NRG WORKING PAPER SERIES

THEORETICAL REVIEW AND FRAMEWORK

THE ROLES OF CONTROLLERS

Hans ten Rouwelaar

April 2007 no. 07-02

Nyenrode Research GroupNRG WORKING PAPER SERIES

Theoretical Review and Framework:

the Roles of Controllers

Hans ten Rouwelaar

April 2007

NRG WORKING PAPER NO. 07-02

NRG

The Nyenrode Research Group (NRG) is a research institute consisting of researchers from Nyenrode Business Universiteit and Hogeschool INHOLLAND, within the domain of Management and Business Administration.

Straatweg 25, 3621 BG Breukelen P.O. Box 130, 3620 AC Breukelen The Netherlands

Tel: +31 (0) 346 - 291 696 Fax: +31 (0) 346 - 291 250 E-mail: [email protected]

NRG working papers can be downloaded at

Abstract

In the last decades, the position of the business unit controller has grown in importance. This study gives a review of the research behind the two roles, which business unit-controllers can fulfill in business life: the support role and the control role. The support role is associated with involvedness of controllers by supporting managerial decision-making in the business unit; the control role focuses on providing reliable and timely financial accounting information for the corporate level and insuring that the financial function complies with relevant regulations. This paper contributes to the Management Accounting literature by documenting the available literature regarding the roles of controllers and by developing a theoretical framework to study the controller involvement in management. Based upon this framework twelve propositions and a regression model are presented, which can be used in future studies to test empirically which factors influence the controller involvement in management.

Please do not quote or distribute without permission of the author

Keywords

Contingency theory, Role theory, business unit controllers, support role, and control role

Address for correspondence Drs J.A. ten Rouwelaar

Nyenrode Business Universiteit

Straatweg 25, 3621 BG Breukelen, The Netherlands E-mail: [email protected]

Phone: (+31) 346 – 291443

This paper has benefited from helpful comments from Jan Bots on earlier drafts of this paper. The first presentation of this paper is planned in April 2007 at the 30th EAA seminar in Lisbon, Portugal. I would like to acknowledge the financial support of the Nyenrode Research Group (NRG) of the Nyenrode Business Universiteit.

1 Introduction

Accounting information is designed to serve as the basis for many important decisions both within and outside an organization. Management Accountants or Controllers1 are the

professionals who are responsible for the financial reports and the management accounting control system within an organization (control role). But beside this role the controllers also provide information to their managers. They assist their managers in planning, coordinating and controlling complex and interrelated activities, and in motivating people at all levels in the organization (Swagerman 2003). According to Sathe (1982), the basic tension in the function of the controller is between involvement (support role) and independence (control role). Controller involvement is the degree to which controllers actually perform various roles as participants in operating and strategic business decisions, that is, role of presenting information and analysis, recommending action, and challenging plans and actions of operating executives (Sathe 1982, page 10).

In the past there have been several publications about what the roles of the controllers should be. The most popular subject of these publications is the change of the controller’s role from ‘bean counter’ to ‘business partner’ (e.g. Kaplan 1995; Lyne & Friedman 1996; Cooper 1996a and 1996b; Friedman & Lyne 1997; Van Helden 1997, 1998, and 1999; Siegel et al. 1997; Meer-Kooistra 1999; Smith & Briggs 1999; Siegel & Sorensen 1999; Williams 2000; Siegel 2000; Colton 2001; Strikwerda 2002; Riedijk et al. 2002; Siegel et al. 2003a and 2003b; Kroon & Van der Steen 2005; Yazdifar & Tsamenyi 2005; Conijn et al. 2005, Kroon et al. 2005; Maas 2005; Perik 2006; De Waal 2003, 2004, 2005 and 2006; and Vaivio & Kokko working paper 2006). Another stream of publications uses the degree of controller involvement in management as an independent variable to test the effects on innovativeness (Emsley 2005) or performance measurement system gaming (Maas 2006). However, Roozen and Steens (2006) conclude “after the research of Vijay Sathe into the controller involvement in 1982, no rigorous research into the controller’s profession was executed” (Roozen & Steens 2006, page 6). Scientific, empirical studies, which actually measure and try to explain the variations of controller involvement in management or the two roles of the business unit (BU)-controllers by testing hypotheses empirically with

1 In this paper, I use the term ‘controllers’ to identify management accountants, financial managers, and

several organizational characteristics, are not available, except for one recently published paper of Zoni and Merchant in 2007, based upon a small sample of 17 large Italian industrial firms (Zoni & Merchant 2007).

Three categories of factors are relevant in understanding and explaining variation in the degree of controller involvement (Sathe 1982): The first category of factors relates to the controller’s motivation, personality, and interpersonal relationships with management (personal characteristics); The second category of factors relates to management’s expectations, orientation, and operating philosophy (manager’s characteristics); Finally, the third category of factors relates to the characteristics of the company’s environment and business (Roozen & Steens 2006, page 24). The basic research question Sathe asked himself was: Quite apart from the influence of the controller’s motivation, personality, and the quality of his or her interpersonal relationships with management, what is the influence of the company’s environment and business and of management’s expectations, orientation, and operating philosophy, on the degree of controller involvement? (Sathe 1982, page 45). This research question is still relevant today. The purpose of this paper is to contribute to the Management Accounting literature by documenting these three categories and to develop a theoretical framework to study controller involvement in management. This total research framework exists of two sides: the demand side (the factors which influence the management’s demands of controller involvement) and the supply side (the factors which influence the controller’s actual supply of controller involvement), and is based upon existing theories, available in management accounting literature: A Psychological theory for the personal characteristics; the Role theory for the connection between the manager’s demands or expectations, and the controller’s supply of information; and the Contingency theory for the third category of factors regarding the company’s environment and business. Future research can be based upon this theoretical research framework.

The remainder of this paper is structured as follows: Section 2 provides an overview of the available studies and frameworks in literature: after an introduction of the different roles of controllers, the frameworks of Sathe (1982) will be discussed followed by the framework of Roozen and Steens (2006). Based upon these frameworks a new, total framework is developed, which is based upon existing theories, like the Contingency theory and the Role theory. In section 3 twelve propositions are presented, which can be used to test which factors influence the controller involvement in management in future studies. In Section 4,

I conclude with discussions, some limitations, and provide areas for future research to explore.

2

Literature review and development Framework

2.1 The roles of the controller

There are several definitions of a controller in the management accounting literature. A widely used definition is:

Controller is the person in charge of both management accounting and financial accounting in an organization; usually the chief accountant. Also called comptroller. (Zimmerman 2005, page 784). Another definition, more linked to the controller’s tasks, is: Controller (or comptroller): The top managerial and financial accountant in an organization. Supervises the accounting department and assists management at all levels in interpreting and using managerial accounting information. (Hilton 2002, page 836).

