2019 International Conference on Information Technology, Electrical and Electronic Engineering (ITEEE 2019) ISBN: 978-1-60595-606-0

What Kind of Online P2P Lending Platforms Are More Likely to

Have Problems

Kang-yu REN

1and Chun-yan GONG

2,*1

International Business School, Beijing Foreign Studies University, Beijing, China

2

Shanghai Tubiaojia Internet Technology Company, Shanghai, China

*Corresponding author

Keywords: P2P lending platforms, Problem platforms, Binary regression model.

Abstract. This paper aims to discern the characteristics of problematic P2P lending platforms. We collected the information of 650 platforms from P2P websites manually and defined 16 variables in five dimensions. Then we used binary regression model to figure out which variables significantly influence the probability of a platform being problematic. Results show that existing time, bank custody, the number of executives with financial working experience, guarantee, annual rate, ICP certificate, backer and the type of products that the platforms offer are significant variables. Particularly, this paper discovers that the platforms offering house mortgage or car loan are less likely to have problems while those offering SEM loan are relatively riskier.

Introduction

Originally imported from western countries, online peer-to-peer lending in China has seen its prosperity since 2007. However, problem platforms are also sharply increasing as the number and scale of P2P lending platforms shoot up. Problems that these platforms have can be separated into three types—insolvency, running off and being closed up for rectification. Reason why they have problems varies according to the type of the problem. First, some platforms’ problems are caused by poor management and inadequate risk control. Second, several platforms are closed up because they failed to meet legal requirements. Third, a group of platforms made off with money purposely.

This paper is going to find out the factors that could influence the possibility of P2P’s having problems, by using the binary logistic regression model.

We are making two major contributions by this paper. First, it finds that platforms with ICP (Internet Content Provider) certificate are less likely to fall down, which strengthens the necessity of ICP certificate. Second, it discovers that platforms offering house mortgage or car loan can decrease the probability of having problems.

Literature Review

The dread situation of problematic platforms worries many researchers. We need to find out the characteristics of P2P platforms first, then their risks, including both platform risks and credit risk.

Platform Characteristics

Platform Risks

The risks come from three parts—the platform itself, borrowers and then the environment (Ma & Wang, 2016) [2]. The risks from the platform itself include strategy risk, operation risk, information technology risk and reputation risk. And the risks from the environment are policy risk and competition risk. And the risk from borrowers is credit risk (Li & Wang 2016) [3]. The credit risk is most likely to happen, followed by technology risk, operation risk, internal management risk and market risk etc. (Zhang & Zhang, 2015) [4].

Credit Risk

Just like in financial market, when lending out and borrowing money online, there exists information asymmetry between the borrowers and the lenders (Klafft, 2008) [5]. Because people are anonymous on the Internet, they are more likely to default (Greiner; Wang, 2009) [6]. Moreover, because online P2P lending has the problems of low access threshold, lack of supervision, lack of information transparency and unsound risk control, that the borrowers default and the platforms run away happens from time to time (Emekter Riza, Tu, Jirasakuldech Benjamas, Lu, 2015) [7].

Theory Analysis and Hypotheses

Information Asymmetry

When making decisions in transactions, one party has more or better information than the other. This asymmetry leads to an unbalance of power which can sometimes cause the transactions to go awry. Therefore, P2P lending platforms are expected to help reduce the information asymmetry by discern and kick out bad borrowers. However, this requires good management and operation of the P2P lending platform. So still information asymmetry is one of the worst problems faced with P2P lending platforms (Ge, et al, 2017)[8]. The transaction happens on an internet platform, on which people only release limited information about themselves. Investors are not able to know enough information about the borrowers and they cannot discern the authenticity of the information because they don’t have much time or are not able to get access to the borrowers' personal information.

Particularly, moral hazard is more popular in the risks resulting from information asymmetry. In online P2P lending, moral hazard happens under two circumstances where investors always bear the cost of risks. First, borrowers may have opportunistic behavior that they may conceal their real purpose of lending money and spend the money on riskier activities because they have information superiority than the investors (Xu, et al,2017) [9]. Second, platforms also have moral hazard. For example, they may introduce a new financing product with the intention of illegal fund-raising or they may misappropriate investors’ money (He, et al.2017) [10]. Therefore, to reduce the risks of P2P lending platforms requires good control of moral hazard.

Hypotheses

Based on the literature and our theoretic analysis, we therefore raise the following hypotheses: H1: The longer a platform exists, the less probable that it has problems.

