parkwood Gateway is zoned a Neighbourhood Centre and Portland Park Residential under the Proposed District Plan.

50. The submitters are seeking deletion of rules providing for integrated retail development, associated provisions for car parks and access ways, and relevant assessment standards and rules in Area A of the Comprehensive Development Plan (Medium Density Residential). They are also seeking deletion of any provision for service stations as a Restricted Discretionary Activity. Their concerns include the lack of section 32 evaluation of the methods adopted, the appropriateness of

the area as a location, lack of detail on actual mix of activities, the assessment of effects, and inconsistency with “the intent of the commercial hierarchy established through the Proposed District Plan” and with District Plan objectives and policies seeking to ensure residential activities remain dominant in residential areas.

Summary of Issues Raised

51. Those submissions opposing the Plan Change provisions for centres generally seek provision for a Suburban Centre in the Knowledge Area to be changed to a Neighbourhood Centre on the grounds that:

(1) There is insufficient demand to support a Suburban Centre; (2) A Neighbourhood Centre zoning is more appropriate;

(3) Provisions for Suburban Centres in the Operative District Plan are inappropriate; and

(4) A Suburban Centre will have adverse effects on the CBD and other centres.

52. With respect to the Integrated Retail Centre planned for the Medium Density Residential area the Parkwood Gateway and Portland Park submissions suggest that:

(1) The proposed centre is not justified; and

(2) There is no need to make provision for a service station. 53. These matters are considered in the following section.

Response to Issues Raised

Issue 1: Demand

54. The most fundamental point to be made is that the commercial centres provided for in the Plan Change Area have been developed as a response to anticipated growth in demand for commercial, including retail, capacity as a result of the investment in and growth of the Ruakura Growth Cell. They comprise the only provision made for commercial centres through the whole Structure Plan Area. The floorspace estimates reflect this, but do not depend on capturing demand from elsewhere. In this respect they are consistent with the

PDP. Indeed, there is nothing in the Plan Change provisions that should in any way limit development in other centres, particularly in light of the likely growth in population in the north and east of the city.

55. The scale and nature of demand for retail floorspace in the Structure Plan Area will be associated with a combination of: residential development, expanding employment, business demands for commercial and professional services, and the presence of a transport hub. In addition, a centre at this locality with Park and Ride and public transit facilities will be an attractive location for a supermarket in an area of the city in which supermarket capacity is currently lacking.

56. The various sources of demand for centre-based commercial capacity are discussed below.

Household Demand

57. Household-based demand is estimated at around $35m a year ($19,400/household) on full development. At this level it would support 5,800sqm GFA of retail floorspace assuming sales of $6,000/sqm (Ruakura Retail Centres report, p9), a relatively high level of floorspace productivity. At the more conservative level of $4,200/sqm the requirement would be for 8,300sqm to meet new household demand.

58. Even this figure may be considered conservative because it makes no provision for the possibility of achieving higher residential densities and thereby generating more demand than estimated here. Nor does it factor in any demand from households in Fairview Downs. This might be expected given the benefits of integration with the new Medium Density Residential area (Plan Change 25H.4.12b, p.16) and the degree of severance from areas to the west of the ring road. Indeed, the majority of Fairview Downs households are likely to be within a ten minute walk of the proposed centre.

59. Household-based retail demand is likely to be split between the Integrated Retail Centre (of 3,500sqm) in the Medium Density Residential Area, the Suburban Centre in the Knowledge Area, and centres elsewhere, including the CBD.

60. My estimates of new floorspace demand assumed no net leakage (i.e., spending by local residents in other centres will be matched more or less by spending by residents in Ruakura from other places). This may be seen as conservative insofar as the rural and lifestyle catchment to the east and south of Ruakura (comprising Tamahere, Matangi, Newstead and Tauwhare) will generate additional retail sales there.

