Principal and Agent Relationships

in the Financial Crisis in 2008

Authors

Preface

The topic of the work deals with the consequences of the principal-agent relationships in the financial crisis of the year 2008, particularly the one of relationships in the AIG. The following questions are dealt with: What kind of relationships are there? Which characteristics do these relations have? Which possible solutions there are to defuse the problems in these relation-ships?

This scientific work was made in the context of the module Business Science. The module is part of the Master of Science of Business Information Systems course of the University of Applied Sciences Northwestern Switzerland (www.fhnw.ch/msc-bis). The work was carried out as teamwork. For the co-ordination of the group the service "Google Sites" was used (sites.google.com/site/bsrgwaig).

We would like to thank all persons and organization who have made for this work a contribu-tion. We thank the authors for their engagement at the search for literature and writing the contributions. We also thank the company Google for the provisioning of the services which has made a smooth cooperation possible.

Olten in December 2008

Table of Contents

Preface... I

Executive Summary...II

Table of Contents...III

List of Figures and Tables...V

List of Abbreviations...VI

1 The American International Group...1

1.1 History...1

1.2 Products...1

1.3 Vision & Values...2

1.4 Corporate Governance...2

2 AIG and the Current Financial Crisis...3

2.1 Chain of the events leading to the call for help at the FED...3

2.2 Situation at the Stock Exchange...5

2.3 Income Situation...6

3 Related Theory and Research Approach...8

3.1 Related Theory for the Principal – Agent Relationships at the AIG...8

3.2 Research Approach...9

3.2.1 Research Question...9

3.2.2 Hypothesis...9

3.2.3 Specific Aim...10

4 Principal – Agent Relationships...11

4.1 Relationship “CDS and CDO Insurance Customer (Banks) -– AIG Financial Products (Joseph J. Cassano)“...11

4.1.1 Characteristics of the Relationships...13

4.1.2 Problematic Nature of the Relationships...13

4.1.3 Solutions to Improve the Relationship...14

4.2 Relationship “AIG Holding – AIG Financial Products (Joseph J. Cassano)“...15

4.2.1 Characteristics of the Relationships...15

4.2.2 Problematic Nature of the Relationships...15

4.2.3 Solutions to Improve the Relationship...16

4.3.1 Characteristics of the Relationships...16

4.3.2 Problematic Nature of the Relationships...16

4.3.3 Solutions to Improve the Relationship...17

4.4 Relationship “AIG Financial Products (Joseph J. Cassano) – Consultant (Gary Gorton)”...17

4.4.1 Characteristics of the Relationships...17

4.4.2 Problematic Nature of the Relationships...17

4.4.3 Solutions to Improve the Relationship...18

5 Conclusion...19

List of Literature...20

List of Figures and Tables

Figure 2-1: AIG Situation: A tiny unit at American International Group... (The New York Times 2008a)...3

Figure 2-2: AIG Situation: ...was well compensated for generating a significant share of revenue... (The New York Times 2008a)...4

Figure 2-3: AIG Situation: ... from selling contracts that protected clients from losses on debt (The New York Times 2008a)...4

Figure 2-4: AIG Situation: Punished by rating agencies into a downward spiral (The

New York Times 2008)...5

Figure 2-5: AIG (Common Stock) Chart from November 15, 2007 to November 14,

2008 compared to the DowJones Index (BigCharts 2008)...5

Figure 2-6: Overview on the quarterly income since 2003 (NYTimes X)...6

Figure 4-1: Major Event between insurance customers the AIG (Mollenkamp et al.,

2008)...12

Figure 4-2: Notional Amounts Outstanding CDS, Semiannual Data 2001 -2008 (ISDA

2008)...14

Table 2-1: AIG (Common Stock) November 14, 2008 (BigCharts 2008)...6

List of Abbreviations

AIG American International Group, Inc. CDO Collateralized Debt Obligation CDS Credit-Default Swaps

1

The American International Group

The American International Group, Inc. (AIG) is a world leader in insurance and financial ser-vices. It is an international insurance organization with operations in more than 130 countries (AIG 2008c).

The AIG holding companies serve commercial, institutional and individual customers through a worldwide property-casualty and life insurance networks of any insurer. AIG companies are providers of retirement services, financial services and asset management.

AIG's common stock is listed at the New York Stock Exchange, and at the stock exchanges in Ireland and Tokyo.

1.1 History

According to the American International Group, Inc. (AIG 2008c), the company history of AIG started in 1919, when Cornelius Vander Starr founded an insurance agency named Ameri-can Asiatic Underwriters in Shanghai, followed by decades of expansion. Despite some diffi-culties in wartimes, Vander Starr established several companies like Asia Life Insurance Company, American International Underwriters, The Philippine American Life and General Insurance Company and American Inter-national Assurance Company, Ltd, represented in about 75 countries by the end of the 1960s. The firm American International Group, Inc. (AIG) was formed in 1967 and went public two years later with Maurice R. Greenberg as President and CEO.

