Bond Market Development in Sri Lanka

C.J.P. Siriwardena

,

Additional Superintendent,

Public Debt Department

Central Bank of Sri Lanka

(A Paper presented at the UN-ESCAP Regional Workshop on Capacity Building for

Development of Bond Markets in ESCAP Member States at UNESCAP, Bangkok)

PART I: OVERVIEW OF THE ECONOMY AND FINANCIAL SECTOR

1/ 1. Overview of the EconomySri Lanka is a small open economy with an estimated population of 20.1 million and an annual average population growth of 1.1. per cent . The economy has grown on average by 5 per cent over the last fifteen years. The gross domestic production in 2006 is estimated at US$ 28.1 billion with a per capita income of US$ 1,414 that falls the country into a group of lower middle income countries in the world. The overall performance of the economy has moved to a high growth path and able to maintain growth momentum in real term over 6 per cent in the recent past. The economy achieved a commendable growth of 7.7 per cent in 2006 and 6.2 per cent in the first half of 2007 and is estimated to grow at 6.7 per cent in real term in the year as a whole. In 2008. the economy is prospected to grow at a higher rate of 7.0-7.5 per cent. The medium term development strategy expects to broad base activities thereby maintain over 8 percent annual growth over next 10 years enabling the country to reach its per capital income over US$ 3,000 level (Appendix Table 1).

2. The economic activities are broad based and the overall production is an outcome of the performance of the three main sectors; services, industry and agriculture sectors in the economy. The services sector has shown a steady growth in its share in the overall production and today plays a dominant role accounting for over 56 per cent of output in the economy. Main services sector activities include international and domestic trade, financial services and transport sector contributing for 70 per cent of the services sector output. The industry sector share in the total output remains around 27 per cent over last three decades period. At present, factory industry and the construction sectors contribute a prominent role accounting for over 75 per cent of total industrial output in the economy. The agriculture sector which was the major sector in the economy, five decades before, contributes for only 17 per cent of the total output in the country. Food and plantation crops sectors represent over 80 per cent of the agriculture sector output. The performance of this sector is highly sensitive to the weather conditions prevail in the country which follows a cyclical pattern impacting volatility in the annual production process. Despite Sri Lanka is an island economy with unlimited marine resources, a share of the fishing production in the overall productions is less than 2 per cent.

3. The economy has been continuously running with the domestic resource gap where country‟s investments are higher than national savings and financing the gap through foreign sources. Both investments and national savings are in the upward trend, reached to 28.0 per cent and 22.9 per cent of GDP respectively in 2006. However, as the current level of savings and investment is not adequate to

1/ The views expressed in this paper are the author‟s own and do not necessarily reflect those of the Central

Bank of Sri Lanka. The structure of the paper is based on the outline provided by the UNESCAP to the regional workshop.

take off the economy to a targeted high economic growth path in a sustainable manner, the medium term macroeconomic strategy expects to enhance the country‟s investment over 30 per cent of GDP giving high priority on more productive sectors in the economy.

4. The government has reiterated the necessity of bringing the fiscal consolidation in order to ensure the fiscal as well as debt sustainability in the country. Persistently high government budget deficit which was largely financed through commercial type domestic borrowings resulted for the mounting debt stock in the public sector in the recent past. In this context, servicing of public debt became a major issue in the government budget and the management of public debt became a complex task which requires drastic changes to the overall fiscal and public debt management in the economy. Understanding the emerging threats in the fiscal sector, Fiscal Management (Responsibility) Act (FMRA) was brought into the system in 2003, in order to improve fiscal discipline and transparency in fiscal operation through rule based fiscal management as practicing in many other countries in the world.

5. Under the FMRA, the government has committed to bring down the overall deficit to below 5 per cent of GDP in the medium term and lower the total debt to GDP ratio to 60 per cent by 2013. The government expects to achieve these targets through more sustainable approach by enhancing revenue efforts, streamlining recurrent expenditure while allocating more funds for public investment and accelerating growth movement in the future. The government budget 2008 has been formulated toward this direction generating surplus in current account operations thereby limiting government borrowings only for public investment activities of the government. Debt to GDP ratio that rose to over 105 per cent in 2004 is already in the downward path and estimated to decline to 85 per cent by end 2007.

6. The external sector operations of the country recorded a substantial expansion in external trade and financial flows that is helpful to maintain surplus in the Balance of Payment (BOP) in most of the years in the recent past. Although export sector maintains a high growth with continuous diversification of products range, country‟s trade balance remained over 10 per cent of GDP in the recent past mainly due to sharp increase of international prices of intermediary goods such as petroleum oil. However, large and steady growth of the inflow of private remittances which becomes a permanent and growing foreign exchange earning source help lower the current account deficit of the BOP to around 3 per cent of GDP. Even though, the economy has an inherited feature of running with current account deficit in the BOP, the overall balance of the BOP has been mostly positive due to high inflow of funds received for government budgetary operations and continuous flow of funds through private remittances and foreign direct investment into the economy. In 2006, the overall balance of the BOP was US$ 204 million and expected to generate surplus of US$ 450 million in 2007. The gross official reserves of the

country gradually increased up to US$ 2.5 billion at end 2006 and further to US$ 2.6 billion at end August 2007 enabling to maintain around 3 –month of import of goods and services. In line with that, total external reserves of the country grew to US$ 4.0 billion at end August 2007and it was sufficient for over 4.3 month of imports of goods and services in 2007. Maintenance of external reserves at this level shows the resilience of the economy to unforeseen external shocks in the future.

7. Sri Lanka entered into Article VIII agreement with the IMF under which current account operations are fully liberalized since 1994. In addition, part of the capital account operations is also liberalized with the intention of continuing the opening path gradually in the future. Sri Lanka has made continuous efforts to strengthen the external trade relations through bilateral, regional and multilateral trade arrangements in order to boost activities in the economy. Of which, bilateral agreements with the EU and India are major events. Even though series of measures has been taken to encourage Foreign Direct Investment (FDI) by granting various incentives and creating conducive infrastructure for foreign investment in the economy, foreign direct investment remained low around 1 per cent of GDP over the past. Understanding the importance of increasing FDI in achieving future growth target in the economy, government has been formulating a new strategy to increase FDI that helped to increase it to 2 per cent of GDP in 2006 and further increase in the future.

