Master Thesis Public Administration

Outward Foreign Direct Investment from

Developing Countries

A study on the economic and institutional factors that can have an influence on the occurrence of outward FDI from India and Brazil

Bruna Consiglio de Souza

Student ID: s1514253

E-mail: [email protected]

Supervisor: Dr. N. A.J. van der Zwan

Second Reader: Dr. S.N. Giest

MSc Public Administration

Governing Markets: Market Competition and Regulation

1

Abstract

2

Contents

1. Introduction ... 4

2. Literature review ... 7

2.1 Brief historical overview of OFDI from developing countries ... 7

2.2 – The pros and cons of OFDI ... 9

2.3 – Economic development and OFDI... 10

2.4 –National institutions and policies as determinants of OFDI ... 14

3. The purpose of this research and its methodology ... 19

3.1- Methodology ... 19

3.1.1 – The choice of Brazil and India ... 20

3.1.2 – Data selection and hypotheses ... 22

3.1.3 – Considerations about replicability ... 28

4. Case study: India ... 29

4.1 – Introduction: Indian economy and OFDI ... 29

4.2 – Economic factors that could have an influence Indian OFDI ... 31

4.3 – Institutional factors that could influence Indian OFDI ... 34

4.3.1 – Background information on the Indian political system ... 34

4.3.2 – Indian policies easing capital controls for OFDI ... 35

4.3.3 - Indian policy-makers and Indian outward FDI... 39

4.3.4 - The provision of financial incentives to Indian firms investing abroad through low-interest rates loans ... 41

4.3.5 - The international dimension: Policy Prescriptions by the IMF and/or World Bank . 42 4.3.6 – Final reflections on institutional factors and Indian OFDI ... 43

5. Case study: Brazil ... 44

5.1 – Introduction: Brazilian economy and OFDI ... 44

5.2 – Economic factors that could influence Brazilian OFDI ... 46

5.3 – Institutional factors that could influence Brazilian OFDI... 49

5.3.1 – Background information on the Brazilian political system ... 49

5.3.2 – Brazilian policies easing capital controls for OFDI ... 50

3 5.3.4 - The provision of financial incentives to Brazilian firms investing abroad through

low-interest rates loans ... 56

5.3.5 - The international dimension: Policy Prescriptions by the IMF and/or World Bank . 58 5.3.6 – Final reflections on institutional factors and Brazilian OFDI ... 59

6. Analysis and discussion ... 61

6.1- Hypotheses based on the Investment Development Path (IDP) ... 61

6.2- Hypotheses based on institutional factors ... 63

7. Conclusion and suggestions for further research ... 68

Bibliography ... 71

4

1.

Introduction

Outward foreign direct investment1 (OFDI) is an economic activity that has been predominantly

practiced by developed countries. In other words, OFDI has consisted mainly of firms from developed countries investing overseas. Interestingly, however, in the past decades, an increasing number of firms from developing countries have engaged in OFDI activities as well, constituting a relatively new phenomenon (Saad et al, 2014; Luo et al, 2010). An analysis on the evolution of OFDI from developing countries indicates that up until the 1980s, outflows of FDI from developing countries took place moderately, without substantial increases. From the 1980s onwards, however, it is possible to see that more substantial increases began to take place. For example, in 1980 outflows of FDI from developing countries totaled approximately USD 3 billion, and one decade later these outflows were significantly higher, totaling USD 13 billion in 1990. Following this trend of substantial increases, more recently, in 2014, this number has risen to USD 468 billion (UNCTAD, 2014).

This phenomenon has gained the attention of many scholars, who want to understand which factors could possibly explain this increase in OFDI from developing countries. As the next chapter will explain, most authors have conducted analyses on the occurrence of OFDI as a result of economic development. This type of analysis is framed by the Investment Development Path hypothesis (hereinafter IDP hypothesis), which suggests that OFDI occurs as a natural consequence of economic growth in a country (Liu et al, 2005). Over the years, however, especially from the mid-2000s onwards, a small group of scholars began to criticize the theoretical approach offered by the IDP hypothesis. According to these scholars (e.g. Stoian, 2013; Khoon & Wong, 2011), the IDP hypothesis cannot fully explain the occurrence of OFDI in developing countries because it neglects other factors that could play important roles influencing this activity. These authors were referring

1The definition of OFDI being used in this research is as follows: “OFDI is a business strategy where a domestic firm expands

5 to governmental factors. That is, they believed that certain public institutions and policies could also have an effect on the occurrence of this economic activity in developing countries. Based on that, many of these authors have combined economic and institutional factors to find out whether or not they could possibly have a relation with OFDI (e.g. Stoian, 2013; Khoon & Wong, 2011). The methodology used by these scholars was to conduct regression analyses to investigate whether or not the variation of numerical variables indicating economic and institutional factors could have a relation with the variation of OFDI for the countries analyzed.

The idea of integrating both economic and institutional factors in a study on the possible determinants of OFDI seems to be plausible, and this study will also follow this line of research. Nevertheless, in this research I argue that this type of study should be carried out in a different way. To find out whether or not certain institutional factors could have an effect on OFDI, I suggest that a research should not take place through linear regressions since such approach only attempts at finding out whether or not a possible relation between variables exists. More importantly, in my view, a study should also attempt to find out how that relation could have taken place, and who the actors enhancing this relation are. Thus, because I want to present a more informative analysis on the factors that could contribute to the occurrence of OFDI, I will combine quantitative and qualitative data to test both theories (i.e. economic and institutional). In this research I will focus on two developing countries, namely Brazil and India, with the goal of answering the following question: To what extent are economic and governmental institutional factors associated with the occurrence of OFDI for Brazil and India?

6 developing countries. Or, on the contrary, this research can also be informative to policy-makers in case it shows that in Brazil and India OFDI seems to be associated mainly with economic development, and not so much with institutional factors. In sum, policy-makers interested in enhancing OFDI in their countries can learn more about the governance of this activity based on the Indian and Brazilian experience.

7

2.

Literature review

This chapter will present an overview of previous academic studies in the field of OFDI in order to provide some background information about this economic activity in developing countries. For the purpose of this research, this chapter will be divided as follows: the first sub-section will offer a brief historical overview of OFDI in developing countries, and the second one will present some of the pros and cons of OFDI for the economy of the investing country; the third and fourth sub-sections will then follow by elaborating more on the economic and institutional factors that, according to the literature, can have an influence on OFDI. These last two sub-sections will be used here as a theoretical framework for this research.

2.1 Brief historical overview of OFDI from developing countries

By examining the literature on the evolution of OFDI from developing countries, it is possible to see that many authors divide this evolution in two waves to explain how this process has taken place (Narula & Nguyen, 2011; Saad et al. 2014). Based on the observations of these authors, the first wave emerged in the 1980s. During this wave, firms from developing countries sought to expand their operations across borders mainly with the purpose of acquiring more natural assets (Narula & Nguyen, 2011). Due to their lack of international experience, however, these firms did not expand their activities into different parts of the globe. Instead, they concentrated their investments in neighboring countries, which in most cases were at an earlier or similar stage of development. In other words, this means that firms from developing countries were mainly investing in other developing countries during this first wave.

