Money and Price Posting under Private Information

Mei Dongy Janet Hua Jiangz

September 10, 2013

Abstract

We study price posting with undirected search in a search-theoretic monetary model with divisible money and divisible goods. Ex ante homogeneous buyers experience match-speci…c preference shocks in bilateral trades. The shocks follow a continuous uniform distribution, and the realizations of the shocks are private information. We show that there exists a unique monetary equilibrium for generic values of the in‡ation rate. In equilibrium, each seller posts a continuous pricing schedule that exhibits quan-tity discounts. Buyers may spend nothing, a fraction or all of their money holdings, depending on their preference-shock realizations. In‡ation reduces the extent of non-linear pricing. The model also captures the hot-potato e¤ect of in‡ation along both the extensive margin, as an increase in the trading probability, and the intensive margin, as higher fractions of money being spent.

JEL classi…cation: D82, D83, E31

For their comments and suggestions, we thank three anonymous referees, Aleksander Berentsen, Jose Dorich, Huberto Ennis, Ben Fung, Ricardo Lagos, Peter Norman, Brian Peterson, Tsz-Nga Wong, Randy Wright and seminar participants at the Aarhus University, Bank of Canada, Brock University, Ryerson University, University of Guelph, University of New South Wales, University of Technology Sydney, Wilfrid Laurier University, the 2009 Canadian Economic Association Meetings, the 2009 Chicago Fed Summer Workshop on Money, Banking and Payments, the 2010 Midwest Macro Meetings, the Econometric Society World Congress in Shanghai, the University of Manitoba Delta Marsh Conference on Monetary Economics and the LMDG Conference on Search and Matching. Dong would like to acknowledge …nancial support under Australian Research Council’s Discovery Early Career Researcher Award scheme (project number: DE120102589). The views expressed in this paper are those of the authors. No responsibility for them should be attributed to the Bank of Canada.

1

Introduction

In this paper, we develop a monetary search model with private information and use the model to study how in‡ation a¤ects the seller’s pricing decision and the buyer’s spending

pattern. The model has three main features: buyers are randomly matched with sellers;

buyers experience match-speci…c preference shocks and have private information about the realizations of the shocks; and the terms of trade are determined by sellers making

take-it-or-leave-it o¤ers. This trading protocol is termedprice posting with undirected search in the monetary search literature. "Undirected" captures the feature that buyers cannot choose which sellers to go to (this is in contrast with competitive or directed search, where sellers

post and commit to prices, and buyers observe the prices and direct their search toward

sellers with the best terms of trade). During a match, the seller makes a take-it-or-leave-it o¤er through monopolistic pricing and o¤ers a menu of price-quantity pairs from which the

buyer can choose. The model has a unique monetary equilibrium in which sellers post a

non-linear pricing schedule that exhibits quantity discounts, and buyers spend a fraction or all of their money holdings contingent on the realizations of their preference shocks. There

are two major implications about the e¤ects of in‡ation on trading behaviors: …rst, in‡ation

reduces the extent of non-linear pricing; and second, in‡ation induces buyers to speed up spending, so the model is able to capture the hot-potato e¤ect of in‡ation.

One of our main contributions is to complement the existing search-theoretic monetary literature on price posting with undirected search. Under this trading protocol, monetary

equilibria do not exist with public information. When the nominal interest rate is positive,

buyers incur a costly ex ante investment when they decide to carry money. The existence of monetary equilibria hinges critically on the condition that buyers extract some trading

surplus during the monetary exchange to cover the investment cost. With public

informa-tion, sellers would propose terms of trade to extract the entire trading surplus. Monetary equilibria would unravel as a result. In the literature, private information about

match-speci…c preference shocks has been introduced to restore monetary equilibrium in this class

of models. The presence of private information forces sellers to share some trading surplus with buyers that covers the cost of holding money.

There are three papers that study price posting with undirected search. Jafarey and

Masters (2003) and Curtis and Wright (2004) use the indivisible-money framework of Trejos and Wright (1995). Curtis and Wright (2004) study the case where there are multiple ( 2)

discrete realizations of the preference shock. Jafarey and Masters (2003) assume that the

preference shock follows a uniform distribution. More recently, Ennis (2008) extends price posting with undirected search to a divisible-money framework, as in Lagos and Wright

(2005), with the preference shock following a two-point distribution. In all three papers,

each seller posts a single price (if money is indivisible) or a single price-quantity pair (if money is divisible). At the aggregate level, at most two prices are observed in equilibrium,

make binary choices, spending either nothing or all of their money. Our study complements

the existing literature by considering a model with divisible money and a continuous uniform distribution of the preference shock. The new environment leads to a di¤erent trading

pattern. Instead of o¤ering a single price, sellers post a continuum of price-quantity pairs that exhibits quantity discounts. For buyers, the dichotomous decision to spend nothing

or all is replaced by a continuous choice, with the fraction of spending ranging from 0 to

100%.

The other main contribution of our paper is to provide a useful framework to study

private information in monetary economies. As described in the previous paragraph,

intro-ducing a continuous distribution of the preference shock to a model with divisible money generates more variation in the trading pattern. This feature enables us to analyze how

private information shapes the trading pattern, and how in‡ation a¤ects the trading

be-havior in the presence of private information. In this paper we are particularly interested in two aspects of the trading behavior: the seller’s pricing choice and the buyer’s spending

decision.

About the pricing schedule, our model shows that sellers use quantity discounts to screen buyers who have private information about their willingness to pay. The result has

been generated in non-monetary models, including Maskin and Riley (1984), Che and Gale

(2000), Thomas (2002) and Faig and Jerez (2005). We show that the result continues to hold in a monetary economy. Furthermore, the model generates a new and testable implication

that in‡ation induces more linear pricing. When buyers have private information about their

preference shocks, sellers use quantity discounts to align buyers’ incentives, encouraging those with higher preference-shock realizations to spend more. The cost of the scheme is

that buyers with lower preference shocks are charged higher unit prices, so they buy little

(or not at all). Sellers weigh the bene…ts and costs to determine the optimal level of quantity discounts. When in‡ation is low, buyers choose to hold a large real money balances. The

bene…t from catering to buyers with higher preference shocks is relatively large. Sellers

respond by o¤ering more quantity discounts to increase trading with buyers with higher preference shocks. When in‡ation is high and buyers hold small real money balances,

sellers have limited capacity to extract surpluses from buyers with higher preference shocks. Instead, the optimal strategy is to turn to buyers with lower preference shocks and expand

trading with them. To induce buyers with lower preference-shock realizations to spend more,

sellers reduce the extent of price discrimination (or quantity discounts). Faig and Jerez (2006) show that quantity discounts are also observed in a competitive-search monetary

model. However, their paper does not explore how in‡ation a¤ects the extent of non-linear

pricing.

About the buyer’s spending pattern, our model predicts the hot-potato e¤ect of in‡ation

as an indirect result of the buyer’s choice of money holdings and the seller’s optimal pricing

by reducing the extent of quantity discounts to induce buyers with lower preference shocks

to either start trading or trade more. As a result, the model captures the hot-potato e¤ect along both the extensive margin (as a higher trading probability) and the intensive margin

(as increased fractions of money being spent). The hot-potato e¤ect exists at all levels of in‡ation.

There are several alternative approaches to generate the hot-potato e¤ect in the

litera-ture. In Peterson and Shi (2004), the economy consists of large households, which send a large number of buyers to purchase goods of varying quality. As in‡ation rises, buyers hold

less money in real terms, which reduces the amount of high-quality goods purchased. In

response, households choose as a substitute, and speed up spending on, low-quality goods. Lagos and Rocheteau (2005) show that, under competitive search, moderate in‡ation may

increase the trading surplus of buyers, thereby inducing them to search harder and trade

more frequently. Faig and Jerez (2006) analyze a competitive-search economy where buyers hold private information about their match-speci…c preference shocks. As in‡ation rises,

sellers compete to o¤er buyers ‡atter pricing schedules that reduce the need for

precau-tionary balances. Therefore, buyers with low preference-shock realizations consume and spend more. Ennis (2008) presents a model in which in‡ation induces buyers who are less

likely to consume to exit the market. Those who stay have a higher tendency to spend.

