Matthew J. Arnold, CFA

Head of Institutional ETF Sales — EMEA, SPDR ETFs

Antoine Lesné

Head of ETF Sales Strategy — EMEA, SPDR ETFs ssga.com

THE CHANGING

LANDSCAPE FOR

BETA REPLICATION

Comparing Futures and SPDR UCITS ETFs

One of the major decisions an institutional investor must make is whether to employ passive management within their portfolios. For most investors, it is a question of how much passive management is employed, rather than if it is used at all. The case for passive investment has been well established over the last 30 years as investors have turned to cost efficient, benchmark-targeted strategies. Exchange Traded Funds (ETFs) have been at the forefront of this investment revolution, bringing low cost, institutional quality portfolio management to the wider investing community. However, the growth of the ETF industry means that institutional investors now have another vehicle option to passively access the various asset class segments available to them.

Historically, the typical institutional investor has used segregated accounts and index funds alongside index futures to passively capture market returns. Some more sophisticated institutions have also employed total return index swaps (TRS). In recent years, ETFs have become a larger component of the institutional investor’s beta replication toolkit — growth in assets has led to lower costs, particularly on ETFs tracking popular market beta indices, and increased liquidity. In contrast, changes in the regulatory and operating environment for the banking sector have contributed to higher costs for investors taking long-term positions in key equity markets via index futures.

In this paper, we present a simple framework for institutional investors to consider when evaluating two of these implementation options — ETFs and equity index futures. The wide range of variables impacting end investors, from external issues such as tax status through to internal circumstances such as governance and operational setup make it a challenge to develop a one-size-fits-all approach. For example, some investors will be comfortable with the operational elements of futures trading, valuing the liquidity and leverage that can be attained on many key asset class exposures. Conversely, others examining the full range of beta replication options might conclude that the simplicity and transparency of ETFs, along with the wide range of exposures available, offset any apparent limitations, such as the potential for tracking error and lower liquidity.

To illustrate the changing industry dynamics, we focus our comparative analysis on a selection of the most commonly used equity indices, such as the S&P 500 and MSCI Emerging Markets. While futures contracts for the more esoteric segments of the equity market, such as low volatility or high dividend equities are available, they are not widely used by investors. ETFs currently appear to be the preferred vehicle for gaining passive exposure to these segments of the market.

straightforward — to provide for the retirements of a workforce

or fund charitable donations, for instance — there are a dizzying

array of choices when it comes to building investment portfolios.

With hundreds of investable asset class segments to consider, a

thousand or more institutionally credible asset managers to call

on, and many thousands more products and strategies to analyse,

the investment world has arguably never been more complex.

In this paper, we examine the characteristics and develop a

framework for evaluation of two key implementation options

for institutional investors — ETFs and equity index futures.

The analysis is conducted from the standpoint of a fully funded investor, meaning the impact of leverage is ignored. Clearly, one of the advantages of futures (and swaps) is the ability to introduce significant leverage into a position. For investors looking to maintain highly levered positions, these vehicles are likely to remain more attractive than ETFs. We restricted the study to equity indices, even though other asset classes can be accessed via both futures and ETFs. The most liquid fixed income futures contracts typically track single points along the maturity curve, such as the 10-year US Treasury, whereas fixed income ETFs typically track an index that includes multiple maturities and potentially different sectors too. Finally, we have not compared commodities futures to ETFs. There are a wide range of commodities futures contracts that actively trade while the universe of highly liquid commodity ETFs, with a few notable exceptions, is relatively limited. We will widen the scope of the research in the future to look more broadly at other asset classes.

It is also worth noting, that while the we have centred the analysis on ETFs and futures, the changing industry dynamics that have contributed to a rise in the cost of running some futures positions have also affected the markets for other synthetic derivatives products such as total return swaps. As with broadening future research to cover different asset classes, there is plenty of scope to add alternative Delta One products such as total return index swaps to later work.

As noted earlier, the goal of this paper is to develop a framework that helps investors evaluate their beta replication options. We begin by discussing the key differences between futures and ETFs, before turning to the range of exposures that each vehicle can cover. We then cover the changing financial landscape that has influenced the relative attractiveness of ETFs and futures. To support our view that some key equity ETFs have become relatively more attractive than comparable futures contracts, we have developed five equity index replication case studies, based on implementation via index futures and ETFs. We conclude with some thoughts on how investors should evaluate their equity beta replication options, particularly on indices where both liquid futures and ETFs exist. Please note, this analysis focused solely on the UCITS range of SPDR ETFs. For investors that are evaluating US domiciled ETFs alongside equity index futures, please contact us for more information. We have generally assumed a basic working knowledge of both ETFs and futures, but for those requiring more information we have provided a detailed appendix covering topics such as Delta One product comparison, an introduction to roll costs and the like. We hope you find the research useful and as always would welcome any feedback.

The analysis is conducted from the standpoint

of a fully funded investor, meaning the impact

of leverage is ignored. Clearly, one of the great

advantages of futures (and swaps) is the ability

to introduce significant leverage into a position.

For investors looking to maintain highly levered

positions, these vehicles are likely to remain more

attractive than ETFs.

Contents

05

Futures versus ETFs – The Key Differences

Pricing Efficiency

Transparency of Holding Costs

Liquidity

Product Maturity

Introduction to Delta One

07

Breadth of Opportunities – A Clear Advantage for ETFs

08

Changes in the Financial Landscape and the Impact on Futures

Regulatory Change Since the Financial Crisis

A Note on Total Return Swaps

Basics of Equity Index Futures Pricing

10

Growing Cost Efficiencies in the ETF Industry

Tradability and Liquidity

12

Is the Price Impact of Change Temporary or Long-lasting?

13

Case Studies Comparing Index Replication Results with

SPDR ETFs and Futures

14

Case Study 1: S&P 500 Total Return Index Exposure

15

Case Study 2: S&P Mid Cap 400 Total Return Index Exposure

16

Case Study 3: FTSE All Share Total Return Index Exposure

17

Case Study 4: MSCI Europe Net Total Return Index Exposure

18

Case Study 5: MSCI Emerging Markets Net Total Return Index Exposure

19

Longer Term Results with SPDR ETFs

20

Futures versus ETFs – A Framework for Comparison

Investment Objective and Time Horizon

Benchmark Selection

Investment Vehicle Selection

Monitoring and Maintenance

22

Conclusion

24

Appendix

25

Delta One Vehicles: Futures, Swaps and ETFs

Vehicle Comparison - for Equity Index Exposure

27

Futures (Mis)Pricing and the Concept of Roll Costs

28

Index Investing via Futures, Swaps and ETFs

Pricing Efficiency

Equity index futures are forward-looking unfunded instruments, and pricing is based primarily on the seller’s cost of capital and the benefits derived from the underlying asset.1 Because these

pricing variables are largely based on sellers’ expectations, futures pricing tends to regularly deviate from the theoretical fair value, and this ‘mispricing’ may persist for relatively long periods. In addition, normal supply-demand dynamics will often play a significant role in the pricing of futures contracts. As many investors are ‘structurally long’ in equity futures—i.e. fully-invested equity investors, such as fund managers and pension funds, rolling futures positions to maintain market exposure— prices can trade at modest premiums to what might be expected due to the supply-demand imbalance. Even with the presence of arbitrageurs, the strong equity markets of the last several years probably exacerbated this, with greater demand for long rather than short equity index futures positions.