Greenberg "was the chairman of the American International Group from 1968 to 2005, during which time he built the small insurance company into what became the world’s largest insur-ance and financial services corporation" (The New York Times 2008b).

Considering the context of today’s financial crisis and AIG's tarnished position, a very impor-tant step in AIG's history may be what AIG entitles with "Expanding into Financial Services" (AIG 2008c): In 1987, AIG Financial Products Corp. was formed in 1987 to specialize in com-plex derivative product transactions later followed by other AIG company foundations includ-ing leasinclud-ing, bankinclud-ing and real estate.

Concerning the company leadership, the past years brought more changes than the previous decades: Greenberg "was succeeded by Martin J. Sullivan and President and CEO…" who "… resigned from AIG in 2008, and was succeeded as CEO by Robert B. Willumstad.…” Mr. Willumstad now holds both the CEO and Chairman positions" (AIG 2008c).

1.2 Products

AIG offers product in four principal business segments (AIG 2008c):

Life Insurance & Retirement Services: AIG has the most extensive global network of any life insurer, a leading U.S. life insurance organization and a premier retirement services franchise with a leadership position in the U.S. fixed annuities market as well as a grow-ing international network.

Financial Services: AIG has a major presence in aircraft finance, capital markets, con-sumer finance and insurance premium finance.

Asset Management: AIG provides institutional and individual assets, retail funds and pri-vate banking through a growing global network.

1.3 Vision & Values

The vision which has given itself the AIG: “To be the world’s first choice provider of insurance and financial services. We will create unmatched value for our customers, colleagues, busi-ness partners, and shareholders, as we contribute to the growth of sustainable, prosperous communities.” (AIG 2008b)

The values which has given itself the AIG: “Our mission at AIG is to provide our customers all over the world with exceptional products and exemplary service; however, this goal can only be realized if we are consistently guided by our shared beliefs - our values.” (AIG 2008b)

1.4 Corporate Governance

The AIG’s Board of Directors has established the AIG Corporate Governance Guidelines to promote the effective functioning of the Board and its committees, to promote the interests of shareholders and to establish a common set of expectations for the governance of the orga-nization.

The Corporate Governance Guidelines contains:

Director Independence Standards

Charters of Audit

Compensation and Management Resources

Finance

Nominating and Corporate Governance

Public Policy and Social Responsibility

Regulatory, Compliance and Legal Committees

Director, Executive Officer and Senior Financial Officer Code of Business Conduct and Ethics

2

AIG and the Current Financial Crisis

Today, AIG is in a very uncomfortable situation due to the current financial crisis. Being the chain of the events represented briefly in the following as it has come to the FED to the call for help. And as the AIG share has developed at the stock exchange and its income in the re-cent years.

2.1 Chain of the events leading to the call for help at the FED

The New York Times (2008a) has the opinion that a tiny unit at American International Group brought the giant to the edge of bankruptcy: The London unit AIG Financial Products which sold complex financial contracts called credit derivatives. The following context turns out from dozens of interviews, from internal documents and testimonies before the U.S. congress.

It was all about Credit default Swaps (CDS) and CDO, a sort of insurance against payment losses. Over years AIG sold insurances for losses on debt in the value of many billions of dollars. All possible loans hid themselves behind these disastrous CDS and CDO: Company loan, second-class building loans (subprime), and credit card liabilities. The customers of these "Swaps" hedged against payment losses for which AIG had to stand in.

The customers of the CDS and CDO normally have the right to ask for securities from AIG if the insured debt lose value or the rating worsens of AIG. Moreover, AIG must then write off the CDS and CDO in the own ledger. AIG insured immense credit sums to 2007 without pro-tecting itself adequately. Eight to nine billion dollars hedged Goldman Sachs for example from AIG and therefore covered the risk of its own almost completely.

The New York Times has illustrated what happened that brought AIG in this difficult situation today, with a short sequence of text and charts.