Employment Demand

61. Based on an estimated 9,150 employees3 we can also anticipate $61m of employment and business-related retail spending at Ruakura (Ruakura Retail Centres, p.99). This would support another 10,200sqm (or more, depending on floorspace productivity) focused on the Ruakura Main Street Centre.

Business Demand

62. In addition, businesses in the area will generate demand for centre-based services other than retailing. Given the information- and skills-intensive nature of organisations likely to be located in the Knowledge Area in particular, and in an industrial area generally, meeting spaces, hospitality, and professional and business services might all be expected be attracted to the Main Street centre.

63. I have not tried to quantify the floor space demands this might make on a commercial centre. However, by way of illustration, I cited in the Ruakura Retail Centres report two examples of centres in industrial areas serving a mix of household, employee and business demand. One is Altitude at Auckland International Airport appears to cater predominantly for the 12,000 on-airport employees and employees from adjoining industrial areas. In 2012 the centre comprised 10,570sqm of retail floorspace on a 2.86ha site, with 508 carparks4. Major tenants included a supermarket, The Warehouse, Warehouse

3 This figure is based on of ratios of employees per hectare for manufacturing and transport related land

use and was calculated by Traffic Design Group for the Structure Plan area. It differs from the estimate of employment generated by Castalia for the development of the logistics centre which includes jobs generated among intermediate suppliers and services, some of which will be met off-site. It also differs from the employment estimate for the Plan Change area only (around 5,800)

Stationery, Postie Plus, Kiwibank/NZ Post, the National/ANZ Bank and six specialty shops. It has since expanded to include café and food outlets.

64. The other is a 25,000sqm centre, The Crossing, opened in late 2013 to serve a 107ha industrial park at Highbrook, East Tamaki. It includes fitness and childcare facilities, several cafes and restaurants, serviced apartments, three banks, lawyer and public accountant offices, a real estate office and recruitment agency. There is clearly an emphasis on business-related services in this centre, and the presence of banks is significant in both. Similar uses are likely (and desirable given objectives for development in Ruakura) in the planned Main Street Centre.

Leakage

65. My estimates of floorspace made no allowance for leakage, in effect assuming that spending by local residents in other centres is matched by spending in Ruakura by residents from other places (excluding local employees). This is probably conservative insofar as the rural and lifestyle catchment to the east and south of Ruakura (Tamahere, Matangi, Newstead and Tauwhare) will generate additional retail sales.

66. In fact, the provision in the Plan Change is for less floorspace in total than I estimated will be needed and favours net outward leakage. Household demand is likely to be split between the Integrated Retail Centre in the Medium Density Residential Area for mainly convenience goods and services and the Suburban Centre in the Knowledge Area for higher order services. However, given that there will also be employee and business demand catered for at the Main Street centre it is likely that significant higher order household demand will be transferred to other centres, such as Five Cross Roads and East Hamilton, as well as to the CBD.

A Transport Hub

67. Both the PDP (3.7.1.5, p3-47) and the Plan Change (25.H.7.1, p28) anticipate a “passenger transport hub” to provide a connection to the

central city and integrate into the city’s public transport as part of the Main Street centre. The Knowledge Zone Draft Master Plan (Boffa Miskell) suggests a total of 451 car parks, 322 on-site and the balance on-street. Assuming that the bulk of the on-site parks are utilised as part of the Park and Ride facilities, this raises the prospect of additional convenience retail demand in the Main Street centre associated with bus and car movement through the transport hub.

A Supermarket Opportunity

68. The development of a diverse centre alongside a transport hub creates the opportunity to integrate a supermarket readily accessible through car and public transport, especially to residents in the east and southeast of Hamilton. Quite apart from the impact of growth in demand from additional day-time (employee) and night-time (household) populations in Ruakura, an analysis of the distribution of current supermarket capacity relative to the distribution of population (with supermarket coverage measured as square metres GFA per person across four city sectors) indicates that the east and south of the city are currently under-served (Table 2).

