Appendices

A.

Data Selection For Empirical Analysis

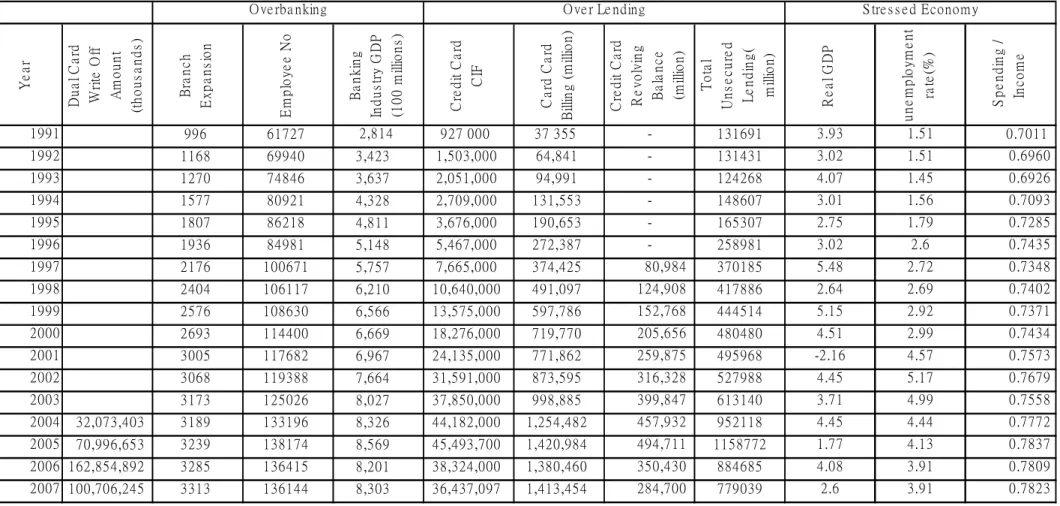

Table A-1

Data Sets from Period 1991 to 2007

Y

ear

D

u

al

C

ar

d

Wr

ite

O

ff

A

m

ount

(t

hous

a

nds

)

Br

a

n

c

h

Ex

pa

n

s

ion

E

m

pl

oy

e

e

N

o

Ba

n

k

in

g

Indu

s

tr

y

G

D

P

(1

0

0

m

illio

n

s

)

C

red

it

C

ar

d

CI

F

Ca

rd

Ca

rd

B

illin

g

(

m

illio

n

)

C

red

it

C

ar

d

Re

v

o

lv

in

g

Ba

la

n

c

e

(m

illio

n

)

To

ta

l

Un

s

e

c

u

re

d

L

e

n

di

ng(

m

illio

n

)

R

eal

G

D

P

une

m

pl

oy

m

e

nt

ra

te

(%

)

