Cost estimation manual

(SM014)

manual number: SM014

© NZ Transport Agency First edition

Effective from November 2010 ISBN 978-0-478-37104-8 (print) ISBN 978-0-478-37103-1 (online)

Material in it may be reproduced for personal or in-house use without formal permission or charge, provided suitable acknowledgement is made to this publication and the NZ Transport Agency (NZTA) as the source. Requests and enquiries about the reproduction of material in this publication for any other purpose should be made to: NZ Transport Agency

Private Bag 6995 Wellington 6141

The permission to reproduce material in this publication does not extend to any material for which the copyright is identified as being held by a third party. Authorisation to reproduce material belonging to a third party must be obtained from the copyright holder(s) concerned. Disclaimer

The NZTA has endeavoured to ensure material in this document is technically accurate and reflects legal requirements. However, the document does not override governing legislation. The NZTA does not accept liability for any consequences arising from the use of this document. If the user of this document is unsure whether the material is correct, they should make direct reference to the relevant legislation and contact the NZTA.

More information Published 2010

ISBN 978-0-478-37104-8 (print) ISBN 978-0-478-37103-1 (online)

If you have further queries, call our contact centre on 0800 699 000 or write to us:

NZ Transport Agency Private Bag 6995 Wellington 6141

This document is available on the NZTA’s website at

NZ Transport Agency’s Cost estimation manual (SM014)

Document management plan

1) Purpose

This management plan outlines the updating procedures and contact points for the document.

2) Document information

Document name Cost estimation manual

Document number SM014

Document availability This document is located in electronic form on the NZ Transport Agency’s website at

Document owner Commercial Engineer

Document sponsor National Manager Professional Services

3) Amendments and review strategy

All corrective action/improvement requests (CAIRs) suggesting changes will be acknowledged by the document owner.

Comments Frequency

Amendments (minor revisions)

Updates incorporated immediately they occur. As required.

Review (major revisions)

Amendments fundamentally changing the content or structure of the document will be incorporated as soon as practicable. They may require coordinating with the review team timetable.

At least annually.

4) Other information (at document owner’s discretion)

There will be occasions, depending on the subject matter, when amendments will need to be worked through by the review team before the amendment is actioned. This may cause some variations to the above noted time frames.

Record of amendments

This document is a controlled document as defined in the NZ Transport Agency’s (NZTA) Corporate services manual (FCS/Man/1). It is therefore, subject to review and amendment from time to time. Amendments will be recorded in the table below. Amendment notices, detailing the changes, will be issued via email to registered manual holders and should be inserted behind this page.

If you wish to be notified by email when any amendment is made, please email estimation manual SM014’ in the subject line and include your contact details: name, organisation and email address. Please ensure that you notify the NZTA of any subsequent changes to these contact details.

All individuals seeking to rely on or implement this manual, or any other manual referred in this document, have a duty to ensure they are familiar with the most recent amendments.

Amendment number

Description of change Effective date Updated by

0 Issue 3 of the Highways and Network Operations Cost Estimation Manual is amended to become the first edition of the NZTA’s Cost estimation manual (SM014), including minor amendments.

NZ Transport Agency’s Cost estimation manual (SM014)

Foreword

The content of this is based on the NZTA’s current best business practices. The manual will continue to evolve and is subject to revision.

The owner of this manual shall be advised of any proposed amendments to ensure continuous improvement in best practice.

While all care has been taken in formulating this manual, the NZTA Board accepts no responsibility for failure in any way related to the application of this manual, or any reference documents noted in it. There is a need to apply judgement to each particular set of circumstances.

This manual is the first edition of the NZTA's Cost estimation manual (SM014). Three previous editions were published by Transit New Zealand.

Copyright in this manual remains with the NZTA. No reproduction of the contents of this manual is authorised in whole or part. Communications about this manual

Contents

Part A – Introduction 1

1.0 Introduction 2

2.0 Terminology and abbreviations 6

3.0 Estimate definitions 10

Part B – Roles and responsibilities 13

4.0 Roles and responsibilities 14

Part C – Procedures 17

5.0 Purpose of cost estimates 19

6.0 Estimates 21

7.0 Escalation 25

8.0 Land and property 26

9.0 Risk analysis and contingency calculation 29

10.0 Reporting estimates 32

11.0 Estimate audit trail 40

12.0 Peer reviews and parallel estimates 41

13.0 Scope and cost control process 44

Part D – Guidelines 47

14.0 Estimate guidelines 48

NZ Transport Agency’s Cost estimation manual (SM014)

Part A – Introduction

1.0 Introduction 2

1.1 General 2

1.2 Manual background 5

2.0 Terminology and abbreviations 6

2.1 Terminology 6

2.2 Abbreviations 9

3.0 Estimate definitions 10

3.1 General 10

3.2 Project life cycle 11

1.0

Introduction

1.1

General

1.1.1Purpose The purpose of this manual is to outline the minimum requirements in preparing project cost estimates for the NZ Transport Agency (NZTA).

1.1.2Objective The primary objective of this manual is to ensure the consistent application of estimating procedures on the NZTA’s projects.

1.1.3Manual status

This manual has the status of a ‘standard’ as defined in the NZTA 's Register of network standards and guidelines. The authority to amend or vary the manual has been delegated to the sponsor of this manual. This manual is a controlled document in accordance with the NZTA’s Corporate services manual (FCS/Man/1).

1.1.4Intended manual users

This manual is intended to be a used by anyone preparing estimates for the NZTA.

1.1.5Communication and

amendment control

Manual users may communicate via email at the address given on the amendment control sheet. All amendments to this manual will be documented in the record of amendments table at the start of this manual.

1.1.6Manual review process

The manual owner is responsible for the review and update of this manual. The review will be carried out in conjunction with the NZTA’s Project Delivery Value Assurance team. The purpose of reviews is to update the procedures to ensure the manual remains current and represents best practice.

All comments relating to amendments to this manual shall be made to either the regional office contact, who will determine the appropriate course of action, or via email to the address given on the record of amendments sheet provided at the start of this manual.

The manual will undergo regular review. In some instances a change to a fundamental part of the manual may require the manual to be reissued outside the programmed review cycle. If this occurs the NZTA’s consultants and registered manual holders will be informed of the change and issued with the new manual.

1.1.7Interrelationships with other

manuals

This manual contains procedures for preparing cost estimates. In addition consultants shall refer to other NZTA’s manuals, standards and guidelines including, but not limited to the following:

Project management manual (SM011)

Annual plan instructions manual (SM018)

Contract procedures manual (SM021)

State highway professional services contract proforma manual (SM030)

Risk management process manual (AC/Man/2)

Planning, programming and funding manual (PPFM)

NZ Transport Agency’s Cost estimation manual (SM014) 1.1.8Document

availability

This manual is available as a PDF on the NZTA’s The following documents are referred to in this manual and are also available on the NZTA’s website:

The example forms are available as electronic Microsoft Excel documents (original copies are held on the NZTA National Office server (G:\Region\Manuals and Forms\SM 014 Cost Estimation Manual - Appendix Templates).

The elemental cost database.

The register of estimate peer reviewers and industry.

This manual is available to road controlling authorities (RCAs). RCAs should contact, in writing, the manual owner at the NZTA National Office (a cost may apply).

1.1.9Feedback The NZTA welcomes feedback about this manual. Please send feedback via email to

NZTA (this form is also available on the NZTA’s website).

Feedback form

To Cost estimation manual (SM014) owner, NZ Transport Agency

Attention Bill Hewitt

Fax number 06 345 7151

Subject Cost estimation manual (SM014) feedback form

From (name and company) Contact number Contact email Contact address Manual reference Comment and/or description of problem

Describe what you would like to happen/suggest change

Feedback ID Action

NZ Transport Agency’s Cost estimation manual (SM014)

1.2

Manual background

The NZTA’s Cost estimation manual (SM014) has been produced jointly by the NZTA and Association of Consulting Engineers New Zealand (ACENZ). These organisations have an interest in the accuracy of cost estimates for roading projects and have agreed a set of policies that are the basis of this manual’s guidelines.

