Market Data

/ Supplier Selection /

Event Presentations / User Experience

Benchmarking / Best Practice /

Template Files / Trends & Innovation

Integrated Customer

Experience Report

Integrated

Customer

Experience

Report

In association with CACI

Econsultancy London

4th Floor, Farringdon Point 29-35 Farringdon Road London EC1M 3JF United Kingdom Telephone: +44 207 269 1450

Econsultancy New York

350 7th Avenue, Suite 307 New York, NY 10001 United States Telephone: +1 212 971 0630 All rights reserved. No part of this publication may be

reproduced or transmitted in any form or by any means, electronic or mechanical, including photocopy, recording or any information storage and retrieval system, without

Contents

1.

Executive Summary and Highlights ... 5

1.1.

About Econsultancy ... 8

2.

Foreword, by CACI ... 9

2.1.

About CACI Ltd ... 10

3.

Methodology ... 11

4.

Findings ... 12

4.1.

Customer experience strategy ... 12

4.1.1.

Macro-level factors ... 12

4.1.2.

Relevance of customer touch points ... 13

4.1.3.

Commitment to customer experience ... 14

4.1.4.

How well developed is strategy? ... 15

4.1.5.

How integrated is customer experience? ... 16

4.2.

Benefits and barriers ... 17

4.2.1.

Benefits of an integrated customer experience ... 17

4.2.2.

Greatest barriers to improving customer experience ... 18

4.2.3.

Problems relating to integration ... 19

4.3.

Key pillars for success ... 21

4.3.1.

Key areas for delivering an integrated customer

experience ... 21

4.3.2.

How well equipped are organisations across key pillars? ... 23

4.3.3.

Key organisational pillars: criticality versus competence ... 25

4.3.4.

Underlying factors needed for an integrated customer

experience ... 27

4.4.

Technology used for integrated customer experience ... 29

4.5.

Measurement ... 30

4.5.1.

Metrics used to measure effectiveness ... 30

4.5.2.

Use of data to improve customer experience ... 32

4.6.

Ownership and budget ... 34

4.6.1.

Ownership of integrated customer experience ... 34

4.6.2.

Dedicated budget for improving customer experience ... 36

4.6.3.

Budget plans for improving customer experience ... 38

4.7.

Improving customer experience ... 40

4.7.1.

Most significant factor for improving customer

experience ...40

5.

Appendix ... 44

5.1.

Respondent profiles ... 44

5.1.1.

Size of company revenue ... 46

5.1.2.

Business Sector ... 48

5.1.3.

Type of Agency ... 49

58% of companies ‘are

just beginning to

develop customer

experience strategies’

1.

Executive Summary and Highlights

This is the first Integrated Customer Experience Report, published by Econsultancy in association with CACI.

Almost to 900 digital marketing professionals were surveyed online during June and July 2013, to examine how their organisations or clients approach this topic, and what they regard as key factors for success.

The research identified these key findings:

1.

Companies typically lack a strategy for integrated

customer experience

The majority of companies (58%) are still in a position where they are just beginning to develop their strategies for improving the customer experience, a percentage not dissimilar to 2011 when Econsultancy carried out a similar survey.

It is clear that commitment to delivering an integrated customer experience doesn’t necessarily translate into a well developed strategy.

Nine in every 10 companies state that there is at least some level of organisational commitment to delivering

an integrated customer experience, including 43% who say they are ‘very committed’. However, only a fifth (20%) say they have a well-developed strategy in this respect and only 8% of

companies surveyed said they provide a ‘very integrated’ customer experience.

While this may be a cause for concern, the reality is that there has been a disparity between commitment and action for some time.

Research carried out by Econsultancy in 2011 found that a similar proportion of companies (61%) were only ‘just beginning to develop strategies’ for improving the customer experience, while more companies had a well developed strategy (26%). The sheer difficulty and complicated nature of integrating the customer experience is identified as the single greatest barrier to improving the customer experience, with more than half of company respondents (54%) identifying the ‘complexity of the customer experience and number of different touch points’ as one of the top-three challenges, a higher

percentage than for any other barrier. The likelihood of companies having budget dedicated to improving the customer experience is largely unchanged from 2011. One in 10 companies say that they have a ‘single dedicated budget,’

though 6% fewer companies than in 2011 said ‘there is no budget at all’ (21%, down from 27%).

How developed is strategy?

2.

Data, systems and processes: organisations seek to

bridge the competency gap

Despite identifying data and systems & processes as the most critical components for delivering an integrated customer experience, these are the areas where companies are least well equipped. More than six in 10 companies (63%) stated that

‘data (single customer view/customer insight)’ is ‘critical’ for delivering an integrated customer experience, and more than half (54%) said the same for ‘systems and processes’. However, significantly fewer companies rated their ability in these areas as ‘excellent’ or ‘good’. This gap was not evident for ‘people & skills’, ‘company culture’ and ‘organisational structure’.

Instead of data and systems being areas that lay the foundation of customer experience, they are proving to be major stumbling blocks to companies. A common lament for company respondents was the continued use of legacy systems within their organisations, which didn’t allow them to collect sufficient data or integrate information across a growing number of customer touch points.

On a positive note, companies appear to have the intention of transforming these areas into strengths. More than half (54%) of companies with budget for customer experience said they plan to increase their spending on improving ‘data and insight’ over the next year, while 46% are planning to do the same to improve their ‘systems and processes.’

