Value Capture and Value Creation in

High-Velocity Networked Environments

Hannu Tuomisaari, Juhana

Peltonen, Timo R Nyberg

Business, Innovation andTechnology

School of Science, Aalto University Espoo, Finland

Xisong Dong

The State Key Laboratory of

Management and Control for

Complex Systems

Institute of Automation, Chinese

Academy of Sciences

Beijing, China

Göte Nyman

Institute of Behavioral Sciences University of Helsinki

Finland

Abstract— The core function of any profitable firm is capturing a share of the value that customer perceives in the firm’s offering. Value capture is traditionally considered to relate to a competitive advantage at the firm level, but not the firm network level. However, the ever increasing role of information and knowledge in today’s economy is profoundly changing how firms can create competitive advantages. Among these changes, we highlight reducing transaction costs in various areas of the economy, which drives the economy to organize more toward rapidly evolving networks or smaller firms. There is also an opposite trend for some internet firms to become larger due to economies of scale and due to network externalities. In this position paper, we examine the issue of value capture by firms that are increasingly small and operate in rapidly changing and evolving networks. We conclude by outlining future research on firm-level capabilities that are required to enable value capture in new forms of dynamic networks.

Keywords—value; value creation, value capture, resource-based theory, trasaction cost economics

I. INTRODUCTION

The core function of any profitable firm is capturing a share of the value perceived by the customer in its offering. In perfectly competed markets, all profits are competed away instantly leaving companies to operate at zero margins. However, in the real economy, there are various barriers to competition that enable firms to create economic rents. Broadly speaking, economic rents refer to the profits that firms can generate in the presence of factors that somehow limit the existence of perfectly competed markets. Naturally, profit is a manifestation of value captured.

Typical sources of economic rents include land, real estate, and legally enforced limitations to competition in some industries or regions. Considering the broader phenomenon of performance differences, the field of strategic management has empirically identified firm-level phenomena, rather than industry level phenomena, to be their most important source [1], [2]. On the firm (or

business unit) level, resource-based theory [3], [4], [5], [6], [7], [8] has become a dominant paradigm to explain variations in economic performance.

Under resource-based theory, heterogeneously distributed, rare and valuable resources and capabilities explain why some firms perform better than others. These performance differences can persist depending on the strength of various isolation mechanisms, which prevent competitors from imitating or finding substitute resources and capabilities.

Over time, several different types of resources and capabilities have been suggested, that may contribute to a competitive advantage. These include firm culture, research and development capabilities, tacit knowledge, brands and other intellectual property. Several phenomena can act as isolation mechanisms that protect these resource advantages, such as time compression diseconomies [9] that shield first movers from competition by making it increasingly costly for competitors to catch up. Matters like causal ambiguity and social complexity may obfuscate the true source of competitive advantage to the point, where competition cannot copy the advantage because even the firm itself holding the advantage does not know the reason for its superior performance [9].

Overall, ‘classical’ resource-based theoretical thinking encourages managers to develop strong positional advantages that once created, enable above normal revenue by shielding the firm from competition. However, for over a decade, this approach has been challenged, and a number of scholars question the existence of sustained competitive advantages. They argue that competitive advantages result from the ability to continuously develop new short-lived advantages (e.g. [10], [11], [12]). Another development worth noting is that economic activity is increasingly conducted by networks of firms compared to individual firms, meaning that the sources of competitive advantage need to be viewed at the firm network level as well.

II. TRENDS SHAPING THE GLOBAL ECONOMY This work is supported in part by NSFC (National Science Foundation

of China) projects 61233001, 71232006 and Tekes - the Finnish Funding Agency for Technology and Innovation, project 2439/31/2012.

In this paper, we follow along the lines of this intellectual evolution in viewing competitive advantages and value capture. One of our goals is to discuss the nature of competitive advantages and value capture in the mid-term future, and the unit of interest moves more from the individual firm toward networks of firms. To accomplish this, we assume that several technological and societal trends today will continue to gain more momentum, and lead to changes in the broader economic landscape. In the spirit of literature that emerged around the early 1990s [13], [14], we consider (i) how information and communication technology is reducing transaction costs in the economy, but also (ii) how the same is creating economies of scale in information-intense areas, such as social networking and online advertising.