ACENZ is the professional body representing consulting engineers in New Zealand. Members of ACENZ are usually engaged to provide cost estimates for the NZTA’s projects.

The NZTA owns and manages this manual. Every person producing, reviewing or submitting estimates for an NZTA’s project must do so with reference to this manual. The manual is intended to be a concise, hands-on, user-friendly and non-prescriptive resource containing sufficient guidance to produce a reliable estimate. It provides guidance on the types and use of project cost estimates and includes example estimate templates. The guidance can apply to all roading projects, whether maintenance or capital, delivered under any procurement method.

The principles of estimating can be applied to all NZTA’s work.

Internal and external peer reviews and independent parallel estimates conducted by experienced practitioners are a vital element of the estimation process. This manual also provides guidance as to the timing and requirements of these processes.

2.0

Terminology and abbreviations

2.1

Terminology

Base date Project costs shall be expressed in dollar values as at 1 July of the financial year in which the estimate is being prepared. Base estimate The total sum of the elements that make up an estimate and including provisional sums but not including a contingency. For example, in physical works it is the sum of the calculated quantities from a drawing multiplied by the current market rates for each work item.

Benchmark estimator Benchmark estimator – Roadworks Strategic Manager is an estimating software package that may be used by the NZTA to validate feasibility estimates (FEs) and option estimates (OEs). The NZTA’s Commercial Engineer (Project Services group - National Office) will manage this process.

Consultant(s) A specialist person or organisation who gives expert advice or information. Consultant(s) are normally external to the NZTA but may also include internal parties.

Contingency A provision for known/unknown risks between the base and expected estimates. This may also be referred to as the risk contingency or an allowance to cover the statistical mean of risks and opportunities.

Elemental costing Estimates of project out-turn costs prepared using composite rates for major components of a project. Escalation An additional allowance to cover for increasing costs due to inflation throughout the project life cycle.

Estimate types Feasibility estimate (FE) – prepared during the feasibility phase, normally as part of a project feasibility report. This estimate is used to provide budgets for forward works programming.

Note: To produce more reliable estimates further investigation beyond a traditional approach may be undertaken in the project feasibility phase.

The FE includes an expected estimate and a 95th percentile estimate. Generally, these estimates are prepared using elemental costs. Major risks must be identified and their impact on the out-turn cost assessed and included in the estimate.

Option estimate (OE) – prepared during the investigation and reporting (I&R) phase for each proposed solution. These estimates are used for comparing project options.

The OE includes an expected estimate and a 95th percentile estimate. These estimates are based on a preliminary brief, limited site information and general information about the type of construction, scope of work and possible alignment. All risks must be identified and their impact on the out-turn cost assessed and included in the estimate.

The OE will be compared with the FE. If there are differences between the estimates, the consultant must explain the reasons in a report to be included when they submit the OE.

Scheme estimate (SE) – prepared during the I&R phase. This estimate is based on the preferred option that will be included in the scheme assessment report (SAR)/assessment of environmental effects (AEE). The SE must be used to support any notice of requirement for designation (NOR).

The SE includes an expected estimate and a 95th percentile estimate. The estimate is based on the identified scope and functionality, appropriate site information and preliminary design drawings. All risks must be identified and their impact on the out-turn cost assessed and included in the estimate.

This SE will be compared with the OE and will be independently peer reviewed. If there are differences between the estimates and/or the peer review, the consultant must explain the reasons in a report to be included when they submit the SE.

NZ Transport Agency’s Cost estimation manual (SM014)

Estimate types continued

Pre-design estimate (PE) – prepared during the I&R phase. It is an estimate of the approved project option, updated to include any hearing or Environment Court conditions (eg notice of requirement/ resource consent). It is prepared prior to seeking funding for the design phase.

The PE includes an expected estimate and a 95th percentile estimate. All risks must be reviewed and their impact on the out-turn cost assessed and included in the estimate.

The PE will be compared with the SE. If there are differences between the estimates, the consultant must explain the reasons in a report to be included when they submit the PE.

Design estimate (DE) – prepared during the design and project documentation (D&PD) phase. This estimate is based on detailed design documentation and prepared prior to seeking construction funding and tendering of the physical works.

The DE includes an expected estimate and a 95th percentile estimate. ‘Detailed design documentation’ includes drawings, specifications, schedule of prices, NOR and all consent conditions. All risks must be reviewed and their impact on the out-turn cost assessed and included in the estimate.

The DE will be compared with the PE. If there are differences between the estimates, the consultant must explain the reasons in a report to be included when they submit the DE.

The DE is a construction phase cost estimate with both the I&R and D&PD phase costs set to nil. An engineer’s estimate for each physical works contract is derived from the DE, prior to issuing the tender documents. The engineer’s estimate is to reflect the expected tender price and will be used for making comparisons during the tender evaluation period. Construction estimate (CE) – prepared during the tender evaluation period and updated at least quarterly during the construction phase until project completion. The estimate is based on the preferred physical works tender(s) and is used to confirm that construction funding allocations are sufficient. Note that the CE is a construction phase cost estimate with both the I&R and D&PD phase costs set to nil.

The CE includes an expected estimate and a 95th percentile estimate. The CE also includes escalation and information received during the physical works tender process. All risks must be reviewed, based on the preferred tender and any new issues that arise from the selection of the physical works contractor(s). The impact of these risks on the out-turn cost must be assessed and included in the estimate.

The CE will be compared with the DE. If there are differences between the estimates, the consultant must explain the reasons in a report to be included when they submit the CE.

Expected estimate The base estimate including an allowance for contingency calculated according to the guidelines in this manual. Note that escalation is only included in the expected estimate when it is used for funding applications. Reference to the expected estimate in this manual will generally exclude allowance for escalation.

Funding applications Funding applications are required prior to undertaking these phases of a project:

I&R

D&PD

construction (management, surveillance and quality assurance (MSQA) and physical works).

All funding applications are made at the expected estimate level (and include advice of the 95th percentile estimates). Future escalation is added to these estimates.

The NZTA also needs the expected and 95th percentile estimates (including future escalation) for the purchase of property interests required to build the project.

In addition, all funding applications (I&R, D&PD and construction phases) for projects where the expected estimate of the construction phase of the project exceeds $4.5 million are accompanied by a separate estimate for the construction phase (including all property costs) of the project. This estimate includes the expected, 5th and 95th percentile estimates and excludes escalation.

Funding risk An additional provision for known/unknown risk between the expected and 95th percentile estimates. This allowance is to cover the difference between the statistical mean and the statistical 95 percent percentile of risks and opportunities.

Out-turn cost These costs include all actual costs. The only exclusions are the goods and services tax (GST) and any NZTA’s administration and overhead costs. The NZTA-managed costs, as defined below, are to be included in the out-turn cost. Project cost centre Cost centre for project costs, excluding property acquisition (as defined in project property cost centre below) but

including property owner accommodation works that form part of the physical work contract. Project property cost

centre

Cost centre for project property costs including property acquisition, property compensation, property owner

accommodation works (unless these are deferred to construction in which case they are charged against the project cost centre) and professional services costs (including valuations, legal surveys and management costs).

Sunk costs Costs irrevocably committed which have no salvage value or realisable value (for example investigation, research and design costs already incurred). Sunk costs are included in an out-turn cost but are not included in economic evaluations. Note that property costs are not normally a sunk cost as it nearly always has a market value that can be realised. However, costs such as property owner accommodation works are not normally recoverable and will be a sunk cost. NZTA-managed costs Includes all project costs incurred by the NZTA that are not managed by the consultant and that are not part of the

NZTA’s administration costs.