3.

Technology not fit for purpose is hindering development

of customer experience

In order to have a complete view of customer interaction over multiple touch points, organisations need to have the appropriate technological infrastructure.

It is more difficult to integrate data sets when the technology platforms used to operate the different touch points are

disparate and not integrated. However, more than half (51%) of companies are using ‘non-integrated tech platforms’ to deliver an integrated customer experience. In contrast, only 8% of respondents are using a ‘single, integrated platform’. This helps to provide some explanation for the challenges around customer experience, including the ‘number of different touch points’, and ‘difficulty unifying different sources of customer data’.

Criticality versus competence

Use of customer retention

metrics

4.

Marketers must measure the benefits

In a testing economic environment, organisations should be focusing not only on developing an integrated customer experience to create a competitive advantage, but also on both identifying and measuring the benefits.

When asked about the business benefits of an integrated customer experience, the top two

benefits were ‘improved customer retention/brand loyalty’ (88%) and ‘increased sales/improved customer acquisition’ (82%). An integrated customer experience will not only have a positive effect on the amount of new custom companies can attract, but it will also help to create repeat sales. However, companies must make sure they have the appropriate metrics in place to prove these business benefits.

The percentage of companies that use customer retention/loyalty to directly measure the effectiveness of the customer experience has dropped by 11% from two years ago. Only 54% of

company respondents still use retention as a metric for measuring the effectiveness of the customer experience. Failure to have the right metrics in place could damage the business case for further improvement. Given the impact of the economic backdrop, this could be critical to business success.

The context of the economic climate continues to have a profound impact on how businesses plan and execute their activities. Unsurprisingly, the biggest influence on

organisational direction and strategy among the company respondents is the ‘economic envir0nment’ (43%), showing that the realities of the economy are top of mind for many companies when it comes to business planning and prioritisation.

Organisations that are committing to delivering an

integrated customer service need to take a long-term view. Although the project may be capital-intensive in the short term, the longer term payoff could be competitive

advantage in a tough business environment. More soberingly, it could also be argued that an integrated customer experience is becoming a hygiene factor, rather than an opportunity to differentiate.

5.

Individual web-related data is being underutilised

As well as looking more generally at theimportance of data at an overall level, the research also looks at the use of specific sources of data for improving the customer experience.

Companies are far more likely to be using offline CRM data than web analytics data relating to individuals. While aggregated web analytics is the most widely used source of data, only 16% of responding companies use

analytics data tied to individuals

extensively. A further 28% make

‘occasional’ use of this data source. This compares to 30% of responding

companies who use CRM data extensively, and 46% who use it occasionally. Marketers need to keep in mind that consumers increasingly expect a personalised experience, which requires knowledge of online behaviour to help enhance the experience across not just digital but also offline touch points.

For multichannel retailers having to create a consistent experience between physical interactions and digital experiences, it is important for them to gather and use data from all of their channels. While only 12% of all company respondents reported that they use data from ‘electronic point of sale’ (EPOS) data extensively to improve customer experience, this percentage increases to 32% for retail organisations.

Using data from EPOS can help create richer links between in-store behaviour and online behaviour. The implications of this are numerous, from seeing how customers are checking the website before they go in-store, to experimenting with the impact online content may have on the amount customers are willing to pay. Whatever the insights are, using them to improve the integrated customer experience will likely have a positive impact on the overall business performance as well as just the customer experience.

However, all of this is only possible when the organisations are able to pair this information together. For many companies, creating this single-view of customer activity and interaction is not yet possible.

1.1.

About Econsultancy

Econsultancy is a global independent community-based publisher, focused on best practice digital marketing and ecommerce, and used by over 400,000 internet professionals every month. Our hub has 200,000+ subscribers worldwide from clients, agencies and suppliers alike with over 90% subscriber retention rate. We help our subscribers build their internal capabilities via a combination of research reports and how-to guides, training and development, consultancy, face-to-face conferences, forums and professional networking. For the last ten years, our resources have helped subscribers learn, make better decisions, build business cases, find the best suppliers, accelerate their careers and lead the way in best practice and innovation.

Econsultancy has offices in London, New York, Sydney and Singapore and we are a leading provider of digital marketing training and consultancy. We are providing consultancy and custom training extensively across Europe, Asia and the US. We train over 5,000 marketers globally each year.

Join Econsultancy today to learn what’s happening in digital marketing – and what works. Call us to find out more on +44 (0)20 7269 1450 (London) or +1 212 971 0630 (New York). You can also contact us online.

2.

Foreword, by CACI

Delivering an integrated customer experience is not a new challenge; it is something that CACI have been helping a wide range of organisations address for over ten years. Since the advent of call centres, we have seen first-hand the business benefits that can be realised when telephone, mobile, front line staff and digital channels come together into a single experience.

For the majority of organisations the challenges to overcome, as highlighted in this report, have remained similar. They need to be better at integrating data, process, technology and the customer strategy. What is new is that the impact of these individual challenges is accelerating with the increase in channels, data and organisational silos.

Overcoming these challenges has always offered a compelling prize; the improvement of all the key customer value drivers across acquisition, retention and cross sales. However, what this report confirms is that although organisations perceive an integrated customer experience to be important, this does not necessarily translate into a focused effort to enhance it.