A critical feature in Ennis (2009) is that sellers are better able to avoid in‡ation taxes than buyers. Higher in‡ation makes buyers rush to dump their money to sellers. Liu et al.

(2011) assume that buyers have to pay an entry fee to participate in monetary exchange.

In‡ation reduces buyers’trading surplus, so fewer buyers enter the market, which increases the trading probability of those who enter. Nosal (2011) assumes that accepting a current

trade reduces the probability of future trading. Facing preference shocks, buyers trade only

when their preference-shock realizations are above a reservation shock level. As in‡ation reduces the value of future trading, the reservation shock level falls and buyers are more

likely to accept a current trade.

The rest of this paper is organized as follows. Section 2 describes the environment. In Section 3, we characterize the monetary equilibrium. Section 4 examines the seller’s

pricing behavior and studies how private information and in‡ation a¤ect non-linear pricing. We investigate the e¤ect of in‡ation on the speed of spending in Section 5. Section 6

discusses the e¢ ciency properties of the monetary equilibrium, the model’s results under

an alternative price-posting mechanism –competitive search, and an extension of the model with a more general distribution of the preference shock. Section 7 concludes. Appendix A

provides the technical proofs of Lemmas 1 and 2. Appendix B discusses the situation where

money holdings are unobservable. Appendix C solves the model under competitive search. Appendix D illustrates the role of private information in generating non-linear pricing in

models with Nash bargaining and competitive search. Appendix E discusses the model’s

2

Environment

The model is based on Rocheteau and Wright (2005). Time is discrete and runs from 0to

1. A decentralized market (DM) and a centralized market (CM) open sequentially in each period. There is one non-storable good in each market: a DM good(q) and a CM good(x).

The discount factor between two periods is 2 (0;1). There are two permanent types of agents: buyers and sellers, distinguished by their roles in the DM. Each type is of measure

1.

In the DM, agents are anonymous. Buyers are those who want to consume but cannot produce. Sellers can produce but do not want to consume. This generates a lack of double

coincidence of wants, which, together with anonymity, makes money essential as the medium

of exchange. By consuming q units of the DM good, a buyer derives utility eu(q); where

e 0is a preference parameter that determines the buyer’s marginal utility of consumption.

The functionu(q) satis…esu(0) = 0,u0>0> u00 and u0(0) =1. For a seller, the disutility

of producingq units of the DM good is equal toq. Buyers and sellers are randomly matched and the matching function is such that one buyer meets one seller with probability 1. All

buyers are ex ante identical before the matches. Ex post, they are subject to

match-speci…c preference shocks and become heterogeneous during their matches with sellers. The realization of e follows a uniform distribution on the interval [0;1].1 Money balances are

assumed to be public information. However, buyers hold private information about the realizations ofe. The …rst-best allocationqe is characterized byeu0(q

e) = 1for alle2[0;1]. The terms of trade in the DM are determined by sellers making take-it-or-leave-it o¤ers.

In a match, the seller sets monopoly prices, taking as given the buyer’s money holding and the fact that the buyer has private information about his or her preference shock. In

the monetary search literature, this trading protocol is calledprice posting with undirected search. The critical feature of the trading mechanism is that buyers choose money holdings and are matched with sellers before observing sellers’ prices.2 As a result, buyers cannot

direct their search toward sellers with more favorable terms of trade (as under competitive

search). The timing makes it possible for the seller to engage in monopolistic pricing. The CM is a centrally located competitive spot market. In the CM, all agents can

consume or produce the CM good x. The utility from consumingx units of the CM good

isx. Ifx <0, it means that the agent produces and incurs disutility.3

Fiat money is supplied by the monetary authority. The money supply Mt grows at a

constant (gross) rate . New money is used to …nance a lump-sum transfer to buyers

1

In Section 6.3 and Appendix E, we show that the main results of the paper continue to hold with a more general speci…cation of the distribution of the preference shock.

2The critical assumption is that the buyer observes the prices after being matched. The seller could post prices either before or after the match.

at the beginning of each CM. Let Tt= ( 1)Mt 1 be the amount of nominal transfer to

each buyer.

In each trading cycle of a CM succeeded by a DM, the sequence of events can be described

concisely as follows. In the CM, agents receive money transfers, produce or consumex and choose money balances. In the DM, buyers and sellers are randomly matched. Upon

matching, the buyer receives the preference shock and observes the terms of trade posted

by the seller. Finally, the buyer decides how much to trade.

3

Equilibrium

To solve for the monetary equilibrium, we begin by analyzing choices in the CM and then

consider decisions in the DM.

3.1 Decision Making in the CM

In the CM, agents rebalance their money holdings by trading money for the CM good, x,

or vice versa. We …rst consider a buyer’s problem. Let Wb(m) denote the buyer’s value function while entering the CM with m units of money. Let Vb( ^m

+) be the buyer’s value

function at the beginning of the following period’s DM, where m^+ is the buyer’s choice of

money holding to enter the DM. The buyer’s problem is described as

Wb(m) = max

x;m^+

h

x+ Vb( ^m+)

i

s.t. x = (m+T m^+);

where is the value of money (in terms of good x) in the CM. De…ning z= m, = T

and z^+ = +m^+;we can rewrite the buyer’s problem in real terms as

Wb(z) = max

^

z+

z+

+

^

z++ Vb(^z+) .

Note that, due to the assumption of quasilinear preferences, the choice ofz^+is independent

of zand Wb(z) is linear inzwith dWb(z)=dz = 1. The …rst-order condition is

dVb(^z+)

dz^+

=

+

ifz^+>0:

For a seller who holds z and z^+ units of real money balances upon entering the CM

and the next DM, let Ws(z) and Vs(^z+) be his or her value functions at the beginning

of CM and DM, respectively. It is a standard result that if the nominal interest rate is positive, the seller spends all the money accumulated in the previous DM on the CM good

x and carries 0money balance to the following DM. The seller’s value function is given by

3.2 Decision Making in the DM

In the DM, the seller posts a menu of price-quantity pairs (qe; ze) for all e 2[0;1]. Here,

qe represents the quantity of trading andze represents the required money payment in real terms. We assume that the seller can observe z^, the buyer’s money balance, so that the

seller’s posting may depend on z^. The matching function is such that each buyer meets a

seller with probability 1. Upon matching, the match-speci…c preference shock is realized and is the buyer’s private information. After seeing the seller’s posting, the buyer decides

whether to trade, and if he or she trades, which (qe; ze) to take.

The seller’s choice of pricing schedule is in essence a mechanism design problem, where the seller is the principal and the buyer is the agent with private information about his or

her preference shock. We can apply the revelation principle to formulate the seller’s problem

as follows: taking the buyer’s money balance,z^, and the distribution of the preference shock as given, choose(qe; ze)e2[0;1] to maximize his or her DM value function. Formally,

Vs(0) = max

fqe;zege2[0;1]

Z 1

0

[ qe+Ws(ze)]de; (1)

s.t. 8 > > > > > > > < > > > > > > > :

qe 0,

ze z^,

eu(qe) ze eu(qe0) ze0 for alle; e0 2[0;1],

eu(qe) ze 0.

(NC)

(CC)

(IC)

(PC)

The four sets of constraints are the non-negativity constraints (NCs), the cash constraints (CCs), the incentive constraints (ICs) and the participation constraints (PCs), respectively.4

The formulation of the ICs and the PCs uses the property that Wb(z) is linear in z. To

solve the problem, we proceed as follows.