Transaction cost economics [15], [16] has emerged to explain why firms internalize certain activities (resort to ‘hierarchy’), and use open markets in others. According to transaction cost economics, firm boundaries exist where transaction costs are minimized. It has been proposed that information and communication technology generally reduces transaction costs (e.g. [15], [16], [17]), which under transaction cost economics implies that firms can be smaller and buy more inputs and sell outputs on competed markets. Empirical evidence indeed suggests that information and communication technology has made firms smaller [18], [19].

However, the implications of information and communication technology in transaction costs are not only around the hierarchies and markets (i.e. ‘make or buy’) dichotomy. Williamson [20] argues that between these extremes there are hybrid forms of organizations. In this space, Powell [21] discusses networked forms of organizations, whose emergence is driven by the existence of distinct knowhow and the demand for speed. From this perspective, information and communication technology not only acts as a disintegrating force to vertically integrated firms, but makes it more feasible for firm networks to exist in their place, rather than only promoting the use of markets to conduct transactions.

While information and communication technology is a force that drives some organizations to become smaller, in some cases, the opposite may be the result. Grant [22] points out that firm boundaries surround organizational entities where knowledge integration and application can be most effectively conducted. When information and knowledge are in question, economies of scale in integration and application can be significant. Economies of scale in information are closely related to positive network externalities [23], which set the stage for the emergence of large information-based firms like Google and Facebook. In addition, Liu and Chen [24] find that economies of scale in know-how have positive influence on firms' business performance, which helps private firms to strengthen their market power in China.

Taken together, we believe that these developments further increase the division of labor leading to smaller specialized organizations that interact more closely with

each other and collectively cooperate and compete with larger firms. In the case of large internet firms, strategic thinking about value capture may perhaps revolve more around traditional resource-based theory thinking.

In order to maximize potential to learn about qualitatively new phenomena that may over time come to be more common and relevant in the economy, we focus on small, specialized firms whose value capture draws strongly on being part of a network of firms. Due to their smaller size, these firms are less likely to enjoy strong “winner takes all” network externalities. Furthermore, these firms’ inclination towards other firms emphasizes the value of getting access to resources rather than owning the resources themselves. This places a premium on pursuing novelty, efficiency and finding complementarities by accessing resources from a network of firms [23]. While positional advantages may be difficult to create and maintain, these firms must renew themselves constantly by using firm networks as their playing field. They may also be able to enforce their position by building an effective intellectual property portfolio [25]. This has been true in the parts of world where IPR laws are well established, and recently also in countries like China, where IPR legislation is relatively new.

III. VALUE CREATION

A proactive and anticipative approach to value creation and value network building require a strong foresight to customer behavior and orientation. In the traditional approach, motivation, plans, beliefs, and need hierarchies [26], [27], [28] have typically been used to describe customer orientation and preferences. However, in the future high-velocity environment and with the trend of addressing increasingly higher-level customer needs globally it becomes necessary to widen the customer models to include the perspectives to the quality of life and higher level consumer values. Gelter [29] for example, has introduced the concept of experience production that represents value creation in the experience realm that has an increasingly significant value on the present and future digital markets.

For the purpose of this discussion, we choose a straightforward definition of value creation in order to isolate the research questions concerning value capture.

Value creation is the basis of modern business thinking [30] and it is a central concept in a lot of research since Aristotle [31]. Leaving the philosophical and political economic discussion aside, we seek a baseline for our research in a notion of value that would ultimately encompasses the process of satisfying a customer to generation of wealth for the service providers and manufactures of physical goods (value contributors).

A definition of value is difficult to come by in a way that all view points are satisfied - ever more so, when the definition of value creation is attempted [32]. In pursuit of a definition of value creation, we chose the definitions of use value and exchange value. Both are discussed in [33] and we like to concur with those definitions. To stress our point

concerning value creation, we depart from the tradition of focusing on the value of company assets. The reader is advised to take note of the discussion on this aspect, in [33]. Our definition of value creation does not differ from [32], but it is rephrased in a simple form as follows:

A. Definition: Value creation

Value creation is the process of addressing a customer's non-trivial need by a firm or group of firms, by offering a product or service that he/she uses for her own perceived satisfaction. The process of value creation will differ based on whether value is created by an individual, an organization or society [32].