So the key question is: if your organisation didn’t feel compelled to address the need for an integrated customer experience previously, what needs to change in order for it to happen now? Overall, we have found that the guiding principles about how to progress in this area have remained consistent:

You need to have an ambitious, integrated cross-channel vision with a pragmatic and incremental approach to achieving it.

Your approach needs to be driven by delivering measurable, incremental business value. – The measures used need to be specific to what you are going to do and what the outcomes

are going to be.

– Silos, both in relation to data, digital and business functions lead to duplication and inefficiencies. Benefits should include cost savings as well as revenue generation. You need to make an informed decision on where to start i.e.

– Do the smaller/quicker/cheaper thing that builds momentum and shows results? – Do the bigger/harder/expensive thing that will make a big difference when it arrives? – If you have a choice then it normally makes sense to start smaller. Our experience is that

the focus on short-term value has always been the norm and demonstrating success early has been key.

– Be careful not to focus on something that seems attractive (e.g. social), but has less immediate commercial value.

You need to be flexible.

– Integrating the customer experience is transformational and will need to adapt over time. – Positioning as an enabler for the wider business as opposed to a blocker is key.

– Regularly re-assessing where the key value opportunities are. Make it clear this is not solely a technology project.

– The business change is often more challenging than the technology requirements. – Overcoming organisational silos typically requires new levels of collaboration across the

business.

– Integrating processes means peoples roles will change along with the skills required. – Timely access to relevant data (be that web, social or customer) is critical to integration.

In reality an organisation’s integrated customer experience will always be a work in progress. There will continue to be new data, new channels and conflicting business priorities.

Focusing on meeting this challenge is one that is proven to unlock value for companies, both in the short and long term, regardless of sector. It is also critical to being ‘fit for purpose’ to operate effectively in the future marketplace. Success is determined by an effective combination of data, technological, operational and commercial change undertaken across channel silos and business departments, and being guided by the needs of prospects and customers.

Matt Hey, Director of Consulting CACI

2.1.

About CACI Ltd

At CACI we are passionate about assisting brands maximise the value from their customers by delivering a truly integrated, multi-channel experience. To us, there is no such thing as an ‘online’ or ‘offline’ customer – there is just a single customer using a mix of channels. These customers expect brands to always be available, to be relevant and treat them and their data with respect. This creates a complex set of challenges around organisation, technology integration and data management.

CACI Integrated Marketing specialises in delivering this Integrated Customer Experience, with data and digital at its heart. We do this by providing a range of services across all channels: Strategy and technology consulting and programme management

Digital and mobile design and build Multi-channel campaigning services Location / store optimisation services Analytics and segmentation services Data products and services

Technology integration and managed services

We understand the need to deliver value quickly and show results throughout a programme of business change by ‘thinking big and starting small’. Our data and analytics heritage is combined with deep expertise in digital development, database and campaign management, technology integration and customer strategy, giving us a unique perspective on delivering an Integrated Customer Experience.

We have supported some of the world’s leading brands in retail, telecoms, insurance, retail financial services, sports and leisure, gaming, media and charities, across the globe for over 30 years, building long-standing trusted partnerships focussed on realising commercial value. To find out more, please contact CACI Integrated Marketing on 0207 602 6000 and speak to Ian Hitt or Jonathan Burston, or email [email protected].

3.

Methodology

This is the first Integrated Customer Experience Report published by Econsultancy in association with CACI.

There were 890 respondents to our research request, which took the form of a Clicktools online survey in June and July, 2013.

Respondents were evenly split between client-side (in-house) organisations and supply-side respondents (i.e. agencies, vendors or consultants). The findings are shown for client-side (or ‘company respondents’) and supply-side (‘agency respondents’) participants separately. Other key facts about the sample include:

Half of the respondents (50%) stated that they were based in the UK, with a further 18% coming from the rest of Europe. Asia Pacific, North America and the MENA region were also represented.

More than four in 10 of company respondents (44%) stated that their annual turnover was more than £150m.

The most well represented business sectors are retail/mail order (20%), consumer products and services (16%) and financial services (12%).

For supply-side respondents, 30% stated they worked for a digital agency, with a further 18% coming from an integrated agency.

Please see the appendix for more detailed information about the profile of survey respondents.

Where percentage change figures are given, these refer to percentage point changes. In some cases for percentage based charts, figures may not add up to 100% due to rounding.

Information about the survey, including the link, was emailed to Econsultancy’s user base. The incentive for taking part was access to a complimentary copy of this report just before its publication on the Econsultancy website. If you have any questions about the research, please email Econsultancy’s Research Director, Linus Gregoriadis ([email protected]).

4.

Findings

4.1.

Customer experience strategy

4.1.1.

Macro-level factors

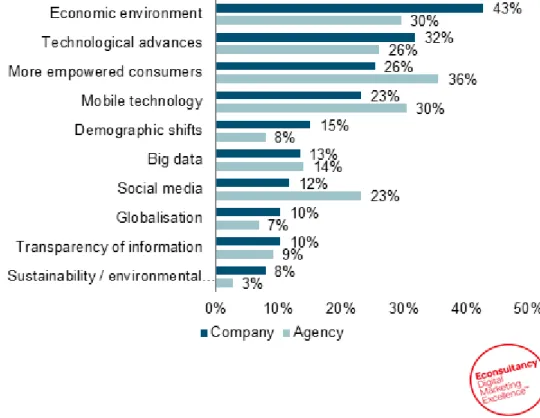

As part of our research, we wanted to establish what macro-level factors are exerting the most influence on businesses, before zooming back in to focus on customer experience in the rest of the report. So, to understand the bigger picture, we asked respondents to indicate two factors which have the biggest influence on their organisational direction and strategy.