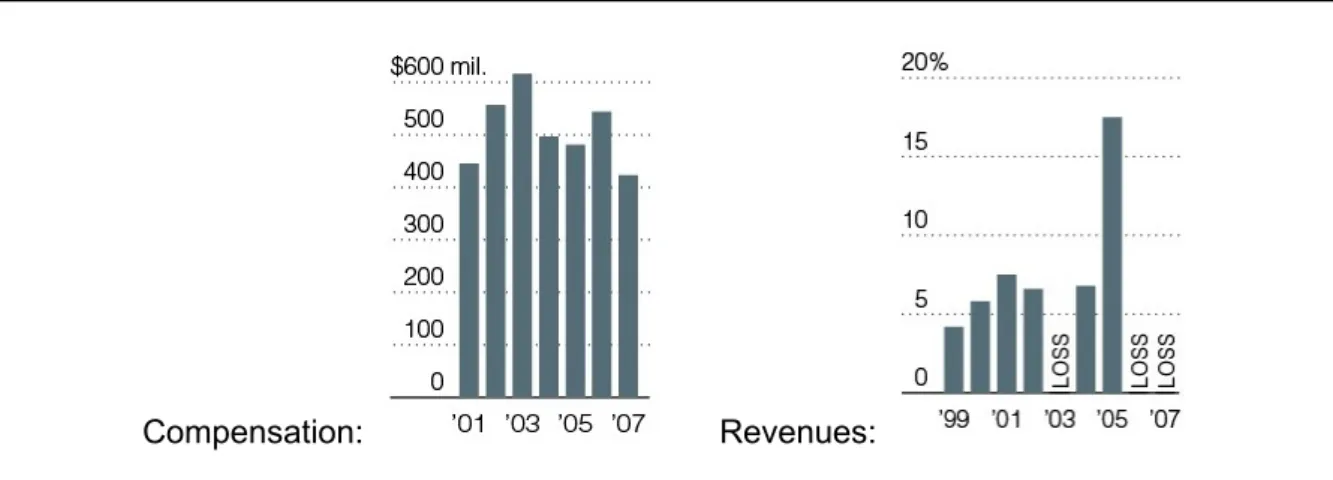

Figure 2-1: AIG Situation: A tiny unit at American International Group... (The New York Times 2008a)

Compensation: Revenues:

Figure 2-2: AIG Situation: ...was well compensated for generating a significant share of rev-enue... (The New York Times 2008a)

The Financial Products unit generated these revenues from selling contracts that protected clients from losses on debt. They insured $513 billion of debt against default using Credit-De-fault Swaps (CDS). $78 billion worth of insured debt was affected by the decline in the U.S. housing market. But as certain debt losses increased, AIG. was forced to enlarge its own fi-nancial reserves and lower the value of some of its own holdings. Ratings agencies punished the company, ultimately forcing it into a downward spiral.

Figure 2-3: AIG Situation: ... from selling contracts that protected clients from losses on debt (The New York Times 2008a)

Figure 2-4: AIG Situation: Punished by rating agencies into a downward spiral (The New York Times 2008)

2.2 Situation at the Stock Exchange

As capital concerns and potential mortgage-related losses continue to bother AIG the share prices drop substantially. During the peaks of the crisis nervous investors continued to sell their shares and hammered AIG stocks. The behavior of rating agencies and customers could also begin to punish the company.

Figure 2-5: AIG (Common Stock) Chart from November 15, 2007 to November 14, 2008 compared to the DowJones Index (BigCharts 2008)

There is a basic pattern: the lower the stock price, the harder it can be for the firm to raise capital. The lower the capital the bigger the concerns, and so on. If this goes on for a while the firm finds itself close to bankruptcy and there is no other possibility than governmental help. This is exactly what happened to AIG.

Table 2-1: AIG (Common Stock) November 14, 2008 (BigCharts 2008)

Price 2.08 Change + 0.02

52 Week High 62.30 52 Week Low 1.25

Currency US Dollar Exchange NYSE

2.3 Income Situation

The consolidated financial results are structured according the main operating segments which are described in chapter 1.2. The following chart shows the development of AIG's fi-nancial results in the past 5 years. In particular the disproportional losses are conspicuous. Whilst the losses of other units (life insurance or asset management) are in the range of their profits in previous years, the financial services segment shows enormous losses since the last quarter of 2007. Concretely financial services accounted a loss of 10'523 million dollars in the third quarter of 2007 (Hamrah & Winans 2007). The financial report of 2007 (AIG 2007) declares a loss of $ 9'515 million, noting, that this "includes an unrealized market valuation loss of $11.5 billion on AIGFP’s super senior credit default swap portfolio".

insurance had a loss of $2,5 billion, life insurances even $15,3 billion and financial services $ 8,2 billion leading to a total net income of $ -37,6 billion for the first 9 month of this year (Hamrah & Ashooh 2008).

3

Related Theory and Research Approach

In this chapter the theory used about principal – agent relationships and the research ap-proach are explained. Theory and apap-proach are valid for all examined relationships de-scribed in chapter 4.

3.1 Related Theory for the Principal – Agent Relationships at the AIG

In the following chapter we will comment on the theory regarding the principal – agent rela-tionship in AIG. A principal-agent model is first developed to formulate the asymmetry of in-formation in knowledge sharing.

A principal – agent relationship has arisen between two or more parties when one, desig-nated as the agent, acts for, on behalf of, or as representative for the other, desigdesig-nated the principal, in a particular domain of decision problems. The agent is empowered to act for the principal because the principal chooses to hire the agent or because there is an implicit con-tract between principal and agent. The Principal agent problem lies in the fact that differ-ences of interest and information between the two parties mean that the agent may not al-ways act in the interests of the principal (Wikipedia 2008a).