S

pe

ndi

ng

/

In

c

o

m

e

1991

996

61727

2,814

927 000

37 355

-

131691

3.93

1.51

0.7011

1992

1168

69940

3,423

1,503,000

64,841

-

131431

3.02

1.51

0.6960

1993

1270

74846

3,637

2,051,000

94,991

-

124268

4.07

1.45

0.6926

1994

1577

80921

4,328

2,709,000

131,553

-

148607

3.01

1.56

0.7093

1995

1807

86218

4,811

3,676,000

190,653

-

165307

2.75

1.79

0.7285

1996

1936

84981

5,148

5,467,000

272,387

-

258981

3.02

2.6

0.7435

1997

2176

100671

5,757

7,665,000

374,425

80,984

370185

5.48

2.72

0.7348

1998

2404

106117

6,210

10,640,000

491,097

124,908

417886

2.64

2.69

0.7402

1999

2576

108630

6,566

13,575,000

597,786

152,768

444514

5.15

2.92

0.7371

2000

2693

114400

6,669

18,276,000

719,770

205,656

480480

4.51

2.99

0.7434

2001

3005

117682

6,967

24,135,000

771,862

259,875

495968

-2.16

4.57

0.7573

2002

3068

119388

7,664

31,591,000

873,595

316,328

527988

4.45

5.17

0.7679

2003

3173

125026

8,027

37,850,000

998,885

399,847

613140

3.71

4.99

0.7558

2004

32,073,403

3189

133196

8,326

44,182,000

1,254,482

457,932

952118

4.45

4.44

0.7772

2005

70,996,653

3239

138174

8,569

45,493,700

1,420,984

494,711

1158772

1.77

4.13

0.7837

2006 162,854,892

3285

136415

8,201

38,324,000

1,380,460

350,430

884685

4.08

3.91

0.7809

2007 100,706,245

3313

136144

8,303

36,437,097

1,413,454

284,700

779039

2.6

3.91

0.7823

O ve rba nking

O ve r Le nding

S tre s s e d Economy

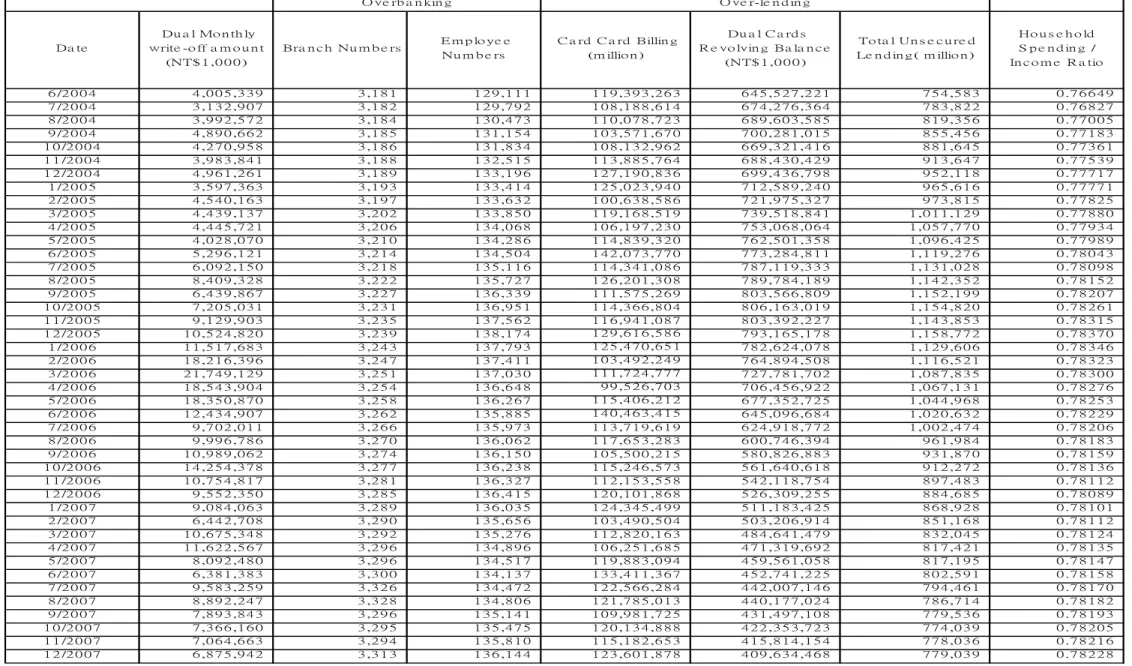

Table A-2

Data Sets from June 2004 to December 2007

Da te Du a l Mo n th ly write -o ff a m o u n t (NT$ 1 ,0 0 0 ) Bra n c h Nu m b e rs E m p lo ye e Nu m b e rs C a rd C a rd Billin g (m illio n ) Du a l C a rd s R e vo lvin g Ba la n c e (NT$ 1 ,0 0 0 ) To ta l Un s e c u re d Le n d in g ( m illio n ) Ho u s e h o ld S p e n d in g / In c o m e R a tio 6 /2 0 0 4 4 ,0 0 5 ,3 3 9 3 ,1 8 1 1 2 9 ,1 1 1 1 1 9 ,3 9 3 ,2 6 3 6 4 5 ,5 2 7 ,2 2 1 7 5 4 ,5 8 3 0 .7 6 6 4 9 7 /2 0 0 4 3 ,1 3 2 ,9 0 7 3 ,1 8 2 1 2 9 ,7 9 2 1 0 8 ,1 8 8 ,6 1 4 6 7 4 ,2 7 6 ,3 6 4 7 8 3 ,8 2 2 0 .7 6 8 2 7 8 /2 0 0 4 3 ,9 9 2 ,5 7 2 3 ,1 8 4 1 3 0 ,4 7 3 1 1 0 ,0 7 8 ,7 2 3 6 8 9 ,6 0 3 ,5 8 5 8 1 