H2: The higher the management level is, the less probable that the platform has problems.

H3: If the platform uses its own money as guarantee, it’s more likely to have problems; if the platform sets aside risk reserves and or has the third party as guarantees, it’s less probable to have problems.

H4: If a platform has more registered capital or has a backer or an ICP certificate, it’s less probable to have problems

Empirical Test and Result Analysis

Data Source

We manually collected the information of 650 P2P lending platforms from the websites of WDZJ and P2P eye. Among them 560 platforms became our data samples: 100 are problem platforms and 460 are normal platforms. Each platform has existing time, registered capital, bank custody, ICP certificate, guarantees, number of senior executives who had financial working experience before, number of senior executives who own a master’s degree or above, backer, average annual rate and at last, the number and the types of lending products the platform provides.

Variables and Statistical Description

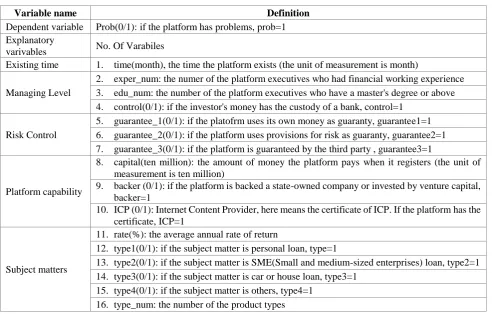

[image:3.595.54.547.275.589.2]Each platform has 11 characteristics, based on which this paper defines 17 variables: 1 dependent (binary) variable and 16 explanatory variables (5 dimensions).

Table 1. Definitions of Variables.

Variable name Definition

Dependent variable Prob(0/1): if the platform has problems, prob=1 Explanatory

varivables No. Of Varabiles

Existing time 1. time(month), the time the platform exists (the unit of measurement is month)

Managing Level

2. exper_num: the numer of the platform executives who had financial working experience 3. edu_num: the number of the platform executives who have a master's degree or above 4. control(0/1): if the investor's money has the custody of a bank, control=1

Risk Control

5. guarantee_1(0/1): if the platofrm uses its own money as guaranty, guarantee1=1 6. guarantee_2(0/1): if the platform uses provisions for risk as guaranty, guarantee2=1

7. guarantee_3(0/1): if the platform is guaranteed by the third party , guarantee3=1

Platform capability

8. capital(ten million): the amount of money the platform pays when it registers (the unit of measurement is ten million)

9. backer (0/1): if the platform is backed a state-owned company or invested by venture capital, backer=1

10. ICP (0/1): Internet Content Provider, here means the certificate of ICP. If the platform has the certificate, ICP=1

Subject matters

11. rate(%): the average annual rate of return

12. type1(0/1): if the subject matter is personal loan, type=1

13. type2(0/1): if the subject matter is SME(Small and medium-sized enterprises) loan, type2=1 14. type3(0/1): if the subject matter is car or house loan, type3=1

15. type4(0/1): if the subject matter is others, type4=1 16. type_num: the number of the product types

The overall descriptive statistics of the explanatory variables are listed below (The observations of all these variables are 560.):

Table 2. Results of Descriptive Analysis.

No. Mean Median Minimum Maximum No. Mean Median Minimum Maximum

1 30.79 30.00 1.00 119.00 9 0.30 0.00 0.00 2.00

2 2.27 2.00 0.00 11.00 10 0.21 0.00 0.00 1.00

3 1.01 1.00 0.00 5.00 11 0.11 0.11 0.00 0.20

4 0.20 0.00 0.00 1.00 12 0.38 0.00 0.00 1.00

5 0.36 0.00 0.00 1.00 13 0.45 0.00 0.00 1.00

6 0.56 1.00 0.00 1.00 14 0.68 1.00 0.00 1.00

[image:3.595.58.538.632.800.2]If we compare the 100 problem platforms and 460 normal ones, there are some systematic differences. The normal platforms have more registered capital, longer existing time, more experienced and educated senior members and bank custody. And they usually have ICP certificates and have the third party as guarantee.

By doing correlation analysis, Time, capital, control, ICP, guanrantee2, guarantee3, exper_num,

edu_num, backer and type_num are all negatively correlated with the probability of having problems,

which comply with the hypotheses. Guarantee1 and rate are positively correlated with prob, which is

also consistent with the hypotheses.

Regarding the four type variables, type1 and type3 are negatively correlated, which means offering

personal loan or house mortgage and car loan may decrease the probability of closing down. Type2

and type4 are positively related, so SEM loan and other loans are riskier.