8. The Central Bank conducted a tight monetary stance in the recent past with the objective of containing inflationary pressures and lowering the rapid growth of monetary aggregates in order to facilitate the high growth momentum of the economy. The Central Bank relies more on market-based instruments such as Open Market Operations (OMO) to conduct the monetary policy with a view of maintaining the price stability in the economy. The financial sector continuously expanded with improved stability and resilience over the past. The performance of financial institutions improved in terms of profits, soundness and a widening of the array of financial products and services. The market infrastructure covering regulatory and payment and settlement systems has been substantially improved to enhance the efficiency in the financial system while ensuring protection to all stakeholders. The banking sector intermediation in the corporate sector is excessively high and their funding requirement is almost entirely met through the banking system in the country.

2) Policy Environment

9. The macroeconomic management in Sri Lanka has been centered around fiscal and monetary policies system in order to take off the economy toward a sustainable high economic growth path with balanced regional development. The fiscal policy has been formulated toward achieving fiscal consolidation while monetary policy focused on prudent monetary management and a well functioning

independent floating exchange rate system. This process has been complemented by the broadening and deepening of structural reforms in order to enhance the efficiency in policy transmission and to ensure the targeted outcome in the future.

10. The fiscal policy framework has been formulated mainly focusing on the fiscal consolidation programme which is compatible with the medium term fiscal and debt sustainability strategy outlined under the Fiscal Management (Responsibility) Act (FMRA). The FMRA aims at among other things two major problems in the fiscal sector; persistently high budget deficit and high public debt stock and therefore, envisages to reduce the overall deficit gradually to below 5 per cent of GDP and lower the debt to GDP ratio to 60 per cent by year 2013. The work plan incorporated into the medium term fiscal consolidation programme include the turning round of current account deficit ( or dis-saving of government which has been a permanent feature in last two decades) to a surplus through expanding tax base, high non-tax revenue efforts from state enterprises, cost effective expenditure management system together with prudent debt management policy and phasing out of budgetary transfers to public enterprises. While achieving the medium term fiscal consolidation targets, the fiscal policy also designed to support economic growth, implementing structural reforms and generating productive employment in the economy. In order to address regional imbalances and high degree of poverty in the economy, pro-poor, pro-growth and regional development strategy has been introduced to enhance the standard of living of low income people and vulnerable groups in the society. This programme is expected to be implemented through the development of socio-economic infrastructure facilities, creating employment and income opportunities for the poor, minimise regional imbalance in development and distribution of benefits of growth. In order to facilitate this programme, the government has determined to increase allocation of resources for the medium term public investments programme giving more priority on infrastructure development to create a conducive environment for private sector investment to accelerate growth momentum in the economy.

11. In line with the medium term fiscal strategy, the preparation of the government budget is an annual process for a rolling period of 3 years. Accordingly, Medium Term Fiscal Framework (MTFF) has been developed consistent with the overall medium term macroeconomic framework. Further, the MTFF explains its financial flow, toward specific targets within the context of sectoral policy strategies. Since the annual budget is published as a rolling plan, the implementation agencies have flexibility to revise their work plan in advance as and when required, thereby ensuring the implementation of the medium term programme as expected originally.

12. The monetary policy stance in Sri Lanka aims at achieving a suitable low and predictable level of inflation, which support economic activities of the economy. The Central Bank as monetary authority

of the country formulates a monetary targeting policy framework to guide the monetary policy operations. At present, the key policy instrument is the Central Bank Policy interest rates (Repo and Reverse Repo rates) maintaining using the active open market operations. The open market operations(OMOs) enables the Central Bank to actively manage market liquidity to achieve its monetary policy targets. The Central Bank conducts several operations; conducting auctions, standing facilities and outright sale or purchase to maintain liquidity position in the market at desired level. In this process, government securities i.e. Treasury bills and Treasury bonds play an important role in the OMOs. In addition, Statutory Reserve Requirement (SRR) on Licenced Commercial Banks is also used as a direct instrument to support the monetary policy operations.

13. Since 2003, the Central Bank has been adopting a tight monetary policy stance to curtail credit growth as it is considered as one of the causal factor in rising inflation in the economy. Accordingly, Central Bank policy rates revised upward by 9 times during the period 2003 – 2006, increasing the repo and reverse repo rate structure by 300 bps from 7.0 –8.5% to 10.0 – 11.5% over the period. In 2007, policy rates revised upward again by 50 bps. to the current level of 10.5 – 12.0%. A cautious approach has been adopted in open market operations to restrict the injecting of funds from the Central Bank to the system while maintaining the market liquidity at required level in order to accommodate smooth transaction in the economy. In addition, several specific prudential requirement measures have also been imposed on commercial banks in the recent past to curb the rising credit growth in the banking system. Beginning 2007, the Central Bank has issued its Roadmap for Monetary and Financial Sector Policies for 2007 and Beyond, explaining the policy strategy to be introduced to maintain the economic and price stability and the financial sector stability of the country.

14. In view of external sector policies, replacement of the managed float exchange rate regime by the independently floating exchange rate regime in 2001 was a major policy move in the recent past. The new regime is expected to strengthen the exchange rate stability, deepen the foreign exchange market and improve the country‟s competitiveness in the international market . Reflecting the effective implications of the new exchange rate policy, country‟s total external assets measured in terms of months of same year imports, increased to 4.7 months by end of 2006 from 3.5 months in 2001. The current account operations are completely free from exchange controls, while capital account is partially opened specially allowing foreign investors to enter into selected markets and sectors in the economy. Although, equity market is almost fully opened for foreign investors, money market is still restricted for foreigners. In 2006, government bond market was opened for foreign investors with a limited access (5 per cent of outstanding total Treasury bond stock) facility. However, more restricted policy has been adopted on local investors investing in foreign market which is permitted only on case by case basis.

3) Financial System

The financial system plays an important role in financial intermediary functions by borrowing from surplus units and lending to deficit units in the economy. The financial institutions comprise the Central Bank which stands as an apex institution responsible for monetary and regulatory authority of the financial system and other financial institutions which dominated by Licensed Commercial Banks (LCBs) in the country. The financial markets in the country consists of inter-bank call money market, domestic foreign exchange market, government securities market, share market and corporate debt securities market. Except corporate bond market, all other financial markets are active and operate largely through various instruments. Financial infrastructure, which covers regulatory framework and payment and settlement system, facilitates the smooth and efficient transaction in the financial market and provide safety to all stakeholders in the financial system (Appendix Table 2).

3.1 Central Bank

The Central Bank, since its inception in 1950 under the Monetary Law Act has been responsible for the administration, supervision and regulation of the monetary, financial and payment and settlement system in the country. Until 2002, the Central Bank had multiple objectives relating to the stabilization of domestic monetary value, preserving the stability of the exchange rate, promotion of high level of production, employment and real income and the encouragement and promotion of the full development of productive resources of the country. With the evaluation of economic and financial sector operations, it has been realised that it would be (expecting difficult) to successfully achieve multiple objects due to conflicts and inconsistencies among them. In fact, the Central Bank recognized price stability as a principle objective, which requires stable macroeconomic condition in the economy. Accordingly, in 2002, “Economic and Price Stability” designated as the core-objective of the Central Bank. Since the stability of the financial system is crucial in preventing economic crisis in the country, “Financial Stability” was also considered as a core-objective of the Central Bank.