8 in 1989 (UNCTAD, 2014). This first wave lasted until the late 1980s, when a shift in OFDI practices began to occur.

By the early 1990s, the second wave of OFDI was taking place. During this wave, an increasing number of firms from developing countries had gained more international experience and began to extend their investments substantially into developed economies. These firms were mainly interested in acquiring natural resources, expanding their markets, exploiting new assets, and augmenting their own assets abroad. Interestingly, many of the economies that were active during the first wave of OFDI did not play a prominent role during this second wave. In fact, the economies that led this second wave were mainly the newly industrialized Asian economies, such as Taiwan, Korea, Hong Kong and Singapore, which were indicating the increased competitiveness of their firms and dynamism of their economies (Narula & Nguyen, 2011; Saad et al. 2014; Dunning, 1998). As a consequence of their expansions, these newly industrialized Asian economies had their share of all developing country OFDI stock increased from 21% in the 1980s to 66% by 1993 (Narula & Nguyen, 2011).

By analyzing these waves of OFDI, one question that arises is: what explains the occurrence of these two waves? One hypothesis is that the waves of OFDI could be a reflection of the different development paths that developing countries have followed. For example, the substantial increase in OFDI experienced by newly industrialized Asian economies could be a reflection of the development model that these economies have adopted decades earlier. For instance, as Haggard (1990 p. 25) explains in his book entitled Pathways from the Periphery, since the 1970s a number of Asian economies (led mainly by Korea, Taiwan, Singapore and Hong Kong) have adopted a model of development based mainly on export-led growth. Governments in many of these economies have promoted this growth by, for instance, providing financial and fiscal support to industries focusing on exports, targeting industrial policies, and liberalizing trade and investment. Possibly, by expanding their export activities, these economies have become more internationalized and open to foreign markets, and this could have led to the significant increase in OFDI that these economies experienced during the first and mainly during the second waves of OFDI.

9 it focused on enhancing self-sufficiency in Latin American economies so they would be less dependent on imports (Haggard, 1990, p. 25). With that been said, it could be possible to suggest here that this economic model that has been adopted in Latin American economies restricted their economic transactions mainly to the home country and to the Latin American region, and this could possibly explain why these countries have not extended their OFDI activities to the same extend as their Asian counterparts during the second wave in the 1990s.

Currently, however, from the 2000s onwards, it is possible to see that an increasing number of developing countries from different regions (e.g. Asia, Latin America, and Eastern Europe) have in general increased their OFDI activities substantially, with investments in both developing and developed economies. As a result of this growth, between 2009 and 2010 outflows of FDI from developing economies increased by 20.9 percent (from USD 270.7 billion in 2009 to USD 327.6 billion in 2010), indicating the significant increase in competitiveness and internationalization of these economies (Saad et al. 2013, p. 238).

2.2 – The pros and cons of OFDI

The aforementioned growth in OFDI indicates that developing countries are becoming increasingly attracted to the possible benefits that they can obtain by extending the operations of their firms abroad. The literature on OFDI points out several benefits that can be associated with this economic activity. For instance, authors such as Saad et al. (2013) and Sauvant (2005) argue that firms investing overseas will benefit by entering new markets as they will gain new customers in different states. Moreover, by operating in other states, these firms will have more access to foreign technology, and they will also benefit from being able to import intermediate products at lower prices in case the prices in their home countries are higher than those in host countries (Saad et al. 2013).

10 workers so they can become highly skilled to meet the growing demand for skilled labor in the labor market (Berman et al. 1994).

There are, however, other aspects of OFDI that are not as positive for the home country as the ones mentioned above. For instance, OFDI is often associated with skills transfer and job losses in the home country (Saad et al. 2013, p.239). The debate about these negative consequences of OFDI, however, leads to mixed conclusions. For instance, Saad et al (2013) argue that in certain instances OFDI could also create jobs in the home country. According to them, if foreign production takes place complementing domestic production, the foreign subsidiary will then use inputs from the home country to produce outputs. If, in this case, the relocation of production processes take place as to use resources in a more efficient way, marginal costs of production could possibly become lower. As marginal costs of production decrease, outputs tend to increase. As a result, the creation of more outputs would require the creation of more inputs, consequently leading to job creation in the home country (Saad et al. 2013, p. 239). It is important to stress, however, that this case described by Saad et al. illustrates a scenario in which the entire production process takes place in an efficient manner, and foreign production complements domestic production. In other cases (e.g. when foreign production does not complement home production), OFDI might not occur as the authors describe, and job losses in the home country can indeed become an issue to be considered. According to Saad et al. (2013, p.239), however, most scholars seem to agree that OFDI end up strengthening the remaining economic activities at home. This claim is mainly based on arguments that OFDI can lead to more efficient production processes, lower prices for consumers, more competitive firms, and more specialized division of labor (Saad et al. 2013; Sauvant, 2005). As a conclusion, based on the analysis of the literature in this field, it is possible to argue here that OFDI can lead to many gains for the economy of a country; however, less positive consequences such as job losses in the home country can also occur and should not be neglected as a possible risk that OFDI entails.

2.3 – Economic development and OFDI

11 rationale used by these scholars is that as the economy of a country develops, that country will develop as well (e.g. that country might experience more technological innovations as a result of increased investments on technology that were enabled due to economic growth). The firms from that country will also benefit from such developments if they incorporate them into their operations. As a consequence of such incorporations, these firms will become more competitive (i.e. more able to exploit their newly acquired advantages against their competitors). Thus, because these firms are more competitive, they will be more likely to expand their operations abroad so they can reach new markets, acquire new resources, and consequently increase their sources of profit. Thus, in sum, according to this rationale the levels of economic development in a country can have an effect on that country’s levels of OFDI (Dunning et al, 2001).

The classic work that has influenced a substantial number of researches in this field in the past decades is the study by Dunning (1981), entitled Explaining the International Direct Investment Position of Countries: Towards a Dynamic Development Approach. Originally, Dunning investigated the variations in a state’s outflows of FDI with the variations of that state’s economic development. This investigation took place mainly by measuring variations of levels of OFDI and variations of levels of GDP per capita in an economy. This analysis is commonly known as the ‘IDP hypothesis’ (standing for Dunning’s Investment Development Path Hypothesis). This hypothesis has been tested over the years by many scholars, and it was often supported by their empirical analyses (e.g. Buckley & Castro, 1998; Barry et al., 2003; Bellak 2001).

12 trade’ and GDP per capita as indicators of economic development to test the IDP hypothesis (Dunning et al, 2001).