Besides the more general definitions of controllers, there is a difference between corporate controllers working at headquarters, divisional or business unit controllers assisting their business unit managers, and controllers working within the controller-departments. In this paper the business unit-controllers are paramount, these are controllers in senior positions who are responsible for the financial control function on divisions or business unit levels, typically operating between headquarters and operating company level and therefore balancing strategic, operating, and financial aspects or control (Roozen & Steens 2006, page 24).

A controller is the crucial person within an organization. The controller plays key roles in line management and in the design and operation of a management control system (Merchant & Van der Stede 2003, page 493). Managers will increasingly need controllers that can obtain information from disparate sources and analyse it in useful ways (Borthick 1996). Controllers are the financial measurement experts within their firm or business unit and are key members of management teams. As a member of the management team, they can influence the decisions taken by the managers (act before the fact). In addition to the controller’s role of contribution in business decisions, the controller is responsible for the accuracy of financial reporting and for the integrity of internal control (after the fact reporting). Heckert and Willson described the controller as follows: “The controller is not the commander of the ship – that is the task of the chief executive – but he may be likened to the navigator, the

one who keeps the charts. He must keep the commander informed as to how far he has come, where he is, what speed he is making, resistance encountered, variations from the course, dangerous reefs which lie ahead, and where the charts indicate he should go next in order to reach the port in safety”. (Heckert & Willson 1952, page 4; Sathe 1982, page 6).

Traditionally, the controller, or management accountant, was tolerated as a necessary evil, viewed as a “bean counter” or a “corporate cop”. Nowadays, the controller is welcomed into the halls of management as a “business partner”, sought after for business acumen and the strategic perspectives this professional brings to the table. From the late 1980s, both the professional and academic literatures started to examine how these roles have been changing (e.g. Kaplan 1995; Lyne & Friedman 1996; Cooper 1996a and 1996b; Friedman & Lyne 1997; Van Helden 1997, 1998, and 1999; Siegel et al. 1997; Meer-Kooistra 1999; Smith & Briggs 1999; Siegel & Sorensen 1999; Williams 2000; Siegel 2000; Colton 2001; Strikwerda 2002; Riedijk et al. 2002; Siegel et al. 2003a and 2003b; Kroon & Van der Steen 2005; Yazdifar & Tsamenyi 2005; Conijn et al. 2005, Kroon et al. 2005; Maas 2005; Perik 2006; De Waal 2003, 2004, 2005 and 2006; and Vaivio & Kokko working paper 2006). Changes triggered by a new competitive environment have created enormous new opportunities for controllers. This new competitive environment demands much more accurate cost and performance information on the organization’s activities, processes, products, services, and customers (Kaplan 1995). Linhardt and Sundqvist agree with these dynamic changes: “Controllership has undergone dynamic changes in recent years. Changes in reporting requirements, personal liabilities, long-term impact of capital expenditures, and sources of funding are redefining the role of the Controller. Controllers are being called upon to become proactive team players and active corporate decision-makers (University of Minosota)”, (Linhardt & Sundqvist 2004, page 9). One of the authors, who has frequently published about the roles of the controller, is Vijay Sathe. He considers two broad questions. The first question is: Why is it that in some companies the controllers are involved more actively in business decision-making process than in others? The second question concerns the consequences of controller involvement for company performance. This issue contains questions like: Does active controller involvement help improve the company’s financial performance? Does active controller involvement compromise controller independence? Does involvement stifle management creativity and initiative? These are important practical questions, but they are extremely difficult to investigate because a multitude of factors affects a company’s performance

(Sathe 1982, page 2). These two broad questions are still relevant today. In this paper I focus at the first question, because the second question about the consequences of controller involvement in management upon the company’s performance, cannot be approached in the direct fashion. Out of the whole mass of factors that determine the performance (profitability) of a business enterprise, the controller involvement in management is only one factor (Simon et al. 1954, page vi). To investigate some other consequences of controller involvement recent publications use the degree of controller involvement in management as an independent variable to test the effects of controller involvement on innovativeness (Emsley 2005) or performance measurement system gaming (Maas 2006).

To answer these questions Sathe (1983) defined four ideal types of controllers: If primary emphasis is placed on the controller’s management-service responsibility, the desired behaviour for the controller is to be actively involved in the business decision-making process (the involved controller). If primary emphasis is placed on the controller’s financial reporting and internal control responsibilities, the desired behaviour for the controller is to retain objectivity and independence in dealing with affiliated management (the independent controller). The potential benefit is a greater assurance of financial reporting and the integrity of internal control. There are two ways, according to Sathe, of underscoring both controller’s financial reporting and his management-service responsibilities. The first is to split the controller’s role and assign each major responsibility to a different individual (the split controller), the other way is to retain both major responsibilities in one individual, but to place a strong emphasis on both (the strong controller) (Sathe 1983). But can strong controllers who are highly involved as part of the management team maintain the requisite degree of independence to fulfil their fiduciary and management oversight responsibilities effectively? In other words can controllers wear two hats - one as a member of the management team and confidant, and the other as a watchdog or police officer? Many people believe that the control and report responsibilities often conflict with the controller’s management-service responsibilities (Sathe 1982; Matĕjka 2002; Strikwerda 2002). As one chief financial officer pointed out:

“If the controller becomes too involved in operating decisions, he loses his integrity and independence when offering the financial implications of operating decisions, that is, it is not clear to others if he is biasing the financial analysis to fit the operating position advocated by him. I don’t want controllers to be business

managers because of the trade-off [losing financial integrity versus contributing by involvement]”. (Sathe 1982, page 25).

A controller always has dual responsibilities and provides information both to the BU-management and top BU-management (Sathe 1978a and 1987b; Matĕjka 2002; and Maas 2006). The BU-controller’s functional responsibility is to ensure that top management knows the ‘true’ financial state of the business unit. This includes regular reporting but also maintaining an informal communication line with the functional superior (dotted line). As a part of the local responsibility, the BU-controller is in charge of local accounting systems and provides reports relevant for decision-making by BU-managers. Sometimes organizations place BU-controllers under supervision of the corporate controlling department (solid line), which emphasis the controller’s independency (San Miguel & Govindarajan 1984; Merchant & Van der Stede 2003, page 496). The BU-controller is in danger of being viewed as an “outsider”, if not a “corporate spy”, by BU-management, and the BU-controller may be denied access to sensitive information or is informed after the relevant decisions and actions have already been taken (Sathe 1983; Anthony & Govindarajan 2006, page 112). Recent research shows that organizational slack (measured by achievability of business unit manager’s performance targets) is higher in settings where business unit controllers focus relatively more on providing decision-making information to business unit managers than on providing information for corporate control (Indjejikian & Matĕjka 2006).

