With the December 2010 passage of the Tax Relief, Unemployment Insurance Reauthorization, and Job Creation Act, investors received much-needed clarity on tax rates through 2012, putting them in a better position to plan effectively. However, now that 2012 is here, the ongoing debate among policymakers about how best to deal with the nation’s burgeoning debt and budget deficit creates considerable uncertainty about tax policy beyond this year.

The U.S. debt crisis became front-page news in 2011. In April, a government shutdown was narrowly averted with the passage of a last-minute budget deal. The Budget Control Act of 2011 was passed in August, providing for $900 billion in discretionary spending cuts over 10 years and creating a bipartisan

congressional “super committee.” The super committee was tasked with reducing the deficit by an additional $1.2 trillion, but failed to reach an agreement before its November 23 deadline. This failure effectively pushed the budget debate into the 2012 election year and magnifies the uncertainty over the longer term.

• A worsening budget deficit and an aging population create considerable uncertainty about tax policy beyond 2012. • Several important tax

provisions expired at the end of 2011.

• New taxes will be levied as a result of 2010’s health- care reform.

• Major tax legislation is unlikely to be enacted before the November elections, and taxes for many investors could increase dramatically in 2013.

• Investors concerned about higher taxes have a number of tax-smart strategies at their disposal.

Ke

y t

ak

ea

w

ay

s

The super committee was tasked with reducing

the deficit by an additional $1.2 trillion, but failed

to reach an agreement before its November 23

Tax planning for 2012

and beyond

Christopher P. Hennessey, CPA Faculty Director, Executive Education, Babson College

Tax Advisor; Estate Planning Attorney Member, Putnam’s Business Advisory Group

William D. Cass, CFP®

Sr. Wealth Management Marketing Manager Global Marketing & Products

Several tax provisions expired at the end of 2011 While lawmakers continue to debate the fate of the Bush-era tax cuts, which are scheduled to expire at the end of 2012, investors should be aware that several important tax provisions expired at the end of 2011. These included:

•

The ability of IRA account owners over the age of 70½ to make annual tax-free distributions of up to $100,000 directly to qualified charities.

•

The alternative minimum tax (AMT) exemption amounts, which are the income levels that trigger the AMT for single and married tax filers. Unless Congress approves a “patch” this year to raise these income levels — which it has done in the past — the exemption amounts will revert back to the much lower levels that were in place in 2000 and extend the tax to an additional 25+ million taxpayers in 2012 (Figure 1).

Figure 1. AMT exemption amounts

Single filers Married filing jointly

2010 $47,450 $72,450

2011 48,450 74,450

2012* 33,750 45,000

1

Amounts if no “patch” is passed by Congress.

•

The ability of small and midsize businesses to immediately write off most or all of the cost of qualifying new and used assets in the first year they are placed into service, up to a maximum of $500,000.

•

The option to deduct state and local sales taxes instead of state and local income taxes on a taxpayer’s federal income tax return.

•

The benefit of deducting up to $4,000 in qualified tuition expenses from income.

A closer look at the nation’s debt crisis

Annual federal budget deficits have increased dramati-cally since 2008, driven largely by spending associated with the global credit crisis and declining tax revenues. As a result, U.S. government debt as a percentage of GDP has reached a level last seen at the end of World War II (Figures 2 and 3).

Figure 2. Annual U.S. federal budget deficit, 2000–2011 ($B)

-1,500 -1,200 -900 -600 -300 0 300

’11 ’10 ’09 ’08 ’07 ’06 ’05 ’04 ’03 ’02 ’01 ’00

Source: Congressional Budget Office, Monthly Budget Review, November 2011.

Figure 3. Gross federal debt as a percent of GDP, 1940–2010

0 20 40 60 80 100 120

’10 ’00 ’90 ’80 ’70 ’60 ’50 ’40

Current level of 93% is the highest since WWII

Source: Office of Management and Budget, Historical Tables, 2011. Total gross federal debt includes debt held by the public as well as intra-governmental debt such as amounts owed to Social Security and federal employee retirement programs.