The NZTA’s project manager will provide these cost estimates to the consultant responsible for the project estimate. 5th percentile

estimate

Note that the 5th percentile estimate is only required for funding applications, and only in relation to the estimate of construction and property costs.

95th percentile estimate

The expected estimate plus an allowance for funding risk, calculated according to the guidelines in this manual. Note that future escalation is only included in the 95th percentile estimate when it is used for funding applications. Reference to the 95th percentile estimate in this manual will generally exclude allowance for future escalation.

95th percentile risk contingency

NZ Transport Agency’s Cost estimation manual (SM014)

2.2

Abbreviations

ACENZ Association of Consulting Engineers New Zealand AEE Assessment of environmental effects

BCR Benefit cost ratio

CE Construction estimate

CI Cost indices

D&PD Design and project documentation

DE Design estimate

FE Feasibility estimate

FCWP Forward capital works programme (now 10-year forecast) HNO Highways and Network Operations group

I&R Investigation and reporting LTPP NZTA’s Long Term Procurement Plan

MSQA Management, surveillance and quality assurance NOR Notice of requirement for designation

OE Option estimate

PADS Property acquisition and disposal system

PE Pre-design estimate

PFR Project feasibility report

PROMAN State Highway Project Financial Management System

SAR Scheme assessment report

SE Scheme estimate

SEP Schedule of elemental prices

3.0

Estimate definitions

3.1

General

There will normally be six out-turn cost estimates within the project development cycle:

1. feasibility estimate (FE)

2. option estimate (OE)

3. scheme estimate (SE)

4. pre-design estimate (PE)

5. design estimate (DE)

6. construction estimate (CE).

There will be two types of estimates for each of the above six cost estimates: 1. The expected estimate (ie on average, across the State Highway Programme,

about half of the time the out-turn cost will come in under the expected estimate and about half of the time the expected estimate will be exceeded).

2. The 95th percentile estimate (ie one in 20 times the 95th percentile estimate will be exceeded).

All cost estimates shall include an assessment of all residual risks (from the risk register) at the time of estimating.

NZ Transport Agency’s Cost estimation manual (SM014)

3.2

Project life cycle

Most projects are developed in four separate phases: 1. Project feasibility.

2. Investigation and reporting (I&R): o scoping

o scheme assessment report (SAR) and/or assessment of environmental effects (AEE)

o notice of requirement for designation (NOR) and resource consents. 3. Design and project documentation (D&PD).

4. Construction (management, surveillance and quality assurance (MSQA) and physical works).

The NZTA applies hold points at various stages of a project, typically at the end of each of the above phases and at other critical milestones. For the success of the project reliable cost estimates are required at each of these hold points.

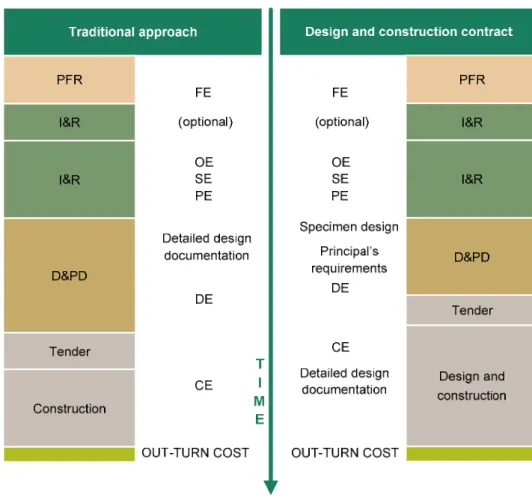

The following diagram of timelines shows the project phases from inception to completion for traditional and design/construct procurement models, and how estimates fit into the life cycle.

Figure 1: Traditional and design and construction contract delivery timeline with estimate deliverable

Each project has one ‘live’ estimate, which is updated progressively as the project develops. This estimate is given different names depending on the project phase or the hold point to which it relates. During the earliest phases of a project more than one OE may be prepared to allow for a number of potential solutions for the project.

1. Project feasibility

The project feasibility phase concludes with the production of a project feasibility report (PFR) and an associated FE. Usually the FE is based on limited knowledge of the project.

2. I&R

The I&R phase includes the development of a scoping report, if required, and a SAR/AEE.

The scoping report summarises the various options and includes OE(s) for each option proposed. A scoping report is not always required.

A SE is prepared during the SAR/AEE production but before the NOR is lodged. The project estimate has to be recalculated once the designation is confirmed and all of the conditions are fully understood. This estimate is the PE that the NZTA will use to secure funding for the design phase.

3. D&PD

Once an option is approved it will progress to detailed design. At the end of this phase a DE is produced and used to secure construction phase funding.

4. Construction

During this phase the design is tendered out to the market. After receipt of tenders and before the contract is awarded, the estimate will be revised to a CE, which the NZTA’s project manager and the consultant then manage until completion of the project.

NZ Transport Agency’s Cost estimation manual (SM014)

Part B – Roles and responsibilities

4.0 Roles and responsibilities 14

4.0

Roles and responsibilities

Each project shall have the following management structure:

The NZ Transport Agency’s (NZTA) project manager is responsible for: – checking that the estimate has been produced according to the guidance given

in this manual

– implementing external peer reviews and parallel estimates at appropriate times – providing cost information for the NZTA-managed costs on previous project

expenditure

– benchmarking estimates against elemental cost data.

The consultant team leader is responsible for:

– establishing the scope of work in consultation with the NZTA’s project manager – preparing and checking the estimate according to the guidance given in this

manual

– collating estimate elements

– checking the estimate is consistent with the scope of works and guidance given in this manual

– internal peer reviewing estimates

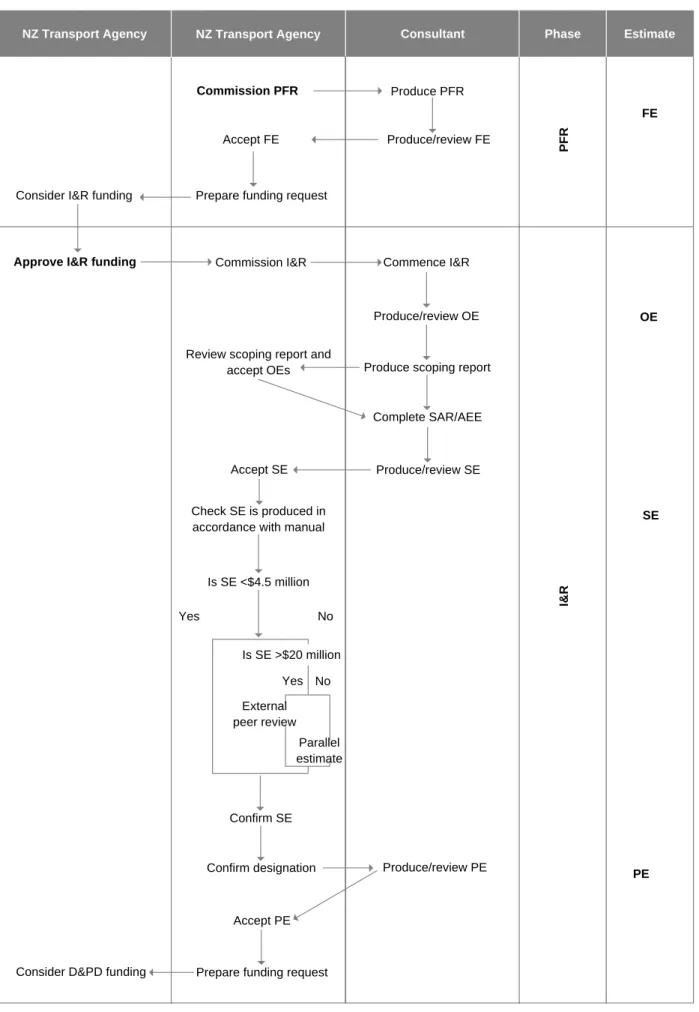

– reconciling differences with external peer reviewer and independent estimator. See figure 2 for a flow chart of the complete project management structure of a typical project from project feasibility report (PFR) to completion.

