COMMISSION OF THE EUROPEAN COMMUNITIES

PRACTICAL GUIDE

TO THE USE OF THE

EUROPEAN COMMUNITIES' SCHEME

OF GENERALIZED TARIFF PREFERENCES

COMMISSION OF THE EUROPEAN COMMUNITIES

Practical Guide

to the Use of the

European Communities' Scheme

of Generalized Tariff Preferences

This publication is also available in the following languages:

FR ISBN 92-825-3525-8

ES ISBN 92-825-3526-6

Cataloguing data can be found at the end of this publication

Luxembourg: Office for Official Publications of the European Communities, 1983

ISBN 92-825-3524-X

Catalogue number: CB-37-83-085-EN-C

Reproduction in whole or in part of the contents of this publication is authorized, provided the source is acknowledged

The Practical Guide to the Use of the European Communities' Scheme of Generalized Tariff Preferences

published on 1 March 1983 is available in English, French and Spanish.

The various versions are updated each year and the Guide is improved and supplemented in the light of

experience in order to cater more fully for the interests of the different users.

The Practical Guide to the Use of the European Communities' Scheme of Generalized Tariff Preferences is

available from the sales offices for official publications of the European Communities indicated on the back

cover of this volume.

For any other details or further information, apply to

Commission of the European Communities,

Directorate-General for External Relations — Service I C 3

Rue de la Loi 200 - 1049 Brussels

Telephone 235 11 11

CONTENTS

Foreword

Page

7

Explanatory notes for the rules of origin applicable to the Community's generalized system of

preferences 12

The Community's generalized tariff preferences scheme for 1983 47

Beneficiaries of the Community's generalized tariff preferences scheme for 1983 353

Terminology 357

Symbols and abbreviations 359

FOREWORD

The generalized system of preferences (GSP) should be seen against

the background of an international effort, beginning with the

launching of the First United Nations Development Decade in

1961, to encourage greater cooperation among the industrialized

countries to promote the development of the poorest countries. The

GSP idea was formally put forward by the Community and the

States associated with it (the AASM) at a GATT ministerial

meet-ing in 1963. What it did, in fact, was to call into question, for the

benefit of the developing countries, the rules of international trade

enshrined in the General Agreement. Painstaking work needed to

be done on this subject at the first two UNCTAD sessions (1964

and 1968) and by the Special Committee on Preferences from 1969

onwards before finally culminating in October 1970 in the latter's

'concerted conclusions', which constitute the charter, as it were, of

autonomous, non-discriminatory generalized tariff preferences. In

June 1971 the GATT accorded a 10-year waiver on

most-favoured-nation treatment, thus giving the go-ahead for the system, which

has the effect of exempting from customs charges the industrialized

countries' imports of products originating in the developing

coun-tries, without reciprocity on the part of the latter. On 1 July 1971

the Community introduced, for a six-month period, its first GSP

scheme, which was subsequently renewed each calendar year. It was

intended for member countries of the Group of 77 (the '

self-elec-tion ' process) and for Member States' or third countries' dependent

territories. Applications from other developing countries to join the

Community's scheme were to be examined on their merits;

Romania and China were included in the list of beneficiaries in

1974 and 1980 respectively.

In March 1975, just over two years after its enlargement to nine

Member States, the Community was already announcing, via a

Council resolution, that it intended to extend its scheme beyond the

initial decade. The Legal Framework Group decided in the

multi-lateral trade negotiations that the generalized preferences system

could be extended without this being made contingent on a further

waiver.

In December 1980, the Council decided to extend the application of

the generalized preferences system for a further period of 10 years,

a period which brings it into line with the development strategy

framed by the United Nations for 1981-90.

The new system applied by the Community, now enlarged by the

accession of Greece, remains autonomous, and this will enable it to

continue to be as open as possible and ensure that it can still be

applied flexibly. As before, it contains differentiated arrangements

for agricultural, textile and industrial products; product coverage,

the conditions governing eligibility, the principle of duty-free

ad-mission and the system of ceilings for industrial products (including

ECSC and textile products) have also been maintained for the first

five-year period of application, at the end of which some of these

aspects may be modified. In practice the main feature of the new

scheme is the extension to all industrial products of the system of

individually allocated and differentiated preferential entitlement,

which was introduced in 1980 but applied only to textile products

covered by the Multifibre Arrangement.

1. Agricultural products

Imports under the preferential arrangements are admitted without

any restrictions as to volume. However, a safeguard clause

mod-elled on Article XIX of the GATT enables duties to be

reintro-duced in part or in full if goods are imported under the preferential

arrangements in such quantities or at such prices as to cause or

threaten serious injury to Community producers of like or directly

competitive products. This clause is selective, i.e. it may be applied

solely in respect of the country or countries causing the injury,

which gives the safeguard mechanism some flexibility and prevents

the other beneficiary countries from being harmed. It has never

been invoked.

The number of products ' in respect of which tariff preference is

enjoyed by all beneficiary countries has risen from 145 in 1971 to

340 in 1983 (8 new products have been brought within the 1983

scheme: horseradish 07.01 G III, frozen or dried okra, 07.02 ex B,

07.04 ex B, sweet peppers, 07.02 ex B, dates, 08.01 ex A, bilberries,

08.08 ex C, dried rose-hips fruit, 08.12 ex G, seasnails, 16.05 ex B).

Over the years, some products have been included in the scheme

because of specific undertakings given by the Community to

devel-oping countries, such as implementation of the Joint Declaration of

Intent on the Asian Commonwealth countries, which was adopted

in the final stage of the negotiations with the United Kingdom and

annexed to the Treaty of Accession. Thus products where

preferen-tial imports were administered in the form of tariff quotas or

ceil-ings were added to the agricultural scheme: cocoa butter, soluble

coffee, preserved pineapple other than in slices and flue-cured

Vir-ginia tobacco in 1974, other types of preserved pineapple and other

raw or manufactured tobaccos in 1977 (the last category is the only

case where there is a tariff ceiling on agricultural products).

Since 1979 the least-developed countries have enjoyed duty-free

entry for all the products covered by the scheme, subject however,

to preferential volumes for raw or unmanufactured Virginia type

tobaccos (for which there is a quota) and for other raw or

unman-ufactured tobaccos (for which there is a ceiling).

1

By 'products' is meant the different tariff entries distinguished in the GSP Regulation.

