Relationship between Marketplace Plan Take-up rate and Monthly Premium from 2014 to 2016.

by

Yifan Wei

A master’s paper submitted to the faculty of The University of North Carolina at Chapel Hill in partial fulfillment of the requirements for the degree of Master of Sciences in Public

Health in the Department of Health Policy and Management, Gillings School of Global Public Health

Chapel Hill 04/28/2017

Approved by:

Abstract: This study estimates the causal relationship between state-level Federally Facilitated Marketplace monthly premiums and take-up rates from 2014 to 2016. A model using fixed

effects was shown to be the right approach. This study found \ small though statistically

significant effects of monthly premiums on the Marketplace plan take-up rate. The results may

suffer from limitations of the model itself and also of accuracy issues in the input data, but if this

finding holds in the upcoming years, the Marketplace may have the chance to stabilize on its

Introduction

Began in October 1st, 2013, the Health Insurance Marketplace (referred to hereafter as

‘the Marketplace’) is one of the central and most visible components of the Affordable Care Act

(ACA). The Marketplace provides consumers a method to enroll in non-group health insurance

and is the only enrollment method where qualifying individuals can get premium- and

cost-sharing subsidies.1 To date, four Open Enrollment periods have been completed. As of the end of

the third open enrollment under the ACA, 12.7 million people had signed up for coverage in the

Health Insurance Marketplace.3

Though providing health insurance coverage to millions of Americans, the Marketplace

has limitations. With the announcement of sizable premium rises and fewer plan choices in 2017,

critics have said that the Marketplace is in a “death spiral”, indicating that the two-way

relationship between the increase in premiums and decreases in enrollment number, called

“adverse selection” by economists, will leave the Marketplace with ever-increasing premiums an

increasingly sicke (and high cost) population, eventually lead to its collapse. However, many

state regulators who permitted large premium increases for 2017 did so primarily to enable

premiums to catch up to the risk profile of the populations enrolling in Marketplace plans, which

is sicker than typical insurance pools. The regulators’ hope is that those increases, coupled with

stable or modestly increasing enrollment, would solidify the Marketplace and return premium

increases to much more moderate levels moving forward.4 How well this will work out depends

on how responsive people are to the rise in premium; if people turn out to be more responsive

than the state regulators expected, a “death spiral” may happen before the Marketplace

This paper looks at the relationship between Marketplace plan take-up rates and

premiums at the state-level. Previous literature looked into this question using

employment-based health insurance and has concluded that employees follow the law of demand and are less

likely to choose health plans with higher monthly out-of-pocket premiums.5,6,7 However, the

Marketplace offers non-group (i.e. individual) plans, rather than group plans, which may affect

response. Marquis and Long measured worker’s demand for health insurance in the non-group

market in their paper and found a price elasticity of -0.3 to -0.4, indicating an inelastic but

nonzero response.8

Though this paper does not try to examine the individual-level relationship of demand for

health insurance’s and premium, instead measuring on an aggregate level, this literatures provide

some insight. My hypothesis for this paper is that increases in premiums should cause a decrease

in the plan take-up rate. If this hypothesis holds, we might also need to know how big the

coefficient is to tell if it is going to lead to the so called “death spiral”. If this hypothesis does not

hold, then maybe after this initial rise in premium to correctly reflect the higher than usual risk

profile of Marketplace population, the number of enrollment will not decrease sharply but may

even increase modestly due to people’s increasing knowledge of the Marketplace; this way, the

Marketplace may normalize after a few years.

Specific Aims

The first specific aim of this study is to estimate the Health Insurance Marketplace plan

take-up rate from Open Enrollment period one to Open Enrollment period three. The second

at the county-level and state average premiums. My hypothesis for this is that an increase in the

premium will be associated with a decrease in the plan take-up rate.

