2017 3rd International Conference on Artificial Intelligence and Industrial Engineering (AIIE 2017) ISBN: 978-1-60595-520-9

Study on Optimization Method of Cost Object Variance Based on

Multi-attribute Combination Dimensions

Wan-lei WANG

*, Shi-kuan ZHOU

and Jing-ping YANG

Dalian Minzu University, Dalian 116600, China*Corresponding author

Keywords: Cost management, Multi-attribute, Data warehouses, Standard cost.

Abstract. An optimization method of cost object variance based on multi-attribute combination dimensions is put forward to solve the problem of screening useful information from a large number of cost variance data. Through the establishment of data warehouses and data models of production process information and cost information, considering the relative importance of cost variance in multiple dimensions, the return of the optimization results, which is based on the specified preference dimension according to the requirements of cost analysis and management, is achieved and the old optimization practice based only on the value of cost variances is changed. Our study focus on the range of cost variance analysis data and help financial personnel to find out the causes of the cost variance effectively.

Introduction

The cost variance analysis is essential for cost control. Liu Xiaomin[1] put forward a variance

analysis method based on the multi-stage ABC calculating model, the variance of each stage is divided into quantity variance, price variance and cost driver variance. Kaplan[2], Mak[3] introduced

the concept of "ability variance" to analyze cost variance. Maliah Sulaiman[4] analyzed cost variance

from price variance, quantity variance, efficiency variance and ability variance. Freitas AA[5]

analyzed multi-objective optimization in data mining.Huang ZiQing and Xiang JianPing[6,7] analyze

on Skyline computation for multi-dimension sorts. These are very useful exploration for cost variance analysis.

However, it is difficult to find out the difference data from a large number of cost data and analyze the causes so as to formulate measures to achieve effective cost control. This paper, combine multiple attributes into five dimensions and analyze the relative importance of cost variance. By this, we determine which data should be used in the analysis of causes of cost variance, which is the basis of setting standard cost.

A Dimensional Analysis of Multi-attribute Cost Object Variance

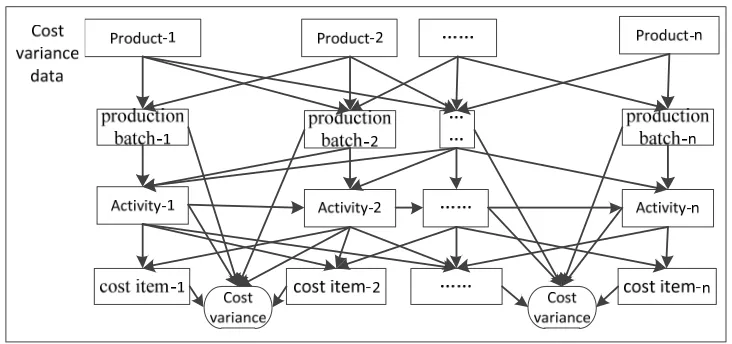

Figure 1. Relationship between cost objects of products, operations, production batches and cost items.

The cost variance is divided into favorable difference and adverse difference, that is to say, the cost variance will have the difference between positive and negative numbers. In this paper, the difference is not refined, and all the values are positive (adverse difference).

After the completion of the cost variance calculation, an recorded attribute value of cost variance has existed in the database. If the data are sorted and screened according to cost variance and only those data with great difference between actual cost and standard cost are analyzed, some important information may be missed. For example, if the cost variance of a cost itemj is obvious in the same

operation, as described above,the other cost items may be omitted. Or the cost variance of the same cost item mis not obvious in different production costs but its different proportion in the cost caused

by this item and production costs in different production should be given different analysis priority. Therefore, this paper combines the three attributes, that is, products, cost items and production batches, into different dimensions, the relative importance degree of the cost variance in different dimensions determines whether the data will be used in the analysis of the causes of cost variance.There are five dimensions: operation-cost item dimension, production batch dimension, cost item dimension, cost item - production batch dimension and product - production batch dimension.

It is assumed that the cost variance CVijk is resulted from the production of the product i,i1,2,3nin Operation A. Among which, the cost item is j, j1,2,3mand the production

batch isk,k 1,2,3x.

Operation-cost item dimension: If Cj is the cost of the cost itemjundertaken by Operation A , the

ratio of each cost item to the sum of the operating cost is pAj, andpAj (0,1]satisfies

m

j Aj

p

1

1so it

is expressed as DimensionpAj.The calculation formula ofpAjis as follows:

m

j j j

Aj C C

p

1 (1) Production batch dimension: When the condition Product ibears Cost Itemjis confirmed, the

importance of production batches that should be involved in the analysis is determined.

x k ijk ijkk CV CV

p

1 (2) Cost item dimension: of the project: On the condition that Production Batchk and Productioni are

given, the importance of Cost Itemj is determined. If all the cost items of Product A consumed in