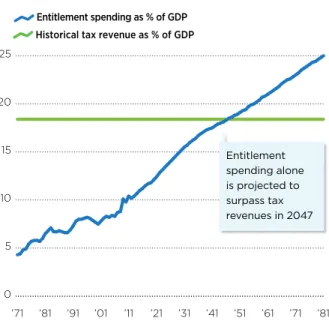

Over the long term, the growth of major government entitlement programs will push the deficit even higher. As baby boomers retire at an increasing rate and health-care costs continue to rise, Social Security and Medicare will face mounting pressure to maintain current benefit levels. And, since nearly two thirds of government spending is tied to mandatory sources,1 it

will be difficult for the federal government to solve the problem of rising deficits simply by cutting spending

(Figures 4 and 5).

Figure 4. Social Security, Medicare, and Medicaid spending as a percent of GDP, 1971–2081

0 5 10 15 20 25

’81 ’71 ’61 ’51 ’41 ’31 ’21 ’11 ’01 ’91 ’81 ’71

Entitlement spending as % of GDP Historical tax revenue as % of GDP

Entitlement spending alone is projected to surpass tax revenues in 2047

Source: Congressional Budget Office, Long-term Budget Outlook, June 2011. Projections are based on CBO alternative fiscal scenario. Tax revenues are based on historical average of roughly 18% of GDP.

Figure 5. U.S. federal government spending by type, 2011 estimated

63%

Mandatory

37%

Discretionary

Source: Congressional Budget Office, Reducing the Deficit, Spending and Revenue Options, March 2011. Mandatory spending types primarily include Social Security, Medicare, and Medicaid, as well as interest on existing debt. Discretionary spending includes defense and non-defense items.

The outlook for tax rates

Given the current economic and political landscape, investors would be wise to prepare for the risk of higher future taxes. During the past 50 years, federal income tax rates have been at current levels or lower only 10% of the time. Total tax revenues as a percentage of GDP have averaged about 18%. If tax rates were to revert back to levels prior to the Tax Reform Act of 1986, the tax savings that investors enjoyed during their working years could be more than offset by higher taxes in retire-ment (Figure 6).

Estates are also taxed at historically low rates. The current maximum estate tax rate of 35% is much lower than the 55% maximum rate of 20 years ago. What’s more, the current federal exemption amount of $5 million — the amount of assets that can be passed free of estate taxes — is more than eight times greater than the $600,000 investors could shelter in the 1990s.

It is unlikely that there will be a major tax deal completed before the

November elections, which could lead to dramatically higher taxes

for many investors in 2013

It is unlikely that there will be a major tax deal completed before the November elections, which could lead to dramatically higher taxes for many investors in 2013. If Congress takes no action, and the Bush-era tax cuts are allowed to expire at the end of 2012, overall tax rates will increase, and a variety of tax-related provisions will change:

•

Qualified dividends and long-term capital gains will no longer be taxed at the historically low level of 15% —

dividends will be taxed at higher ordinary income rates and long-term capital gains will be taxed at a maximum of 20%.

•

Income limits on itemized deductions and personal exemptions will be reinstated, meaning these benefits will once again be phased out for higher-income taxpayers.

•

The so-called “marriage penalty,” which had been eliminated by doubling the standard deduction for couples and adjusting tax brackets, will return.

•

The maximum federal estate and gift tax rates will increase to 55%, with the exemption amounts decreasing to $1 million.

•

The 10% income tax bracket will be eliminated.

•

The 0% tax rate on long-term capital gains and dividends for taxpayers in the lowest brackets will be eliminated.

•

Among education funding provisions, the American Opportunity Tax Credit will expire, the contribution limit for Coverdell Education Savings Accounts will revert back to $500, and student loan interest will no longer be deductible.

Figure 6. Historical maximum U.S. federal tax rates, 1960–2012

0 20 40 60 80 (%) 100

Income: 35%

Long-term capital gains: 15%

Tax r

at

e

Source: Internal Revenue Service, 2012.

Figure 7. Taxes are poised to increase in 2013

Tax item 2012 2013

Ordinary income 35.0% 43.4%

Dividends 15.0% 43.4%

Capital gains 15.0% 23.8%

Payroll tax (employee) 4.2% 6.2%

Estate and gift taxes 35.0% 55.0%

Estate and gift

tax exemption amounts $5.12M $1M

Tax rates reflect highest marginal rate and incorporate additional taxes related to the health-care reform law. Health-care-related taxes include a surtax of 3.8% on net investment income and an additional 0.9% payroll tax affecting single filers with income in excess of $200,000 and joint filers with income in excess of $250,000. The chart assumes employee payroll tax rate of 4.2% is extended into 2012.