Table 2 Distribution of Supermarket Capacity, 2013

Supermarket Sqm Population Sqm/ Person Northwest 11,210 26,970 0.42 Southwest 26,880 40,480 0.66 Northeast 10,780 27,980 0.39 Southeast 3,400 46,190 0.07 Hamilton 52,270 141,620 0.37

Note: (1) City divided west-east by the Waikato River; north south by Mill St/SH23 and Boundary Rd/Fifth Ave. Southwest includes CBD

(2) Progressive is considering a stand-alone supermarket of 4,400sqm for the former Mighty River Power site on Peachgrove Rd. If this goes ahead the ratio for the Southeast based on the 2013 population would be 0.17.

Source: Colliers International, Census 2013

69. A supermarket in the Main Street centre would improve currently low supermarket access and choice in these areas, catering at the same time for local employees. Outcomes of supermarket development in Ruakura Main Street would include diminished distances travelled residents in the southeast, enhanced opportunities for multi-purpose

visits especially among Ruakura-based employees, and more intensive use of private and public transport infrastructure.

Issue 2: A Neighbourhood or a Suburban Centre?

70. The business zones provided for by the PDP are explained in the Hamilton City Council s149G report to the Board of Inquiry in terms of a hierarchy the aim of which is “to re-establish the primacy of the Hamilton Central City and define its relationship with the sub-regional centres and suburban centres, …” (p16)

71. The report stated that the purposes of the Knowledge Zone include providing “further opportunities for a wide range of education, research and development activities with supporting retail and mixed use activities” and that one of the objectives is “to support the continued development of a research, education, innovation and technological activity precinct at Ruakura”. At the same time it suggests that the zone is “appropriate for a neighbourhood centre” within which activities “shall principally serve their immediate neighbourhood”.

72. However, Neighbourhood Centres are defined in the PDP as providing “a limited range of everyday goods and services and essentially serve a walk-in population. … it is essential that the range and scale of activities is compatible with neighbouring residential and local amenity values. Very limited opportunities exist for expansion of these centres”. The PDP also states that “neighbourhood centres are small in land area and shop sizes are between 100-300m² with the overall floorspace for a centre between 500-5,000m². The anchor store is likely to be a superette” (PDP Objective 6.2.3, Explanation, Vol. 1 p.6-7,8).

73. These constraints are inappropriate for the Ruakura Main Street Centre on the following grounds:

(a) Demand associated with new businesses, employment, and residents in the Ruakura Growth Cell will support and require substantially more retail and service capacity than might be provided at a Neighbourhood Centre. Recognising the form of demand in the immediate neighbourhood is important to supporting the growth of the businesses, organisations, and

employment generating much of that demand, growth that is the reason for the Plan Change. Conversely, under-providing will diminish the efficiency of retail behaviour by creating demand for longer trips and may also slow the rate of growth in Ruakura relative to what might otherwise be achieved.

(b) Neighbourhood Centres are generally established in existing residential areas with little capacity to expand. The policy focus is on retaining the character of small shops offering convenience goods for households within walking distance. The Ruakura Main Street centre is effectively a greenfield site that does not face any physical constraints and will serve diverse demands. It is not located in a residential zone.

(c) It is to be expected that the range of goods and services offered by a commercial centre will reflect its setting. In Ruakura households, business, tertiary, and research institutions, their employees, and students will populate the wider (suburban) catchment and help shape its character and functions. The constraints set out for Neighbourhood Centres focus on a character and scale inappropriate and inadequate for this setting. (d) Provision for a transport hub is inconsistent with provisions for a

Neighbourhood Centre zoning in which parking lots are classified as non-complying activities. A transport hub may serve as a destination or origin for commuters, for recreation and retailing trips, and for people attending to personal business. This will no doubt place some additional pressure for activities and amenities in the vicinity unlikely to be found in a Neighbourhood Centre. 74. I conclude that a Neighbourhood Centre zone is inappropriate for the

location and the anticipated demands on a commercial centre within the Ruakura Knowledge Area.

