Roland Berger Strategy Consultants – Automotive Competence Center & Forschungsgesellschaft Kraftfahrwesen mbH Aachen

E-mobility index for Q1 2013

E-mobility index for Q1 2013

Key takeaways of the E-mobility Index Q1 2013

1. Overall, production forecasts for EVs and PHEVs are in decline, posing a serious threat to national targets to raise the share of xEVs in vehicle fleets. In the long term, South Korea, Germany and France will increase their share in global xEV production. 2. South Korean, German and French OEMs are catering to customer preferences more

than their competitors in positioning their vehicles. Their products offer better value for money than those of US and Japanese competitors.

3. Government support for e-mobility is waning. Overall, subsidies are growing more slowly than GDP. None of the programs that ended in 2012 were renewed. China is a special case in this regard

Summary comparison of the competitive positions of the world's seven leading automotive nations

The Q1 2013 index shows that the seven leading automotive nations have seen their competitive positions shift since the last survey, in some cases significantly (Figures 1 and 2).

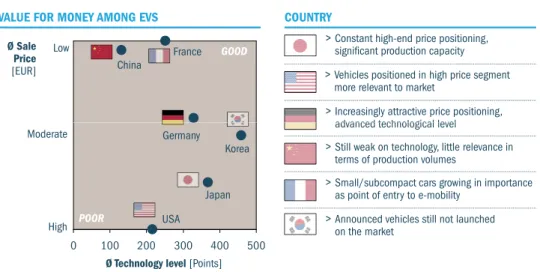

South Korea is still out in front in terms of technology. However, the considerable lead it used to enjoy over its closest rivals France and Germany has been eroded, mainly because subsidy programs have not been renewed. While South Korea and Japan still have the most advanced vehicle technology, Germany has improved its value for money: German OEMs have maintained constant technological performance while reducing price levels overall. The reverse is true in the US, where dwindling overall sales and a shift toward more expensive models are resulting in lower value for money (Figure 3). With the exception of China, government support for e-mobility is declining in all the countries surveyed. None of the subsidy programs that ended at the end of 2012 were renewed. Moreover, the support that exists is inversely proportional to the increase in these countries' economic performance, meaning that the subsidy situation does not benefit from increases in economic output (Figure 4).

Japan continues to lead in terms of industry. However, the sharp downward correction of vehicle production forecasts and scaled-back cell production means that it has lost a lot of ground to South Korea. In terms of the value created in manufacturing, South Korea is the only country that is advancing. This is attributable to more optimistic forecasts for domestic vehicle production and the country's substantially improved share in global cell production.

Overall, worldwide sales forecasts – and hence the related production forecasts for EVs and PHEVs – are more conservative than in the preceding survey period. Among the seven automotive nations tracked by the index, the share of production in some segments is shifting in favor of individual countries. Since the previous survey, forecasts for vehicle production in Germany, France and South Korea have experienced positive development but remain at comparably low levels. Forecasts for vehicle sales in China, the US and Japan have been corrected downward. Growth in France is attributable above all to significantly higher sales forecasts for the Renault Twizy (Figure 5).

In the future, cell production will be concentrated even more heavily in Japan and South Korea. There are two reasons for this: One is a trend toward consolidation, driven by the exit of individual market players and the termination of cooperative ventures that have shaped the market up to now. The other is shaped by battery manufacturers' own more pessimistic view of the market as a whole, as a result of which plans to build cell production facilities outside Japan and South Korea themselves have been put on ice. Current estimates indicate that France will have no domestic cell production in 2015 (Figure 6).

In the period from Q1 2012 through Q4 2012, EVs and PHEVs both saw positive development in their share of the new vehicle sales market relative to the previous survey period (Q1 2011 through Q4 2011). In all the markets surveyed, they nevertheless account for only a tiny fraction of the market. While China and France have already ramped up existing programs to boost sales, South Korea only recently followed suit. In Japan, however, many sales development programs have already expired and – despite their positive effect on EVs' market share – have not been extended (Figure 7).