Most researchers use two different roles for controllers, but they use different names: One role is the management-service role (support role, or business advocate role), which involves helping managers with their decision-making and control functions. The other role is the oversight-role, which involves ensuring that the actions of everyone within the organization, (specially those of the managers) are legal, ethical, and in the best interests of the organization and its owners (Merchant & Van der Stede 2003, page 493 or Hopper 1980, page 402). In American research there is a distinction between: Corporate Policeman (control role), and Business Advocate (support role) (Jablonski et al. 1993; Van Helden 1999, page 22). The Corporate policeman profile is built upon three core values: oversight and surveillance; administration of rules and regulations; and impersonal procedures. The Business Advocate profile is built upon three contrasting core values: service and involvement; knowledge of business; and internal customer service. (Jablonski et al. 1993).

Verstegen et al. (2005) have distinguished two groups of controllers that perform roughly similar activities in practice: the ‘transformers’, who transform internal and external reports, and the ‘watchmen’, who score high on prevailing activities that relate to accounting information system and risk management.

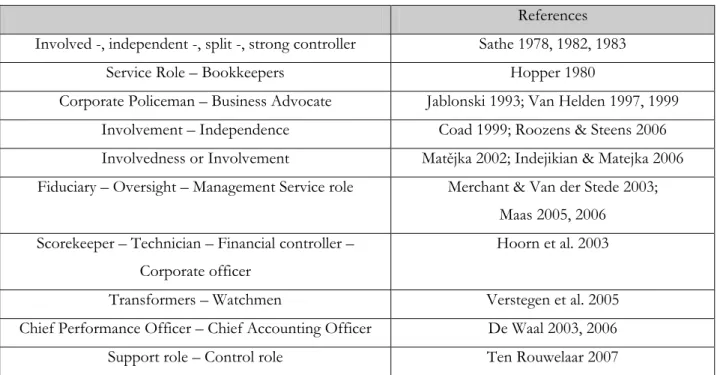

An overview of the classifications of the different roles of controllers is given in table 1: ---

INSERT TABLE 1 ABOUT HERE ---

In this paper I also distinguish two roles of the controller: the support- and the control role. The main reason for this choice, besides the connection to prior management accounting literature, is the ambiguity of the two extreme points of the spectrum. This dilemma between the responsibilities for assisting (support) and monitoring (control) has relevance beyond the controller’s role. There are other staff positions in which these two responsibilities of support and control are both increasingly important. One the one hand, because of the increase of the organizational size and complexity, management relies more than ever on specialist advice and expertise. Active staff involvement increases the likelihood that the appropriate specialized knowledge and judgment will be brought to bear when business decisions are made. On the other hand, as the modern corporation experiences mounting external pressures from litigation and regulation, the importance of staff independence for positions such as personnel and quality assurance is also increasing (Sathe 1982, page 3). There is a lot of speculation about the question if one person is capable to fulfil these two controller’s roles at the same time. (Hopper 1980; McGree et al. 1989; McGregor et al. 1989; Sathe 1982, page xvii; San Miguel & Govindarajan 1984; Siegel 2000; Merchant & Van der Stede 2003, page 494; Anthony & Govindarajan 2006, page 112; and Zimmerman 2005, page 15). There are also authors, who claim that on must split up the roles into two persons: the Chief Performance Officer (CPO) for the support role (strategic analysis, improving performances) and the Chief Accounting Officer (CAO) for the control role (insuring integrity, transparency and governance) (Sathe 1982; De Waal 2006, page 66).

2.2. Frameworks of Sathe

Much has changed since Vijay Sathe wrote his book Controller involvement in management

(1982), but his theoretical frameworks to study controller involvement are still relevant today. Three categories of factors are relevant in understanding and explaining variation in the degree of controller involvement (Sathe 1982): The first category of factors relates to the controller’s motivation, personality, and interpersonal relationships with management; The second set of factors relates to management’s expectations, orientation, and operating philosophy; Finally, the third category of factors relates to the characteristics of the company’s environment and business (see figure 1, Sathe 1982, page 46).

--- INSERT FIGURE 1 ABOUT HERE ---

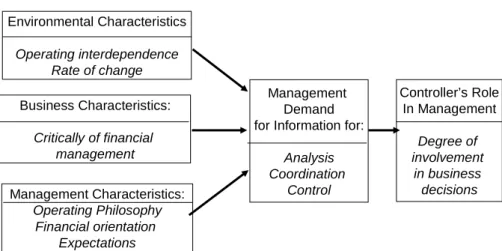

In his book Sathe focused only upon the last two categories of factors, because these are not related to the controller as a person, but rather to the controller’s position. Another way to state the distinction is, that were the controller to be replaced, the factors in category 1 would most likely change but those in categories 2 and 3 would not (Sathe 1982, page 45). The third category of factors, which relates to the company’s environment and business, effects management’s demand for information and also effects controller involvement (see figure 2, Sathe 1982, page 53). With figure 2 Sathe introduces the basic conceptual framework and briefly outlines how the major concepts drawn from prior research and other variables in three major areas – the company’s environment, business and management – are relevant for his study. First, in an environment characterized by rapidly changing products and markets, management is for instance likely to place great emphasis on quick decision-making, requiring the controller to provide timely information and analysis as rapidly as needed. Such a role for the controller, calling for increased involvement in decision-making, may be far less important for a company in a more stable market environment. Another characteristic of the company’s environment that may influence on the controller involvement is its operating independence. If the manager has greater responsibilities, the manager will have greater needs for coordination and information. Since the controller may be involved in these management’s tasks the controller’s role may be influenced by the company’s operating independence. Second, a characteristic of the company’s business that could have an important influence on

controller involvement is the extent to which sound financial management is critical to business success. In an era of continuing inflation and capital shortages, most companies recognize the importance of good financial management. In companies for which financial management is more critical to success, the controller may play a more active role in business decision-making. Finally, management’s operating philosophy, orientation and expectations may have an important influence on controller involvement. To the extent that the manager is financially orientated (seeks financial information in running the business) the opportunity for controller involvement increases.