Data

The data I used in this study are longitudinal (three years) at the county-level. The 580

counties included in this dataset are from 35 states that use Healthcare.gov website to enroll in

their Marketplace plans (that is, federally facilitated marketplaces). The dependent variable is the

estimated Marketplace plan take-up rate (in percentage points) for 2014 – 2016; the explanatory

variable is the average monthly premium for the Marketplace plans before tax credit for 2014 –

2016. Due to data limitations, the most granular premium data available are state-level premium

data; this will be addressed in the Limitation section. The plan take-up rate is estimated using the

small area estimation method, with plan selection data from Office of The Assistant Secretary for

Planning and Evaluation (ASPE) and state demographic variables from the American

Community Survey (ACS). The primary explanatory variable is derived from ASPE’s annual

report on premium affordability, competition, and choice in the Health Insurance Marketplace

from 2014 – 2016.9,10,11 Marketplace plans are categorized into four metal levels: bronze, silver,

gold and platinum; as the metal level increases, plans are with higher premium and better

coverage. Nearly 90% of people enrolled into Marketplace plans choose bronze or silver plans,

which are the two lowest costs plans; the average monthly premium for the Marketplace plans

before the tax credit, the explanatory variable in this model, should be a proxy for the price most

people faced when signing up for Marketplace plans. Because pre-subsidy and after-subsidy

premiums are positively correlated, so the pre-subsidy is a rough proxy for the after-subsidy

avoid the two-way causal relationship problem. The tax credit rate is set by federal government

and is the same for every state; it is related to income, so the model will include the percentage

of people in different poverty categories as control variables to control for its effect.

Control variables included in this model are: county-level demographic variables (log

county population, county percentage male, county median age, county percentage of population

in racial/ethnicity groups, county percentage of population in different poverty categories) from

the ACS; number of plans available on county Marketplace from CMS Health Insurance

Marketplace Public Use Files, to control for competition’s impact on premium level; state’s

Medicaid Expansion status, because study has shown that that Medicaid Expansion is associated

with lower Marketplace premiums12; navigator grant amount (per capita) and number of

navigator grantees for each state from CMS website, to control for outreach and enrollment

effort’s effect on take-up rate; year indicator variables, to control for the fact that people’s

knowledge on Marketplace increases over time, and knowledge on Marketplace has positive

impact on take-up rate. All the county demographic variables are from 2013 – 2015; because the

enrollment for a specific year’s Marketplace plan starts in previous year’s November and ends in

January that year, so it makes sense to use demographic variables of the enrolling time in the

model (for example, the state demographic variables used with 2014 take-up rate and premium

are from 2013).

After merging county-level demographics variables from ACS with other variables, there

are 580 counties included in the study sample. The data may suffer from autocorrelation because

it is a county-level study. I will test and address with Huber clustered ex-post standard errors. I

do not suspect heteroscedasticity will be an issue because my outcome variable is a rate; but I

Below in Table 1 are summary statistics for outcome, explanatory and control variables included

in the model.

Method

First Part (take up rate)1 I build on earlier work and use the method outlined here: (excerpted from Dr. Holmes’s research brief)

ASPE provided the number of plan selections by ZIP code during three Open Enrollment

periods. Plan selections for the ZIP code were based on the home address provided for

that individual applicant, or if home address was unavailable, the applicant’s residential

address. The number of plan selections was suppressed for ZIP codes with 50 or fewer

plan selections for privacy reasons. Note that this variable contains the number of

selections, not the number of plans purchased; that is, ASPE did not know whether the

applicant ultimately enrolled in the plan. This variable serves as the numerator. We

calculated the denominator(s) using a three step approach similar to the method used in

other approaches to small-area estimation. The approach is summarized briefly here.

Step 1: Modeling individual probabilities. First, we used the 2012 Public Use Microdata

Sample (PUMS) of the American Community Survey (ACS) to model factors associated

with an individual’s probability of being eligible for the marketplace. An individual was

identified as being “eligible” if they were age 0-64, uninsured or insured through

non-group only, and a citizen of the United States. Children living in households with income

deeming them eligible for Medicaid or CHIP5 were classified as ineligible. Note that this

with access to employer sponsored insurance, but is likely a reasonable estimate based on

data available in the ACS. We developed two estimates: one for those with income 100%

FPG and above and one for those 138% FPG or above.