9 ,3 5 6 0 .7 7 0 0 5 9 /2 0 0 4 4 ,8 9 0 ,6 6 2 3 ,1 8 5 1 3 1 ,1 5 4 1 0 3 ,5 7 1 ,6 7 0 7 0 0 ,2 8 1 ,0 1 5 8 5 5 ,4 5 6 0 .7 7 1 8 3 1 0 /2 0 0 4 4 ,2 7 0 ,9 5 8 3 ,1 8 6 1 3 1 ,8 3 4 1 0 8 ,1 3 2 ,9 6 2 6 6 9 ,3 2 1 ,4 1 6 8 8 1 ,6 4 5 0 .7 7 3 6 1 1 1 /2 0 0 4 3 ,9 8 3 ,8 4 1 3 ,1 8 8 1 3 2 ,5 1 5 1 1 3 ,8 8 5 ,7 6 4 6 8 8 ,4 3 0 ,4 2 9 9 1 3 ,6 4 7 0 .7 7 5 3 9 1 2 /2 0 0 4 4 ,9 6 1 ,2 6 1 3 ,1 8 9 1 3 3 ,1 9 6 1 2 7 ,1 9 0 ,8 3 6 6 9 9 ,4 3 6 ,7 9 8 9 5 2 ,1 1 8 0 .7 7 7 1 7 1 /2 0 0 5 3 ,5 9 7 ,3 6 3 3 ,1 9 3 1 3 3 ,4 1 4 1 2 5 ,0 2 3 ,9 4 0 7 1 2 ,5 8 9 ,2 4 0 9 6 5 ,6 1 6 0 .7 7 7 7 1 2 /2 0 0 5 4 ,5 4 0 ,1 6 3 3 ,1 9 7 1 3 3 ,6 3 2 1 0 0 ,6 3 8 ,5 8 6 7 2 1 ,9 7 5 ,3 2 7 9 7 3 ,8 1 5 0 .7 7 8 2 5 3 /2 0 0 5 4 ,4 3 9 ,1 3 7 3 ,2 0 2 1 3 3 ,8 5 0 1 1 9 ,1 6 8 ,5 1 9 7 3 9 ,5 1 8 ,8 4 1 1 ,0 1 1 ,1 2 9 0 .7 7 8 8 0 4 /2 0 0 5 4 ,4 4 5 ,7 2 1 3 ,2 0 6 1 3 4 ,0 6 8 1 0 6 ,1 9 7 ,2 3 0 7 5 3 ,0 6 8 ,0 6 4 1 ,0 5 7 ,7 7 0 0 .7 7 9 3 4 5 /2 0 0 5 4 ,0 2 8 ,0 7 0 3 ,2 1 0 1 3 4 ,2 8 6 1 1 4 ,8 3 9 ,3 2 0 7 6 2 ,5 0 1 ,3 5 8 1 ,0 9 6 ,4 2 5 0 .7 7 9 8 9 6 /2 0 0 5 5 ,2 9 6 ,1 2 1 3 ,2 1 4 1 3 4 ,5 0 4 1 4 2 ,0 7 3 ,7 7 0 7 7 3 ,2 8 4 ,8 1 1 1 ,1 1 9 ,2 7 6 0 .7 8 0 4 3 7 /2 0 0 5 6 ,0 9 2 ,1 5 0 3 ,2 1 8 1 3 5 ,1 1 6 1 1 4 ,3 4 1 ,0 8 6 7 8 7 ,1 1 9 ,3 3 3 1 ,1 3 1 ,0 2 8 0 .7 8 0 9 8 8 /2 0 0 5 8 ,4 0 9 ,3 2 8 3 ,2 2 2 1 3 5 ,7 2 7 1 2 6 ,2 0 1 ,3 0 8 7 8 9 ,7 8 4 ,1 8 9 1 ,1 4 2 ,3 5 2 0 .7 8 1 5 2 9 /2 0 0 5 6 ,4 3 9 ,8 6 7 3 ,2 2 7 1 3 6 ,3 3 9 1 1 1 ,5 7 5 ,2 6 9 8 0 3 ,5 6 6 ,8 0 9 1 ,1 5 2 ,1 9 9 0 .7 8 2 0 7 1 0 /2 0 0 5 7 ,2 0 5 ,0 3 1 3 ,2 3 1 1 3 6 ,9 5 1 1 1 4 ,3 6 6 ,8 0 4 8 0 6 ,1 6 3 ,0 1 9 1 ,1 5 4 ,8 2 0 0 .7 8 2 6 1 1 1 /2 0 0 5 9 ,1 2 9 ,9 0 3 3 ,2 3 5 1 3 7 ,5 6 2 1 1 6 ,9 4 1 ,0 8 7 8 0 3 ,3 9 2 ,2 2 7 1 ,1 4 3 ,8 5 3 0 .7 8 3 1 5 1 2 /2 0 0 5 1 0 ,5 2 4 ,8 2 0 3 ,2 3 9 1 3 8 ,1 7 4 1 2 9 ,6 1 6 ,5 8 6 7 9 3 ,1 6 5 ,1 7 8 1 ,1 5 8 ,7 7 2 0 .7 8 3 7 0 1 /2 0 0 6 1 1 ,5 1 7 ,6 8 3 3 ,2 4 3 1 3 7 ,7 9 3 1 2 5 ,4 7 0 ,6 5 1 7 8 2 ,6 2 4 ,0 7 8 1 ,1 2 9 ,6 0 6 0 .7 8 3 4 6 2 /2 0 0 6 1 8 ,2 1 6 ,3 9 6 3 ,2 4 7 1 3 7 ,4 1 1 1 0 3 ,4 9 2 ,2 4 9 7 6 4 ,8 9 4 ,5 0 8 1 ,1 1 6 ,5 2 1 0 .7 8 3 2 3 3 /2 0 0 6 2 1 ,7 4 9 ,1 2 9 3 ,2 5 1 1 3 7 ,0 3 0 1 1 1 ,7 2 4 ,7 7 7 7 2 7 ,7 8 1 ,7 0 2 1 ,0 8 7 ,8 3 5 0 .7 8 3 