Even though Dunning admits that other variables should be used together with the variable GDP per capita, he makes it clear that the variation of GDP per capita is still paramount in the analysis of economic development. For instance, in 2001 Dunning et al. published a reviewed elaboration on the process of the investment development path (Dunning et al. 2001). By analyzing their elaboration on this process, it is possible to conclude that GDP per capita still plays a significant role in the IDP analysis. According to the authors, the process of investment development path (IDP) takes place through the following four stages (Dunning et al. 2001):

The first stage corresponds to a pre-industrial phase in the investment development path. Economies at this stage should have a GDP per capita bellow USD 1000 (at 1994 prices), and in general they only receive a small volume of inward FDI. This small volume is mainly a consequence of the economy’s underdevelopment and weak locational advantages (e.g. a poorly educated labor force) which makes the economy less attractive to foreign investors. In addition to that, the underdevelopment of these economies lead them to have smaller market sizes, which again makes these economies less attractive to foreign investors due to limited purchasing power. OFDI in these economies is insignificant due to their poor locational advantages (e.g. poorly educated labor, low investment in innovation, etc.), and for this reason, economies at this first stage are mainly net recipients of FDI.

13 new markets and acquire more resources. OFDI in these economies, however, is still small. Therefore these economies are still mainly net recipients of OFDI.

At the third stage, economies enjoy a higher GDP per capita (between USD 3000 – 10,000 at 1994 prices). Economies at this stage experience continuous improvements in their locational advantages, which eventually end up becoming ownership advantages to their firms (e.g. locational advantages such as an increase in investments in technology becomes an ownership advantage to firms as these firms begin to gain technological knowledge as a result of these investments). At this stage economies experience increasing outflows of FDI. The firms in these economies are more prepared to enter international markets and compete internationally, seeking possibilities to start exploiting their own assets across borders. These economies, however, remain net recipients of FDI.

The fourth, and final, stage, corresponds to those economies enjoying a GDP per capita above USD 10,000 (at 1994 prices). At this stage, economies are net outward investors due to the ownership advantages enjoyed by their firms. These economies see their outward FDI growing faster than inward FDI. If these economies keep developing they will go beyond stage four, which means that they will finally become major exporters, enjoying highly advanced technologies and higher living standards.

14 simply as an automatic consequence of economic development, without considering the possible effects that institutions and policies can have on the occurrence of OFDI.

A good example here is the study that Liu et al. (2005) conducted on Chinese OFDI. According to Liu et al. (2005, pp. 112 -113), the emergence and growth of Chinese OFDI is consistent with the IDP hypothesis. They conclude that, for that reason, there is no need to look into the Chinese institutional framework to understand the origins and evolution of Chinese OFDI. In fact, these authors suggest that policies designed to directly promote OFDI in a country might be unnecessary, and this is because OFDI can evolve simply as a result of economic growth (Liu et al. 2005, pp. 113).

Those scholars who criticize the IDP hypothesis on the grounds that it neglects the power of institutions, claim that the IDP hypothesis should be further extended to include institutional variables (e.g. Stoian, 2013; Kalotay & Sulstarova, 2010). Especially in the context of OFDI from developing countries, these scholars argue that analyzing institutional factors can be of relevance. For instance, according to Stoian (2013), developing countries (especially emerging markets and transition economies), often have particular institutional characteristics that have been put in place in order to enhance and drive their economic development so they can “catch up” with developed economies in a globalized world. These institutional characteristics, according to Stoian (2013), deserve the attention of researchers conducting analyses on the determinants of OFDI in these economies since they might have an influence on OFDI.

This kind of argument has gained the support of an increasing number of scholars from the 2000s onwards. As a consequence, by the mid-2000s, it is possible to see that several researchers focusing on OFDI from developing countries began to give more attention to institutional variables in their analyses on the determinants of OFDI (e.g. Stoian, 2013; Khoon & Wong, 2011; Wang et al., 2012). The next sub-section will elaborate on these scholarly works.

2.4 –National institutions and policies as determinants of OFDI

15 OFDI, excluding possible economic determinants (e.g. Wang et al. 2012; Luo et al. 2010). What these studies have in common, however, is that they all recognize that national institutions and policies can have an impact on the occurrence of OFDI. Most of these researches focus on two specific groups of developing countries, namely emerging markets (Khoon & Wong, 2011; Wang et al. 2012; Luo et al. 2010), and transition economies (Stoian, 2013; Blanke-Ławniczak, 2009)2.

The reason why these groups of developing countries have gained increasing attention by scholars is because they are the ones experiencing the most substantial increases in OFDI (Stoian, 2013). According to Luo et al. (2010), including national institutional factors in the analysis of the determinants of OFDI in developing economies is of great importance. They justify this claim by explaining that, in this type of economy, enterprises often face competitive disadvantages such as, for instance, lack of international experience and/or lack of capital. Thus, for that reason, governments in these countries often step in to coordinate the functioning of institutions and policies in order to offset these competitive disadvantages. In the context of outward FDI, this means that governments can coordinate the functioning of institutions and policies in order to promote OFDI (e.g. governments can design programs aimed at assisting firms to expand their operations across borders - more specific examples of such programs can be found further in this sub-section).

Institutional factors, in fact, seem to have an influence on the occurrence of OFDI. For instance, Stoian (2013) has conducted an analysis on the determinants of OFDI from twenty Central and Eastern European states. The analysis conducted by Stoian was an extended version of the IDP hypothesis (using linear regression), in which not only economic, but institutional numerical variables were also included as possible determinants of OFDI. What Stoian has found is that one particular institutional variable can be considered as a significant determinant of OFDI from Central and Eastern European states. This factor is ‘overall institutional reforms’, which includes, for instance, privatization, price liberalization, and banking reforms. According to Stoian (2013, p.623), ‘overall institutional reforms’ comprise a wide mix of institutional reforms that have been

2 To clarify the difference between these two groups of developing countries, emerging markets can be defined as

16 implemented in post-communist economies with the purpose of ensuring their transition from centrally planned to market economies. The author explains that these overall institutional reforms reflect an economy’s level of competitiveness and development. That means that the more advanced these overall institutional reforms are, the more competitive and developed an economy is. As a consequence of this increased development and competitiveness, the author suggests, firms in these economies gain more entrepreneurial confidence and increase their investments both inside and outside their home country (Stoian, 2013, p. 623). Other authors have conducted similar studies and their findings also supported the idea that institutional factors can have an effect on OFDI. For instance, Khoon & Wong (2011) have found that the liberation of capital outflows can lead to an increase in OFDI for Malaysia, and Salehizadeh (2007) has found that the deregulation of financial and capital markets, and the maintenance of sound monetary and fiscal policies can enhance OFDI in both emerging markets and transition economies.

The studies mentioned above present the role that broad institutional reforms can play in enhancing OFDI in developing countries. In other words, they focus on outcomes of institutional reforms and operations, and on whether or not these outcomes can possibly have an impact on OFDI. For instance, the deregulation of financial markets allows firms to invest abroad more easily. If firms can carry out investments abroad more easily, they can take part in OFDI activities more easily as well. Thus, deregulation of financial markets might lead to an increase in OFDI. These studies, however, are limited to such broad conclusions. Possibly because they have been conducted mainly through quantitative analyses (e.g. regression analyses), they fail to investigate in depth the possible relationships between institutional operations and the occurrence of OFDI. For instance, these researches do not investigate in depth which actors (i.e. policy-makers) are involved in these institutional operations, and which specific tools they use in order to facilitate OFDI. Moreover, questions such as what are the specific motivations of these actors? And what are the main institutions that seem to have a direct influence on outward FDI? are left unanswered in such studies. This means that even though these studies further contribute to the theoretical knowledge on possible institutional determinants of OFDI, they still do not address in depth how and which institutions could possibly have an impact on OFDI in a country.