Using a separate linear probability model for each state, we estimated the probability an

individual was eligible for the marketplace as a function of eight age categories (0-6,

7-11, 12-17, 18-24, 25-34, 35-44, 45-54, 55-64), gender, three race/ethnicity categories

(Hispanic-any race, white only-not Hispanic, at least one race other than white-not

Hispanic), six income categories (0-100% FPG, 100-150% FPG, 150-200% FPG,

200-300% FPG, 300-400% FPG, 400+% FPG), industry/unemployed (for adults), whether the

individual was born in the United States, and indicators for the Public Use Microdata

Area (PUMA). Sampling weights were used to ensure the sample was representative of

the state population. The parameter estimates for each regression were set aside.

Step 2: Developing Small Area Estimates. With the individual parameter estimates in

hand, we then collected ZCTA- level data on corresponding characteristics from the ACS

summary data. For example, table S2407 was used to characterize the proportion of the

ZCTA that worked in each industry, B17024 was used to characterize the age/income

profile of the county, and B05003 was used to characterize the age/sex/nativity of the

community. These data were then used with the parameter estimates from Step 1 to

develop the average probability in the ZCTA of being eligible for the marketplace. This

probability, multiplied by the number of non-elderly in the ZCTA, served as the initial

estimate for the ZCTA-level denominator. Using the MABLE data engine provided by

that the ZCTA-specific estimates could be allocated to PUMAs (ZCTAs spanning

multiple PUMAs were allocated proportionally by population).

Step 3: Raking Estimates. The first two steps of this process do not require the sum of the

ZCTA-specific estimates to equal the estimated number of eligibles from the ACS

PUMA. Therefore, the ZCTA-specific estimates were ”raked” to ensure that the sum of

the ZCTA-estimates in a PUMA equals the estimated number in the PUMA.7 For

example, if the summed number of eligibles in the ZCTAs was 100 but the PUMA

estimate was 110, each ZCTA-specific estimate was increased by 10%. Similarly, the

models do not impose that the number of eligibles with incomes above 138% FPG is less

than the number of eligibles with incomes above 100% FPG; the model is iteratively

raked to ensure that the data are internally consistent in this respect. The final

denominator was the number of estimated eligibles in the ZCTA with incomes above

100% FPG for Medicaid non-expansion states and above 138% FPG for Medicaid

expansion states.

Because ZCTAs can be small, and thus impose considerable sampling variation, we

calculated (weighted) local uptake rates. Briefly, we calculated weighted sums of

enrollees and eligible individuals for a latitude/longitude grid. We identified all ZCTAs

with centroids within 50 miles of the grid point and calculated weights based on the

distance from the ZCTA to the grid; the function exp(-0.1 * miles) means a ZCTA 30

miles away receives 5% of the weight of a ZCTA with centroid equal to the grid point.

With the takeup estimates in hand, I then turn to estimating takeup rates as a a function of

premiums and other factors. I used the OLS/FE/RE method for this paper. The equation is:

TAKEUP = 0 + 1*PREMIUM + 2*X + ,

with TAKEUP being my outcome variable, PREMIUM being my explanatory variable and X

being all the control variables as mentioned above in the Data section; 1 is the parameter that will test my hypothesis.