First, note that we can ignore the PCs for alle >0because they are implied by the PC

fore= 0and the ICs. In addition, note that the PC binds for buyers with e= 0. Finally,

using the result from Mas-Collell et al. (1995, Proposition 23.D.1, page 888), we transform the ICs in Lemma 1.

Lemma 1 De…neve eu(qe) zeas the buyer’s ex post trading surplus when the realization

of the preference shock is e. The incentive constraints (IC) hold if and only if

dqe=de 0; (IC1)

dve=de=u(qe): (IC2)

4

Proof. See Appendix A.

Using the results above, we can restate the seller’s problem as an optimal control problem withve as the state variable and qe as the control variable:

max

fqe;vege2[0;1]

Z 1

0

[ qe+eu(qe) ve]de,

s.t. 8 > > > > > > > > > > < > > > > > > > > > > :

qe 0, (NC)

eu(qe) ve z^, (CC)

dqe=de 0, (IC1)

dve=de=u(qe), (IC2)

v0 = 0, (PC)

where the seller’s objective function is rewritten by using the property thatWs(z) is linear

inz. The solution to the seller’s problem is a schedule of (qe; ze)e2[0;1] as a function ofz^.

De…ne z as

z= 1

2[u(q1) +q1] (2)

where q1 solves u0(q1) = 1. The interpretation of z is the amount of real money balance

charged to a buyer who has e = 1 and buys q1. Lemma 2 fully characterizes the seller’s

optimal pricing schedule as a function of the buyer’s money holding, z^.

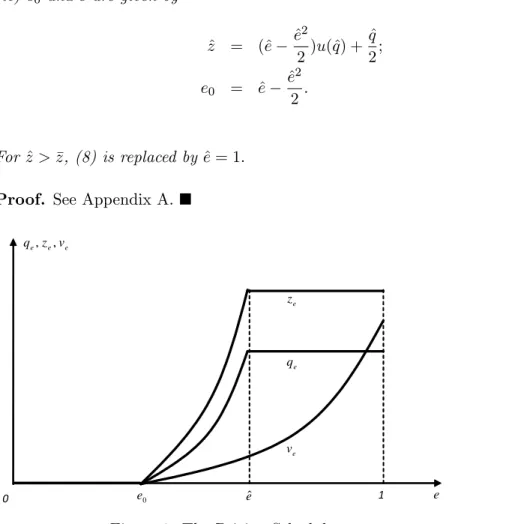

Lemma 2 For any givenz^ z, the solution[qe(^z); ve(^z); ze(^z)]e2[0;1] to the seller’s pricing

problem is unique and is characterized by: (i) for e2[0; e0], qe=ze=ve= 0;

(ii) for e2[e0;e^],

qe : (2e 2^e+ ^e2)u0(qe) = 1; (3)

ve : ve= e ^e+

^

e2

2 u(qe)

qe

2; (4)

ze : ze = ^e

^

e2

2 u(qe) +

qe

2; (5)

(iii) for e2[^e;1],

qe : qe= ^q where e^2u0(^q) = 1; (6)

ze : ze= ^z; (7)

(iv) e0 and ^eare given by

^

z = (^e ^e

2

2)u(^q) + ^

q

2; (8)

e0 = ^e

^

e2

2: (9)

For z > z^ , (8) is replaced by ^e= 1:

Proof. See Appendix A.

e e e z v

q , ,

e

0

e eˆ

e

z

e

q

e

v

1 0

Figure 1: The Pricing Schedule

For a given z^, the seller’s optimal pricing schedule (qe; ze)e2[0;1] is such that buyers

with low preference-shock realizations (e 2 [0; e0)) do not consume at all; buyers with

intermediate preference-shock realizations (e2(e0;^e)) consume positive amounts and spend

part of their money; and buyers with high preference-shock realizations (e2[e0;1]) spend

all their money on consumption. Figure1 illustrates the solution to the seller’s problem.

3.3 Monetary Equilibrium

After solving the seller’s optimal pricing schedule in the DM, we go back to the CM to derive the buyer’s demand for money. Plugging the optimal pricing schedule into the buyer’s DM

value function, we have

Vb(^z) = Z 1

0

[eu(qe(^z)) + ^z ze(^z)]de+Wb(0)

whereS(^z) is the buyer’s expected trading surplus in the DM, and can be expressed as

S(^z) = Z 1

0

ve(^z)de

= Z e^

e0

"

e e^(^z) +e^(^z)

2

2 !

u(qe(^z))

qe(^z) 2

#

de+

Z 1

^

e

[eu(^q(^z)) z^]de:

Note that since e0, ^e, qe2[e0;^e] and q^ are all smooth functions of z^ following Lemma 2,

S(^z) is a also a smooth function of z^. In the CM, the buyer chooses z^+ to maximize

fz+ ( = +)^z++ [S(^z+) + ^z++Wb(0)]g, or equivalently,fS(^z+) [( = +)= 1]^z+g.

We will focus on the stationary equilibrium, where z^is constant and the in‡ation rate

= + is equal to . Let i = = 1 be the nominal interest rate implied by the Fisher

equation. We can rewrite the buyer’s choice of money holding as

max

^

z S(^z) iz^.

The choice of z^satis…es the …rst-order condition

S0(^z) =i: (10)

De…nition 1 A stationary price-posting monetary equilibrium is a list of [qe(^z); ze(^z)] for

all e 2 [0;1] and z^ such that (i) [qe(^z); ze(^z)] maximizes Vs(0) given z^ (characterized by (3),(5),(6),(7), (8) and (9); and (ii) z^maximizes S(^z) iz^(and satis…es (10)).

In the following, we discuss the properties of the functionS(^z). The …rst-order derivative

is

S0(^z) = Z ^e

e0

dve<^e(^z)

dz^ de+

Z 1

^

e

dve ^e(^z)

dz^ de: (11)

Fore <^e, the ex post trading surplus is ve<^e= e e^+ ^e2=2 u(qe) qe=2. The e¤ect of z^ on ve is captured by

dve<e^

dz^ = (^e 1)u(qe)

d^e dz^ <0;

where

de^

dz^ =

1

(1 e^)u(^q) + ^eu0(^q)dq^

de^

>0; (12)

follows from (8) and (6), and

dq^

de^=

2^e[u0(^q)]2

u00(^q) >0: (13)

is derived from (6).

captured by

dve ^e

dz^ =eu

0(^q)dq^

dz^ 1 =

eu0(^q)

(1 ^e)u(^q)u00(^q)

2^e[u0(^q)]2 + ^eu0(^q)

1:

The term dve ^e=dz^ is negative when e = ^e. Notice that the buyer would never increase

the money holding to the point where he or she is made worse o¤ in all realizations of e; therefore, in equilibrium,ve0(^z) must be positive fores that are high enough. Lete <^ e <~ 1

be the solution to dve e^=dz^= 0. The e¤ect ofz^is such thatdve=dz <^ 0 fore2[e0;~e] and

dve=dz >^ 0 for e2 [~e;1]. In other words, as z^ increases, buyers with low realizations ofe are hurt, while those with high realizations ofeare better o¤.

We can summarize the e¤ect ofz^on the buyer’s expected trading surplus by substituting the expressions ofdve=dz^into (11),

S0(^z) = (1 e^) d^e

dz^ [^eu(^q) z^] + 1 + ^e

2 u

0(^q)dq^

d^e 1 : (14)

The bene…t of a higherz^is that it relaxes the cash constraint and allows the buyer with a

high realization of eto buy more. At the same time, the buyer with a low realization ofe

receives worse terms of trade and is made worse o¤. The bene…t dominates when z^and q^

are small and the cash constraint is more binding. Asz^becomes big, the loss dominates.

Lemma 3 Properties of S(^z) : (i)S0(0) = +1;(ii) S0(^z z) = 0;and (iii)S00(z)>0.