In line with the changes of objectives of the bank, a new organizational structure was established categorising departments of the bank under the primary objectives or by function groups such as price stability, financial system stability, agency functions and corporate services. At the same time, several non-core functions were developed to give priority on core function of the Bank. These changes in the organizational structure were accompanied by the establishment of advisory technical committees system to streamline the decision making process in the bank. Accordingly, several committees have been appointed to advise and recommend to the Monetary Board on monetary policy, financial system stability and auditing. The Monetary Policy Committee (MPC) is responsible to recommend on

monetary policy and Financial System Stability Committee (FSSC) is entrusted to recommend on the regulatory aspects of banking and financial institutions. The Audit Committee (AC) is responsible to recommend on financial accountancy and risk aspects of the bank. In addition, the Monetary Board was enhanced by increasing its membership from 3 to 5 which facilitated to accommodate two more private sector representatives in the Board.

The formulation and conduct of monetary policy also underwent significant changes during the last four years. The Central Bank has moved toward market oriented measures in monetary management and Open Market Operations (OMO) become the principle tool in monetary management in the economy. In view of the financial sector stability, a series of new measures adopted to improve the liquidity and strengthen the supervisory and regulatory functions in the bond market. Main policy measures include, acceptance of treasury bonds for the transactions of secondary window of the Central Bank that help improve liquidity in the bond market, introduction of new accounting standard and technological advancement in payment and settlement system in the market. In order to accommodate these reforms, necessary changes were introduced to the legal framework in the financial system.

The Central Bank has played a vital role as a market maker by designing new debt instruments and necessary market infrastructure and establishment of effective monitoring and regulatory mechanism for the development of the bond market. In turn developments in the government bond market have facilitated the Central Bank to further strengthen the market oriented monetary management strategy. Because of new policies adopted to create a liquid bond market and consideration of bonds as tradable instruments at the Central bank windows enabled the monetary authority to use Treasury bonds in the open market operations (OMO) and manage monetary operations in a more effective manner. Further development of the domestic bond market would help the monetary authority to conduct the of monetary management more efficiently in the future.

3.2 Banking System

In Sri Lanka, the banking sector is the systemically most important and dominant sector of the financial system. The banking sector comprises Licensed Commercial Banks (LCBs) and Licensed Specialized Banks (LSBs) and representing over 58 per cent of the financial system in terms of the asset base and 94 per cent of the total deposits in the financial system.

There are 23 LCBs operating in the country with an island-wide network with a market share of 81 per cent of banking sector assets and 48 per cent of entire financial system‟s assets of the country. In terms of ownership, 11 domestic banks and 12 foreign banks are in operation in the country. The banking

system is dominated by the performance and financial strength of the 6 largest LCBs, comprising of 2 state banks and 4 largest domestic private commercial banks. These 6 banks are recognized as Systemically Important Banks (SIBs), accounting for 78 per cent of the LCB sector assets and 65 per cent of the banking sector assets. In terms of deposits, the SIBs have a market share of 83 per cent of LCBs and 68 per cent of banking system deposits. Two state owned LCBs continue its dominance in the banking system having a market share of 37 per cent of assets and 44 per cent of deposits of the LCBs.

There are 14 LSBs conducting banking business excluding acceptance of demand deposits and dealing in foreign exchange. Their share in the entire financial system‟s assets and financial system deposits are 9.5 per cent and 17.2 per cent, respectively. Of this sector, state owned National Savings Bank (NSB) is the largest LSB accounting for over 50per cent of LSB assets and two large LSBs account for 83 per cent of assets and 88 per cent of deposits of LSBs. In comparison to LCBs, the businesses of LSBs are diverse and therefore, risks too are spread out. The systemic importance of the LSBs is less compared to LCBs. However, the share of LSBs in the financial system is continuously declining over the period due to rapid expansion of other sectors in the financial system.

3.3 Non Bank Financial Institutions

The market share of the non-bank financial institutions (NBFIs) registered with the Central Bank comprising Licensed Finance Companies and specialised leasing companies is about 6 per cent of the financial sector assets. There are 28 NBFIs and 18 specialised leasing companies registered with the Central Bank and most are private owned institutions. These institutions mobilise funds offering relatively higher interest rates to depositors who are ready to bear higher risk. Further, lending rates charged by NBFIs are also high due to high cost of funds as well as to the greater risk associated with each advances. Mostly these institutions lend for leasing and hire purchase businesses.

The other financial institutions account for 26 per cent of total financial sector assets. The contractual saving institutions dominate in this sector sharing over 80 per cent in terms of total assets . Employees Provident Fund (EPF) for which Central Bank plays a custodian role is the largest contractual saving fund in the country representing 50 per cent of this sector asset base. Other main institutions include insurance companies, private provident funds, Employees Trust Fund (ETF) and primary dealers.

The financial system plays a multiple role in the bond market operations acting as issuers, investors, intermediaries and liquidity providers in the market. The primary dealer system (11 primary dealers) and licensed commercial banks mainly operate as intermediaries in the bond market in addition to maintaining bonds in their portfolios for trading and investment purposes. In the investment front,

contractual saving institutions which own long term capital are major institutional investors in the bond market representing over 60 per cent of total outstanding bond stock in the market. The position available in the financial system for bond holders to undertake discount or repo operations (keep) improve the liquidity in the bond market.

4) Financial Markets

Financial markets play an important role for the efficient allocation of financial resources and diversifying risks in the economy. The government has given high priority to develop financial markets that help lower the cost of raising liquidity and capital. Since financial markets represent a key segment of the overall financial system, safety and efficiency of financial markets are important to ensure the stability in the overall financial system.

4.1 Money Market

Money market operations in Sri Lanka comprises two active markets; the first is interbank call money market and the second is Treasury bill (primary and secondary) market. The other money market operations such as commercial paper market and central bank securities market are not significant in the domestic market.

Inter bank call money market is a very vibrant market that facilitates licensed commercial banks to meet their liquidity mismatches arising from day to day operations thereby matching the liquidity risks in the banking system. The stability in the liquidity situation in the call market is supported by the provision of repo and reverse repo facilities through the Central Bank. The borrowing and lending operations in this market are largely for overnight period. The call market interest rate vary mainly with the liquidity situations and Central Bank policy rates mostly act as a benchmark to determine the lending rate in the call market, which is mostly settled in between the two policy rates under normal market conditions.