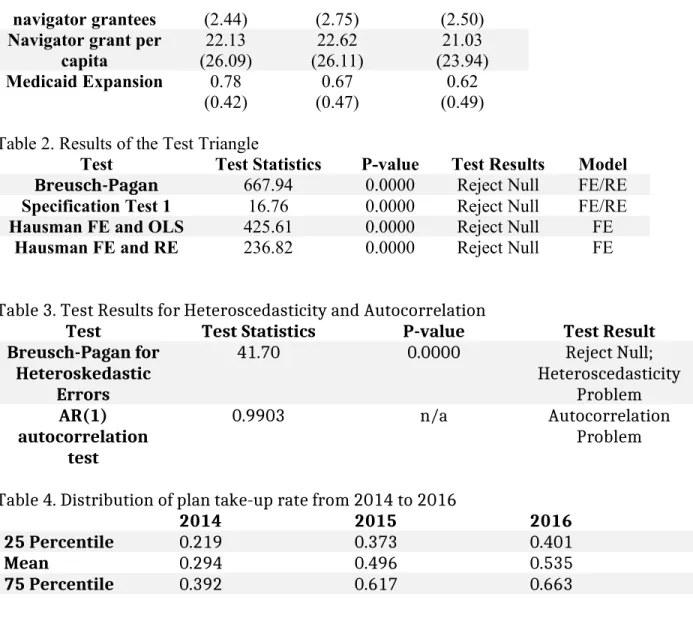

To test which method to use, I performed the Test Triangle. First, I conducted the

Breusch-Pagan test to see whether error terms are independent within the unit to choose between

OLS and RE; then, I conducted a specification test if the coefficient for the individual indicator

is zero to choose between OLS and FE; finally, I conducted Hausman tests between FE and OLS,

FE and RE to test if the consistent estimator (FE) and the efficient estimator (OLS or RE) are

different from each other to choose between these three methods. The results of the Test Triangle

are shown in Table 2. Breusch-Pagan tests whether error terms are independent within the unit to

choose between RE/FE and OLS, and the null hypothesis is σu2 = 0. The result for

Breusch-Pagan shows that it rejected null and should choose RE/FE over OLS. Specification Test 1 tests

whether the coefficient for the individual indicators is zero to choose between FE/RE and OLS,

and the null hypothesis is they are zero. The result for Specification Test 1 shows that it rejected

null and should choose FE/RE over OLS. The Hausman tests if the consistent estimator (FE) and

the efficient estimator (RE/OLS) are different from each other, and the null is they are not

different. The result for both the Hausman tests rejected the null and should choose the consistent

one over the efficient ones. Based on results from the Test Triangle, FE is the best method to use

I would also like to test for heteroscedasticity and autocorrelation. To test for

heteroscedasticity, I used the Breusch-Pagan test for heteroskedastic errors; to test for

autocorrelation, I used the AR (1) serial correlation model. To test for heteroscedasticity

problem, I used Breusch-Pagan Test. After running FE regression, predict and store the residual;

then run auxiliary regression of squared residual on all explanatory variable and control

variables. The F-statistics of this auxiliary regression is shown in Table 3. The F-statistics is

41.70 and the corresponding p-value is 0. We can reject the null hypothesis and from this result,

we could see that there is heteroscedasticity problem with the model. To test for autocorrelation

problem, I used AR(1) autocorrelation test. I predict the residual of FE regression and lag 1 FE

regression, and the correlation coefficient between these two residuals is shown in Table 3. The

correlation coefficient is 0.9903, there is autocorrelation problem with this model. So in the final

model, I use robust standard error and cluster on county level.

Results

Estimation of Plan take-up rate

Table 4 shows summary of plan take-up rate estimation from 2014 to 2016. Graph 1, 2 and 3 are

histograms showing the distribution of plan take-up rate estimation from 2014 to 2016. We could

see from the graph that in 2014, more counties had a lower than average take-up rate; while in

2015 and 2016, this distribution tends to be more normal.

Regression results

The regression results using fixed effects model are shown in Table 5. As shown in Table 5, the

effect of premium on plan take-up rate is

for poverty categories, this effect is 0.02; one dollar increase in premium will increase

percentage plan take-up by 0.02 percentage point. Considering the mean value for take-up and

premium over three years shown in Table 1, this effect is very small.

Other variables that have a statistically significant effect are: natural log of population,

navigator grant per capita, number of plans available on Marketplace and the year indicator

variables.