NZ Transport Agency’s Cost estimation manual (SM014) Figure 2: Project management structure

NZ Transport Agency NZ Transport Agency Consultant Phase

Commission PFR

Estimate

Produce PFR

Accept FE Produce/review FE

Prepare funding request Consider I&R funding

PFR

FE

Approve I&R funding Commission I&R Commence I&R

Produce/review OE

Produce scoping report

Complete SAR/AEE

Produce/review SE Review scoping report and

accept OEs

Accept SE

Check SE is produced in accordance with manual

Is SE <$4.5 million Yes No Is SE >$20 million Parallel estimate External peer review Yes No Confirm SE Confirm designation Accept PE

Prepare funding request Consider D&PD funding

Produce/review PE

I&R

OE

SE

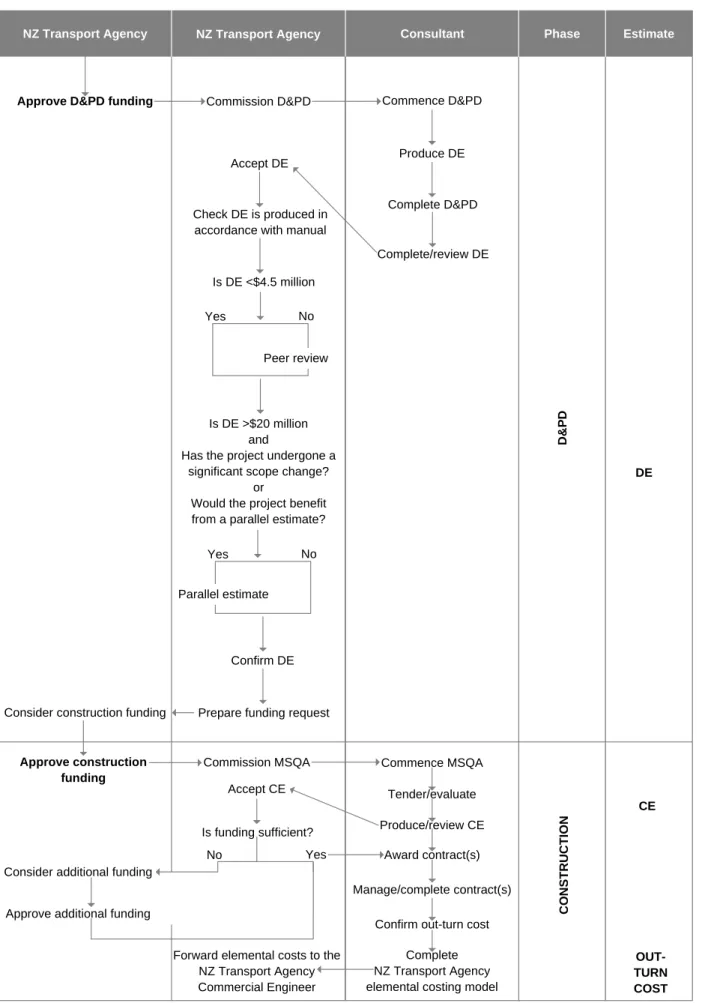

Figure 2: Project management structure continued

NZ Transport Agency NZ Transport Agency Consultant Phase Estimate

Approve D&PD funding Commission D&PD Commence D&PD

Produce DE

Complete D&PD

Complete/review DE Accept DE

Check DE is produced in accordance with manual

Is DE <$4.5 million

Yes No

Peer review

Is DE >$20 million and

Has the project undergone a significant scope change?

or

Would the project benefit from a parallel estimate?

Yes No

Parallel estimate

Confirm DE

Prepare funding request Consider construction funding

Commence MSQA Tender/evaluate Produce/review CE

Award contract(s) Manage/complete contract(s)

Confirm out-turn cost Complete NZ Transport Agency Commission MSQA

Accept CE

Is funding sufficient?

Consider additional funding

Approve additional funding

No Yes

Forward elemental costs to the NZ Transport Agency Approve construction funding D& PD DE CO NST R U C T ION CE OUT-TURN

NZ Transport Agency’s Cost estimation manual (SM014)

Part C – Procedures

5.0 Purpose of cost estimates 19

6.0 Estimates 21

6.1 General 21

6.2 Resource input for estimates 22

6.3 Estimate responsibility and ownership 23

6.4 Consultant performance 23

6.5 Project scope and functionality 24

7.0 Escalation 25

8.0 Land and property 26

8.1 Property purchase 26

8.2 Net property cost 26

8.3 Total property cost 28

8.4 Property acquisition fees 28

9.0 Risk analysis and contingency calculation 29

9.1 General 29

9.2 Terminology 29

9.3 The risk management approach for calculating contingency 30

9.4 Calculating likelihood and consequence 31

9.5 Sensitivity analysis 31 10.0 Reporting estimates 32 10.1 General 32 10.2 Reporting FE and OE 33 10.3 Elemental breakdown 34 10.4 Estimated costs 34

10.5 Funding application 37

10.6 Cash flow/Accrual reporting 37

10.7 Management of contingency 38

10.8 NZTA’s elemental cost database 39

11.0 Estimate audit trail 40

11.1 General 40

11.2 Estimates updates 40

12.0 Peer reviews and parallel estimates 41

12.1 General 41

12.2 Internal peer review 41

12.3 External peer review 42

12.4 Parallel estimates 43

13.0 Scope and cost control process 44

13.1 General 44

13.2 The records 44

13.3 Monthly reporting requirements 44

NZ Transport Agency’s Cost estimation manual (SM014)

5.0

Purpose of cost estimates

Cost estimates are required for:

financial planning programming option selection project specification funding approval committing contracts cost control. Financial planning

The NZ Transport Agency (NZTA) requires cost estimates of all projects in the NZTA’s State Highway Plan to help with financial planning. The NZTA requires expenditure forecasts to be able to advise government of long-term revenue requirements and to arrange alternative funding where appropriate.

Once a particular project is identified and a project feasibility report (PFR) is

completed, the project is programmed according to its priority. The NZTA manages a 10-year forecast using State Highway Project Financial Management System

(PROMAN). The 10-year forecast is continually updated as more information on individual projects is gained and as project priorities change. Any changes to a project estimate are reflected in a change to the 10-year forecast. Each phase of a project is included in the 10-year forecast therefore, reliable estimates of each phase are required. The expected estimate will be used in the 10-year forecast and for long-term financial planning.

Programming

As the Crown agency responsible for planning, developing and operating the state highway network, the NZTA works to achieve government priorities. It is necessary to use funding prioritisation processes based on the NZTA’s allocation process which has a number of criteria. One of these is efficiency, which is largely based on the benefit cost ratio (BCR). This helps to determine the optimum timing of a project. The NZTA’s use of the BCR requires reliable estimates of cost throughout the development of projects so that they can be advanced for investigation, design and ultimately construction at the optimum time.

The expected estimate will be used in the economic analysis. The consultant must undertake a sensitivity analysis of the BCR using the 95th percentile estimate. Option selection

The cost estimates of options are used to select the preferred option for the development of each project. In particular, reliable estimates are required for the differences in option costs to compare with the differences in option benefits.

Estimates of the costs of options are generally required during the investigation phase, initially where options are being shortlisted and later when the preferred option is being selected.

Project specification

The NZTA uses cost estimates to help determine appropriate standards and mitigation measures to be adopted for each project. Care must be exercised to ensure that standards are not changed without adequate consideration of the potential cost impact (direct and indirect).

