CGG 2014 July Presentation

All results are presented before Non-Recurring Items linked to Fugro (NRFI) and before impairment & write-off, unless stated otherwise

Catherine Leveau, SVP IR : [email protected] Julie Coulot, IR & SRI Officer : [email protected]

Forward Looking Statements

This presentation contains forward-looking statements, including, without limitation, statements about CGG (“the Company”) plans, strategies and prospects. These forward-looking statements are subject to risks and uncertainties that may change at any time, and, therefore, the Company’s actual results may differ materially from those that were expected. The Company based these forward-looking statements on its current assumptions, expectations and projections about future events. Although the Company believes that the expectations reflected in these forward-looking statements are reasonable, it is very difficult to predict the impact of known factors and it is impossible for us to anticipate all factors that could affect our proposed results. All forward-looking statements are based upon information available to the Company as of the date of this presentation. Important factors that could cause actual results to differ materially from management's expectations are disclosed in the Company’s periodic reports and registration statements filed with the SEC and the AMF. Investors are cautioned not to place undue reliance on such forward-looking statements.

Agenda

1.

CGG at a glance : An integrated business model

2.

Equipment Division

3.

Acquisition Division

4.

GGR Division

5.

Financial Review

6.

Conclusion

3CGG at a glance:

Integrated business model

Revenues split by activity(3)

Revenues split by region(2)

Market leader in geoscience industry globally, providing a comprehensive range of leading geological, geophysical and reservoir capabilities

Market capitalisation of c.$2.5bn (as of July 1st 2014) c.9,500(1) staff working across the globe

Equipment

Sercel, CGG’s Equipment division, is the world-leading designer and manufacturer of land and marine seismic equipment and reservoir monitoring instruments Acquisition

Geophysical data acquisition services include land, marine, airborne and seabed, being operated either directly or through joint ventures

Revenues: $3,766m(2) Net Debt: $2,218m Cash: $530m EBITDAS(4): $1,160m EBIT(5)(6): $423m Net Leverage:1.9x FY2013 Financials

(1)As of December 31, 2013 (2)Operating revenues (3)Revenues from unaffiliated customers (4)Excluding $20m non-recurring items linked to Fugro (NRFI) (5)Earnings before interest

and tax (6)Excluding $17m NRFI and $800m to Acquisition impairment and write-off

3 bu si ness acti vi ties Diversified business

CGG at a glance: An integrated business model

Geology, Geophysics & Reservoir (“GGR”) Key activities include developing and licensing multi-client seismic surveys, processing seismic data, data and software management, reservoir consulting services

From cyclical and capital-intensive businesses to more profitable, less capital intensive

and more cash generating businesses

Our strategy: 2014-2016 Transformation Plan

6

2013 revenues

(1):

$3.8bn

2016 revenues

(2): >

$4.0bn$3.8bn

Strong organic growth for equipment

GGR growth despite reduced MC capex

Equipme

nt

Revenues: $1,045m

Ebit margin: 28.0%

Capital Empl. $0.9bn

508XT & high-channel-count / mega crews

New generation of streamers

Revenues(2): : $1,2-1,3 bn

Ebit margin(2): >28.0%

(1)Operating revenues (2)Assuming unchanged market conditions

Ac

quis

ition Revenues: $2,226m

Ebit margin: 2.5%

Capital Empl. $2.4bn

High-end and flexible fleet & reduced costs

Land & Airborne successful turnarounds

Strengthened partnerships / JV

Revenues(2): $1,6-1,8bn

Ebit margin(2): 8-10% 25% reduction in marine fleet capacity

GGR

Revenues: $1,296m Ebit margin: 24.5% Capital Empl. $2.8bn

Expected future Gulf of Mexico lease sales Continued leadership in Subsurface Imaging Integrated Geosciences offerings & workflows

Revenues(2): $1,5-1,6bn Ebit margin(2): 20-25%

35% 35% 30%

Focus on Management actions

2014-2016 Transformation Plan on track

The Symphony vessel was de-rigged as planned

Ongoing reduction in the marine fleet and associated support structure

Restructuring of Land North America activity ongoing

7

Two successful refinancing operations conducted in April to extend debt maturity

Issue of a €400m Senior Notes due 2020 and of a US $500m Senior Notes due 2022

Full repurchase of the 2016 Convertible Bond, reimbursement of all the Senior Notes

due 2016 and 2/3 of the Senior Notes due 2017

Equipment Division

Equipment: Sercel a leading seismic equipment provider

Streamer:

Strong footprint in land, 70% market share in cable systems

Strong footprint in marine, 95% market share in

streamers

Maintain technological edge ahead of

competitors

Reliability of products, reactive customer

support

2013 Key Figures

Market Positioning

Main products

2013 Geographical sales

breakdown

Total sales $1,045m Number of employees c.2,500 R&D / Revenues 5.6% Number of sites 20 Nautilus Unite Sentinel NomadCable and wireless system:

Digital sensor: MaxiWave Downhole: Vibrator: EBIT $293m EBIT margin 28%

Equipment Division growth driven by Land equipment

markets

Marine driven by sustainable replacement

market

70% sales based on replacement or spread extension

Declining new builds markets

Land: more channels per conventional crew

Continuous channel count growth multiplied by 5every 10 years for conventional crews Number of crews increasing worldwide

508XT launched Q413, powerful response to clients needs, first deliveries July 2014

Middle East: seismic for production is key

5 to 9 tenders for high channels count crewsexpected in 2014-2016

Sercel: strategic supplier agreement with Argas, our historical long-term partner

2010 2011 2012 2013

km Sentinel® sold New builds

5 15 0 0 800 km Sentinel® sold New builds 1000 10 600 400 200 10

Sa

OMAN two potential tenders for 250 000 channel count crews expected in 2015-16?

KUWAITtwo tenders ongoing for 240 000 and 30 000 channels count crews

UAE onetender ongoing for 150 000 channel count crew

SAUDI ARABIA two tenders ongoing for 50 000 channel count crews

Evolution of the New Builds Market

Expected tenders of high channel count crews in the Middle East

Equipment profitability: Operating margin driven by

volumes and product mix

Sercel’s business model highly sensitive to volume sold and product mix

Higher electronic content leads to a higher operating margin

400 350 300 250 200 150 100 50 0 15% 20% 25% 30% 35% 40%

Revenue vs. % Operating Income

by quarter

11 0 200 400 600 800 1000 1200 1400 2008 2009 2010 2011 2012 2013 789 563 515 679 777 673 420 295 485 463 427 3720 1 209 858 1 000 1 142 1 204 1 045 32% 22% 29% 31% 32% 28% EBIT Margin Marine LandAcquisition Division

Acquisition: Ongoing right sizing

Among top 3 leaders with

WesternGeco, PGS

High-end player in Land acquisition A leading Airborne player with

25-30% market share

Market Positioning

2013 Key Figures

Total sales $2,226m Number of employees c.3,000 Industrial CAPEX $250m Vessel availability / productivity rate 89% / 92%Asset

Portfolio

17 3D vessels 13 high-capacity 3D vessels (12+ streamers) 4 mid-capacity 3D vessels (8-12 streamers)

15 land crews including 4 High-Channel-Count

crews

2 Arctic crews

20 fixed-wing aircrafts 1 helicopter

Marine

Land

Airborne

EBIT(1)

$56m

EBIT Margin(1)

2.5%

Oceanic Vega

20 Tow Points

Oceanic Sirius

20 Tow Points 16 Tow Points Geo Coral 16 Tow Points Geo Caspian

Oceanic Champion 14 Tow Points Geo Celtic 12 Tow Points Oceanic Challenger 12 Tow Points Viking Vision 14 Tow Points Viking 10 Tow Points Viking II 8 Tow Points Vantage 10 Tow Points Symphony 12 Tow Points Geowave Voyager 12 Tow Points Viking Vanquish 12 Tow Points Oceanic Endeavour 16 Tow Points Alizé

16 Tow Points Oceanic Phoenix

14 Tow Points

Geo Caribbean

14 Tow Points

Vessel in JV Amadeus 8 Tow Points

3D vessels after having de-rigged Symphony

& in JV

15

1

14

Strategic Roadmap: Reduction of the size of the fleet

Reformat the fleet down to the critical size of 13 vessels to:

Address global and regional markets and optimize transit time Operate during the winter campaign with positive cash contribution Be an enabler for Equipment & GGR divisionsUsed as source vessel De-rigged

Land Acquisition: Refocusing on niche & “techno” markets

& partnerships

15

North America: Refocused on our MC activity &

land contract ongoing restructuring

Rest of the World: Opportunities for franchising /

Technology consulting model

Middle East:

Strengthen our local partnership holding 49% of the new Argas

North Africa: Only direct footprint focus on

technology

The Land situation:

An enabler for Sercel and Processing activities with the right footprint considering the risks

Ramp up of the Seabed Geosolutions activity 40% JV with Fugro

GGR Division

GGR: Geology, Geophysics & Reservoir

Multi client library in key areas (Gulf of

Mexico, North Sea, Brazil)

Technology and broad spectrum of technical

expertise

Highly-skilled people business

Strong geosciences brand

2013 Key Figures

Market Positioning

Strong expertise in GGR

2% 4% 27% 36% 31% Master PhD High School Diploma Other/ Technical / Secondary Bachelor Subsurface Imaging (SI):

46 locations in 32 countries

GeoConsulting /

GeoSoftware:

Presence in 23 countries

Data Management Services:

Presence in 9 countries

Footprint per activity

Total sales

$1,296m: $585m Multi-client and $711m SI &

other businesses Number of employees c.3,500 Countries with GGR implantation 36 EBIT $317m EBIT margin 24.5%

For NALA:

Gulf Of Mexico– StagSeis DEUXFast Trax available – TROIS (293 blocks) being acquired

Brazil– Four new programs on going – 43,000km²of new BroadSeis data

For EAME:

Norway– HORDA: The Largest BroadSeis survey. Acquisition has started

in Norwegian North Sea

North Sea

– Innovative Technology with promising results

– DAZ (Dual Azimuth) on Q30 Phase 7 & 8

– TomoML, GWE, Pore Pressure Prediction and Facies Finder AVO. Cornerstone 35,000km²

Delivering the right data with the best available technology at the right time

20,000 km²

19,000km²

Multi-Client: Building librairies in key areas

18

3 years program started in July 2012 and finishing end 2014, ahead of 2016-2018 ultra-deep water licensing rounds

Subsurface Imaging: Maintaining our leadership position with our

high skilled people

64 k CPU Cores

84 k CPU Cores

95 k CPU cores

110 k CPU cores

160 k CPU cores

453 k GPU cores / 884 cards

150 k CPU cores

2150 k GPU cores / 3400 cards

CPU GPU 0 1 2 3 4 5 6 7 2008 2009 2010 2011 2012 2013

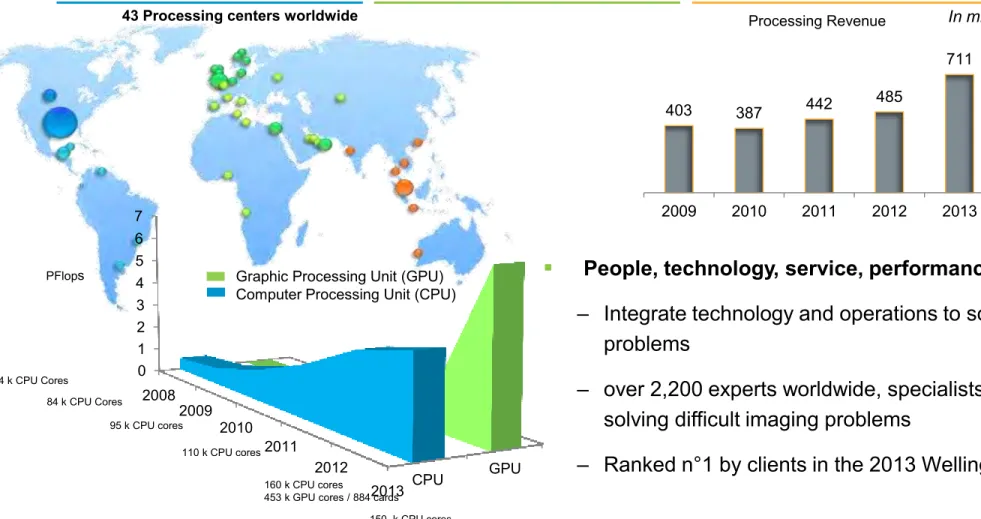

43 Processing centers worldwide

Growth driven by unique worldwide presence and technology leaps in computing

and imaging algorithms

PFlops 403 387 442 485 711 2009 2010 2011 2012 2013 Processing Revenue 19 In million $

Graphic Processing Unit (GPU) Computer Processing Unit (CPU)

People, technology, service, performance

– Integrate technology and operations to solve problems

– over 2,200 experts worldwide, specialists in solving difficult imaging problems