Production Batchk is considered as a set sj each cost item jsjhas a corresponding probability

j

p and pj(0,1]satisfies

m j j p 11so it is expressed as Dimension pj. The calculation formula

ofpjis as follows:

m j ijk ijkj CV CV

p

1 (3) Cost item - production batch dimension: On the condition that Product i is given, the importance

of Cost Itemj and Production Batchk is determined. All the cost items undertaken by Productiof

the branch factory and all the production batches bearing the corresponding cost items are considered as a setsjk, each production batch kand each cost item jhas a corresponding probability pjkin Set

jk

s , and pjk (0,1]satisfies 1

1 1

m j x k jkp so it is expressed as Dimension pjk. The calculation

formula ofpjkis as follows:

m j x k ijk ijkjk CV CV

p

1 1 (4) Product - production batch dimension: On the condition that Cost Item j is given, the importance

of Product iand Production Batchk is determined. All the products undertaking Cost Item jin the

branch factory and all the production batches bearing Cost Item jare considered as a setsik, each

production batch k and each product j has a corresponding probability pik in Set sik , and

] 1 , 0 ( ik

p satisfies 1

1 1

n i x k jkp so it is expressed as Dimensionpik. The calculation formula ofpikis

as follows:

n i x k ijk ijkik CV CV

p

1 1 (5) It is a multi-objective optimization problem that how to select a subset from the set of dimensions above, and that any point in the subset is no worse than the other points.

Modeling of Dimensional Cost Object Variance Based on Multi-attribute Combination

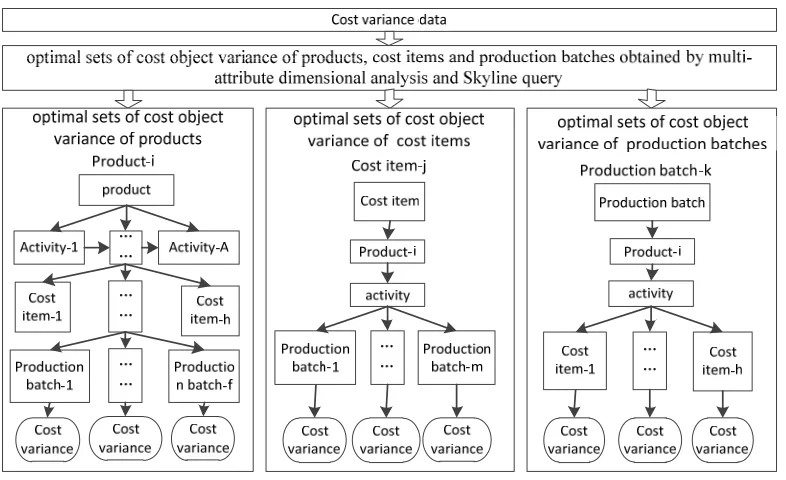

Figure 2. Optimal sets of cost object variance.

In practical application, according to the requirements of cost analysis and management, difference analysis tends to be made based on different combination of attributes. For example, only pj which

represents which cost item difference should be first analyzed in each production batch and pjk

which stands for which cost item and production batch cost variance should be first analyzed on each product. In this paper, BBS algorithm is adopted and is taken as the basic method. The flexible choice of attribute combination is allowed and attributes can be used as parameters. Reconfigurable program modules are used and attribute preference is set according to the requirements of cost analysis and management. Thus, dimensional data are obtained. After comparison and calculation, optimal results will be returned.as shown in Figure 3, to build the optimal models of the cost object variance based on multi-attribute combination, analysis should be made from a single or multiple dimensions according to the requirements of cost analysis and management.

j

p

k

p

Aj

p

ik

p

jk

p

Figure 3. Optimal models of the cost object variance based on multi-attribute combination.

[image:4.612.235.377.487.618.2]analysis. Considering the relative importance of cost variance in multiple dimensions we put forward the optimization method of cost variance based on multi-attribute combination dimensions. In this way, the return of the optimization results, which is based on the specified preference dimension according to the requirements of cost analysis and management, is achieved and the old optimization practice based only on the value of cost variances is changed. Our study focus on the range of cost variance analysis data and help financial personnel to find out the causes of the cost variance effectively.

Acknowledgement

This research was financially supported by the Science and Technology Funds From Liaoning Educational Department(L2013511) and the Fundamental Research Funds for the Centre Universities(DC201502010301).

References

[1] Liu Xiaomin, Deng Weimin, Liu Qizhi. Variance Analysis in ABC [J]. Management Review, 2005, 17(2): 27-32(in Chinese).

[2] Kaplan R.S. Flexible budgeting in an activity-based costing framework [J]. Accounting Horizons, 1994,6:104-109.

[3] Mak Y.T., Roush M.L. Flexible budgeting and variance analysis in an activity-based costing environment [J]. Accounting Horizons, 1994, 6: 93-103.

[4] Maliah Sulaiman, Nik Nazli Nik Ahmad, Norhayati Mohd Alwi. Is standard costing obsolete? Empirical evidence from Malaysia [J]. Managerial Auditing Journal. 2005, 20(2):109-124.

[5] Freitas A.A. A critical review of multi-objective optimization in data mining. A Position Paper: ACM SIGKDD Explorations, 2004, 6(2): 77-86.

[6] Huang ZiQing, Liu DongSu. The Application of Skyline query processing in literature retrieval [J]. Information Studies:Theory & Application,2011,34(10): 104-108.