Proof. Using (12), rewrite (14) as

S0(^z) = (1 e^) (

[^eu(^q) z^] + 1+^2eu0(^q)dq^

de^

(1 e^)u(^q) + ^eu0(^q)dq^

de^

1 )

.

When z^= 0, we have ^e= ^q = 0 and

S0(0) = 1

2^e 1 =1.

When z^=z, we have e^= 1,u0(^q) = 1 orq^=q 1 and

S0(z) = (1 ^e) (

[u(^q) z^] +u0(^q)ddqe^^

u0(^q)dq^

d^e

1 )

= (1 ^e)[u(q1) z] u

00(q 1)

2u02(q 1)

| {z }

…nite

= 0:

According to Lemma 2, the terms of trade do not respond to z^ any more if z > z^ . As a

result,S0(^z >z^) = 0.

atz=z. At z^=z, we have e^= 1,u0(^q) = 1, and dq=d^ z^= 1. Thus, we arrive at

S00(z) = de^

dz^ 1 2u

0(q 1)

dq^

dz^+ 1 + 1

2[u(q1) c(q1)]

de^

dz^

= de^

dz^ 1 2+

1

2[u(q1) c(q1)]

d^e dz^ >0:

One direct implication of S0(^z z) = 0 is that buyers will not choose to hold z > z^ :

oncez^exceedsz, the net bene…t from holding more real money balances,S0(^z) i, is either 0 (if i= 0) or negative (if i > 0). As a result, we can restrict our attention to0 z^ z

while considering the buyer’s demand for z^.

Proposition 1 For generic values of <1; there exists a unique monetary equilibrium with 0<z < z^ and dz=d <^ 0.

Proof. Given that Lemma 2 establishes that there is a unique solution to the seller’s optimal-pricing problem givenz^, it remains to prove that there is a unique solution to the

buyer’s demand for real money balances.

First we prove 0<z < z^ . We have z >^ 0because S0(0) =1. Following S0(z) = 0 and

S00(z)>0, we knowS0(^z) i <0 forz^in the left neighborhood ofz and, therefore,z < z^ .

Now we prove that the solution to the buyer’s demand for real money balances exists

and is unique for generic values of . Given that S0(0) = 1 and S0(^z) i <0 in the left neighborhood ofz, by the Intermediate Value Theorem, there exists a solution0<z < z^ to

the …rst-order condition S0(^z) =i. If the solution is unique, it is automatically the unique

maximizer. One can show that this is the case if buyers have constant relative risk aversion (CRRA) withu(q) =q = (0< <1). For general utility functions, given the complicated

forms taken byS andS0, there may exist multiple solutions toS0(^z) =i. However, because

S0(^z)does not directly depend oni, we can still prove uniqueness using the same approach as in Wright (2010). The argument is as follows. The multiple solutions to S0(^z) = i

could be either local maximizers or local minimizers. Among the local maximizers, only

one solution is selected as the unique global maximizer for generic values of .

In terms of the e¤ect of on z^, notice that the global maximizer satis…es S00(^z) < 0.

From (10),dz=d^ = 1=[ S00(^z)]<0 for generic values of .

Proposition 1 establishesdz=d <^ 0for generic values of the in‡ation rate. If we sacri…ce

di¤erentiability, we can state the result that in‡ation reduces the equilibrium real money

holding for any < 1. In the special cases where takes non-generic values leading to multiple global maximizers, buyers may hold di¤erent amounts of money. However, as

argued in Wright (2010), the global maximizer can only decrease with . While drawing the

aggregate money demand curve, we can treat the points with non-generic values of (or

i) by assigning any fraction of buyers to each of the multiple global maximizers. Then the

everywhere except for a measure0 of non-generic values of . At these non-generic values

of , the aggregate demand curve consists of vertical segments. Given any money-supply curve (here, any given in‡ation rate or nominal interest rate), the equilibrium aggregate

money holding must decrease with the in‡ation rate.5 Besides making the equilibrium money holding non-di¤erentiable with respect to the in‡ation rate, another complication

raised by non-generic values of is that multiple sets of pricing schedules may be observed

if buyers choose to hold di¤erent amounts of money corresponding to the multiple global maximizers.

Jean et al. (2010) show that the existence of multiple equilibria is quite robust in

mon-etary models under price posting if the buyer chooses money holding and the sellers posts pricing schedules simultaneously without observing each other’s choice. In our framework,

sellers post prices after observing buyers’ money holdings. There are no multiple

mone-tary equilibria arising from coordination. In Appendix B, we show that multiple monemone-tary equilibria arise if money holdings are unobservable. This issue is also discussed in Ennis

(2009).

We next highlight two features of the monetary equilibrium in our model and compare them with existing papers on price posting with undirected search; i.e., Jafarey and Masters

(2003), Curtis and Wright (2004), and Ennis (2008). First, given that the buyer chooses a

positive amount of money holding, the seller posts a continuum of price-quantity pairs with measure ^e e0, which implies a continuum of real unit pricespe2[e0;e^]:

pe=

ze

qe

= e^ e^

2

2

u(qe)

qe +1

2: (15)

In previous studies, each seller posts a single price, and the law of two prices established

by Curtis and Wright (2004) holds at the aggregate level. Our analysis shows that these previous results are due to the assumption of indivisible money or a two-point distribution

of the preference shock: the results are overturned with the combination of divisible money

and a continuous distribution of the preference shock.6 The result that the seller posts more than one price allows us to study several interesting questions. Is there non-linear pricing?

What is the role of private information? How does in‡ation a¤ect the extent of non-linear

pricing? We answer these questions in Section 4.

The second feature that we highlight is that, in our model, buyers spend various amounts

of money, with the fraction of spending ranging from0to100%. Buyers with e2[0; e0]do

5

Note that according to Lemma 2, e0;^e;q; qe^ 2(e0;^e) and ze2(e0;e^) are all smooth functions ofz, so the^

only source of discontinuity of these variables as functions of is the discontinuity of the function z^( ). Note also that the discontinuity of^z( )only a¤ects the di¤erentiability, but not the monotonicity, of these functions. In the rest of the paper, we de…ne the comparative-statics derivatives with respect to only for generic values of . However, all of our comparative-statics results hold for all values of if we replace the comparative-statics derivatives with descriptive statements such as "z^increases with ".

not spend at all. For those with e2[^e;1], the cash constraint binds and the entire money

holdings are exhausted during exchange. Buyers withe2(e0;e^)spend part of their money

holdings, and qe and ze increase with e. The continuous spending pattern is in contrast

to the binary choice of spending either nothing or everything in earlier papers on price posting with undirected search. The variation in the fraction of spending makes the model

a suitable framework in which to address how in‡ation a¤ects the speed of spending. The

coexistence of buyers who spend nothing and those who spend various positive amounts of money implies that the model can be used to study how in‡ation a¤ects trading along both

the extensive (the probability of spending) and intensive (the amount of spending) margins.

We address these issues in Section 5.

4

Non-linear Pricing

As long as < 1, buyers choose to hold a positive amount of money and sellers post a continuum of price-quantity pairs (qe; ze)e2[e0;^e], which may imply di¤erent unit prices. In

this section, we examine the pricing schedule in more detail. We begin by investigating

whether the pricing schedule involves non-linear pricing. If there is non-linear pricing, we analyze the role played by private information in generating the result. Finally, we explore

how in‡ation a¤ects the pricing schedule in the presence of private information.

