City, University of London Institutional Repository

Citation

: Pesenti, S. M., Millossovich, P. ORCID: 0000-0001-8269-7507 and Tsanakas, A.

ORCID: 0000-0003-4552-5532 Cascade Sensitivity Measures. .

This is the preprint version of the paper.

This version of the publication may differ from the final published

version.

Permanent repository link:

http://openaccess.city.ac.uk/id/eprint/20808/Link to published version

:

Copyright and reuse:

City Research Online aims to make research

outputs of City, University of London available to a wider audience.

Copyright and Moral Rights remain with the author(s) and/or copyright

holders. URLs from City Research Online may be freely distributed and

linked to.

City Research Online: http://openaccess.city.ac.uk/ [email protected]

Cascade Sensitivity Measures

∗

Silvana M. Pesenti†1, Pietro Millossovich2,3, and Andreas Tsanakas2

1Department of Statistical Sciences, University of Toronto

2Cass Business School, City, University of London

3DEAMS, University of Trieste

23. July 2019

Abstract

In risk analysis, sensitivity measures quantify the extent to which the probability

distri-bution of a model output is affected by changes (stresses) in individual random input factors.

For input factors that are statistically dependent, we argue that a stress on one input should

also precipitate stresses in other input factors. We introduce a novel sensitivity measure,

termedcascade sensitivity, defined as a derivative of a risk measure applied on the output,

in the direction of an input factor. The derivative is taken after suitably transforming the

random vector of inputs, thus enabling the cascade sensitivity measure to capture both the

direct impact of the stressed input factor on the output, as well as indirect effects via other

input factors that are dependent on the one being stressed. Alternative representations of

the cascade sensitivity measure, which can be calculated from a single Monte Carlo sample,

are provided for two types of stress: a) a perturbation of the distribution of an input

fac-tor such that the stressed input follows a mixture distribution, and b) an additive random

shock applied to the input factor. The calculation of those representations does not require

simulating under different model specifications or the explicit study of the properties of

the model function, making the proposed method attractive for applications, as illustrated

through numerical examples.

∗

Earlier versions have been presented at the University of Trieste, at the University of Milano-Bicocca, at

the10thConference in Actuarial Science & Finance (Samos), at the4th European Actuarial Journal Conference

(Leuven), at theWorkshop on Recent Developments in Dependence Modelling with Applications in Finance and

Insurance (Aegina), at the KU Leuven & Cass Business School PhD colloquium (Leuven), at the University

of Liverpool, at the RiskLab, ETH Zurich, at the Vrije Universiteit Brussel and at the Ninth International

Conference on Sensitivity Analysis of Model Output (Barcelona). The authors are grateful for discussions with

and comments from Vali Asimit, Patrick Cheridito, Paul Embrechts, Mike Ludkovski, Ludger R¨uschendorf, Steven

Vanduffel, Ruodu Wang and Mario W¨uthrich.

†

Keywords Sensitivity analysis, importance measures, perturbation analysis, risk measures,

importance sampling, dependence, Rosenblatt transform.

1

Introduction

1.1 Overview and contribution

Sensitivity analysis is concerned with the attribution of the uncertainty of a model output to

the uncertainties of a model input (Saltelli et al.,2008). Principal tools in sensitivity analysis

are sensitivity measures (also called ‘importance measures’), which assign to each input factor

a score, ranking inputs according to their ability to influence (a probabilistic summary of) the

output, seeBorgonovo and Plischke (2016) for an extensive review. Variance-based sensitivity

measures, for example, distinguish input factors by their ability to affect the output’s variance

(Saltelli, 2002). In this paper, and as is typical in risk management applications, the output

distribution is summarized through a quantile-based measure of risk. Specifically, we consider

the class of distortion risk measures introduced by Wang (1996), which subsumes expected

utilities and the two most common risk measures in financial risk management, Value-at-Risk

(VaR) and Expected Shortfall (ES).

Sensitivity measures are often constructed via partial derivatives either of outputs with

re-spect to inputs (‘local’ sensitivity measures, see Borgonovo and Plischke (2016) and references

therein) or of the output risk measure in the direction of random inputs (Tsanakas and

Mil-lossovich, 2016;Antoniano-Villalobos et al.,2018). One drawback of such sensitivity measures

is that they do not fully account for interactions among or statistical dependence between input

factors. Extensions have so far focused on higher order derivatives (Mara and Tarantola,2012;

Borgonovo and Plischke, 2016). However, dependence structures between input factors might

substantially impact the sensitivity to an input factor, as is illustrated in the following example.

Example (Non-linear insurance portfolio). Consider an insurance company with losses from

three different lines of business,X1, X2andX3, each of which is subject to the same

multiplica-tive factorX4 arising from, e.g. inflation. The insurance company holds a reinsurance contract

on the loss from the first two lines of business, L=X4(X1+X2), with deductible dand limit

l. This means that the aggregate loss faced by the insurer is

Y =L−min{(L−d)+, l}+X3X4. (1)

In this simple model, which we will use as a running example throughout the paper, we view

(X1, X2, X3, X4) are dependent through a Gaussian copula with correlation matrixR:

R =

1 0.3 0 0.8

0.3 1 0 0

0 0 1 0

0.8 0 0 1

.

Each elementrij ofR closely approximates the Spearman rank correlation CorrS(Xi, Xj) of the

respective pair of input factors. Note that the aggregate portfolio lossY is symmetric inX1 and

X2but the dependence structure is not;X1 has a high rank correlation toX4, CorrS(X1, X4) =

0.8, while CorrS(X2, X4) = 0. Measuring the sensitivity to X1 and X2, via a local method

involving ∂X∂Y

1,

∂Y

∂X2, obviously fails to reflect the asymmetry in statistical dependence. More

generally, as is demonstrated in the continuation of this example in Section3, such asymmetry

is also not fully reflected by global sensitivity measures based on partial derivatives, in the vein

of Tsanakas and Millossovich(2016).

Example (London Insurance Market portfolio). Consider the situation of a model user or

re-viewer, who has only partial access to the model specifications. It is typical in risk management

applications, for models to be high dimensional with calculation of the model’s output

distri-bution proceeding by Monte Carlo simulation (Arbenz et al.,2012;Choe et al.,2018;Risk and

Ludkovski,2018). A model user will often be supplied with a set of simulated scenarios from

variables of interest (model inputs or outputs), without easy access to either (a) the

distribu-tional assumptions of inputs (which may themselves be outputs from sub-models) or (b) the

model function mapping inputs to outputs (which may be highly non-linear and

computation-ally expensive to evaluate). This situation is typical in the regulatory review of internal models

in insurance (Cadoni,2014).