--- INSERT FIGURE 2 ABOUT HERE ---

Besides the more general framework that is presented in figure 2, Sathe (1982) also developed hypotheses dealing with the influence of many different contextual factors of (1) the inter-company’s environment and business characteristics, (2) the corporate management characteristics, and (3) the corporate controller characteristics on (A) the degree of corporate controller involvement at Headquarters, and (B) the degree of typical division (business unit) controller involvement in the company. Corporate managements differ in their financial background, financial orientation, expectations regarding BU-controller involvement operating style, and management philosophy. Sathe presented a summary on how various environmental, business-, corporate management-, and corporate controller characteristics influence the degree of typical controller involvement (see figure 3, Sathe 1982, page 110). First, working asset intensity has a strong association with management expectations regarding BU-controller involvement. If corporate management is highly financially oriented, this may lead to a greater degree of involvement for the BU-controller. Second, the expectations of corporate management could be important because of their hierarchical position and opportunity to “set the tone” of the organization. The greater the corporate management emphasis on the company’s financial planning, budgeting, and capital expenditure review system, the greater the degree of BU-controller involvement. The traditional distinction between “line” and “staff” is emphasized along traditional lines: the “line” is responsible for results, the “staff” for advice and services. In case of strong line transfers, the distinction between line and staff blurs, and greater controller involvement in decision-making is likely to occur under these conditions. Finally,

the greater the corporate controller’s emphasis on the service role in dealing with management or the emphasis the human resource development of controllership personnel within the company, the greater the degree of typical BU-controller involvement.

--- INSERT FIGURE 3 ABOUT HERE ---

Sathe (1982) reviewed the findings related to prior research and developed a new theoretical framework, in which it is possible to link situational variables to role behavior (see figure 4, Sathe 1982, page 119). According to this framework, situational factors not only influence role behavior indirectly via role sender expectations, as assumed in Role theory (arrow 2), but also directly by generating a demand for role behavior (arrow 3) just as role sender expectations do (arrow 4). What these variables have in common – the reason for their influencing behavior of the focal role – is the varying degrees of demand for controller involvement that they generate. The rationale was explained when formulating the hypotheses. The role sender’s expectations may also be seen as influencing role behavior in this manner: the higher the role sender’s expectations concerning a particular aspect of role behavior, the greater the demand for it. The translation of the demand behavior into actual behavior is moderated by attributes of the person in the focal role and interpersonal factors, as in Role theory (arrow 5).

--- INSERT FIGURE 4 ABOUT HERE ---

Sathe concluded in 1982: ”The question of how and why situational factors are related to role sender expectations has not received much research attention and their independent and joint effects on role behavior have not been explored. Although these questions could not be addressed more adequately here using multivariate techniques, the findings indicate that this is a rich arena for future research” (Sathe 1982, page 119).

2.3. Framework of Roozen & Steens

Based upon the frameworks of Sathe (1982), Roozen and Steens (2006) have developed their research framework to study controller effectiveness (see figure 5, Roozen & Steens, 2006, page 28). The degree of actual controller involvement (support role) and the degree of actual controller independence (control role) are effected by “expectations and attributes of controller” and “interpersonal factors” (arrow D1 and D2). Both affect the degree of controller effectiveness (arrow C1 and C2). Besides this part of the research framework, Roozen and Steens also paid attention to two items, which effect the degree of importance of controller involvement, and two items, which effect the degree of controller independence. The two items related to controller involvement are: (1) criticality of controller contribution in light of business and environmental conditions, and (2) the managers’ expertise in the area of controller contribution. The first item has a positive relationship, the second item a negative relationship with the degree of importance of controller involvement. The degree of importance of controller independence is related to the following two items: positively related to (A) the extend of external pressure in area of controller activity e.g. from litigation and regulation, and negatively related to (B) the extend in which executives at higher levels have confidence in the integrity and good judgment of managers at lower levels.

--- INSERT FIGURE 5 ABOUT HERE ---

Testing the hypothesis is not part of their research project but is recommended as a result of their findings (Roozen & Steens 2006, page 29). Their study involved six short case studies, and the findings and the discussion thereof support the relevance of further exploring and testing their hypotheses about more demanding the governance regime in relation with the senior controller involvement and independence in management.

2.4. Total framework

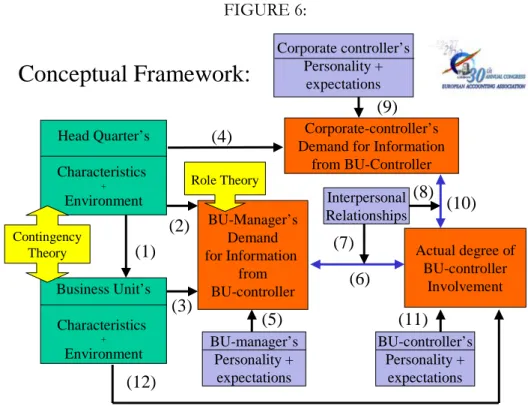

The framework of Roozen and Steens (2006) is relatively simple. The four items in their model are not the only factors explaining the degree of importance of controller involvement versus independence or influencing the controller effectiveness. In the total framework (see figure 6) the three categories of Sathe (1982) are presented, and three

persons are identified who are affecting the degree of controller involvement in management: the corporate controller, the BU-manager, and the BU-controller. Psychology theory indicates that each person has his/her own personality and expectations. The first category, the personal characteristics influence the demands for information, the supply of information, and the actual degree of involvement in management (arrows 5, 9, and 11). The second category, the management’s expectations

influence the demand for information by the BU-manager (arrow 5). The third category, the company’s environment and business, is also presented in the framework by the headquarters- and business unit characteristics. The relationships between the demand of the BU-manager (arrow 6), and also the demand of the corporate controller (arrow 10) with the actual degree of involvement in management are influenced by the interpersonal relationships between the two demanding persons and the BU-controller (arrows 7 and 8). ---

INSERT FIGURE 6 ABOUT HERE ---

The Contingency theory approach advocates that there is no one ‘best’ design for a management accounting information system, but that ‘it all depends’ upon the situational factors (Drury 2004, page 696). Headquarters and business units respond upon the business environment and settle their Management Accounting System. Headquarters delegate adequate responsibilities to the BU-managers (arrow 1). Based upon these responsibilities, and the corporate characteristics, the BU-managers set their demand for information from their BU-controllers (arrow 2), and adjust their demand for information to their own business unit characteristics (arrow 3). This demand for information is sent to the BU-controller (arrow 6). As the literature on Role theory indicates, “role” is a useful tool for the examination of the position of the controller as it links three central concepts: role expectations (what the BU-manager and the BU-controller believe he should do); role behaviour (what he actually does) and how his position is linked to others, thus shaping his “role set” (Gross et al. 1958). Shaping his role set, is answering the question: Why do BU-controllers behave in a certain way? Role theorists may say that they share expectations for their own behaviour and that of others (Biddle 1972, page 115). Thus BU-controllers “expect” that BU-managers want to have a bonus and they “expect” that the corporate controllers want to receive the proper information of the business unit performance. There

could be a gap or differences between the demand for information by the BU-manager and the supply of information by the BU-controller. This gap can be explained by the differences between the sender and receiver, by Role theory, the interpersonal relationships (arrows 7 and 8), and the differences between BU-manager’s - and BU-controller’s personality and expectations (Kahn et al. 1964).