17 often focuses only on the national government as an actor that can have an influence on the occurrence of OFDI. This means that such studies neglect possible economic and international institutional factors that could possibly have an influence on OFDI.

One such study, for instance, is the one conducted by Luo et al. (2010) on government determinants of OFDI from China. What Luo et al. suggest in their study is that the Chinese strategy which is commonly known as ‘going global strategy’ seems to contribute significantly to the country’s levels of OFDI. Luo et al. present in their study an in-depth analysis of many domestic institutions that are involved in the Chinese ‘going global’ strategy. According to the authors, this strategy comprises a set of policies and institutional reforms such as: (1) the creation of incentives for OFDI (e.g. the provision of fiscal incentives such as tax incentives and low-interest loans to firms that want to invest abroad), (2) easing capital controls for OFDI by designing more liberal policies, and (3) providing information and guidance to firms with regards to possible investment opportunities abroad (Luo et al. 2010, p. 70).

18 sum, thus, it is possible to infer here that OFDI has been recognized by different governments in both the developed and the developing world as an important strategy to achieve economic development. For that reason, many of these governments have created incentives specifically targeted at promoting OFDI.

19

3.

The purpose of this research and its methodology

As previously mentioned in the literature review, through this research I want to conduct a more informative analysis on some of the economic and institutional factors that could have an influence on OFDI in developing countries. What will make this study different from previous ones is that this study will not be restricted to a more superficial analysis on the government institutions and policies that can have an influence on OFDI. Instead, this research will go more in depth and will include an analysis on the policy-makers that participate in the governance of those institutions, with observations on their economic motivations and policy preferences. In addition to that, in this research I will not only observe national policies and institutions, but also international ones, such as the International Monetary Fund (IMF) and the World Bank. My goal here is to carry out these observations in order to offer more context to the role that public institutions can play in the occurrence of OFDI in developing countries. In my view, these observations, combined with observations on economic factors, will result in a more holistic analysis of the different factors that could have an influence on OFDI.

3.1- Methodology

Because the goal of this study is to provide a deeper understanding on the possible determinants of OFDI in developing countries, I have chosen to conduct this research in the form of a multiple case study. For this research, two developing countries will be analyzed, namely Brazil and India. The reason why I have chosen to conduct two case studies is:

1- A case study design will allow me to investigate in depth how a phenomenon – in this case OFDI – is taking place in two different developing countries.

20 similar policies to enhance OFDI could indicate that these countries have similar motivations to promote this economic activity. Thus, in sum, by analyzing two countries a greater contribution to the current knowledge on the possible determinants of OFDI in developing countries can be provided.

3.1.1 – The choice of Brazil and India

For this research I have selected one specific group of developing countries to focus my analysis on, namely emerging markets. The reason why I have chosen to focus on emerging markets is because, as mentioned in the literature review (e.g. by Luo et al. 2010 and Sauvant, 2005), they have experienced some of the most substantial increases in OFDI among developing countries in the past decades. Thus, because they are experiencing such significant increases, it would be informative to understand more in depth how and why these increases have taken place.

To clarify, it is first important to define what the term emerging markets means in this study. In sum, emerging markets could be defined here as those developing countries – or economies – that are experiencing rapid economic development, and therefore present certain characteristics similar to those of a developed economy. More formally, according to the definition by the Morgan Stanley Capital International’s Market Classification Framework, emerging markets are economies that present certain characteristics of a developed economy, but still do not meet all the economic standards (e.g. such as sustainability of economic development) to be considered a developed economy (MSCI, 2014, p. 1).

21 Figure 3.1.1.1 – Evolution of OFDI from BRICS countries (UNCTAD, 2014)

By analyzing the graph above, it is possible to see that Brazil presented the highest rates of OFDI until the 2000s. By the 2000s, Russia’s OFDI skyrocketed, followed by China that also experienced substantial increases by the mid-2000s. In comparison to these three countries, South Africa and India present more modest outflows of FDI, with India presenting the lowest rates during most of the years from 1980 until 2014.

Based on these observations, I have decided to focus my analyses on two countries that have presented significantly different levels of OFDI over the years. I have chosen India because this country presents the lowest rates, and Brazil because it presents high rates of OFDI since the 1980s. The reason why I have not chosen China or Russia instead of Brazil is mainly due to language barriers. While conducting a qualitative analysis on the institutional factors that might influence OFDI from these countries, I will have to analyse many documents, including policy documents and transcriptions of public speeches. Thus, due to the fact that I do not speak the local languages spoken in Russia and China, I believe I will be limited in my analysis if I select these countries. In the case of India and Brazil, however, documents are issued in Portuguese and English, and these are languages that I have a good command of.

0 100000 200000 300000 400000 500000 600000 700000 800000

OFDI

sto

ck

(U

SD

m

ill

ion

s)

Year

OFDI Evolution from BRICS countries (1980 - 2014)

22 My motivation to select countries presenting different rates of OFDI is mainly because both of them have experienced significant increases in economic development; however, whereas one presents high rates of OFDI over the years, the other presents somewhat more modest increases since the 1980s. My goal, therefore, is to find out whether some institutional and economic factors could possibly explain the historical variation of OFDI between these two countries.

To summarize, in terms of unit of observation and unit of analysis, it can be said that the units of analysis of this research are Brazil and India. The unit of observation refers to the time-space element for which my observations will be conducted. In this case the units of observation will be country-by-year. This is because in this research I will carry out observations on Brazilian and Indian OFDI within the timeframe between 1980 and 2014. This timeframe has been chosen because of data availability. For instance, variables indicating variations of OFDI are only available from 1980 until 2014.

3.1.2 – Data selection and hypotheses

For this research data referring to the variables will be collected in two different ways. Firstly, quantitative data will be collected for the analysis of the economic factors that could possibly have a relation with OFDI. Secondly, qualitative data will be collected for the analysis of the institutional factors that might possibly affect the occurrence of OFDI from Brazil and India. 3.1.2.1 – Data indicating economic factors that could have a relation with OFDI

The first part of the case studies on Brazil and India will elaborate on the possible economic factors that can be related with their levels of OFDI. This part of the case studies will be similar to those studies conducted by scholars testing the extended version of the IDP hypothesis. The dependent variable that I will use is OFDI stock. This variable has been used in many studies testing the IDP hypothesis (e.g. Liu et al 2005; Stoian, 2013). The source of this variable is the UNCTAD. According to the UNCTAD’s definition, OFDI stock is “the value of the share of capital and reserves (including retained profits) attributable to the parent enterprise investing abroad, plus

the net indebtedness of affiliates to the parent enterprises” (UNCTAD, 2014).