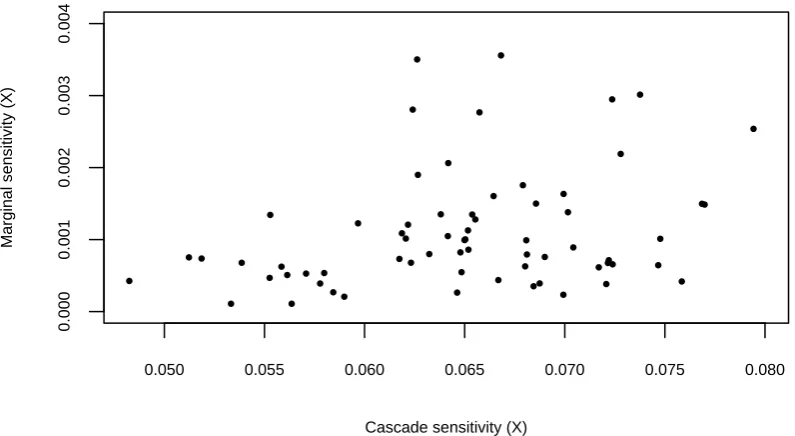

For illustration of those points, we consider a proprietary model of a London Insurance

Market portfolio, currently in use by a participant in that market. The model represents

a portfolio with 72 input factors; the output is the portfolio loss. We do not have access

to the marginal nor the joint distribution of the input vector; indeed, the input factors are

themselves outputs of different models. We were supplied by the model owner with a Monte

Carlo sample of size M = 500,000, consisting of simulated observations from the model’s

inputs and corresponding output. We have no access to the data generating mechanism, hence

we cannot re-simulate under different model assumptions.

In Figure 1we summarize the distributions of individual input risk factors, by plotting the

mean and the Expected Shortfall risk measure (at 90% level) of each. The question we aim to

0.5

1.0

1.5

2.0

2.5

Input risk factor

Mean and ES (p=0.9) of r

isk f

actors

● ●

● ● ● ● ● ● ●● ● ● ● ●

● ● ● ● ● ● ● ● ● ● ● ● ● ●

● ● ● ● ● ● ● ● ● ● ● ● ● ● ● ● ● ● ● ● ● ●● ● ● ● ● ● ● ●

● ● ● ● ● ● ● ● ● ●

● ● ●

●

41 9

45543522 5 4851282952473716

30363313325631716558691134596821635561462326622070 6 49 4 12 2 3 1 5060 7 3814

1939572527536440181567104344 8 42

246672 17

[image:5.595.92.475.127.318.2]● mean ES

Figure 1: Expected value and ES0.9 risk measure of input risk factors in the London Market

portfolio.

of perturbations in a particular risk factor, taking fully into account the dependence between

inputs? We return to this example in Section 5.

In this paper, we aim to address the issues raised by the preceding two examples. We propose

a novel sensitivity measure, termed cascade sensitivity, which explicitly accounts for the direct

and indirect dependence between input factors. Specifically, the cascade sensitivity is defined

as the partial derivative of a distortion risk measure applied to the output, in the direction of

a stressed input factor; hence it is closely related to the approaches of Hong (2009);Hong and

Liu(2009);Tsanakas and Millossovich(2016). However, in our case the derivative is taken after

a suitable transformation of the random vector of inputs, which enables cascade sensitivity

measures to fully capture the impact of dependence between input factors. Specifically, our

cascade sensitivity framework is underpinned by a variation of the inverse Rosenblatt transform

(Rosenblatt,1952), which permits a stress on one input factor to propagate through the entire

input vector, changing all its components according to the input vector’s dependence structure.

Thus, a stress on an input impacts on the output risk measure both directly and indirectly,

via the generated cascade of stresses on other (dependent) inputs. In particular, the cascade

contribution of an input factor to the sensitivity of the output.

A sensitivity measure that fully reflects the dependence of the random vector of inputs is

useful in applications where the dependence structure of the inputs is of particular interest, as in

risk management applications (Glasserman and Xu,2014;Lam,2017). The computational costs

of evaluating importance measures is a persistent theme in the sensitivity analysis literature

(Saltelli et al., 2008;Lam and Qian, 2018), given the need for costly evaluations of the (high

dimensional, non-linear) model function at different simulated scenarios. We provide explicit

analytical representations of the cascade sensitivity, which do not require calculation of the

gradient of the aggregation function and allow for a straightforward implementation on a single

Monte Carlo sample, thus avoiding multiple model runs. These alternative representations of

the cascade sensitivity are derived for two types of stress on an input factor: a) a perturbation

of the distribution of an input factor, such that the stressed input factor follows a mixture

distribution, and b) an additive random shock applied to the (tail of the) input factor itself.

Hence, our proposed cascade sensitivity framework is practically useful, as illustrated through

an application to a commercially used London Insurance Market portfolio model.

1.2 Relation to existing literature

The statistical functional whose sensitivity we are evaluating, i.e. a composition of a risk

measure with a multivariate (non-linear) aggregation function, also appears in the study of

systemic risk (Chen et al.,2013). While we do not actively purse this interpretation, systemic

risk quantification is within the scope of the methods developed in the present paper.

Derivatives of distortion risk measures, applied to a model output in the direction of an

input, have been extensively studied in sensitivity analysis and in capital allocation; notably by

Hong(2009);Cont et al. (2010) for the VaR risk measure,Hong and Liu(2009) for the ES risk

measure andTsanakas and Millossovich(2016) for general distortion risk measures. Sensitivity

to linear portfolios summarized by Haezendonck-Goovaerts and entropic risk measures are

con-sidered in Wang et al. (2018) and Tsanakas (2009), respectively. Cao and Wan(2017) analyse

derivatives of expected utilities in connection to optimal portfolio selection, while Gourieroux

et al. (2000, 2006) consider directional derivatives of distortion risk measures with respect to

parameter uncertainty for linear aggregation functions. See also Antoniano-Villalobos et al.

(2018) for a discussion on sensitivity measures to input parameters. However, in this stream of

literature, sensitivity measures generally do not account explicitly for the impact of the

depen-dence between input factors and thus do not lend themselves to investigations of dependepen-dence

Uncertainty in the dependence of an input vector is typically addressed by calculating the

worst-case of a risk measure applied on the output, such that the input vector belongs to an

uncertainty set. We refer toGlasserman and Xu(2014);Lam(2016,2017);Pesenti et al.(2019)

for uncertainty sets defined though probability distances and toEmbrechts et al.(2013);Wang

and Wang(2016);Li(2018) for worst-case spectral risk measures. While these papers deal with

dependence uncertainty, by assessing risk on (potentially unrealistic) worst-case models, they

not fully address the sensitivity to dependence of the baseline models in use.