Funding approval

The NZTA requires reliable cost estimates in order to seek funding approval for these phases:

investigation and reporting (I&R)

design and project documentation (D&PD)

construction (including management, surveillance and quality assurance (MSQA)). The funding allocation for each phase is based on the expected estimate including future escalation. The cash flow forecasts are based on the expected estimate of expenditure in each year. Each funding allocation must also advise the 5th and 95th percentile estimates including future escalation.

All funding applications for projects where the expected estimate of the construction phase of the project exceeds $4.5 million are to include a separate estimate for the construction phase (including all property costs) of the project. This estimate is to include the expected, 5th and 95th percentile estimates.

Committing contracts

The cost estimate is updated once tenders are received and evaluated. By this time, any pricing risk has been closed out and some risks may have changed as a consequence of tender offers. Cost estimates need to be updated following selection of preferred tenders to adjust funding allocations, if necessary, and make appropriate contingency provisions.

Cost control

To maintain optimal programme performance cost estimates, including annual cash flows, need to be continually updated during project delivery. Good cost control is demonstrated through regular (at least quarterly) update of the cost estimate during project delivery.

NZ Transport Agency’s Cost estimation manual (SM014)

6.0

Estimates

6.1

General

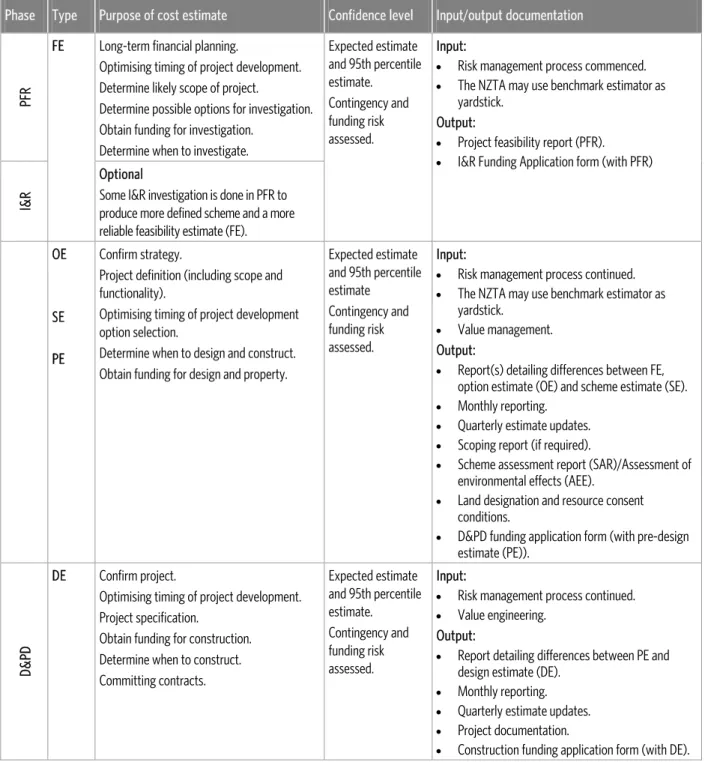

The following figure provides a summary of the type and purpose of each estimate, along with the required confidence levels and input/output documentation.

Figure 3: Purpose, confidence and documentation for estimates

Phase Type Purpose of cost estimate Confidence level Input/output documentation

PFR

Long-term financial planning.

Optimising timing of project development. Determine likely scope of project.

Determine possible options for investigation. Obtain funding for investigation.

Determine when to investigate.

I&R

FE

Optional

Some I&R investigation is done in PFR to produce more defined scheme and a more reliable feasibility estimate (FE).

Expected estimate and 95th percentile estimate. Contingency and funding risk assessed. Input:

Risk management process commenced.

The NZTA may use benchmark estimator as yardstick.

Output:

Project feasibility report (PFR).

I&R Funding Application form (with PFR)

OE

SE PE

Confirm strategy.

Project definition (including scope and functionality).

Optimising timing of project development option selection.

Determine when to design and construct. Obtain funding for design and property.

Expected estimate and 95th percentile estimate Contingency and funding risk assessed. Input:

Risk management process continued.

The NZTA may use benchmark estimator as yardstick.

Value management. Output:

Report(s) detailing differences between FE, option estimate (OE) and scheme estimate (SE).

Monthly reporting.

Quarterly estimate updates.

Scoping report (if required).

Scheme assessment report (SAR)/Assessment of environmental effects (AEE).

Land designation and resource consent conditions.

D&PD funding application form (with pre-design estimate (PE)).

D&PD

DE Confirm project.

Optimising timing of project development. Project specification.

Obtain funding for construction. Determine when to construct. Committing contracts. Expected estimate and 95th percentile estimate. Contingency and funding risk assessed. Input:

Risk management process continued.

Value engineering. Output:

Report detailing differences between PE and design estimate (DE).

Monthly reporting.

Quarterly estimate updates.

Project documentation.

Figure 3: Purpose, confidence and documentation for estimates continued

Phase Type Purpose of cost estimate Confidence level Input/output documentation

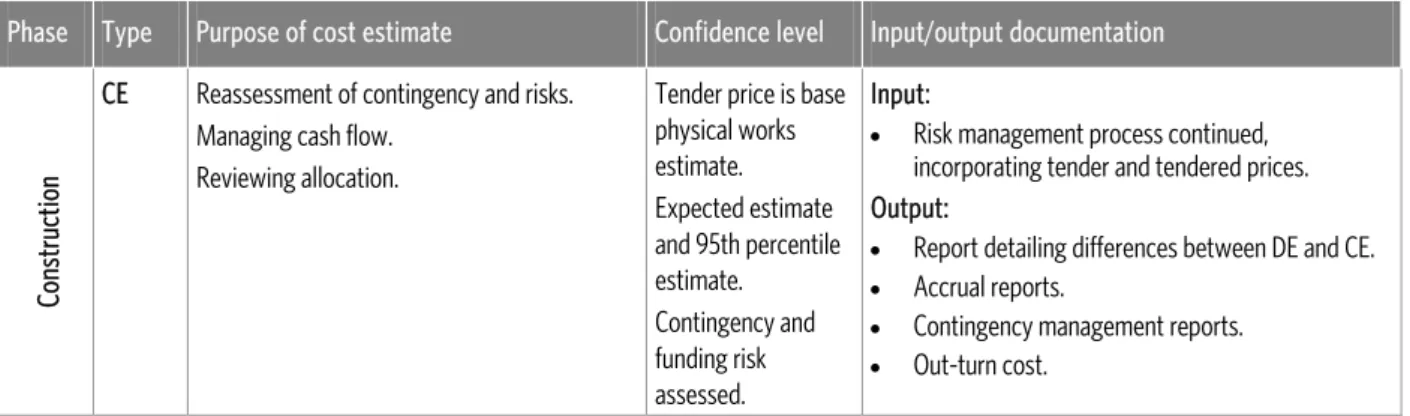

Construction

CE Reassessment of contingency and risks. Managing cash flow.

Reviewing allocation.

Tender price is base physical works estimate. Expected estimate and 95th percentile estimate. Contingency and funding risk assessed. Input:

Risk management process continued, incorporating tender and tendered prices. Output:

Report detailing differences between DE and CE.

Accrual reports.

Contingency management reports.

Out-turn cost.

The estimate life cycle of a project is illustrated below, together with the perceived amount of risk at each phase.

Figure 4: Estimate life cycle with indicative uncertainty curves

6.2

Resource input for estimates

The estimate is critical to the successful development and delivery of a project. When planning or pricing consultancy services, the NZTA’s project manager and the consultant must allow sufficient time and resources to reflect the importance of the estimate. FE OE SE PE DE CE Cost Project completion Timeline Expected cost

Optimistic cost estimate

NZ Transport Agency’s Cost estimation manual (SM014)

6.3

Estimate responsibility and ownership

6.3.1Estimate responsibility

The consultant is responsible for the estimates prepared during the phase(s) for which they are commissioned.