0 0 4 /2 0 0 6 1 8 ,5 4 3 ,9 0 4 3 ,2 5 4 1 3 6 ,6 4 8 9 9 ,5 2 6 ,7 0 3 7 0 6 ,4 5 6 ,9 2 2 1 ,0 6 7 ,1 3 1 0 .7 8 2 7 6 5 /2 0 0 6 1 8 ,3 5 0 ,8 7 0 3 ,2 5 8 1 3 6 ,2 6 7 1 1 5 ,4 0 6 ,2 1 2 6 7 7 ,3 5 2 ,7 2 5 1 ,0 4 4 ,9 6 8 0 .7 8 2 5 3 6 /2 0 0 6 1 2 ,4 3 4 ,9 0 7 3 ,2 6 2 1 3 5 ,8 8 5 1 4 0 ,4 6 3 ,4 1 5 6 4 5 ,0 9 6 ,6 8 4 1 ,0 2 0 ,6 3 2 0 .7 8 2 2 9 7 /2 0 0 6 9 ,7 0 2 ,0 1 1 3 ,2 6 6 1 3 5 ,9 7 3 1 1 3 ,7 1 9 ,6 1 9 6 2 4 ,9 1 8 ,7 7 2 1 ,0 0 2 ,4 7 4 0 .7 8 2 0 6 8 /2 0 0 6 9 ,9 9 6 ,7 8 6 3 ,2 7 0 1 3 6 ,0 6 2 1 1 7 ,6 5 3 ,2 8 3 6 0 0 ,7 4 6 ,3 9 4 9 6 1 ,9 8 4 0 .7 8 1 8 3 9 /2 0 0 6 1 0 ,9 8 9 ,0 6 2 3 ,2 7 4 1 3 6 ,1 5 0 1 0 5 ,5 0 0 ,2 1 5 5 8 0 ,8 2 6 ,8 8 3 9 3 1 ,8 7 0 0 .7 8 1 5 9 1 0 /2 0 0 6 1 4 ,2 5 4 ,3 7 8 3 ,2 7 7 1 3 6 ,2 3 8 1 1 5 ,2 4 6 ,5 7 3 5 6 1 ,6 4 0 ,6 1 8 9 1 2 ,2 7 2 0 .7 8 1 3 6 1 1 /2 0 0 6 1 0 ,7 5 4 ,8 1 7 3 ,2 8 1 1 3 6 ,3 2 7 1 1 2 ,1 5 3 ,5 5 8 5 4 2 ,1 1 8 ,7 5 4 8 9 7 ,4 8 3 0 .7 8 1 1 2 1 2 /2 0 0 6 9 ,5 5 2 ,3 5 0 3 ,2 8 5 1 3 6 ,4 1 5 1 2 0 ,1 0 1 ,8 6 8 5 2 6 ,3 0 9 ,2 5 5 8 8 4 ,6 8 5 0 .7 8 0 8 9 1 /2 0 0 7 9 ,0 8 4 ,0 6 3 3 ,2 8 9 1 3 6 ,0 3 5 1 2 4 ,3 4 5 ,4 9 9 5 1 1 ,1 8 3 ,4 2 5 8 6 8 ,9 2 8 0 .7 8 1 0 1 2 /2 0 0 7 6 ,4 4 2 ,7 0 8 3 ,2 9 0 1 3 5 ,6 5 6 1 0 3 ,4 9 0 ,5 0 4 5 0 3 ,2 0 6 ,9 1 4 8 5 1 ,1 6 8 0 .7 8 1 1 2 3 /2 0 0 7 1 0 ,6 7 5 ,3 4 8 3 ,2 9 2 1 3 5 ,2 7 6 1 1 2 ,8 2 0 ,1 6 3 4 8 4 ,6 4 1 ,4 7 9 8 3 2 ,0 4 5 0 .7 8 1 2 4 4 /2 0 0 7 1 1 ,6 2 2 ,5 6 7 3 ,2 9 6 1 3 4 ,8 9 6 1 0 6 ,2 5 1 ,6 8 5 4 7 1 ,3 1 9 ,6 9 2 8 1 7 ,4 2 1 0 .7 8 1 3 5 5 /2 0 0 7 8 ,0 9 2 ,4 8 0 3 ,2 9 6 1 3 4 ,5 1 7 1 1 9 ,8 8 3 ,0 9 4 4 5 9 ,5 6 1 ,0 5 8 8 1 7 ,1 9 5 0 .7 8 1 4 7 6 /2 0 0 7 6 ,3 8 1 ,3 8 3 3 ,3 0 0 1 3 4 ,1 3 7 1 3 3 ,4 1 1 ,3 6 7 4 5 2 ,7 4 1 ,2 2 5 8 0 2 ,5 9 1 0 .7 8 1 5 8 7 /2 0 0 7 9 ,5 8 3 ,2 5 9 3 ,3 2 6 1 3 4 ,4 7 2 1 2 2 ,5 6 6 ,2 8 4 4 4 2 ,0 0 7 ,1 4 6 7 9 4 ,4 6 1 0 .7 8 1 7 0 8 /2 0 0 7 8 ,8 9 2 ,2 4 7 3 ,3 2 8 1 3 4 ,8 0 6 1 2 1 ,7 8 5 ,0 1 3 4 4 0 ,1 7 7 ,0 2 4 7 8 6 ,7 1 4 0 .7 8 1 8 2 9 /2 0 0 7 7 ,8 9 3 ,8 4 3 3 ,2 9 6 1 3 5 ,1 4 1 1 0 9 ,9 8 1 ,7 2 5 4 3 1 ,4 9 7 ,1 0 8 7 7 9 ,5 3 6 0 .7 8 1 9 3 1 0 /2 0 0 7 7 ,3 6 6 ,1 6 0 3 ,2 9 5 1 3 5 ,4 7 5 1 2 0 ,1 3 4 ,8 8 8 4 2 2 ,3 5 3 ,7 2 3 7 7 4 ,0 3 9 0 .7 8 2 0 5 O ve rb a n kin g O ve r-le n d in gB.