Issue 3: Provisions associated with the Operative District Plan

75. The PDP objectives for Ruakura include providing “a significant new employment area based around the development of a regional logistics hub”, maximising the use of existing infrastructure, and creating

“opportunities for the ongoing development of research, learning and innovation activities” (PDP, Volume 1, 3-44).

76. Provisions made for Suburban Centres in the Operative District Plan (ODP) offer a more promising way of contributing to these objectives and accommodating both the uncertainty and diversity of activity there than the rules associated with either Neighbourhood or Suburban Centre zoning under the PDP. The ODP focuses more on the quality and needs of individual centres rather than on seeking to moderate or allocate growth across centres. It aims at: “accommodating rapid change, minimising restraints on competition, and recognising and responding to differing environmental implications” (p.6.0-1).

77. There are two general objectives for the Suburban Centre zone in the ODP (additional provisions are made for the Rotokauri centre). Objective 6.2.1 aims to facilitate a wide range of suburban business opportunities throughout the city in association with residential neighbourhoods in an environmentally acceptable manner. The associated policies focus on accessibility relative to the distribution of the population and on effects in the immediate locality, particularly with respect to the residential environment. They are intended to:

a) Enable a wide range of commercial and related activities to be established within suburban centres.

b) Facilitate the wide distribution of suburban centres throughout the city including the new growth areas, which enables convenient access to a wide range of goods and services, provided the adverse effects of any development on adjoining areas can be minimised.

c) Ensure that the scale of suburban centres is compatible with the amenity values of the surrounding residential neighbourhood.

d) Enable the expansion of existing suburban centres in established residential areas in circumstances where the scale and location of development would not impact significantly on the wider residential neighbourhood.

e) Minimise the adverse effects associated with suburban centres on the traffic safety and efficiency of the city’s transport network (6.2-2). 78. The second objective deals with the amenity values associated with

commercial centres and potential impacts on surrounding residential environments.

79. The rules allow for a range of activities subject to complying with design and site coverage requirements. Permitted activities include:

Any Retail Activity, Offices, Health Care Services, Restaurants, Licensed Premises, Community Centres, Places of Assembly, Marae, Education and Training Facilities, Warehouses, Accessory Buildings, Informal Recreation and Ancillary Buildings, Relocated Buildings

80. Activities controlled with respect to design and configuration of buildings, site layout, vehicular provision include:

Apartment Buildings, Residential Centres, Managed Care Facilities, Rest Homes, Visitor Accommodation

81. Discretionary Activities include:

Drive-Through Services, Parking Lots and Parking Buildings, Any other residential activity, Fire Stations

(ODP, pages 4.2-2, 3)

82. The PDP is more prescriptive (as indicated in Table 1, p.8 above) and consequently less flexible. It seeks in an open-ended way to limit activities in the Business 5 Zone (Suburban Centres) that might compete with the CBD by treating offices over 250sqm and retail premises over 450sqm as discretionary, for example (Chapter 6 Business Zones, PDP). In the present case the threat of “excessive” competition with the CBD is curtailed by the commitment to a 15,000sqm cap on the Main Street Centre.

83. In contrast, the flexibility provided for in the ODP allows for changing consumer behaviour, changes in retailing itself, and greater diversity of demand. It appears more appropriate for a growth cell where demands

for a range of centres-based activities unlikely to be found in, or suited to, a Suburban Centre subject to the rules of the PDP.

Issue 4: Impact on the CBD and the Subregional Centres

84. This issue is discussed below under several subheadings. The first one deals with the significance of the proposed retail centres in the wider Hamilton retail market. Subsequently, it addresses in more detail the issue of whether or not the Main Street Centre will undermine in any way the primacy of the CBD.

Significance

85. In this section I consider the significance of the additional retail floorspace proposed in the Plan Change compared with the PDP (an additional 12,000sqm GFA) on other centres and then assess in more detail the possible impact on the Central City.

