Featuring Insights on ...

Q4 2012

Underwritten in part by

Electronic Invoice Management

Going with the (Work)flow

Barriers to eInvoice Adoption

Making a Case for Automation

Usage of AP Automation

Challenges in Current AP Operations

Factors Driving AP Automation Interest

AP Outsourcing Providers & Case Studies

Executive Summary ...1

Move to the Middle ...2

And Now, the Numbers . . . ...4

Making a Case for Automation ...6

Overcoming Barriers to Adoption ...12

U.S. Bank ...14

Conclusion ...18

Research Methodology... 19

About PayStream Advisors...19

Executive Summary

Although PayStream Technology Insight reports are grounded in statistics, it is often what we see and hear in product demonstrations that gives us a sense of the market at ground level. Last year, this “chatter” was all about The Cloud and supplier recruitment. In 2012, we saw more streamlined navigation, more integrated workflow automation, and heard about mobile applications for smart phones and tablets, offering a range of functionality from notifications to simple transactional capabilities.

Adoption has been of keen interest among an elite group of suppliers, and innovations like Software as a Service (SaaS), fee-free supplier portals, dynamic discounting, and mobile transactional capabilities, are opening up the middle market. But we still have a long way to go.

Consider that there are, say, 15 million businesses, in the United States alone, transacting business with other businesses (B2B), and only 700,000 of those companies are sending invoices electronically. And that’s using the term

“electronic” loosely – about half of those electronic invoices are electronic paper – static scans that must still be converted to data and assimilated into an electronic workflow.

That said, there does seem to be a growing acceptance within the industry that eInvoicing is not an end in itself, but rather part of a process and a culture involving integrated accounting systems, workflow, communications and supplier management.

Earlier this year, PayStream Advisors documented these trends in the “eInvoicing Adoption Benchmarking Report 2012,” based on the responses of more than 300 AP and procurement professionals at U.S.-based enterprises. Subsequent research has followed the trend through the supply chain and found that it holds true from purchase to pay. This report elaborates on those findings by putting them in a broader context.

PayStream Advisors has developed this Technology Insight Series report titled “Electronic Invoice Management: Going with the (Work)flow,” for organizations with an active interest in eInvoicing who would benefit from an in-depth analysis of recent trends and solutions, plus profiles of leading solution providers.

Electronic Invoice Management is one of several reports available for download from our corporate research library at: http://www.paystreamadvisors.com/ eResearch/

Move to the Middle

“Companies with revenues over USD $2 billion (“Titans”) have largely

automated . . . The good news: Titans only represent 10 percent of the invoice volume to be automated.”

– Henry Ijams, Managing Director of PayStream Advisors

– PayStream Advisors Market Update and Research Preview, Oct. 23, 2012

After more than a decade of market excitement about the coming electronic future, only now are we beginning to move from the long tail of large early adopters into the fat middle market of small and medium-sized enterprises (SME). And, as we reported in last year’s report “Electronic Invoice Management: The Cloud’s Silver Lining,” the future looks much different than the past.

Cloud payments, measured at $4.7 billion in 2011, are forecasted to more than double over the next four years, as the buyers and vendors of the middle market increasingly find common ground in the fast, flexible, affordable and mobile internet future.

The technology has been proven. The results of the larger companies are there for all to see. The challenge now is to replicate those results across a broader spectrum of companies with cultures and processes that become increasingly ad hoc as you move down the revenue range.

Figure 1

Adoption of Imaging and Workflow Technologies by Company Size While large companies

lead the pack in automation, small companies are quick to embrace automated workflow. 62% 51% 23% 27% 17% 15% 59% 46% 32%

Front-End Imaging Back-End Imaging Automated Workflow Large Medium Small

Integration, more than new functionality – with the possible exception of mobile applications – is the order of the day. If an invoice comes in electronically without a system in place to route it through accounts payable, you’re really not much better off than you were with a paper invoice. As the saying goes: It’s not what you do, it’s how you do it that counts. This convergence of eInvoicing with Workflow Automation is the story of 2012.

And Now, the Numbers . . .

Any discussion of adoption, logically begins with a look at what we are up against, and while resistance, overall, is decreasing, the barriers themselves remain,

proportionally the same, with supplier resistance, the perennial favorite, still on top, followed by the persistent belief that the old ways work best, and, as always, the “We can’t afford it,” argument. It should not be surprising then, to see solution providers focusing aggressively on supplier recruitment and affordable Software-as-a-Service delivery models.