Physically-backed equity ETFs on the other hand, represent ownership of assets being managed by the provider (and disclosed daily) on behalf of the fund. As a result, the underlying net asset values (NAV) for ETFs generally involve more

straightforward estimations, particularly for publicly-listed equities that are currently trading. While ETFs can also trade at premiums due to strong demand or for other reasons — markets being closed, for instance — any significant moves away from the fair value can usually be arbitraged away by market participants. This generally ensures tight pricing efficiency for these products.

Transparency of Holding Costs

Pricing deviations in futures contracts represent costs that may be hard to assess, and can have significant bearing on investor portfolios over time. ETFs have transparently defined fee structures, with explicit cost metrics such as the Total Expense Ratio (TER), which makes it easier for investors to estimate their cost of holding over any time frame. However, there are some variables, particularly for very broad multi-country products which may be more challenging to accurately assess in advance.

Tracking difference — or the amount that the performance of an ETF differs from the index it tracks — represents some uncertainty, particularly in ETFs where the fund manager does not hold all underlying securities in the index and/or trading costs are high. For fully replicated developed equity ETFs, managed by reputable institutional managers, the tracking differences should generally be minimal, but for broad market multi-country indices like the MSCI Emerging Markets, there is potential for some tracking difference over and above the TER. Evaluating the fund manager’s historical record in delivering performance close to the benchmark is an important element of the selection process.

Another variable that may impact holding costs is securities lending. While not all ETFs participate in securities lending programs, some do and this will have the effect of reducing investor holding costs over time. The challenge for investors is the returns to the funds will generally not be known in advance as lending conditions change over time.

Finally, there is the negative impact of dividend withholding tax (and stamp duty where applicable), something which typically impacts ETFs more than futures contracts.* We will discuss this further later, but one of the key influencing factors on the amount of dividend withholding tax applied relates to the ETF’s country of domicile and the tax status of the end investor.

Futures versus ETFs —

The Key Differences

Beyond the basic structural differences between equity index

futures and ETFs (see appendix for more information), there are

several factors which may contribute to different performance

results for investors. We detail these below.

Another variable that may impact holding costs is

securities lending. While not all ETFs participate

in securities lending programs, some do and this

will have the effect of reducing investor holding

costs over time. The challenge for investors is the

returns to the funds will generally not be known in

advance as lending conditions change over time.

Liquidity

Futures on bellwether equity indices like the S&P 500 or EURO STOXX 50 typically offer deep liquidity with extended trading hours, low commissions and very tight bid-ask spreads. However, most of the liquidity is concentrated in the contract with the shortest time to expiry, which means an investor taking a long-term position will have to ‘roll’ the contract frequently. ETFs have two layers of liquidity based on the trading dynamics of the ETF itself and the characteristics of the underlying baskets. These factors, combined with other variables such as time of day and general market sentiment, influence the bid-ask spreads. It is important to note that there are significant variations in liquidity in seemingly similar products. The SPDR S&P 500 ETF, for example, trades upwards of $20 billion a day2 at a penny wide while some smaller S&P 500 ETFs record

much smaller volumes at wider spreads. Investors should also be aware that due to the fragmented nature of the European market (i.e. multiple exchanges, different currencies etc.) and the lack of a requirement to report all trades, assessing the true liquidity of a European domiciled ETF may require more investigation than for US ETFs, where all trading is reported and generally occurs at a single venue.

Product Maturity

Futures typically have expiries of one to three months. For longer-term beta exposure, regular buying and selling of contracts needs to be undertaken (a process known as rolling of futures), which involves not only explicit costs such as trading commissions and bid-ask spreads, but also exposes investors to mispricing costs on every roll.3 In addition, efficient management of the collateral is

required in order to achieve the embedded yield in the contract. While this might not be a huge issue in today’s low rate

environment, it will become more relevant as rates begin to go up. ETFs are typically open-ended instruments with no set maturity, so beyond the re-investing of dividends (in cases where the ETF distributes income, rather than re-investing it), there is limited ongoing maintenance required by investors to take a long-term position on a particular market.

Introduction to Delta One

Delta One products are designed to provide investors with exposure to a reference asset without actual direct ownership of the underlying securities. The term has its genesis in the language of risk analysis, where ‘delta’ measures the sensitivity of a pay-out of a derivative contract to movements in price of an underlying asset. As the name suggests, in theory Delta One products have a delta close to one, meaning that these instruments essentially provide investors with one-for-one exposure to the underlying asset before fees and expenses. As an example, if the underlying asset, such as US large cap equities, gained 10%, the Delta One equivalent should also gain approximately 10% less costs. Through a wide array of delivery mechanisms including futures, forwards, swaps, custom baskets and ETFs, Delta One trading desks offer exposure to a broad range of standard as well as customized underlying exposures.

The various product structures have different

characteristics which may impact end results for investors. Please refer to the appendix for a detailed discussion on three of the main Delta One vehicles — Futures, Swaps and ETFs.

* For more information, please consult your tax advisor.

1 Please see the appendix for basics on futures pricing theory. 2 Source: Bloomberg as at 30 September 2014.

Investors looking to implement an equity beta replication strategy via futures are as a result likely to be subject to significant ‘basis risk’ — or risk that the position does not accurately reflect their desired allocation — particularly in segments of the market where there are not liquid contracts on the commonly-used asset class benchmarks.

As an example, there has been a trend among institutional investors towards the adoption of broad market, all-encompassing indices as benchmarks for their portfolios, such as the Russell 3000 for US equities or the FTSE All Share for UK equities. However, there are not currently liquid futures contracts available on many of these indices, so investors are forced to combine futures contracts in the appropriate proportions to build a position that approximates their desired broad market exposure, or, as is more often the case, simply buy a large cap index futures contract as a proxy for the total market.

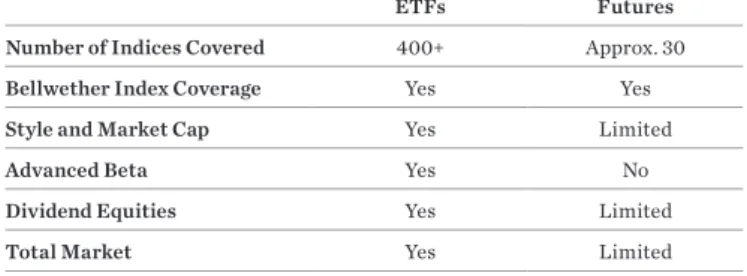

In contrast, ETF investors have a much wider choice of exposures, so they are more likely to be able to find an ETF that tracks the specific index they are looking for. And for those looking to target a more niche segment of the market, say, emerging markets small cap stocks, any replication strategy using futures is likely to result in uncomfortably high long-term tracking error. So as well as offering broad exposure, ETFs also offer very targeted exposure, a useful tool for investors looking to implement a range of investment strategies from tactical asset allocation to transition management. As an example, in the US equity market there are less than 30 liquid futures contracts compared to more than 400 different ETF exposures, as shown in Figure 1. This issue of investor choice is more pronounced outside of US equities, with fewer liquid futures contracts available and a more limited range of exposures compared to ETFs.

Breadth of Opportunities — A Clear

Advantage for ETFs

One of the clear advantages of ETFs over futures is the

sheer range of exposures available. ETFs can be used to gain

broad market or targeted exposure to almost every investable

asset class segment, whereas liquid futures contracts are

typically only available on a few bellwether equity and fixed

income indices (or maturities) and on a range of currencies

and commodities.

So as well as offering broad exposure, ETFs

also offer very targeted exposure, a useful

tool for investors looking to implement a range

of investment strategies from tactical asset

allocation to transition management.