23 analyzed under the theory proposed by the IDP hypothesis. As I explained in the literature review, there is a consensus among many scholars that variations in GDP per capita directly reflects variations in economic development in a state. This is mainly because GDP per capita indicates the gross domestic product generated in a country in relation to its citizens. Data on this variable will be collected from the database of the World Bank (World Bank, 2015). Based on the IDP hypothesis which suggests that an increase in economic development can lead to an increase in OFDI, the first hypothesis that I will raise here is the following:

H1: An increase in GDP per capita coincides with an increase in levels of OFDI in Brazil and India.

The second independent variable has also been used by Stoian (2013) when she expanded the IDP hypothesis in her study. This variable is ‘expenditure on research and development’. This variable is based on the idea that as a country develops economically, it will invest more on research and development (R&D) so it can keep developing further. If a country experiences improvements in R&D, its domestic companies can benefit from it by incorporating these improvements into their operations (e.g. companies can benefit from advances in science and technology that occurred through improvements in R&D). As a consequence of these improvements, domestic companies can grow in scale and can be more able to expand their operations overseas to enhance their access to foreign resources and markets and possibly increase their sources of profit. The variable ‘expenditure on research and development’ refers to both private and public expenditures, and the source of this data is the World Bank (World Bank, 2015) and the UNCTAD (UNCTAD, 2014). The numerical values used in this research have been calculated by me, by using the World Bank’s variable “expenditure on R&D as a percentage of GDP”, and the UNCTAD’s variable “Country GDP”. For this case, the hypothesis that I will test will be the following:

H2:An increase in expenditures on research and development coincides with an increase in levels of OFDI in Brazil and India.

24 an annual basis, without deducting the liabilities of those foreign firms investing in these countries. Data on this variable will be collected from the UNCTAD (UNCTAD, 2014).

According to Dunning et al. (2001), inward FDI is an important factor in the investment development path. As mentioned in the literature review, as the economy of a country develops, the market in that economy will be likely to grow, and investments for further development (e.g. investments in research and development) are also more likely to happen. These new local assets (e.g. expanded market and more technological improvements) make the home country more attractive to foreign firms. For that reason, foreign firms will be more likely to invest in that country through FDI. With more inward FDI, the home country can benefit as foreign firms can transfer their own assets to the home country (e.g. skills, technology, and expertise). Local firms in the home country can benefit from these transfers if they incorporate them into their operations. As a result, domestic firms enjoying more technology, skills, and expertise will be more competitive and consequently will be more likely to exploit their new assets through OFDI (Dunning et al, 2001). Under this rationale, the third hypothesis that I will test is the following:

H3: An increase in inward FDI coincides with an increase in that country’s OFDI.

To test the three hypotheses presented above, I will conduct a quantitative analysis on the variation of the independent variables ‘GDP per capita’, ‘expenditure on R&D’, and ‘inward FDI’ and the dependent variable ‘OFDI’. My goal will be to find out whether or not the variations of those variables coincide as I suggested in the hypotheses.

3.1.2.2 – Data indicating institutional factors that could possibly have a relation with OFDI The second part of the case studies on Brazil and India will be based on the possible institutional factors that could have a relation with the levels of OFDI in both countries. This part will receive greater attention as I intend to elaborate in depth on the roles that public institutions and the actors within them seem to play in the field of outward FDI in the two countries.

25 of policies easing capital controls for OFDI’ in this research. To have access to data on this variable I will use sources such as: (1) policy documents from the governments of Brazil and India (especially from the Central Bank of Brazil and the Reserve Bank of India), (2) speeches from politicians from both countries (often available online), and (3) direct communication with relevant institutions in both countries via e-mail. One of my goals here is to find out whether or not such policies have been adopted in these countries, and which national institutions have contributed to the development of such policies. My main goal, however, is to test the following hypothesis, which suggests that such policies could lead to an increase of OFDI:

H4: The existence of national policies easing capital controls for OFDI activities coincides with an increase in OFDI.

The second independent variable is the ‘presence of pro-market policy-makers holding central positions in strategic policy-making institutions’. This variable has not been used in the researches mentioned in the literature review; however, I will employ it here because in this research I want to include an analysis on the actors (i.e. policy-makers) that could possibly have an influence on the occurrence of OFDI in India and Brazil. My goal is to find out whether or not the pro-market inclinations of key policy-makers could possibly have an influence on the occurrence of OFDI in the countries being observed. The term ‘pro-market policy-makers’ refers to the idea that these policy makers support the creation of an economic environment less restrictive to the conduction of businesses. That is, economic transactions can, to a larger extent, be regulated by the market itself and not so much by government regulations and interventions. Another term in this variable is ‘strategic policy-making institutions’. In this research, this term stands for those public institutions that have the authority to create and/or approve policies that can directly govern OFDI activities in Brazil and in India. Finally, the term ‘central positions’ refers to those policy-makers who have great authority to create and pass policies within the strategic policy-making institutions. In this research, actors holding central positions are the governors (e.g. presidents) of those ‘strategic policy-making institutions’.

26 explain the political views of those central actors. Sources for such texts and public speeches are, for instance, online pages of policy-making institutions (e.g. Central Bank of Brazil, Reserve Bank of India, Indian Ministry of Commerce, etc.).

My rationale for this specific variable is that, if key policy-makers are more pro-market, they will provide more freedom for local businesses to carry out their OFDI activities. Thus, with this line of thought, the hypothesis that I will be testing is the following:

H5: The presence of pro-market makers holding central positions in strategic policy-making institutions coincide with an increase in the occurrence of OFDI in Brazil and in India.

The third independent variable that I will use is ‘the existence of public financial institutions providing low-interest loans to firms engaging in OFDI’. The reason why I chose to use this variable is because I want to find out whether or not public financial institutions in Brazil and India offer financial services to assist local firms in their overseas direct investments. This variable is based on the studies by Luo et al. (2010) and Sauvant (2005). These authors have mentioned in their researches that many developed countries and China have such financial services in place to assist their local firms to invest abroad. In fact, Luo et al. (2010) have suggested that the provision of low-interest loans by national governments are important tools that can enable local firms to engage in OFDI. Based on this argument, I want to find out in this research whether or not India and Brazil also have institutions offering such services, and also whether or not these services seem to have an influence on levels of OFDI in these countries. To obtain data on this variable I will look for information on previous researches in the field, and on documents by the government in Brazil and India. This variable will be tested through the following hypothesis:

H6: The presence of institutions providing low-interest loans to firms engaging in OFDI coincides with an increase in OFDI.

27 When it comes to economic-related policies, the IMF and the World Bank have great international influence. These institutions often provide loans to developing countries to assist them in their economic development, and in fact, both India and Brazil have already borrowed from at least one of these two institutions in the past decades (IMF, 2015; IMF, 2015 a). Both the IMF and the Wold Bank can have an influence on national policy-making because the loans that they provide are often followed by policy prescriptions (named by them as adjustment policies).