This adaptability seems to be paying dividends as more than 70 percent of

companies surveyed have either adopted or are evaluating eInvoicing technology – up 3 percentage points from 2011.

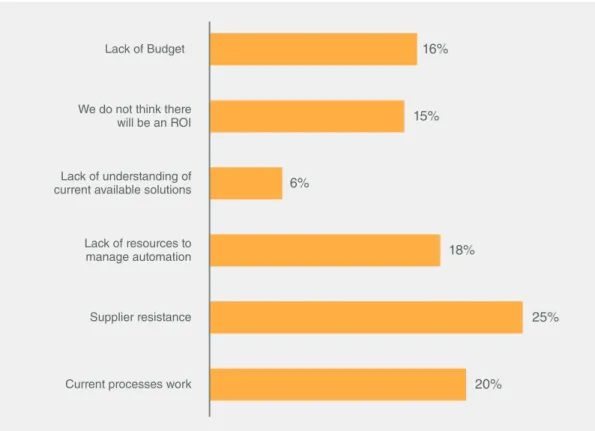

Figure 2 Barriers to eInvoice

Adoption

2012 survey results reveal that supplier resistance is the number one challenge to electronic invoice adoption.

16%

Lack of Budget

15%

We do not think there will be an ROI

6%

Lack of understanding of current available solutions

18% Lack of resources to manage automation 25% Supplier resistance 20%

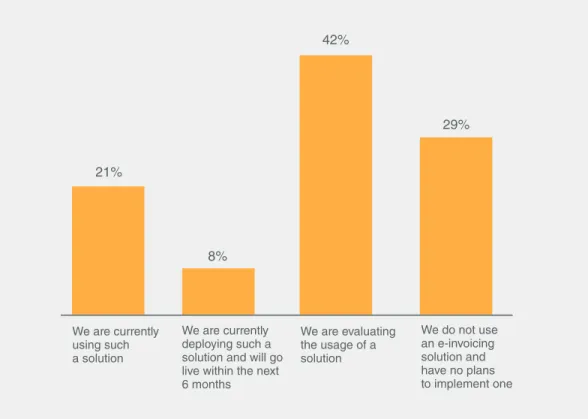

Figure 3 Adoption of eInvoicing

Solutions Over 70 percent of companies surveyed have either adopted or are evaluating eInvoicing technology. 29% We do not use an e-invoicing solution and have no plans to implement one 42% We are evaluating the usage of a solution 8% We are currently deploying such a solution and will go live within the next 6 months We are currently

using such a solution

Making a Case for Automation

Culture is Critical

With the possible exception of archiving, a static electronic invoice isn’t much better than a paper one. The real value of eInvoicing lies in how successful you are at assimilating invoice data into accounting systems and management workflows. It is this culture of integration that will yield the best return on investment.

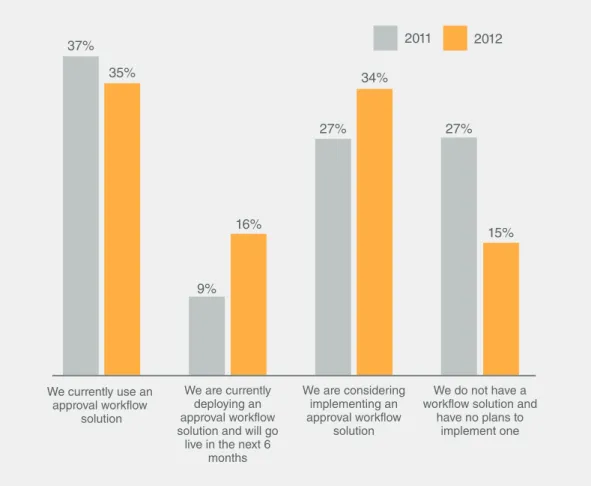

More than 80 percent of the companies surveyed by PayStream Advisors over the past year responded they have adopted an imaging solution, or are considering purchasing one.

Figure 4 Adoption of Workflow

Technologies More than 80 percent of the companies surveyed by PayStream Advisors over the past year responded they have adopted an imaging solution, or are considering purchasing one. 2011 2012 35% 37% We currently use an approval workflow solution 16% 9% We are currently deploying an approval workflow solution and will go

live in the next 6 months 34% 27% We are considering implementing an approval workflow solution 15% 27% We do not have a workflow solution and

have no plans to implement one

The volume of paper invoices received is also decreasing – dropping from more than three quarters to just a little under two thirds of total invoices, in the past year alone.