Dried cut flowers (06.03 ex B), for instance, bearing a GSP duty of 7%, and other cui

flowers (06.03 ex B), bearing a GSP duty of 16%, are considered as two different products.

Some CCT subheadings are grouped together under a single GSP entry where the

prefer-ential duty is the same. The five agricultural quotas and the agricultural ceiling count as six

products (though in fact they correspond to ten CCT tariff entries).

Also since 1980 a number of products (a total of 14 in 1982) have

been included in the scheme solely for their benefit. The list of

these products has been considerably extended for 1983, as a result

of which the least-developed countries will enjoy virtually the same

advantages as the ACP in respect of all agricultural products which

are not subject to levies or other such charges. This doubles the

number of products in the offer made to the least-developed

coun-tries; the detailed list is given on p. 277. '

2. Industrial products

In accordance with Resolution 21 (II) of the second UNCTAD

Conference, primary industrial products are not covered by the

Community scheme. The fact that the Community has excluded

these products has only a very limited impact since almost all

industrial raw materials already enter the Community duty-free.

For finished and semi-finished industrial products the Community

system has from the outset been based on three features: ceilings,

duty-free entry and the principle that no products are excepted.

Since the new system was put into effect in 1981, two additional

features have been introduced — individualization and

differentia-tion of concessions — to take account of changing patterns of trade.

Over the past few years a number of the beneficiary countries have

speeded up their development and are now capable of exporting

their products and marketing them in the Community on normal

competitive terms. The granting of the tariff preference under the

old GSP system's global ceilings led to an imbalance as these

coun-tries made greater use of the preferential arrangements. The

butoir 2

mechanism was not an adequate correcting factor, as the

less-com-petitive countries were left only limited scope for taking advantage

of the ceilings

2

and quotas

2

that had already been considerably

eaten into by the most dynamic beneficiaries. In order to prevent

this, under the new scheme the global quotas and ceilings and the

butoirs

have been done away with and the principle of individual

preferential amounts has been adopted (in the same way as for

MFA textile products), according to the beneficiaries' relative

com-petitiveness.

1

As a result of internal difficulties the Community offer on dried grapes is suspended for

Products are classified in two categories, to which different

admin-istrative rules apply, but in every case each beneficiary is

guaran-teed an individual preferential amount. Firstly, in the case of

sen-sitive products, which are listed in Annex A to the Regulation

open-ing preferences where a beneficiary country is particularly

compe-titive for a given product, GSP imports from that country are

admin-istered by quota, while the individual amounts opened for the

other countries are administered by ceiling. If no beneficiary is

out-standingly competitive GSP imports from all beneficiary countries

are administered under a system of individual ceilings. As a result

each beneficiary knows that it can avail itself of the preferential

facilities offered by the Community and will not be affected by the

performance of other countries; these arrangements have also

widen-ed to the greatest possible extent the advantages reservwiden-ed for the

less-competitive countries, which are the ones that most need

facil-ities to promote their exports. In the case of quotas the duty is

reintroduced at national level when the share, plus any drawings on

the reserve, is totally used up. In the case of ceilings the duty is

reintroduced by the Commission for the whole of the Community

vis-à-vis

the beneficiary country in question. In order to optimize

the collection ofinformation on duty-free imports detailed practical

arrangements determine how often and within what period the data

supplied by the customs departments of the Member States have to

be transmitted to the Commission.

Secondly, there are non-sensitive products, which are listed in

Annex B to the Regulation opening preferences. In the case of these

products duties may likewise be reintroduced by the Commission,

at the request of a Member State, but only after an information

procedure designed to make the mechanism more flexible. For

these products the reference basis to be taken into account for

rein-troducing the normal duty is worked out product by product and is

generally 138% of the maximum country amount

(butoir)

for 1980;

the reference basis is not published in the Regulation, since this

would complicate the presentation and be of little practical use.

For three products—ex 29.03 (musc-xylene), ex 29.44 (antibiotics

excluding chloramphenicol and tetracyclines) and ex 39.06 (certain

high polymers)—the reference basis is at a lower level (see pp. 108,

121 and 140 respectively) specified in Annex B to Regulation (EEC)

No 3377/82.

The least-developed countries enjoy duty-free entry on all

indus-trial products without any quantitative limitation.

3. Textile products

Textile products falling within Chapters 50 to 63 of the CCT are

subject to the same general arrangements as other industrial

pro-ducts (duty-free entry, non-exclusion, ceilings). However, in the

case of two categories — products covered by the Arrangement

regarding International Trade in Textiles (MFA), and jute and coir

products — special conditions apply because of the particular

sensi-tivity of the sector and the arrangements governing international

trade.

The textile scheme was radically overhauled in 1980 with regard to

MFA products, in respect of which preferences are reserved for the

developing country bénéficiaires of the general scheme which have

concluded bilateral agreements with the Community on trade in

textile products (or entered into undertakings similar to those

pro-vided for in the agreements).

Depending on its level of development, measured in terms of GNP,

and of competitiveness, measured in terms of textile exports, each

beneficiary was reserved an individual amount of duty-free imports

for each category based in 1980 on its exports to the Community in

1977 (the categories are those used for the bilateral agreements).

At the same time, a flat-rate offer on each category was made to the

beneficiary countries for which a specific individual ceiling could

not be calculated because their exports were zero or negligible in

1977. This minimum offer corresponds to a percentage of the

Com-munity's total extra-EEC imports, varying according to the

sensitiv-ity of the groups of textile categories defined under the bilateral

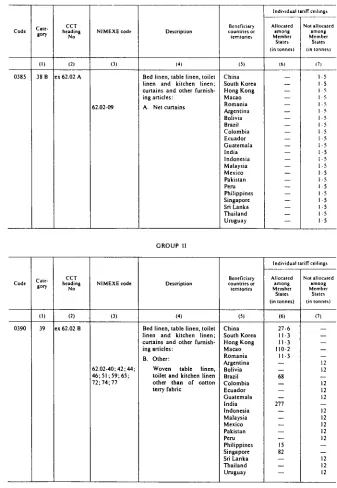

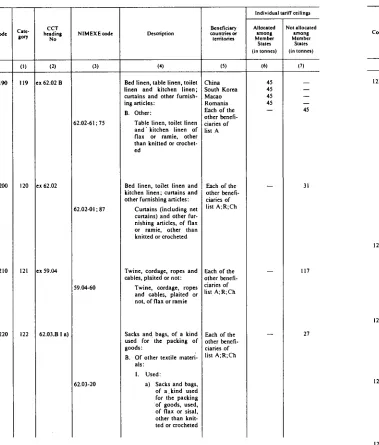

agreements: for Group I, 0.01 %; for Group II, 0.06%; for Groups

II, IV and V, 0.15%.