In short, these organizations provide loans to a country under the condition that that country will adopt certain adjustment policies which, according to the IMF and the World Bank, are aimed at establishing economic stabilization and development in the country receiving the loan (IMF, 2006). These international institutions, however, have clear pro-market inclinations. For instance, their policy prescriptions often include the liberalization of investment and trade policies, as well as the abolition of anti-competitive policies (IMF, 2006 a).

In sum, both institutions have pro-market inclinations, and both have a history of loan provision to India and Brazil. Thus, considering their loan conditionalities and their inclinations, it could be possible that they have prescribed policies aimed at enabling OFDI in these countries. Through this research, therefore, I want to find out whether or not these institutions have a possible relation with the occurrence of OFDI in India and Brazil. To obtain information on this, I will analyze previous researches in this field and will communicate directly with the institutions via email. The hypothesis that I aim to test here is the following:

H7: The adoption of adjustment policies from the IMF and/or World Bank promoting the deregulation of OFDI activities in Brazil and India precede an increase in OFDI in these countries.

Finally, the dependent variable that I will use in this part of the research will be the same that I will use to test the hypotheses related to the economic factors that can influence OFDI. That is, the dependent variable will be OFDI stocks, and the data source is the UNCTAD.

28 3.1.3 – Considerations about replicability

29

4.

Case study: India

This chapter will present my observations on Indian OFDI. Throughout this case study I aim to present all the information that is needed in order to test the hypotheses mentioned in the previous chapter for the country of India. For the purpose of this research, this case study will be presented as follows: firstly, it will start with a brief introduction on the Indian economy and outward foreign direct investments. This first part will present some of the main characteristics of OFDI in the country, including growth rates, main drivers, countries of destination, and the sectors in the Indian economy most engaged in OFDI. After that, the second and third sections of this case study will elaborate more extensively on the economic and institutional factors that could possibly have a relation with the occurrence of OFDI in the country.

4.1 – Introduction: Indian economy and OFDI

India is a federal parliamentary republic located in southern Asia. More recently, the country stood out as one of the fastest growing economies in the developing world. In the past decade alone, India’s GDP grew from USD 715,459 million in 2004 to USD 2,041,085 million in 2014 (UNCTAD, 2014 a). India has a population of 1.252 billion citizens, which makes it the second most populous country in the world. Given its significant economic growth and massive population, it is no surprise that India, in the past years, has been considered worldwide as an emerging market (Koesterich, 2015; Holmes, 2015).

In terms of OFDI, since the mid-2000s an increasing number of Indian firms have engaged in overseas direct investments, indicating their growing participation in a global economy (Khan, 2012). As a result of that, levels of OFDI from India have increased significantly. For instance, in 2000 the volume OFDI from India totaled USD 1,733 million, and in 2005 this amount rose up to USD 9,741 million. Finally, by 2010 in totaled USD 96,901 million (UNCTAD, 2014).

30 In terms of industry sector, the Indian firms most engaged in OFDI are those active in the transport, storage and communication services sector (30.4% of total OFDI). Other sectors such as manufacturing, and agriculture and mining are also significant, corresponding respectively to 25.8% and 16.5% of Indian OFDI (Care Ratings, 2014). The table below illustrates in more details the distribution of Indian OFDI by sector in US dollars (April 2013 – Jan. 2014).

Table 4.1.1 – Indian direct overseas investments by sector (April 2013 – Jan. 2014)

Sector Total invested (in USD million)

Transport, storage and communication services 8,906

Manufacturing 7,560

Agriculture and mining 4,826

Wholesale, retail trade, restaurants and hotels 2,903

Financial, Insurance and business services 2,351

Construction 1,394

Community, social and personal services 1,268

Miscellaneous 56

Electricity, gas and water 23

TOTAL 29,294

Source: (Care Ratings, 2014)

In terms of country of destination, Indian firms invest predominantly in the Netherlands (28.8% of total OFDI), Singapore (15.2%), and the British Virgin Islands (12.6%). (Care Ratings, 2014). The table below illustrates Indian OFDI by country (April 2013 – January 2014).

Table 4.1.2 – Indian direct overseas investments by country (April 2013 – Jan. 2014)

Country Total investments (in USD) Share in total (%)

Netherlands 8,427 28.8

Singapore 4,454 15.2

British Virgin Islands 3,687 12.6

Mauritius 3,029 10.3

United States of America 2,052 7.0

United Arab Emirates 1,446 4.9

United Kingdom 1,356 4.6

Switzerland 994 3.4

Azerbaijan 814 2.8

Cayman Island 523 1.8

Hong Kong 309 1.1

Cyprus 275 0.9

Saudi Arabia 269 0.9

Belgium 180 0.6

Oman 121 0.4

TOTAL 29,294 100.0

31 Thus far, this chapter has shown that levels of OFDI from India have increased substantially since the 2000s, and, in general, Indian firms engaged in OFDI tend to invest both in developing and developed countries in Asia and other continents across the globe. In view of the substantial growth of Indian OFDI, we can raise the following question: what are the factors that could possibly have an influence on the occurrence and evolution of Indian OFDI over the past decades? To address this question, the remainder of this chapter will present some of these factors.

4.2 – Economic factors that could have an influence Indian OFDI

In the scholarly literature, economic development is often mentioned as the prime explanatory factor for OFDI (Stoian, 2013). This rationale is proposed by the IDP hypothesis, which suggests that as a country develops economically, its firms tend to develop as well and, consequently, they expand their operations overseas to obtain new sources of productivity and profit (Stoian, 2013). As mentioned in the previous chapter, for this research the IDP hypothesis will be tested using three economic factors (i.e. variables), namely GDP per capita, investments in R&D, and inward FDI. If the IDP hypothesis is correct, we should see that the variations of the aforementioned variables present continuous similarities with India’s variations of OFDI. The next paragraphs, therefore, will contain some observations on these three economic factors together with OFDI from 1980 until 2014. The graph that follows illustrates India’s variations of GDP per capita and OFDI:

Figure 4.2.1: Indian GDP per capita and OFDI: 1980 – 2014 - Sources (UNCTAD 2014; World Bank 2015)

As the graph shows, Indian levels of OFDI did not always vary according to the country’s variations of GDP per capita. For instance, whereas GDP per capita presented a moderate, but

0 200 400 600 800 1000 1200 1400 1600 1800 1 10 100 1000 10000 100000 1000000

1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014

In d ian G DP p er cap ita (cu rre n t U SD) In d ian OFDI (U SD m ill ion ) Year

Indian GDP per capita and OFDI (1980 - 2014)

OFDI India

32 continuous growth throughout the 1980s, the country’s levels of OFDI have remained virtually unchanged. Moreover, between 1991 and 1993 the country’s GDP per capita decreased, whereas levels of OFDI increased. Again, in the early 2010s, GDP per capita decreased whereas levels of OFDI kept increasing. In sum, therefore, it is possible to conclude that whereas both OFDI and GDP per capita increased over the years, such increases did not always occur simultaneously. The next graph illustrates India’s variations of expenditures on R&D and OFDI. For this observation, the variations will be limited to the time period ranging from 1996 and 2011. This is because the variable ‘expenditures in R&D as percentage of GDP’ is only available for those years.