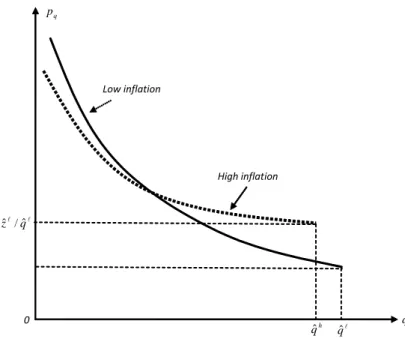

The unit price paid by a buyer witheis calculated in (15). To study non-linear pricing, we can alternatively express the unit price,pe, as a function of the quantity, qe:

pq = e^

^

e2

2

u(q)

q +

1 2:

The derivative dpq=dq captures the degree of non-linear pricing,

dpq

dq = ^e

^

e2

2

qu0 u

q2 <0:

Aspqdecreases inq, the model suggests that quantity discounts are observed in equilibrium.

The result is stated in Proposition 2.

Proposition 2 Quantity discounts: dpq=dq <0.

Private information plays two important roles in the model. The …rst is to prevent sellers

from extracting the entire trading surplus and, in turn, to ensure the existence of monetary equilibria. This role is restricted to models with price posting and undirected search (or

monopoly pricing). The second is to shape the pricing schedule. Private information forces sellers to use quantity discounts to screen buyers with di¤erent willingness to pay and induce

those with higher marginal utilities to buy more.

bargaining with public information, (ii) competitive search with public information, and (iii)

competitive search with private information. In addition, Faig and Jerez (2006) present another version of the competitive-search monetary model where buyers hold private

in-formation about their match-speci…c preference shocks.7 We …nd that private informa-tion is essential for generating the quantity-discount result if the utility funcinforma-tion satis…es

d[u=(qu0)]=dq 0.8

The result that private information leads to quantity discounts can also be found in non-monetary models; examples are Maskin and Riley (1984), Che and Gale (2000), Thomas

(2002) and Faig and Jerez (2005). Compared with a non-monetary model, a new feature of a

monetary model is that the buyer’s budget constraint is endogenously a¤ected by in‡ation. Since the seller’s pricing schedule depends on the buyer’s money holding, we can use the

model to study how the extent of quantity discounts is a¤ected by in‡ation.9 The e¤ect of

in‡ation on the extent of non-linear pricing is captured by

d[dpq=dq]

d = (1 e^)

qu0 u

q2

| {z }

d^e dz^

dz^

d

| {z }

>0.

Proposition 3 E¤ ect of in‡ation on quantity discounts: for generic values of ,d[dpq=dq]=d

>0.

Proposition 3 states that the extent of quantity discounts decreases with in‡ation. When

buyers have private information about their preference shocks, quantity discounts allow

sell-ers to induce buysell-ers with high preference shocks to spend more and extract more trading surplus from them. The trade-o¤ is that it reduces purchases from buyers with low

pref-erence shocks. When in‡ation is low, buyers hold large real money balances. It is more

pro…table for sellers to extract surplus from buyers with higher preference shocks (by in-ducing them to spend more). The bene…t of applying steeper quantity discounts outweighs

the loss of trading surplus from buyers with low preference shocks. When in‡ation is high

and buyers hold very small real money balances, the seller has limited capacity to extract surpluses from buyers with high preference shocks and starts to rely on buyers with lower

preference shocks for pro…ts. To induce buyers with lower preference shocks to spend more, the seller lowers the extent of price discrimination. The e¤ect of in‡ation on quantity

discounts is depicted in …gure2.

7

The competitive-search model we study allows the buyer to walk away without trading so ex post participation constraints have to be satis…ed. Faig and Jerez (2006) assume that buyers can commit to trading even if their ex post trading surplus is negative. See Section 6.2 for further discussion.

8

Environments (i) and (ii), which feature public information about the preference shock, lead to quantity premiums (linear pricing) if d[u=(qu0)]=dq > (=) 0. In contrast, in our model, environment (iii) and the

model in Faig and Jerez (2006), where there is private information about the preferenc shock, quantity discounts are always observed irrespective of the sign ofd[u=(qu0)]=dq.

9

q p

q

l

qˆ 0

High inflation Low inflation

h qˆ l

l

q zˆ/ˆ

Figure 2: E¤ect of In‡ation on Quantity Discounts

5

Hot-Potato E¤ect of In‡ation

The model has the feature that buyers hold precautionary money balances and may spend nothing, part or all of their money during exchange. This allows us to study how in‡ation

a¤ects the speed at which buyers spend their money. The results are stated in Propositions

4 and 5.

Proposition 4 E¤ ects of in‡ation on (e0;^e) and qe for e 2 (e0;e^): for generic values of

, de0=d <0,de=d <^ 0, anddqe=d >0.

Proof. From (9),

de0

dz^ = (1 e^)

d^e

dz^ >0: (16)

Recall from Proposition 1 thatdz=d <^ 0. Using (12) and (16), we can show thatde0=d <0

and de=d <^ 0. From (3), we have

dqe

de^ =

2(1 ^e)[u0(qe)]2

u00(qe) <0:

It then follows thatdqe=d = (dqe=de^)(de=d^ )>0:

Proposition 5 E¤ ects of in‡ation on (ze; ze=z^) for e 2 (e0;e^): for generic values of ,

Proof. From (5) we have

dze

de^ = eu

0(qe)dqe

d^e + (1 ^e)u(qe)

< e^2u0(^q) | {z }

=1

2(1 ^e)[u0(qe)]2 ^

eu00(qe) + (1 ^e)u(qe)

= (1 e^) 2 ^

e

[u0(qe)]2

u00(qe) +u(qe) :

In Section 3 we argued that ve0(^z) must be positive for e ~e with e <^ ~e < 1. Using

v10(^z) > 0, we can show that 2u0(^q)2=[^eu00(^q)] +u(^q) < 0. If u(q) is CRRA, the term

u0=(u00u) is constant. As a result,dze=d^e <0. In addition, dze=d = (dze=d^e)(de=d^ ) >0.

We have d(ze=z^)=d >0because dze=d >0and dz=d <^ 0.

Alternatively, we can also prove the comparative statics result in Proposition 5 under the assumption 2u02 +u00u > 0. In general, we always have ze and ze=z^ increasing for

some buyers in response to higher in‡ation, because e0 and e^decrease with in‡ation. The

additional assumption of CRRA utility functions or2u02+u00u >0makes the e¤ect stronger such thatdze=d >0 for alle2(e0;e^).

Conventional wisdom holds that people tend to spend money faster as in‡ation rises (see,

for example, Keynes, 1924). This phenomenon is often referred to as the hot-potato e¤ect of in‡ation. Our model’s prediction is consistent with the observation. Although in‡ation

induces buyers to carry less real cash balances so that those who are cash constrained

(e e^) consume less (which is a standard result in monetary models), buyers who are not cash constrained respond in the opposite direction by consuming more. As shown in

Proposition 4, in‡ation induces more buyers to start trading (captured as a decrease in

e0); we label this the extensive-margin e¤ect. Meanwhile, there is also the intensive-margin

e¤ect as buyers who are not cash-constrained increase their spending: the amount of goods

being purchased (qe), the real balances being spent (ze) and the fraction of money being spent (ze=z^) all increase for e 2(e0;e^). Because more people start to spend, more people

become cash constrained and spend everything, and those who are not cash constrained

e q

e

1 0

e

1 0

e z

e l

eˆ 1

0 h

e0

h eˆ

l

0

e z

ze/ˆ

High inflation High inflation High inflation

Low inflation

l eˆ

h e0

h eˆ

l

0

e

l eˆ

h e0

h eˆ

l

0

e

Low inflation

Low inflation

Figure 3: Hot-Potato E¤ect of In‡ation

In the following, we compare our paper with other existing papers about the hot-potato

e¤ect of in‡ation. Broadly speaking, there are three approaches to generate this e¤ect. The …rst is to construct models where in‡ation a¤ects the buyer’s matching probability.