If an up-to-date estimate is requested before the consultant has prepared the phase estimate(s), the consultant is to provide the previous estimate, having updated it to include any cost indices (CI) movement, changes in scope and assumptions.

The project team is responsible for preparing reliable base estimates for the elemental sections of an estimate. However, the consultant is responsible for the overall

compilation, completeness and accuracy of the estimate.

The NZTA’s project manager will provide all actual cost information from the previous project phase(s). These will be recorded in future estimates. Commercially sensitive information, such as professional fees, shall be provided as a total element cost instead of a full breakdown.

6.3.2Estimate ownership

The entire project team must take ownership of the estimate and ‘buy-in’ to the estimate.

6.4

Consultant’s performance

Association of Consulting Engineers New Zealand (ACENZ) and the NZTA have agreed that the NZTA will assess the performance of consultants based on their track record in estimating costs. The NZTA will monitor cost estimates against subsequent estimates and final out-turn costs.

The NZTA intends to publish the accuracy of estimates. The pricing indicator of estimating performance will be the construction cost estimate at out-turn and the DE measured against the SE.

The NZTA will also measure the out-turn cost against the FE although this will not be a performance measure. While it is inherently recognised the FE is based on an ‘educated guess’ particularly for larger transportation problems, the industry needs to note the FE is used to allocate I&R funds.

6.5

Project scope and functionality

The starting point for any estimate is definition of the project scope and functionality. Scope and function definition requires an understanding of the project objectives and the means by which those objectives will be delivered. One key element of this is the programme for development and delivery of the project. All time-related costs must take account of the risk-adjusted programme for the project. The NZTA’s Risk management process manual (AC/Man/2) describes the process for developing risk-adjusted programmes.

The amount of information available and hence the degree of scope and function definition achievable, varies depending on the phase of the project. Adequate

contingency must be allowed for changes in standards, particularly where development of the project is expected to take a number of years.

Definition of project scope and functionality is an important aspect of producing a reliable estimate. It is essential that, even at the project feasibility phase, the project scope and functionality is known and understood in sufficient detail to allow the production of a meaningful estimate. Any changes in scope or functionality need to be recorded and agreed in order to provide an audit trail through the life cycle of the project estimate.

Project estimates must take into consideration project scope creep, for example update of the NZTA’s Geometric design manual. If this is impractical, consultants must qualify project estimates or specifically exclude these items from the project estimate. This will ensure that the NZTA can fully understand the limitations of the current scope of works and therefore, the project estimate.

The NZTA will monitor the variations between FE and out-turn cost across the project portfolio.

NZ Transport Agency’s Cost estimation manual (SM014)

7.0

Escalation

An allowance is to be provided in the expected estimates, 5th and 95th percentile estimates in all funding applications and construction estimates (CE) to cover the risk of escalating costs, commonly referred to as escalation.

Escalation is calculated cumulatively for the balance of the predicted project life cycle. Consultants need to assess the future escalation risks for the project’s cash flow and delivery timing. Escalation shall be applied from the date of the estimate preparation, through to the expected completion of the project.

In preparing the future escalation for an estimate the consultant shall consider the following:

The amount of escalation occurring between preparation of estimate and close of tenders.

Any transference of escalation risk to the supplier post-tender close.

The retention of escalation risk by the NZTA post-tender close provided under the cost fluctuation provisions.

The consultant shall allow within the base estimate for any changes to market rates since the initial estimate was prepared.

Expected estimates, without the addition of future escalation, shall be used for long-term programming purposes. The NZTA will escalate expected estimates to common base dates for portfolio analyses and update them.

Expected estimates with the addition of future escalation shall be used for application of professional services (I&R and D&PD) and construction funds.

To be consistent with the NZTA’s Economic evaluation manual (EEM) escalation is excluded from any economic analyses (BCR).

Appendix D contains example funding application forms. Refer to appendix G for an escalation calculation example.

8.0

Land and property

8.1

Property purchase

The NZTA runs two separate cost centres for any particular project:

project cost centre

project property cost centre.

The project cost estimate includes cost items funded from both of the above cost centres.

Applications to the NZTA for project cost centre funding normally exclude any costs associated with property purchase (eg valuations, legal surveys, management, acquisitions and compensation fees) but normally include property owner

accommodation works to be undertaken as part of the project physical works contract. The NZTA is block-funded nationally for property acquisition and any project property cost centre needs to be prioritised within this fund. Nevertheless, property purchase costs are an important component of a project cost and the NZTA has its own system – Property Acquisition and Disposal System (PADS) – to manage these costs.

The Crown purchases property interests so that the NZTA can carry out its statutory functions and responsibilities in developing New Zealand’s state highway network. Currently those interests are acquired using the provisions of the Public Works Act 1981 (the Act). The Act’s provisions take a number of forms but primarily involve the acquisition of the freehold or leasehold title. Acquisition of these interests and the settling of compensation issues normally involve costs that need to be included in the project cost estimates.

The NZTA uses the services of specialists in the Act to conduct Crown property acquisition negotiations. This ensures that property owners are correctly informed of their rights. As described in the NZTA’s State highway professional services contract proforma manual (SM030) project managers, consultants and property advisers are to work together closely when assessing project property estimates.

It is necessary to estimate the:

nett property cost – used for project cost estimates and economic evaluation

total property costs – used for establishing the project property cost centre budgets

property acquisition agent’s fees.

8.2

Net property cost

8.2.1 General Property costs required for the project estimate and the project’s economic evaluation can be divided into:

nett property costs

property compensation costs

NZ Transport Agency’s Cost estimation manual (SM014) 8.2.2 Net

property costs

Nett property cost is defined as the market value, at the base date, of any property required to be purchased for a project, plus the out-turn cost (obtained from PADS) of any property already purchased for a project, less the market value of any surplus property, ie nett property only includes the corridor required.

For economic evaluation purposes, the NZTA’s Economic evaluation manual (EEM) states that where property has to be acquired, its resource cost is assumed to equate to its market value1. Similarly, where property becomes available for disposal, it is

included as a cost saving in the economic evaluation.

The nett property cost shall be included in the total project out-turn cost and therefore, updated in parallel with the project estimate phases.

8.2.3 Property compensation costs

In certain circumstances the Act considers other losses apart from the market value of the property taken. This is termed ‘property compensation’ and may include:

permanent depreciation in the value of any remaining property and improvements (injurious affection) caused by the taking of the required property

costs or reinstatement of physical damage to land and/or buildings arising from the construction of the public works

additional compensation for loss that results from the acquisition, provided it is not ‘too remote’ and is the natural and reasonable consequence of the public works (disturbance)

professional fees reimbursement (excluding property acquisition agents fees)

loss of actual business profit

solatium payment (only applies to total purchase of property where residences are occupied by the owner)

temporary occupation of property outside the corridor required.

This list is not exhaustive and expert advice should be sought to determine all relevant compensation costs and make due allowance in the estimates.

It may be necessary to also compensate for disturbance and/or damage to various interests resulting from construction contracts. These costs are not normally planned for but the consultant should consider the particular risk of this happening.

8.2.4 Property owner

accommodation works costs

During the property acquisition process, the NZTA may agree to carry out works as part of a property purchase or compensation agreement. For instance, an agreement might require the NZTA to erect fencing or construct driveways before or during construction of the project.

This work may be either a property compensation cost that has been deferred until construction or it could be an extra item agreed in lieu of property, or compensation entitlement. This work may be included in a subsequent physical works contract as ‘property owner accommodation works’ with a due allowance included in the project construction cost estimate. It is preferable that all property owner accommodation works be funded from the project cost centre.

The consultant must identify these accommodation works separately in the cost estimates.