In a tough financial climate, it is unsurprising to see that 43% of companies say ‘economic environment’ is the biggest influence. Whilst an integrated customer experience may seem an obvious necessity and potentially source of competitive advantage, the decision to focus on it is likely to be driven by ROI and the overall profitability of the organisation. Customer experience is, after all, a means to an end.

The supply-side perspective on the relative importance of these macro-level factors is noticeably different, with agencies viewing their clients as more consumer-centric in their strategic thinking than they actually are. Agency respondents are more than twice as likely to point to ‘social media’ as being one of the two most influential factors, and are also significantly more likely to cite ‘more empowered consumers’. It may be that agencies are slightly removed from the financial realities facing organisations, with a slightly rosy view of how much impact socially-driven consumer empowerment is having within the boardroom.

Figure 1: Which macro-level factors have the biggest influence on your

organisation’s (or your clients’) direction and strategy?

Company Respondents: 349 Agency Respondents: 348 Note: Respondents could check up to two options

4.1.2.

Relevance of customer touch points

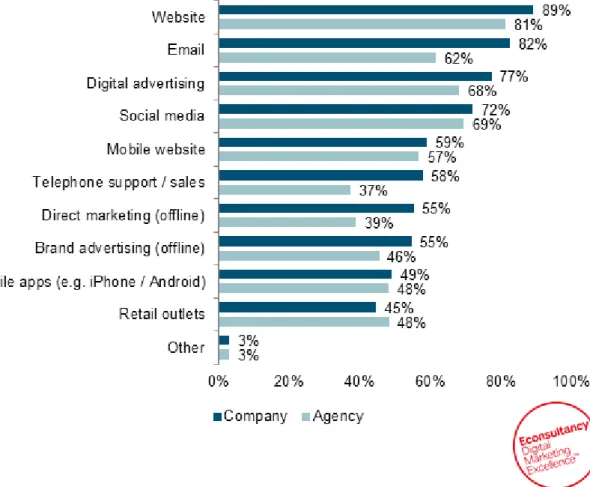

Respondents were asked to indicate which customer channels and touch points are relevant for their organisations [Figure 2]. The options were not meant to be exhaustive, but rather to give a selection of the diverse ways in which companies can engage with customers, and vice-versa. The overarching trend is that the most relevant consumer channels are online. The most frequently cited channel is ‘website,’ which was selected by 89% of companies, while the most relevant offline channel, ‘telephone support/sales’, was selected by only 58% of companies.

“Mobile apps” was considered significantly less relevant than other digital touch points. Less than half of company and agency respondents (49% and 48% respectively) stated that the channel was relevant, whereas ‘mobile website’ was mentioned by more companies and agencies (59% and 57%).

Agency perspectives on which channels are relevant are mostly aligned with companies. The most glaring exceptions to this are ‘email’ and ‘telephone support/sales.’ The difference for email is interesting, given that email is considered a strong channels for delivering a discernible ROI.1

Figure 2: Which consumer channels or touch points are relevant for your (or your

clients’) business?

Company Respondents: 347 Agency Respondents: 347 Note: Respondents could check all the options that applied

1 Econsultancy/Adestra Email Marketing Industry Census 2013 http://econsultancy.com/reports/email-census

4.1.3.

Commitment to customer experience

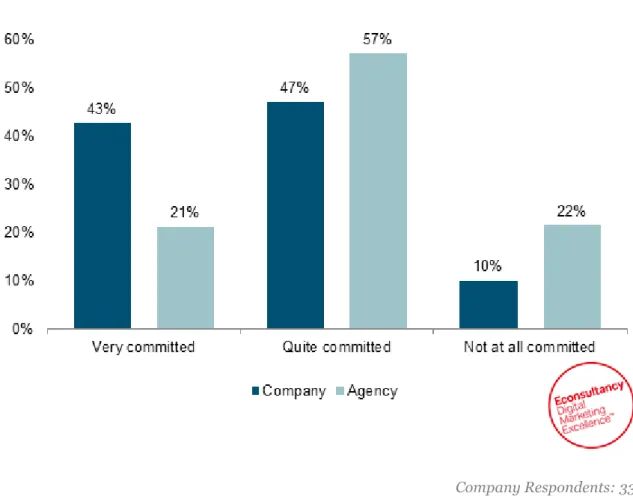

Figure 3 shows the extent to which responding companies view themselves as being ‘committed’ to customer experience.

It is encouraging to see most companies are committed to delivering an integrated customer experience. Only 10% of companies are ‘not at all committed’ while 43% say they are ‘very committed’ to delivering an integrated customer experience.

Agencies were less convinced about their clients’ commitment to customer experience. In fact, agencies were more likely to suggest that clients were not committed (22%) than committed (21%).

Figure 3: How committed is your organisation (or your clients’) to delivering an

integrated customer experience?

Company Respondents: 339 Agency Respondents: 325

4.1.4.

How well developed is strategy?