National Credit Card Center

By 1980, the Ministry of Finance authorized a banking committee (Taiwan Bank, First

Commercial Bank, ICBC, Taiwan Middle and Small Enterprise, Cathay Trust, and China

Trust Investment) to form a separate committee to study the feasibility of developing plastic

payment in Taiwan.

Soon, in 1983, the National Union Card Center was setup to issue Union Card for

domestic transactions when the New Taiwan Dollar was not one of the international clearing

currencies, and in the following year, the center was renamed as National Credit Card

(NCC), and renamed again in 1988 as National Credit Card Center (NCCC), with setup of

over 200,000 merchant acceptance and 25 alliance banks to issue cards. By 1989, VISA

NT dollar card was introduced, and MasterCard NT dollar card came in the following year.

20

Before the NCCC was set up, the key players were mostly foreign banks, which

included Citibank, Bank of American, and American Express. Credit card was not a

popular payment media,

With support from VISA and the bank committee, NCCC was set up to process

domestic clearing and settlement and to support the electronic transaction exchange from

merchant acquiring bank to issuing bank, and at that time, new Taiwanese dollar was not an

international clearing currency, and international organization such as VISA or MasterCard

did not support NTD clearing and settlement.

The fee that NCCC charges includes the setup fee or joining fee, and a 50 basis charge

on the transaction amount to the acquiring bank and issuing bank. The revenues from the

fees are used to support to the operation of the NCCC, expansion of the merchant network,

network, system infrastructure, and development of future payment products.

20

C.

Join Credit Information Center

Joint Credit Information Center (JCIC) was established in 1975 under the Bankers

Association of Taipei, and is responsible for collecting, processing, and exchanging credit

data among financial institutions. In the 17 years of operation, JCIC keeps expanding its

business. As a result, the Bankers Association of Taipei decided in 1992 to donate all the

operating surplus of JCIC to establish the non-profit “Foundation of Joint Credit

Information Center”. The new JCIC continues to serve member institutions by providing

accurate and quality credit information on a user pay basis.

21

D.

Financial Supervisory Commission

In order to promote consolidated financial supervision, the Legislative Yuan passed the

Act of Governing the Establishment and Organization of the Financial Supervisory

Commission of the Executive Yuan on July 10, 2003. A new agency, named the Financial

Supervisory Commission (FSC), was set up on July 1 2004 to consolidate the supervision of

banking, securities and insurance industries under one roof, as well as to integrate the tasks

of examining these industries.

22

21

http://www.jcic.org.tw/history_eng.htm

22

E.

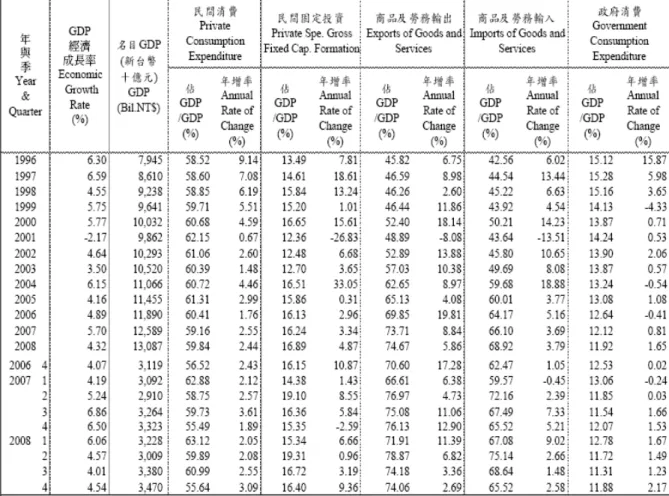

GDP Detail Break Down

This chapter provides the break down of the GDP from 1996 to April 2008. One of

the main reasons for the negative GDP for 2001 was lack of domestic and foreign

investment activity.

Table A-3

GDP Detail Break Down

F.

Financial Performance of ChinaTrust FHC and Taishin FHC

From the examination of 13 FHCs’ banking income statements, given there is one FSC

does not have a bank as its subsidiary, the top 3 banks that have huge reduction in the interest

income, for the fiscal year of 2005 and 2007, are Taishin Bank (45% reduction), ChinaTrust

(43% reduction), and Sinopac (41% reduction).

23

Furthermore, data also shows there is a

shift from consumer finance as major source of income to other businesses. Since Taishin

and ChinaTrust are the 2 largest credit card issuers, and have the greatest reduction of

interest income, this chapter takes a closer examination of the 2 FHCs, Taishin FHC and

China Trust FHC.

According to Taishin FHC’s annual reports, Taishin FHC has suffered loss since 2005.

Troubled financial performance is mainly due to their business weight on credit cards and

cash cards. Taishin is the largest cash card issuer and the 2

nd

largest credit card issuer in

2005.

Table A-4

Taishin Financial Holding Co Ltd: Operational Indicators

Unit: millions

2004 2005

2006

Net Operating Revenue

NT$59.1

NT$85.3

n/a

Net profit

NT$11.3

(NT$1.2)

(NT$8.0)

Number of employees

10289

10752

9515

Source: Taishin Bank’s Annual Report

In terms of sales revenue contribution in the banking business, dual card, credit card

combined with cash card, accounted for 42% in 2004, 50% in 2005, but has reduced to 43%

in 2006. The credit card share has decreased from 27% of the net sales revenue in 2005 to

21% in 2006, and its corporate business then showed a sign of increase as a result.