Additionally, there will be two new taxes levied on higher-income taxpayers resulting from the health-care overhaul that was passed in 2010. For individuals earning at least $200,000 ($250,000 for couples), there will be a 3.8% Medicare surtax on investment income such as interest, dividends, and capital gains above individuals’ or couples’ income threshold.2 These higher-income

taxpayers will also face an increase in Medicare payroll taxes from 1.45% currently to 2.35% (Figure 7).

What to watch for in 2012

The failure of the congressional super committee to reach an agreement on debt-reduction triggered auto-matic, across-the-board spending cuts that are slated to be implemented over the next 10 years, beginning in January 2013. However, it is likely that legislation will be introduced to counteract these spending cuts, partly due to concern about reductions in defense spending. Prospects for changes in these automatic cuts may be remote since there are indications that the administra-tion would oppose and potentially veto measures to delay or reduce them.

In March, the U.S. Supreme Court will review the consti-tutionality of the 2010 health-care reform legislation, with particular focus on the “individual mandate.” The law currently requires individuals and families to obtain health insurance coverage by 2014 or face a tax penalty (up to $695 for individuals, $2,085 for families by 2016). If the high court rules that this provision is unconstitutional, it likely would have a profound effect on other aspects of the health-care law.

Congress is expected to negotiate a full-year exten-sion of the payroll tax cut, which was extended for two months in December 2011. At issue is continuing the current 4.2% payroll tax levied to fund Social Security, rather than allowing it to return to 6.2%, its rate prior to 2011. An extension of certain unemployment benefits

and Medicare payments to providers (often referred to as the “doc fix”) will be part of the discussions as well. Tax planning strategies for investors

In light of these and other potential developments in 2012, and the risk of higher taxes in the future, there are a variety of tax-smart strategies that investors can incor-porate into their overall financial plan. With the help of financial and tax advisors, investors are likely to find that many of the strategies discussed in this section of the report may help to reduce their tax burden and increase their net after-tax income.

Strategy: Accelerate income

While today’s historically low tax rates remain avail-able, investors may want to consider recognizing more income in 2012. One strategy for accelerating income is to convert a traditional IRA to a Roth IRA. Any type of tax-deferred IRA, including traditional, rollover, SIMPLE,3

SEP, and SAR-SEP, can be converted to a Roth IRA. Taxes on the amount converted are generally due in the year of the conversion. After conversion, investment earnings compound tax free and can be distributed tax free during retirement.

Additional ways to accelerate income include:

•

Taking distributions from a traditional IRA (only advis-able for investors over age 59½, in order to avoid the 10% tax penalty)

•

Realizing long-term capital gains to take advantage of the 15% tax rate and avoid the 3.8% Medicare surtax beginning in 2013. This may be especially attractive to investors who own appreciated stock or mutual funds in taxable accounts, or are contemplating a major transac-tion such as the sale of real estate or business interests

•

Business owners may want to consider increasing their salary, if feasible.

There will be two new taxes levied on higher-income taxpayers resulting

from the health-care overhaul that was passed in 2010.

Strategy: Accelerate deductions

In addition to accelerating income, it may also make sense for investors to accelerate deductions during 2012, since itemized deductions will not be phased out for higher-income taxpayers. Examples of ways to accel-erate deductions include:

•

Prepay mortgage interest or property taxes

•

Make charitable contributions

•

Schedule elective medical procedures if they will entail significant out-of-pocket expenses

•

“Bundle” miscellaneous deductions together such as unreimbursed employee expenses, educator expenses, and expenses related to job searching

An important caveat on accelerating deductions into a specific tax year: It is important to determine your AMT status. That is, if you are subject to the AMT, many common tax deductions, such as the deduction for property taxes, are unavailable. Mortgage interest is one of the few deductions available in calculating AMT liability and regular income tax liability.

Strategy: Review estate plans

Investors should consider reviewing their estate plans to ensure that all elements are in place and up to date. Are basic documents such as wills, powers of attorney, health-care directives, and revocable trusts drafted and current? Are beneficiary designations for retire-ment accounts, annuities, and life insurance policies up to date? Review existing trusts in light of the current $5 million federal exemption, recognizing that this threshold could be lowered in 2013. For many inves-tors, 2012 may be an opportune time to consult with an attorney on more complex wealth-transfer strategies, such as those involving irrevocable life insurance trusts, charitable trusts, or grantor retained trusts.