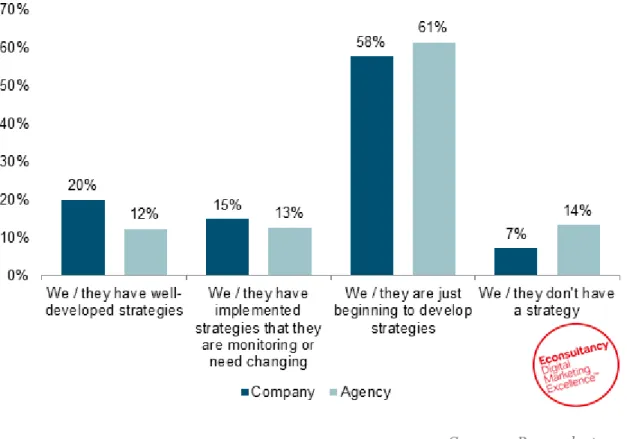

Most companies are still only just starting to develop strategies for customer experience. Almost six out of 10 company respondents (58%) state that they are ‘just beginning to develop strategies,’

which shows that not much has changed since 2011 when we asked a similar question as part of our Multichannel Customer Experience Report.2 Then, 61% of companies said they were only just

starting to develop strategies.

It is remarkable that although 90% of companies were at least ‘quite committed’ to delivering an integrated strategy, only 35% of company respondents have actually implemented their strategy. Although a commitment to customer experience is important, it does not necessarily lead to a defined strategy that can be executed.

Agencies were twice as likely as companies to say there is no strategy in place. Correspondingly, they were also significantly less likely to say their clients had ‘well developed strategies.’ It is possible that agencies and companies have different ideas about what a developed customer experience strategy looks like. Irrespective of the differing perceptions, it is clear that more effort and resources need to go into developing customer experience initiatives.

Figure 4: How well developed is your (or your clients’) strategy for improving the

customer experience?

Company Respondents: 349 Agency Respondents: 348

2 Econsultancy/Foviance Multichannel Customer Experience Report 2011 http://econsultancy.com/reports/multichannel-customer-experience-report

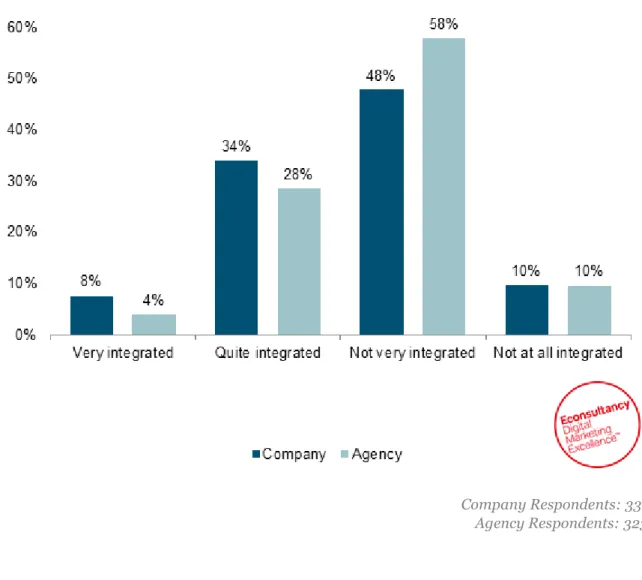

4.1.5.

How integrated is customer experience?

With consumers interacting with brands across a growing number of devices and channels, it has never been more important that these touch points are integrated. Therefore, respondents were asked about the level of customer experience integration they provide.

In a similar story to the previous section, Figure 5 highlights the difference between an organisation’s commitment and execution. Only 8% of company respondents have a ‘very integrated’ customer experience, despite 43% saying they are ‘very committed’ to delivering an integrated customer experience. Almost half of the companies represented in this survey (48%) state their customer experience is ‘not very integrated.’

Figure 5: How integrated is the customer experience your organisation (or your

clients’) provides?

Company Respondents: 331 Agency Respondents: 323

4.2.

Benefits and barriers

4.2.1.

Benefits of an integrated customer experience

Figure 6 shows the perceived benefits of having an integrated customer experience.

It is important to understand what the impact of an integrated customer experience is on an organisation, in order to help build a business case and build boardroom buy-in for further investment. With organisations so mindful of economic and financial conditions as part of their strategic thinking [Figure 1], decision makers will be keen to see how an integrated customer experience affects business performance.

The results show that perceived benefits are most likely to be around attracting and retaining customers. Companies that were surveyed cited ‘improved customer retention/brand loyalty’

(88%)and ‘increased sales/improved customer acquisition’ (82%) as benefits of an integrated customer experience. This is encouraging for organisations that are concerned that economic conditions may have an adverse effect on sales revenue, as the results suggest an integrated customer experience may assist in mitigating that risk.

Figure 6: What do you see as the business benefits of an integrated customer

experience?

Company Respondents: 331 Agency Respondents: 331 Note: Respondents could check all options that applied

4.2.2.