Figure 4.2.2: Indian levels of OFDI and Expenditure on R&D - Sources (UNCTAD, 2014; World Bank, 2015)

As the graph shows, both Indian OFDI and expenditures on R&D have presented continuous increases between 1996 and 2011. Nevertheless, these increases present different patterns in some years. For instance, the expenditures on R&D have presented their most substantial increases from the early 2000s up until 2011. In the case of OFDI, however, the most substantial increases took place from the mid-2000s onwards. It was by the late 2000s and early 2010s that both variables began to present very similar variations. In sum, therefore, the graph illustrates that during all the years observed, both OFDI and expenditures on R&D have increased, but it was from 2009 onwards that they began to present more similar variations.

The next graph summarizes the variation of Indian inward FDI and OFDI.

0 2000 4000 6000 8000 10000 12000 14000 16000 18000 0 20000 40000 60000 80000 100000 120000 Exp en d itu re in R& D (% o f G DP) in USD m ill ion In d ian OFDI (in U SD m ill ion ) Year

Indian expenditure on R&D and Indian OFDI (1996 - 2011)

Indian OFDI

33 Figure 4.2.3: Indian levels of inward FDI and OFDI - Source (UNCTAD, 2014)

As the graph illustrates, the levels of Indian OFDI present a very similar pattern as the country’s levels of inward FDI. According to the illustration, similarly to its levels of inward FDI, Indian levels of OFDI have also presented their most substantial increases during the mid-2000s. The difference between Indian levels of inward FDI and OFDI, however, is that inward FDI presented more significant increases throughout the 1990s, whereas Indian OFDI increases during that decade was, in comparison, more modest. Moreover, from 2010 onwards, levels of OFDI kept increasing continuously, whereas levels of inward FDI presented more oscillations.

In short, while the observations on these three economic factors revealed that all of them increased over the years, just like the levels of Indian OFDI, not all of them presented the same patterns of variations. From the factors observed, the one presenting the most similar variations with OFDI is inward FDI. Next to that, expenditures on R&D also present similar variations in a sense that, just like OFDI, it presented uninterrupted increases over the years. The variable presenting the least similarities with OFDI is GDP per capita, mainly because this variable presented decreases in some years when OFDI presented increases. Because not all these three factors present variations similar to those of OFDI, the IDP hypothesis cannot be entirely confirmed here as an explanatory theory for Indian OFDI. For this reason, an alternative explanation for the occurrence of Indian OFDI should be considered and tested. The next section, therefore, will follow by elaborating on some institutional factors that could have an influence on Indian OFDI.

0 20000 40000 60000 80000 100000 120000 140000 0 50000 100000 150000 200000 250000 300000

1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014

In d ian OFDI (U SD m ill ion ) In d ian inw ard FDI (U SD m illi on ) Year

Indian inward FDI and OFDI (1980 - 2014)

34 4.3 – Institutional factors that could influence Indian OFDI

In this section four institutional factors that could be related with Indian OFDI will be observed. In sum, there factors are: (1) policies easing capital controls for OFDI in India, (2) the politico-economic inclinations of key policy-makers in the country, (3) the existence of financial services providing low-interest loans to firms engaging in OFDI, and (4) policy prescriptions by the IMF and/or World Bank. Before observing these factors, however, it is important to first understand the functioning of the Indian political system. This understanding is important because it provides background information on the most relevant public institutions and national actors that could have an influence on Indian OFDI policy. The following sub-section will elaborate on this.

4.3.1 – Background information on the Indian political system

India has a parliamentary system of government. Thus, because of that, its executive branch is accountable the legislature (i.e. the parliament). Moreover, the head of government and the head of state are two different entities. The head of government is the actor who holds real power over the country’s government, being the chief of government and adviser to the president. In addition to that, it is the head of government (India’s prime minister) who advises the president on the selection of ministers for the country’s cabinet. Because the executive branch is strongly connected to the parliament (e.g. it derives its legitimacy from the legislature), the chief of the executive branch has also strong connections with the country’s parliament. In the case of India, the chief of executive, or prime minister, is actually the leader of the party holding the majority of seats in the Lok Sabha (the lower house of India’s bicameral parliament) (CIA, 2015).

35 4.3.2 – Indian policies easing capital controls for OFDI

When it comes to Indian policy on capital control for OFDI, policy-makers in India tend to divide the evolution of this policy in two phases (Khan, 2012). The first phase is framed by the General Guidelines on Indian Joint Ventures Overseas, which is a policy guideline that came into force in 1969, and the second phase is framed by the Guideline for Indian Joint Ventures and Wholly-owned Subsidiaries Abroad, which replaced the policy guideline mentioned above in 1992 (ibid.). Both policy guidelines were established by the Indian Ministry of Commerce.

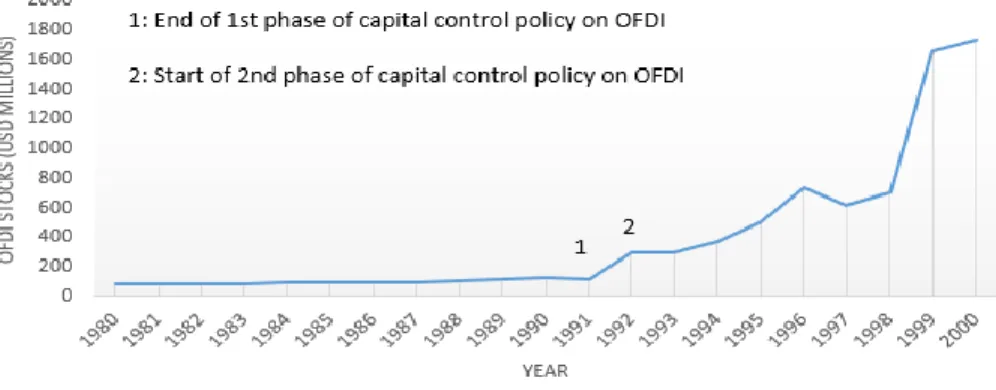

The first phase of Indian capital control policy, which lasted until 1992, had as one of its main characteristics a highly restrictive framework for OFDI activities (Pradhan, 2008, p. 176). Coincidently or not, during the time that this policy regime was in place, the levels of Indian OFDI remained virtually the same. As the graph below illustrates, it was only by 1992 – when a new policy on capital controls was adopted – that Indian levels of OFDI began to rise.