Strategy: Consider lifetime gifts for efficient transfer of wealth

The $5 million exemption applies to lifetime gifts as well as transfers at death. As a result, in 2012, investors can gift up to $5 million in assets without paying gift taxes. Keep in mind that individuals may gift up to $13,000 per beneficiary ($26,000 for couples) annually without utilizing the lifetime gift allowance. Gifting assets now removes those funds, as well as any future appreciation, from an investor’s estate, avoiding potentially higher estate taxes and lower exemption amounts in the future. Since the $5 million gift tax exemption is scheduled to revert to $1 million in 2013, affluent investors and families may benefit from completing gifts now.

Strategy: Hedge against the uncertainty of future tax rates by pursuing tax diversification

Tax diversification involves allocating assets across accounts and investment vehicles that are taxed differently — taxable, tax deferred, and tax free. Taxable accounts include regular brokerage accounts, mutual funds held outside of retirement plans, savings accounts, and so forth. Tax-deferred accounts include traditional retirement accounts such as 401(k)s and IRAs, as well as annuities. And tax-free accounts/investments include Roth IRAs and municipal bonds.

Depending on your tax situation and life circumstances, tax diversification offers several distinct benefits, including the flexibility to draw income from different sources to gain the most tax benefit (Figure 8). It also

allows investors to hedge their portfolios against higher future tax rates, and may help assets last longer. Tax diversification does not assure a profit or protect against loss.

Figure 8. Tax treatment of various types of retirement assets

Type of asset/account Taxability

Traditional

retirement accounts (e.g., pensions, IRAs, 401(k)s)

Taxable at ordinary income rates when distributed

Roth IRAs and

Roth 401(k)s Contributions made with after-tax dollars; not taxed when distributed

Taxable investment accounts

Capital gains and dividends:

taxed at a maximum 15% rate

Other income:

taxed at ordinary income rates Return of principal:

not taxable

Social Security May be partially taxable at ordinary income rates

Strategy: Invest in municipal bonds

Higher tax rates will increase tax equivalent yields on municipal bonds. Additionally, affluent investors may want to consider an investment in municipal bonds since the interest on municipal bonds is not subject to the new Medicare investment income surtax.

Conclusion

Significant changes may be on the horizon in 2013, and investors would do well to keep a close eye on how such changes may affect their personal finances. As we have seen, there are numerous strategies that can help inves-tors manage their assets in the most tax-smart ways possible. We encourage you to work closely with your financial advisor and tax professional to find ways to benefit from the continued low tax rates in 2012, and to plan prudently for the risk of higher taxes after 2012.

Tax-smart strategies for

investors during 2012

•

Accelerate income by converting a traditional IRA to a Roth IRA, taking distributions from a traditional IRA, or realizing long-term capital gains.

•

Accelerate deductions by prepaying mortgage interest or property taxes, making charitable contributions, or scheduling elective medical procedures.

•

Review your estate plan to ensure that all the necessary components are in place and up to date.

•

Consider making lifetime gifts to take advantage of the $5 million federal exemption.

•

Diversify assets across taxable, tax-deferred, and tax-free accounts and investment vehicles. Consider investing in municipal bonds to create tax-free income.

There is no guarantee that any proposals or plans discussed in this material will be implemented. The views and opinions expressed are those of the authors, are subject to change with market conditions, and are not meant as investment advice. This informa-tion is not meant as tax or legal advice and should only be considered a summary of complex tax rules. Please consult with the appropriate tax or legal professional regarding your particular circumstances and the suit-ability of these strategies before making any investment decisions.

Request a prospectus, or a summary prospectus if available, from your financial advisor or by calling Putnam at 1-800-225-1581. The prospectus includes investment objectives, risks, fees, expenses, and other information that you should read and consider carefully before investing.

William D. Cass is a Senior Wealth

Management Marketing Manager for Putnam. He is a Certified Financial Planner and holds FINRA Series 6, 7, 26, and 63 licenses. He has a B.A. from Tufts University and has been in the investment industry since he joined Putnam in 1990.

Christopher P. Hennessey is a lawyer and

CPA, and is a member of Putnam’s Business Advisory Group. He holds a B.S. and B.A. from Babson College, a J.D. from Suffolk University Law School, and a LL.M. in Taxation from Boston University Law School. He is a member of the American Bar Association, the Massachusetts Bar Association, the Institute of Certified Public Accountants, and the Massachusetts Society of Certified Public Accountants.