Figure 5 Usage of AP Automation

Technologies ePayment and P-Cards continue to hold the lead in AP automation technologies.

Using Implementing In 6 Months

56% 24% Front-end Imaging 37% 30% OCR/Automated Data Capture 53% 27% Automated Workflow 83% 17% Electronic Payments Purchasing Cards 16% 84% Figure 6 Methods Used to Trade

B2B Invoices Paper invoices are decreasing; however, they continue to lead the pack in methods used to trade B2B invoices. 13% Email 6% Fax 22% eInvoice/Portals/EDI Paper 59%

Historically, the move from paper to electronic invoicing has been driven by the accuracy and efficiency of workflow achieved by eliminating manual data entry and the time-consuming routing of hard-copy invoices for approval. The current wave of automation, however, is being driven by a variety of factors. More than half of companies that adopted eInvoicing solutions cited a reduction in full time employee (FTE) or processing costs and faster approval cycles as key system benefits, along with a broader application of eInvoicing solutions as management information tools to provide greater visibility into spending, improved cash management, and an increased ability to capitalize on early-payment discounts.

Challenges Faced in Current AP Operations

PayStream’s “Invoice Automation Adoption Survey 2012” documented the challenges that current AP operations face. The good news is that significant progress is being made. The first step toward improving a process is understanding the faults and failures of the current system. But as the following graph illustrates, much remains to be done.

Factors Driving Interest in Automation

As accounts payable departments become more centralized, companies are reaping the benefits of stronger trading relationships, dynamic discounting,

risk-Figure 7 Challenges in the Invoice

Management Process 2011 2012 65% 52% 17% 16% 18% 14% 43% 40% 13% 11% 24% 19% 16% 15% Majority of invoices received in paper format Decentralized invoice receipt Lost or Missing invoices Manual data entry and inefficient processes Lack of visibility into outstanding liabilities High number of discrepancies and exceptions Inability to approve invoices in time to capture discounts

management and cash management. Automation solutions that enable trading partners – buyers, suppliers and banks – to seamlessly exchange transaction-related information and funds are becoming increasingly popular. Specific factors driving interest in automation include:

» A competitive business environment is forcing businesses, especially small and medium-sized ones, to focus on reducing processing costs and increase efficiencies associated with invoices and employee expenses. » Streamlining the AP process has become vital in a tough economy where

adequate cash flow and greater control over payables are critical to maintaining liquidity and sustaining business operations.

» Increased interest in early payment discount capture drives smaller

organizations in particular to investigate tools and technologies that enable them to compress their invoice receipt-to-approval cycles.

Buyer Benefits of AP Automation

Buyers, particularly small and medium-sized companies, are responding to the low upfront costs, minimal IT commitment, enhanced reporting and cash management services offered by Cloud-based solutions. It’s true that for some companies, the Cloud isn’t always an option. In particular, some larger companies and

governmental entities have policies requiring onsite hosting and/or staff-managed

Figure 8 Top Financial Automation Goals for 2012

Automated approval workflow and eInvoicing are the top two automation goals for 2012. 14% 8% 2% 28% 19% 29% Increase electronic invoicing Implement invoice imaging Automated approval workflow for Invoices

Automate payment processing ERP application upgrade Outsource portions of AP process

Workflow Adoption Survey provides results that make a compelling case for AP Automation:

» 75 percent of all adopters reported shorter invoice approval cycles » 58 percent experienced lower processing costs

» 50 percent increased employee productivity

» 33 percent of adopters surveyed had used automation to improve visibility over liabilities

» 20 percent reported a reduction in late payment penalties and interest » 14 percent reported an improvement in regulatory compliance

These results are consistent with previous years although most categories show a slight increase. The survey demonstrates a trend toward businesses using AP Automation as a business information and cash management tool and not just a means to reduce head count.

Supplier Value Proposition of AP Automation

Suppliers, too, seem to be rallying behind recent value-added services, such as supplier networks, dynamic discounting, purchase order to invoice flips, and low to no-fee supplier transaction costs. Suppliers who have adopted electronic invoicing have reaped a number of tangible benefits:

Figure 9 Benefits of Approval

Workflow Quicker approval cycles ranks as the top benefit to approval workflow. 58% 20% 14% 75% 50% 33% Quicker approval of invoices Increased employee productivity Improved visibility over liabilities

Lower processing costs

Reduction in late payment penalties and interest

Better compliance with regulatory requirements (SOX, FASB)

» Increased Efficiencies: Significant time is saved when employees do not have to print paper invoices and mail them to their customers, freeing up accounts receivable staff to focus on more value-added activities like collections and customer relations.