The principle – agent problem describes the effect of the agent’s motivation or incentive in executing their task, and how it satisfies the desired objectives of a task. In mortgage lend-ing, the agents of the lenders functioned with their own compensation in mind: They origi-nated mortgages and helped people obtain mortgages, regardless of whether it seemed like they could afford it of if they were even being truthful in their application, as they were paid their fee by origination. They operated, as most everyone does, with their self-interest in mind.

Agency problems can be classified in three big categories (Quelle XXX?): Moral Hazard de-scribes situations, in which the agent uses information not observable by the principal which is than called hidden information or performs actions not observable by the principal hidden action) in order to increase his own utility against the principal’s best interest.

The second category Holdup describes situations in which the agent systematically uses gaps in incomplete contracts, in which not every future state is specified, in his favor after the closing of the contract and after specific investments have been made and sunk costs have been incurred by the principal, the agent reveals his previously hidden intentions openly in-terpreting the fulfillment of his commitments in his favor and forcing the principal into renego-tiations

called the subprime mortgage crisis. The global financial crisis really started to show its ef-fects in the middle of 2008. Around the world stock markets have fallen, large financial insti-tutions have collapsed or been bought out, and governments in even the wealthiest nations have had to come up with rescue packages to bail out their financial systems.

The extent of the problems has been so severe that some of the world’s largest financial in-stitutions have collapsed. Others have been bought out by their competition at low prices and in other cases, the governments of the wealthiest nations in the world have resorted to exten-sive bail-out and rescue packages for the remaining large banks and financial institutions.

While explaining the cause of this crisis seems complicated to even the best of minds, it seems a proximate cause for bankruptcies like AIG was excessive investment in instruments like credit default swaps that insured the debt of other institutions like Goldman and then sent AIG down-under once the housing bubble decided to burst.

To a large extent the troubles that have claimed AIG are not so much a financial crisis as an ownership crisis. It is not markets that have failed, but a peculiar form of ownership that we have taken for granted for decades - stock market-listed companies with dispersed share-holders. So, one form of ownership has caused a crisis, and another hasn't. The reason for this lies in the principal-agent problem.

3.2 Research Approach

The research approach includes the research question, the hypothesis derived from it and the specific aim on which one has worked towards for results.

3.2.1 Research Question

As it is represented chapters above in detail, there were some events at the AIG which indi-cate the existence of hidden information in principal – agent relationships. Hidden information often is the reason that risks are not recognized correctly or assessed wrongly. Or that den information is used of one party for the better of one's own. It also can happen that hid-den information is not analyzed at all since two parties trust themselves very strongly. The examination question therefore is:

Were too high risk aversion, moral hazard and blind confidence responsible for the fi-nancial crisis of AIG and how is it possible to prevent these situations in their princi-pal-agent relationship in the future?

3.2.2 Hypothesis

The risk of hidden information must be shared up equally between principal and agent. One result from the spread of the risk will be lesser moral hazard.

With risk guidelines it can be prevented that in financial transactions a too high risk is taken even if there exists apparently not the slightest risk in the financial transactions.

3.2.3 Specific Aim

With pursuing of the specific aim the hypotheses made has to be proved. In the chapter 4 were four specific principal – agent relationships situations of the AIG explained. On these relationships it is shown that the claims made can be fulfilled. The specific aim therefore is:

4

Principal – Agent Relationships

There are many principal – agent relationships in and to an enterprise like the AIG. During this work approx. 10 different relationships which could have a certain meaning in the current financial crisis were identified by the authors. In opinion of the authors the four principal – agent relationships described in the following chapters are the ones who can most strongly be taken to connection with the crisis.

Each of the examined relationships was processed by one of the four authors.

Table 4-2: Examined Principal – Agent Relationships

Principal Agent Processed by

CDS and CDO Insurance Customer (Banks)

AIG Financial Products (Joseph J. Cassano)

Michael Quade

AIG Holding AIG Financial Products (Joseph J. Cassano)

Stefanie Huthmacher

AIG Financial Products (Joseph J. Cassano)

Rating Agencies Simon Lutz

AIG Financial Products (Joseph J. Cassano)

Consultant (Gary Gorton)

Simon Nikles

4.1 Relationship “CDS and CDO Insurance Customer (Banks) -– AIG Financial Prod-ucts (Joseph J. Cassano)“

As in the chapter 1 described, the AIG is primarily an insurance company. The AIG offers also special insurance products next to common and ordinary insurance products like acci-dent or life assurances. Such a special insurance product is insurance for Credit Default Swaps or CDS and Collateralized Debt Obligations (CDO).

In principle, this one is the relationship between a policyholder and an insurance supplier. But this insurance business is special then it is about gigantic sums of money and there are only a few customers. In this relation the principal are the CDS insurance customer (banks) and the agent is the head of AIG Financial Products division, Joseph J. Cassano.