Geoconsulting and Geosoftware: Developing integrated

workflow

20

7.0%

Geoconsulting: offering integrated projects

Acknowledged leader in geopolitical multi-client

products and reports, and high-end consulting services across the E&P value chain

Integrated geophysics, geology & geochemistry

studies

Geosoftware: from seismic to simulation

Advanced reservoir characterization: integrating

seismic, well and production data to better de-risk prospects and further optimize production

Powered by Hampson-Russell and Jason

For unconventionals: tools to help for better well

planning (ProAz), predict sweet spots (Emerge) and to optimize well paths (FractureSpark)

Financial Review

Balance Sheet as of end of March 2014

22

Net Debt at $2.4bn by end of March 2014

Euro-denominated component at €1.0bn Net Debt to Equity ratio at 65%

Total Capital Employed at $6,279m as of end

of March

Multi-Client Library Book Value up at $916m

Increase mostly due to the IBALT program in

the Gulf of Mexico

Cash multi-client Capex pre-funded at 51% Amortization rate at 61%

23

In April, issue of two new

High Yield Bonds

…

€400m due 2020 at 5.875% coupon $500m due 2022 at 6.875% coupon

… to push-back 2016-2017

mandatory instalments

€360m 2016 Convertible Bond $225m 2016 Senior Notes 2/3 $400m 2017 Senior NotesAccelerated Refinancing Program with Senior Debt

Maturity extended by 2 years

A €400m High Yield Bond at 5.875% due 2020:

A $500m High Yield Bond at 6.875% due 2022:

2013 Senior Debt Maturity Profile (in $m)

Maturity as of end of

March extended to 6 years

from 4 years

Average cash cost of Debt

at 5.3%

New Notes 6.3% interest-weighted

on average

2014 Achievements & Outlook

25

Equipment

Sercel awarded the 1st tender in Saudi Arabia for 50 000 channels count crews in June 2014

1st deliveries of 508XT expected in July with the addition of a new system sold in June to PanAmerican

Geophysical in North America

Launch of two new tenders in Saudi Arabia for 50 000 channels count per crew

Acquisition

First steps of the rightsizing the fleet and the Land activity achieved and next ones well engaged First effects of these measures on our cost structure during H2

New set up with Argas operational in H2

CGG and Sovcomflot signed an agreement to create a JV for Arctic 3D seismic exploration, the legal

entity will be created in January 2015

GGR

Completion in September of the three year IBALT program in the GoM with the StagSeis technology

ahead of the 2016-2018 licensing rounds

Sustained activity in Subsurface Imaging driven by increasing volume of data linked to more complex

surveys

2014 Management priorities reaffirmed

Seismic market conditions expected to remain flattish

26

CGG management fully committed to implementing its 2014-2016 transformation plan

First steps in the Acquisition division downsizing plan in Q1 2014

Positive cash generation and active debt management

o 2014 Industrial Capex: $275-300m

o 2014 Multi-client Cash Capex: $500-550m o Prefunding level above 70%

Target 400 bps EBIT improvement in 2016o Rebalanced portfolio

o Operational & commercial efficiency o Cost reductions & tight cash management

Q1 2014 Results: In line with our expectations

28

Group Revenue at $806m, down 7% y-o-y

Equipment at $206m, down 18% GGR at $290m, up 12%

Acquisition at $559m, down 6%

Solid operational performance, notably in Marine

Fleet availability rate at 94% Fleet production rate at 93%

Operating Income at $35m

In line with our expectations

EBIT at $18m, including a $(17)m contribution

from the Equity from Investees

Mainly related to Seabed Geosolutions JV

Net Income at $(39)m

CGG backlog as of April 1

st:$1.2bn

Fleet coverage: 97% in Q2, 60% in Q3 & 10% in Q4

Q1 2013 Q4 2013 Q1 2014 Group Revenue (In million $) 871 806 955 Group EBIT (In million $) Q1 2013 Q4 2013 Q1 2014 128 117 66 73 18 35 Operating Income EBIT

Q1 2013 Q4 2013 Q1 2014

Equipment: 1Q14 Resilient despite lower revenues

29

Total sales were $206m, down 18%

External sales at $163m, down 14%

• Lower land sales across all regions following strong deliveries in Q4 2013

Internal sales represented 21% of total sales

versus 24% last year

51% marine equipment sales and 49% land

equipment sales

EBIT margin at 20.1%

Unfavorable € / $ exchange rate Low volume of sales

Unfavorable product mix with lower electronic

components for land equipment sales

EBIT (In million $) Q1 2013 Q4 2013 Q1 2014 69 102 41 20.1% 32.1% 27.6% Revenue (In million $) 251 317 206 Land Equipment Marine Equipment 51% 37% 63% 41% 54% 46% 49%