Lagos and Rocheteau (2005) endogenize search intensity. They show that when in‡ation

is low and the terms of trade are determined by competitive search, in‡ation may increase a buyer’s trading surplus. In response, buyers search more intensively, which increases the

probability of matching/spending. The result, however, holds only for low in‡ation and

a particular trading mechanism – competitive search. Bargaining cannot deliver similar results, because in‡ation monotonically reduces the buyer’s surplus in a match and thus

the search intensity. Liu et al. (2011) assume that buyers have to pay an entry fee to participate in the DM. Under Nash bargaining, in‡ation reduces buyers’trading surplus, so

fewer buyers enter the DM. For those who do enter, the matching probability increases. The

result that the buyer’s matching probability increases with in‡ation depends critically on the assumption that buyers pay the entry fee. If sellers pay the entry fee, as in Rocheteau

The second approach is described by Ennis (2009). Key to this approach is the

assump-tion that buyers can access the CM to rebalance money holdings only every two periods, so they hold enough money to spend in two DMs. Sellers, on the other hand, have access to

the CM in every period and therefore are better able to avoid the in‡ation tax. Whenever the nominal interest rate is positive, there is a wedge between the valuations of money by

sellers and buyers who are in the …rst DM. To avoid in‡ation taxes, buyers consume more

in the …rst DM than in the second DM. The extent of frontloading increases with in‡ation. Furthermore, Ennis (2009) also endogenizes search intensity and creates an additional

chan-nel of the hot-potato e¤ect: in‡ation makes buyers search harder in order to …nd sellers to

dump money to them.

The common feature of the third approach is to introduce match-speci…c preference

shocks. The preference shock induces buyers to hold precautionary balances, and the

frac-tion of spending depends on the realizafrac-tion of the shock. Besides our paper, others who follow this approach include Peterson and Shi (2004), Faig and Jerez (2006), Nosal (2011)

and Ennis (2008). Each paper presents a di¤erent channel to generate the hot-potato e¤ect

of in‡ation.

In our model, the hot-potato e¤ect is an indirect result of the buyer’s choice of money

holdings and the seller’s optimal pricing strategy. The seller acts as a monopolist to extract

trading surplus from buyers who are budget constrained and have private information about their willingness to pay. Sellers maximize pro…ts by o¤ering quantity discounts to induce

buyers with higher preference shocks to buy more. As in‡ation rises, buyers choose to

carry less real money balances and have a smaller budget. For sellers, buyers with lower preference shocks become a more important source of pro…t. As a result, sellers respond by

reducing the extent of price discrimination (or quantity discounts) to induce buyers with

lower preference shocks to either start trading (the extensive margin) or trade more (the intensive margin).

As in our model, Peterson and Shi (2004), Faig and Jerez (2006) and Nosal (2011) have

uniformly distributed preference shocks. Peterson and Shi (2004) use the large-household monetary model, as in Shi (1997). Each household sends a large number of buyers to

purchase goods of varying quality. During a match, the buyer makes a take-it-or-leave-it o¤er and purchases more when the good is of higher quality. In‡ation reduces the demand

for real money balances. Buyers have a smaller budget, which reduces the amount of

high-quality goods households can buy. As a result, households choose low-high-quality goods as a substitute. In some meetings, the quantity of goods traded and real cash balances in

exchange increase. The model captures the hot-potato e¤ect along the intensive margin. In

the model, buyers always purchase a positive amount irrespective of the in‡ation rate, so there is no extensive margin.

In Faig and Jerez (2006), the terms of trade in the DM are determined by competitive

trading surplus, the model does not generate the extensive-margin e¤ect. As in‡ation

rises, competition among sellers forces them to post schedules that reduce the need for precautionary balances, inducing buyers with low preference-shock realizations to consume

more. The model can therefore capture the hot-potato e¤ect along the intensive margin. Nosal (2011) assumes that accepting a current trade reduces the probability of future

trading (consider the purchase of durable goods). As a result, buyers trade only when the

realizations of their preference shocks are above a reservation preference shock level. As in‡ation reduces the value of future trading, the reservation preference shock level falls

and buyers are more likely to accept current trades. The model can therefore capture the

hot-potato e¤ect along the extensive margin. Once buyers decide to trade, they make take-it-or-leave-it o¤ers to sellers. An unconstrained buyer always purchases the socially e¢ cient

quantity of goods (qe =qe), and the amount of money that the buyer spends is just enough

to compensate the seller for his or her disutility from production (ze=qe). That is, qe and

ze do not increase with in‡ation, as in our model (the fraction of money being spent does

increase due to a lowerz^).

In Ennis (2008), the preference shock follows a two-point distribution. There are ex ante heterogeneous agents who di¤er in the probability of receiving a high shock. In equilibrium,

those who receive a high realization of the shock choose to trade and spend all their money,

while those with a low realization of the shock choose not to trade at all. In‡ation causes agents with a lower probability of receiving the high shock to withdraw from the market.

As a result, those who choose to participate have a higher probability of receiving a high

shock, and the probability of trading is higher. Ennis (2008) captures the hot-potato e¤ect only along the extensive margin.

6

Discussion

In this section, we analyze the e¢ ciency properties of the monetary equilibrium under price

posting and undirected search. We also discuss our main results under an alternative

price-posting mechanism where buyers engage in directed search. Finally, we consider a more general distribution of the preference shock.

6.1 E¢ ciency

The …rst-best allocation (characterized by eu0(qe) = 1) cannot be achieved in the mon-etary equilibrium (refer to equation (3)). There are three sources of distortion: private

information, the trading mechanism and in‡ation.

As discussed in the Introduction, the presence of private information actually improves welfare under price posting with undirected search. It prevents the seller from exploiting

the entire trading surplus and gives the buyer an incentive to hold positive money balances.

To understand the ine¢ ciency caused by the trading mechanism, we can follow Hu et al.

(2009) and Rocheteau (2012), who study the optimal mechanism in the Lagos and Wright (2005) environment. The approach is to keep the competitive market structure in the CM,

but adopt an optimal mechanism in the DM. Rocheteau (2012) also discusses the situation where buyers hold private information about their match-speci…c preference shocks. One

can show that there exist mechanisms to achieve the …rst-best allocation if the nominal

interest rate or the in‡ation rate is not too high, or more speci…cally, ifi { with{solving

Z 1

0

[eu(qe) qe]de={q1.

The condition guarantees that the expected total trading surplus at the …rst-best allocation

is su¢ cient to cover the cost of holding enough money to support the purchase of q1. One

optimal mechanism is such that, if, during a match, a buyer holds at least q1 units of real cash balances, the buyer makes a take-it-or-leave-it o¤er and reaps the entire trading

surplus: this gives the buyer the incentive to truthfully reveal his or her preference and

solves the problem of private information. If the buyer holds less thanq1, the seller makes a take-it-or-leave-it o¤er and gets the entire trading surplus: this gives the buyer the incentive

to hold the socially optimal amount of money balances. In contrast, under price posting

with undirected search, the …rst-best allocation can never be implemented. Buyers always consume strictly less than the socially optimal level, except for buyers with e = 0, who

always consume 0.

Regarding the cost of in‡ation in our model, …rst note that as in‡ation rises,qeincreases

for buyers withe <^eand loose cash constraints, which increases total welfare, and decreases

for buyers withe e^and binding cash constraints, which reduces total welfare. Addition-ally, in‡ation reduces e0, so that more buyers consume in the DM. This extensive-margin

e¤ect tends to increase welfare. Therefore, in‡ation may be bene…cial for the economy,

especially when in‡ation is low, or when z^ is high and the cash constraint is less binding. In general, it is di¢ cult to analytically sign the e¤ect of in‡ation on total welfare. We have

conducted various numerical examples with CRRA utility functions, all of which suggest

that in‡ation reduces welfare. The reason may be that the trading mechanism is very dis-tortionary and buyers always choose to hold a small amount of money, so z^is never large

enough for the bene…t of in‡ation to dominate. Even at the Friedman rule withi= 0, we

have z < z^ ande <^ 1.