The Rosenblatt transform has been used in various statistical contexts, e.g. see Dawid

(1984), but only recently has it been utilized to measure effects of dependence between input

factors for sensitivity purposes. Notable contributions are Mai et al. (2015), who study model

robustness through introducing uncertainty via a transformation of the input vector, andMara

and Tarantola (2012) in the context of variance based sensitivity measures. Kraus and Czado

(2017) carry out bank stress testing using graphical (D-vine) dependence models; their approach,

while methodologically different, is conceptually close to the ideas in this paper.

Further work related to ours is the stream of research on quantile sensitivity estimation in a

Monte Carlo simulation setting. Sensitivity to quantiles, as well as risk contributions, typically

involves estimation of conditional expectations, where the conditioning event has small or zero

probability of occurring. State-of-the-art estimators rely on variance reduction techniques such

as importance sampling, see Fu et al. (2009); Glasserman and Li (2005); Tasche (2009) and

Merino and Nyfeler (2004) for an application of importance sampling to risk contributions of

VaR and ES, respectively. Restricted importance sampling, a variation of importance sampling,

has recently been proposed by Liu (2015) to improve convergence rates of estimators of risk

contributions.

1.3 Structure of the paper

The paper is organized as follows. Section 2 introduces the notation and mathematical

frame-work. In section3the cascade sensitivity measure is defined as a partial derivative of a distortion

risk measure applied to the output, in the direction of a stressed input factor, via a variation

of the inverse Rosenblatt transform. The impact of input vectors’ dependence structure on

sensitivity is discussed and illustrated through numerical examples.

Section 4 is devoted to the calculation of the cascade sensitivity. We provide alternative

representations of the cascade sensitivity for two classes of stresses that allow for calculations

on a single Monte Carlo sample by importance sampling. The applicability of the cascade

We conclude in Section 5, with an application of cascade sensitivity to the commercially used

London Insurance Market portfolio discussed above, illustrating the challenges of sensitivity

testing ‘black box models’. All technical assumptions, proofs and detailed analytical calculations

for the examples are gathered in Appendix A.

2

Preliminaries

Throughout the paper we work with a probability space (Ω,A, P) and a random vector X = (X1, . . . , Xn) whose integrable components, X1, . . . , Xn, represent input factors. We denote

by Fj the marginal distribution function of the input Xj, j = 1, . . . , n, and by F the joint

distribution function of X. It is assumed that the joint density f of X exists and we denote by fj the marginal density of input factor Xj, j= 1, . . . , n. The vector of input factors, X, is

mapped by anaggregation function,g:Rn→R, assumed to be almost everywhere differentiable,

to the (univariate) outputY =g(X). We writeH, hfor the distribution function and the density of the outputY, respectively.

The left inverse of the distribution of any random variableW ∼FW is defined byFW−1(u) =

inf{x ∈R | FW(x) ≥u}, u∈(0,1]. We use the notation UW for a standard uniform random

variable comonotonic toW, that is, W =FW−1(UW) a.s. In the case when W has a continuous

distribution function, it holds thatUW =FW(W). Moreover, for an n-dimensional vector W,

we denote byW−j = (W1, . . . , Wj−1, Wj+1, . . . Wn) its sub-vector deprived of thejthcomponent.

The distribution of the output Y =g(X)∼H, representing a decision variable, is summa-rized through a risk measure. Risk measures are tools in financial risk management to assess

different levels of risk severity (Artzner et al.,1999; F¨ollmer and Schied,2011). Here we work

with the class ofdistortion risk measuresintroduced byWang(1996);Acerbi and Tasche(2002),

which are defined through

ργ(Y) = Z 1

0

H−1(u)γ(u)du=E H−1(UY)γ(UY)

,

where γ: [0,1]→ [0,∞) is a normalized weight function such that R1

0 γ(u)du = 1. The focus

on distortion risk measures is not restrictive, as the proposed framework is also applicable for

utility type performance measures, see the remark at the end of Section 3.1. Throughout this

paper, the examples will be based on the two most common distortion risk measures used in

practice, VaR and ES. The VaR of the random variable Y at level α ∈ (0,1) is defined as its

the left α-quantile, VaRα(Y) = H−1(α) or through the weight function γ(u) =δα(u), for the

Dirac measureδα. The ES, also called Conditional Value-at-Risk, at levelα∈[0,1) arises from

γ(u) = 1−α1 1{u>α}, thus has representation ESα(Y) = 1−α1 R1

αH

The objective of this paper lies in the study of the sensitivity of ργ(Y) to input factor

Xi, 1 ≤ i ≤ n. For simplicity, we fix i ∈ {1, . . . , n} for the rest of the paper, such that

sensitivity to the same input is considered throughout. We call a stress on input factor Xi a

family of random variables Xi,ε(ω) = K(Xi(ω), ω, ε), for ε≥ 0,ω ∈Ω and some mapping K,

that is almost everywhere differentiable in ε in a neighbourhood of 0, uniformly in x and ω.

Moreover, K satisfies K(x, ω,0) = x, for all x ∈ R and almost all ω ∈ Ω. In particular, for

any stressXi,ε, it holds that (X1, . . . , Xi,ε, . . . , Xn)|ε=0 =X a.s. We denote byFi,ε, ε≥0, the

distribution function of Xi,ε.

A typical choice of a stress is to apply a random shock Z to the input factorXi, such that

Xi,ε= Xi+εZ (Tsanakas and Millossovich, 2016). Alternatively, the distribution function of

the input factor,Fi, can be perturbed, an approach conceptually different from adding a shock.

Adding uncertainty via the distribution function of the input factor is a common technique

in sensitivity analysis and also used in Bayesian and robust statistics (Hampel et al., 2011;

Borgonovo and Plischke,2016;Glasserman,1991;Saltelli et al.,2008). Such aperturbation can

be constructed starting from a family of distribution functions Fi,ε,ε≥0, that is continuously

differentiable in ε, admits a density for all ε in a neighbourhood of 0, and fulfills Fi,0 = Fi.

We then define the stress to input factor Xi through a perturbation by Xi,ε =Fi,ε−1(Z), for a

standard uniform random variable Z. Depending on the choice of Z, the stress may not only

distort the input factorXi but might also change the dependence structure of the input vector

X. A natural choice, which we consider in the sequel, isZ to be comonotonic toXi, generating

perturbations of the form Xi,ε = Fi,ε−1(UXi), thus not altering the dependence between input

factors.

3

Sensitivity measures

3.1 Marginal sensitivity

To assess the sensitivity of the outputY to the inputXi, sensitivity measures are defined. The

approach we follow here is to take a directional derivative of the risk measure applied to the

output distribution, in the direction of a stress to input Xi.

