Asymmetric cointegration and the J Curve: Evidence from commodity trade between Turkey and EU

Full text

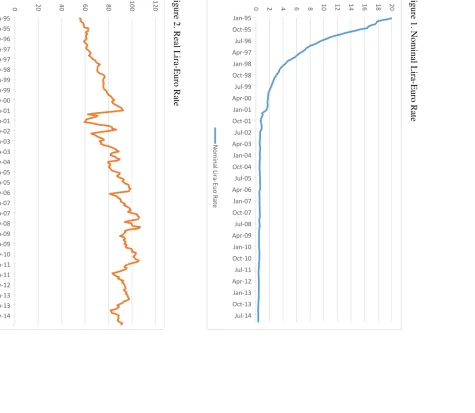

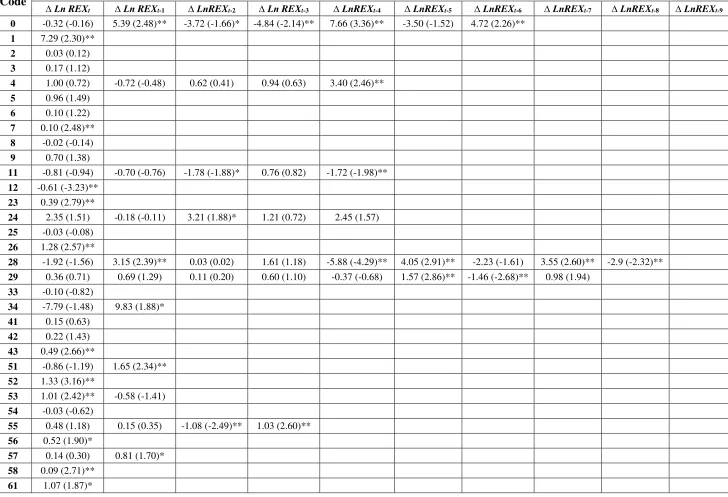

Figure

Related documents

Individual pride itself is closely related to positive emotional behaviour, which is shown in each inherent identity based on (1) professional pride, (2) professional satisfaction,

The prepared microspheres were characterized for drug - polymer compatibility by IR, percentage yield, particle size analysis, drug entrapment efficiency, surface morphology

This quaternized phosphonium salt catalyzed the regioselective ring opening of epoxides by thiocyanate ion to give β-hydroxy thiocyanates in high yields under

The clinician performs a diagnostic assessment to identify whether the patient suffers from a psychiatric illness associated with higher suicide risk, especially mood

Both data-sets were linked on the basis of the initial of name and surname, birthdate and gender (see also data report). We use the final exam grades, the occupation and

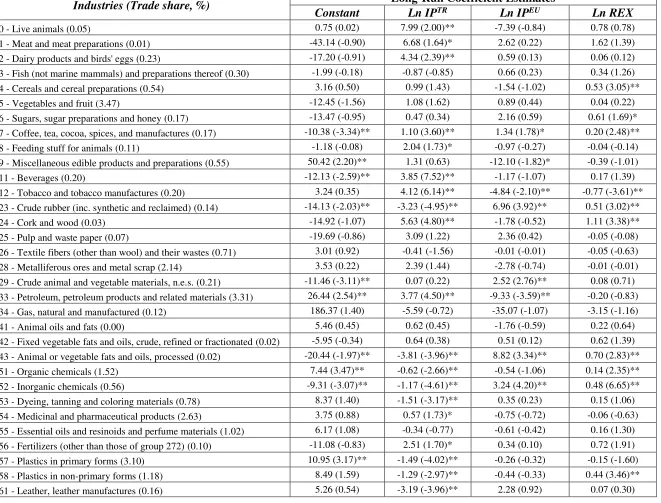

This variable is lagged one year in order to avoid the effects of shocks that can simultaneously affect the probability of becoming unemployed and the share of Chi- nese imports

Methods: In a nationwide study, 596 patients filled validated Gastrointestinal Symptom Rating Scale and Psychological General Well-Being questionnaires and were interviewed

and thus control the network traffic flow, as shown fig 1, where a malicious node M can interface between any of the intermediate nodes participating in the communication in