Headquarters also delegate responsibilities to their corporate controller (arrow 4), who will ask his/her BU-controllers for information (arrow 10). The relationship among the corporate controllers and the BU-controllers is different than the relationships between the BU-managers and their BU-controllers. In practice the corporate controllers demand reports and control responsibilities from their BU-controllers.

The total framework is completed with the demand-side: the factors, which influence the management’s demand of controller involvement, and the supply-side: the factors, which influence the controller’s supply of controller involvement. The Contingency factors, which influence the demand-side, are related to: the corporate management -, environmental -, business -, corporate controller characteristics, and manager’s expectations & expertise. Examples of these contingency factors can be filled into each characteristic: (1) corporate management characteristics (e.g., corporate culture, decentralization, interdependencies among business units, corporate financial distress, and information asymmetry); (2) environmental and business characteristics (e.g., perceived environmental uncertainty, business unit’s culture, interdependencies among business units, and task uncertainty); (3) manager’s characteristics (e.g., leadership style, working experience, and financial knowledge); (4) Corporate controller characteristics (e.g., corporate strategy, the degree of decentralization, information asymmetry, the quantity of legislations and regulations, the degree of corporate financial distress). The factors, which have influence on the characteristics, are summarized in figure 7.

--- INSERT FIGURE 7 ABOUT HERE ---

The factors, which influence the supply-side, are related to the personal characteristics of the BU-controller (like e.g. the personal expectations, attributes and skills of the BU-controller

(arrow 11), the interpersonal relationship between the BU-controller and the manager (arrow 7), and the interpersonal relationship between the BU-controller and the corporate controller (arrow 8)). Besides on personal characteristics, the supply of the BU-controller involvement in management also depends on the BU-controller’s own interpretation of the business unit’s characteristics (arrow 12).

The fit between the demand-side and the supply-side could also influence the controller effectiveness. The better the controller is able to fulfill the demands of the manager for information for analysis, coordination and control, the more the decision-making of the manager will improve, so the supply of the information by the controller is important for the controller effectiveness. If a controller is able to supply what is being asked for, the effectiveness of the information will improve. Sathe (1983) characterized this kind of controller as a “strong controller”.

3 Proposition

development

3.1. Introduction

Because each organization is unique, the potential range of situations or contingent factors is enormous, thus it is nearly impossible to study each one separately. There is a lot of literature based upon the Contingency theory (Otley 1980; Drury 2004). I use the Contingency theory approach to select several Contingency factors for the analysis of the BU-controller involvement in management, because in 1980 Hopper already stated that: “accounting systems may be contingent upon organizational circumstances and that it is a short step from such work to suggest that the role of the accountant is similarly contingent”. (Hopper 1980, page 401). Developing a framework is not enough to test what kinds of factors influence the degree of controller involvement in management. To develop testable propositions several factors behind the model have to be identified, which can be measured by constructs. These constructs are related to management accounting literature and the relationships among these can be tested empirically. In the next section I will introduce twelve propositions, which can be used in future studies to test empirically which of these factors influence controller involvement in management. The next section concludes with an empirical model, which can be used to test these propositions.

3.2 Propositions

Based upon the conceptual framework and the factors, which probably influence the degree of controller involvement in management, the following propositions are presented:

A. Propositions based upon the personal characteristics: controller’s motivation, personality and interrelationship with management:

1. BU-controllers with high scores on Extraversion (extravert), Originality (explorer), or Accommodation (adapter) are positively related to the degree of business unit controller involvement in management.

2. BU-controllers with low scores on Neuroticism (resilient), or high scores on Consolidation (focused) are negatively related to the degree of business unit controller involvement in management.

3. A strong interpersonal relationship between the controller and the BU-manager is positively related to the degree of business unit controller involvement in management.

B. Propositions based upon the business unit manager characteristics: Management expectations, orientation, and operating philosophy:

1. Perceived environmental uncertainty of the business unit manager is positively related to the degree of business unit controller involvement in management. 2. Market -, and Clan Culture of the business unit are positively related to the degree

of business unit controller involvement in management.

3. Interdependencies among business units are negatively related to the degree of business unit controller involvement in management.

4. Task uncertainty of business unit managers is positively related to the degree of business unit controller involvement in management.

C. Propositions based upon the company’s environment and business characteristics: 1. In case of prospector strategy, the degree of business unit controller involvement

in management will be higher than within business units with a defender strategy.

2. Decentralization is positively related to the degree of business unit controller

involvement in management.

3. Information asymmetry between HQ and business units is positively related to

the degree of business unit controller involvement in management.

4. In case of many rules and regulations regarding the reporting activities of the

business units, the degree of business unit controller involvement in management will be less.

5. In times of financial distress within the organization or business units, the degree

of business unit controller involvement in management will be less.

3.3 Regression model

Empirical testing of the propositions derived earlier involved assessing the impact of the contingency factors on the controller involvement in management. To estimate the impact of the contextual factors, the following empirical model of three equations is defined:

AI = f (DM, DC, N, E, O, A, C, INTERREL) + i ε i

DM = g (AI, DC, PEU, CULTURE, IMPATHEM, IMPAYOU, TASKUNC) + i ν i DC = h (AI, DM, STRATEGY, DECENTR, CORPCNTR, RULES, STRESS) + i μi

Where:

The dependent variables of this regression model are:

AI = i Actual Involvement of BU-controller of organization i. DM = i Demand for information by the BU-manager of organization i.

DC = i Demand for information by the Corporate Controller of organization i.

The Independent variables in the three linear functions f, g, and h are: Personal Characteristics:

N = i the degree in which the BU-controller is concerned or attentive. E = i the degree in which the BU-controller is extrovert or social involved.

= the degree in which the BU-controller is open to new experiences. O i

A = i the degree in which the BU-controller is agreeable or tolerant. C = i the degree in which the BU-controller is conscience or disciplined.