Treasury bills which are short term government debt instruments issued under multiple bidding system used to raise funds from the domestic market for government budgetary operations. Treasury bills are highly liquid money market instruments and considered as an alternate source of liquidity and investment vehicle. Under the existing debt management strategy, new issues of Treasury bills to raise funds for budgetary operations are limited to a minimum level to reduce the share of short term public debt stock in the total debt portfolio in order to lower the volatility in the debt market. However, re-issue or roll-over of existing Treasury bill stock (Rs. 257 billion) through a regular weekly auction process help maintain the liquidity in the market. The primary market operations are

limited only to Primary Dealers (PDs) who are permitted to access to the primary auctions at the Central Bank through the electronic bidding system. Treasury bill is the only government debt instrument permitted the Central Bank to purchase from the primary market. The secondary market for Treasury bills is very active and covers outright sales and purchases and repo and reverse repo transactions. With the introduction of scripless form issue under the Scripless Securities Settlement System (SSSS) complement with Real Time Gross Settlement (RTGS) system and Central Depository System (CDS), Treasury bill market operations recorded significant improvement in the recent past.

4.2 Equity Market

Sri Lanka has one of the oldest share markets in the world. Share market operations began during the British colonial period with the inception of Colombo Share Brokers‟ Association in year 1896. Over the last 110 years period, it has been evolved and since 1990, renamed as Colombo Stock Exchange (CSE). During last two decades, the CSE has undergone significant changes in order to develop the activities in the equity market. These developments include establishment of a public trading floor and inauguration of trading on the open outcry system (1984), liberalization of investment for non-nationals (1990), automation of the clearing system with the establishment of Central Depository System (1991) and automation of trading with the inception of screen based trading system (1997). As at end 2006, 238 companies were listed on the CSE and their market capitalization was over Rs. 840 billion equivalent to 32 per cent of estimated GDP for 2006. In several occasions in the recent past, the CSE was ranked as the most active stock market in the region.

Local investors both individuals and institutions play a dominant role in the equity market in terms of market value. However, foreign investors, mainly institutional investors played a significant role until the recent past increasing their share in the market up to 43.3 per cent in 2000. Since then, foreign investors‟ share showed gradual decline and decrease to below 14 per cent by end of 2005 due to rapid increase of local participation in the market. Although, this analysis is in terms of a share to the total market value, foreign investment in value terms has gradually increased over the past. The equity market is not fully liberalized for foreign investors as there are some restrictions still remain prohibiting or limiting foreign investors entering in to certain sectors of the market.

The equity market comprises 20 sub sectors. In terms of market capitalization, telecom sector dominates in the market followed by financial institutions, diversified holdings, hotel services and food & beverage sector accounting for over 77 per cent of the market. Since the introduction of the CDS, it acts as the depository for all securities traded and is responsible for the post trade clearing and settlement of transactions. Trades are in scrip less form that enable to record trading transactions in the form of book keeping entry by making corresponding debit and credit entries in client accounts. The

settlement of the equity market differs for buyers and sellers with T+3 and T+4 settlements dates‟ system, respectively. In addition, inter-participatory settlement takes place through the nominated settlement bank of the CDS. In addition to normal trading in the market, stock borrowing and lending system was introduced in 2001. This is similar to the collateral loans of securities for a limited period of time under which lender can transfer securities to borrower with an agreement for the borrower to replace them on agreed time.

The operations of the equity market are highly sensitive to the changes in the political and

peace environment in the country as in most of other markets. In addition, the market

performance is closely related to the sound fundamentals and profitability of key players in the

market. The financial institutions exposure to the equity market through investment and

lending activities are low and threrefore impact of equity market operations to the financial

system stability is relatively low.

4.3 Bond Market

The bond market in Sri Lanka commenced its active operations in 1990‟s with the issuance of medium and long-term bonds, both by the government and the corporate sector. This process has been accelerated in line with the financial sector reforms and restructuring programme implemented in the last decade. The debt management policy of the government has substantially reformed by shifting from issuing non-marketable instruments (such as Rupee loans) and short-term marketable instruments (such as Treasury bills) to medium and long-term marketable instruments. As a result, the government compelled to introduce a long-term marketable and fixed income type new debt instrument; Treasury bond in 1997 to raise funds from the domestic market to finance the government budgetary operations. Subsequently, government borrowings through non- marketable instruments and short-term marketable instruments have been gradually reduced over the period. Furthermore, the government has exercised the early retirement facility or „call option‟ of the existing stock of non-marketable securities to replace them by Treasury bonds to accelerate the development of the bond market. The gradual increase of the maturity structure of the Treasury bonds enabled the market to establish a medium-term yield curve which has provided a benchmark for the domestic corporate bond market.

Concomitant to this programme, steps have also been taken to develop the market infrastructure. These include the improvement of primary and secondary markets, computerisation of market infrastructure, scrip less form issuing system and improvement of payments and settlements systems. The required reforms have also been brought into the legal framework, appropriate to the development of the bond market for the smooth transformation towards the market based debt management. The

authority strengthened the monitoring and regulatory work at the central level, in order to ensure the safety and security of investment made by the public and stability of the overall financial system. The authority‟s continuous commitments on this process and fairly developed domestic money market operations helped develop the bond market, specially government bond market within a relatively shorter time period.

Although, a more active market exists for government bonds, the corporate bond market is still at an under-developed stage. The government has recognized the importance of developing the corporate bond market to diversify the funding sources in order to reduce the high reliance on the banking system and the equity market. Further, it would lower the vulnerability of the corporate sector to unforeseen forces as experienced by some of Asian countries during the Asian Financial Crisis. In this regard, a number of policy measures have been implemented with a view of developing the corporate bond market. They include mandatory requirement of credit rating and publication of such rating for all varieties of debt instruments, registration requirement of all corporate bonds, entrust regulatory functions of corporate bonds to the Colombo Stock Exchange (CSE) and providing facilities to trade corporate bonds in the stock market. This development process has to be continued with a well-designed awareness programme to educate both corporate players and investors about the important role that could be played by the bond market providing alternative options for investors to invest their savings and for corporate players to reduce the vulnerability to the system risks by diversifying their alternative funding sources.

4.4 Foreign Exchange Market

The foreign exchange market which plays an important role in the financial system of redistributing liquidity within the banking system consists of two main sub sectors; retail or client market and wholesale or inter-bank market. In Sri Lanka, all Licensed Commercial Banks (LCBs) are registered as authorized foreign exchange dealers in the country and the inter-bank market operations take place between LCBs. The transactions in the inter-bank foreign exchange market partly result from the transaction in the retail market.