Figure 1: Comparison of Available Exposures via US Equity ETFs and US Equity Index Futures

ETFs Futures

Number of Indices Covered 400+ Approx. 30

Bellwether Index Coverage Yes Yes

Style and Market Cap Yes Limited

Advanced Beta Yes No

Dividend Equities Yes Limited

Total Market Yes Limited

A Note on Total Return Swaps

Despite significant operational differences, the underlying structure and the pricing/hedging mechanism for equity index swaps is similar to equity index futures.4 Stated simply,

variables such as a bank’s net cost of capital would impact the cost for swaps as well. Hence, dynamics that are affecting futures markets are also applicable for a broader range of funding-based derivatives instruments like swaps. Additionally, as the financial crisis has increased investors’ attention on liquidity and counterparty credit risks, greater hedging requirements for these risk factors in swaps are leading to higher costs and slippage for investors. For more details on total return swaps including how they differ to ETFs and futures, please consult the appendix.

Regulatory Change Since the Financial Crisis

Banking and financial markets have been subject to considerable regulatory reforms since the onset of the financial crisis of 2008, aimed at reducing the potential for significant systematic shocks in the future.Key developments:

• The regulatory changes have increased the cost of capital for the investment banking industry, in turn making funding-based synthetic instruments like futures and swaps more expensive.

• Efforts to improve transparency of trading and reporting, under the Dodd-Frank Act in the US, have increased the operational burden for banks as well as investors.

• Mandatory capital requirements set by the Basel III Accord have increasingly constrained banks’ balance sheets, moving some participants away from riskier market making activities.

As banks face higher operational complexities, and liquidity constraints increase the opportunity cost of capital, these costs are increasingly being passed on to investors. This reflects a significant structural rise in the cost of accessing traditional instruments for equity beta exposure, such as futures and swaps. One way to illustrate the impact of changing regulations is to look at changes in bank capital levels over time. Figure 2 depicts the Tier 1 Capital to Risk Weighted Assets of US banks since 2009, highlighting that they are now holding more capital, a cost that is ultimately passed on to customers.

The unfunded nature of futures and total return swaps — implying no or very little upfront capital requirement to trade them – is often considered an advantage over fully-funded instruments like ETFs. However, an important component behind the pricing of unfunded instruments is the net funding

cost charged by the bank (please see “Basics of Equity Index Futures Pricing” on the following page for a detailed

explanation). Owing to the policies of many central banks that have brought ultra-low interest rates, investors’ cash balances are yielding lower rates compared to the net funding costs implied in the pricing of futures and swaps. As long as this yield differential persists, the fully-funded ETF structure may present a more cost-effective tool for long-term market exposure.

Changes in the Financial Landscape and the

Impact on Futures

Figure 2: Regulatory Tier 1 Capital to Risk-Weighted Assets for US Banks 11 11.5 12 12.5 13 13.5 10.5 2009 2010 Q1 2011 2012 2013 2014Q1

Source: IMF Financial Soundness Indicators, State Street Global Advisors (SSGA) as of 31 March 2014.

Basics of Equity Index Futures Pricing

To understand why costs have increased in many futures contracts and decreased in some comparable ETFs, it is necessary to recognize the various dynamics at play, all of which will influence the end results for investors.

When an investor buys a futures contract they are being promised delivery of an underlying asset at the end of a set period of time. Counterparties to these futures trades (usually investment banks) will either need to sell the other side of the trade, or hedge out their market risk. The hedging mechanism would require the bank to buy and hold the underlying basket of index constituents until such obligation expires. In buying index constituents, the bank commits its capital over the life of the contract, and would need to be compensated for the cost of the capital.

Any dividends paid by the stocks, or revenue earned by lending these stocks would accrue to the bank, as the bank holds actual ownership of this stock basket. Thus, the price of the futures contract would exhibit sensitivity to the following variables:

• Bank’s cost of capital (any increase in funding costs would increase futures costs)

• Expected dividends from the underlying stocks (any increase in dividends would reduce futures costs) • Stock lending fees (any fees earned

from lending out the securities would reduce futures costs)

In other words, the summation of these exposures is equivalent to the net funding cost borne by the bank, and ultimately represents the fair value of a futures contract for investors. Long-term futures-based index exposure requires

the continuous rolling of short-term expiry futures contracts. The market price of futures, however, often deviates from fair value (primarily due to market biases in supply-demand, and varying expectations around the above mentioned factors), leading to at times sub-optimal trades at the time of the roll. Over time, such deviations represent serious tracking challenge for investors maintaining a long-term buy and hold exposure through rolling futures strategy. The following table, provided by

JP Morgan’s Global Quantitative & Derivatives team, depicts the current estimated roll costs on a range of equity index futures. The table illustrates how costs have crept up on many key indices in recent times.

For a detailed discussion on the pricing of futures contracts, and the costs involved in rolling exposure, please refer to the appendix.

Region Index Futures Ticker FrequencyRoll Last Trading DayUpcoming Roll

Roll Cost (Annualized)

Last (%) Average (%)Past 1 year since 2007* (%)Average Percentile* (%)

Asia Pacific

TOPIX TP Quarterly 12-Mar-15 0.43 0.07 -0.23 87

Nikkei 225 NK Quarterly 12-Mar-15 0.24 0.08 0.10 81

S&P ASX 200 XP Quarterly 19-Mar-15 0.25 0.27 0.07 61

KOSPI 200 KM Quarterly 12-Mar-15 0.53 0.28 0.08 77

Thai SET 50^ BC Quarterly 30-Mar-15 -4.22 -1.37 -0.31 6

Hang Seng HI Monthly 29-Jan-15 0.51 0.60 0.05 71

Hang Seng China Enterprises HC Monthly 29-Jan-15 1.78 0.54 -0.24 100

CSI 300 IFB Monthly 16-Jan-15 27.07 -0.17 0.86 100

FTSE China A50 XU Monthly 29-Jan-15 -1.70 -1.98 -1.83 57

MSCI Taiwan TW Monthly 29-Jan-15 1.02 0.88 -0.50 83

Taiwan TAIEX FT Monthly 21-Jan-15 1.37 0.09 -1.78 87

S&P CNX NIFTY (NSE) NZ Monthly 29-Jan-15 1.87 1.76 -3.03 89

S&P CNX NIFTY (SGX) IH Monthly 29-Jan-15 2.92 2.13 -3.09 89

MSCI Singapore QZ Monthly 29-Jan-15 1.39 0.31 0.28 86

KLCI IK Monthly 30-Jan-15 IK Monthly 30-Jan-15 -1.92 0.16 -0.89 28

Europe

Euro Stoxx 50 VG Quarterly 20-Mar-15 0.63 0.40 0.20 94

FTSE 100 Z Quarterly 20-Mar-15 0.46 0.31 -0.07 90

DAX GX Quarterly 20-Mar-15 0.46 0.28 0.11 94

SMI SM Quarterly 20-Mar-15 0.02 -0.01 -0.05 61

FTSE MIB ST Quarterly 20-Mar-15 0.66 0.35 0.21 80

CAC CF Monthly 16-Jan-15 0.71 0.14 0.00 99

OMX QC Monthly 16-Jan-15 0.22 0.34 0.14 67

AEX EO Monthly 16-Jan-15 0.66 0.31 0.19 95

IBEX IB Monthly 16-Jan-15 1.58 0.38 -0.12 99

Americas/EM

S&P 500 ES Quarterly 20-Mar-15 0.62 0.34 0.13 100

S&P Mid 400 FA Quarterly 20-Mar-15 0.05 0.12 0.01 50

Russell 2000 RTA Quarterly 20-Mar-15 -0.49 -0.57 -0.59 56

NASDAQ 100 NQ Quarterly 20-Mar-15 0.66 0.36 0.18 100

Dow Jones Industrial Avg DM Quarterly 20-Mar-15 0.65 0.35 0.20 100

S&P/TSX 60 PT Quarterly 19-Mar-15 -0.31 -0.12 -0.19 21

MSCI EM Mini MES Quarterly 20-Mar-15 -0.13 -0.05 0.52 15

Source: J.P. Morgan, Global Equity Index Futures Roll Chartbook, 5 Jan 2015.