1 Market value: The current achievable sale price of the land/property based on the doctrine of willing buyer/willing seller relative to its size,

8.3

Total property cost

At the outset of a project, the NZTA needs to understand the amount of funding necessary to purchase the property required for the project. This is necessary to set the budget for the project property cost centre and for programming purposes. This estimate data is entered into the NZTA’s PROMAN (via Project Setup – Property Tab – Total Property Cost column) and allows the NZTA to collectively consider all project property cost centres competing for funding, and make decisions on when individual property interests can be purchased.

It is not always possible to purchase only the portions of property required for a proposed new road corridor. In some instances it is necessary to buy entire properties to secure the road corridor required. In these cases the remaining property will at some stage be declared surplus and sold. The realisable value of the surplus property is not credited to the particular project property cost centre of the specific project but it is credited to the collective property block fund.

The estimated cost of the property will usually be derived following the development of a property purchase strategy in conjunction with the NZTA’s property acquisition agent.

8.4

Property acquisition fees

Property acquisition fees may include:

property acquisition agent’s fees

other professional fees, eg the NZTA’s legal, valuation, specialists and survey fees

Land Information New Zealand (LINZ) title and other disbursements

advertising, eg section 23 notices.

All of these fees shall be separately and individually identified in the I&R, D&PD and construction phase estimates under consultancy fees. Note that as these are property purchase costs, they will normally be funded from the project property cost centre.

NZ Transport Agency’s Cost estimation manual (SM014)

9.0

Risk analysis and contingency calculation

9.1

General

This manual is supplementary to the NZTA’s Risk management process manual

(AC/Man/2) which describes the risk management process to be followed for the NZTA’s projects.

For cost estimation purposes risk is defined as the chance of something happening that will have a beneficial or detrimental impact on the final out-turn cost. Both the

consequence and likelihood of the risk needs to be assessed.

Application for increases for I&R, D&PD and construction phases will be treated as an increase through the NZTA’s review process. The risk profile should be used as supporting information for the application for an increase in the allocation.

9.2

Terminology

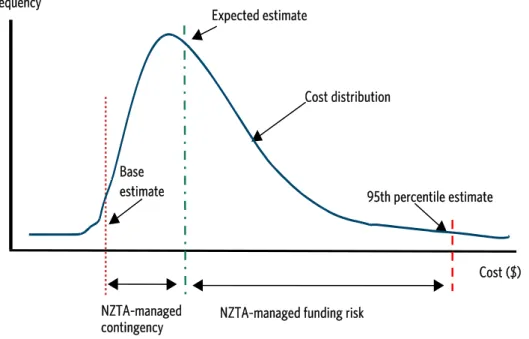

The figure below shows the terminology used for risk-adjusted cost estimates.

Figure 5: Risk-adjusted cost estimate terminology

Cost distribution Expected estimate 95th percentile estimate Base estimate NZTA-managed contingency

NZTA-managed funding risk

Cost ($) Frequency

9.3

The risk management approach for calculating contingency

The following figure details the risk management approach that shall be used to calculate contingency and funding risk at the various phases of the project life cycle. Note: Segment values are the construction phase costs of the expected estimate.Estimate < $4.5 million $4.5–$10 million > $10 million

FE Informal/General General General

OE Informal/General General/Advanced General/Advanced

SE General General/Advanced Advanced

PE General Advanced Advanced

DE General Advanced Advanced

CE General Advanced Advanced

Figure 6: Use of informal, general or advanced approach to risk management

Where informal/general or general/advanced is detailed as the applicable approach, the NZTA’s project manager shall determine the most appropriate of the two approaches.

9.3.1Informal approach

The informal approach consists of the management of existing procedures and controls. It is applied where the formal risk management process is not necessary – either because existing procedures and controls are adequately managing the risk or because the risks have minimal effect on the attainment of the project objectives. The informal approach would usually be appropriate where the activity:

has an expected cost estimate less than $100,000

is short-term, eg less than six months in durations

is routine and follows a well-proven process, eg business planning

has little or no effect on the NZTA’s goals and objectives. 9.3.2General

approach

The general approach is to be used for all NZTA’s projects where the informal

approach is not used. This approach to risk management is a qualitative approach. It is targeted at achieving the appropriate management of opportunities and threats, through the systematic application of generalised risk management processes and qualitative tools.

Where the general approach is used to calculate contingency and funding risk, the risks must be identified, analysed and evaluated according to the qualitative general

approach specified in the NZTA’s Risk management process manual (AC/Man/2). The consultant needs to assess the impact on the estimate and include an appropriate contingency and funding risk allowance in the estimate. This assessment can be based on percentages or lump sums but must recognise the impact the identified risks may have on the out-turn cost.

NZ Transport Agency’s Cost estimation manual (SM014) 9.3.3Advanced

approach

The advanced approach is quantitative. It is based around the modelling of individual risks to provide greater levels of certainty and confidence.

Where the advanced approach is used to calculate contingency and funding risk, the consultant is to analyse and evaluate risks according to the quantitative advanced approach specified in the NZTA’s Risk management process manual (AC/Man/2). The advanced approach should also be used where the general approach reports a significant risk. The existence of one extreme risk or five very high risks within a project indicates a significant risk.

Risk impacts have to be quantified to produce an analytical outcome based on Monte Carlo simulation techniques. Software such as Crystal Ball, @RISK and Analytica may be used.

9.4

Calculating likelihood and consequence

The NZTA’s Risk management process manual (AC/Man/2) details the processes required to provide contingency and funding risk allocations within cost estimates for each of the above approaches, and contains the NZTA’s standard tables for rating likelihoods and consequences.

9.5

Sensitivity analysis

The consultant is required to undertake a sensitivity analysis to identify the risks that have the greatest impact on the expected estimate. The consultant must use linear regression theory to undertake the sensitivity analysis, and use the outcomes to rank the risks in terms of largest financial risk to the expected estimate. The report must include the sensitivity analysis and comments on the results, including treatment and mitigation plans for large financial and programme risk items.

The consultant is required to show all results in tabular or graph form. These need to include outputs for each phase, ie I&R, property purchase, D&PD and construction, as well as the total project out-turn.

10.0

Reporting estimates

10.1

General

Cost estimates need to be prepared and presented using a standardised industry format. This is essential to improve understanding of estimates and to reduce the risk of items being left out of presented costs.

Consultants are to use the templates included in this manual:

Elemental breakdown (appendix B).

Estimated costs (appendix C).

Funding applications (appendix D).

Cash flow/accrual reporting (appendix E).

Elemental cost database (appendix F).

Cost reporting and scope management (appendix H).

For projects incorporating a number of contracts, the consultant will present each contract separately and then summarise all the contracts on a main form. This provides a ready reference from which an overall understanding of the estimated/actual out-turn cost for a project can be gained.

All cost estimates shall be accompanied by a report that as a minimum shall include:

scope and functionality statement and assumptions

the base estimate

the risk register

the risk-adjusted programme

residual risks for costing

the pricing of residual risks

expected and 95th percentile estimates

date and cost index

ranked sensitivity analysis on risks that have the greatest financial impact

exclusions and assumptions

NZ Transport Agency’s Cost estimation manual (SM014)

10.2

Reporting FE and OE

It is important that the full cost range for a project is reported accurately from the conception of the project. During the period from conception to the selection of a preferred option, it is important that the project’s estimate, contingency and funding risk is not limited to one option and ranges over the entire scope of potential options. In undertaking this, the consultant is required to report all options considered, including the preferred option and the probability for each option being the successful outcome for the project.

This is particularly important in the following circumstances:

Block projects, where any option will take the expected estimate for the project over the block cost threshold ($4.5 million).

Projects with an expected estimate between $4.5 million and $10 million, where there is a difference between any two options of 20 percent or more.

Projects where the probability of the preferred option being carried through to delivery is less than 50 percent.

All projects with an expected estimate of $10 million or more.

For the scenarios identified above, the consultant shall provide an overall probability curve, overlaid on all the individual option probability curves for the project.