Figure 4.3.2.1 – India’s first OFDI capital control policy - source: (UNCTAD, 2014)

36 To minimize foreign exchange costs, this first policy regime required that Indian firms could only engage in OFDI through non-cash investments. That is, under this policy regime, firms would have to engage in activities such as the exports of Indian made machines, equipment, and technical know-how in their overseas direct investments. Cash remittances were virtually forbidden. Therefore, only very small amounts of cash were allowed to be remitted to meet preliminary expenses related to setting up a new unit abroad (Khan, 2012). The main purpose of this policy regime was to exploit the export potentials of Indian outward FDI. That is, under this policy regime OFDI was seen as a means to promote Indian exports (e.g. exports of machines and technical know-how). This first phase of capital control policy was also restrictive in terms of granting permission to firms to invest abroad. Under this policy framework, the Indian Ministry of Commerce required that all investing firms had to obtain authorization before engaging in OFDI (Pradhan, 2008). The main entity in charge of evaluating and approving OFDI proposals by Indian firms was the Ministry of Commerce (Pradhan, 2008).

The second phase of capital control policy initiated in 1992, when the Guidelines for Indian Joint Ventures and Wholly Owned Subsidiaries was established, changing the Indian OFDI scenario. With these new guidelines, the Indian OFDI policy regime became less restrictive. In fact, in the early 1990s, the Indian economy as a whole was experiencing liberalizations to increase India’s participation in the global economy. For instance, such liberalizations included less barriers to inward FDI and to trade (Pradhan, 2008). As a consequence of these liberalizations, an increasing number of foreign firms were investing and exporting their products to India. To survive in this new and increasingly competitive environment, Indian firms realized that they would have to become more competitive as well. With that, restrictions on OFDI were relaxed by Indian national authorities as they began to see OFDI as a suitable strategic tool that could enable Indian firms to become more competitive (ibid.).

37 to USD 2 million every three years. Moreover, cash remittances were still highly limited (restricted to USD 500,000 within a period of three years) (ibid). Interestingly, however, as the government relaxed capital controls in 1992, Indian levels of OFDI more than doubled, rising from USD 113 million in 1991 to USD 294 million in 1992 (UNCTAD, 2014).

In 1995 a new step in the process of capital control relaxation took place as the Fast Track Route

(or automatic route) was established by the Reserve Bank of India (hereinafter RBI). Under this policy, Indian firms could obtain automatic permission to invest overseas if their investments did not exceed USD 4 million within a period of three years (Khan, 2012). The firms that intended to invest more than USD 4 million were required to apply for an approval. Under this policy, the main institution in charge of granting approval to OFDI projects was the RBI, and no longer the Ministry of Commerce (ibid).

38 relaxed capital restrictions for OFDI activities by firms in these sectors. In that year, firms active in these sectors obtained permission to invest in excess of 400 percent of their net worth through overseas direct investments (Khan, 2012).

Representatives of the RBI believe that these substantial liberalizations that took place by the mid-2000s onwards were only possible because, at that time, India was experiencing a steady rise in foreign capital inflows. Thus, with an increase in foreign capital inflows (e.g. due to increases in India’s exports), Indian authorities were in a better position to progressively relax the country’s capital controls for OFDI since the country enjoyed larger exchange reserves (Khan, 2012). As these major reforms took place, the levels of Indian OFDI continued to grow exponentially. For example, in the second half of the 2000s, the country’s OFDI levels increased from USD 9,741 million in 2005 to USD 96,901 in 2010 (UNCTAD, 2014).

Currently, virtually any Indian firm can take part in OFDI under the automatic route. The only exception is for certain real estate investments (e.g. buying or selling of real estate) and banking investments, which must first obtain approval (Khan, 2012). As mentioned earlier, firms still can invest up to 400 percent of their net worth in OFDI activities. Cash remittances remain limited, with a ceiling of USD 125,000 within a financial year (RBI, 2014 ). The two graphs that follow summarize with illustrations the policies that have been mentioned in this section. The graphs also illustrate the variations of OFDI over the years under observation.

39 Figure 4.3.2.3: OFDI capital control policies – India (2001 – 2014)

4.3.3 - Indian policy-makers and Indian outward FDI

Shifting this case study more towards an observation of Indian policy-makers, it is possible to affirm here that policy-makers in strategic institutions (e.g. chairman of Reserve Bank of India, Minister of Commerce, and Prime Minister) have not always been favorable to a pro-market governance of the Indian economy. Prior to the 1990s, economic policies were predominantly of a restrictive nature, and, as a consequence, India was more of a closed economy, with little international economic transactions. Up until the 1990s, policy-makers focused mainly on constraining the reach of Indian firms to serve the local market only (Chidambaram, 2007). This characteristic of Indian economic policy was already in place by 1947, when the country gained its independence. At that time, many Indian policy-makers had socialist influences, and, consequently, they passed legislations that were highly influenced by socialism (ibid).

40 restricted production, capacity, production mix, and marketing in the manufacturing sector (Chidambaram, 2007). As a consequence of this policy, Indian firms were not experiencing significant developments, and the Indian economy was not operating in a competitive fashion (ibid). This policy regime persisted throughout the 1980s.

It was only by the early 1990s that national authorities began to open the Indian economy for international economic transactions. In 1991, under the government of Prime Minister P. V. Narasimha Rao, the country’s economic policy regime began to be less restrictive for activities such as trade and investments, and the License Raj was completely abolished by the Minister of Finance Manmohan Singh. At that time, policies related to inward and outward FDI were mainly governed by the Ministry of Commerce, which was being led by Minister Chidambaram Palaniappan. Mr. Palaniappan was – and still is - a strong advocate of policy liberalization to allow the expansion of Indian businesses overseas. In his view, OFDI allows Indian firms to have more access to foreign resources and markets, and it also enables these firms to have more access to new technologies and skills from abroad (Chidambaram, 2007). In fact, it was during his tenure as Minister of Commerce in 1991 and 1992, and again in 1995 – 1999 that significant relaxations on capital controls took place in India.

41 In short, the observations included in this section indicated that only from the 1990s onwards key policy-makers in strategic institutions began to be more favorable to pro-market policies. With that, up until the present time, these policy-makers have created an environment less restrictive to economic activities and more favorable to OFDI. It could be for that reason Indian levels of OFDI presented continuous increases from the early 1990s onwards.

4.3.4 - The provision of financial incentives to Indian firms investing abroad through low-interest rates loans

While the increasing acceptance of OFDI among Indian policy-makers seems to be reflected in the adoption of several policies easing capital controls for this activity in the country, in the field of financial assistance to promote OFDI India still does not seem to have very ambitious policies in place. In developing countries such as China (see Luo et al, 2010) and Brazil (see Caseiro et al. 2014), public financial institutions have lines of credit specifically designed to provide loans to firms engaging in OFDI. These lines of credit have been designed by national governments as a tool to promote OFDI in their countries. For that reason, the loans provided by them have low-interest rates (Luo et al, 2010).

In India, contrary to Brazil and China, there seems to be no banking institution providing financial incentives to Indian firms investing abroad through low-interest loans. According to Mr. Harun R. Khan, the Deputy Governor of the RBI, India’s Exim Bank is the institution with the most significant mandate in this regard. The Exim Bank, which was launched in 1982 by the Indian government, is considered as the country’s premier export finance institution (Exim Bank, 2015). The Exim Bank has the mandate of enhancing exports from India and integrating the country’s investments (including foreign investments) with the country’s overall economic growth (Exim Bank, 2015).