Definition 3.1. For a stress Xi,ε and a distortion risk measure ργ, we define the marginal

sensitivity to input factor Xi by

Si(X, g, ργ) =

∂

∂εργ g(X1, . . . , Xi,ε, . . . , Xn)

ε=0,

The general form of the marginal sensitivity for distortion risk measures follows directly

from Hong and Liu (2009) and stated in the next proposition for completeness. It consists of

an expectation involving the derivative of the stress, the partial derivative of the aggregation

function in the direction of the stressed input factor and a weighting according to the chosen

risk measure.

Proposition 3.2. Given a stressXi,εand under AssumptionsA.1in the appendix, the marginal

sensitivity to input factorXi is

Si(X, g, ργ) =E ∂

∂εXi,ε

ε=0gi(X)γ(UY)

,

where gi(x) = ∂x∂ig(x) denotes the partial derivative of the aggregation function in the ith

component and ∂ε∂Xi,ε(ω) = ∂ε∂K(Xi(ω), ω, ε), for almost allω∈Ω.

Remark. Further work on derivatives of risk measures, and closely related to ours, is Hong

(2009);Tsanakas and Millossovich (2016). Our framework also includes sensitivity of expected

utilities, considered in Cao and Wan (2017); Antoniano-Villalobos et al. (2018). Note that,

for the trivial weight function γ ≡ 1, the distortion risk measure reduces to the expectation,

ρ1(·)≡E(·). Thus, for an utility functionu:R→R, we can write

E(u(g(X)) =ρ1 (u◦g)(X)

,

implying that expected utilities are a special case of our framework, with aggregation function

u◦g:Rn→Rand an expectation risk measure.

3.2 Inverse Rosenblatt transforms

The marginal sensitivity of Definition 3.1 does not fully account for interactions among or

dependence between input factors, since, by its definition, when stressing one input factor, all

other marginal input distributions remain unaltered; see also the discussion in Borgonovo and

Plischke (2016). Note that the representation of the marginal sensitivity in Proposition 3.2

incorporates the derivative of the aggregation function solely in the direction of the stressed

input factor.

In order to address the indirect effects induced by the dependence between the input factors,

we utilize a representation of random vectors, termedinverse Rosenblatt transform (Rosenblatt,

1952;R¨uschendorf and de Valk,1993).1

1

We call representation (2) theinverse Rosenblatttransform since, to be precise, the Rosenblatt transform is

Definition 3.3. An inverse Rosenblatt transform of ann-dimensional random vectorX, start-ing at Xi, is given by a differentiable function ψ = (ψ(1), . . . , ψ(n))>:Rn →Rn and a (n− 1)-dimensional random vector V = (V1, . . . , Vn−1), consisting of independent standard uniform

variables, independent of Xi, such that

X =ψ(Xi,V) = ψ(1)(Xi,V), . . . , ψ(n)(Xi,V)

a.s. (2)

The set of inverse Rosenblatt transforms ofX, starting atXi, is denoted byRi ={(ψ,V)|X =

ψ(Xi,V)}.

It can be shown that forψ(j), 1≤j≤n, to exist and be differentiable in the first component,

it is sufficient that the joint density f is almost everywhere differentiable.

An inverse Rosenblatt transform can be explicitly constructed via the following process

(R¨uschendorf and de Valk, 1993; Rubinstein and Melamed, 1998). For r = 1, . . . , n and J ⊆

{1, . . . , n}\{r}, denote by Fr|J(· | xj, j ∈J) the conditional distribution function ofXr given

Xj =xj, j ∈J. Then, it holds a.s. that

X1=F1−|i1(V1|Xi) =ψ(1)(Xi,V),

X2=F2−|i,11(V2|Xi, X1) =ψ (2)(X

i,V),

X3=F3−|i,11,2(V3|Xi, X1, X2) =ψ (3)(X

i,V),

.. .

Xi=ψ(i)(Xi,V),

.. .

Xn=Fn|−11,...,n−1(Vn−1|X1, . . . Xn−1) =ψ(n)(Xi,V),

where ψ(i) is the identity function in the first argument. Note that in the above construction,

each random variableXj depends onXi both directly and indirectly throughX1, . . . , Xj−1.

Deploying an inverse Rosenblatt transform of the vector X =ψ(Xi,V), (ψ,V) ∈ Ri, we

can stress input Xi throughXi,ε

Xi,ε=ψ(Xi,ε,V) = ψ(1)(X1,ε,V), . . . , ψ(n)(X1,ε,V)

. (3)

Observe that the stress Xi,ε is carried through the entire input vector, changing all factors

according to their dependence onXi,ε, resulting in a cascading effect.

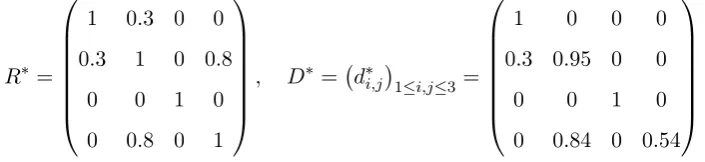

this example, thati= 1. For a vector of independent standard uniformsV = (Vj)j=1,...,n−1

inde-pendent ofX1, define the standard normal variablesZ1= Φ−1 F1(X1)

andTj = Φ−1(Vj), j=

1, . . . , n−1. Then, an inverse Rosenblatt transform starting fromX1, (ψ,V) ∈ R1, is derived

by setting

ψ(1)(X1,V) =X1

ψ(2)(X1,V) =F2−1 Φ (d21Z1+d22T1)

.. .

ψ(n)(X1,V) =Fn−1 Φ (dn1Z1+dn2T1+· · ·+dnnTn−1)

,

where Φ denotes the standard normal distribution function and D = (di,j)1≤i,j≤n is the lower

triangular matrix resulting from the Cholesky decomposition of R. Following this

represen-tation, one can stress X1 through substitution by X1,ε, which implies substituting Z1 by

Z1,ε = Φ−1 F1(X1,ε)

, in the right hand-side of the above equations. It is then apparent

how the stress on X1 also produces a stress on Xj, j = 2, . . . , n (provided dj1 6= 0).

3.3 Cascade sensitivity

The inverse Rosenblatt transform, by propagating stresses on one input factor across the vector

of inputs, allows us to construct a sensitivity measure that fully reflects both the direct and

indirect the impacts on the output.

Definition 3.4. For a stress Xi,ε, (ψ,V)∈ Ri and a distortion risk measure ργ, we define the

cascade sensitivity to input factorXi by

Ci(X, g, ργ) =

∂

∂εργ g ψ(Xi,ε,V)

ε=0,

whenever the derivative exists.