86. In order to place this difference in context I have compared the size of the Ruakura development with Hamilton’s current area (based on LINZ Topographic 50 series, sourced by Boffa Miskell), and the anticipated additions to household numbers, employment, retail spending, and floorspace at Ruakura when it is fully developed with current estimates for Hamilton City. For the Hamilton figures I have used the 2013 Census, the SNZ Business Directory, Quotable Value New Zealand (QVNZ) floorspace data, and spending estimates contained in my Retail Review and June 2013 Report.

87. QVNZ identified 410,000sqm in its Retail category in Hamilton City in 2012, an increase of 170,000sqm (70%) since 2000, or 13,000sqm per year5. On this basis, the additional floor area proposed for the Ruakura centres represents less than a year’s historical gain.

88. The QVNZ retail category excludes integrated centres (allocated to the Mixed/Other category by QVNZ). Including Chartwell Square, Centre Place, and Te Awa malls lifts the figure to 508,500sqm retail GFA. On

this basis, the difference between PDP and Plan Change provisions is equivalent to just 2.4% of Hamilton’s current retail floor space.

89. Other indicators confirm the limited significance of the retailing proposed for Ruakura and consequently the limited impacts (if any) it might have on other centres. At full development the anticipated population at Ruakura represents 3.6% growth of current Hamilton household numbers (Table 3). Anticipated employment represents 12% of 2013 city employment. The projected gain in household and business spending is 5% of estimated spending in 2011. However, the total provision for retail centres represent only 3.6% of current floorspace.

Table 3 Indicators of Ruakura’s Development

Ruakura Projected Hamilton Current Ruakura (future) as % of Hamilton (current) Land Area (ha) 822 10,254 8.2% Households 1,800 50,388 3.6% Employment 9,150 76,295 12.0% Spending ($m) 95 1,831 5.2% Total Floor Area (Sqm GFA) 18,500 508,500 3.6% Net Additional (Sqm GFA)* 12,000 508,500 2.4%

Note: * 2,000sqm additional for neighbourhood centre and 10,000sqm for the suburban Main Street centre

90. In other words, the provisions made for retail floorspace match the anticipated gains in household demand but fall well below the combined employment-related and household spending growth that will take place in the Ruakura Structure Plan area.

91. On these grounds I conclude that the development of the centres as proposed will not have a significant – if any – effect on the integrity or form of retailing in Hamilton other than that associated with catering for the demands of a new growth cell. This is consistent with the fact that my estimates of demand for floorspace are higher than planned provision indicating that there will be significant spill-over in demand into nearby centres as a result of Ruakura’s growth.

Impact on the Central City

92. With respect to the Central City the Hamilton Urban Growth Strategy Technical Report in 2008 concluded that the “main difficulties facing the Hamilton CBD are the adverse development economics in the retail heart and the lack of suitable sites nearby to attract the clustering of good quality, affordable small office space”. This is because “there appears to be no financial benefit from locating in CBD (sic). There is (sic) cheaper land, lower rates, and lower rentals for new premises located elsewhere, where there is plenty of free car parking”. In addition, “rentals do not support rebuilding or refurbishment of existing buildings”, “CBD pedestrian traffic is falling” and [there is] “lack of activity, energy and vitality to energise all the existing and possible future retail frontages and laneways” (p24). This explanation of under-performance highlights failings in the CBD, not the merits or performance of other centres.

93. The implication is that the CBD is subject to more fundamental influences on performance than any disadvantage that might arise from the progress of other centres. If there were to be an adverse impact from the additional 10,000sqm that lifts the Ruakura Main Street centre from neighbourhood to suburban status, for example, it would be difficult technically to disentangle this impact from the influence of more fundamental drivers of change. In fact, that increment would represent just 5.3% of the Central City floorspace (based on the QVNZ 2012 figures for Retail, adjusted to include Centre Place).