In our discussion of use value, we also make note of the so-called “service-dominant logic” [34] and the concept of value co-creation embraced by it. According to this perspective, the process of creating value for the user is always an interaction between the service provider and the customer. Service-dominant logic treats products as artifacts that encapsulate services. The network perspective we emphasize highlights that there may be more than one firm (and potentially more than one customer) that nearly simultaneously participate in the creation of use value, i.e. the benefit experienced by the user(s). Collectively, we refer to the firms (and users) that participate in the creation of value as value contributors.

B. Definition: Use value

Value that the customer subjectively assesses when making use of the product (service or physical good) for his/her own particular reasons [33].

C. Definition: Exchange value

Value can be measured at the moment of transaction between the seller and the buyer. Value as it is realized at the point of sale [33] does not involve a process of value creation, but rather it anticipates, or estimates the potential of the product and certainly provides the actual income to be divided between service providers and manufacturers of physical goods.

The difference between use value (the value experienced by the user) and exchange value (the monetary sum the user is willing to pay) is sometimes referred to the user (or consumer) surplus, which users aim to maximize.

Further, we expect the "velocity" of value creation and capture to increase by orders of magnitude from today’s prevailing business environments. Moreover, dynamism is caused by continuously changing configurations of small firms as they seek access to resources.

It should be noted that a company as a value contributor should not be afraid of explaining their mission in terms of "creating value to customers" - the statement is colloquial in essence and as such its meaning is admirable. But use value cannot be delivered to the customer by any firm alone. It will only be realized by the customer by perception that may or may not be induced by the promise or the use of the offering.

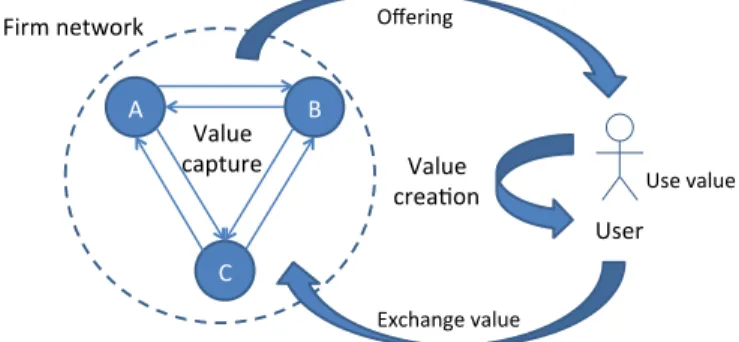

The relationship of a dynamic value network of firms and a user of their offering is depicted in the figure 1. Value creation is shown to be pertinent to the user's context. Next, we discuss value capture, which we consider to be a concept of the firm and the network of firms.

Fig. 1. Firm network, relation with user and value

IV. VALUE CAPTURE

Value capture by firms is equal to the exchange value of an offering minus the costs of production, i.e. the profit margin. However, as we are no longer dealing only with individual firms, but a network of firms, of which several may interact with the user in the value creation process, value capture must also consider revenue sharing within the firm network. Taken together, the captured value of the firm network (for a given transaction) is equal to the exchange value minus total costs, but at the firm level, it is equal to their share of exchange value obtained minus their share of all costs. In high technology industries and in service industries based on high technology the share of exchange value is significantly boosted by the ownership of intellectual property [35].

These considerations highlight special aspects within our previous discussion about economic rents and unique firm capabilities, as the relationship between a firm’s contribution to value creation and the exchange value it obtains in a network can be greatly disconnected.

As we noted, the firm’s ability to capture a share of revenue in the firm network, which closely relates to its competitive advantage and the ability to capture rents (in a traditional resource-based theory sense), is most likely to be increasingly temporary in the future. Further, if the small networked firms that are of our primary interest are inclined to access other firms’ resources rather than owning them, their continued ability to capture value lies on continuously creating network relationships that enable creating high value to the customer, while maintaining a position in the network that allows it to capture a proper share of the resulting exchange value. Again, if the firm has an effective intellectual property portfolio, it may prolong its competitiveness and the firm may enjoy a greater share of the network’s revenues for longer.