» Lower Costs: Reduction in labor, material and postage costs are common with all eInvoicing solutions. Our research reveals that suppliers who adopt electronic invoicing can slash their invoice management costs by more than 50 percent.

» Error Reduction: Validation rules configured into eInvoicing solutions flag errors at the time of submission itself and prompt suppliers to correct them, reducing the number of exception invoices downstream.

» Faster Settlement: Electronic invoicing shortens the invoice processing and approval cycle on the buyer side. Combined with electronic payments, this ensures that suppliers are paid on time, or in some cases, early.

» Improved Visibility: Suppliers have real-time access to invoice and payment status from a standard Web browser, providing for quicker handling of

reconciliation questions and fewer help desk calls.

» Better Cash flow Forecasting: Automating invoice processing and payments reduces uncertainties. Consistency around payment timing means suppliers can better perform cash flow forecasting.

» Eliminate Reprint Requests: Electronic invoicing solutions drastically reduce the number of lost and missing invoices, which means reprint requests from buyers will virtually be zero.

» Quicker Dispute Resolution: Suppliers now can view disputed invoices at any time and provide supporting/backup documentation as needed, making dispute resolution a collaborative process as well as accelerating resolution. » Decreased Days Sales Outstanding: Dynamic discounting and supply

chain finance capabilities available as part of eInvoicing solutions allow suppliers to decrease days sales outstanding (DSO) without adversely affecting customer relations.

» Access to Cheaper Capital: Dynamic discounting delivers financing at more attractive rates to suppliers than factoring or asset based lending.

Overcoming Barriers to Adoption

Despite the steady increase in the number of companies adopting electronic invoicing, paper invoices remain the primary method of B2B billing in the United States, see Figure 6. Barriers to adoption today remain the same as they’ve always been. Here’s where things stand.

Supplier Resistance

Although eInvoicing expedites payments, the very prospect can raise the hackles of suppliers who are content with their paper-based system and not of a mind to change. Twenty-three percent of survey responders cited their belief that “current processes work” as the main reason for avoiding eInvoicing. It can be difficult to overcome resistance from suppliers who believe the saying, “if it isn’t broke, don’t fix it.” In this case, the buyer’s success depends upon demonstrating to their supplier a compelling value proposition.

Suppliers want to know “what’s in it for them.” Buyers need to have a compelling answer. Suppliers will respond positively to evidence that participating in a cloud-based eInvoicing solution will result in accelerated payments, new business referrals, enhanced reporting, financing opportunities, and improved cash management. Supplier recruitment also requires an ongoing effort. The steady growth of supplier participation demonstrates the positive results of persistence.

Technical Challenges

This was once a formidable obstacle. Today, however, the challenge of integrating new applications with legacy systems is becoming less daunting. Most applications on the market today integrate easily with systems on buyer and supplier sides, resulting in secure and seamless data transfer, as well as streamlined processes and more efficient workflows. This trend should accelerate as companies replace older legacy systems with modern architecture, and

adopters realize the benefits of faster approval and cycle times, better cash flow forecasting and vendor relations.

For those companies concerned with the upfront costs of technology, hosted solutions and Software-as-Service (SaaS) delivery models offer minimal

implementation costs. The technology providers are responsible for maintenance and upgrades.

Business Practices

Old habits die hard. It’s human nature. That’s especially true in business, where change usually means learning new skills, spending more money, and training. Giving up the old ways is hard enough when change is driven by your own business practices. It can be even more challenging when the change is driven by outside factors. Solution providers have made great strides in recent years addressing this barrier to adoption,

making it easier for suppliers to transact compared to legacy EDI solutions – including supplier portals to manage transactions and track their status, and providing vendor support services that encourage adoption and minimize disruption.

Today, simply allowing vendors to submit electronic invoices by returning or “flipping” purchase orders as invoices has gone a long way toward breaking down supplier resistance.