Sensitive products were placed under ceilings allocated among the

Member States (without reserve shares) and the other products

under non-allocated ceilings. Non-MFA products remained subject

to global preferential ceilings (plus a

butoir)

open to all beneficiaries

In 1981, all the preferential amounts were increased by 2% in order

to take account of the impact of Greece's accession to the

Commu-nity, and for 1982 the scheme was maintained as it stood.

For 1983 various amendments have been made to the textile

scheme in accordance with the line followed in the negotiations for

the renewal of the bilateral agreements under the MFA. Thus the

number of groups of categories is now three; categories 10 and 11,

which have become less sensitive, have moved to Group III, while

categories 32 (ex 32 and 32 a in GSP) and 39, which previously

came under Group III, and 68, 73, 76, 78, 81 and 83, which were in

Group IV, have been added to Group II; also, categories 13, 21, 26

and 73 have been made subject to the same rules as Group I.

Last-ly, categories 19 and 89 (handkerchiefs) have been merged;

catego-ries 10 and 11, however, and categocatego-ries 24 and 25 remain separate

although they are lumped together under the MFA.

For five ('dominant' or State-trading) countries, the textile offer

has been maintained at the same level as in 1982, but rounded off

to the nearest decimal point, except with regard to the ceilings

cor-responding to the minimum offer for the Group III categories

which have been reassessed in the same way for all countries.

The other beneficiaries' specific individual ceilings have been

maintained with the 1982 amounts for Group I categories and the

four which are treated in the same way; they have been increased

by 2.5% and 5% respectively for the Group II and Group III

cate-gories. The minimum offer has been reassessed on the basis of 1980

figures, subject to the necessary corrective factors being applied to

take account of the varying degree of sensitivity of the different

categories.

Generally speaking, the way in which the specific ceilings are

administered has not changed since 1982. In the case of the

mini-mum offer, however, the ceilings are not allocated among the

Mem-ber States except for the five countries referred to above (China,

Hong Kong, Macao, Romania and South Korea) in respect of

Groups I and II and the Group III categories regarded as sensitive

in 1982 (Annex A to Regulation (EEC) No 3602/81). Some

excep-tions have had to be made to this principle in the case of supplier

countries which, although they exported negligible amounts in 1977

(and therefore received a minimum offer) have been exporting

con-siderable amounts in recent years; to compensate for this, the level

of the offer has been raised to that of the specific ceiling

immediate-ly above (except in one case, where the ceiling would otherwise

have been increased nineteen-fold).

For non-MFA products, the system of global ceilings and

butoirs

has been abolished; the individual ceilings are based on the

butoirs

in force in 1982, i.e., 50% or 30% of the theoretical global ceilings

fixed at 55% of the Community's imports in 1980, plus 2% in

order to take account of Greece, whose trade has been included in

Community statistics only since 1981.

As in the industrial scheme, the ceilings are allocated among the

Member States for preferential imports from competitive

coun-tries.

For all textile products the least-developed countries enjoy

prefer-ences without any restriction except those which might result from

implementation of bilateral agreements (negotiated voluntary

res-traint amounts).

Jute and coir products are not subject to ceilings, but the granting of

preferences is conditional on special measures (voluntary restraint

agreements or similar undertakings) to be negotiated with the

ex-porting developing countries. Currently the least-developed

coun-tries are eligible for preferences on all such products, and India, Sri

Lanka and Thailand for preferences on some of them.

4. The beneficiaries

(a) There are 126 countries on the general list of beneficiaries.

Six-ty-three of those countries already enjoy preferential trade

ar-rangements under the Lomé Convention, and a further nine do

so by virtue of bilateral agreements with the Community. Of the

22 dependent countries and territories, 15 are subject to the

same trade arrangements as the ACP States themselves.

94.01 Β II and 94.03 Β). For Romania three new industrial pro

ducts have been brought in (64.03, 71.16 and 85.15 AHI); the

first of these is nonsensitive while the other two are sensitive.

Since 1978 Romania has no longer been excluded from benefit

on any product on the scheme for agricultural products.

(c) From 1983 onwards Bolivia and Ecuador have become benefi

ciaries for the

whole

of the textile scheme : these two countries

have now given undertakings similar to those provided in the

bilateral agreements on trade in textile products concluded with

the Community under the Multifibre Arrangement.

On 1 January 1983, 21 countries or territories had met the con

ditions required for the granting of preference on products cov

ered by the MFA: Bolivia, Brazil, China, Colombia, Ecuador,

Guatemala, Hong Kong, India, Indonesia, Macao, Malaysia,

Mexico, Pakistan, Peru, Philippines, Romania, Singapore, South

Korea, Sri Lanka, Thailand and Uruguay.

(d) For GSP purposes the Community recognizes a list of 38 least

developed countries—including for 1983 two new countries,

Togo and Sierra Leone. Of these 27 are ACP countries which

already enjoy preferential treatment under the Lomé Conven

tion, so that the special rules introduced by the Community in

1977 apply essentially to Afghanistan, Bangladesh, Bhutan, Hai

ti, Laos, Maldives, Nepal, North Yemen and South Yemen.

As noted above, the leastdeveloped countries enjoy full dutyfree

entry for all agricultural products covered by the scheme, subject to

the quota and ceiling arrangements for tobacco. Furthermore the

list of agricultural products included for their benefit alone has been

greatly enlarged in 1983.

EXPLANATORY NOTES FOR THE RULES OF ORIGIN APPLICABLE

TO THE COMMUNITY'S GENERALIZED SYSTEM OF PREFERENCES

Introduction

This set of notes sets out to explain how the concept of 'originat

ing products' works and how it is controlled by the authorities.

In

order to benefit from the Community's Generalized System of

Preferences the goods concerned have to be shown

to

originate in

one of the countries to which the scheme applies.