In addition to the graph, the consultant shall ensure that the assumptions, probabilities and descriptions of each of the options, and the overall curve are described on the same page as the graph. This is to reduce the possibility of premature reduction of the large tail (funding risk) of the overall project curve before the SE is completed. This information shall be incorporated into the estimate report until the project has a confirmed option (ie reaches the SE stage).

95th percentile estimate

$45 million $25 million

Option A: ‘preferred’ 60% probability of being able to achieve

Overall project curve

Option B: 25% probability of being able to achieve Project ML ML ML Option C: 15% probability of being able to achieve $10 million $5 million B A $30 million ML C $15 million

10.3

Elemental breakdown

The example elemental breakdown form presents the estimated out-turn cost for a project. The form is designed to be consistent with the elemental cost information that the NZTA holds at a national level for each element.

The consultant is required to use an elemental breakdown form to prepare an estimate, and to supply it to the peer reviewer, and the NZTA’s project manager so they can understand what is included in the out-turn cost estimate.

10.4

Estimated costs

10.4.1Estimated property

acquisition costs

Example forms are included in the appendices to present the estimated project property costs and the total purchase cost of property.

The consultant is to use a project property cost form for economic analysis. The project property cost is to be included in the project estimate as a single-line item. The

consultant shall get assistance from the NZTA’s property acquisition agent to estimate the nett and total project property costs.

A total purchase cost of property form must be submitted to identify the cash flow required for the purchase of property.

10.4.2Summary

of estimated costs

The consultant must use the appropriate form for the phase of the project life cycle to report the estimated costs. More information as to which form to use is detailed in section 3 of this manual. Appendix C contains example forms for the following project estimates: FE OE SE PE DE CE.

The I&R, D&PD and MSQA fee sections are to be rolled up and summarised as single-line items. Physical works must be broken down into the element headings for a project. 10.4.3Project

estimates

These are required at different stages of the development of a project:

FE (form A) OE (form B) SE (form C) PE (form D) DE (form E) CE (form F).

NZ Transport Agency’s Cost estimation manual (SM014) 10.4.3 Project

estimates continued

Property costs are to be estimated by the property acquisition agent.

Professional services fees (I&R, D&PD and MSQA) to be estimated as a percentage of the physical works estimate only at the early phases of the project (FE, OE and SE). For all other phases of the project a detailed estimate of these costs is required.

Estimates for the NZTA-managed costs and consent monitoring fees to be provided by the NZTA’s project manager.

Fees are removed from the project estimate as and when they become sunk costs. Estimates calculated on these forms are as at the date of the estimate and include no allowance for escalation.

10.4.4Project phase estimates and contract estimates

These are required when ready to seek a funding allocation for any contract and forms G, H and I are used depending on the phase of the project being contracted. The NZTA-calculated base contract estimate (for professional services) or the consultants-calculated base contract estimate (for physical works) are used to complete the assessment of the funding allocation required.

Once funding has been approved, evaluation of the tenders completed and a preferred tenderer’s price available, these forms are updated by inserting the tender price in box A, replacing the previous base contract estimate. The NZTA’s project manager (for professional services) and the consultant (for physical works) will reassess the adequacy of the previously assessed allowances for contingencies and confirm the expected contract estimate and the expected phase estimates. These reassessed estimates are transferred to appendix V of the NZTA’s Contract procedures manual

10.4.5Capital project estimating – Navigation diagram Project estimate(2) Project I&R Phase estimate Project D&PD Phase estimate Project construction Phase estimate Land purchase estimate

I&R contract estimate(1)

I&R phase NZTA-managed costs

D&PD contract estimate(1)

D&PD phase NZTA-managed costs

MSQA contract estimate(1)

Construction phase NZTA-managed costs and consent monitoring fees Physical works contract estimate

Base contract estimate (in RFT) Contingencies and escalation estimate

Funding risk estimate

Base contract estimate (in RFT) Contingencies and escalation estimate

Funding risk estimate

Base contract estimate (in RFT) Contingencies and escalation estimate

Funding risk estimate

Base contract estimate (in RFT) Contingencies and escalation estimate

Funding risk estimate

Expected I&R Contract estimate 95% I&R contract estimate

Expected D&PD Contract estimate

95% D&PD contract estimate

Expected MSQA Contract estimate 95% contract estimate

Expected physical works Contract estimate

95% physical works contract estimate

(1) Professional services may be contracted in one or multiple contracts, ie the I&R, D&PD and MSQA project phases, and may be combined into one contract estimate. (2) The project estimate at the end of the PFR is the FE as per the NZTA’s Cost estimation manual (SM014).

The project estimate at the end of the scoping phase is the OE as per SM014.

The project estimate at the end of the I&R phase is the SE as per SM014 with I&R costs sunk to nil.

The project estimate at the commencement of the D&PD phase is the PE as per SM014 with I&R costs sunk to nil. The project estimate at the end of the D&PD phase is the DE as per SM014 with I&R and D&PD costs sunk to nil.

NZ Transport Agency’s Cost estimation manual (SM014)

10.5

Funding application

The consultant must use a funding application form to present estimates. The NZTA uses these to obtain funding approval. Example funding forms are included in the appendices for the following funding submissions:

I&R (submitted with PFR)

D&PD (submitted with PE)

construction (submitted with DE).

All funding applications for projects over the block cost threshold ($4.5 million) are to be accompanied by a separate estimate of the construction phase of the project. This estimate is to include all property costs and show the expected, 5th and 95th percentile costs of the construction phase of the project. An example form for this purpose is included in appendix D.

For the majority of projects, there will only be one contract per phase, however, for more complex projects requiring the services of more than one contract, each contract for a phase shall be identified separately on the appropriate funding application form. This will enable the base estimate for each contract to be able to be transferred directly to in appendix V form of the NZTA’s Contract procedures manual (SM021) for tender evaluation and comparison purposes.

During tender evaluation of the contract, after opening the price envelopes, and prior to award, the base estimate, contingency and funding risk for the contract shall be reviewed, taking into account the tender and tender price of the preferred tenderer.

10.6

Cash flow/Accrual reporting

The consultant is to submit with each estimate the likely expenditure of the expected cost estimate (cash flow) over the project life and provide monthly reports of accruals. Definitions of the costs to be included in the monthly reports are:

actual – past years and months

accrual – value of work done this month and to date

forecasts – future months and years

escalation – inflation

total allocation – financial allocation for this phase/project

accepted contract price

retentions held (physical works contracts)

variations

forecast final out-turn cost.

The example form included in appendix E present the cash flow in a format compatible with PROMAN.

Separate cash flows are to be prepared for separate contracts/phases, along with a total report summarising the contracts/phases.

Consultants shall estimate forward cash flows in accordance with a methodology appropriate to the type, scale and stage of the project. One such methodology may include the derivation of a project programme and applying the applicable estimated cost(s) to each individual programme item. For some projects, applying standard‘s curve methodology may be more appropriate.

10.7

Management of contingency

Contingency between the base and expected estimates should be shown as a single-line item in reports. Contingency cannot be transferred from one phase to another on a project as each phase is funded separately.

Figure 7: Contingency management

The NZTA’s State highway professional services contract proforma manual (SM030) provides information for the NZTA’s project manager and the consultant to agree an allocation for each physical works contract that includes the contract price, and an operating contingency over which the consultant has control. However, the consultant is required to report on any high-cost variations and the allocation will be reviewed as the contract progresses.

The NZTA’s project manager manages the contingency allowance. The NZTA manages the funding risk element of the out-turn estimate.

NZTA-managed contingency NZTA-managed funding risk

Base estimate Expected estimate

Consultant operational contingency

NZ Transport Agency’s Cost estimation manual (SM014)

10.8

NZTA’s elemental cost database

The NZTA maintains an elemental cost database wh