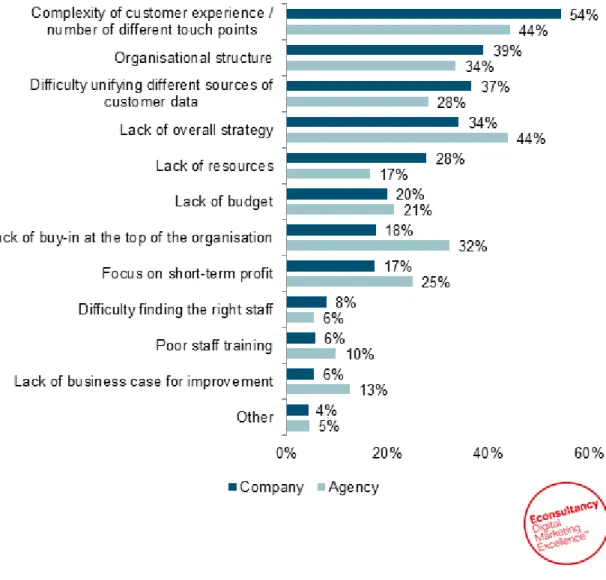

Greatest barriers to improving customer experience

According to respondents, the complicated nature of the customer experience is the biggest barrier to its improvement, and has become an even bigger problem than it was two years ago. More than half (54%) of company respondents say ‘complexity of customer experience/number of different touch points’ prevents them from refining their customer experience, which is a 14% increase from the 2011 Econsultancy Multichannel Customer Experience Report.

‘Organisational structure’ has also become a barrier to more companies, increasing by 5% since 2011 to 39%.The proportion of companies having ‘difficulty unifying different sources of

customer data’ is unchanged since 2011, suggesting that there has been little, if any, improvement in this area.

Reaffirming opinions from the previous section, agencies say ‘lack of strategy’ is just as significant a barrier as dealing with the complexity of customer experience.

Figure 7: What are the three greatest barriers preventing your (or your clients)

organisation from improving the customer experience?

Company Respondents: 327 Agency Respondents: 327 Note: Respondents could check up to three options

4.2.3.

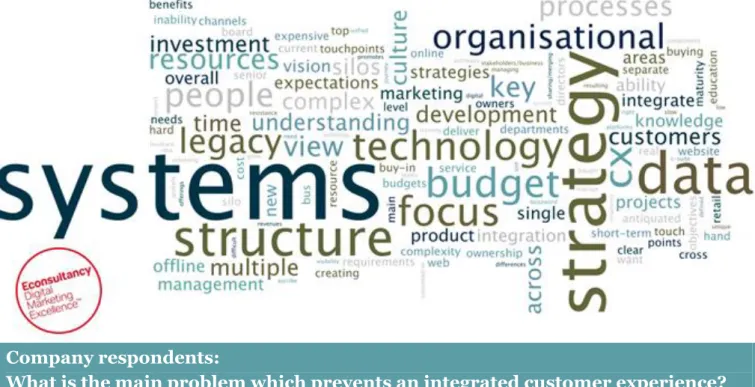

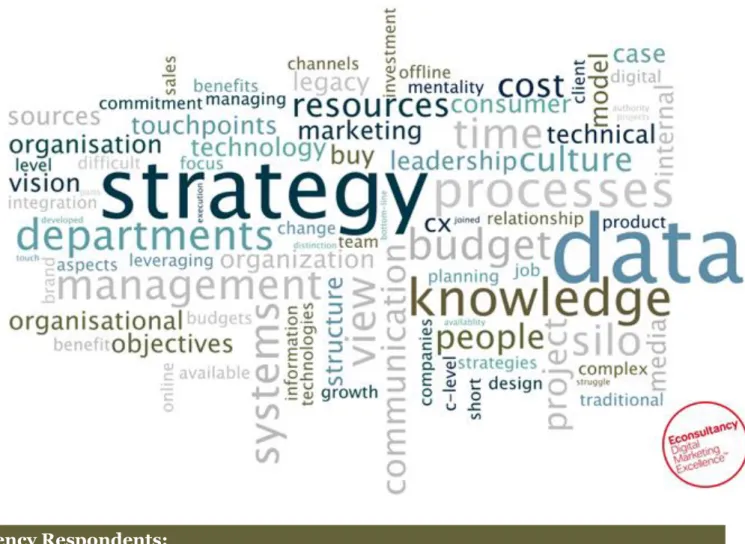

Problems relating to integration

When asked to give further insight into what the main barriers to delivering an integrated customer experience are, it is clear companies and agencies have different perspectives. Figure 8

and Figure 9 show the answers to an open-ended question presented as a tag cloud for in-house and supply-side respondents respectively, with the size of the word depicting the frequency of mentions.

Themes relating to strategy and organisational structure were commonly cited by respondents. However, the challenges that the majority of companies are experiencing seem to revolve around the technical infrastructures and systems that exist (or don’t exist). The transition to creating an integrated customer experience requires organisations to re-evaluate the usefulness of their legacy systems and for many it seems to be a painful process.

While agencies agree that there are constraints when using dated technology, they do not think it is the most significant barrier to developing an integrated customer experience. Agencies suggest that the impact of a lack of knowledge and strategy within many organisations is a greater obstacle, echoing the quantitative findings of Figure 7. With customer experience touching many parts of the business, organisations that have worked in departmental silos will have to rely on collaborative knowledge from different parts of the business.

Companies

Figure 8

:

What is the main problem which prevents an integrated customer

experience?

Company respondents:

What is the main problem which prevents an integrated customer experience?

“Legacy systems, processes and structures are the main contributors to our poor customer experience but also a lack of focus on the customer in real practice and too much focus on technology and the product.”“Legacy platforms and development, which makes it hard to view customers across different touch-points.” “Legacy disparate systems, perpetual lack of investment in new systems and technology, short-term systems strategy, other business priorities & focus.”