Part 1 — The general concept of an originating product and the

rule on direct transport

1.1. The general concept of an originating, product

A product is an originating one if it has been entirely produced

(wholly obtained) in the country concerned, for example flowers

plucked from a plant growing in that country are originating flow

ers.

In addition to this simple rule,

if sufficient work is carried out

on an imported product originating status can be obtained for the

end product.

1.2. The concept of a wholly obtained or entirely produced product

This concept has

been

defined

as

follows:

(a) mineral products extracted from the soil or from the seabed of

a country;

(b) vegetable products harvested in a country;

(c) live animals born and raised in a country;

(d) products obtained in a country from live animals;

(e) products obtained by hunting or fishing conducted in a coun

try;

(0 products of sea fishing and other products taken from the sea

by the vessels of a country';

(g) products made on board the factory ships of a country from the

products in (0 above;

(h) used articles collected in a country which are only capable of

being used for the recovery of the raw materials they contain;

(i) waste and scrap resulting from manufacturing operations car

ried out in a country; and

(j) any product produced in a country using only products which

fall into categories (a) to (i) above.

1.3. The concept of sufficient working or processing

The concept of sufficient working or processing is defined as that

amount of working or processing that places the final product in

a different tariff heading under the Customs Cooperation Council

Nomenclature (CCCN) than that of any of the imported ingredients.

But there are exceptions to this general rule which are contained

in Lists A and Β annexed to Commission Regulation (EEC)

No 3606/82 (see further on pages 23 to 40). List A says that, for the

final products listed there, in addition to the change of tariff head

ing condition the supplementary conditions listed also have to be

met. List Β on the contrary says that, for the final products it con

tains, the change of tariff heading criterion does not have to be

satisfied if certain other conditions have been satisfied instead.

1.3.1. The rules in Lists A and Β can be either specific rules requir

ing that a particular kind of processing is carried out or that specific

raw materials have to be used, or percentage rules requiring that a

specific proportion of the value of the final product be attributable

to the country concerned.

EXAMPLES

1. Change of tariff heading case (no rule in List A or B)

Scrap of unhardened rubber of heading No 40.04 imported from a

third country is processed in a GSP-country into reclaimed rubber

of heading No 40.03; the change of

tariff

heading confers on the

reclaimed rubber the status of a product originating in the GSP

country.

2. List A specific rule case

Products obtained

Heading No

61.01

Description

Men's and boys' outer

garments

Working or processing that does not confer the status of originating

products

Working or processing that confers the status of originating products when the following conditions are met

Manufacture from

yam

Outer garments of heading No 61.01 obtained in a country which is

a beneficiary under the GSP can be considered as originating in that

country only if they are manufactured from, say, third country yarn;

if such clothing were manufactured from third country fabrics, it

would not be considered as an originating product.

3. List A percentage rule case

Products obtained

Heading No

71.15

Description

Articles consisting of,

or incorporating,

pearls, precious or

semi-precious stones

(natural, synthetic or

reconstructed)

Working or processing that does not confer the status of originating

products

Working or processing that confers the status of originating products when the following conditions are met

Manufacture in which

the value of the pro

ducts used does not

exceed 5096 of the va

lue of the value of the

product obtained

Articles consisting of, or incorporating, pearls, precious or semi

precious stones, etc. of heading No 71.15 obtained by working in

a country which is a beneficiary under the GSP can be considered

as originating in that country only if the value of the third country

products used does not exceed 50% of the value of the finished pro

duct.

4. List Β percentage rule case

Products obtained

Heading No

ex

Chapters

28 to 37

Description

Products of the chemical and allied

industries excluding sulphuric an

hydride (ex 28.13), tannins (ex

32.01), some products falling with

in heading No 33.01, preparations

for tenderizing meat, clarifying

beer and preparations for the

desiz-ing of textiles (ex 35.07)

Working or processing that confers the status of

originating products

Working or processing in which

the value of the non-originating

products used does not exceed

20% of the value of the product

obtained

Natural boric acid containing more than 85% of orthoboric acid,

calculated on the dry weight, of heading No 28.12 is imported

from a third country and used in a GSP country to obtain

ortho-boric acid of heading No 28.12; the orthoortho-boric acid obtained is an

originating product on condition that the value of the third coun

try natural boric acid does not exceed 20% of its value.

The use of percentage rules of value implies that the basis for de

termining the value has to be defined. Paragraph 1.5. below ex

plains this.

EXAMPLE

1. List A rule

Products obtained

Heading No

38.15

Description

Prepared rubber accel

erators

Working or processing that does not confer the status of originating

products

Working or processing thai confers the status of originating products

when the following conditions are met

Manufacture in which

the value of the pro

ducts used does not

exceed 50% of the va

lue of the product ob

tained

2. List Β rule

Products obtained

Heading No

ex

Chapter 38

Description

Miscellaneous chemical products,

other than refined tall oil (ex 38.05)

and wood pitch (wood tar pitch) (ex

38.09)

Working or processing that confers the status of

originating products

Working or processing in which

the value of the non-originating

materials used does not exceed

2096 of the value of the product

obtained

Heading 38.15 'prepared rubber accelerators' has a 50% rule in

List A and a 20% rule in List B. This means that, if all the raw

materials are imported, only 20% of the value of the final product

can be composed of imported products which were classified under

heading 38.15 at import and that not more than 50% of the value

of the final product can be made up of the imported products in

total.

1.3.3. In Annex I to these notes there is a 'logical tree' designed

to help you decide if your product is an originating product or not.

1.4.

Minimal processing

However the rules on sufficient working or processing explained

above do have the proviso or condition that, even if the work

car-ried out satisfies the change of tariff heading rule and/or the List

A or Β conditions as appropriate, if the work carried out consists

only of a minimal process origin is

not

conferred.

The following are what are considered as minimal processes:

(a) operations to ensure the preservation of products in good con

dition during transport and storage (ventilation, spreading out,

drying, chilling, placing in salt, sulphur dioxide or other aque

ous solutions, removal of damaged parts, and like operations);

(b) simple operations consisting of removal of dust, sifting or

screening, sorting, classifying, matching (including the

making-up of sets of articles), washing, painting, cutting making-up;

(c) (i) changes of packing and breaking up and assembly of con

signments,

(ii) simple placing in bottles, flasks, bags, cases, boxes, fixing

on cards or boards, etc., and all other simple packing oper

ations;

(d) the affixing of marks, labels or other like distinguishing signs

on products or their packaging;

(e) simple mixing of products, whether or not of different kinds,

where one or more components of the mixture do not meet the

conditions laid down to enable them to be considered as origi

nating products;

(0 simple assembly of parts of products to constitute a complete

product;

(g) a combination of two or more operations specified in (a) to (f);

(h) slaughter of animals.