Acquisition 1Q 14: Still difficult market conditions

30

Acquisition revenue at $559m, down 6%

External revenue at $353m, down 16%

Land & Airborne revenue at $106m, down 26%

Record low winter campaign in North America Airborne impacted by still depressed mining market

Marine revenue at $453m, quite stable y-o-y and

up 25% sequentially

The Symphony was de-rigged as planned Solid operational performance

Acquisition Operating Income at breakeven and

EBIT at $(16)m

Marine profitability increased significantly sequentially due to an availability rate at 94% versus 83% in Q4 2013 Land acquisition suffered from a historically low winter

season

Negative contribution from Seabed Geosolutions JV

Acquisition Revenue (In million $) Q1 2013 Q4 2013 Q1 2014 568 559 459 363 453

Land & Airborne Marine Acquisition EBIT (In million $) 38 47 (69) (61) Q1 2013 Q4 2013 (2.8)% 7.9% (13.4)% Q1 2014 449 594 106 95 145 0 (16) Operating Income EBIT

Q1 2013 Q4 2013 Q1 2014

Q1 2013 Q4 2013 Q1 2014

GGR 1Q 14: Continuing Sustained Profitability

31

GGR revenue at $290m, up 12% y-o-y

Multi-Client at $127m, up 18% y-o-y, the best

Q1 performance since 2008

Prefunding revenue was $80m

Good level of after-sales in Canada & Brazil Amortization rate at 61%

Subsurface Imaging (SI) & Reservoir at

$163m, up 7% y-o-y

Subsurface Imaging: strong performance CGG and Baker Hughes signed an exclusive

agreement for RoqSCANTM technology

GGR EBIT at $63m, a 21.8% margin

Quite stable y-on-y, excluding the $20m

Spectrum capital gain

GGR Revenue (In million $) MC Revenue GGR EBIT (In million $) 108 166 127 152 206 163 260 371 290 SI & Reservoir 63 86 81 31.1%* 23.2% 21.8% EBIT margin $20m Spectrum capital gain

Q1 2014 Cash: A typical Q1 pattern

32 EBITDAs (In million $)

EBITDAs : $188m, a 23.4% margin

Equipment at $52m, a 25% margin Acquisition at $79m, a 14% margin GGR at $159m, a 55% margin

Cash Flow from Operations at $118m, up 87%

y-o-y

Total Capex of $258m

Industrial Capex: $86m R&D Capex: $16m

Multi-Client Cash Capex: $156m

• Marine Capex at $143m, up 20% y-o-y

(GoM program & Brazil)

• Cash prefunding rate at 51% versus 48% in Q1 2013

Negative Free Cash Flow at $(152)m

Operating Cash Flow / Capex

(In million $) Q1 2013 Q4 2013 Q1 2014 272 280 188 Q1 2013 Q4 2013 Q1 2014 203 63 451 231 258 31.3% 29.3% 23.4% 118 156

Operating Cash Flow Industrial

Multi-client cash capex R&D and other capex

95 117 86 126 65 12 19 16

2014-2016 Strategy: Rebalancing portfolio

33Equipment

Acquisition

GGR

Main Drivers

2013

$3.8bn Revenue

11% Ebit margin2016

>$4.0bn Revenue

15% Ebit margin Revenue: $1.2-1.3bn Ebit margin: >28% Revenue: $1.6-1.8bn Ebit margin: 8%-10% Revenue: $1.5-1.6bn Ebit margin: 20%-25% At unchanged market conditions Revenue before intra-group eliminations

Business line breakdown within Acquisition: Marine 80% / Land & Airborne 20%

Reformatting impact: at iso-market conditions

Intra-Group production: 25% of the fleet capacity corresponding to 20% of total Division revenue

“1.5” mega-crews ordered; when by the New ARGAS:

Fully booked in revenue and in cash, as acquired by a third party

Intra-Group production (marine mainly): c. 10% of total sales

2015 and onwards, MC Cash Capex back to c. $400m, 70%+ pre-funded

Depreciation rate at c. 65%, leading to a stable MC Library Net Book Value

SI & reservoir businesses organic growth sustained by 5% net hiring per year

22% 43% 35% 30% 35% 35%