“For us, organisational structure. Too many departments trying to connect with the same sets of data using different messaging and emotional diversity.”

Agencies

Figure 9: What is the main problem which prevents an integrated customer

experience?

Agency Respondents:

What is the main problem which prevents an integrated customer experience?

“It's a big project which takes time, budget, know-how and resources. Securing all of these is difficult, even if the returns are evident.”“Lack of ownership, or interdepartmental struggles to who should own the process. Lack of understanding, fear of change.”

“Lack of planning and strategy to perform a proper integrated campaign.”

“Understanding how online and offline are both shuffled into experience, and that this distinction (between online and offline touch points) from the customer perspective is nearly non-existent.”

“No strategy, no appreciation of what is involved, misconception that it conflicts with business requirements/needs.”

4.3.

Key pillars for success

4.3.1.

Key areas for delivering an integrated customer experience

Understanding the key elements needed to deliver an integrated customer experience is vital for shaping strategy, implementation and investment.

Of five key pillars for delivering an integrated customer experience identified by Econsultancy and CACI, respondents were asked how important these areas are for success.

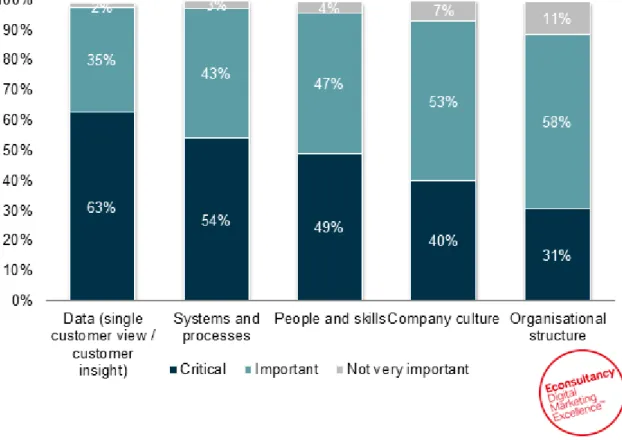

Companies identified ‘data (single customer view/customer insight)’ and ‘systems and processes’

as the most important areas for delivering an integrated customer experience, with 63% and 54% of companies describing these (respectively) as ‘critical’. It seems as though organisations are well aware of the impact that the proliferation and availability of data is having, as well as the tools and infrastructure needed to utilise that data.

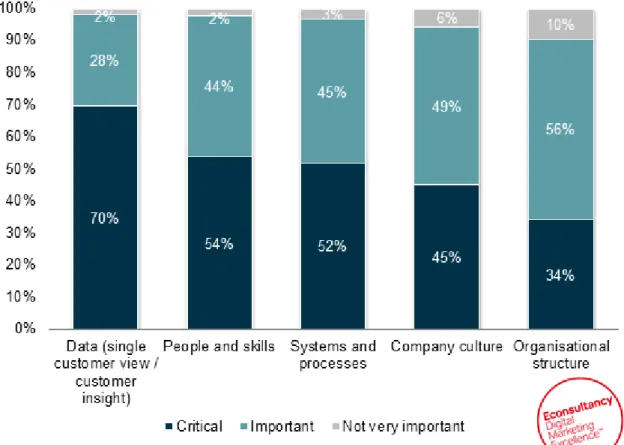

Agencies are in agreement on the importance of ‘data’, with 70% of agency respondents saying that it is critical to delivering an integrated customer experience [Figure 11]. Slightly more supply-side respondents place critical value on ‘people and skills’ (54%) than they do on ‘systems and processes’ (52%) .

Companies

Figure 10: How important are the following areas for delivering an integrated

customer experience?

Agencies

Figure 11: How important are the following areas for delivering an integrated

customer experience?

4.3.2.

How well equipped are organisations across key pillars?

The chart below shows that many organisations are ill-equipped to deliver across all five pillars identified by this research as being key components of an integrated customer experience. The area where most companies rated themselves as ‘excellent’ for was ‘company culture.’

However, only 12% of companies gave themselves this distinction, with an additional 31% identifying themselves as having a ‘good’ company culture in the context of delivering an integrated customer experience.

To reinforce the issue companies seem to be having with technology, more than three out of four respondents (76%) rated their ‘systems and processes’ as average or below.

Agencies’ perception of the ability of clients to deliver in key areas is even worse than the company respondents’ self-diagnosis [Figure 13]. No more than 27% of agencies rated their clients as excellentor goodin any particular key area.

Companies

Figure 12: Across these areas, how well equipped is your organisation for

delivering an integrated customer experience?

Agencies

Figure 13: Across these areas, how well equipped are your clients for delivering

an integrated customer experience?

4.3.3.

Key organisational pillars: criticality versus competence

The chart below shows the proportion of companies regarding each key area as ‘critical’, as well as the percentage of those describing themselves as ‘excellent’ or ‘good’.

Despite identifying ‘data’ and ‘systems and processes’ as the most critical areas for developing an integrated customer experience, half or less (in the case of systems and processes) have the ability to deliver to a decent standard.

Only 32% of companies rated their ability in ‘data’ to be excellentor good, despite 63% of companies rating the area as critical. The gap between perception of importance and ability is even more significant for ‘systems and processes,’ with a 30% discrepancy between the percentage of companies that considered the area critical and the proportion of companies deeming themselves at least ‘good’.

