Fraud profile and fraud prevention in public sector: Internal audit perspective

Full text

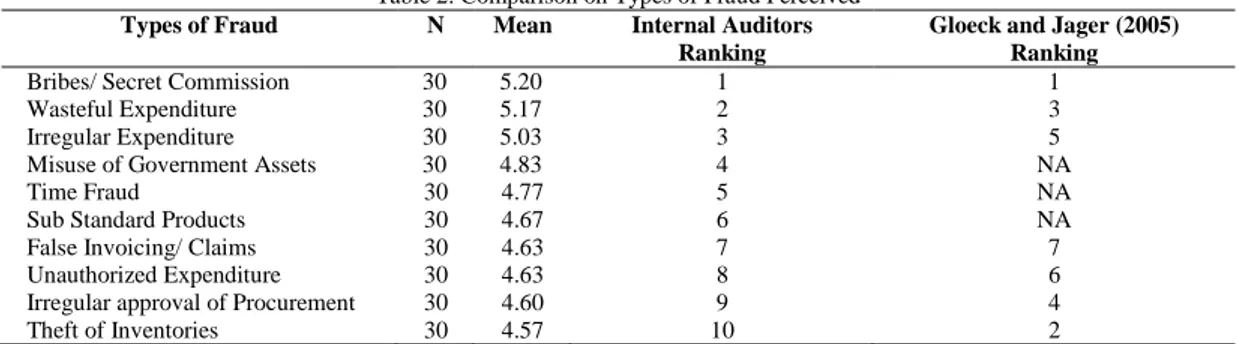

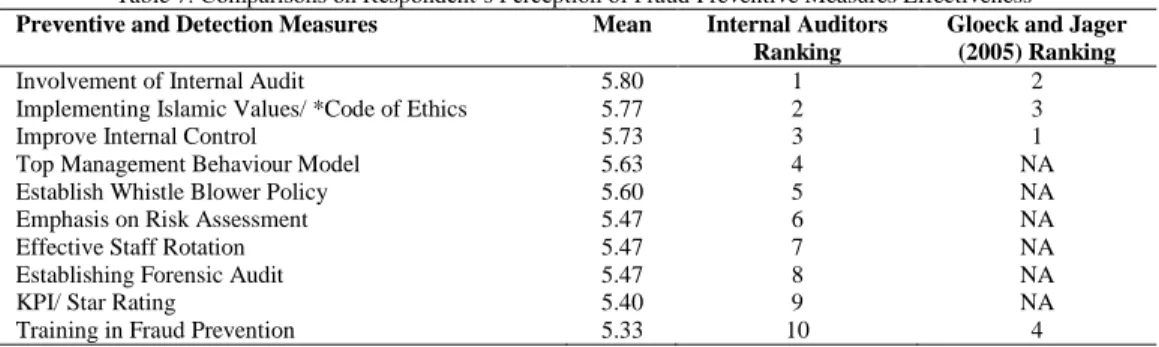

Figure

Related documents

Source: Lord & Benoit, LLC www.Section404.org.. Ten Steps IT Controls Effectiveness Of Controls Design of Controls Accounting Standards Mapping Risk Assessment Framework

In February, 2004, as part of a meeting with researchers at the Universidade Federal de Sao Paulo, Pacific Institute representatives were informed that the City of Diadema had

On our site, we plan to have the basic features of social networks, such as a wall, calendar, members, messaging, chat, and posts, along with customized features by the

The biggest change in our welfare estimates comes when we modify the baseline case to assume that, in addition to the 20 percent of wealth in a private annuity, 50 percent of wealth

However, while the notion of moral identity potentially offers a fresh approach to understanding ethical behaviour in a business context, through the study of an individual-

We focus on the use of foreign currency derivatives and interest rate derivatives because they are directly related to the management of cross-border M&A risk exposures.

Tidsskrift for Arbejdsliv, Human Technology, Scandinavian Journal of Information Systems, Nordiska Organisations Studier, Medical Technology Assessment at Danish National Board

Products in this section have been tested by UL and shown to meet the construction and performance requirements of UL Standard Number 98, Enclosed and Dead Front Switches. —Meet