In the inter-bank market, transactions occur on various forms such as spot, tom, cash or forward basis. Total transactions in this market in value term has been growing over the past and daily average turnover increased to about US$ 45 million in 2006 in comparison to US$ 30 million in 2005 and US$ 18 million in 2004. The spot market continues its domination in the forex market account for over 60 per cent of total operations while forward market, which shows steady growth over the past account for about 35 per cent of total inter-bank transactions in the market. Although, there are 23 LCBs operate in the forex market, four major banks account for over 60 per cent of transactions in the market. Increase

of international trade and foreign private remittances are main contributory factors for increasing transactions in the forex market.

Sri Lanka introduced floating exchange rate regime that replaced managed float exchange system in 2001. The exchange rate i.e. value of Sri Lankan rupee against United States Dollar (USD), is determined in the inter-bank market through market mechanism. However, since the excessive volatility in the forex market could have negative impact on the stability in the financial system and the performance of the economy, the Central Bank intervenes in both sides of the forex market to curb excessive exchange rate fluctuations. In addition, Central Bank plays a regulator role in the forex market in order to maintain safe, orderly and stable forex market conditions in the economy.

5. External Debt and Foreign Exchange Reserves

5.1 External Debt

In Sri Lanka, the outstanding external debt consists of Central government debt, public corporation debt, private sector debt and drawings from the IMF. The external debt, in US dollar terms, is in an upward trend and increased to US dollar 12,235 million at end 2006. However, total external debt as a percentage of GDP is in a downward path in the recent past and declined to 43.3 per cent in 2006, from 59 per cent in 2003.

The Central government external debt accounts for over 85 per cent of total external debt. Over 90 per cent of government external debt is concessional debt raised from multilateral (such as IDA, ADB etc.) and bilateral donors (mainly Japan). A large share of these loans is project loans received for specific development projects operate under the public investment programme of the government. However, policy makers maintained a very cautious approach in dealing with international capital markets. As a result, government or corporation sector have not yet issued foreign currency denominated international bonds to raise funds from the international capital market.

Of the total external debt, medium and long-term external debt accounts for 94 per cent of the total outstanding external debt. The central government represents over 85 per cent of medium and long term external debt while the public corporations and the private sector accounts for balance medium and long term external debt and the entire short term external debt. The objective of raising medium and long-term external debt was mainly for the funding of investment activities of the public and private sectors. The short-term external debt is mainly trade credit facilities, widely used for the importation of raw materials. Since the country‟s capital account is largely closed, private sector is not permitted to issue rupee denominated corporate bonds to foreign investors or issue foreign currency denominated corporate bonds in the international market.

5.2. Foreign Exchange Reserves

The Central Bank in Sri Lanka has adopted a very cautious approach in managing foreign exchange reserves in order to stabilize the markets in the unlikely event of an additional foreign currency requests by the financial system in the economy. Hence, the Central Bank recognized a required floor level of gross official reserves of the country to be maintained that is equivalent to three months of import cover of the corresponding year. Since commercial banks also maintain a substantial amount of external assets, the country‟s total external reserves comparatively maintained at fairly high level (around 5 months of import cover) in the recent past. In value terms, gross offered reserves and total reserves of the country at end 2006 amounted to US$ 2,837 million (covering 3.0 months of imports of goods and services) and US$ 4,005 million (covering 4.1 months of imports of goods and services).

6. Foreign Direct Investment in the Financial Sector

In Sri Lanka, foreign direct investment in the institutional structure of the financial system are mainly concentrated in licensed commercial banks (LCBs) and insurance companies while in financial markets foreign investors participation are almost entirely in the equity market.

In the licensed commercial banks system (23 banks), 12 banks belong to foreign ownership accounting for 27per cent of the total assets in the banking system. Foreign banks are largely involved in lending to international trading business and actively operate in the forex market. In the insurance industry (16 companies), the share of. foreign owned insurance companies operate in the local market is still low.

Except the equity market, all other financial markets were closed for foreign direct investment due to restrictions in the capital account operations in the country. However, toward the end of 2006, rupee denominated Treasury bond market was opened for foreign investors with limited access (5% of total outstanding bonds). Since the long-term macroeconomic strategy expects to liberalise the capital market, more foreign direct participants would be expected in the financial system in the future.

PART II:

DEVELOPMENT OF THE BOND (GOVERNMENT AND CORPORATE

BOND) MARKET

1. General Overview

In Sri Lanka, bonds issued in the domestic market could be broadly divided into three types in terms of the issuers‟ ownership; government bonds, debentures issued by public enterprises and debentures issued by the corporate sector

.

The domestic bond market commenced its active operations only after the issuance of medium and long term tradable government bonds: Treasury bonds in 1997. It is a product of the new public debt management strategy envisaged by the government towards the issuance of medium and long term marketable securities to raise funds for government budgetary operations. The issuance of a marketable, liquid and long term debt instrument such as Treasury bonds was a long felt need in the domestic market enabling local investors to match their supply of long-term funds with the demand for long-term funds from the government. In line with this process, necessary steps have been taken to improve the market infrastructure and streamline the regulatory framework to enhance the liquidity and efficiency in the bond market operation. In addition, government has extended series of concessions specially tax concessions to the participants in the bond market to popularize government bonds among local investors. Although, the corporate bond market is relatively small, the development of government bond market and establishment of the long term yield curve with liquid secondary market play as benchmark role and guide the activities of the corporate bond market.

Box 1 Major Developments in the Government Bond Market in Sri Lanka

Year Event

1997 Issue of Treasury bonds commenced with maturity ranging from 2-4 years. 1997 Permit primary dealers to access to primary auction of Treasury bonds

1998 Accept Treasury bonds for the transaction of secondary window of the Central Bank

1998 Introduction of electronic bidding system. 1998 Admit Treasury bonds as a liquid asset 1998 Introduction of ‘Jumbo Issues’ system.

1999 Extend maturity structure of Treasury bonds upto 6 years 2000 Issue of Treasury bonds with ‘Call Option’ (Later suspended) 2003 Issue of 10, 15 and 20 year Treasury bonds commenced.

2003 Bloomberg Bond trading system for primary dealers was introduced. 2004 Scripless Securities Settlement System (SSS) and Central Depository System

(CDS) for government securities commenced operations.