Hence, the cascade sensitivity framework directly extends approaches to sensitivity analysis

that are based on partial derivatives in the direction of input factors, to fully account for

dependence of input factors. In particular, the cascade and the marginal sensitivities only

differ in the way a stress on an input propagates across the whole vector of input factors, there

being no account for propagation in the marginal case. Though the current paper is focused on

distortion risk measures (and expected utilities), the use of the inverse Rosenblatt transform for

sensitivity analysis is a tool that could also be used in other (e.g. variance-based) sensitivity

The cascade sensitivity to an input factor can be decomposed into the marginal sensitivity

and additional components, each reflecting statistical, as well as functional, dependence between

inputs.

Proposition 3.5. Given a stress Xi,ε, (ψ,V) ∈ Ri, and under Assumptions A.1 in the

ap-pendix, the cascade sensitivity to input factorXi is

Ci(X, g, ργ) = n X

j=1

Ci,j, (4)

where

Ci,j =E ∂

∂εXi,ε

ε=0gj(X)ψ (j)

1 (Xi,V)γ(UY)

,

forj= 1, . . . , n.

The set of inverse Rosenblatt transforms of a random vector,Ri, is generally not a singleton,

implying that the inverse Rosenblatt transform is not unique. For instance, in the last example,

a different tranform would be obtained for some permutation of (X2, . . . , Xn). However, as the

next result shows, the cascade sensitivity does not depend on the particular choice of inverse

Rosenblatt transform, (ψ,V)∈ Ri.

Proposition 3.6. If the cascade sensitivity exists for one (ψ,V) ∈ Ri, then it exists and admits the same value for all other transforms (φ,U) ∈ Ri. Moreover, decomposition (4) is

unique.

The decomposition of the cascade sensitivity Ci in Proposition 3.5 allows to quantify the

contribution of each input factors’ indirect effects, stemming from the dependence with the

one being stressed, to Ci. Specifically, Ci,j is the indirect contribution of input Xj to the

sensitivity Ci, when stressing input factor Xi. Moreover, note that Ci,i = Si is the marginal

sensitivity; hence Ci − Ci,i is the component of the cascade sensitivity which is solely due to

the dependence structure between input factors. The components Ci,1, . . . ,Ci,n, contributing to

the cascade sensitivities, Ci, i = 1, . . . , n, can be visualized as shown below. Each row shows

a cascade sensitivity decomposed into its n-summands, Ci = Pnj=1Ci,j, i = 1, . . . , n. The

diagonal contains the marginal sensitivities, while off-diagonal elements Ci,j reflect the indirect

contribution of Xj to the cascade sensitivity of Xi.

Remark. The cascade sensitivity framework also includes sensitivity to uncertain statistical

parameters of input factors (Antoniano-Villalobos et al.,2018). Let Fi|Θi(·|θi) denote the

con-ditional distribution of Xi given parameter Θi=θi. Then it holds almost surely that

X1 X2 . . . Xn

C1 S1 C1,2 . . . C1,n

C2 C2,1 S2 . . . C2,n

..

. ... ... . .. ...

Cn Cn,1 Cn,2 . . . Sn

for a function η: R2 → R and a standard uniform random variable Ui independent of Θi.

Hence, instead of stressing the input factor Xi, we can perturb the variables Θi and Ui via

representation (5), in this way reflecting the sensitivity ofργ(Y) to the parameter and process

uncertainty ofXi, respectively.

Example (Non-linear insurance portfolio continued). We calculate the cascade sensitivity for

the insurance portfolio example introduced in Section1, assuming that the two lines of business,

X1, X2, are each modelled by a Log-Normal(µ= 4.98, σ2= 0.232) distribution with mean 150

and standard deviation 35. The third line of business,X3, follows a Gamma(100,1) distribution

with mean 100 and standard deviation 10, while the multiplicative factor,X4, is assumed to be

Log-Normal(µ4 =−0.005, σ24 = 0.12) distributed, that is with mean 1 and standard deviation

0.1. All the calculations are based on a simulated Monte Carlo sample of sizeM = 100,000.

We consider an additive shock to the first two lines of business defined byXi,ε=Xi+ε(Xi−

m), i= 1,2, wherem= 138.5 is the mode of either. Stressing relative to the mode is motivated

by Section4.2, as it results in an easily tractable calculation of the cascade sensitivity on a single

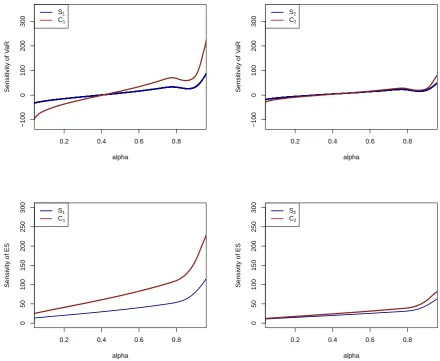

Monte Carlo sample. Figure2displays the marginal and cascade sensitivity to input factorsX1

and X2 for the risk measure VaRα (top) and for ESα (bottom), for 0.075< α <0.925. Note

that the marginal and the cascade sensitivity for the second line of business,X2, are fairly close

(compared to the sensitivities toX1), indicating that the indirect effects contributing toC2 are

minor (compared to those of C1).

The choice of distortion risk measure has a notable impact on the sensitivities, as seen by

comparing the top (VaR) and the bottom (ES) plots. This is particularly pronounced when

contrasting the marginal and the cascade sensitivity toX1. While the VaR is defined through the

Dirac weight function, hence only encompasses a single point, γ(·) =δα(·), the weight function

of the ES, γ(·) = 1−α1 1{·>α}, incorporates the entire right tail of the output’s distribution function. Thus, sensitivities utilising VaR can be seen as local measures of sensitivity, since

inputs are assessed in how they affect one quantile of the output’s distribution function. This

is in contrast to employing the ES, which leads to a ranking of inputs according to their ability

0.2 0.4 0.6 0.8

−100

0

100

200

300

alpha

Sensitivity of V

aR

S1

C1

0.2 0.4 0.6 0.8

−100

0

100

200

300

alpha

Sensitivity of V

aR

S2

C2

0.2 0.4 0.6 0.8

0

50

100

150

200

250

300

alpha

Sensivity of ES

S1

C1

0.2 0.4 0.6 0.8

0

50

100

150

200

250

300

alpha

Sensivity of ES

S2

[image:15.595.70.511.100.461.2]C2

Figure 2: Marginal and cascade sensitivity to input factorX1 (left) and input factorX2 (right),

for stresses Xi,ε=Xi+ε(Xi−m), where m is the mode ofXi, i= 1,2. The top displays the

sensitivities for the risk measure VaRα and the bottom graphs depict the risk measure ESα, for

0.075< α <0.925.

sensitivities to X1 and to X2, as functions of α, cross once, that is, S1 ≤ S2, C1 ≤ C2 for α

small and S1 ≥ S2, C1 ≥ C2 forα close to 1, whereas for ESα the sensitivities to X2 dominate

the corresponding sensitivities toX1, that is C2≥ C1 andS2 ≥ S1 for all 0≤α <1.