*Average of roll cost and percentile of the latest roll cost based on the data since 2007 (since Jun-09 for US listed futures, since Sep-11 for MSCI EM and since 2010 for S&P/TSX 60). **For Korea, Taiwan, India, Malaysia, Indonesia and Thailand, the roll costs in the table above are based on offshore rates. ^Thai SET 50 futures now have monthy contracts while their liquidity has yet to pick up.

Figure 3: J.P. Morgan — Summary of Global Equity Index Futures Roll Cost As of December 2014

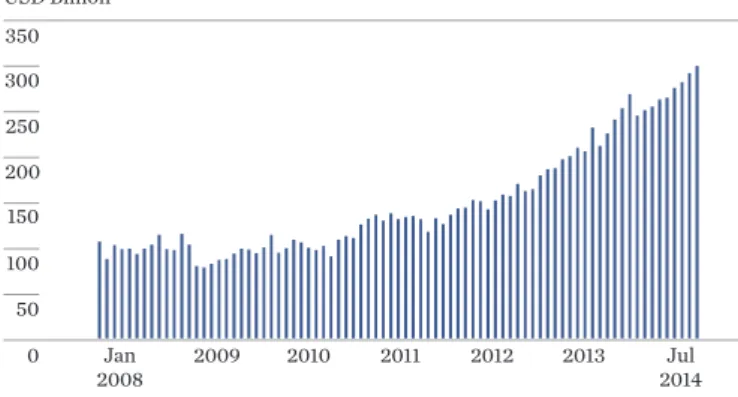

Economies of scale and fierce competition have driven providers to cut the total expense ratios (TER) on a range of products, most notably those funds that track bellwether equity indices. For example, while the first S&P 500 ETF domiciled in Europe still carries a TER of 40 basis points, the TER for S&P 500 ETFs offered by some providers, such as SPDR ETFs, today are in the single digits. Costs for other market beta ETFs have also come down significantly. Figures 4 and 5 show total assets in S&P 500 ETFs domiciled in Europe and the US, and the average TER for the products over time.

Growing Cost Efficiencies in the

ETF Industry

While structural changes within the banking industry have

negatively impacted some costs in the futures market, the ETF

industry is characterised by a reduction in investor costs.

Figure 4: Europe and US Domiciled S&P 500 ETF Assets

USD Billion 0 50 100 150 200 250 300 350 Jan 2008 2009 2010 2011 2012 2013 2014Jul

Source: Morningstar Direct. Month-end total assets in European and US domiciled ETF tracking the S&P 500. Does not include hedged, short or leveraged ETFs. Last reading as of 31 October 2014.

Figure 5: Average Total Expense Ratio on Europe and US Domiciled S&P 500 ETFs

0.12 0.14 0.16 0.18 0.20 0.10 2008 2009 2010 2011 2012 2013 2014 %

Source: Morningstar Direct. Average year-end total expense ratios for European and US domiciled ETF tracking the S&P 500. Does not include hedged, short or leveraged ETFs. Last reading as of 31 October 2014.

Tradability and Liquidity

The ability to enter and exit a trade in a timely and cost effective manner is essential to a successful equity beta replication strategy. The liquidity of futures on indices like the S&P 500 and EURO STOXX 50 is a key advantage, although ETF volumes have grown and spreads on key index products have tightened as the industry has grown. The original ETF for example, the SPDR S&P 500 ETF, trades upwards of $20 billion per day,5 providing

liquidity for investors of almost any size. While the size of the fund — it had assets greater than $200 billion at the end of 2014 — makes it something of an outlier in terms of liquidity, there are currently more than 600 ETFs globally with assets under management of more than $500 million. This enables investors of all sizes to take positions in a range of asset classes via ETFs. In Europe, the fragmented nature of the trading venues adds a layer of complexity as much of the off-exchange trading goes unreported – so investors may only be seeing a fraction of the possible liquidity in a given ETF. This nuance may be one reason why the European industry is still smaller than the US, but should not discourage investors from comparing European domiciled ETFs to similar futures contracts.

To illustrate the liquidity characteristics, we have displayed assets under management (or open interest for futures) and average daily trading volumes for US and European domiciled S&P 500 ETFs and S&P 500 index futures (Figure 6).

Despite increasing assets under management in S&P 500 ETFs, futures clearly maintain an advantage relative to both US and European domiciled ETFs in terms of average daily volume. In addition to volume, trading spreads are also important as ultimately this is a cost that is borne by all investors. We discuss this in more detail in the case studies later in the piece.

ETF providers are not the only ones noticing the evolving landscape. Increasingly, the sell-side is alerting their customers to the changing dynamics within the Delta One space:

Figure 6: Comparison of Assets Under Management and Trading Volumes for S&P 500 ETFs and Futures

S&P 500 US ETFs European ETFs Futures

Number of Vehicles 3 22 1

AUM in mn$ 263,282 40,031 274,643

Total ADV in mn$ 26,727 25 131,434

Max ADV (single fund) in mn$ 25,727 9 N/A

Source: Bloomberg – 9/30/2014 – for futures we show open interest in the current closest contract. For futures we show the max open interest around the month end preceding of the futures roll.

For portfolio managers seeking to replicate the

performance of a major equity index, futures have

historically been a preferred instrument for tracking

the benchmark. This preference towards futures

has several origins. Firstly, equity index futures

have virtually no tracking error to the index, since

they ultimately settle at the underlying index level.

Secondly, futures are extremely liquid — S&P

500 futures are arguably the most liquid financial

product in the world … However, in recent years,

the equity derivatives market has witnessed a

dislocation in the futures roll, with the cost surging

to multi-year highs on the S&P 500 and many other

contracts. The rising cost has largely been the result

of balance sheet and liquidity constraints (e.g. the

Basel Accords, and Dodd-Frank Wall Street Reform

and Consumer Protection Act).

—Accessing Efficient Beta: ETFs versus Futures, BNP Paribas Equity Derivative Strategy, Americas, October 2014

The regulatory and funding pressures that have driven futures costs higher are structural in nature, suggesting the recent trend is likely to persist. As the current regulatory shift is in its initial stages, and will continue to evolve and influence banks going forward, the traditional mechanisms used by banks to finance their derivatives offerings will likely face ongoing challenges. Our analysis indicates that between 2000 and 2012, a quarterly rolling strategy on CME E-Mini S&P 500 Index Futures would have experienced an average quarterly performance difference of around 10 bps. Since September 2012, this difference increased to 22 bps, indicating a significant rise in performance slippage for futures-based portfolios.6 Figure 7 illustrates the impact

of this drag in performance relative to the total return index.