Any single firm in the network cannot appropriate a disproportionately high share of the network’s revenue

indefinitely. In other words, any single firm must also consider the value capture of the firm network while it considers its own value capture, even while capturing a high share of value would be possible in short-term.

In addition to direct economic value, firms in the network (the customers they serve alike) may capture important value that is not directly and immediately economic. This indirect value, which can be characterized as some type of relational capital (cf. [36]), may in long-term be an important prerequisite of eventual economic value capture. Motivation for pursuing indirect economic value may be based on gains in e.g. knowledge, information, customer-base and market share.

The network approach brings issues like organizational conflict and agency problems from inside firms to the firm network level, adding another layer of dynamism. Certain firms may be disproportionately effective in participating in this network-level politics, and driving events in their favor beyond what conventional strategic analysis might suggest. Taken together, this brings a premium to firms that are consistently able to foresee a broad range of developments in their networked environment, possibly influence these external developments and obtain valuable positions in order to maximize value capture in the long run.

These issues point out that dynamism in business networks is an evasive phenomenon to manage with traditional management means. For example, it will not be adequate to conduct a market research study for one month, report the results back to the headquarters in another two months and launch a consequential product development project to meet the changing market demand in another 18 months' time.

One example of the dynamic kind of operating model is the fast-fashion garments enterprise Zara [37]. The case study is revealing in the sense that it was considered both important and interesting in the Supply Chain Forum in 2000. In fact, it is the background for our research as well: traditional supply chain, or distribution chain, practices, methods and disciplines are proving insufficient in high-velocity markets that constantly change and transform themselves across the globe.

Physical goods are being integrated in solutions and service concepts and as such are inseparable from them. Service-dominant logic actually states that even the most primitive piece of hardware, like a hammer, is actually an embodiment of a service that is rendered by using it [34]. The blurring of services and goods is evident in modern smart phone service concepts that invariably include audiovisual contents, navigation and points-of-interest services as well as office applications - not forgetting synthetic voice assistants.

As is the case with the concept of value and value creation, value capture is a concept that we seek to understand from several different viewpoints [30], [32], [33]. We cannot be satisfied by the notion of value chain [30] and the view that, along the chain at each stage value is added based on price of purchased resources from the

previous stage. On the other hand, we don't find it enough to discuss division of revenues (exchange value) as the only point of view of value appropriation within dynamic value networks.

We find interesting research on value appropriation from the view points of platform, architecture and modular design as well as intellectual property. See e.g. [25], [35], [38].

V. CAPABILITIES OF CAPTURING VALUE IN DYNAMIC VALUE NETWORKS

The reason to study dynamic value networks is to find out how they are good for business. For some firms, they are, indeed, a matter of survival. In our view, the measure of good-for-business is the value capturing capacity of the business model of each value contributor in their own right, and the super-business model of the dynamic value network as a whole - no matter how fluid and flexibly structured it may be.

We foresee that in mid-term, customer needs are being satisfied faster, and services are offered and consumed in new, probably more complex constellations. Higher-level customer needs are being addressed. Fast speed and complex offerings of goods, content and services require more and more companies to work in cooperation and the networked business will have to be dynamic instead of fixed. Furthermore, automation in new generations of service business platforms is anticipated to move to new operational areas and previously automated services will be likely to experience transformation into faster and more dynamic technologies.

It is our hypothesis that value capture is the single most important factor of dynamic value networks in terms of business motivation and guarantee of commitment, in circumstances where there just is no time to build rigid and heavy contractual legal and organizational structures. For instance, it will not stand as an option to start all product development from scratch every time a new signal from the market is observed. This phenomenon is strikingly obvious in the Internet's social media services. There, user-centered design has undergone evolution towards co-development with a very short distance between actual users of service and the developers [39].

In order to advance research on this topic, we need to understand the broad question of what are the capabilities required of value contributors individually, and of the dynamic value network as a whole, to manage value capture, and how do these capabilities come into existence and developed further?