94. While the limited increment in floor space proposed in the Plan Change means it is unlikely to have a significant impact on the CBD or sub-regional centres, I present below the results of an assessment of indicators of central city performance since 2000. These correspond broadly with matters to be considered in the proposed Centre Assessment Reports6. They include the impact on the vitality, function and amenity of the Central City and the sub-regional centres other than those associated with competition (item a) and whether a proposal reinforces the primacy of the Central City and the functions of other

6 Hamilton City Proposed District Plan, Section 42A Hearing Report 5 February 2014 Report on Submissions and Further Submissions, Appendix 1 – Volume 2

centres (item d). The Information Requirements for a Centre Assessment Report set out in s42A report are retail expenditure patterns, floorspace and activity mix, employment by type, pedestrian environment and flows, parking and public transport connections, and retail and office demand and supply, including vacancy levels (1.2.19 PDP, s42A proposal).

95. In the assessment I have used relevant indicators based on Hamilton Central CAU. This corresponds broadly with the Central City Zone (CCZ) in the PDP, although it also contains a residential and motel precinct between Mill Street and Edgecumbe Park. Conversely, it excludes the Opoia and Sonning carpark areas on the eastern side of the river which are included in the CCZ.

Central City Indicator 1: Employment

96. Hamilton City and Hamilton Central employment peaked in 2008 when the latter accounted for 28% of the city’s total. It has fallen since, by 15% in the centre and 4% across the city (Figure 1). The CBD loss has been offset in part by growth in central suburbs, the Northeast, Southeast and Te Rapa (Figure 1). It appears that the downturn associated with the GFC impacted unevenly on employment across the city, and was particularly pronounced in the CBD.7

97. This is not surprising. The pressures on business from an economic downturn can be expected to impact most heavily on the largest and longest established areas where older business units are most likely to be concentrated and costs are likely to be relatively high. This appears to have been the case with the impact of the GFC on the Hamilton CBD, accelerating the contraction of lower order employment there.

98. However, while employment fell after 2008, this varied by sector. Between 2000 and 2013 Hamilton Central CAU experienced falls in manufacturing (with employment down by 240 jobs), transport, storage, and wholesaling (-330), retailing (-660), financial services (-370), information, media and telecommunications (-350), and business

administration (-170). Other than in manufacturing and wholesaling, these falls all took place after 2008. They were offset, though, by gains in professional, technical and scientific services (+1,360), health and social services (+780), government administration (+270), and education (+240).

Figure 1 Changes in Employment, Hamilton City Geographic Divisions, 2000-2013

Source: Business Directory, Statistics New Zealand

99. The loss from Hamilton Central CAU of 3,430 jobs between 2008 and 2013 would have seen retail demand in the City Centre decline by $22m according to the Property Economics’ employee retail demand multiplier adopted for this study ($6,460/employee). This means that any decline in CBD retailing would be attributable in part to local labour market changes rather than a response to retail expansion elsewhere.

100. The share of Hamilton Central’s employment in the secondary sectors (manufacturing, transport, storage, construction) fell from 10.1% in 2000 to 6.4% in 2013. Retailing fell from 17.4% to 13.0% of central city jobs, and business services (information media and telecoms, financial services, and business administration and support) from 18.3% to 13.1%. The professional services sector, on the other hand grew from 10.7% to 17.4%. Public sector employment increased its dominance,

with public administration, social and health services, and education employment jointly growing from 27.7% to 33.2% of central city jobs.

101. There is no doubt that the City Centre retains its primacy despite the more rapid growth of retailing elsewhere in the city. In 2012 one quarter of the city’s jobs was in Hamilton Central. Over two thirds of employment in financial services was there, 56% of government administration, 48% of information, media and telecommunications, 45% of professional and scientific services, 43% of hospitality services, 40% of rental and real estate services, one third of employment in utilities, 32% of arts and recreation services, and 30% of retailing.

102. In keeping with this primacy, employment in Hamilton Central remains diverse relative to other parts of Hamilton. The two sectors (of 19 ANZSIC categories) with the largest share of employees accounted for only 31% of total Central City employment in 2013, compared with 41% in Te Rapa and 58% in Chedworth (with its dependence on retailing in Chartwell Square) and 28% for the City as a whole (Table 4).