Detailed analysis

Negative overall development in the market for EVs and PHEVs, despite mature technologies and optimized cost structures, suggests that the right conditions are not in place. Yet politicians still hold fast to the targets already set to ramp up the market for this class of vehicles – while conceding that realization will be delayed in some cases. Three major challenges currently stand in the way of compliance with these targets and of political demands for the market to be ramped up:

1. xEVs unattractive to OEMs as a financial proposition – Conservative planning for volume roll-outs

OEMs realize lower margins on the sale of electric vehicles than on vehicles with conventional powertrains. In terms of the total cost of ownership (TCO), partially or fully electrified powertrains are still at a significant cost disadvantage over the entire lifecycle compared to conventional powertrains. OEMs experience a shortfall in profit margins if they sell a plug-in hybrid vehicle (PHEV) rather than a vehicle with a conventional powertrain. The customer benefits from lower energy costs due to lower fuel consumption, but the OEM is not fully recompensed for the extra cost it incurs (Figure 8). As long as emissions standards and CO2 targets can still be met with optimized internal combustion

engines, there is thus no special incentive – marketing reasons aside – for OEMs to place more than the politically required minimum number of xEVs on the market (to comply with market access regulations, for example). Moreover, if governments such as the US administration succeed in stabilizing the oil price overall by expanding nationwide fracking projects, this would put alternative propulsion systems at an even greater cost disadvantage.

2. Battery safety a key area of technology – Innovative concepts needed

Apart from attractive cost considerations, customers' acceptance of EVs also hinges to a large extent on the safety of the vehicles on offer. In this context, the lithium-ion energy storage systems used in most of the EVs and PHEVs currently on the market are safety-critical components. Deformation of or damage to these systems can lead to safety-critical behavior (a fire or an explosion, for instance). Verification of this problem in mechanical tests at cell level, in real accidents (in China and the US) and in crash tests has had a significant negative impact on public perception. At the time of writing, problems with lithium-ion systems in Boeing's new 787 ("Dreamliner") aircraft were widening this perception to also include normal operating situations involving neither crashes nor deformation. To ensure functional operating safety, the legislator has created stable conditions by defining clear rules for the approval of EVs (e.g. ECE-R 100). For their part, OEMs are using rigid safety structures to provide passive protection against mechanical stresses on the battery systems. These measures are intended to avoid critical impacts as a result of accidents in the current generation of vehicles. However, these structures increase the weight of the vehicles and thus reduce their range, which is another important factor for customers. Innovative safety concepts for these battery systems are thus a key area in the development of EVs that are both safer and more efficient.

SPOTLIGHT:

Example of an innovative battery safety concept

To improve crash safety while also avoiding significantly heavier weights, partners such as Audi AG and the Institute of Automotive Engineering at RWTH Aachen University have jointly developed an innovative battery protection concept as part of the "e performance" project backed by the German Federal Ministry of Education and Research. The concept is based on the idea of a deformable battery system in which, in the event of an accident, individual trapezoidal macrocells diffuse the force of the crash in different directions before the energy is finally absorbed by deformation elements (Figure 9).

3. Infrastructure is fast becoming a global hurdle – joint efforts essential The purchasing potential represented by early adopters is right now being tapped by the current array of vehicle offerings for both private customers and institutional fleets. Once replacement buyer potential has been exhausted, just how suitable e-mobility is for unrestricted everyday use will come more sharply into focus. The public perception is that the problem of electric vehicles' limited range has not yet been adequately addressed. Since optimized storage technologies will not be available until after 2020 (see E-mobility Index Q2 2012), this problem cannot be resolved on the basis of existing technology for pure-play battery electric vehicles. Only one thing can provide the stimulus for the full integration of BEVs in existing public and private mobility offerings that is needed in the medium term, and that is the availability of a comprehensive charging infrastructure that also features fast-charging options. An indication of the required scope of this supply network is provided by the level of infrastructure currently available in countries (such as Japan) that already have EV fleets worthy of the name. In these countries, the average ratio is around 20 vehicles to one public charging station (Figure 10).

In this context, Germany, France, China and South Korea have already spelled out concrete targets for the kind of charging infrastructures they envisage in the future. However, in view of considerable uncertainties surrounding planning, high required upfront investments and long payback periods, there are currently no business models that would make it attractive for private investors to enter this market. Nor will the lower hardware costs that are expected in the future ease this situation in the long run. Accordingly, only a lasting public-sector commitment that is understood to be an issue of national importance can elevate battery electric vehicles from a niche functions and establish their role in national vehicle fleets in the long term.

Methodology

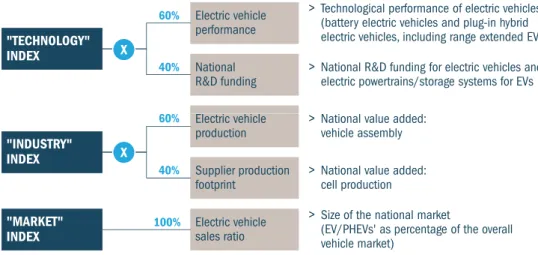

The relative competitive position of individual automotive nations is compared to that of the others on the basis of three key indicators:

1. Technology: The current status of technological development in vehicles made

by indigenous OEMs and the support for vehicle development provided by national subsidy programs

2. Industry: The regional value added created in the automotive industry

by national vehicle, system and component production

3. Market: The size of the national market for electric vehicles based

on current customer demand

Roland Berger Strategy Consultants and fka weight the individual indicators and combine them to form the E-mobility Index (Figure 11).