However, type_num is highly correlated with type1, type2, type3 and type4. And then the

multi-collinearity test was made to confirm type_num as a redundant variable. So it was deleted from

the regression model.

Binary Logistic Regression Model

The model dealing with binary variables is called binary logistic regression. Compared with linear regression, binary regression has no requirement for the distribution mode of the variables and can predict the probability of happenings. Since our dependent variable is whether a platform has

problems, which is a binary variable, so we can use Logistic model and Probit model to estimate the

factors that lead to a platform’s closure.

A binary Logit model is ln(p/1-p) = i= i+𝜺, where p is the probability that a platform has

problems; is a constant; 𝛽 is the coefficient of each explanatory variable. When xi changes a unit, y

changes 𝛽 units; 𝜺 is the error term.

Since this paper has separated all the variables into 5 dimensions, 5 Logit models are devised to

study the effects of 5 dimensions one by one.

The first Logit model includes time as the only one explanatory variable. The second model adds

the three variables from the dimension of managing level. The third model adds the three variables from the dimension of risk control; the fourth model includes the three variables from the dimension of platform capability. The fifth one includes the first five variables from the dimension of subject matters.

Probit regression model is no different from logistic model basically. But the Probit model applies to normal distribution while logistic model applies to logistic distribution.

Results Analysis

Then we did the regressions for the explanatory variables group by group to see how they influence the independent variable. The results are presented in the table below:

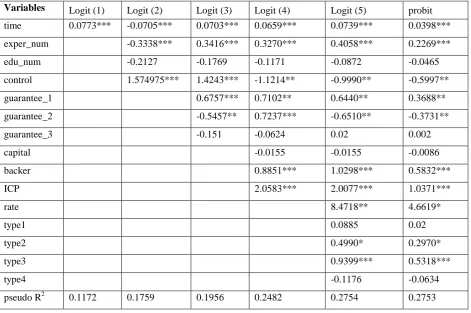

The coefficient in Logit (1) is negative and significant on the level of 1%, denoting that the longer a platform exists, the less probable it has problems. Logit (2)’s result also complies with our expectation. People who had financial experience before know how to manage their team and control the risk. Also, presumably, if they have higher education degrees, they tend to manage the platform better. What’s more, if a platform has bank custody, the ratio of having problems is about 1/5 that of those don’t. Putting the investors’ money into the bank custody account will effectively prevent the platform from misappropriating it. This is why the government is urging all platforms to have bank custodies nowadays.

likely to have problems. What’s more, platforms with ICP certificates are less likely to be closed up than those without the certificate. Other researches have not mentioned this factor yet.

[image:5.595.64.536.193.506.2]Logit (5) shows the platform dealing with mortgage or car loans will help decrease the risk of the platform. Moreover, the platform providing SME loan is more likely to have problems. SME are those companies which have difficulties in borrowing money from banks or other formal channels. Therefore, they resort to P2P lending platform for help. Normally, they will borrow large amounts of money. If risk is not controlled well, problems are due to happen.

Table 3. Results of Binary Regression.

Variables Logit (1) Logit (2) Logit (3) Logit (4) Logit (5) probit

time 0.0773*** -0.0705*** 0.0703*** 0.0659*** 0.0739*** 0.0398***

exper_num -0.3338*** 0.3416*** 0.3270*** 0.4058*** 0.2269***

edu_num -0.2127 -0.1769 -0.1171 -0.0872 -0.0465

control 1.574975*** 1.4243*** -1.1214** -0.9990** -0.5997**

guarantee_1 0.6757*** 0.7102** 0.6440** 0.3688**

guarantee_2 -0.5457** 0.7237*** -0.6510** -0.3731**

guarantee_3 -0.151 -0.0624 0.02 0.002

capital -0.0155 -0.0155 -0.0086

backer 0.8851*** 1.0298*** 0.5832***

ICP 2.0583*** 2.0077*** 1.0371***

rate 8.4718** 4.6619*

type1 0.0885 0.02

type2 0.4990* 0.2970*

type3 0.9399*** 0.5318***

type4 -0.1176 -0.0634

pseudo R2 0.1172 0.1759 0.1956 0.2482 0.2754 0.2753

Note: ***, **, * represents significance respectively on the level of 1%, 5%, 10%

The last one is the Probit model. Its results are consistent with that of logit (5). However, R2 of this

model is slightly lower than that of logit (5), so we prefer the logit (5) for further analysis.