23

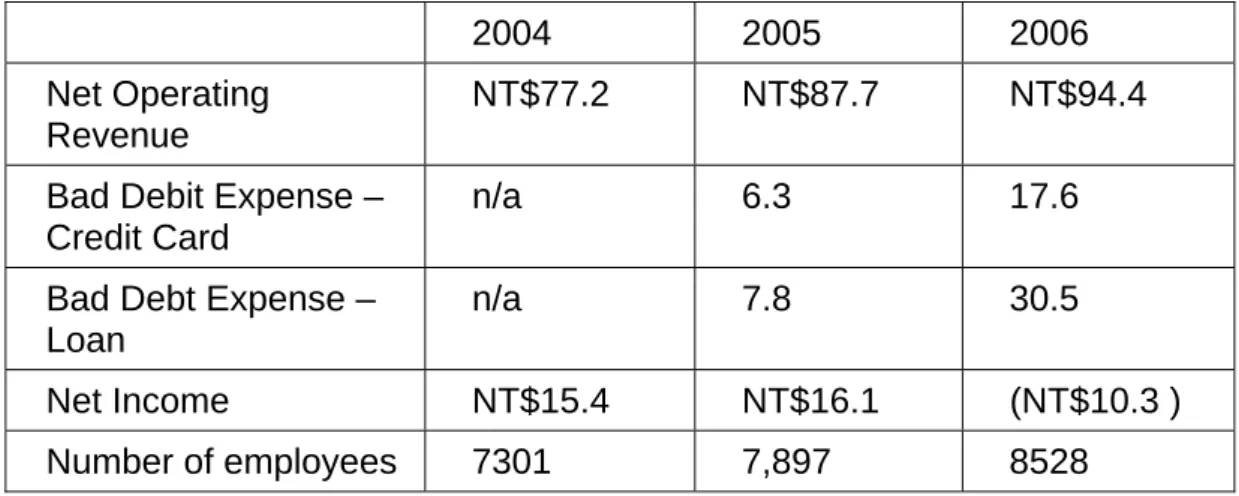

In terms of financial performance of China Trust FHC, she has suffered a loss in 2006,

including bad debt expense of 17.6 million in 2006 and only 6.3 million in 2005. The credit

card revenue only accounted for 26% of the business in 2004, and has increased to 31% in

2005.

Table A-5

Chinatrust Financial Holding Co Ltd: Operational Indicators

Unit: millions

2004

2005

2006

Net Operating

Revenue

NT$77.2 NT$87.7 NT$94.4

Bad Debit Expense –

Credit Card

n/a 6.3 17.6

Bad Debt Expense –

Loan

n/a 7.8 30.5

Net Income

NT$15.4

NT$16.1

(NT$10.3 )

Number of employees

7301

7,897

8528

G.