The E-mobility Index makes it possible to compare the competitive positions of the world's seven leading automotive nations (Germany, France, Italy, the US, Japan, China and South Korea), juxtaposing their individual automotive markets on the basis of uniform global standards. The index thus reveals the extent to which individual nations are able to participate in the market that e-mobility is creating. The criteria applied are assessed as follows:

1. Technology:

– Technological performance and value for money of electric vehicles that are currently available on the market or are soon to be launched

– National e-mobility R&D programs through 2015. Only research grants and subsidies are taken into account (but not credit programs for manufacturing, budgets for purchase incentives, etc.)

2. Industry:

– Cumulative national vehicle production (passenger cars, light commercial vehicles) for the period 2012-2015, taking account of BEVs and PHEVs

– Cumulative national battery cell production (kWh) through 2015 3. Market:

– Electric vehicles' current share of the overall vehicle market (over a twelve-month period)

Figures

Figure 2: Japan leads the index in industry and market; Korea is top in technology

INDUSTRY TECHNOLOGY MARKET

E-mobility index – Ranking by indicator

1.3 1.9 3.1 2.8 3.3 3.5 3.3 3.6 3.7 0.8 0.9 1.7 2.7 0.4 1.1

Figure 1: The competitive positions of the seven leading automotive nations have in some cases shifted significantly in the Q1 2013 index

INDUSTRY 5 4 3 Japan E-mobility index – Q1 2013 TECHNOLOGY 2 1 0 1 2 3 4 5 Korea Germany France China Italy USA 0

Source: fka; Roland Berger

Figure 4: With the exception of China, government funding for e-mobility is declining in all the countries surveyed

[EUR m]1)

COUNTRY

7,684

National R&D funding for e-mobility [EUR m]/[% of GDP]

1,984 2,093 [% of GDP]2) 0.147 0.077 0.019

1) Not including subsidy programs that expired at the end of 2012 2) Subsidies expressed as a share of current GDP

Source: fka; Roland Berger

925 143 220 180 0.046 0.003 0.027 0.011

Figure 3: South Korea and Japan still offer the most advanced technology – Value for money has improved in Germany

VALUE FOR MONEY AMONG EVS

>Constant high-end price positioning, significant production capacity Ø Sale Price [EUR] Low China France GOOD COUNTRY

>Vehicles positioned in high price segment more relevant to market

>Increasingly attractive price positioning, advanced technological level Value for money among market-ready BEVs and PHEVs

0 100 200 300 400 500

Moderate

High

Ø Technology level[Points] Korea

Japan USA Germany

POOR

advanced technological level

>Still weak on technology, little relevance in terms of production volumes

>Small/subcompact cars growing in importance as point of entry to e-mobility

>Announced vehicles still not launched on the market

Note: Italian OEMs have no market-ready, mass-produced EV/PHEV models Source: fka; Roland Berger

Figure 6: In the future, cell production will be concentrated even more heavily in Japan and South Korea

PROJECTED GLOBAL MARKET SHARE, 20151)

10% 22% 25% ∑USD2.8 bn 2) 2 974 4,236 7,124

DOMESTIC CELL PRODUCTION, 2012-2015 [MWh]

>Primarily LG Chem and Samsung

>Former SB-Limotive units now part of Samsung

>Primarily A123 and Japanese manufacturers with

>Leading cell producer

>Primarily Panasonic, AESC, Toshiba GS Yuasa

Key cell manufacturers and production, by country, through 2015

10%

201 1,267

2,974 local production (AESC)y p

>Primarily "local for local"

>A123 also included after sale of US footprint

>Primarily LiTec

>No production footprint following dissolution of

Johnson Controls-Saft

>No significant cell production

0 0 9% 8% 6% 4%

Figure 5: Production forecasts for EVs/PHEVs are more pessimistic overall – Market shares are shifting in favor of individual countries

DOMESTIC PRODUCTION EVs/PHEVs['000 units]

COUNTRY

267 283

Projected production of EVs and PHEVs through 2015

TOP THREE MODELS IN EACH COUNTRY Toyota Prius PHEV, Nissan Leaf EV, Mitsubishi i-MiEV

Chevrolet Volt (PHEV), Nissan Leaf EV, Fisker Karma

122 182

205

47

BMW i3, VW Golf PHEV, VW e-up! Renault Twizy EV, Renault ZOE Z.E., Smart ForTwo EV