Conclusions and Suggestions

Conclusions

This paper verifies that if the existing time of a platform is longer, it’s less likely for it to have problems. Platforms with more financial-related executives or having bank custody are less likely to fall down. What’s more, platforms using their own money as guarantee are more probable to have problems. And platforms setting aside risk reserves can reduce its risk while surprisingly having a third party as guarantee is not significantly correlated with the failure of a platform. If the platform has backers and ICP certificate, it’s less probable to fail. ICP certificate, especially, has huge influence on the probability of having problems. Interest rate, consistent with previous researches, denotes the risk. Therefore, Platforms with higher yield rate must be riskier. Particularly, platforms offering house mortgage or car loan are more reliable and those offering SME loan tend to be riskier.

this model, such as the liquidity of capital, location, information disclosure and the comments or rating from users. This may account for why R2 of this model is small.

Suggestions

Based on our theoretic analysis and the empirical results from the regression, we can give some advices to investors, the P2P platforms and the government respectively.

For investors, “old” platforms are more reliable while fresh new ones are green hands in both management and risk control. Also, qualifications of those who manage the platform can reveal some information of whether the platform is good. People with financial working experience before may have a better understanding of how a financial intermediary works, thus providing better services to users. Bank custody is extremely important. Investors should feel more reassured if their money is put in the bank account. Normally, employing a third party is the best way to provide guarantee. If the platform has set aside a certain amount of money as risk reserve, it is also acceptable but using its own money as guarantee is not reliable. Platforms with different backgrounds also differ in their risks. Investors should pay attention to private companies without any backup. ICP certificate is also a solid proof that the platform has the ability to provide online lending service. Last but not least, investors should make decisions rationally when lending money to small and medium enterprises since these companies are riskier.

For the platforms, the most important thing is risk control. Platforms should select borrowers carefully through various ways. Setting a particular department for risk control is necessary. Also, self-regulatory organizations should be set up to promote cooperation and self-discipline among different companies. A credit information sharing system is in desperate need because it enables platforms nationwide to easily get access to the debtors’ information. Finally, platforms should always bear in mind that they are just intermediaries since any confusion about the rights and obligations will lead to illegal actions such as fund-raising, misappropriating money and asset management.

For the government, the most urgent and important concern is how to regulate the platforms properly. First, industry standards should be revised and released officially. Second, all lending platforms should be required to put their money in bank custody and to have the ICP certificates. Third, government should construct a series of alert signals for P2P platforms and pay more attention to those riskier platforms.

References

[1]Ye Qing, Li Zeng-quan, Xu Wei-hang, The Study on Risk Identification of P2P Internet Lending

Platforms[J]. Accounting Research, 016, 06:38-45+95.

[2]Ma, Hui-Zi, Wang, Xiang-Rong, Influencing factor analysis of credit risk in P2P lending based on

interpretative structural modeling[J]. Journal of Discrete Mathematical Sciences & Cryptography, Jun 2016, 19(3):777-786.

[3]Li Qi, Wang Zhen, The Study on the Platforms Risks and the Targets Risks of P2P[J]. Shanghai

Finance 2016, 10:92-95.

[4]Zhang Qiao-liang, Zhang Li, The Study of Risk Assessment Index of P2P Lending Platform[J],

Journal of Nanjing Audit University 2015, 06:85-94.

[5]Klafft, M. Online peer-to-peer lending: A lenders’per- spective. In H. R. Arabnia and A. Bahrami

(eds.). Proceedings of the 2008 International Conference.

[6]Greiner, M. E., Wang, H The Role of Social Capital in People-to-People Lending Marketplaces.

Proceedings of the International Conference on Information Systems 2009.

[7]Emekter Riza, Tu Yanbin, Jirasakuldech Benjamas, Lu Min, Evaluating credit risk and loan

[8]Ge Ru-yi, Feng Juan, Gu Bin, Zhang Peng-zhu, Predicting and Deterring Default with Social Media Information in Peer-to-Peer Lending[J]. Journal of Management Information Systems. 2017, 34(2):401-424.

[9]Xu Rong-zhen, Yin Yuan-xing, Wang Shuai, The Operational Formants and the Risk Control of

P2P Lending Platforms[J], Journal of Finance and Accounting. 2017, 05:33-38.

[10]He Guang-hui, Yang Xian-yue, Pu Jia-jie, The Risk and Its Decisive Factors of China’s P2P