= the personal interrelationships of the BU-controller. INTERREL i

Business unit Characteristics, like e.g.:

CULTURE = i the type of culture of the business unit of organization i.

IMPATHEM = i the impact of the business unit on other business units of organization i. IMPAYOU = i the impact of other business units on the business unit of organization i. TASKUNC i = the degree of perceived task uncertainty of the BU-manager of

organization i.

Organizational Characteristics, like e.g.:

STRATEGY = i the type of corporate strategy of organization i.

DECENTR = Degree of decentralization of activities to the business unit of organization i.

i

CORPCNTR = Hierarchy Dummy of organization i. (i.e. 1 = corporate-controller is hierarchical principal of the BU-controller, 0 = other is hierarchical principal of the BU-controller)

RULES = i the degree of legislation and regulations within organization i. = the degree of financial distress within organization i.

STRESS i

ε, ν, μ = error terms.

This research model can be used in future studies to test empirically which factors influence controller involvement in management.

4

Discussion and Concluding Comments

4.1. Discussion

Combining all available theoretical frameworks, I come to the conclusion that modeling these frameworks into one total framework is possible to do. By dividing the model into a demand-side and a supply side, the model is fitting to Role theory. The demand side leads to the “demand for role behavior”, like in the theoretical framework of Sathe (figure 4), and is based upon BU-manager’s expectations and organizational characteristics (situational factors). These situational factors are based upon the Contingency theory. Each organization is unique, because the situational factors, with which the organizations have to deal, are different. Environmental uncertainties, competitive strategies and missions, have their impact upon the expectations of the management and the management’s demand for analysis, coordination and control. Different demands of BU-managers will lead to different degrees of their BU-controller involvement in management.

On the other hand, there is the supply side of the research model. The supply of analysis, coordination and control by the BU-controller depends upon the personal characteristics, skills, competences and attributes of the controller, the interpretation of the BU-controller of the manager’s needs for information, and the interpersonal factors between the BU-controller and his BU-manager.

4.2. Limitations

Organizations are complex systems. It is possible to describe different parts of organizations, using research models or frameworks to focus upon several aspects and relationships among these aspects. However, it is not possible to study all relationships at the same time due to multicolliniarity and other mathematical or econometric problems.

The parts of the research framework that is developed in this study, haven’t been empirically tested yet. Until now the research in this area was qualitative research, also known as “interpretative interactionism” (De Loo et al. 2006; Verstegen & De Loo 2007). Empirical evidence of the relationships among the variables of this model and the propositions presented in this paper is not yet available.

The twelve factors presented in the twelve propositions are probably not the only factors, which influence the controller involvement in management. Other factors can be developed and tested within this conceptual research framework.

The twelve propositions must be developed further into hypotheses. The associations mentioned in these twelve propositions already have a base in management accounting literature, but need more explanation for becoming soundly based.

4.3. Future research

By reviewing the available studies and by developing a total framework all different smaller frameworks are combined into one total framework, which is based upon existing theories. By splitting up the total framework into smaller pieces there will be manageable studies in future, without losing trace of the relationships within the total framework.

Based upon the twelve proposition presented in this paper, testable hypotheses must be developed, linked to management accounting literature and tested by instruments available within the management accounting literature.

In future research manageable parts of the total research model will be explored, which will lead to insight in the cohesion or correlation among the variables in the research model. The purpose of this paper is to give an impulse to the discussion on the roles controllers perform within companies. Controllers are staff officials whose raison d’être is formed by the need for and the quality of their services. The conceptual framework, which is introduced in this paper, is a starting point for answering the questions of how and why situational factors are related to role sender expectations (of BU-managers and corporate controllers) and how these factors influence the roles controllers fulfill in companies. Future research will prove if the framework is useful, and if the propositions in this paper

can be developed in testable hypotheses. This framework can serve as an instrument for this, more detailed research.

References

Anthony, R.N., & Govindarajan, V. (2006). Management Control Systems, twelfth edition, New York, McGraw-Hill Irwin (ISBN 007-125410-2), 768 pp.

Biddle, B.J. (1972). Role theory: Expectations, Identities, and Behaviors, New York, Academic Press, (ISBN 0-12-095950-X), 416 pp.

Borthick, A.F. (1996). Helping Accountants Learn to Get the Information Managers Want: The Role of the Accounting Information Systems Course, Journal of Information Systems, 10, no. 2, 75 – 85.

Coad, A.F. (1999). Some survey evidence on the learning and performance orientations of management accountants, Management Accounting Research, 10, 109 – 135.

Colton, S.D. (2001). The Changing Role of the Controller, Journal of Cost Management, 5 – 10.

Conijn, F., Everts, A., Koops, E. & Uiterlinden, R. (2005). Het speelveld van de CFO, omgaan met dilemma’s, ’s-Hertogenbosch, Tutein Nolthenius, (ISBN 90-72194-73-X), 212 pp.

Cooper, R. (1996a). Look out Management Accountants, part I, Management Accounting, 16, (May/June), 20 – 26.

Cooper, R. (1996b). Look out Management Accountants, part II, Management Accounting, 16, (May/June), 35 – 41.

De Loo, I., Nederhof, P. & Verstegen, B. (2006). Detecting Behavioural Patterns of Dutch Controller Graduates Through Interpretive Interactionism Principles, Qualitative Research in Accounting & Management, 3 (1), 46 – 66.

Drury, C. (2004). Management and Cost Accounting, 6th edition, London, Thomson Learning,

(ISBN 1-84480-028-8), 1280 pp.

Emsley, E. (2005). Restructuring the management accounting function: a note on the effect of role involvement on innovativeness, Management Accounting Research, 16 (2), 157 – 177.

Friedman, A..L. & Lyne, S.R. (1997). Activity-based techniques and the death of the bean counter, The European Accounting Review, 6 (1), 19 – 44.

Gross, N., Mason, W.S. & McEachern, A.W. (1958). Explorations in Role Analysis: Studies of the school superintendency role, New York, John Wiley & Sons, Inc., (ISBN 471-32802-2), 379 pp.

Heckert, J.B. & Willson, J.D. (1952). Controllership – The work of the Accounting Executive, New York, Roland Press, 645 pp.

Helden, G.J. van (1997). Management Accountinggoeroes over de toekomst van de controller, Tijdschrift Financieel Management, 17, 81 – 87.

Helden, G.J. van (1998). De Controller van de toekomst: over de kloof tussen droom en werkelijkheid, Tijdschrift Financieel Management, nov-dec 1998, 14 – 22.