Table 4 Comparing Employment Diversity by Area , 2000-2013

2000 2008 2013 Te Rapa 54% 46% 41% Northeast 36% 38% 36% Chedworth 67% 62% 58% East 34% 33% 44% Southeast 54% 48% 51% Central Suburbs 51% 48% 49% Hamilton Central 29% 29% 31% West 45% 44% 38% South 38% 34% 41% Hamilton City 26% 25% 28%

Note: % is employment share of top two of 19 sectors in each area Source: Business Directory, Statistics New Zealand

Employment Shifts – Evidence from Elsewhere

103. To put the Hamilton CBD into context, employment shifts are shown for New Zealand’s six largest cities (Table 5). Since 2000 there has been a significant reduction in the share of employment located within the CBD in Tauranga and, to a lesser extent, Dunedin. In Auckland’s case

there was some recovery following the post-2007 downturn8, while the reductions in share for Wellington and Christchurch were minor.

Table 5 Shares of City Employment in the CBD, Six Cities

All Industry Retailing

2000 2006 2012 2000 2006 2012 Auckland 14.0% 13.2% 14.1% 5.9% 6.2% 5.9% Hamilton 31.7% 30.0% 25.2% 47.8% 43.1% 30.4% Tauranga 26.0% 23.4% 22.2% 38.1% 35.5% 35.9% Wellington 37.5% 37.0% 37.0% 5.8% 6.4% 5.6% Christchurch* 29.3% 28.0% 28.0% 26.3% 23.7% 21.2% Dunedin 32.0% 32.4% 30.0% 43.9% 38.5% 34.8%

Note: * Christchurch data for 2010 (pre-earthquake), not 2012 Source: Business Directory, Statistics New Zealand

104. The concentration of retailing in the CBD appears inversely related to city size. The CBD contains only 6% of Auckland’s retailing, with an even smaller share in Wellington CBD (relative to the wider urban area including Upper and Lower Hutt, and Porirua). Among the smaller cities Dunedin (127,500 residents) and Tauranga (117,600) have smaller populations than Hamilton (150,200), explaining in part why they have retained a larger share of retailing in the CBD. The implication is that as Hamilton expands the share of retailing and employment in the city centre can be expected to diminish further.

Employment Trends - Conclusion

105. Rather than denoting a decline, the recent contraction of employment can be seen as a transition as the city centre reduces its dependence on lower order employment (including retailing) while retaining its role as the diverse and dominant economic and commercial, social, administrative and community centre of Hamilton City and Waikato Region. There is no reason to suggest that providing a Suburban Centre at Ruakura in any way threatens the future of the CBD, if only on the grounds of the latter’s changing structure and the increasing importance of specialised and public services to employment there.

8 The recently announced withdrawal of department store The Farmers from the Auckland CBD (The New Zealand Herald, 19 February, p.A9) is indicative of the reduced status of CBD retailing, however.

Central City Indicator 2: Area of Commercial Floorspace

106. QVNZ floorspace data reveals a decline in the Retail category in Hamilton Central of 4,400sqm between 2007 and 2012 (Table 6). This was less than might be expected from the decline in retailing spending suggested in paragraph 99, above (5,300sqm at sales of $4,200/sqm GFA) and was, in any case, not sufficient to offset the longer term increase (a net gain of 15,200sqm since 2000).

Table 6 Commercial Floor Space, Hamilton Central, 2000-2012.

2000 2007 2012

Sqm Share Sqm Share Sqm Share

Retail 143,900 19.3% 163,500 20.7% 159,100 21% Office 183,300 24.5% 188,200 23.8% 187,600 24% Other/Mixed 311,400 41.7% 315,500 39.9% 290,700 38% Other 108,700 14.5% 124,400 15.7% 132,800 17% Total 747,300 100.0% 791,600 100.0% 770,200 100% Source: Quotable Value New Zealand

107. Presumably, there was some growth in household or visitor based spending to offset any decline in local retail spending associated with contracting CBD employment. It is also possible that the more

specialised employment structure indicated in the figures is supporting a greater level of workplace-based spending per head.