A similar dynamic is evident in the eurozone, with Figure 8 showing the accumulated tracking difference for EURO STOXX 50 Futures Roll Total Return Index7 versus EURO

STOXX 50 Gross Total Return Index — since September 2012, average quarterly tracking difference rose to 10.5 bps, compared to 1 bp in the period 2001–2012. Furthermore, we think it is telling that STOXX Indices felt the need to start publishing a Futures Roll index at all, perhaps indicating that more EURO STOXX 50 futures investors are questioning the results generated though a futures strategy.

Looking forward, implementation of the Volcker Rule in the US and the European Market Infrastructure Regulation (EMIR) in Europe will maintain pressure on the cost of capital for banks. We believe this is a long term trend and one that all financial market participants will have to adapt to over time.

Figure 7: Accumulated Tracking Difference Between CME E-Mini S&P 500 Index Future and S&P 500 Total Return Index 2005 2003 2001 1999 2007 2009 2011 2012 2014 0 -3 -6 -9 -12 Sep – 12 to Sep – 14 %

Source: Bloomberg, SSGA, as of 30 September 2014. Past performance is not a guarantee of future results.

Index returns are unmanaged and do not reflect the deduction of any fees or expenses. Index returns reflect all items of income, gain and loss and the reinvestment of dividends and other income.

Figure 8: Accumulated Tracking Difference Between EURO STOXX 50 Futures Roll Total Return Index and EURO STOXX 50 Gross Return Index

2005 2003 Jan 2001 2007 2009 2012 2014Sep 2 1 0 -1 -2 -3 Sep – 12 to Sep – 14 %

Source: Bloomberg, SSGA, as of 30 September 2014. Past performance is not a guarantee of future results.

Index returns are unmanaged and do not reflect the deduction of any fees or expenses. Index returns reflect all items of income, gain and loss and the reinvestment of dividends and other income.

6 For a description of the definitions and assumptions used in our analysis, please

refer to the appendix.

7 Launched during Nov-13, the index measures the return of a hypothetical,

rolling portfolio invested into a series of EURO STOXX 50 futures contracts.

Is the Price Impact of Change Temporary or

Long-lasting?

In this section, we use five case studies to examine the costs of taking equity

index exposure via futures or through an investment in a SPDR UCITS ETF.

The type of return index that is used — total net or total gross — is based on

what is tracked by the futures contract, rather than the ETF. In several cases,

we believe there was a cost advantage for investors holding the exposure over

a 12-month period via a SPDR UCITS ETF. As mentioned earlier, we have only

included our European domiciled range of SPDR UCITS ETFs in this analysis.

When we expanded the analysis using comparable US domiciled ETFs, we

found the ETF to be a more cost efficient means of gaining exposure over the

period analysed, primarily due to the lack of withholding tax applicable to

US stocks in US domiciled ETFs. For investors that are evaluating US domiciled

ETFs alongside equity index futures, please contact us for more information.

The following analysis is designed to reflect the actual implementation costs

and total returns that would have been experienced by investors had they

taken the respective positions over the trailing 12-month period. The only

costs ignored are normal brokerage commissions. We have made some

important assumptions in conducting the analysis, some of which might not

apply to all investors. As always, we encourage investors to supplement our

research with their own due diligence to ensure all applicable variables are

considered. For full details of the assumptions used in the case studies as well

as the hypothetical cash flows, please refer to the appendix.

Case Studies

Comparing Index Replication Results with

SPDR ETFs and Futures

In this case study, we have compared results for investors taking a $10 million long position in two products, the E-Mini S&P 500 Index Futures and the SPDR S&P 500 UCITS ETF. The time period of the analysis was the 12 months to 30 September 2014. Figure 9 shows the total costs of holding the positions, using actual performance of the underlying vehicles. The costs include implementation and holding costs, but do not include standard brokerage commissions.

Note that the SPDR S&P 500 UCITS ETF domiciled in Ireland is subject to 15% withholding tax on dividends paid by the underlying companies, whereas there is no tax drag assumed in the E-Mini S&P 500 Index Futures contract. An investor’s tax status with the US tax authorities is thus vitally important when selecting the appropriate investment vehicle. For example, some investors (such as UK pension schemes, provided they supply the relevant information) in US domiciled ETFs may be eligible for 0% withholding on ETF distributions, so clearly that will lead some investors to ETFs domiciled in the US rather than the UCITS SPDR ETF used in this example.

By our calculations, investors holding the SPDR S&P 500 UCITS ETF would have been worse off than the comparable E-Mini Index futures position, although this can probably be explained by the 15% withholding tax that is applied to dividend payments from the underlying stocks in the ETF.

Case Study 1

S&P 500 Total Return

Index Exposure

Initial Investment $10 million

Vehicles E-Mini S&P 500 Index Futures, SPDR S&P 500 UCITS ETF

Investment Period One year (from September 2013)

Benchmark S&P 500 Total Return Index

Figure 9: Total Cost of Holding Position

%

Sep

2013 2013Dec 2014Mar 2014Jun

0.73 0.56 Sep 2014 0.8 0.6 0.4 0.2 0

— E-Mini S&P 500 Index Futures vs S&P 500 TR

— SPDR S&P 500 UCITS ETF (SPY5) vs S&P 500 TR

Source: Bloomberg, SSGA as at 30 September 2014 Past performance is not a guarantee of future results..

Figure 10: Cost Differential with SPDR ETF (Assuming $10 Million Investment)

E-Mini S&P 500 Index Futures SPDR S&P 500 UCITS ETF (SPY5) $ (k) 80 40 0 20 -20 60 $56,310 $73,024 -$16,713 Difference -40

Source: Bloomberg, SSGA as at 30 September 2014. Past performance is not a guarantee of future results.

Index returns are unmanaged and do not reflect the deduction of any fees or expenses. Index returns reflect all items of income, gain and loss and the reinvestment of dividends and other income.

In this case study, we have compared results for investors taking a $10 million long position in two products, the E-Mini S&P Mid Cap 400 Index Futures and the SPDR S&P 400 US Mid Cap UCITS ETF. The time period of the analysis was the 12 months to 30 September 2014.

We find that an investor taking the position via the Irish domiciled SPDR UCITS ETF would have been worse off, largely due to the dividend withholding tax applied to funds that hold US equities, as discussed in the previous example. As with the case above, an investor’s underlying tax status (and comfort in purchasing non-local ETFs) should impact which domicile they use for the ETF position.

Case Study 2

S&P Mid Cap 400 Total Return

Index Exposure

Initial Investment $10 million

Vehicles E-Mini S&P Mid Cap 400 Index Futures, SPDR S&P Mid Cap 400 UCITS ETF

Investment Period One year (from September 2013)

Benchmark S&P Mid Cap 400 Total Return Index

Figure 11: Total Cost of Holding Position

%

Sep

2013 2013Dec 2014Mar 2014Jun

0.86 0.60 Sep 2014 0 20 40 60 80 100

— E-Mini S&P MidCap 400 Index Futures vs S&P 400 TR

— SPDR S&P 400 US MidCap UCITS ETF (SPY4) vs S&P 400 TR

Source: Bloomberg, SSGA as at 30 September 2014. Past performance is not a guarantee of future results.

Figure 12: Cost Differential with SPDR ETF (Assuming $10 Million Investment)

E-Mini S&P MidCap 400 Index Futures

SPDR S&P 400 US MidCap UCITS ETF (SPY4) $ (k) 90 30 0 -30 60 $60,013 $85,837 -$25,824 Difference -60

Source: Bloomberg, SSGA as at 30 September 2014. Past performance is not a guarantee of future results.