Domestic Banks’ Abridged Income Statement, Consolidated by FSC

Table A-6

Fubon Bank’s Abridged Income Statement

Unit: Million NTD

Tota l

Inte re s t

Income

S e rvice

Income

Ga in of

Fina ncia l

As s e t

a nd

Lia bilitie s

Othe rs

Tota l

Inte re s t

Expe ns e

S e rvice

Expe ns e

Ga in of

Fina ncia l

As s e t

a nd

Lia bilitie s

P e rs onne

l

Expe ns e

Othe rs

2005

Fubon Ba nk

50,796

34,925

9,227

4,044

-

2,600

44,017

19,398

3,997

4,744

15,879

3,643

1 0,422

2006

Fubon Ba nk

82,271

41,567

10,047

3,799

26,857

83,003

23,293

4,340

3,239

5,209

46,922

5 58

-173

2007

Fubon Ba nk

86,640

37,040

9,488

37,024

3,088

82,410

19,859

2,243

36,424

5,753

18,130

-

4,231

Othe r

Ga ins or

Los e s

Income

Be fore

Income

Ta x

Ye a r

Na me

Re ve nue

Expe ns e

Table A-7

Hua Nan Bank’s Abridged Income Statement

Unit: Million NTD

Tota l

Inte re s t

Income

S e rvice

Income

Ga in of

Fina ncia l

As s e t

a nd

Lia bilitie s

Othe rs

Tota l

Inte re s t

Expe ns e

S e rvice

Expe ns e

Ga in of

Fina ncia l

As s e t

a nd

Lia bilitie s

P e rs onne

l

Expe ns e

Othe rs

2005

Hua Na n Ba nk

53,361

37,900

4,337

3,742

-

7,382

43,398

20,605

879

8,678

13,235

1,991

11,954

2006

Hua Na n Ba nk

72,544

50,161

4,823

10,247

7,314

62,511

27,349

1,072

8,479

8,812

16,800

1,173

11,205

2007

Hua Na n Ba nk

78,068

55,970

6,654

9,529

5,916

66,055

30,717

1,344

9,578

9,078

15,339

-

12,013

Othe r

Ga ins or

Los e s

Income

Be fore

Income

Ta x

Ye a r

Na me

Re ve nue

Expe ns e

Table A-8

China Development Bank’s Abridged Income Statement

Unit: Million NTD

Tota l

Inte re s t

Income

S e rvice

Income

Ga in of

Fina ncia l

As s e t

a nd

Lia bilitie s

Othe rs

Tota l

Inte re s t

Expe ns e

S e rvice

Expe ns e

Ga in of

Fina ncia l

As s e t

a nd

Lia bilitie s

P e rs onne

l

Expe ns e

Othe rs

2005

China De ve lopme nt Ba nk

9,045

3,078

562

187

490

4,728

4,613

1,387

35

1,184

2,007

6,144

10,576

2006

China De ve lopme nt Ba nk

33,362

3,945

361

7,122

21,934

19,204

2,184

16

4,679

1,454

10,870

219

14,378

2007

China De ve lopme nt Ba nk

45,791

5,904

314

15,453

24,119

32,957

3,459

91

15,673

1,432

12,303

-

12,833

Othe r

Ga ins or

Los e s

Income

Be fore

Income

Ta x

Ye a r

Na me

Re ve nue

Expe ns e

Table A-9

Cathay Bank’s Abridged Income Statement

Unit: Million NTD

Tota l

Inte re s t

Income

S e rvice

Income

Ga in of

Fina ncia l

As s e t

a nd

Lia bilitie s

Othe rs

Tota l

Inte re s t

Expe ns e

S e rvice

Expe ns e

Ga in of

Fina ncia l

As s e t

a nd

Lia bilitie s

P e rs onne

l

Expe ns e

Othe rs

2005

Ca tha y Ba nk

53,976

39,768

6,835

933

-

6,440

48,529

12,929

1,378

4,735

29,485

-335

5,11 2

2006

Ca tha y Ba nk

70,608

40,867

5,694

7,536

16,511

77,030

17,009

1,168

8,276

4,516

46,061

58 7

-5,835

2007

Ca tha y Ba nk

79,251

40,285

6,434

28,874

3,658

71,125

19,121

1,302

29,333

6,485

14,885

-

8,126

Othe r

Ga ins or

Los e s

Income

Be fore

Income

Ta x

Ye a r

Na me

Re ve nue

Expe ns e

Table A-10

E. SUN Bank’s Abridged Income Statement

Unit: Million NTD

Tota l

Inte re s t

Income

S e rvice

Income

Ga in of

Fina ncia l

As s e t

a nd

Lia bilitie s

Othe rs

Tota l

Inte re s t

Expe ns e

S e rvice

Expe ns e

Ga in of

Fina ncia l

As s e t

a nd

Lia bilitie s

P e rs onne

l

Expe ns e

Othe rs

2005

E.S un Ba nk

21,105

17,497

2,491

436

-

681

17,285

6,878

630

2,607

7,169

1,022

4,841

2006

E.S un Ba nk

67,564

20,637

2,903

27,062

16,963

67,107

11,256

682

26,299

3,289

25,581

23

479

2007

E.S un Ba nk

50,275

22,123

3,993

22,969

1,191

46,937

13,146

740

22,436

3,441

7,174

-

3,339

Othe r

Ga ins or

Los e s

Income

Be fore

Income

Ta x

Ye a r

Na me

Re ve nue

Expe ns e

Table A-11

Mega Bank’s Abridged Income Statement

Unit: Million NTD

Tota l

Inte re s t

Income

S e rvice

Income

Ga in of

Fina ncia l

As s e t

a nd

Lia bilitie s

Othe rs

Tota l

Inte re s t

Expe ns e

S e rvice

Expe ns e

Ga in of

Fina ncia l

As s e t

a nd

Lia bilitie s

P e rs onne

l

Expe ns e

Othe rs

2005

Me ga Ba nk

15,795

11,879

2,357

1,014

-47

592

12,916

4,530

226

2,903

5,257

181

3,060

2006

Me ga Ba nk

81,053

57,029

6,095

5,010

12,919

66,235

37,284

835

782

9,235

18,099

715

15,533

2007

Me ga Ba nk

83,812

61,396

7,030

5,696

9,690

66,469

38,970

777

2,061

8,718

15,943

-

17,342

Othe r

Ga ins or

Los e s

Income

Be fore

Income

Ta x

Ye a r

Na me

Re ve nue

Expe ns e

Table A-12

Yuanta Bank’s Abridged Income Statement

Unit: Million NTD

Tota l

Inte re s t

Income

S e rvice

Income

Ga in of

Fina ncia l

As s e t

a nd

Lia bilitie s

Othe rs

Tota l

Inte re s t

Expe ns e

S e rvice

Expe ns e

Ga in of

Fina ncia l

As s e t

a nd

Lia bilitie s

P e rs onne

l

Expe ns e

Othe rs

2005

Yua nta Ba nk

11,784

9,969

1,764

-142

6