External Change Begins with Internal Change

In negotiating it is often easier to get what you want when you offer something of value in return. Flippable purchase orders – the electronic equivalent of business reply mail – are a good start. With more than 32 percent of survey respondents indicating that they send more than half of their purchase orders electronically to suppliers, having the ability for suppliers to simply turn those purchase orders around into error-free invoices with the promise of straight-through processing — read that: lower processing costs, faster payment, and fewer invoice errors – is proving to be a major persuader. And, of course, once the transaction has gone electronic, it opens the door for powerful back-end benefits, such as dynamic discounting, a valuable source of liquidity, especially for small and mid-sized suppliers.

U.S. Bank

U.S. Bancorp is one of the oldest and most-trusted banks in America. Founded in 1863, it has grown to the fifth-largest bank in the United States. The company prides itself on having the expertise and stability to meet all of their clients’ financial needs, and doing it with a level of service no other provider can match. U.S. Bank Electronic Invoice Presentment and Payment (EIPP) is a cloud-based Software-as-a-Service (SaaS) solution. Since it is cloud-based, it requires no software installation, and minimizes IT requirements and resources to enable clients to quickly achieve speed to value, lower their total cost of ownership and increase user adoption and employee productivity.

Website www.usbpayment.com

Founded U.S. Bancorp: 1863; Corporate Payment Systems division: 1986

Headquarters Minneapolis, MN

Other Locations Global offices located in North America, Europe and Asia

Employees U.S. Bank: 61,000; Corporate Payment Systems: 630

Net Income U.S. Bancorp: $4.87 billion (2011)

Customers U.S. Bank: 17.4 million; Corporate Payment Systems: 6,300

End Users 41,000

Annual Transaction

Volume 24 million invoices; more than 78 million supporting documents

Industry Segments Transportation, public sector (federal/state/ municipal), commercial real estate, education & nonprofit, energy, healthcare & pharmaceutical, insurance, manufacturing, oil & gas, retail & apparel, services, telecom & utilities, among others

Key Accounts Due to client confidentiality, U.S. Bank does not disclose this information

Awards / Recognitions Enterprise Value Award (CIO), Most Admired Superregional Bank (Fortune), One of America’s Greenest Banks (Bank Technology News), Most Reputable Companies (Forbes), Best Bank in the United States (Euromoney), #1 Most Trusted Bank in Consumer Protection (Ponemon Institute), One of the World’s 50 Safest Banks (Global Finance)

Solution Overview

U.S. Bank pioneered electronic payment products as the first commercial bank card issuer, and is proud to still lead the way today. U.S. Bank provides a comprehensive array of B2B payment solutions across all market segments, program sizes and locations. Customer retention averages over 10 years because many clients view U.S. Bank Corporate Payment Systems as a trusted, dependable partner.

U.S. Bank EIPP facilitates complex, data rich, high-value transactions that enable clients to eliminate costs associated with paper processing, increase control over payments and better manage cash flow. U.S. Bank EIPP is built on the Syncada® from Visa network––a joint venture between U.S. Bank and Visa that provides the most up-to-date technology and access to the only non-proprietary global multi-bank invoice and payment processing and financing network.

Supplier Recruitment

Full service supplier enrollment is included in the U.S. Bank EIPP offering.

Approximately 12,000 suppliers are already connected to the network. U.S. Bank’s supplier enrollment team works closely with clients to identify and prioritize

additional suppliers they want to join the network. Bank personnel actively support the recruitment effort by enabling suppliers for eInvoicing and providing training prior to going online and after enrolling. U.S. Bank EIPP provides a powerful incentive for suppliers to enroll, including reduced billing and payment errors, lower costs from the elimination of expensive paper processes and access to financing.

Electronic Invoicing

After the U.S. Bank EIPP solution captures the data, the system automatically validates invoices against the vendor master data, providing two-way or three-way matching to the PO or goods received note. Flexible business rules enable the client to customize the validation process to meet their specific business needs. This results in the majority of invoices processed “straight-through” to payment without human intervention.

The solution visually flags discrepancies for immediate attention, thus increasing processing efficiency and speed of pay. Enrolled suppliers can log in to a self-service supplier portal, which allows them to complete key accounts receivable tasks such as dispute resolution. Clients can use the system to send suppliers direct messages regarding invoice errors, and suppliers can make the appropriate adjustments to their invoices right in the system.

The solution also offers a unique ability to track utility bills. The system loads not only total invoice amount but also usage statistics such as BTUs. This enables

Approval Workflow

U.S. Bank EIPP includes an automated approval and workflow tool. Clients have the ability to customize the solution according to their business rules during system implementation. In addition to choosing their own method of invoice routing, the client can also determine the level of authority and accessibility for each user. The client determines invoice routing based on the criteria mission critical to their business.