Based on our review, we argue that investigating this issue relies strongly on understanding how information is managed in the network of firms. In particular, how is information about value capture collectively obtained, distributed, and processed so that the relevant value contributors of the value network can promptly act to enable customer's value creation and capture value? Further, as the networks are undergoing constant flux, we should further study that what are the means to manage value capture in a

dynamic value network, where the number and configuration of entities and the life time of their relations is not constant? This question also involves asking that what are the limits of individual firms to influence this process, and how this influence is dependent on the firm’s properties.

VI. CONCLUSIONS

As is the case with the concept of value and value creation, value capture is a concept that must be understood from several different viewpoints [30], [32], [33].

To help small firms execute in high-velocity markets and value creation, enabling elements and capability requirements must be identified. In this working paper on value capture, we have identified a number of considerations for dynamic value network capabilities, which we believe should be studied and elaborated further:

1) What is the most appropriate definition of value capture in general?

2) How is each value contributor’s value capture defined in a new way so as for the firm to justify its participation in dynamic and networked value creation?

3) What are the new means to communicate and manage value capture globally, across geographies, cultures and markets that enable agile and fast value creation?

4) What are the new customer models of behavior and orientation that enable proactive addressing of higher-level customer needs?

5) How does indirect, or deferred, value capture play out in dynamic value networks? E.g. the case of allowing loss in the early stages of a startup firm while expecting profit in future.

ACKNOWLEDGMENTS

The authors acknowledge the valuable discussions that have taken place in the course of the past year within the dynamic value networks team. We thank Tekes, Nokia and Stora Enso for their support in making the Dynamic Value Networks Project a reality.

REFERENCES

[1] R. P. Rumelt, “How much does industry matter?,” Strategic Management Journal, vol. 12, no. 3, pp. 167–185, Mar. 1991. [2] A. M. McGahan and M. E. Porter, “How much does industry

matter, really?,” Strategy: critical perspectives on business and management, vol. 2, no. I997, p. 260, 2002.

[3] E. T. Penrose, The theory of the growth of the firm, 3rd ed. Oxford University Press, USA, 1959.

[4] B. Wernerfelt, “A resource-based view of the firm,” Strategic Management Journal, vol. 5, no. 2, pp. 171–180, 1984. [5] M. A. Peteraf, “The cornerstones of competitive advantage: a

resource-based view,” Strategic management journal, pp. 179– 191, 1993.

[6] J. B. Barney, “Strategic factor markets: Expectations, luck, and business strategy,” Management Science, vol. 32, no. 10, pp. 1231–1241, lokakuu 1986.

[7] J. B. Barney, “Firm resources and sustained competitive advantage,” Journal of Management, vol. 17, no. 1, 1991.

[8] R. Amit and P. J. . Schoemaker, “Strategic assets and

organizational rent,” Strategic Management Journal, vol. 14, no. 1, pp. 33–46, 1993.

[9] I. Dierickx and K. Cool, “Asset stock accumulation and sustainability of competitive advantage,” Management Science, vol. 35, no. 12, pp. 1504–1511, Dec. 1989.

[10] D. J. Teece, G. Pisano, and A. Shuen, “Dynamic capabilities and strategic management,” Strategic management journal, vol. 18, no. 7, pp. 509–533, 1997.

[11] D. J. Teece, “Explicating dynamic capabilities: the nature and microfoundations of (sustainable) enterprise performance,”

Strategic Management Journal, vol. 28, no. 13, pp. 1319–1350, Dec. 2007.

[12] K. M. Eisenhardt and J. A. Martin, “Dynamic Capabilities: What Are They?,” Strategic Management Journal, vol. 21, no. 10/11, pp. 1105–1121, Oct. 2000.

[13] V. Gurbaxani and S. Whang, “The impact of information systems on organizations and markets,” Communications of the ACM, vol. 34, no. 1, pp. 59–73, Jan 1991.

[14] T. W. Malone, J. Yates, and R. I. Benjamin, “Electronic markets and electronic hierarchies,” Communications of the ACM, vol. 30, no. 6, pp. 484–497, 1987.

[15] R. H. Coase, “The nature of the firm,” Economica, pp. 386–405, 1937.

[16] O. E. Williamson, “The economics of antitrust: Transaction cost considerations,” University of Pennsylvania Law Review, vol. 122, no. 6, pp. 1439–1496, 1974.