Index returns are unmanaged and do not reflect the deduction of any fees or expenses. Index returns reflect all items of income, gain and loss and the reinvestment of dividends and other income.

There is not currently a liquid futures contract on the FTSE All Share Index, meaning investors looking for UK equity market exposure (as represented by a FTSE index) via futures are essentially limited to FTSE 100 and FTSE 250 futures contracts. Some investors use the FTSE 100 contract alone, while others use a combination of the two. Neither approach fully replicates the FTSE All Share Index from an exposure perspective, so investors using these futures contracts as a proxy for the broad market are subject to basis risk.

As already noted, we believe institutional investors are

increasingly adopting broad market benchmarks for their equity allocations as they more accurately represent the potential opportunities available to them, so this basis risk should not be overlooked. In the following analysis we compare the results of the FTSE 100 Futures strategy with the SPDR FTSE UK All Share UCITS ETF and the Vanguard FTSE 100 UCITS ETF. Our benchmark is the FTSE All Share Index, so the costs of the FTSE 100 Futures and ETFs positions will in large part be driven by the relative performance of the FTSE 100 and FTSE All Share index.

Both the FTSE 100 ETF and FTSE 100 Futures contract added value relative to the FTSE All Share index, due in large part to the outperformance of large cap stocks over small caps in the period analysed. The SPDR FTSE UK All Share UCITS ETF cost 36 basis points or about £36,000. Comparing the FTSE 100 futures and ETF positions we find that the futures strategy outperformed by 16 basis points. We suspect much of that can be accounted for in the stamp duty costs of trading the underlying in the ETF that are not applicable in a futures contract. So in this case, the FTSE 100 futures strategy is more efficient than the ETF strategy. However, for investors using the futures contracts as a proxy for the overall market, it may make more sense to use an ETF tracking the broad market, such as the SPDR FTSE UK All Share UCITS ETF.

Figure 13: Total Cost of Holding Position

%

Sep

2013 2013Dec 2014Mar 2014Jun

0.02 0.36 -0.14 Sep 2014

— FTSE 100 Index Future vs FTSE UK AS TR

— Vanguard FTSE 100 UCITS ETF (VUKE) vs FTSE UK AS TR — SPDR FTSE UK All Share UCITS ETF (SPYF) vs FTSE UK AS TR -0.5

1.5 1 0.5 0

Source: Bloomberg, SSGA as at 30 September 2014. Past performance is not a guarantee of future results. Figure 14: Cost Differential with ETFs (Assuming £10 Million Investment)

■ FTSE 100 Index

■ Vanguard FTSE 100 UCITS ETF (VUKE)

■ SPDR FTSE UK All Share UCITS ETF (SPYF)

£ (k) 40 0 -20 -40 20 -£13,992 £35,628 £1,645 -£49,619 Difference -£15,637 Difference -60

Source: Bloomberg, SSGA as at 30 September 2014. Past performance is not a guarantee of future results.

Index returns are unmanaged and do not reflect the deduction of any fees or expenses. Index returns reflect all items of income, gain and loss and the reinvestment of dividends and other income.

Initial Investment £10 million

Vehicles FTSE 100 Index Future, SPDR FTSE UK All Share UCITS ETF, Vanguard FTSE 100 UCITS ETF

Investment Period One year (from September 2013)

Benchmark FTSE All Share Total Return Index

Case Study 3

FTSE All Share Total Return

Index Exposure

In this case study we have compared results for investors taking a €10 million long position in two products, the MSCI Europe Net Total Return Index Futures and the SPDR MSCI Europe UCITS ETF. The time period of the analysis was the 12 months to 30 September 2014.

We find that an investment via the SPDR MSCI Europe UCITS ETF would have outperformed an investment via MSCI Europe Futures. The total cost of the exposure for the ETF strategy was €24,000, more than €100,000 cheaper than the total costs of the futures strategy. It should be noted that there is currently little activity in the MSCI Europe futures contract, so investors looking to replicate the return of that market via index futures may be using a basket of country and regional contracts, rather than the broad market contract.

Case Study 4

MSCI Europe Net Total Return

Index Exposure

Initial Investment €10 million

Vehicles MSCI Europe Net Total Return Futures, MSCI Europe UCITS ETF

Investment Period One year (from September 2013)

Benchmark MSCI Europe Net Total Return Index

Figure 15: Total Cost of Holding Position

%

Sep

2013 2013Dec 2014Mar 2014Jun

1.27

0.24 Sep 2014

— MSCI Europe NTR Futures vs MSCI Europe Net TR €

— SPDR MSCI Europe UCITS ETF (ERO) vs MSCI Europe Net TR € 0

1.6 1.2 0.8 0.4

Source: Bloomberg, SSGA, as of 30 September 2014. Past performance is not a guarantee of future results.

Figure 16: Cost Differential with SPDR ETF (Assuming €10 Million Investment)

■ MSCI Europe NTR Futures ■ SPDR MSCI Europe UCITS ETF (ERO)

€ (k) 160 80 40 120 €127,013 €24,200 Difference €102,813 0

Source: Bloomberg, SSGA, as of 30 September 2014. Past performance is not a guarantee of future results.

Index returns are unmanaged and do not reflect the deduction of any fees or expenses. Index returns reflect all items of income, gain and loss and the reinvestment of dividends and other income.

Initial Investment $10 million

Vehicles Mini MSCI Emerging Markets Index Futures, SPDR MSCI Emerging Markets UCITS ETF

Investment Period One year (from September 2013)

Benchmark MSCI Emerging Markets Total Return Index

Case Study 5

MSCI Emerging Markets Net Total Return

Index Exposure

In this example, we compare the results of the MSCI Emerging Markets (EM) Futures position (tracking the total return index) with the SPDR MSCI Emerging Markets UCITS ETF (tracking the net total return index) relative to the MSCI EM Total Return Index. In this case, we find investors would be considerably better off investing via the SPDR ETF, even accounting for the significant withholding taxes that are applied to dividend payments from the underlying securities. On a $10 million investment, we found the ETF to be $190,000 cheaper than the comparable futures contract.

Figure 18: Cost Savings with SPDR ETF (Assuming $10 Million Investment)

Mini MSCI Emerging Markets Index Futures

SPDR MSCI Emerging Markets UCITS ETF (SPYM) $ (k) 300 100 200 $291,551 $100,746 $190,805 Difference 0

Source: Bloomberg, SSGA as at 30 September 2014. Past performance is not a guarantee of future results.

Index returns are unmanaged and do not reflect the deduction of any fees or expenses. Index returns reflect all items of income, gain and loss and the reinvestment of dividends and other income.

Figure 17: Total Cost of Holding Position

%

Sep

2013 2013Dec 2014Mar 2014Jun

2.92

1.01

Sep 2014

— Mini MSCI Emerging Markets Index Futures vs MSCI EM TR

— SPDR MSCI Emerging Markets UCITS ETF (SPYM) vs MSCI EM TR 0

1 2 3

Source: Bloomberg, SSGA as at 30 September 2014. Past performance is not a guarantee of future results.

Over time, if pricing inefficiencies lead to greater holding costs for futures, any apparent withholding tax related disadvantage for ETFs might be mitigated, allowing investors achieve better performance relative to futures on a net-after-tax basis. Figure 21 illustrates this point — on comparing the total holding costs for SPDR UCITS ETFs providing exposure to the S&P 500 net total return index, over the last two years, we witness that net returns on SPDR ETFs are higher even compared to the gross return yielding futures. Combined with the earlier analysis this suggests that for many exposures long-term investors would be better off taking exposure via ETFs, even accounting for the tax advantage that futures have over ETFs for some investors.