This perception of the relation coincides with the theory, where the ordering customer is the principal which pays money to the agent, that this one delivers a given performance. The customer pays a premium and expects of the insurance company that this renders the pay-ments promised by contract for them in the event of loss. The main problem in this respect is that it has come just to the event of loss.

AIG started with CDS's sale in 1998 (Mollenkamp et al., 2008) The head of AIG Financial Products, Joseph Cassano, then was convinced based on Gary Gorton models (see chapter 4.4) that it is a goldmine. The credit risks seemed extremely low. AIG became largest sup-plier for CDS. Over years the business was extremely lucrative.

mort-gage market, doubts arose. AIG stopped the protection against complex CDO at the begin-ning of 2006. Though, AIG had already got a security coverage risk of 80 billion dollars there.

Still in 2006 the insurer described the risk of having to pay for losses as highly improbable to the stock exchange supervision SEC. AIG charged its customers the fraction of a penny for every insured dollar of a credit.

Middle of 2007 then the unexpected scenario: The rating agencies started to grade credit se-curitizations down (see also chapter 4.3). With the customer Goldman Sachs which had as-sured with AIG securities in the volume of about 20 billion dollars, the nervousness in-creased. Goldman demanded 1.5 billion dollars with the reference to the depreciation of the attested loans for securities in August 2007. AIG agreed on 450 million dollars. Goldman soon afterwards demanded another three billion. AIG shoved half of the sum after.

The auditor of AIG, Pricewaterhouse Coopers, heard about the Goldman’s claims and as-sessed the CDS newly. AIG reported the first greater depreciation in November 2007: 352 million dollars. AIG then decided to inform investors extensively at the end of 2007. The head of the board in those days, Sullivan, still praised the risk models in his presentation as "very reliable". But banks which had purchased CDS insurances of AIG demanded more and more securities: It was UBS, Barclays, Calyon and the Royal Bank of Scotland by the end of 2007. The Deutsche Bank, CIBC and the Bank of Montreal also shall have required securities which the AIG does not have. This was the reason the AIG asked the FED for help. The AIG simply could not afford the payments they have to made because of the claims of the banks.

As it makes the appearance, the agent (Cassano) has primarily pursued the objective of earning a lot of money. Whether he has put his personal interests for the AIG behind this one is inexplicit. It is well possible that his supervisors either have primarily seen the lucrative business but not the risk. However, it is possible even well that Cassano was himself for the risk conscious. A risk which he, however, did not have to take but the AIG have to.

The objectives of the principals (customers, banks) are obvious: They wanted to insure them-selves against a credit risk. The banks were the risks in their business probably stronger con-scious as Cassano. It cannot this be only risk aversion were alone the reason for the comple-tion of the CDS insurances at the AIG. It rather makes the appearance that the offer of the AIG was simply for the banks so favorable that they simply had to purchase the insurance. For a fraction of a penny per dollar, they were insured against the loss of a lot of capital. We also can assume that the AIG has its product in the appropriate positions at the bank adver-tised.

With the insurances everything went as long as good, as the credit market stably ran and the model of Gorton suited. Only when the first losses were declared, it walked dramatically downhill. The insured banks got increasingly nervous when they noticed that the AIG cannot cover their possible losses. They insisted on the fulfillment of the insurance contracts very quickly.

Hidden information surely also was to blame for the debacle in this respect. The banks (prin-cipals) on the one hand knew not the model after Cassano calculate the premium for the banks and that the AIG cannot make the payments at all under its own steam in worst case. The banks were probably not quite open on the other hand, the risk concerns that the in-sured credits held in themselves. The Rating agencies are probably also not quite guilty of it (see chapter 4.3).

Also hidden action has been the reason on the two sides, of the relationship that the situation deteriorated so quickly. Joe Cassano has failed simply to take care that the insurance risks are spread. Looks like, there was simply not any coverage. The banks probably have not economized carefully by the insurance at all.

4.1.2 Problematic Nature of the Relationships

This problematic nature of this principal – agent relationship fits into the categories of moral hazard and adverse selection (see chapter 3.1).

Moral hazard was especially on the side of Joseph J. Cassano, because he underestimated risk and trusted an incomplete model. He saw only the business as a goldmine. But on the side of the bank there was moral hazard too. Because they were completely insured against loss, they could make relatively venturesome transactions with subprime mortgages. (Dr. Housing Bubble’s Blog, 1008)

fact, that in the event of loss the AIG gets insolvent. The banks have paid for insurance but they had the risk of being left with their claims and losses.

The consequences of this moral hazard are obvious. The banks have been able to assert only the half of their depreciations on the insured credits at the AIG. This has nevertheless sufficed; the AIG would have gone broke without the help of the FED.