2004 Operation of the Debt Securities Trading System (DEX) by the Colombo Stock Exchange(CSE) commenced

2005 Issuance of Index Link Treasury Bond

A rupee denominated government bond market is represented by Treasury bonds and accounted for over 60 per cent (Rs 890 bn or US$ 8.3 bn) of government domestic debt stock at end 2006. Treasury bonds are tradable, medium and long term fixed income securities issued under the Registered Stock and Securities Ordinance (RSSO) carrying semi-annual coupon (interest) payments. These bonds are issued under multiple bidding auction basis in scrip less form. The coupon rate is announced by the Central Bank prior to each auction and the market at the auction in the primary market determines yield of the bond. Treasury bonds are considered as a liquid asset and opened for Central Bank window for outright sales and purchases and Repo and Reverse Repo transactions since 1998. The opening of the government Treasury bond market for foreign investors in 2006 could be considered as a major milestone to improve the competitiveness and expand the investor-base in the bond market.

In addition, the Central Bank introduced a new foreign currency denominated debt instrument, called Sri Lanka Development Bonds (SLDBs) in 2001 to finance growing fiscal deficit thereby lower the pressure on the domestic rupee market. The issues of SLDBs, are made under the Foreign Loan Act and issues are in scrip form. It is a floating rate bond and the interest rate is linked to LIBOR plus a competitive margin. However, there is no regular issuing pattern as in the Treasury bond market. Due to these features, SLDBs are not considered as an active, tradable and liquid debt instrument. The outstanding SLDB stock as at end 2006 amounted to US$ 580 mn.

In the past, few public enterprises (such as Housing Development Finance Corporation (HDFC)) have issued debentures to raise funds for their long-term resource requirement and lower their dependency to the government budget. However, this process was gradually abandoned in the recent past and outstanding stock of debentures issued by public enterprises is now at a negligible level. In addition, Sri Lanka government issued its debut sovereign bonds to international capital market in 2007. The issuance size determined at US$ 500 million to make it bench mark size, in order to get the highest appetite from the investor comments. The bond has a maturity period of 5 years and a coupon rate of 8.25%. The bond issue was over subscribed amounted to US$ 1.62 billion and investors‟ profile shows its attractiveness across the entire global capital markets.

The corporate bond market mainly consists of debentures issued by financial institutions and few large corporate players in the domestic market. Although, the corporate bond market is relatively small, recent debenture issues have vast differences in their features such as fixed and variable interest bonds, unsecured and secured bonds, capital guaranteed bonds, subordinated bonds, convertible bonds and callable bonds. However, high degree of financial intermediation, a complex issuance process of

corporate bonds, lack of proper risk reward structure and high issuance cost specially for small corporate hinder the issuance of corporate bonds in the domestic market.

2. Size, Structure and Market Liquidity

2.1 Size of the Market

The persistently high budget deficit, which was largely financed by domestic sources mainly through Treasury bonds resulted in a rapid growth of outstanding Treasury bonds stock in the recent past. Accordingly, the size of the Treasury bond market increased from Rs.10 bn (US$ 163 mn) at end 1997 to Rs 896 bn (US$ 8.3 bn) at end 2006. As a ratio of GDP, the Treasury bond stock increased to over 30 per cent in 2006 from below 1 per cent in 1997.

The amount of corporate bonds issued by the corporate sector in comparison to the size of the government bond stock is at insignificant level. According to the information available at the Colombo Stock Exchange (CSE), market capitalisation of corporate bonds increased gradually from Rs.0.3 bn (US$ 5 mn) in 1997 to Rs. 12.5 bn (US$ 120 mn) in 2004. The corporate bond market‟s share to the total domestic bond market is less than 2 per cent.

2.2 Issuers Characteristics

In Sri Lanka, the Central Bank on behalf of the government has the sole authority of issuing Treasury bonds in the domestic market while sub-national governments (provincial councils and local governments) are prohibited to issue debt instruments to raise funds from the domestic market. According to the present constitutional arrangement for inter-governmental operations, the central government is responsible for funding the resource gap of sub-national governments under the “gap filling approach”. In addition, resource gap of most of pubic enterprises are also financed by the central government. Therefore, the central government has to raise funds for its own budgetary operations as well as to finance other public institutions.

In the past, public financial institutions (such as Housing Development Finance Corporation) issued debentures to raise long-term funds to provide long-term housing loans. However, such debenture issues have gradually declined over the recent past and the stock of debentures has declined to an insignificant level. The corporate bond market, though relatively a small market, has been dominated by financial institutions and well-reputed large non-financial players in the corporate sector. The purpose of issuing bonds by financial institutions was to enable them to reduce their asset/liability mismatch while other non-financial corporate issued bonds as an alternative resource base to reduce their reliance on the banking system.

2.3.Investors Characteristics

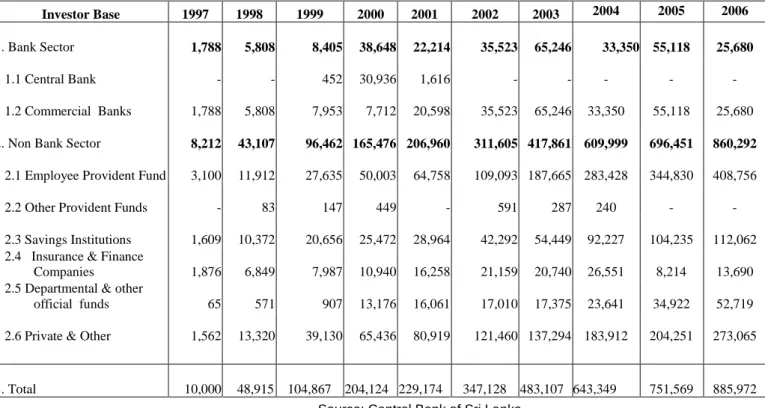

In the government bond market, state sector investors play a major role, accounting for about 70 per cent of the total bond market. They include the Employees Provident Fund (EPF), which is a superannuation fund and the largest fund in the country with the asset base of Rs.492 bn (US$ 4.6 bn) as at end 2006. This fund has invested over 70 per cent of its total investment portfolio in government bonds while its total investment on government securities amounted to over 95 per cent of the total investment. In addition, National Savings Bank (NSB), which is a government owned savings institution (Licensed Specialised Bank) with island-wide branch network and deposit base of Rs.225 bn (US$ 2.2. bn) and Employees Trust Fund (ETF), which is also a superannuation fund with a total asset base of over Rs.63. bn (US$ 0.6bn), are the other major captive investors in the bond market. In view of non-captive type investors, insurance companies, privately managed provident funds, commercial banks and other various funds play an important role. The strategy adopted in the recent past to popularize government bonds helped diversify the investor base capturing non-bank sector investors and consequently non-bank sector share in the total bond market increased to 97 per cent at end 2006. Concomitantly, the private sector share in the bond market too increased accounting for over 30 percent of non-bank sector investment in the bond market.