Longer Term Results with SPDR ETFs

Figure 19: S&P 500 Index: Total Cost of Holding SPDR UCITS ETF (Net Total Return) versus Futures (Gross Total Return)

%

Jun

2012 2012Dec 2013Jun 2013Dec

2.12 2.04

Jun 2014

— E-Mini S&P 500 Index Futures vs S&P 500 TR

— SPDR S&P 500 UCITS ETF (SPY5) vs S&P 500 TR 0 0.5 1 1.5 2 2.5

Source: Bloomberg, SSGA as at 30 September 2014. Past performance is not a guarantee of future results.

For the purposes of this analysis, we have assumed investors are essentially agnostic as to the vehicle for equity index exposure and are focused only on getting the best deal from a financial perspective. We have also assumed that investors are not looking for significant leverage in their positions – clearly one of the advantages of both futures and swaps is the ability to simply introduce leverage into common equity index exposures. We think investors should consider the following when building a framework to evaluate ETFs and Futures contracts:

Investment Objective and Time Horizon

Defining the investment objective is a key element of a successful beta replication strategy. What is the primary goal and how long is the investment horizon?Investor reasons to look for beta replication products range from transition management through to long-term strategic positioning. Generally speaking, the shorter the time frame – both from a time to initiation and duration of investment perspective – the greater the attention that should be paid to liquidity and trading costs.

The potential benefits gained by investing in a broad, more representative equity index product such as one that tracks the Russell 3000 or FTSE All Share Index may be outweighed by the higher trading costs associated with vehicles that track these indices, particularly in the short term.

With the exception of a few very liquid ETFs, most notably the SPDR S&P 500 ETF which trades $20 billion a day, the tight spreads and near 24 hour trading of Futures contracts on indices such as the S&P 500 and EURO STOXX 50 suggest that investors looking for very short-term exposure might be better off holding

Benchmark Selection

Selecting the right benchmark is crucial to a successful equity beta replication strategy. After taking the decision to invest in an asset class, the identification of a suitable index to represent that asset class is arguably the next most important decision for investors. So any discussion about the relative merits of futures and ETFs as a means of beta replication must also include analysis of the underlying exposures available.

Many of the most liquid and widely used futures contracts track only small segments of the underlying asset class. So while institutional investors like asset managers or pension funds might use a EURO STOXX 50 or FTSE 100 Futures contract as a proxy for the equity market, they are perhaps better served investing in a vehicle that more accurately reflects the actual beta they are trying to capture. The EURO STOXX Total Market Index, or the MSCI EMU for eurozone equities, or the FTSE All Share for UK equities are examples of broad market equity indices with currently limited futures activity.

For investors looking to access areas such as emerging markets bonds, convertibles, dividend equities amongst others, the relatively limited liquid futures market means ETFs or total return index swaps are often the most viable means of gaining passive exposure. The selection of a benchmark should not be done in isolation however. Liquidity and trading costs – both of which are particularly important for short-term positions – should also be factored in. Generally speaking, a relatively narrow large cap index product will have higher liquidity and lower costs than a very broad all cap index product. The trade-off here is that it is likely to be less representative of the asset class than the investor is looking for.

Futures versus ETFs – A Framework

for Comparison

An investor’s unique set of preferences and experience will often

determine the most appropriate vehicle for any beta replication

strategy. Governance and structural characteristics of the

investor will also likely play a role. We recognize the impact of

such factors, but below we detail a simple evaluation framework

that aims to help investors find the right beta replication tool for

their needs.

The Changing Landscape for Beta Replication

Investment Vehicle Selection

(and if Applicable, Manager Selection)

Once the objective has been identified and a likely holding period defined, investors are in a better position to assess the relative merits of ETFs versus futures. Some important variables that will impact the end results of investors will not be known in advance; for example, roll costs on futures positions or tracking differences on ETF positions. However, an analysis of historic results allows investors to make an informed judgement as to the most efficient beta replication strategy for the likely length of their investment.Manager selection may be an issue with ETFs, as there are sometimes dozens of funds tracking the same index. Fund domicile, replication method, securities lending, total expense ratio and liquidity are factors that investors need to consider when analysing their ETF options. Operational considerations are also relevant. Regular rolling of futures positions is required for investments longer than the nearest expiration, while reinvestment of ETF dividend payments (if applicable) is a consideration for investors in ETFs.

Monitoring and Maintenance

All trades require ongoing monitoring and maintenance. One of the great advantages of the ETF structure is its simplicity. They can be bought or sold in as little as single share lots, and benefit from ongoing professional portfolio management. There is no fixed maturity for the vast majority of ETFs, so they can be held indefinitely. Some ETFs will pay out dividends, which would require re-investment, but generally speaking the ease of using ETFs is one of their great advantages. Futures contracts are also relatively straightforward to manage, particularly for experienced investors. However, regular rolling of contracts will be required for long-term strategic positions.

In addition, efficient management of the collateral is required in order to achieve the embedded yield in the contract. While this might not be a huge issue in today’s low rate environment, it will become more relevant as rates begin to rise.

Many of the most liquid and widely used futures

contracts track only small segments of the underlying

asset class. So while institutional investors like

asset managers or pension funds might use a

EURO STOXX 50 or FTSE 100 Futures contract as a

proxy for the equity market, they are perhaps better

served investing in a vehicle that more accurately

reflects the actual beta they are trying to capture.

The rise of passive management within the investment industry has been a key secular trend of the last 30 years. Historically, institutional investors have generally used index funds and segregated accounts alongside index futures, swaps and ETFs as part of their beta replication strategies. Regulatory changes triggered by the global financial crisis have transformed the financial landscape however, and this is raising the cost of capital for the banking industry. This increased cost is filtering through to the end purchasers of futures and other products where the seller’s cost of capital influences pricing. By way of contrast, the ETF industry is benefitting from a secular trend towards passive management, as well as an increasing focus on costs by a diverse range of investors across the globe. With this growth, ETF investors today benefit from even lower costs as well as a wider range of viable investment options.

This paper illustrates how a framework to analyse futures and ETFs tracking equity indices can support investors’ decision-making process. To assist in this process, our six case studies provide a hypothetical illustration of how ETFs fare against futures over a 12-month period. While each investor will have their own unique circumstances, we believe the case studies reflect positively on ETFs as efficient and typically more cost-effective tools than futures for replicating equity market beta returns over the medium to long term (and for fully funded investors).

In summary, we suggest investors consider the following as part of any evaluation process:

1. Define the investment objective and time horizon. Our work suggests that the longer the investment time horizon, the more attractive the ETF options relative to the futures become.

2. Select the benchmark that best represents the investment objective. As our analysis has shown, one of the great advantages of ETFs over futures is the range of available exposures. This wider choice potentially allows for a more precise beta replication strategy.

3. Select the investment tool that most closely captures the desired market exposure, after all costs and expenses are considered. While we encourage investors to do their own research and consider factors specific to their circumstances, our research suggests that on several key equity indices, the SPDR ETF is a more cost-effective means of getting exposure than the comparable futures contract for a fully-funded investor over a 12-month period.