6.2 Competitive Search

Another price-posting trading protocol used in the literature is called competitive search

or price posting with directed search. The main di¤erence between competitive search and the trading protocol considered in this paper is whether buyers observe prices before

search, sellers advertise/post prices and buyers observe the prices before the choice of money

holdings and matching. Buyers can thus direct search toward sellers o¤ering the best terms of trade, which creates competition among sellers. Under price posting with undirected

search, buyers observe prices only after they are matched with sellers. This allows the seller to engage in monopolistic pricing.

We explore the model’s implications under competitive search. To do this, we keep all

other features of the model …xed except for the timing of events. In each trading cycle of a CM succeeded by a DM, the sequence of events can be described concisely as follows. In

the CM, agents receive money transfers. Sellers post terms of trade, which they commit

to follow in the DM. Observing the terms of trade posted by sellers, buyers choose money balances and consume or produce x. In the DM, buyers direct search toward sellers who

post the best terms of trade and enter into the matching process. Upon meeting, the buyer

receives the match-speci…c preference shock and decides how much to trade. As before, we assume that buyers cannot commit to trade and may choose to walk away without trading.

In Appendix C, we illustrate the steps to solve the model under competitive search.

Similar to the case with undirected search, sellers post a continuum of price-quantity pairs and use quantity discounts to screen buyers with di¤erent realizations of the match-speci…c

preference shocks. Buyers still hold precautionary balances and choose to spend a fraction

of money ranging from 0 to 100%, depending on the realizations of their willingness to pay. The model is, in general, too complicated to solve analytically. We have conducted

extensive numerical exercises with CRRA utility functions and found that all our main

results continue to hold under competitive search. In‡ation reduces the extent of non-linear pricing. As in‡ation rises, more buyers trade, and some buyers trade a higher quantity and

spend a higher amount of real cash balances. Therefore, the model can also capture the

hot-potato e¤ect along both the extensive and intensive margins.

Faig and Jerez (2006) study a very similar model of competitive search with one

im-portant modelling di¤erence. They assume that agents can commit to trading even if the

ex post trading surplus is negative, while we maintain the ex post participation constraints ensuring that all agents get non-negative surpluses. One implication of the modelling

dif-ference is that buyers always spend in Faig and Jerez (2006), so they can capture the hot-potato e¤ect only along the intensive margin. Faig and Jerez (2006) do not explore how

in‡ation a¤ects the extent of non-linear pricing. Instead, they are mainly concerned about

two points. The …rst is the mechanism through which in‡ation distorts allocation in the presence of private information versus the case with public information. The second is how

the introduction of private information improves the model’s …t of historical U.S. data on

6.3 Extension to More General Distribution of the Preference Shock

The previous analysis assumes that the preference shock follows a uniform distribution.

In Appendix E, we extend the model by considering a more general distribution of the preference shock. We focus on distributions with the same support for the shock, i.e.,

e2[0;1], but allow the density function, f(e), to be more general. Under the assumption

that ef(e) increases ine, we can solve the monetary equilibrium following the same steps as in Section 3.10 We can still prove that a unique monetary equilibrium exists for generic

values of . In equilibrium, each seller posts a continuous pricing schedule that exhibits

quantity discounts. Buyers may spend nothing, a positive fraction or all of their money holdings contingent on the realizations of their preference shocks. The result that in‡ation

induces more linear pricing can be proved under additional assumptions about the density

functionf(e). As in‡ation rises, the probability of spending increases (e0 decreases) so the

model can capture the hot-potato e¤ect along the extensive margin. About the intensive

margin, we can still show that all buyers with e 2 (e0;e^) consume larger quantities, and

more buyers exhaust their money holdings (^edecreases), but we need additional assumptions about f(e)to proveze increases for alle2(e0;e^).

7

Conclusion

In this paper, we study trading behaviors in a monetary model of price posting and

undi-rected search where buyers have private information about match-speci…c preference shocks.

This paper contributes to the literature on price posting with undirected search by consid-ering a continuous uniform distribution of the preference shock in a divisible-money

frame-work. The model has a unique monetary equilibrium where the seller posts a continuous

pricing schedule. Our study overturns the result in earlier papers that each seller posts a single price, and the law of two prices established in Curtis and Wright (2004) no longer

holds in this new environment.

The model also provides a useful framework in which to study the role of private in-formation in monetary economies. We …nd that the existence of private inin-formation plays

an important role in generating non-linear pricing. Faced with buyers who have private

information about their preferences, sellers resort to quantity discounts to screen buyers, inducing those with higher willingness to pay to buy more. As in‡ation rises, buyers reduce

money holdings in real terms and have smaller budgets. Sellers optimally adjust the pricing

schedule to lower the extent of price discrimination (or quantity discounts), in order to start and expand trading with buyers with lower preference shocks. The expansion of trading

also allows the model to capture the hot-potato e¤ect of in‡ation along both the extensive margin (as an increase in trading probability) and the intensive margin (as an expansion in

trading quantity and the fraction of money being spent).

1 0Alternatively, we can assume that the distribution has a monotonic hazard rate; i.e., f(e)

Finally, note that our model generates a testable implication that in‡ation reduces

the extent of quantity discounts. Recently, scraped data have been constructed to sample price information from online retailers over a time span of a few years in countries with

high and variable in‡ation, such as Argentina, Brazil, Chile and Colombia (see Cavallo, 2012, for a description of the data-collecting procedure). The data contain information

about commodities with di¤erent package sizes that could be potentially used to empirically

A

Proof of Lemma 1 and Lemma 2

A.1 Lemma 1 (Transformation of the Incentive Constraint)

Proof. First we prove necessity. Consider two types of buyers: one with a preference shock level of eand the other with a preference shock level of e0 > e. The IC implies that

eu(qe) ze eu(qe0) ze0 and e0u(qe0) ze0 e0u(qe) ze;or equivalently,

e[u(qe0) u(qe)] ze0 ze e0[u(qe0) u(qe)]: (17)

It then follows thatqe0 > qe ordqe=de 0. Using ve eu(qe) ze, we can rewrite (17) as

u(qe)

ve0 ve

e0 e u(qe0) (18)

Lettinge0 !ein (18) gives dve=de=u(qe).

Now we prove su¢ ciency. Again consider e0> e. (IC1) and (IC2) imply thatve0 ve= Re0

e u(qx)dx Re0

e u(qe0)dx = (e0 e)u(qe0), which can be rearranged as eu(qe) ze

eu(qe0) ze0. Similarly, we can deriveve0 ve (e0 e)u(qe) ore0u(qe0) ze0 e0u(qe) ze.

It then follows that the (IC) is satis…ed.

A.2 Lemma 2 (Seller’s Optimal Pricing Schedule)

Proof. The seller’s choice of pricing schedule is a standard optimal control problem withqe

as the control variable andve as the state variable. The problem has a solution because the feasible set of the control variable is non-empty and compact. We can apply the Maximum

Principle to …nd the necessary conditions for the optimal paths of the control and state

variables.

We …rst disregard (IC1),dqe=de 0(and we will impose it later), and …nd the conditions

that characterize the optimal choice of (qe; ze). The Hamiltonian of the optimal control

problem is

H = [ qe+eu(qe) ve] + eu(qe),

where e is the co-state variable. The Lagrangian is

L= qe+eu(qe) ve+ eu(qe)

+ e[^z eu(qe) +ve] + eqe,

The …rst-order conditions are

qe : (e+ e ee)u0(qe) = 1 e, (19)

ve : 1 + e=

d e

de , (20)

e : u(qe) =

dve

de, (21)

e : z^ eu(qe) +ve 0, if >0, then e= 0, (22)

e : qe 0, if >0, then e= 0. (23)

The transversality condition is 1v1 = 0. In a monetary equilibrium, v1 >0 and 1 = 0.