Helden, G.J. van (1999). Veranderingen in de functie en de rol van de controller, Handboek Management Accounting, 1 – 19.

Hilton, R.W. (2002). Managerial Accounting: Creating Value in a Dynamic Business Environment, 5th edition, New York, McGraw-Hill Inc., (ISBN 007-112076-9), 858

pp.

Hoorn, H.P., Slagter, J. & Swagerman, D.M. (2003). Rollen en competenties: Portret van de Noord-Nederlandse Controller, Controllers Magazine, Dec, 16 – 18.

Hopper, T.M. (1980). Role Conflicts of Management Accountants and their Position within Organizational Structures, Accounting, Organizations and Society, 5, 401 – 411. Indejikian, R.J., & Matĕjka, M. (2006). Organizational Slack in Decentralized Firms: The

Role of Business Unit Controllers, The Accounting Review, 81, 849 – 872.

Jablonski, S.F., Keating, P.J., & Heian, HJ.B. (1993). Business advocate or corporate

policeman? Assessing Your Role as a Financial Executive, Morristown NJ, The

Financial Executives Research Foundation, (ISBN 0-910586-8-61), 40 pp.

Kahn, R.L., Wolfe, D.M., Quinn, R.P., Snoek, J.D & Rosenthal, R.A. (1964). Organizational Stress: studies in role conflict and ambiguity, New York, John Wiley & Sons Inc., (ISBN 0-89874-8-07), 470 pp.

Kaplan, R.S. (1995). New Roles for Management Accountants, Journal of Cost Management, 9 (4), 6 – 13.

Kroon, J. de, Mater, F, & Steen, E. van der (2005a). Directeur krijgt controller die hij verdient, Tijdschrift Controlling, 4, 10 – 16.

Kroon, J. de, & Steen, E.Th. van der, (2005b). Rasadministrateur wordt nooit Supercontroller, Tijdschrift Controlling, 8, 8 – 13.

Linhardt, M. & Sundqvist, S. (2004). The Role of the Controller, Master Thesis, Lulea University of Technology, 2004:187 SHU, 1 – 74.

Lyne, S.R. & Friedman, A.L. (1996). Activity-based techniques and the ‘new management accountant’, Management Accounting, 74 (7), 34 – 35.

Maas, V.S. (2005). De rol van de controller in Nederland, Maandblad voor Accountancy en Bedrijfseconomie, 5, 16 – 20.

Maas, V.S. (2006). The effect of Controller Involvement in Management on Performance Measurement System Gaming, Proefschrift Universiteit van Amsterdam (ISBN 90-0-21388-0), 161 pp.

Matjĕka, M. (2002). Management Accounting in Organizational Design: Three Essays,

Dissertation Tilburg Universiteit.

McGree, G.W., Ferguson, C.E. & Seers, A. (1989). Role conflict and role ambiguity: do the scales measure these two constructs?, Journal of Applied Psychology, 74 (5).

McGregor, C.C. Killough, L.N. & Brown, R.M. (1989). An investigation of organizational-professional conflict in management accounting, Journal of Accounting Research, 1, 104 – 118.

Meer-Kooistra, J. van der (1999). Ontwikkelingen in de controllersfunctie, Praktijkboek Financieel Management, 44, II.2, 1 – 20.

Merchant, K.A., & Van der Stede, W.A. (2003). Management Control Systems, Harlow, Pearson Education Limited, (ISBN 0-273-65596-5), 701 pp.

Otley, D.T. (1980). The contingency theory of management accounting: achievement and prognosis, Accounting, Organizations and Society, 15, 649 – 672.

Perik, K. (2006). Haal het beste uit je financieel manager, Pearson Education Benelux, (ISBN 90-430-1018-9), 104 pp.

Riedijk, F., Tillema, S., & Moen, E. (2002). De ontwikkeling van de Controller in Nederland, Maandblad voor Accountancy en Bedrijfseconomie, 337 – 347.

Roozen, F.A., & Steens, H.B.A. (2006). Reflections on the Future of Finance and Control, Kluwer, (ISBN 0-13-03884-0), 343 pp.

San Miguel, J.G. & Govindarajan, V. (1984). The contingent relationship between the controller and internal audit functions in large organizations, Accounting, Organizations and Society, 9 (2), 179 – 188.

Sathe, V. (1978a). Who should Control Division Controllers?, Harvard Business Review, 56, 99 – 104.

Sathe, V. (1978b). Controllership in Divisionalized Firms: Structure, Evaluation, and Development, AMACOM.

Sathe, V. (1982). Controller Involvement in Management, Prentice-Hall, (ISBN 0-13-171660-3), 189 pp.

Sathe, V. (1983). The Controller’s Role in Management, Organization Dynamics, 11, 31 – 48. Siegel, G., Kulesza, C.S. & Sørensen, J.E. (1997). Are You Ready for the New Accounting?,

Journal of Accountancy, August , 42 – 46.

Siegel, G & Sorensen, J.E. (1999). Counting more, counting less: transformations in the management accounting profession, The 1999 practice analysis of management accounting, Montvale NJ: Institute of Management Accountants, 26 pp.

Siegel G. (2000). Business Partner and Corporate Cop: Do the Roles Conflict?, Strategic Finance, 82 (3), 89 – 90.

Siegel, G., Sørensen, J.E. & Richtmeyer, S.B. (2003a). Are You a Business Partner? Part 1,

Strategic Finance, Sept, 39 – 43.

Siegel, G., Sørensen, J.E. & Richtmeyer, S.B. (2003b). Becoming a Business Partner, Part 2,

Strategic Finance, Oct, 1 – 5.

Simon, H.A., Guetskow, H., Kozmetsky, G., & Tyndall, G. (1954). Centralization versus decentralization in organizing the controller’s department, New York, The Controllership Foundation, reprint 1978, (ISBN 0-914348-24-8), 106 pp.

Smith, M. & Briggs, S. (1999). From Bean counter to Action Hero, Accounting & Tax Periodicals, 70 (1), 36 – 39.

Strikwerda, H. (2002). Kerncompetent of universele adviseur?, Controllers Magazine, 33 – 37. Swagerman, D.M. (2003). Op weg naar herstel van vertrouwen: Wat kan de controller daaraan

bijdragen?, Oratie, Groningen, Rijksuniversiteit Groningen, (ISBN 90-367-1959-3), 62 pp.

Vaivio, J. & Kokko, T. (working paper). Counting Big: Re-examining the Concept of the Bean Counter Controller, LTA, 2006, 1/06, 49 – 74.