However, what one cannot claim for certain that Cassano has not hedged. This is exactly the problems with the adverse selection now. Cassano surely has insured only such credits against losses which were judged by the rating agencies with AAA or more highly. He simply could not know that these ratings were downgraded suddenly and so drastically. For what one can reproach him, that he only has relied on the ratings of the agencies which had judged the credits to be insured best (see chapter 4.3).

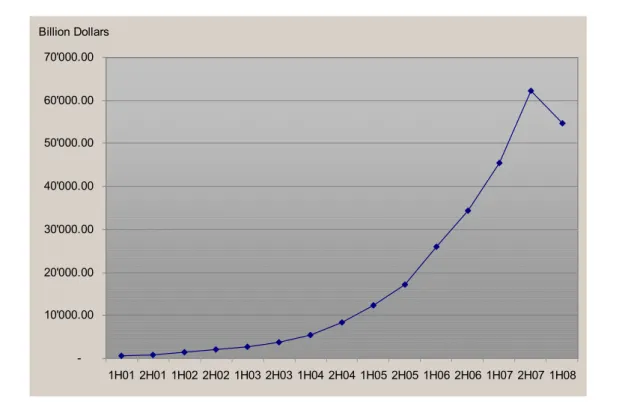

The consequences of this adverse selection are that the market with CDS is after a continu-ous increase since 2001 now for the first time decreasing: From 62'173.20 billion Dollars in the second half of 2007 to 54'611.82 in the first half of 2008 (ISDA 2008).

-10'000.00 20'000.00 30'000.00 40'000.00 50'000.00 60'000.00 70'000.00

1H01 2H01 1H02 2H02 1H03 2H03 1H04 2H04 1H05 2H05 1H06 2H06 1H07 2H07 1H08 Billion Dollars

Figure 4-8: Notional Amounts Outstanding CDS, Semiannual Data 2001 -2008 (ISDA 2008)

4.1.3 Solutions to Improve the Relationship

on the one hand be adjusted. I.e. the premium for the insurances against the loss at credits must get more expensive. The insurance policies must further contain an excess of the banks. For normal insurances for homes this is natural today. In future, the AIG must not take into account only assessments of rating agencies, which are well-intentioned to CDS derivates of banks. For the assessment of an insurance policy all rating agencies must be questioned. The regulations also must be intensified by the state for the coverage of insur-ances: Only insurances which can be covered by securities in the event of loss may be com-pleted.

The times for high boni at AIG Financial Products are for certain past. To furthermore be able to motivate the agent, it needs a new system of the success measuring. The success of the agent may not be measured by the regular profit any more with insurance premiums. Be-cause this provokes a short-term positive way of thinking only, and this is not sustainable. Lastingly, it only can be when long-term success objectives are consulted for the boni.

The principal can for example stipulate insurance contract with the agent in one that this con-tract is screened on the risk constantly. With the change of the risk changes the premium so automatically. The principal does not suffer any loss with CDS for three years {annuals} in consequence due to the automatic assessment by the agent this gets a boni. The agent gets so more critical and judges the CDS more carefully what in the long run for the two parties results in a stable success.

It will be a potential side effect of this measure that the business will be no longer so lucrative with the insurances for CDS. Whether it has not got anyway less lucrative by the financial cri-sis . The times for the gold-diggers are past. Let's wait for the next gold fever!

4.2 Relationship “AIG Holding – AIG Financial Products (Joseph J. Cassano)“

General description of the Relationship

Who is agent and who is principal? Why?

Hypothesis and Sub-Hypothesis

4.2.1 Characteristics of the Relationships

What are the objectives / interests of the agent?

What are the objectives / goals of the principal?

What are current measures in this relationship?

Where are possible hidden information?

What are possible hidden actions?

4.2.2 Problematic Nature of the Relationships

What are the consequences of this adverse selection?

Are there situations of moral hazard / unequal risk?

What are the consequences of this moral hazard?

4.2.3 Solutions to Improve the Relationship

Explicit Contract

Implicit Contracts

Regulations

Each team has to work out regarding the relationship:

How could we align the agent’s interests to the principal’s objectives?

How could we write explicit incentive contracts / regulations / effective measures for this relationship?

Each team has:

to prove why their proposal to align the interests will work!

to propose a concept how to motivate the agent to apply this proposal.

to analyze possible side-effects of their proposal.

4.3 Relationship “AIG Financial Products (Joseph J. Cassano) – Rating Agencies“

General description of the Relationship

Who is agent and who is principal? Why?

Hypothesis and Sub-Hypothesis

4.3.1 Characteristics of the Relationships

What are the objectives / interests of the agent?

What are the objectives / goals of the principal?

What are current measures in this relationship?

Where are possible hidden information?

What are possible hidden actions?

4.3.2 Problematic Nature of the Relationships

Are there cases of adverse selection (Risk Aversion)? Why?

What are the consequences of this adverse selection?