1.5.

Values to be used in the case of percentage rules

The values to be used in the calculation of percentage rules are

as follows:

For imported goods

Their customs value at the time of importation as defined in the

convention concerning the Valuation of Goods for Customs signed

in Brussels on 15 December 1950.

For final products

The ex-works price of the goods, which is understood as the price

paid or notionally payable to the manufacturer in whose plant the

last working or processing took place, provided the price includes

the value of all the inputs. However the amount of local internal

taxes paid (example — sales tax) which can be reclaimed at export

shall be subtracted.

1.6.

'Direct shipment' or 'Direct transport'

In addition to being an originating product a product has to be

shipped direct from the country of production to the Community.

However, goods may go through another country if the crossing of,

or entry into, that country is necessary for geographical reasons or

because of transport requirements and then only under the following

conditions:

(a) that the goods do not undergo any operations other than

tran-shipment or temporary warehousing. However, this does not

ex-clude any process only intended to keep the goods in good

con-dition;

(b) that the goods do not 'enter into the commerce of the transit

country'—that is, for exemple,that the goods are not bought or

sold there;

(c) that the goods do not enter into home use—that is the goods

are not cleared through customs; and

(d) that the goods remain under customs surveillance there.

If goods are passed through another country for geographical or

transport reasons the fulfillment of the above four conditions must

be demonstrated to the customs authorities in the Community.

This can be done by submission of either:

(a) a through bill of lading drawn up in the exporting beneficiary

country covering the passage through the country of transit; or

(b) a certification by the customs authorities of the country of

transit:

— giving an exact description of the products,

— stating the dates of unloading and reloading of the products

or of their embarkation or disembarkation, identifying the

ships used,

— certifying the conditions under which the products remained

in the transit country; or failing these

(c) any substantiating documents that are acceptable to the customs

authorities in the Community.

Furthermore, products which pass through the territory of certain

EFTA countries which are preference donors (Austria, Finland,

Norway, Sweden and Switzerland) may be re-exported in full or in

part to the Community provided that the conditions relating to

direct transport have been observed in these countries. In such

cases, the EFTA countries concerned will issue replacement

certifi-cates of origin Form A for importations into the Community. ' This

procedure applies on a reciprocal basis, for the Community to the

EFTA countries, mentioned above.

However, slightly different rules apply to goods sent to exhibitions

in other countries. These are explained in Article 10 of Commission

Regulation (EEC) No 3606/82.^

Part 2 - What has to be done at export

2.1.

What documents are needed?

After the origin of an export consignment has been established to

the satisfaction of the exporter he has to consider how much it is

worth and how it is to be sent in order to decide what

documen-tation, if any, is to be used.

2.1.1. No documentation necessary

No documentation is necessary if:

(a) the goods are sent as small packages from private persons to private

persons and the value is not more than 105 ECU.

2

(b) the goods form part of the personal luggage of a traveller and

the value is not more than 325 ECU.

2

However this concession is restricted to those imports which are

occasional and are made up only of products for the personal use

of the person to whom they are sent or the traveller or their

fam-ilies. It must be obvious from the nature and quantity of the goods

that no commercial purpose is served. The customs authorities in

the Community may require a declaration that the goods have

orig-inating status and the necessary conditions outlined above have been

complied with.

2.1.2. Forms APR

If the consignment is by post, including parcel post, its value does

not exceed 1 600 ECU

2

the exporter may choose to use a Form

1

See Nos 7 and 8 of the explanatory notes to Regulation (EEC) No 3606/82 (OJ L 377,

31.12.1982).

2

The equivalent of the ECU in the national currencies of the Member States of the

APR (see p. 41) which he fills in himself or allows his authorized

representatives to complete. The form may be completed in English

or French : if it is done by hand, ink and block capitals must be

used.

One APR form must be completed for each consignment.

In the case of consignment by parcel post the exporter attaches the

form to the despatch note. In the case of consignment by letter post

he encloses the form in the package.

2.1.3. Origin certificates Form A

For all shipments other than those mentioned in 2.1.1 and 2.1.2

above a Form A (see p. 45) must be filled out. The Form A origin

certificate contains twelve numbered boxes to be filled in by the

exporter and one un-numbered box which must contain the name

of the issuing country. Boxes 1, 3, 4, 5, 6, 7, 9 and 10 call for no

particular observation.

Box 2 does not have to be filled out if the consignee is not known.

It is filled in but the consignee is later changed this does not mat

ter.

Box 12 contains the exporter's declaration as to the origin of the

goods and must clearly indicate that the goods are for the European

Economic Community or one of its Member States or in cases

where the transit procedure referred to in point 1.6 is used, one of

the EFTA countries concerned, The use of the word 'Europe' is not

enough. Box 8 ('Origin criteria') has to be filled out according to

the code explained in Note 3 on the back of the form.

Box 11 ('Certification') is for the approved issuing authority to

certify the form as correct, using the stamp designed for that pur

pose.

When the form is filled out and signed by the exporter or his

authorized representative it must be taken to the governmental

authority authorized to issue Form A in the country concerned. If it

is incorrectly made out the customs authorities of the importing

country may refuse to accept it.

Certificates issued retrospectively

In exceptional cases an origin certificate Form A can be issued af

ter the export of the goods where it can be shown that a request

was not made at the proper time because of an error, involuntary

omission or some other special circumstance. In such cases the Form

A may be issued only if the issuing authorities are satisfied that the

certificate of origin Form A corresponds to the goods sent on the ba

sis of comparison with the export documentation, and that no cer

tificate of origin Form A had already been issued.

A certificate so issued is marked 'ISSUED RETROSPECTIVELY'

in box 4.

Duplicates

It is of course always possible that a certificate of origin Form Λ

that has been issued is lost, stolen or destroyed. In these cases the

exporter may ask the issuing authority for a replacement or du

plicate. This is marked in box 4 'Duplicate' and is given the

same

date of issue as the original and is valid for the same period (see

PART 3 paragraph 3.1).

2.2.