The main investors in the corporate bond market are again statutory funds and saving institutions. These funds are permitted to invest relatively small percentage of their assets on high quality corporate bonds in the market. Most of corporate bonds are high quality bonds and interest rates offered are higher than the yields on government securities, making them more attractive among institutional investors. In addition, such features enable corporate players to attract private investors in to the corporate bond market.

2.4 Maturity Structure

At the beginning of the government bond market in 1997, the maturity structure of Treasurybonds had to be limited to 2 years to test the market appetite for medium term tradable securities. Subsequently, maturity structure extended up to 6 years. However, the maturity structure of Treasury bond could not be extended over 6 years until end 2002 due to uncertain fiscal and macroeconomic environment in the economy. In 2003, government was able to extend the maturity structure up to 20 years with the considerable progress made on both fiscal and macroeconomic management in the economy. However, this momentum could not be continued in the recent past due to rising inflation and uncertain peace environment in the country, limiting the maturity structure of new bond issues below 10 year period.

In the corporate bond market, the original maturity period of most bonds are 5 years. However, the reputed high quality corporate players are able to extend the maturity period of their bond upto 10 years. The existing corporate bond stock has original maturity ranging from 2-10 years.

2.5 Market Liquidity

A critical feature of a well functioning bond market is a level of market liquidity that gives price signals and determine the size of the investor-base. In a liquidity market, dealers and other market participants can buy, sell or maintain a bond portfolio at a price reasonably related to the prevailing market price. A bondholder‟s ability to sell at a market price at any given movement is a very important part of an investors‟ decision-making process when determining whether to invest in a particular bond.

Since a liquid and well functioning bond market is a prerequisite to mobilize low cost funds, series of measures have been taken over the past to enhance the liquidity especially in the government bond market. Key measures include consolidation of outstanding bond series mainly by introducing re-opening process, building liquid bond series in various maturities on a regular basis, develop inter dealer market, opening of new bond series on a market friendly basis, conduct regular auctions for different maturities to develop market based yield structure, improve the exit mechanism and participation of the Central Bank as last resort in order to guarantee liquidity to the bond market. The effectiveness of these measures in improving the liquidity in the bond market was complemented by the infrastructure developments in both primary and secondary market. Consequently, a turnover ratio of the Treasury bond market (the ratio of trading volume excluding repurchase transaction to total outstanding bond stock) which is an indicator to assess the level of liquidity in the market increased to 1.2 in 2006. However, in comparison to government bond market, market liquidity in the corporate bond market is very low.

2.6 Primary Market

Treasury bonds are traded through competitive auctions conducted by the Central Bank on a regular basis. Primary dealers who have been involved in the government debt market since 1992 have direct access to the primary auctions. According to the present regulatory framework, primary dealers (11 PDs) should subscribe the entire sale and single primary dealer minimum investment level is set at 10 per cent of the volume of sale to avoid any possibility of under subscription. The present auction system is on multiple price basis. Since 2000, all auctions are conducted electronically using an on - line system. Before each auction, the debt authority accesses the potential investors via primary dealers to make sure the availability of funds for the full subscriptions. Private placements of Treasury bonds also take place as a contingency to accommodate unexpected borrowings to avoid market shocks by offering large volumes to the auctions and cancellation of planned bond auctions. Successful

bidders are informed on the same day of the auction and the settlement is two days after the auction (T+2 system).

Since the establishment of the primary dealer system, the Central Bank continued its role as a debt manager to develop the primary dealer system. They include streamlining of dealers (removing non-active dealers, appointing new dealers, etc.), introducing necessary regulatory framework for dealers and building up close relationship between primary dealers and the Central Bank.

The sales of corporate debentures in the primary market are made mostly through public offerings. In this trading system, brokers play intermediate role, as there is no appointed primary dealer system for the corporate bond market.

2.7. Secondary Market

The secondary market operations, which have been developed initially for trading of Treasury bills were then extended to the trading of Treasury bonds in the market. Today, market intermediaries can freely transact and intermediate in the secondary market for government bonds. Main participants or intermediaries in the secondary market are primary dealers, commercial banks, finance companies and institutional investors. The secondary market transactions of government securities include outright sales and purchases, Repurchase agreements (Repo) and Reverse Repurchase Agreements (Reverse Repo).

Mostly thin spread maintained by primary dealers make secondary market operations more attractive for investors. Further, the introduction of Scrip less Securities Settlement System (SSSS) could be recognized as major event to enhance secondary market trading, as it help to solve the problem of time lag, physical delivery and settlement risk. Trading in the secondary market take place between primary dealers and the Central Bank, among primary dealers and between primary dealers and other institutions or investors. Over the past, Repo and Reverse Repo market are more active compared to outright sales and purchases. Although large and wide participation of investors have contributed to enhance the liquidity situation in the secondary market, dominance of the captive investors in the market retards the development of the secondary market. In comparison to government bond market, secondary market operations in the corporate bond market are at marginal level.

In addition, a debt securities trading system (DEX) has been introduced for government securities for secondary market trading of government bonds in the stock market. DEX trading is scrip less and

all transactions are carried out electronically. This DEX facility is also available for corporate bond listed with the stock exchange.

3. Bond Market Infrastructure

The priority of developing the bond market is to make sure that market structure including the legal and regulatory framework, clearing and settlement system and rating agencies are put in place to support the issue of bonds, investment process and trading activities in the bond market. A well-developed and robust market infrastructure is a pre-requisite for the development of an efficient bond market. A legal and regulatory framework and institutional set up are two fundamental pillars for a sound debt management system in the economy. In addition, enforcement of rating requirement and improvement of settlement and clearing systems help improve the attractiveness of the bond market, protecting both issuers and investors and minimize the default risk.

3.1 Regulatory Framework

A properly designed legal and regulatory framework plays a main role for the sound bond raising and management in the economy. The laws governing the government local bond market include Registered Stock and Securities Ordinance (RSSO), Monetary Law Act (MLA) and Annual Appropriation Act (AAA). The RSSO has empowered the Minister in charge of the subject of Finance to raise any amount of money by way of issuing Treasury bonds while the MLA has empowered the Central Bank to act as the agent of the government for the issuance of Treasury bond and management of public debt. The AAA approved by parliament authorizes the Central Bank to raise the total loans „in or outside Sri Lanka”, on behalf of the government, to finance the annual expenditure of the government. Accordingly, the AAA sets the upper ceiling of the annual bond issues (i.e. gross borrowing limit) and the MLA authorizes the Central Bank to issue Treasury bonds under the RSSO. In addition, the law governing the government‟s issuance of foreign currency denominated bonds {such as Sri Lanka Development Bonds – SLDBs} includes Foreign Loan Act (FLA).