108. These floorspace figures also exclude Centre Place which as an integrated centre falls in the QVNZ “Mixed/Other” category and not retailing. Centre Place expanded by around 11,500sqm GFA in 2013. This investment reinforces the conclusions that retailing in the central city is not contracting across the board.

109. However, the expansion of Centre Place is consistent with changes in the form of retailing in the Central City, away from independent medium format main street stores selling comparison and personal items and towards more chain store outlets co-located within a large, integrated centre with an attached car-park. Refurbishing, and redeveloping central city retail space even as the labour force declines is consistent with a change in the structure of the sector which is, among other things, leading to gains in labour productivity.

110. Despite the expansion of Centre Point, the Other/Mixed category suffered a fall in CBD floorspace (Table 6). However, the relatively poor performance of the office category between 2007 and 2012 has been offset recently with the opening of the PWC Building in 2013 which together with the Riverside development (Project Grantham) added 9,000sqm of new A grade office space.

111. If we take a medium-term view (2000-2012) and include these recent additions, the evidence is not consistent with any claim that central Hamilton is in decline despite the expansion of office and retail floorspace in other areas. The Central City does not appear to have lost retail and office floorspace. Indeed it appears to be undergoing a boost in investment following of a hiatus from 2008 to 2012.

Central City Indicator 3: Investment in Buildings

112. The suggestion of a recent recovery in central city retailing is confirmed by building consents data which is the most readily available indicator of investment in floorspace among areas and sectors. 9

113. Retail floor area growth of 37,800sqm between 2000 and 2012 within Hamilton Central accounted for 15% of the 245,00sqm consented across the city as a whole (31% between 2000 and 2004, 2% over the next four years, and 10% from 2009 to 2012). Limited investment when retailing was buoyant in the middle of the decade may have penalised the sector there in the more challenging times after 2007 (Figure 2).

9 Inferred growth from consented floor area does not allow for demolitions, however, and not all

consents issued will be acted on (particularly with the onset of a downturn) so they are useful as a broad indicator of investment trends only.

Figure 2 The Value of Consents Issued, Hamilton Central 2000-2012

Source: Statistics New Zealand

Central City Indicator 4: The Pedestrian Environment

114. Pedestrian counts have been falling since at least 1994 (Figure 3).10 However, the trend (best described by a logarithmic curve R2= 0.75) indicates a falling rate of decline. The exception, the downturn of 2012, is most likely associated with the impact of Centre Place redevelopment.

Figure 3 CBD Pedestrian Counts, 1994-2012

Source: Property Institute of New Zealand, Waikato Branch

115. Retail employment expanded 14% between 2000 and 2006 while pedestrian counts fell at the same time, indicating that changes in the pedestrian environment are not related directly to retail performance. Rather, increased commercial car park capacity indicates a shift from pedestrian to car-based access to and around the centre (Figure 4).

116. Greater car use suggests that over time the centre’s regional reach (a measure of primacy) may have expanded. It is also associated with changes in how the centre is used. When counts are aggregated into broad precincts, for example, the North/West more or less held its own (Figure 5) while the South contracted. The Centre also fell, despite a short rebound late in 2011.

Figure 4 Aggregate Pedestrian Counts and Commercial Car Parking Capacity

Source: Car Park data sourced from Hamilton City Council, Boffa Miskell Ltd

117. Such changes are no doubt continuing. They are consistent with retail and other activity concentrating in and around Centre Place. At the same time, large format stores have established on the edge of the CBD with significant car parking. These include Kmart and The Warehouse, Countdown and PAK’nSAVE. Together with the Victoria-Hood Street café and cultural quarter they create alternative destinations which rely more on vehicle than pedestrian access.