Goods sent in instalments

Goods classified under Chapters 84 and 85 of the Customs Co

operation Council Nomenclature, that is 'Machinery and mechan

ical appliances; electrical equipment and parts thereof' which are

imported by instalments may be considered as making up one whole

only subject to the conditions made by the customs authorities of

the country of importation and a certificate of origin Form A made

out for the total may be submitted at the time of the first import

to cover subsequent instalments as well.

2.3.

Accessories, spare parts and tools sent with a piece of equip

ment, machine, apparatus or vehicle

These, if they are part of the normal equipment and are not

separately invoiced or paid for, are regarded as part of the equip

ment etc. Naturally the rules of origin contained in PART 1 of

these notes apply equally to the accessories, spare parts and tools

but they are regarded as being classified under the same heading

as the equipment etc., and their value must be included in any

percentage value calculation carried out for the purposes of applica

tion of a percentage rule.

2.4.

Sets

considered to have originating status if all the articles making up

the set have that status.

A set made up of both originating and non-originating articles may

be considered to have originating status provided the value of the

non-originating articles does not exceed 15% of the total value of

the set.

2.5.

Packing

Packing, which is of the normal type for the article packed, and itself

has no intrinsic utilization value of a durable nature except as

pack-ing is considered to be a part of the article packed. Again its value

must be taken into account in calculation carried out in application

of a percentage rule.

Part 3 — What has to be done at import into the Community

3.1.

Period of validity of certificates of origin Form A

The certificate of origin Form A shall be valid for 10 months from

the date of issue by the competent authority in the country of

export.

3.2.

Expiry of period of validity

If the Certificate is submitted after the period of validity has

expired, the customs authorities in the Community may accept the

certificate afterwards provided they are satisfied that the delay was

unavoidable or due to exceptional circumstances.

3.3.

Submission of certificates of origin Form A to customs

As a general rule, the certificate of origin should accompany the

goods to which they refer. However certificates may be submitted

afterwards within a period of four months from the date on which

the entry form for the release of goods into free circulation was

accepted by customs. The customs authorities reserve the right to

request the importer to produce a translation of the certificate into

one of the Community languages and they may also require the

importer to make and sign a declaration that the goods satisfy the

conditions concerning origin and direct transport.

3.4.

Slight differences between the descriptions of the goods and the

goods themselves

The customs may ignore any small differences between the

descrip-tion on the Form A and the actual goods provided that they can be

sure the certificate does in fact correspond to the goods.

3.5.

Treatment of Forms APR

When a postal package arrives it will be seen by the customs

autho-rities, who will check the contents and the Form APR.

Part 4 — When verification takes place

The Community customs authorities may request verification of

cer-tificates of origin Form A or Forms APR by the issuing authorities

in the country concerned.

Part 5 — Regional Cumulation

5.1.

Who is concerned

There are three special schemes, which are identical, for three

re-gional groupings:

(a) ASEAN (Association of South East Asian Nations),

compris-ing:

Indonesia Singapore

Malaysia Thailand

The Philippines

(b) CACM (The Central American Common Market), comprising:

Costa Rica Honduras

El Salvador Nicaragua

Guatemala

(c) The Andean Group, comprising:

Bolivia Peru

Colombia Venezuela

Ecuador

5.2.

What is cumulation?

Under the Communities' GSP scheme each developing country

nor-mally is considered in isolation and goods cannot be further worked

in another country without losing the status of originating products

nor can they go through another country unless geographical or

transport requirements render this necessary (see Part 1 paragraph

5.3.

How cumulation works

(a) If goods originating in one country in a regional grouping are

not further processed after they have gone to a second country

in the regional grouping, from which they are sent to the Com

munity, then originating status is not lost.

(b) If further working or processing of goods originating in one coun

try of a regional grouping takes place in a second country of the

same regional grouping using only products originating in the re

gional grouping, then originating status is preserved.

(c) However, if further working or processing of goods originating in

one country of a regional grouping takes place in a second coun

try of the regional grouping, using products

not originating

in the

regional grouping; then there are two different possibilities de

pending on whether

(i) the final product is covered by a List A or Β percentage rule

or

(ii) the final product is covered by the change of tariff heading

rule or a List A or Β rule not involving percentages.

5.4.

Application of percentage rules

In the case of the application of a percentage rule (see paragraph

5.3. (c) (i) above), those goods incorporated that originate in anoth

er country in the regional grouping are regarded as neutral, that is

they are regarded as neither originating goods nor nonoriginating

goods and they are left out of the calculation. For example, where

the percentage rule to be applied is one which allows up to 40% of

nonoriginating goods to be incorporated, if the imported products

originating in another country in the same regional grouping have a

value of USD 50 and the value of the final product is USD 100,

then nonoriginating parts incorporated in the country in the re

gional grouping where final processing takes place cannot exceed

USD 20, that is 40% of the value added in this last country of

processing (which is USD 50), if the final product is to have origi

nating status.

EXAMPLE

List A limits the value of any nonoriginating products incorpo

rated in products of Chapter 84 to 40% of the value of the finished

product. By way of illustration, an incomplete machine has ac

Products obtained

Heading No

ex

Chapter 84

Description

Boilers, machinery and

mechanical appliances

and parts thereof, ex

cluding

refrigerators

and

refrigerating

equipment

(electric

and

other)

(heading

No 84.15) and sewing

machines,

including

furniture specially de

signed for sewing ma

chines (heading No ex

84.41)

Working or processing thai does not confer the status of originating

producís

Working or processing thai confers lhe status of originating products when the following conditions are met

Working,

processing

or assembly in which

the value of lhe pro

ducts used does noi

exceed 40% of lhe va

lue of the produci ob

tained

quired the status of originating product of one country of the group

ing in question through the use in manufacture of third country

products to the value of USD 300, the cost of the processing and

the use of originating parts amounting to USD 700 and the ma

chine being therefore worth USD 1 000. This machine is sent to

another country of the grouping where it has added to it USD 200

worth of third country nonoriginating parts covered by a tariff

heading other than that covering the machine; as the cost of pro

cessing etc., amounts to USD 300 the value of the machine after

this operation is USD 1 500; it retains its originating status since

the value of the third country parts incorporated in it (USD 200)

does not exceed 40% of the amount of the total value added in the

second country in the regional grouping (USD 500).

5.5.