4. Develop a process for monitoring the investment, including ongoing maintenance of positions. One of the great benefits of ETFs is their ease of use. Because they are settled like ordinary equity trades, and with little ongoing maintenance required, ETFs are time efficient as well as being a cost efficient way of accessing markets. Adopting a structured framework such as the above to evaluate futures and ETFs should help investors as they aim to build efficient equity beta replication strategies. A significant benefit of using a structured approach is that it can accurately reflect the prevailing market conditions, enabling investors to react to changes in the environment that will ultimately impact end results.

Acknowledgement

We would like to acknowledge the significant contribution to the research and analysis by Rajat Tiwari, CFA, who worked with the SPDR ETF Capital Markets team. We would also like to thank Emiliano Rabinovich, CFA at State Street Global Advisors.

F. Goltz, D. Schröder. ‘Passive Investing before and after the Crisis: Investors’ Views on Exchange-Traded Funds and Competing Index Products’. EDHEC Business School and University of London, working paper (2010)

A. Madhavan, U. Marchioni, W. Li, and D. Du. ‘Equity ETFs versus Index Futures: A Comparison for Fully Funded Investors’.

The Journal of Index Investing, Vol. 5, No. 2: pp. 66-75 (2014) D. Morillo, N. Da Conceicao, J. Edrosolan, and S. Stewart. ‘Index Futures: Do They Deliver Efficient Beta?’ The Journal of Index Investing, Vol. 2012, No. 1: pp. 107-111 (2012)

‘The Relationship Between MSCI Emerging Markets Index, mini MSCI Emerging Markets Index Futures And The iShares MSCI Emerging Markets ETF’. ICE Futures US, White Paper (2014) M.Tagliani. ‘The Origins And Evolution Of Delta-One’.

Journal of Indexes Europe, Vol. 2, No. 6: pp. 8-11, 17 (2012) BNP Paribas Equity Derivative Strategy, Americas. ‘Accessing Efficient Beta: ETFs versus Futures’ (2014)

Unless otherwise mentioned, the source for all data is Bloomberg L.P. and SSGA

The growth of Delta One has been driven in part by the

increasing demand for passive investment strategies around the world. The rise in popularity of tactical asset allocation and absolute return strategies since the financial crisis has also contributed to an increased demand for cost efficient products that provide long (and short) index exposure. Below we compare and contrast the key features of three main Delta One vehicles — futures, equity swaps, and ETFs.

Futures: Standardized, Exchange-Traded,

Leveraged Exposure

• An obligation on the buyer to purchase the underlying asset at a pre-specified future date and price.

• Easily accessible and allow for short selling. Typically low transaction costs and substantial liquidity for futures tracking most of the major global equity indices.

• Capital efficient — classified as margined investments, only a small fraction of the total trade notional is required to be posted with the Exchange.

• Minimal counterparty risk as contracts are guaranteed by the Exchanges.

• Narrower range of offerings compared to swaps and ETFs. • Daily position management via marking-to-market entails

ongoing operational costs.

• Short-dated rolling expiries, with liquidity concentrated in near-term contracts only.

• Typically suited for short-term, tactical allocation. Longer-term exposure may be costly and inefficient as frequent rolling of the positions introduces implicit risks/costs.

Swaps: Over-the-Counter (OTC) Instruments,

Fully-Customizable, Leveraged Exposure

• An agreement in which two parties agree to exchange paymentsbased on the performance of an underlying reference asset. • Long or short exposure to a wide range of standard benchmarks

and other custom baskets. • Minimal tracking error.

• Capital efficient – exposure gained without tying-up the entire capital.

• Significant counterparty risk – effective cost of exposure may be higher due to credit hedging.

• Defined maturity – early termination may attract penalties, and presents exposure to financing risk.1

• Specialized expertise required to manage OTC positions, higher operational costs due to collateral management and documentation (usually in the form of an International Swaps and Derivatives Association, Inc. (ISDA) contract). • No exchange-based liquidity.

ETFs: Exchange-Traded, Fund Structure,

High Level of Transparency

• Listed securities representing a fully-funded position in an underlying fund that trades throughout the day on an exchange in the same way as shares.

• Broad range of exposures allowing dynamic portfolio construction. Suitable for strategic and tactical exposure. • Multiple levels of liquidity — liquidity of the underlying

constituent basket supplements secondary market volumes for the fund.

• Exchange pricing visibility — creation/redemption mechanism2 ensures efficiency of ETF pricing relative to

the underlying securities.

• Day-to-day investment management dealt by the fund manager in exchange for a fee.

• Management fees and other costs (Total Expense Ratio) along with trading expenses (bid/ask spreads, commissions, market impact) may increase tracking costs.

• Counterparty risk may be an issue with synthetically- replicated ETFs and physically-replicated ETFs using securities lending3.

Delta One Vehicles: Futures,

Swaps and ETFs

1 Financing risk is similar to the concept of funding shortfall for futures contracts, and

implies a mismatch between the cost of funding paid by the investor to the seller and the yield available on her cash balances.

2 Process of creating new ETF units or redeeming the existing ones, which takes place

in the primary market between the fund and the authorized participants. Please refer to the article How ETFs Are Created and Redeemed by SSGA discussing the ETF creation/redemption process in detail.

3 Securities lending is the practice of making short-term loans of the underlying

securities to the borrow market, in order to generate additional income for fund holders.

Delta One Vehicle Comparison — For Equity Index Exposure

Features Futures Swaps ETFs

Coverage

Exposures Major equity indices only, limited

coverage in other asset class segments Extensive. Entirely customizable contracts Extensive. Offerings span across different asset classes globally

Investor Accessibility Lower minimum notional requirements. However, sophisticated pricing and cash flow management, limits their appeal to small investors

Limited to big institutional investors due to typically higher notional requirements, and significant operational considerations

Market-wide appeal due to:

• smaller minimum notional requirements • multiple layers of liquidity for large notionals • operational simplicity

Return Type Total returns (price-based performance

+ discount for forecasted dividends) Typically, total returns (price + actual dividends) Variable Trading

Trading Venue On-Exchange OTC On-Exchange, OTC

Market Making Multiple participants trading

on exchange Single counterparty issuer • Multiple participants trading on Exchange• Primary market via Authorized Participants (AP)

Liquidity Deep liquidity, however, limited to

major indices only Non-tradable Private contract between two counterparties

Multiple levels/pools of liquidity: • Secondary market (fund) • Primary market (underlying basket)

Pricing Intra-day, on Exchange Upon request Intra-day, either on Exchange, or from APs for OTC quotes

Redemption • Cash settled at expiry (Index futures) • Prior to expiry, position can be closed via

contra-position in the same contract

Determined by the ISDA contract. Early redemption could lead to penalties

Continuous intra-day cash-based or in-specie redemption

Operational

Product Classification Derivative Derivative Fund

Capital Requirement Partial funding (in the form of margin

posting requirement with the Exchange) Partial funding (levels can be negotiated) Fully-funded (100% upfront payment)

Documentation Exchange-level agreement Extensive ISDA documentation Standard fund prospectus

Position Management Significant requirements on account of • daily margin posting / cash flow

management • regular rolling at expiry

Typically higher, as cash flows

are exchanged periodically Minimal

Contract Maturity Typically, monthly or quarterly Negotiated Open-ended structure

Position Settlement Cash settled at any time during regular market trading hours up to the expiry of the contract

Periodic cash flow streams Cash- or in-specie settlement at any time during regular market trading hours Structural

Leverage Very high; Typical margin requirements

stand at 5% of the contract notional Variable - based on the contract Higher leverage may, however, require the investor to post additional collateral

None, other than for leveraged funds

Counterparty Risk Minimal Significant Minimal