If the invoice does not match a PO or other approval categories, the system flags it for further action by the appropriate staff member. That staff member can send the supplier a message directly from the U.S. Bank EIPP page that displays the invoice, allowing the supplier to immediately identify the discrepancy. If the supplier is not on the network, the system allows buyers to create an eBill (credit memo) for the supplier, which is a supplemental transaction correction document that offsets for the difference. U.S. Bank EIPP records and maintains a complete history of all user actions and events, enabling an efficient auditing process.

Working Capital Management

A key differentiator for U.S. Bank EIPP is its unique ability to make payments to suppliers on behalf of buyers. As the fifth largest bank in the United States, U.S. Bank provides a host of financing options and services for its customers. U.S. Bank EIPP’s improvements in processing efficiency for clients enable them to take advantage of early payment discounts and improve overall cash management. U.S. Bank offers a buyer financing model, where U.S. Bank pays the suppliers on the net due date and the buyer pays U.S. Bank directly on a later date, allowing buyers to conserve cash when necessary.

U.S. Bank also offers a supplier financing model, where U.S. Bank provides liquidity to suppliers for buyers who don’t wish to utilize their own cash to fund early payment discounts. By leveraging this program, buyers can extend days payable outstanding while suppliers decrease days sales outstanding. The

system is configured to take advantage of financing for both suppliers and buyers, depending upon what works best for the client’s business.

Electronic Payments

U.S. Bank EIPP is the largest network offering both invoice and payment

processing in conjunction with buyer and supplier trade payables financing. U.S. Bank’s experience with electronic payment processing enables all payments to be made seamlessly and efficiently. The solution accepts a wide range of payments including ACH/EFT, wire transfer and cardless payment accounts through U.S. Bank. Of course, the system also supports conventional paper check issuing.

Reporting and Analytics

U.S. Bank EIPP includes a dashboard that enables users to track key activities, tasks and Accounts Payable-related operational and productivity metrics. The solution includes a wide range of standard reports and the ability for users to create custom reports at both summary and transaction levels. A robust search tool allows users to find specific documents, transactions, invoices requiring approval and other information quickly and efficiently. Data can also be exported into third-party tools like Crystal reports in formats including HTML, PDF, Excel, CSV and XML.

Pricing and Implementation

Standard implementation is 90 days. The process is designed to be collaborative while maintaining appropriate checks and balances, so individual client times may vary due to resource availability, process and system complexity. U.S. Bank offers a “warranty period” for a period of time after implementation where U.S. Bank project managers stay directly involved with the customer team to ensure a smooth transition. U.S. Bank offers ongoing support via a dedicated, multi-tier client support team that includes online tools as well as a toll-free customer service line. Fees are charged on a per-invoice basis and follow a tiered-pricing structure.

Conclusion

Electronic Invoice Management is a top priority among executives in the

PayStream 2012 survey. Twenty-eight percent said they have already launched an invoice automation initiative and another 47 percent said they plan to within a year. But eInvoicing, alone, is not enough. Companies considering adoption need to plan for what they’re going to do with data once they get it. Without a supplier management strategy and culture conducive to workflow automation, the potential for friction is high. The solution providers profiled at the back of this report, have devoted considerable developmental resources toward addressing this problem, and we are encouraged by what we are seeing.

The market for eInvoicing is opening up. Currently at $280 million, PayStream predicts demand is growing at a compound average annual growth rate of 13 percent. But if you look at where we are in the big picture, we are still in about the third inning.

Research Methodology

The findings in this report are based on the results of PayStream Advisors 2012 Invoice & Workflow Automation Adoption and Electronic Invoice surveys. Participants in the surveys included more than 300 AP professionals. Based on our experience and the number of respondents, the survey has a confidence level of +/-5 percent.

About PayStream Advisors, Inc.

PayStream Advisors is a technology research and consulting firm that improves the way companies plan, evaluate, and select emerging technologies to achieve their business objectives. PayStream Advisors assists clients in sorting through the growing complexities of IT applications related to business process automation with the goal of making objective, analytical, and actionable recommendations. Wherever business process automation technology is an issue, PayStream Advisors is there to help. For more information, call (704) 523-7357 or visit us on the web at www.paystreamadvisors. com.