The supervision and enforcement of regulations on the Treasury bond market operations are exclusively under the authority of the Central Bank. The existing regulatory framework covers the operations of primary dealers. However, all other players in the secondary market are outside the current regulatory system. The operational manual issued by the Central Bank to primary dealers provides guidelines to assess risks involved and is used to assess the soundness of primary dealer operations.

The structure of the public debt management offices, Public Debt Department (PDD) of the Central Bank has also been reformed in the recent past in order to handle growing complexities in the domestic debt market in a more efficient manner. Accordingly, functions of the department are broadly divided into five main divisions; front office (responsible for debt issuance), middle office (handling database management and research), back office (for servicing of debt), supervision division (supervise PD operations) and LankaSecure division (which handles SSSS and CDS) as done in most other countries that have developed debt markets.

The legal and regulatory framework for the prudent operations of corporate bond market includes the Registrar of Companies Act and regulations issued by SEC and CSE. In addition, Securities and Exchange Commission (SEC) of Sri Lanka has also issued regulations to permit specialized debt trading members to use the DEX to trade bonds in the stock market. All corporate bonds are required to register with the Registrar of Companies and have to be listed at the CSE under the existing regulatory framework.

Box 2 Directions Issued to Primary Dealers

The Central Bank as the agent of government in public debt management is responsible for the supervision of primary dealers to ensure an efficient, sound and safe primary dealers system (PDS). In order to achieve these objectives, the Central Bank has issued directions to primary dealers to promote their financial soundness and to adopt best practices in trading government securities. Major directions issued so far are listed below:

Direction on segregation of Proprietary Accounts into Trading and Investment Securities Account and the Revaluation of Trading Securities at market prices

Direction on Financial statements.

Direction on custodial holding of scrip securities Direction on Effective Two Way Quotes.

Direction on New Products.

Direction on Establishment of Branches Direction on Repurchase (Repo) Agreements. Direction on Capital Adequacy.

Direction on Forward Rate Agreement (FRA) and Interest Rate Swaps (IRSs).

Direction on Firm Two Way Quotes (Bid and offer prices) for Benchmark maturities. Direction on Accounting for Repo Transactions.

Direction on Minimum Subscription level for Treasury bills and Treasury bonds auctions. Direction on minimum capital requirement.

Direction on special risk reserve. Direction on short selling of securities. Direction on adjusted trading.

Risk management measurement of PDs.

Mark to market valuation of Treasury bills and Treasury bonds Intra structure Risk Weighted Capital Adequacy Framework

Permit to record customer transactions through cost from CBSL Wide Area Network

3.2 Clearing and Settlement System

An efficient and robust clearing and settlement system is vital for the development of the financial system and also for maintaining financial system stability in the economy. The clearing and settlement system in the domestic debt market moved to a more advanced payment system; the Real Time Gross Settlement System (RTGS) in 2003. With the introduction of the RTGS system, the manual payment and settlement system which was in operations was converted to a computer based electronic system. Under the RTGS system, transactions become final and irrecoverable after entries are recorded in the system. Present structure covers all key market participants namely, the Central Bank, commercial banks, primary dealers, EPF and Central Depository System of the CSE (total of 34 participants). The RTGS system settles large volume and time critical payments between direct participating institutions and customer to customer through direct participating institutions. In addition to operations of bond market, it includes transactions in the call market, government Treasury bill market, Central Bank open market operations and inter-bank net clearing.

Since 2004, Central Bank commenced SSS System to facilitate the online settlement of marketable government securities (both Treasury bonds and Treasury bills). In order to maintain settlement risk at zero level, Delivery Verses Payment (DVP) System was introduced for settlement process by connecting to the RTGS System. The SSS System operates through two-tier registering mechanism where Central Bank maintain the central registry as the top tier which is supported by designated sub registries. Meanwhile, sub registries maintain the registers for all non-bank institutions participating in the market.

Box 3

Recent Developments in the Payment and Settlement System

Year Event

1998 Establishment of Sri Lanka Automated Cleaning House (SLACH) 1994 Introduction of Inter-bank Payment System (SLIPS)

2002 Outsource the functions of SLACH and SLIPS and formed Lanka Clear (Pvt) Ltd. to undertake functions of inter-bank clearing system.

2003 Introduction of RTGS system

2003 Introduction of Automated General Ledger System (GLS) to the Central Bank 2004 Introduction of Treasury Dealing Room Management System to Central Bank 2004 Introduction of Scrip less Securities Settlement System (SSSS).

3.3 Local Credit Rating Agencies

Credit rating is an assessment of the creditworthiness of an issue of debt either by a corporate or a government that help investors to assess the quality of investments. In Sri Lanka, two rating companies are in operation now. The first rating company, Duff and Phelps Credit Rating Lanka (DCRL) was established in 1999, and subsequently became Fitch Ratings Lanka (FRL). The FRL is a joint venture with the Central Bank and other financial institutions. Later, a second rating company; Lanka Rating Agency (LRA) too commenced its operation in Sri Lanka. The LRA is a wholly owned subsidiary of Rating Agency of Malaysia Berhad (RAM), which is an affiliate of Standard and Poors (S& Ps). Both rating companies are recognized by the CBSL to carry out mandatory rating of organizations, which comes under its purview. Establishment of mandatory rating requirement would help to improve efficiency, transparency, stability and investor confidence in the bond market.

In 2003, government made credit rating and publication of such rating mandatory for all deposit taking institutions and all varieties of debt instruments other than those issued by the government. The main objective of this policy is to develop the corporate bond market keeping in mind the safety and security of the investments made by the public. Rating from an independent source enables the public to assess the risk involved in their investments. This mandatory requirement is applied to all corporate bond issues exceeding Rs.100 mn. The regulation of rating activities, including the regulation of rating fees, is entrusted to the SEC.

Since there is no guarantee either from a third party or collateral in the corporate bond market, a rating company plays an important role in helping investors to evaluate the default risk that helps to assess the possibility of risk of loss of their investment. Rating of any particular corporate is a reflection of its credit risk evaluation that improves the awareness of investors to choose bonds in the market. However, in this process, rating agencies are responsible to provide an effective, credible and independent credit rating system for the development of the bond market.

In 2005, Sri Lanka too obtained its first sovereign rating from two major international rating agencies. Fitch Rating assigned BB- for both sovereign long term findings and local currency rating with positive outlook while S & P assigned B+ for long term foreign currency rating and BB- for long term local currency. However, with the escalation of hostilities in the country resulted in revising the country‟s rating outlook from stable to negative in mid 2006. In 2007, S & P upgraded the + rating outlook to stable. The government has committed in the medium term macroeconomic