Application of non-percentage rules

In the case of the application of a nonpercentage rule (see para

graph 5.3. (c) (ii) above), the goods retain originating status prov

ided that in addition to the use of any products originating in the

regional grouping the third country nonoriginating goods incorpo

rated do not exceed 5% of the total value of the final product

and

EXAMPLE

Products obtained Heading No

55.09

2Description

Other woven fabrics of

cotton

Working or processing that does not confer the status of originaling

products

Working or processing that confers lhe status of originating products when the following conditions are met

Manufacture from

pro-ducts falling within

heading No 55.01,

55.03 or 55.04

Cotton cloth of heading No 55.09 is manufactured in the first

coun-try of the regional grouping from imported carded cotton of heading

No 55.04. This product, which has originating status by virtue of the

rule in List A, is exported to a second country in the regional

group-ing where imported dye is used to dye the cotton cloth. The value

of the dye being less than 596 of the value of the final product, the

product retains its originating status upon export to the Community

because:

(1) the value of the dye is less than

5%

of the total value; and

(2) if the dye had been used in the first country of the regional

grouping the product would not have lost originating status

there.

5.6.

Determination of the actual country of origin in the regional

group-ing

A product which obtains originating status by reason of the

appli-cation of the cumulation rules as regarded as originating in the

coun-try which has contributed the highest percentage of the final value.

5.7.

Special reference on certificates of origin Form A

'LOGICAL TREE' TO ESTABLISH WHETHER A PRODUCT HAS ORIGINATING STATUS

1Is your product 'entirely produced'?

YES —

originating product

NO — Q2

Q5

Is your product listed in List B?

YES — Question 6

NO — non-originating product

Q2

2Do the imported parts have a different 4 figure

CCCN classification from that of the final product?

YES — Question 3

NO — Question 5

Q6

Does your product satisfy the additional criteria set

out in List B?

YES —

originating product

NO — non-originating product

Q3

Is your product listed in List A?

YES — Question 4

NO —

originating product

N.B.

At the head of the last column in List Β is a general

596

wai

ver for products of Chapters 84-92.

Q4

Does your product satisfy the additional criteria set

out in List A?

YES —

originating product

NO — non-originating product

This 'logical tree' does not take into account the possibilities available under the cumu

lation system (see PART 5).

Notes to Lists A and Β

1. The lists contain some products which do not benefit from tariff preferences but which may be used

in the manufacture of products which do benefit.

2. The description of the products in column 2 in the lists corresponds to that of the same heading

number in the Customs Cooperation Council nomenclature.

L I S T A

List of working or processing operations which result in a change in the nomenclature heading without conferring the status of originating products on the products undergoing such operations, or conferring

this status only subject to certain conditions

Prod u a s obtained Tariff

heading Nu

Description

Working or processing thai docs not confer the status of originating

products

Working or processing that confers the status of the originating products when the following conditions are met

1 1.05 15.02

M e a t a n d edible meat offals (except poultry liver), salted, in brine, dried or s m o k e d

Fish, dried, salted or in brine, s m o k e d fish, w h e t h e r or n o t cooked before or d u r i n g the s m o k i n g process Vegetables [whether or not cooked), preserved by freezing

Vegetables provisionally preserved in brine, in sulphur w a t e r or in other preservative solutions, but not spe cially prepared for immediate con s u m p t i o n

Dried, d e h y d r a t e d or e v a p o r a t e d vegetables, whole, cut, sliced, broken or in p o w d e r , but not further pre p a r e d

Fruit (whether or not cooked) pre served by freezing, not c o n t a i n i n g added sugar

Fruit provisionally preserved (for e x a m p l e , by sulphur dioxide gas, in brine, in sulphur water or other preservative solutions), but unsuit able in that state for immediate c o n s u m p t i o n

Fruit, dried other than t h a t falling within h e a d i n g N o 0 8 . 0 1 , 0 8 . 0 2 , 0 8 . 0 3 , 0 8 . 0 4 or 0 8 . 0 5

Flour of the dried leguminous veg etables falling within h e a d i n g N o 0 7 . 0 5 or of the fruiti falling within any h e a d i n g in C h a p t e r 8 Flour, meal and flakes of p o t a t o Fats of bovine cattle, sheep or goats, un rendered; rendered or solvent extracted fats (including ' p r e m i e r ¡us') obtained from those u n r e n d e r c d fats

Fais and oils, of fish and m a r i n e m a m m a l s , w h e t h e r or not refined

Salting, placing in brine, drying or s m o k i n g of meat a n d edible m e a t and edible meat offals of h e a d i n g N o s 0 2 . 0 1 a n d 0 2 . 0 4

Drying, salting, placing in b r i n e ; s m o k i n g of fish, w h e t h e r c o o k e d or not

Freezing of vegetables

Placing in brine or in other solutions of vegetables falling within h e a d i n g N o 0 7 . 0 1

Drying, d e h y d r a t i o n , e v a p o r a t i o n , cutting, b r e a k i n g , p o w d e r i n g of vegetables falling within h e a d i n g N o s 0 7 . 0 1 to 0 7 . 0 3 inclusive

Freezing of fruit

Placing in brine or in other solutions of fruit falling within h e a d i n g N o s 0 8 . 0 1 to 0 8 . 0 9 inclusive

Drying of fruit

M a n u f a c t u r e from dried leguminous vegetables falling within h e a d i n g N o 07.OS or from fruits falling within C h a p t e r 8

M a n u f a c t u r e from p o t a t o e s M a n u f a c t u r e from p r o d u c t s of heading N o s 0 2 . 0 1 a n d 0 2 . 0 6

M a n n f . u t u r e from p r o d u c t s falling within C h a p t e r s 2 and 3

List A (cont'd)

Products obtained Tariff

heading No

15.06

ex 15.07

16.02

16.04

16.05

ex 17.01

17.02

ex 17.03 17.04

18.04

18.06

ex 19.02

ex 19.02

19.03

Description

Other animal oils and fats (including neat'sfoot oil and fats from bones or waste)

Fixed vegetable oils, fluid or so!id. crude, refined or purified, but not including Chinawood o i l , myrtle wax. Japan wax or oil of tungiuits, oleococca seeds or oiticica seeds; also not including oils of a kind used in machinery or mechanical appliances or for industrial purposes other than the manufacture of foodstuffs for human consumption