4.3.3 Solutions to Improve the Relationship

Explicit Contract

Implicit Contracts

Regulations

Each team has to work out regarding the relationship:

How could we align the agent’s interests to the principal’s objectives?

How could we write explicit incentive contracts / regulations / effective measures for this relationship?

Each team has:

to prove why their proposal to align the interests will work!

to propose a concept how to motivate the agent to apply this proposal.

to analyze possible side-effects of their proposal.

4.4 Relationship “AIG Financial Products (Joseph J. Cassano) – Consultant (Gary Gorton)”

General description of the Relationship

Who is agent and who is principal? Why?

Hypothesis and Sub-Hypothesis

4.4.1 Characteristics of the Relationships

What are the objectives / interests of the agent?

What are the objectives / goals of the principal?

What are current measures in this relationship?

Where are possible hidden information?

What are possible hidden actions?

4.4.2 Problematic Nature of the Relationships

Are there cases of adverse selection (Risk Aversion)? Why?

What are the consequences of this adverse selection?

Are there situations of moral hazard / unequal risk?

4.4.3 Solutions to Improve the Relationship

Explicit Contract

Implizit Contracts

Regulations

Each team has to work out regarding the relationship:

How could we align the agent’s interests to the principal’s objectives?

How could we write explicit incentive contracts / regulations / effective measures for this relationship?

Each team has:

to prove why their proposal to align the interests will work!

to propose a concept how to motivate the agent to apply this proposal.

List of Literature

Ahrens, Frank, (2008, October 7). Joe Cassano: The Man Who Brought Down AIG?. The Washington Post. Retrieved November 19, 2008 from http://voices.washingtonpost.-com/livecoverage/2008/10/joe_cassano_the_man_who_brough.html

American International Group, Inc., (2007). Annual Report 2007. Retrieved November 23, 2008, from http://www.ezodproxy.com/AIG/2008/AR2007/images/AIG_AR2007.pdf

American International Group, Inc., (2008a, June 15). Corporate Governance Guidelines. Retrieved November 14, 2008, from http://library.corporate-ir.net/library/76/761/76115/ items/300256/Corporate_Governance_Guidelines_061508.pdf

American International Group, Inc., (2008b, October 10). Vision & Values. Retrieved Novem-ber 16, 2008, from http://www.aig.com/vision-and-values_547_103195.html

American International Group, Inc., (2008c, November 4). Information about AIG. Retrieved November 6, 2008, from http://www.aig.com/About-aig_20_19308.html

baz.online, (2008, November 10). AIG: Riesenverlust und neue Hilfe. baz.online. Retrieved November 11, 2008, from http://www.bazonline.ch/wirtschaft/unternehmen-und-kon-junktur/AIG-Riesenverlust-und-neue-Hilfe/story/22372795

BigCharts, (2008, November 14). Advanced Chart about AIG American International Group, Inc (NYSE). Retrieved November 16, 2008 from http://bigcharts.marketwatch.com/ad-vchart/frames/frames.asp?symb=aig&time=8&freq=1

Bøhren, Øyvind (1998) The Agent's Ethics in the Principal-Agent Model [Electronic Version]. Journal of Business Ethics Volume 17 Number 7 p. 745-755

Broadbenta Jane, Dietricha, Michael, Laughlin, Richard (1996). The Development of Princi-pal–Agent, Contracting and Accountability Relationships in the Public Sector: Concep-tual and Cultural Problems [Electronic Version]. Critical Perspectives on Accounting Vol 7 No 3 p. 259 - 284

Dr. Housing Bubble’s Blog, (2008, September 17). AIG Bailout: Federal Reserve Bails AIG out with $85 Billion - World’s Foreclosing Balance Sheet: The Myth of Decoupling, Moral Hazard, and American Dream Disappearing. Retrieved November 19, 2008, from http://www.doctorhousingbubble.com/aig-bailout-federal-reserve-bails-aig-out-with-85- billion-worlds-foreclosing-balance-sheet-the-myth-of-decoupling-moral-hazard-and-american-dream-disappearing/

Drucker, Jesse, (2008). AIG's Tax Dispute With U.S. Has Twist of Irony. The Wall Street Jounal Online. Retrieved November 14, 2008, form http://online.wsj.com/article/ SB122662579362126965.html?mod=MKTW&ru=MKTW

posts huge loss. Reuters. Retrieved November 23, 2008, from http://www.reuters.com/ article/ousiv/idUSTRE4A92FM20081110

Fernando, Nilesh, (2008, September 29). Principal, Agents and Bailouts. India Development Blog. Retrived November 10, 2008, from http://www.indiadevelopmentblog.com/

2008/09/principals-agents-and-bailouts.html

Garson,David (2007, December 28) Key Concepts and Terms of the Principal-Agent Theory. North Carolina State University. Retrieved November 10, 2008 from http://faculty.chas-s.ncsu.edu/garson/PA765/agent.htm