Roewe 550 EV, BYD F3 PHEV, Chang'an Benben Mini EV Hyundai BlueWill PHEV, Kia Ray EV, Chevrolet Spark EV

Note: No significant EV/PHEV production is expected in Italy Source: fka; Roland Berger

10.2 45.5 16.9 28.6 8.0 11.2 35.3

Figure 8: From a TCO1)perspective, OEMs cannot fully realize the margins they need to sell EV/PHEVs profitably

CONVENTIONAL POWERTRAIN (gasoline) xEV POWERTRAIN (PHEV)

TCO comparison for vehicles with conventional and alternative powertrains [EUR '000]

10.0 0.2 8.0 1.6 5.1 4.4 9.4 2.4 8.0 Retail cost and taxes Vehicle retail price ICE power-train cost2) OEM margin ICE optimi-zation cost2)

TCO1) Fuel and

electricity cost Vehicle base cost2) Retail cost and taxes Vehicle retail price Fuel

cost marginOEM power-EV

train cost2)3) ICE power-train cost2) Vehicle base cost2)

1)Total cost of ownership [EUR] 2) Parts and assembly 3) Including the battery, battery management system and engine

MARGIN SHORTFALL

Source: fka; Roland Berger

Figure 7: China, South Korea and France have increased purchasing incentives – Japan has cut them sharply in spite of positive effects to date

0.4 5,183/0.36% USA 7,000/0.33% France 8,652/0.36% Japan (Q2/2012) % of BEVs/PHEVs

(sales figures for Q1 2012-Q4 2012)

0.5 0.3 1,720/0.37%Japan 0.0 10,000 9,000 8,000 7,000 6,000 5,000 4,000 3,000 2,000 1,000 0 2,725/0.04% Korea 0/0.11% Germany 3,500/0.03% Italy 8,236/0.03% China

INCENTIVES TO BUY[EUR]1)

1) At the national level. Additional incentives are available at regional level in some cases. Tax exemptions are not included 0.2

0.1

Figure 10: Different countries envisage different levels of coverage in terms of the ratio of vehicles to the charging infrastructure

EV FLEET AND CHARGING STATION INFRASTRUCTURE

Charging stations

EVS PER CHARGING STATION

12,000 16,000 2 1 1.6 1.4 0.3 EV fleet 5,000 10,000 15,000 20,000 25,000 30,000 0 0 4,000 8,000 6.8 3.4 2.1 19.5 Figure 9: Innovative battery safety concepts are a key part of developing safer

and more efficient EVs

BEFORE CRASH IMPACT Deformation elements Macrocell AFTER CRASH IMPACT Force = Displacement Image source:

Figure 11: The e-mobility index compares automotive nations on the basis of three parameters

Electromobility index – Three parameters: technology, manufacturing, market

"TECHNOLOGY" INDEX Electric vehicle performance National R&D funding

> Technological performance of electric vehicles (battery electric vehicles and plug-in hybrid electric vehicles, including range extended EVs)

> National R&D funding for electric vehicles and electric powertrains/storage systems for EVs

X 60% 40% "INDUSTRY" INDEX "MARKET" INDEX Electric vehicle production Electric vehicle sales ratio Supplier production footprint

> National value added: vehicle assembly

> National value added: cell production

> Size of the national market

(EV/PHEVs' as percentage of the overall vehicle market)

X

60%

40%

100%

Contacts

Dr. Wolfgang Bernhart

Partner

Roland Berger Strategy Consultants, Stuttgart

Loeffelstrasse 46, 70597 Stuttgart Phone: +49 711 3275-7421 Fax: +49 711 1377-7421 E-mail: [email protected] Dr. Thomas Schlick Partner

Roland Berger Strategy Consultants, Frankfurt

Bockenheimer Landstraße 2-8, 60306 Frankfurt

Phone: +49 69 29924-6202

Fax: +49 69 29924-6102

E-mail: [email protected]

Dipl.-Kfm. Ingo Olschewski Geschäftsbereichsleiter

Forschungsgesellschaft Kraftfahrwesen mbH Aachen Strategie und Beratung, Steinbachstraße 7, 52074 Aachen Phone: +49 241 8861 160

Fax: +49 241 80 22147 E-mail: [email protected]

Dipl.-Ing. Markus Thoennes Senior Engineer

Forschungsgesellschaft Kraftfahrwesen mbH Aachen Strategie und Beratung, Steinbachstraße 7, 52074 Aachen Phone: +49 241 80 25586

Fax: +49 241 80 22147 E-mail: [email protected]