Integrating d x=dxover the interval[e;1], we have

Z 1

e

d x

dx dx =

Z 1

e

(1 x)dx

! 1 e= 1 e

Z 1

e x

dx

! e=e 1 + e with e

Z 1

e x

dx,

where the last step uses the transversality condition. Substituting e into (19), we have

[(2e 1) + e ee]u0(qe) = 1 e. (24)

Now we impose the constraint dqe=de 0 (and as a resultdze=de 0). Given this, we can consider the seller’s problem in three regions of edivided by0 e0 ^e 1.

Case (i). When e is small (e e0), no exchange occurs or qe = ze = ve = 0. (NC)

binds and (CC) is loose.

Case (ii). For intermediate values of e(e0 e ^e), neither (NC) nor (CC) binds, i.e.,

e= e = 0. In this case, (24) reduces to11

[(2e 1) + ^e]u0(qe) = 1, (25)

which can be used to solveqe. Since u00<0 c00, the solution to (25) satis…esdqe=de >0.

Therefore, we can use (25) to solve qe fore2[e0;e^]. Given qe, we can derive ve and ze as

1 1Notice that since

follows. Integrating the two sides of (25) with respect toqe over the interval[0; qe], we get

Z qe

0

[(2x 1) + ^e]u0(qx)dqx = qe!

2 Z qe

0

xd(u(qx)) + ( ^e 1)u(qx) = qe!

2 2 6 6 4eu(qe)

Z e

0

u(qx)dx

| {z } ve

3 7 7

5+ ( e^ 1)u(qe) = qe!

ve = 1

2[(2e 1) + ^e]u(qe) 1

2qe. (26)

It follows that

ze=eu(qe) ve= 1

2(1 e)^ u(qe) + 1

2qe. (27)

Case (iii). When e is high(e e^), the buyer is charged all his or her money holding,

orze= ^z and qe= ^q: We can solve q^from

[(2^e 1) + ^e]u0(^q) = 1. (28)

In the next step, we will …nd the term e^ in (25) and (28) as a function of ^e. Since

qe= ^q for all e >e^, we know q^also solves

[2e 1 + e ee]u0(^q) = 1. (29)

Combining (28) and (29) and using e= d e=de, we have a di¤erential equation of e;

2^e+ e^= 2e+ e+e

d e

de : (30)

To solve for e, integrate the two sides of (30) frome^to1 and use the boundary condition

1= 0,

(2^e+ ^e)(1 e^) = 1 e^2+ Z 1

^

e

ede+ Z 1

^

e

ed e= 1 e^2 e^ e^!

^

e = (1 e^)2. (31)

Plugging (31) into (25), (26), (27) and (28),we can derive (3), (4), (5) and (6), respectively. Note thate0 can be expressed as a function of^eand is determined by

[(2e0 1) + ^e]u0(0) = 1ore0= ^e

^

e2

2 .

deter-mined by e^. The …nal step to complete the solution to the seller’s problem is to determine

^

eas a function of z^. From (25) and the de…nition of ve, we can …nd the unique solution of ^

eas a function ofz^from

^

z= (^e e^

2

2)u(^q) + 1 2q^.

It is possible that ^etakes the corner solutione^= 1 (so that no buyer is cash constrained) when z^is large enough. This situation occurs when z^ z withz given by

z= u(q1) +q1

2 .

Finally note that the Hamiltonian is jointly concave in the control and state variables

(qe; ve) for all e2[0;1]. The …rst-order necessary conditions are also su¢ cient conditions. Additionally, the solution to the …rst-order conditions is unique. Therefore, there is a unique

pricing schedule that maximizes the seller’s Vs(0).

B

Unobservable Money Holdings

In this Appendix, we show that multiple monetary equilibria arise if money holdings are

unobservable. This is equivalent to the setting where buyers choose money holdings and sellers post prices simultaneously. We maintain the assumption of undirected search.

The seller’s best response remains the same as described in Lemma 2. Let (qe; ze) be

the pricing schedule posted by the seller and z^be the maximum of zein the schedule. The buyer’s best response is to take the seller’s pricing schedule as given and choosez^b z^to

(note that the buyer will not choose z^b >z^because he or she can not spend more than z^)

max

^

zb

S(^zb) iz^b= Z e^b

e0

[eu(qe) ze]de+ Z 1

^

eb

[eu(^qb) z^b]de

| {z }

S(^zb)

iz^b,

withe^b(^zb) solvingefrom ze(e) = ^zb.

From (5),

dze

dqe

= e^ ^e

2

2 u

0(q

e) + 1 2 =eu

0(q

Taking the derivative ofSb with respect toz^b, we have

dSb dz^b

= fe^bu(^qb) z^b [^ebu(^qb) z^b]g

d^eb

dz^b +

Z 1

^

eb

eu0(^qb)dq^b

dz^b

1 de

= Z 1

^

eb

eu0(^qb)dq^b

dz^b

1 de

= Z 1

^

eb

he ^

eb 1

i

de

= (1 e^b)

2

2^eb .

The buyer choosesz^b = ^zifdSb=dz^b 0. As a result, a Nash equilibrium exists for any

^

z that satis…es

[1 e^(^z)]2

2^e(^z) i >0,

where e^(^z) is de…ned as in Lemma 2. For any i < 1, there is a continuum of monetary

equilibria. Ifi=1, the only Nash equilibrium is ^e= ^z= 0.

C

Competitive Search

In this Appendix, we illustrate how to solve the equilibrium allocation under competitive

search.

Let be the buyer/seller ratio in a particular submarket formed by sellers who post

the same terms of trade (qe; ze)e2[0;1]. We use the Cobb-Douglas matching function, which

implies the matching probability is s( ) = & (0< & <1) for the seller and b( ) = &

for the buyer. Let J be the buyer’s maximum expected surplus from participating in the

DM. The seller chooses and fqe; zege2[0;1] tomax s( )

R1

0[ze qe]desubject to

iz^+ b( ) Z 1

0

[eu(qe) ze]de = J, (32)

eu(qe) ze eu(qe0) ze0,

qe 0,

ze z^,

eu(qe) ze 0.

The …rst constraint states that sellers compete with each other to ensure buyers get surplus

J. This extra constraint re‡ects the di¤erence between directed search and undirected search. For an individual seller, J is taken as given. The value of J will be determined in

equilibrium.

variable is ve=eu(qe) ze, and the control variable is qe.

max ; ;^z;v0;fqe;vege2[0;1]

s( ) Z 1

0

[eu(qe) ve qe]de+ iz^+ b( ) Z 1

0

vede J

s.t. 8 > > > > > > > < > > > > > > > :

dve=de=u(qe),

qe 0,

eu(qe) ve z^,

v0= 0,

where is the Lagrangian multiplier associated with (32).

We can solve the problem in two steps. In the …rst step, we take ( ; ;z^) as given and

solve for(qe; ve)as functions of( ; ;z^). In the second step, we …nd the equilibrium( ; ;z^)

using the solution in the …rst-step.

The Hamiltonian in the …rst-step optimal control problem is H = s( )[eu(q e) qe

ve] + b( )ve, and the Lagrangian is

L = s( )[eu(qe) qe ve] + b( )ve

+ eu(qe)

+ e[^z eu(qe) +ve]

+ eqe,

where the multipliers( e; e; e) are de…ned as before. The …rst-order conditions are

qe : [ s( )e+ e ee]u0(qe) = s( ) e, (33)

ve : s( ) + b( ) + e=

d e

de , (34)

e : u(qe) =

dve

de, (35)

e : z^ eu(qe) +ve 0, if >0, then e= 0, (36)

e : qe 0, if >0, then e= 0. (37)

The transversality condition is 1v1 = 0. In a monetary equilibrium, we have v1 >0 and

1= 0.

Integrating (20) over [e;1], we have

Z 1

e

d

dxdx = [

s( ) b( )](1 e) Z 1

e x

dxor