Other prepared or preserved meat or meat offal

Prepared or preserved fish, including caviar and caviar substitutes Crustaceans and molluscs, prepared or preserved

Beet sugar and cane sugar, solid, flavoured or coloured

Other sugar in solid f o r m ; sugar syrups, not containing added flavouring or colouring matter; arti ficial honey, whether or not mixed with natural honey; caramel Molasses, flavoured or coloured Sugar confectionery, not containing cocoa

Cocoa butter (fat or oil)

Chocolate and other food prepara tions containing cocoa

Malt extract

Preparations of flour, meal, starch or malt extract, of a kind used as infant food or for dietetic or culinary pur poses, containing less than 50"Λ. by weight of cocoa

Macaroni, spaghetti and similar products

Working or processing that does not confer the status of originating

products

Manufacture from products falling within Chapter 2

Manufacture from products falling within Chapters 7 and 12

Manufacture from products falling within Chapter 2

Manufacture from products falling within Chapter 3

Manufacture from products falling within Chapter 3

Manufacture from any product

Manufacture from any product

Manufacture from any product Manufacture from other products falling w i t h i n Chapter 17

Manufacture from sucrose or manu facture in which the value of the products falling within heading Nos 18.01 to 18.05 inclusive used ex ceeds 40 % of the value of the pro duct obtained

Manufacture from products of heading N o 11.07

Manufacture from cereals and de rived products, meat, milk and sugars

Working or processing that confers the status of the originating products when the following conditions are met

Manufacture beans

Manufacture

rom originating cocoa

List A (cont'd) Products obtained Tariff heading No 19.04 19.05 19.07 19.08 20.01 20.02 20.03 20.04 20.05 20.06 20.07 21.04 21.05 ex 21.07 Description

Tapioca and sago; tapioca and sago substitutes obtained from potato or other starches

Prepared foods obtained by the swel-ling or roasting of cereals or cereal products (puffed rice, corn flakes and similar products)

Bread, ships' biscuits and other ordi-nary bakers' wares, not containing added sugar, honey, eggs, fats, cheese or fruits; communion wafers, empty cachets of a kind suitable for pharmaceutical use, sealing wafers, rice paper and similar products

Pastry, biscuits, cakes and other fine bakers' wares whether or not con-taining cocoa in any proportion

Vegetables and fruit, prepared or preserved by vinegar or acetic acid, with or without sugar, whether or not containing salt, spices or mus-tard

Vegetables prepared or preserved otherwise than by vinegar or acetic acid

Fruits, preserved by freezing, con-taining added sugar

Fruit, fruit-peel and parts of plants, preserved by sugar (drained, glacé or crystallized)

Jams, fruit jellies, marmalades, fruit puree and fruit pastes, being cooked preparations, whether or not con-taining added sugar

Fruit otherwise prepared or pre-served, whether or not containing added sugar or spirit

Fruit juices (including grape must) and vegetable juices, whether or not containing added sugar, but unfer-mentcd and not containing spirit

Sauces; mixed condiments and mixed seasonings

Soups and broths, in liquid, solid or powder form; homogenized compo-site food preparations

Sugar syrups, flavoured or coloured

Working or processing that does not confer the status of originating

products

Manufacture from any product

Manufacture from any product

Manufacture from products falling within Chapter 11

Manufacture from products falling within Chapter 1 1

Manufacture from products falling within heading No 20.02

Manufacture from any product

Working or processing that confers the status of the originating products when the following conditions are met

Manufacture from originating prod-ucts falling within Chapters "* and 8

Manufacture from originating prod-ucts falling within Chapter 7

Manufacture from originating prod-ucts falling within Chapters 8 and 17

Manufacture from originating prod-ucts falling within Chapters 8 and 17

Manufacture from originating prod-ucts falling within Chapters 8 and 17

Manufacture from originating prod-ucts falling within Chapters 8, 9, 17 and 22

Manufacture from originating prod-ucts falling within Chapters 7, 8 and 17

Manufacture from tomato concen-trate the value of which does not exceed 5 0 % of the value of the produci obtained

List A (cont'd)

Tariff heading

Produas obtained

Description

Working or processing that does not confer the status of originating

products

Working or processing that confers the status of the originating products when the following conditions are met

Lemonade, flavoured spa waters and flavoured aerated waters, and other non-alcoholic beverages, not includ-ing fruit and vegetable juices fallinclud-ing within heading No 20.07

Vermouths, and'other wines of fresh grapes flavoured with aromatic extracts

Spirits (other than those falling within heading No 22.08); liqueurs and other spirituous beverages; compound alcoholic pi epa ration s (known as 'concentrated extracts') for the manufacture of beverages

Vinegar substitutes for vinegar

Sweetened forage; other prepara-tions of a kind used in animal

feed-Cigarettes,

tobacco to

cigars and cigarillos.

moking

Aluminium sulphate

Medicaments (including veterinary medicaments)

Wadding, gauze, bandages and simi-lar articles (for example, dressings, adhesive plasters, poultices) impreg-nated or coated with pharmaceuti-cal substances for medipharmaceuti-cal or surgipharmaceuti-cal purposes)

Other fertilizers; goods of the pre-sent Chapter in tablets, lozenges and similar prepared forms or in pack-ings of a gross weight not exceeding 10 kg

Colour lakes

Other colouring matter; inorganic products of a kind used as luminophores

Artists', students' and signboard painters' colours, modifying tints, amusement colours and the like, in tablets, tubes, jars, bottles, pans or in similar forms of packings, includ-ing such colours in sets or outfits, with or without brushes, palettes or other accessories

Manufacture troni fri

Manufacture from products of heading No 08.04, 20.07, 22.04 or 22.05

Manufacture from products tailing within heading No 08.04, 20.07, 22.04 or 22.05

Manufacture from products of heading N o 08.04, 20.07, 22.04 or 22.05

Manufacture from cereals and de-rived products, meat, milk, sugar and molasses

Manufacture from products falling within heading No 28.20

Manufacture from active substance

Manufacture from products falling within heading Nos 32.04 and 32.05

M i x i n g of oxides or salts falling within Chapter 28 with extenders such as barium sulphate, chalk, barium carbonate and satin white

Manufacture from products falling within heading Nos 32.04 to 32.09 inclusive

Manufacture in which at least 7 0 % by quantity of the products falling within heading No 24.01 used are originating products

Manufacture from originating phar-maceutical substances