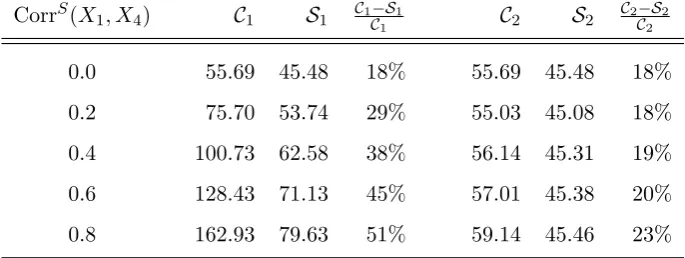

Table1reports the cascade sensitivities to inputs X1 andX2 for the risk measure ES0.9. In

this particular example, the terms reflecting the indirect effects of the dependence between the

input factors are scaled according to their Spearman rank correlation with the stressed input

factor, that is, Ci,j is proportional to CorrS(Xi, Xj) (for explicit calculations see A.3). Note

that CorrS(X2, X3) = CorrS(X2, X4) = 0, hence C2,3 =C2,4 = 0, and thus C2 =C2,1+S2 only

Table 1: The cascade sensitivities to inputs X1, X2 (along with standard errors) for ES0.9 and

its decomposition into the direct effect of the stressed input (Ci,i =Si) and the indirect effects

of the other input factors (Ci,j).

Ci,1 Ci,2 Ci,3 Ci,4

C1= 162.93 (0.017) 79.61 (0.009) 19.28 (0.002) 0 64.04 (0.006)

C2= 59.14 (0.009) 13.68 (0.002) 45.47 (0.007) 0 0

indirect impact of X4,C1,4, constitutes a substantial 39% = 16264..0493 to the cascade sensitivity to

X1.

To further illustrate the effects of the dependence structure of the input vector on cascade

sensitivities, we report the marginal and cascade sensitivities for ES0.9, with CorrS(X1, X4) =

0.0, . . . ,0.8 in Table 2. Table2 also states the percentage of the cascade sensitivity that stems

solely from the effects of the dependence between inputs, Cj−Sj

Cj , j = 1,2. As seen in Table

2, both the marginal and the cascade sensitivity to X1 increase with CorrS(X1, X4), with C1

impacted more heavily. The marginal sensitivity to input X2 is practically constant, implying

that changes in the dependence between X1 and X4 only have a very minor impact on S2,

which is in contrast to the cascade sensitivity to inputX2, which increases by 6.2% = (59.14−

[image:16.595.126.469.497.626.2]55.69)/55.69, thus reflecting such indirect effects.

Table 2: Marginal and cascade sensitivity for the ES0.9 with CorrS(X1, X4) = 0.0, ...,0.8.

CorrS(X1, X4) C1 S1 C1C−S1 1 C2 S2 C2C−S2 2

0.0 55.69 45.48 18% 55.69 45.48 18%

0.2 75.70 53.74 29% 55.03 45.08 18%

0.4 100.73 62.58 38% 56.14 45.31 19%

0.6 128.43 71.13 45% 57.01 45.38 20%

0.8 162.93 79.63 51% 59.14 45.46 23%

3.4 Comparison of the marginal and cascade sensitivities

Proposition 3.5 showed that the cascade sensitivity decomposes into the marginal sensitivity

and components reflecting the dependence between the input factors. Thus, a natural question

arises to whether, in general, positive (negative) dependence among inputs results into a larger

in that direction: first, for independent input factors the cascade sensitivity reduces to the

marginal sensitivity, irrespective of the aggregation function or the choice of distortion risk

measure. Second, the cascade sensitivity dominates the marginal sensitivity, given positive

dependence of the input vector, a non-decreasing aggregation function and a suitable stress.

For this, we review the notion of conditional increasingness in sequence (CIS). A random

vector W is said to be CIS if, for allj = 2, . . . , n,E(l(Wj) | W1 =w1, . . . , Wj−1 =wj−1) is a

non-decreasing function ofw1, . . . , wj−1, for all non-decreasing functionl:R→Rfor which the

expectation exists (M¨uller and Stoyan, 2002).

Proposition 3.7. Let (ψ,V)∈ Ri and under AssumptionsA.1 in the appendix, the following

hold:

1. If Xi is independent ofXj, for i6=j then Ci,j = 0. Hence, if Xi is independent of X−i,

thenCi(X, g, ργ) =Si(X, g, ργ).

2. If the vector (Xi, Xπ(1), . . . , Xπ(n)) is CIS for a permutation π on {1, . . . , n}\{i}, the

aggregation function is component-wise non-decreasing and ∂ε∂Xi,ε

ε=0 ≥ 0 a.s., then

Ci(X, g, ργ)≥ Si(X, g, ργ).

Examples of stresses with non-negative gradient include additive shocks,Xi,ε=Xi+εZ, for

Z ≥0 a.s. Other examples are perturbationsXi,ε=Fi,ε−1(UXi) withFi,ε= (1−ε)Fi+εFˆi, ε≥0,

such as those studied in Section 4.1, whenever the distribution ˆFi first order stochastically

dominatesFi.

Note that, by Proposition 3.6, it is enough in Proposition 3.7, case 2, that the vector

(Xi, Xπ(1), . . . , Xπ(n)) is CIS for one permutationπ. Examples of vectors that are CIS, which is

a dependence concept of the copula alone (M¨uller and Scarsini,2001, Prop. 3.5), include the

mul-tivariate normal distribution whose inverse covariance matrix contains non-positive off-diagonal

elements, as well as the multivariate logistic, gamma and negative binomial distributions (M¨uller

and Scarsini, 2001; Karlin and Rinott, 1980). We also refer to Karlin and Rinott (1980) for

further examples of multivariate totally positive of order 2 distributions, a slightly stronger

dependence concept than CIS.

4

Calculation of the cascade sensitivity

The calculation of the marginal and cascade sensitivities requires a choice on how to stress an

input factor. Here, as is typical in the sensitivity analysis literature (Borgonovo and Plischke,

input factor or a perturbation of its distribution function. In both cases, an additional source

of noise is applied in order to stress an input, i.e. Xi,ε=Xi+εZ, for stressing via an additive

shock and Xi,ε=Fi,ε−1(Z), for stressing via a perturbation.

The dependence between the noiseZ and the inputXi is an important aspect of the stress.