Limitations

The first limitation of this paper is that the plan selection value used to estimate plan

take-up rate is not actual enrollment number, the actual enrollment should be smaller. There

should be people that select the plan but do not pay the premium, so they are not actually

enrolled into the plan, but they are included in this paper’s plan take-up rate. This affects how

accurate this paper could estimate the relationship between premium and plan take-up. If most

people only start taking premium into consideration on whether or not to enroll after they select

the plan, then this paper’s model might have larger limitatons. But the ASPE plan selection data

is the best available data on Marketplace enrollment number.

A second limitation is that because plan take-up rate is a possibility between 0 and 1, a

maximum likelihood model is a better choice than a linear model in this case. In this case,

however, the range of takeup estimates is largely within the 0-1 range and does not tend to have

a large number of counties with “corner values” at 0 or 1.

A third limitation is that the premium value in this paper is on the state-level because

county-level data is not available. Also, this paper chooses to use the second lowest silver plan

on a range of other characteristics (like smoking or not, family member, age, etc.), the premium

facing everyone is different. A better approach might be to include a premium number with more

variation in the model to better represent the real price that people are facing when deciding

whether or not to enroll into a Marketplace plan. In any event, the premium used here is likely a

fair representation of the overall state-level rates; in other words, states with higher values for the

the measure used here likely have higher after-subsidy premiums.

Another limitation of this paper is that there is potentially a simultaneity issue. The

premium has effect on plan take-up rate, but in turn, the take-up rate or enrollment number in

one area will also affect premium when the insurance issuers and state regulators decide next

year’s premium. So the the two values are determined simultaneously and this is not addressed

by this paper’s model.

Discussion

This study found the effect of premium on plan take-up rate in the Marketplace is very

small, though significant, on the county-level, using 2014-2016 data. If this finding holds true

during the coming years for the Marketplace, ‘death spiral’ might not happen. Even if the finding

itself is reliable, which may not be true due to limitations stated above, the relationship between

premium and take-up rate during 2014 to 2016 may be different with this relationship for

following years. During 2014 to 2016, the Marketplace has just been established, reduction in

take-up rate due to increasing premium may be balanced by increases in the take-up rate due to

more people learning about their eligibility for Marketplace plans and enrolling in. This is

supported by the very large and statistically significant coefficients on both year indicator

variables included. During the first introduction of Marketplace, maybe most of the between-year

variation in plan take-up rate can be explained by difference in year, thus how well people

learnted about the Marketplace. Though this model tries to separate the effect of people’s

knowledge of the Marketplace by including year indicators, it might still be problematic.

Existing studies on relationship between out-of-pocket premium and plan take-up rate on other

kinds of health insurance market show at least a modest negative relationship. For the

Marketplace to stabilize, it may need to finish its premium adjustment for riskier populations in

the initial three to five years, when more people are learning about Marketplace and enrolling in.

After this period, if the fast-increasing premium continues, more people will drop out

Marketplace plan than the number of new enrollees, and that will lead to the collapse of the

References

1. Holmes, Mark, et al. "Geographic variation in plan uptake in the federally facilitated marketplace." NC Rural Health Research Program. September (2014). Available at: http://www.shepscenter.unc.edu/wp-content/uploads/2014/09/EnrollmentFFMSeptember_rvOct2014.pdf

2. State Health Insurance Marketplace Types, 2016. The Kaiser Family Foundation, 2016. Available at:http:// kff.org/health-reform/state-indicator/state-health-insurance-marketplace-types/?

currentTimeframe=0&sortModel=%7B%22colId%22:%22Location%22,%22sort%22:%22asc%22%7D

3. Levitt L, Claxton G, Damico A. and Cox C. Assessing ACA Marketplace Enrollment.The Kaiser Family Foundation. March (2016). Available at:

http://files.kff.org/attachment/issue-brief-assessing-aca-marketplace-enrollment

4. Altman D. Why the Key Indicators to Watch on Health-Care Marketplace Come in 2017. The Kaiser

Family Foundation. October (2016). Available at: http://kff.org/health-reform/perspective/why-the-key-indicators-to-watch-on-health-care-marketplaces-come-in-2017/

5. Feldman, Roger, et al. "The demand for employment-based health insurance plans." Journal of Human Resources (1989): 115-142.