187

11,991

4,132

523

2,110

5,226

312

105

2006

Yua nta Ba nk

17,363

10,883

1,346

2,111

3,023

22,848

5,035

354

1,834

2,555

13,070

11

-5,4 74

2007

Yua nta Ba nk

20,401

11,140

1,404

5,491

2,366

22,845

5,522

350

5,670

2,789

8,512

-

-2,443

Othe r

Ga ins or

Los e s

Income

Be fore

Income

Ta x

Ye a r

Na me

Re ve nue

Expe ns e

Table A-13

Taishin Bank’s Abridged Income Statement

Unit: Million NTD

Tota l

Inte re s t

Income

S e rvice

Income

Ga in of

Fina ncia l

As s e t

a nd

Lia bilitie s

Othe rs

Tota l

Inte re s t

Expe ns e

S e rvice

Expe ns e

Ga in of

Fina ncia l

As s e t

a nd

Lia bilitie s

P e rs onne

l

Expe ns e

Othe rs

2005

Ta is hin Ba nk

62,343

48,279

9,232

1,146

741

2,946

49,952

11,687

5,127

7,229

25,910

751

13 ,142

2006

Ta is hin Ba nk

106,011

38,828

7,568

15,354

44,261

126,737

14,257

2,124

13,019

7,267

90,0 71

155

-20,571

2007

Ta is hin Ba nk

101,394

32,537

8,427

35,237

25,192

98,356

16,038

1,864

33,287

7,077

40,09 1

-

3,038

Othe r

Ga ins or

Los e s

Income

Be fore

Income

Ta x

Ye a r

Na me

Re ve nue

Expe ns e

Table A-14

Shin Kong Bank’s Abridged Income Statement

Unit: Million NTD

Tota l

Inte re s t

Income

S e rvice

Income

Ga in of

Fina ncia l

As s e t

a nd

Lia bilitie s

Othe rs

Tota l

Inte re s t

Expe ns e

S e rvice

Expe ns e

Ga in of

Fina ncia l

As s e t

a nd

Lia bilitie s

P e rs onne

l

Expe ns e

Othe rs

2005

S hin Kong Ba nk

15,491

12,846

2,077

16

-176

728

16,392

4,021

577

2,821

8,973

568

-333

2006

S hin Kong Ba nk

16,666

11,728

1,596

780

2,562

24,436

4,592

448

308

2,684

16,404

17

-7,754

2007

S hin Kong Ba nk

21,010

12,266

2,228

135

6,381

19,548

5,803

486

528

2,774

9,957

-

1 ,462

Othe r

Ga ins or

Los e s

Income

Be fore

Income

Ta x

Ye a r

Na me

Re ve nue

Expe ns e

Table A-15

SinoPac Bank’s Abridged Income Statement

Unit: Million NTD

Tota l

Inte re s t

Income

S e rvice

Income

Ga in of

Fina ncia l

As s e t

a nd

Lia bilitie s

Othe rs

Tota l

Inte re s t

Expe ns e

S e rvice

Expe ns e

Ga in of

Fina ncia l

As s e t

a nd

Lia bilitie s

P e rs onne

l

Expe ns e

Othe rs

2005

S inopa c Ba nk

18,826

15,855

2,026

1,045

95

-194

16,386

10,133

201

2,905

3,147

139

2,579

2006

S inopa c Ba nk

63,954

24,289

2,112

12,928

24,624

61,679

16,162

271

12,385

3,542

29,320

23 2

2,506

2007

S inopa c Ba nk

97,443

41,979

4,744

21,479

29,241

97,484

28,618

579

24,074

6,063

38,149

-

-41

Othe r

Ga ins or

Los e s

Income

Be fore

Income

Ta x

Ye a r

Na me

Re ve nue

Expe ns e

Table A-16

Chinatrust Bank’s Abridged Income Statement

Unit: Million NTD

Tota l

Inte re s t

Income

S e rvice

Income

Ga in of

Fina ncia l

As s e t

a nd

Lia bilitie s

Othe rs

Tota l

Inte re s t

Expe ns e

S e rvice

Expe ns e

Ga in of

Fina ncia l

As s e t

a nd

Lia bilitie s

P e rs onne

l

Expe ns e

Othe rs

2005

China Trus t Ba nk

80,472

53,545

18,620

2,326

-

5,981

62,847

17,292

536

12,459

32,561

-1,002

16,623

2006

China Trus t Ba nk

165,359

54,868

18,782

68,991

22,718

183,161

24,018

628

65,072

12,160

81,2 84

-39

-17,841

2007

China Trus t Ba nk

209,396

49,632

24,661

114,146

20,957

196,139

26,435

1,015

111,717

12,143

44,829

-

13,256

Othe r

Ga ins or

Los e s

Income

Be fore

Income

Ta x

Ye a r

Na me

Re ve nue

Expe ns e

Table A-17

First Bank’s Abridged Income Statement

Unit: Million NTD

Tota l

Inte re s t

Income

S e rvice

Income

Ga in of

Fina ncia l

As s e t

a nd

Lia bilitie s

Othe rs

Tota l

Inte re s t

Expe ns e

S e rvice

Expe ns e

Ga in of

Fina ncia l

As s e t

a nd

Lia bilitie s

P e rs onne

l

Expe ns e

Othe rs

2005

Firs t Comme rica l Ba nk

53,174

40,924

4,712

68

150

7,319

40,197

20,928

953

8,781

9,535

664

13,640

2006

Firs t Comme rica l Ba nk

70,721

46,962

5,569

10,851

7,340

57,016

26,349

1,074

9,560

8,693

11,340

56 3

14,269

2007

Firs t Comme rica l Ba nk

94,992

52,839

7,960

18,832

15,361

79,140

30,783

1,076

17,004

8,888

21,389

-

15,851

Othe r

Ga ins or

Los e s

Income

Be fore

Income

Ta x

Ye a r

Na me

Re ve nue

Expe ns e

Table A-18

Jih Sun Bank’s Abridged Income Statement

Unit: Million NTD

Tota l

Inte re s t

Income

S e rvice

Income

Ga in of

Fina ncia l

As s e t

a nd

Lia bilitie s

Othe rs

Tota l

Inte re s t

Expe ns e

S e rvice

Expe ns e

Ga in of

Fina ncia l

As s e t

a nd

Lia bilitie s

P e rs onne

l

Expe ns e

Othe rs

2005

J ih S un Ba nk

13,933

11,854

1,717

156

44

162

19,575

3,959

1,285

2,314

12,017

51

-5,590

2006

J ih S un Ba nk

22,529

10,777

1,411

2,318

8,022

36,940

4,343

1,241

2,573

1,980

26,803

63

-1 4,348

2007

J ih S un Ba nk

18,289

8,718

1,894

817

6,859

21,393

4,171

768

1,018

1,775

13,661

-

-3,104

Othe r

Ga ins or

Los e s

Income

Be fore

Income

Ta x

Ye a r

Na me

Re ve nue

Expe ns e