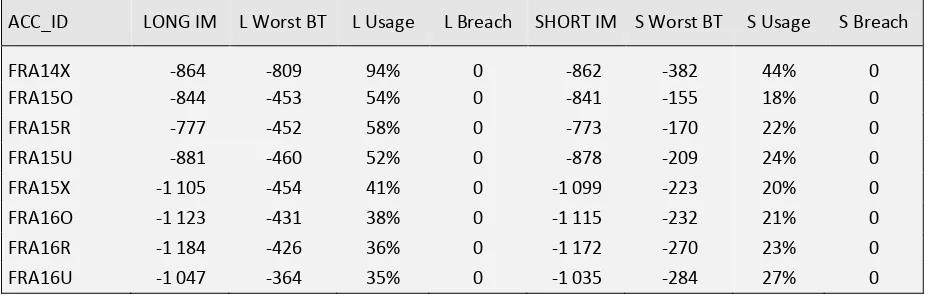

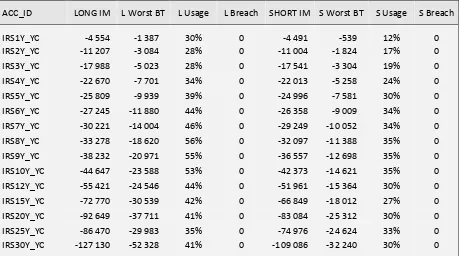

Validation of CFM A validation of the Margin Model CFM for interest rate products used by Nasdaq OMX

Full text

Figure

Related documents

For interval-valued intu- itionistic fuzzy multicriteria group decision-making problem with incomplete information on the weights of criteria, an entropy weight model is established

In this present study, antidepressant activity and antinociceptive effects of escitalopram (ESC, 40 mg/kg) have been studied in forced swim test, tail suspension test, hot plate

Satcom and IT Engineering and Management Consulting, Program & Project Management, Technical Support Services, Satcom and IT network design, installation and maintenance

EMT: Epithelial-to-mesenchymal; EndMT: Endothelial-to-mesenchymal transition; HFD: High-fat diet; HUVECs: Human umbilical vein endothelial cell line; LDL-C: Low-density

This gives us the possibility to observe the features selected by different feature selection approaches and to assess classification performance of different classification

According to that idea, this paper proposes a model for estimating VoIP quality provided by G.729, a common codec used over WAN, that has been created from subjective Mean

The observed difference compared with integrated buoyant jet models can be attributed to four possible effects: (i) entrainment of turbulent kinetic energy from the ambient