6. Chernew, Michael, Kevin Frick, and Catherine G. McLaughlin. "The demand for health insurance coverage by low-income workers: Can reduced premiums achieve full coverage?." Health Services Research 32.4 (1997): 453.

7. Cooper, Philip F., and Jessica Vistnes. "Workers’ decisions to take-up offered health insurance coverage: assessing the importance of out-of-pocket premium costs." Medical Care 41.7 (2003): III-35.

8. Marquis, M. Susan, and Stephen H. Long. "Worker demand for health insurance in the non-group market." Journal of health economics 14.1 (1995): 47-63.

9. Burke Amy, Misra Arpit, and Sheingold Steven. "Premium Affordability, Competition, and Choice in the Health Insurance Marketplace, 2014." ASPE Research Brief (2014).

10. Misra Arpit and Tsai Thomas. “Health Insurance Marketplace 2015: Average Premiums after Advance

Premium Tax Credits through January 30 in 37 States Using the Healthcare.gov Platform.” ASPE Issue

11. ASPE. “Health Insurance Marketplace Premiums after Shopping, Switching, and Premium Tax Credits,

2015-2016.” ASPE Issue Brief (2016).

12. Sen Aditi and DeLeire Thomas. “The Effect of Medicaid Expansion on Marketplace Premiums.” ASPE

Issue Brief (2016).

13. Wooldridge J. “Introductory Econometrics – A Modern Approach” 5th Edition, Chapter 3 & 4. (2013)

14. Aizer, Anna. "Low Take-Up in Medicaid: Does Outreach Matter and for Whom?." The American Economic Review 93.2 (2003): 238-241.

15. Enroll America. “State of Enrollment: Helping North Carolina Get Covered and Stay Covered,

2014-2015.” Enroll America (2015).

16. Jane B. Wishner, Anna C. Spencer, and Erik Wengle. (November 2014). Analyzing Different Enrollment

Outcomes in Select States That Used the Federally Facilitated Marketplace in 2014. The Urban Institute.

Tables and Graphs

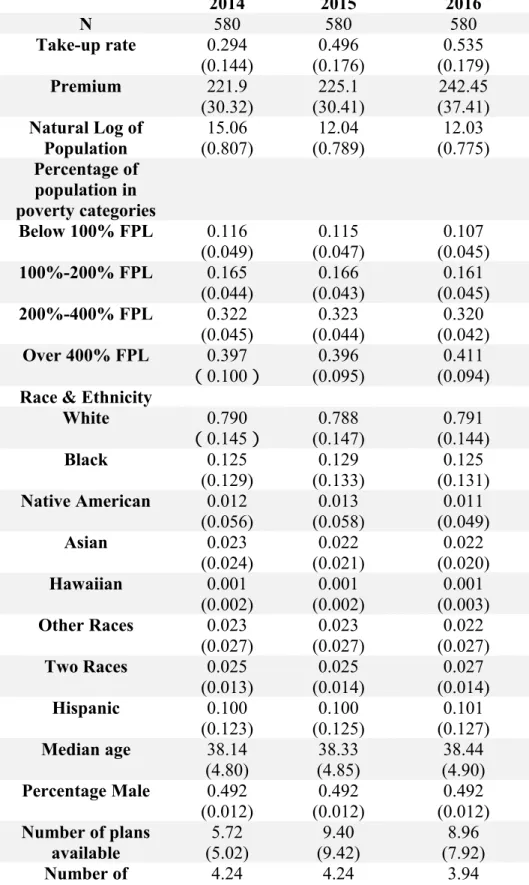

Table 1. Summary Statistics

2014 2015 2016

N 580 580 580

Take-up rate 0.294

(0.144) 0.496 (0.176) 0.535 (0.179) Premium 221.9

(30.32) (30.41)225.1 (37.41)242.45

Natural Log of Population 15.06 (0.807) 12.04 (0.789) 12.03 (0.775) Percentage of population in poverty categories