[17] B. L. Xu, “‘知识经济条件下的网络组织运作模式研究’ [Knowledge economy under the conditions of the mode of operation of the network organization],” Modern Finance & Economics, vol. 22, no. 2, 2002.

[18] E. Brynjolfsson, T. W. Malone, V. Gurbaxani, and A. Kambil, “Does Information Technology Lead to Smaller Firms?,”

Management Science, vol. 40, no. 12, pp. 1628–1644, Dec. 1994. [19] L. M. Hitt, “Information technology and firm boundaries:

Evidence from panel data,” Information Systems Research, vol. 10, no. 2, pp. 134–149, 1999.

[20] O. E. Williamson, “Comparative economic organization: The analysis of discrete structural alternatives,” Administrative science quarterly, vol. 36, no. 2, 1991.

[21] W. W. Powell, “Neither Market nor Hierarchy: Network Forms of Organization,” 1990.

[22] R. M. Grant, “Toward a Knowledge-Based Theory of the Firm,”

Strategic Management Journal, vol. 17, pp. 109–122, 1996. [23] R. Amit and C. Zott, “Value creation in e-business,” Strategic

Management Journal, pp. 493–520, 2001. [24] H. J. Liu and C. M. Chen,

“‘企业组织资本、战略前瞻性与企业绩效:

基于中国企业的实证研究’ [Organizational capital, strategic

prospective and Firm Performance: An Empirical Study Based on Chinese Enterprises],” Management World, no. No. 5, pp. 83–93, 2007.

[25] A. Leiponen and J. Byma, “If you cannot block, you better run: Small firms, cooperative innovation, and appropriation strategies,”

Research Policy, vol. 38, no. 9, pp. 1478–1488, Nov. 2009. [26] A. H. Maslow, R. Frager, and J. Fadiman, Motivation and

personality, vol. 2. Harper & Row New York, 1954. [27] G. A. Miller, E. Galanter, and K. H. Pribram, Plans and the

structure of behavior, vol. 960. Holt New York, 1960.

[28] U. Neisser, Cognitive psychology, vol. 4. Appleton-Century-Crofts New York, 1967.

[29] H. Gelter, “Towards an understanding of experience production,”

Articles on experiences, vol. 4, pp. 28–50, 2006.

[30] A. M. Brandenburger and W. S. Harborne Jr, “Value-based business strategy,” Journal of Economics & Management Strategy, vol. Volume 5, no. Issue 1, p. pages 5–24, Mar. 1996.

[31] B. J. Gordon, “Aristotle and the Development of Value Theory,”

Quarterly Journal of Economics, vol. 78, no. 1, pp. 115–128, Feb. 1964.

[32] D. P. Lepak, K. G. Smith, and M. S. Taylor, “Value Creation and Value Capture: A Multilevel Perspective.,” ACAD MANAGE REV, vol. 32, no. 1, pp. 180–194, Jan. 2007.

[33] C. Bowman and V. Ambrosini, “Value Creation Versus Value Capture: Towards a Coherent Definition of Value in Strategy,”

British Journal of Management, vol. 11, no. 1, pp. 1–15, Mar. 2000.

[34] S. L. Vargo and R. F. Lusch, “Evolving to a new dominant logic for marketing,” Journal of marketing, pp. 1–17, 2004.

[35] J. Ali-Yrkkö, Ed., Mysteeri avautuu - Suomi globaaleissa arvoverkostoissa [The Mystery Unravels: Finland in Global Value Networks]. Helsinki: Taloustieto Oy (ETLA B257), 2013. [36] J. H. Dyer and H. Singh, “The relational view: Cooperative

strategy and sources of interorganizational competitive

advantage,” Academy of management review, pp. 660–679, 1998. [37] K. Ferdows, M. Lewis, and J. A. D. Machuca, “Zara,” Supply

Chain Forum: International Journal, vol. 4, no. 2, pp. 62–66, Jun. 2003.

[38] “Modularity for Value Appropriation--How to Draw the Boundaries of Intellectual Property — HBS Working Knowledge,” 12-Jan-2011.

[39] M. Johnson, “How Social Media ChangesUser-Centred Design - Cumulative and Strategic User Involvement with Respect to Developer–User Social Distance,” 2013.