Verstegen, B.H.J., De Loo, I., Mol, P., Slagter, K., & Geerkens, H. (2005). The Classification of Dutch Controller Graduated by Activities: Images of a Profession, (working paper February 2005), (ISSN 676351), 1 - 18.

Verstegen, B.H.J., & De Loo, I. (2007). Gedragspatronen van Nederlandse controllers: een analyse aan de hand van interpretatief interactionisme, Maandblad voor Accountancy en Bedrijfeconomie, 19 – 27.

Yazdifar, H. & Tsamenyi, M. (2005). Management accounting change and the changing roles of management accountants: a comparative analysis between dependent and independent organizations, Journal of Accounting & Organizational Change, 1 (2), 180 – 198.

Waal, A. de, (2003). Ontwikkelingen en trends in de financiële functie, Controlling in Praktijk reeks, no 58, Deventer, Kluwer, (ISBN 90-130-0005-3), 76 pp.

Waal, A. de (2004). Trends en ontwikkelingen in de financiële functie, Tijdschrift Controlling, nr. 1 / 2, 2004, 4 - 8.

Waal, A. de (2005). Trends en ontwikkelingen in de financiële functie, Tijdschrift Controlling, nr. 1 / 2, 2005, 34 - 39.

Waal, A. de (2006). De financiële manager van de 21ste eeuw, Controlling in Praktijk reeks, no 74, Deventer, Kluwer, (ISBN 90-13-03295-8), 92 pp.

Williams, K. (2000). Are controllers really becoming business partners?, Strategic Finance, 81 (11), 25 – 26.

Zimmerman, J.L. (2005). Accounting for Decision making and Control, fifth edition, McGraw-Hill Higher education (ISBN 0-07-297586-5), 800 pp.

Zoni, L., & Merchant, K.A. (2007). Controller involvement in management : an empirical study in large Italian corporations, Journal of Accounting & Organizational Change, 3 (1), 29 – 43.

FIGURE 1:

Factors Influencing Controller Involvement:

(3) Characteristics of the Company’s Environment and Business (2) Management’s Expectations, Orientation, and Operating Philosophy

(1) Controller’s Motivation, Personality, and Interpersonal Relationships with Management

Figure 1: Factors Influencing Controller Involvement, Sathe (1982), page 46

TABLE 1:

References Involved -, independent -, split -, strong controller Sathe 1978, 1982, 1983

Service Role – Bookkeepers Hopper 1980

Corporate Policeman – Business Advocate Jablonski 1993; Van Helden 1997, 1999 Involvement – Independence Coad 1999; Roozens & Steens 2006 Involvedness or Involvement Matějka 2002; Indejikian & Matejka 2006 Fiduciary – Oversight – Management Service role Merchant & Van der Stede 2003;

Maas 2005, 2006 Scorekeeper – Technician – Financial controller – Hoorn et al. 2003

Corporate officer

Transformers – Watchmen Verstegen et al. 2005 Chief Performance Officer – Chief Accounting Officer De Waal 2003, 2006

Support role – Control role Ten Rouwelaar 2007

FIGURE 2: Environmental Characteristics Operating interdependence Rate of change Business Characteristics: Critically of financial management Controller’s Role In Management Degree of involvement in business decisions

Conceptual Framework

Management Characteristics: Operating Philosophy Financial orientation Expectations Management Demand for Information for:Analysis Coordination

Control

Figure 2: Conceptual Framework, Sathe (1982), Exhibit 3-1, page 53

FIGURE 3:

Contextual Factors and Degree of Divisional

Controller Involvement:

Environmental and Business Characteristics:

Working asset intensity

Emphasis on planning, Budgeting and capital expenditure review

Financial orientation Expectations regarding typical Division controller involvement

+ + + Corporate Management Characteristics + +

+ Degree of typical division

controller involvement in business decisions

Emphasis on planning, Budgeting and capital expenditure review

Corporate Controller Characteristics

Emphasis on service role in dealing with management Duration of sustaining emphasis on development of controllership

personnel

Figure 3: Contextual Factors and Degree of Typical Division Controller Involvement in the Company, Sathe (1982), Exhibit 6-4, page 110, adjusted

FIGURE 4:

Theoretical Framework:

Role Sender’s Expectations Situational Factors Demand for Role Behavior Expectations And Attributes of Person in the Focal RoleActual Behavior of Person in the Focal Role Interpersonal Factors (2) (4) (3) (5)

Figure 4: Daniel Katz and Robert L. Kahn, The Psychology of Organizations, 2nd ed., Chap. 7, and the findings of

Sathe. (see exhibit 7-2 in Sathe 1982, page 119).

FIGURE 5:

Research Framework Roozen & Steens (2006)

Criticality of controller contribution in light of business and environmental conditions

Management’s expertise in area of controller contribution

Extend of external pressure in area of controller activity, e.g. from litigation,

regulation

Extend to which executives at higher levels have confidence in the integrity and good

judgement of managers at lower levels

Degree of importance of controller involvement Degree of importance of controller independence D eg ree o f co ntr o lle r e ffe ctiv en es s Degree of actual controller involvement Degree of actual controller independence Expectations And attributes of controller Inter-personal factors + + -C1 C2 D2 B A D1

FIGURE 6: Business Unit’s Characteristics + Environment Actual degree of BU-controller Involvement Interpersonal Relationships (2) (4) (3) (5) (1) Head Quarter’s Characteristics + Environment BU-Manager’s Demand for Information from BU-controller BU-manager’s Personality + expectations BU-controller’s Personality + expectations Corporate controller’s Personality + expectations (6) (7) (8) (11) (9) Role Theory Contingency Theory Corporate-controller’s Demand for Information

from BU-Controller

(12)

(10)

Conceptual Framework:

Figure 6: Conceptual research framework to study controller involvement, Ten Rouwelaar (2007)

FIGURE 7:

Framework Factors:

Head Quarter’s Characteristics + Environment Business Unit’s Characteristics + Environment• perceived environmental uncertainty • market or clan culture of the BU • interdependencies among BUs • task uncertainty BU-controller’s Personality + expectations BU-manager’s Personality + expectations Corporate controller’s Personality + expectations • corporate strategy • decentralization • information asymmetry

• rules and regulations • corporate financial distress

• extrovert • open to experiences • agreeable • neuroticism • consolidation • inter-relationships

Nyenrode Research Group

Nyenrode Business Universiteit Nyenrode Research Group Straatweg 25 Postbus 130, 3620 AC BREUKELEN T +31 346 291 696 F +31 346 291 250 E [email protected] www.nyenrode.nl/nrg