Below 100% FPL 0.116

(0.049) (0.047)0.115 (0.045)0.107

100%-200% FPL 0.165

(0.044)

0.166 (0.043)

0.161 (0.045)

200%-400% FPL 0.322

(0.045)

0.323 (0.044)

0.320 (0.042)

Over 400% FPL 0.397

(0.100) (0.095)0.396 (0.094)0.411

Race & Ethnicity

White 0.790

(0.145)

0.788 (0.147) 0.791 (0.144) Black 0.125 (0.129) 0.129 (0.133) 0.125 (0.131)

Native American 0.012 (0.056) 0.013 (0.058) 0.011 (0.049) Asian 0.023 (0.024) 0.022 (0.021) 0.022 (0.020) Hawaiian 0.001 (0.002) 0.001 (0.002) 0.001 (0.003)

Other Races 0.023

(0.027) (0.027)0.023 (0.027)0.022

Two Races 0.025

(0.013) 0.025 (0.014) 0.027 (0.014) Hispanic 0.100 (0.123) 0.100 (0.125) 0.101 (0.127)

Median age 38.14

(4.80)

38.33 (4.85)

38.44 (4.90)

Percentage Male 0.492 (0.012)

0.492 (0.012)

0.492 (0.012)

Number of plans

available (5.02)5.72 (9.42)9.40 (7.92)8.96

navigator grantees (2.44) (2.75) (2.50)

Navigator grant per capita 22.13 (26.09) 22.62 (26.11) 21.03 (23.94)

Medicaid Expansion 0.78 (0.42)

0.67 (0.47)

0.62 (0.49)

Table 2. Results of the Test Triangle

Test Test Statistics P-value Test Results Model

Breusch-Pagan 667.94 0.0000 Reject Null FE/RE

Specification Test 1 16.76 0.0000 Reject Null FE/RE

Hausman FE and OLS 425.61 0.0000 Reject Null FE

Hausman FE and RE 236.82 0.0000 Reject Null FE

Table 3. Test Results for Heteroscedasticity and Autocorrelation

Test Test Statistics P-value Test Result Breusch-Pagan for

Heteroskedastic Errors

41.70 0.0000 Reject Null; Heteroscedasticity

Problem AR(1)

autocorrelation test

0.9903 n/a Autocorrelation Problem

Table 4. Distribution of plan take-up rate from 2014 to 2016

2014 2015 2016

25 Percentile 0.219 0.373 0.401

Mean 0.294 0.496 0.535

75 Percentile 0.392 0.617 0.663

Table 5. Fixed Effects Regression Results after Adjusting for Heteroscedasticity and Autocorrelation

Variable Coefficient

Premium** 0.225

(0.083) Interaction terms: premium and

percentage of population in poverty categories

Premium*under 100 FPL -0.328

(0.204) Premium*between 100 and 200 FPL -0.332

(0.232) Premium*between 200 and 400 FPL -0.331

(0.217) Natural log of population*** 124.1

(42.4)

Median age 0.448

(0.373)

Percentage White 16.48

(42.10)

Percentage Black 60.19

(37.65)

Percentage Native American -72.59

(62.20)

Percentage Asian 10.85

(54.81)

Percentage Hawaiian 110.61

(110.48)

Percentage Other Race 10.92

(42.51)

Hispanic -60.01

(102.20)

Percentage under 100 FPL 57.48

(48.36) Percentage between 100 and 200 FPL 67.12

(52.05) Percentage between 200 and 400 FPL 65.45

(49.42) Navigator grant per capita*** 0.452

(0.056) Number of navigator grantees -0.223

(0.181) Number of plan available on

Marketplace*** (0.001)0.191

Medicaid Expansion -0.429

(1.162)

Year 2014 indicator*** -23.21

(0.822)

Year 2015 indicator*** -4.422

(0.508)

Constant*** -1554.5

(275.5)