Hamrah, Charlen, Ashooh, Nicholas, (2008). AIG Reports Third Quarter 2008 Results. Amer-ican International Group, Inc.. Retrieved November 23, 2008, from http://media.corpo-rate-ir.net/media_files/irol/76/76115/releases/AIG%203Q08%20Press%20Release.pdf

Hamrah, Charlen, Winans, Chris, (2007). AIG Reports Full Year and Fourth Quarter 2007 Results. American International Group, Inc.. Retrieved November 23, 2008, from http:// media.corporate-ir.net/media_files/irol/76/76115/releases/Q407_Press_Release_fi-nal.pdf

Haubrich, Joseph, (1994). Risk aversion, performance pay, and the principal-agent problem [Electronic version]. Journal of Political Economy 102, 258-276.

Holmstrom, Bengt (1979). Moral hazard and observability [Electronic Version]. The Bell Jour-nal of Economics Vol. 10 No. 1 p. 74-91

International Swaps and Derivatives Association, Inc., (2008). ISDA Market Survey. Retrvied November 28, 2008 from http://www.isda.org/statistics/pdf/ISDA-Market-Survey-histori-cal-data.pdf

Mollenkamp, Carrick, Ng Serena, Plevin Liam, Smith, Randall, (2008, November 3) "Behind AIG's Fall, Risk Models Failed to Pass Real-World Test" [Electronic Version]. The Wall Street Journal, p. 1.

Morgenson, Gretchen, (2008, September 27). The Reckoning: Behind Insurer’s Crisis, Blind Eye to a Web of Risk. The New York Times. Retrieved November 14, 2008, from http:// www.nytimes.com/2008/09/28/business/28melt.html?_r=1&oref=slogin

Morkötter, Stefan, Westerfeld, Simone, (2008) Asset Securitisation: Die Geschäftsmodelle von Ratingagenturen im Spannungsfeld einer Principal-Agent-Betrachtung" [Electronic Version]. Zeitschrift für das gesamte Kreditwesen 9/2008, p. 393-396

Munro , Lauchlan T. (1999 September) A Principal-Agent Analysis of the Family: Implications for the Welfare State. Institute for Development Policy and Management, University of Manchester. Retrieved November 10, 2008, from http://www.sed.manchester.ac.uk/ idpm/research/publications/wp/dp/documents/dp_wp58.pdf

Reuters (2008a, September 15). AIG bittet Fed um kurzfristige Finanzhilfe. Reuters. Re-trieved November 23, 2008, from

http://de.reuters.com/article/topNews/id-DEMIG52008220080915

Reuters (2008b, October 9). New Yorker Fed stellt für AIG knapp 38 Mrd Dollar bereit. Reuters. Retrieved November 23, 2008, from http://de.reuters.com/article/topNews/id-DEBEE49800S20081009

Sappington, David E M, (1991). Incentives in Principal-Agent Relationships [Electronic ver-sion]. Journal of Economic Perspectives, American Economic Association, vol. 5(2), p. 45-66

SF - ECO - 24.11.2008 - Rating Agenturen in der Kritik

Tharp, Paul, (2008, February 12). AIG IS BURNED BY $5.9B CDO MESS. New York Post. Retrieved November 19, 2008, from http://www.nypost.com/seven/02122008/business/ aig_is_burned_by_5_9b_cdo_mess_97272.htm

The Accidental Hunt Brothers, (2008, November 10). Gary Gorton, AIG and Commodities, Retrieved November 19, 2008, from http://accidentalhuntbrothers.com/?p=110

The New York Times, (2008a). An Insurance Giant, Brought Down, Retrieved November 14, 2008, from http://www.nytimes.com/imagepages/2008/09/27/business/

20080928_MELT_GRAPHIC.html

The New York Times, (2008b). Maurice R. Greenberg - Hank Greenberg, Retrieved Novem-ber 28, 2008, from http://topics.nytimes.com/top/reference/timestopics/people/g/mau-rice_r_greenberg/index.html?s=oldest&&&

The Wall Street Journal, (2008). The Making of a Mortage CDO. Retrieved November 19, 2008, from http://online.wsj.com/public/resources/documents/info-flash07.html? project=normaSubprime0712&h=530&w=980&hasAd=1&settings=normaSub-prime0712

Walsh, Mary Williams (2008, October 30). AIG used billions from Fed but hasn't said for what. Internatinal Herad Tribune. Retrived November 9, 2008 from http://www.iht.com/ articles/2008/10/30/business/30aig.php?page=3

Wikipedia. (2008a, October 31). Principal-agent problem. Retrieved November 6, 2008, from http://en.wikipedia.org/wiki/Principal-agent_problem

Wikipedia, (2008b, November 5). American International Group. Retrieved November 6, 2008, from http://en.wikipedia.org/wiki/AIG