For example, stressing via independent noise, that is, with Z independent of X, is equivalent to adding a deterministic stress, see alsoTsanakas and Millossovich (2016). Specifically, when

stressing through an additive shock,Xi,ε=Xi+εZ, Zindependent ofX, the cascade (marginal)

sensitivity is equivalent to the cascade (marginal) sensitivity when applying a stress of the form

Xi,ε=Xi+εE(Z). Analogously, for a perturbation with Fi,ε= (1−ε)Fi+εFˆi and Fi,ε−1(U),U

independent of X, the cascade (marginal) sensitivity becomes equal to the cascade (marginal) sensitivity when adding the deterministic shock Xi,ε=Xi+εE

h

Fi(Xi)−Fˆi(Xi)

fi(Xi)

i

.

In the more interesting case of stresses with noise Z that is dependent on X, the question arises of what dependence structure to chose. Here we confine to choices of stress such thatXi,ε

is comonotonic to Xi. For such stresses we provide alternative representations of the cascade

sensitivity that are calculable on a single Monte Carlo sample and do not require evaluation of

derivatives of the functionsgandψ, thus making the proposed sensitivity framework attractive for applications.

Remark. Recall from Proposition 3.7 that, if Xi is independent of X−i, then Ci(X, g, ργ) =

Si(X, g, ργ). Hence, in the case of independence, the methods developed in this section allow for

an alternative evaluation of marginal sensitivities of the type studied by Hong(2009), without

knowledge of the gradient of the function g.

4.1 Stressing through a perturbation

One choice of a stress on an input factor via a perturbation is such that the stressed input

follows a mixture distribution, see Cont et al. (2010) for an application in a financial context.

For these types of stress, the cascade sensitivity can be calculated as follows.

Proposition 4.1. Let (ψ,V) ∈ Ri and define the perturbation Xi,ε = Fi,ε−1(UXi), where

Fi,ε= (1−ε)Fi+εFˆi, ε≥0, for a continuous distribution function ˆFi. Under AssumptionsA.1

in the appendix, the cascade sensitivity to input factor Xi is

Ci(X, g, ργ) =E

hFi(Xi)−Fˆi(Xi)

fi(Xi)

(g◦ψ)1(Xi,V)γ(UY) i

=EhH(Y)−Hˆ(Y)

h(Y) γ(H(Y))

i

,

We provide the representation of the cascade sensitivity for the two most common distortion

risk measures in practice, VaR and ES.

Corollary 4.2. Let (ψ,V) ∈ Ri and define the perturbation Xi,ε =Fi,ε−1(UXi), where Fi,ε =

(1−ε)Fi+εFˆi, ε≥0, for a continuous distribution function ˆFi. Denote by ˆH the distribution

function of ˆY =g(ψ( ˆXi,V)), with ˆXi= ˆFi−1(UXi). Then the following hold:

1. Under AssumptionsA.1i)−iv) forq =αin the appendix, the cascade sensitivity to input

factor Xi for VaRα, 0< α <1, is

Ci(X, g,VaRα) =

α−Hˆ(H−1(α))

h(H−1(α)) .

2. Under AssumptionsA.1i)−vi) forq =αin the appendix, the cascade sensitivity to input

factor Xi for ESα,0≤α <1, is

Ci(X, g,ESα) =

1 1−α

h

E Yˆ −H−1(α) +

−E Y −H−1(α) +

i

.

In the second representation of the cascade sensitivity in Proposition 4.1, the requirement

for knowledge of the gradient of the aggregation function has been replaced with the need to

evaluate ˆH, arising as a distorted distribution of the output, after substituting inputXi with

ˆ

Xi = ˆFi−1(UXi). This can in itself be seen as a different kind of sensitivity test, in particular

if ˆFi is more dispersed than Fi. For example, the formula for the sensitivity of ES in Corollary

4.2, case 2, involves the difference between two expectations over the right tail of the output,

measuring the impact on the output of substitutingXi with its distorted version ˆXi.

More broadly, rewriting the representation of the cascade sensitivity in Proposition 4.1, we

obtain

Ci(X, g, ργ) = Z

H(y)−Hˆ(y)γ H(y)dy, (6)

where the integral is over the support of Y. Thus, the cascade sensitivity can be seen as a

measure of the difference of the distribution functions of the outputY and the distorted output ˆ

Y = g(ψ( ˆXi,V)), weighted according to the choice of the risk measure ργ. Formula (6) also

implies that the cascade sensitivity is robust to small changes in the weight function γ of the

distortion risk measure. In particular, the cascade sensitivities for the risk measures VaRα and

ESα are continuous inα.

4.2 Stressing through an additive shock

In this section we give examples of additive shocks that are comonotonic to input Xi and lead

the aggregation function’s gradient. Specifically, we consider the family of shocks given by

Xi,ε=Xi+εk(Xi), for non-decreasing Lipschitz continuous functions k:R→Rwith Lipschitz

constant 1 and some further (non-restrictive) regularity assumptions on the inputXi as stated

in Lemma A.2. Examples of additive shocks as above include stressing the tails of an input

factor, by

Xi,ε=Xi+ε(Xi−t1)1{Xi≤t1}+ε(Xi−t2)1{Xi≥t2},

for t1 ≤ t2 ∈ R where fi(·) is monotone on (−∞, t1]∪[t2,∞). Alternatively, for a unimodal

input factorXi with modem, one may define, as in the example of Section 3.3,

Xi,ε=Xi+ε(Xi−m).

Scaling deviations from the mode preserves, to some extent, the shape of the distribution of

Xi. For example, if input factor Xi ∼ N(µ, σ2), then Xi,ε ∼ N(µ,(1 +ε)2σ2), while for

an exponentially distributed input factor, Xi ∼ Exp(λ), the stressed input follows Xi,ε ∼

Exp(1+λε).

Proposition 4.3. Let (ψ,V)∈ Riand define the stressXi,ε=Xi+εk(Xi), for a non-decreasing

Lipschitz continuous function k:R → R with Lipschitz constant 1, that satisfies k(x) ≤0 on

the set where fi(x) is non-decreasing and k(x) ≥ 0 on the set where fi(x) is non-increasing.

Under Assumptions A.1in the appendix, the cascade sensitivity to input factor Xi is

Ci(X, g, ργ) =E

hH(Y)−H˜(Y)

h(Y) γ(H(Y))

i

,

where ˜H denotes the distribution function of ˜Y =g(ψ( ˜Xi,V)), with ˜Xi = ˜Fi−1(UXi), where ˜Fi

is given by ˜Fi(x) =Fi(x)−k(x)fi(x), x∈R.

The cascade sensitivity for the risk measures VaR and ES, when stressing an input factor via

Xi,ε=Xi+εk(Xi) for a functionkfulfilling the assumptions in Proposition 4.3, are analogous

to Corollary4.2, replacing ˆH with ˜H.

The representation of the cascade sensitivities in Proposition 4.3 involves a weighted

dif-ference of the distribution functions ˜H and H, similar to equation (6). Thus, calculating the

sensitivity to a shock Xi,ε = Xi +εk(Xi), corresponds to comparing the output Y with the

distorted output ˜Y =g ψ( ˜Fi−1(UXi),V)

, where ˜Fi(x) = Fi(x)−k(x)fi(x), x∈R. Hence, a

stochastic comparison ofFiand ˜Fiis of interest. The next proposition shows that, provided that

E(k(Xi))≥0, ˜Fi−1(UXi) dominatesXi inincreasing convex order, so that the distorted output

˜

Y could be seen as more conservative than Y. Recall that a random variableW dominates Z

in increasing convex order,Z icxW, ifE(l(Z))≤E(l(W)), for all increasing convex functions

Proposition 4.4. Let Xi have finite expectation and define the random variable ˜Xi with

distribution function ˜Fi(x) = Fi(x) −k(x)fi(x), x ∈ R, as in Proposition 4.3. Then the

following hold:

1. IfE(k(Xi))≥0, then Xi icxX˜i.

2. If 0<ess supk(Xi), thenXi does not dominate ˜Xi in increasing convex order.

Consider an input factor that is symmetric around zero and the stress Xi,ε =Xi+ε(Xi−

t1)1{Xi≤t1} +ε(Xi −t2)1{Xi≥t2} for t1 < 0 < t2, such that the density of the input is

non-decreasing on{x≤t1}and non-increasing on{x≥t2}. Then, Proposition4.4case 1, is fulfilled

if t2 < |t1|. For a one-sided stress of an input factor, that is Xi,ε = Xi +ε(Xi−t)+, t > 0,

Proposition 4.4 case 1 is always satisfied. For an unimodal input factorXi with mode m and

stressXi,ε=Xi+ε(Xi−m), Proposition4.4, case 1 holds ifE(Xi)≥m, and case 2 is satisfied

form <ess supXi.

4.3 Numerical evaluation via importance sampling

In practical applications, when the marginal distributions and the copula of the input vector

are separately specified and estimated, the inverse Rosenblatt transform ofX may be available and ψ( ˆXi,U) and ψ( ˜Xi,U) in Propositions 4.1 and 4.3, respectively, can explicitly be

calcu-lated. For example the Rpackage copula (Hofert et al.,2017) provides the inverse conditional

distribution functions for Archimedean and elliptical copulas. The computation of the inverse

Rosenblatt transform (Probability Integral Transform) for canonical and D-vine copulas is

pre-sented in Algorithms 5 and 6 inAas et al.(2009) and implemented in theRpackageVineCopula

(Nagler et al.,2019;Schepsmeier,2015).

A computationally expensive aggregation function, however, might render a direct

calcula-tion of the cascade sensitivity unfeasible, as Proposicalcula-tions4.1 and 4.3 require the evaluation of

ˆ

Y =g ψ( ˆXi,V)

as in Section 4.1 and ˜Y = g ψ( ˜Xi,V)

as in Section 4.2, respectively. For

example, in a Monte Carlo simulation setting with sample sizeM, the calculation of the cascade

sensitivity to one input factor requires an inverse Rosenblatt transform and M evaluations of

ˆ

Y or ˜Y. Fortunately, using importance sampling, the distribution functions ˆH and ˜H can be

computed on the same Monte Carlo sample without the need to explicitly calculate an inverse

Rosenblatt transform. Indeed, it holds that, fort∈R,

ˆ

H(t) =E 1{g(ψ( ˆX

i,V))≤t}

=E1{Y≤t}

ˆ

fi(Xi)

fi(Xi)

, (7)

where ˆfi denotes the density of ˆFiand ˆ fi(Xi)

fi(Xi) play the role ofimportance weights. Note that, due

formula holds for ˜H. Thus, starting with a Monte Carlo sample of the input vectorX and the knowledge of the density ˆfi or ˜fi, the calculation of the cascade sensitivity is straightforward

without the need to calculate an inverse Rosenblatt transform of X. Specifically, the cascade sensitivity for the VaR and the ES in Propositions 4.1 (4.3), can be estimated through the

following procedure:

1. Sample M multivariate scenarios x1 = (x11, . . . , x1n), . . . ,xM = (xM1 , . . . , xMn ) from input vectorX and calculate the corresponding realisations of the outputy1=g(x1), . . . , yM =

g(xM).

2. Estimate the distribution function and density of the outputY, for example, through the

empirical distribution function and a kernel density estimator

Hemp(t) = 1

M

M X

j=1

1{yj≤t}, t∈R,

ˆ

Hemp(t) = 1

M

M X

j=1

1{yj≤t}

ˆ

fi(xji)

fi(xji)

, t∈R,

hkern(t) = 1

M

M X

j=1

κ(t−yj), t∈R,

for a suitable kernel κ.

3. Denote by vα=Hemp,−1(α), and estimate the cascade sensitivity for the VaR and ES by

Ciemp(VaRα) =

1

hkern(v α)

α−Hˆemp(vα)

,

Ciemp(ESα) =

1

M(1−α)

M X

k=1

ˆ

fi(xki)

fi(xki)

−1

!

yk−vα

+.

Estimators of the cascade sensitivity for a distortion risk measure different from VaR and ES

can be obtained by utilizing the weight functionγ and Propositions4.1 and4.3.

Example (non-linear insurance portfolio continued). To calculate the cascade sensitivity, the

importance sampling routine of this section can be employed, where the distorted densities

˜

fi, i= 1,2, are given by

˜

fi(x) =

x−m x

1 +ln(x)−µ

σ2

fi(x), x >0. (8)

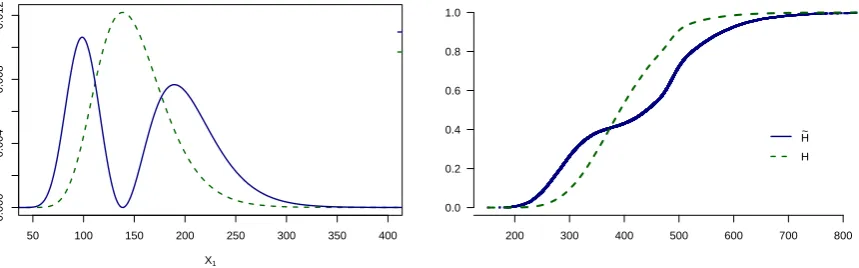

The left plot in Figure 3 shows the importance weights f˜1(X1)

f1(X1) against the input factor X1.

Note that the importance weights are zero at the mode of X1 and give more weight to high