This discrepancy isn’t evident for the three other pillars shown in Figure 14, but the same cannot be said for supply-side respondents [Figure 15].

It is clear that agencies feel many clients are not able to deliver an integrated customer experience based on currently ability. The results show most clients that work with agencies to deliver an integrated customer experience do not typically have adequate abilities in the critical areas needed to execute.

Companies

Figure 14: Importance of areas for delivering an integrated customer experience,

compared to how well equipped companies are

Agencies

Figure 15: Importance of areas for delivering an integrated customer experience,

compared to how well equipped clients are

Company Respondents: 321

4.3.4.

Underlying factors needed for an integrated customer

experience

When respondents were asked in an open-ended question what factors are needed for an integrated customer experience, there were a variety of answers. Many of these responses were about understanding the journey that customers take or getting a single view of the journey. In addition, many company respondents spoke of needing better technology or data solutions so they can make better decisions.

According to agencies, strategy is equally as important a factor as those mentioned above. In addition, agencies stressed the importance of getting the right people within the organisation. Not only does there need to be buy-in across the board, but there also needs to be adequately trained staff involved in integrating the customer experience.

Companies

Figure 16: What is the main factor which underpins an integrated customer

experience?

Company respondents

What is the main factor which underpins an integrated customer experience?

“Solid reporting allowing you to make informed decisions.”“Shared systems and procedures across all the different touch points.” “Integrated marketing department rather than working in silos.”

“The tools we use working across all customer touch points. Allowing us greater customer insight, then being able to retarget them.”

Agencies

Figure 17: What is the main factor which underpins an integrated customer

experience?

Agency Respondents

What is the main factor which underpins an integrated customer experience?

“Providing the customer with the correct information that they require quickly and enabling them to get wherever they need to with minimal effort. For example, integrating registration and login processes across websites.”“Understanding all the different touch points where one can reach a customer - and then committing to being aggressively present at all those touch points.”

“Understanding and learning about the individual customers, and implementing that into the organisational environment.”

4.4.

Technology used for integrated customer experience

The importance of technology when developing an integrated customer experience is vital. When the right technology is not being used, it can create significant barriers to delivery, exacerbating other problems relating to data, processes and execution.

It was seen earlier that ‘complexity of customer experience’ and ‘difficulty unifying different sources of customer data’ are two of the top three biggest barriers to improving customer experience (54% and 37% respectively).

Figure 18 shows the extent to which organisations have integrated technology for delivering a joined-up customer experience. The majority of companies (51%) are using “non-integrated tech platforms”, while only 8% are using a ‘single integrated platform.’ Around a third of respondents (34%) say they have ‘integrated tech platforms’.

Given the increasing complexity of the customer experience across so many touch points, it should be acknowledged that related technological requirements are very diverse, ranging from digital marketing advertising and communications to data warehouses containing purely ‘offline’ data.

For large, multichannel organisations especially, this may make the use of a single, integrated platform unfeasible.

Figure 18: How would you describe the technology you (or your clients) use for

delivering an integrated customer experience?

Company Respondents: 305 Agency Respondents: 309

4.5.

Measurement

4.5.1.

Metrics used to measure effectiveness

‘Sales and revenue’ continues to be seen as the greatest indicator of how effective a customer experience is. Two thirds of companies (66%) are using ‘sales and revenue’ figures to directly measure the effectiveness of the customer experience, which is unchanged since similar Econsultancy research in 2011. Agencies are also more likely to be using sales as a metric in the context of customer experience than they were two years ago, with the percentage of agency respondents increasing from 69% to 78%.

At the same time, customer retention/loyalty is being used less as a metric for customer experience. The amount of companies and agencies who use retention to measure customer experience has decreased by 11% for companies and 21% for agencies.

This decrease is surprising in the context of Figure 6 earlier in the report, which showed that

improved customer retention and brand loyalty are seen as business benefits of an integrated customer experience by 88% of company respondents.

More companies need to be systematically measuring the benefits of customer experience if they want to be able to build a business case for further investment.

Companies

Figure 19: What types of metrics do you use to directly measure the effectiveness

of the customer experience?

Company Respondents: 292 Note: Respondents could check all the options that applied

Agencies

Figure 20: What types of metrics do your clients typically use to directly measure

the effectiveness of the customer experience?

Agency Respondents: 299 Note: Respondents could check all the options that applied

4.5.2.

Use of data to improve customer experience

Improving customer experience requires organisations to harness data across a range of different channel. As part of this research, we asked respondents to what extent they use different data sources.

The data source that is used the most widely in this context is ‘aggregated web analytics’ , used extensivelyby 43% of companies and occasionally by 41%. ‘Email data’ is also popular among companies with 86% at least occasionally using data from emails to improve the customer experience.

CRM data is also being widely used to improve the customer experience, though the same cannot be said of web analytics data relating to individuals.

In a world where customers are increasingly demanding personalised digital customer experiences, it is interesting only 16% of companies are using ‘web analytics data tied to individuals’ extensively.

While only 12% of all company respondents reported that they use data from ‘electronic points of sale’ (EPOS data) extensively to improve customer experience, this percentage increases to 32% for retail organisations.

The use of data reported by agency respondents is broadly similar to the companies. However, agencies said clients were less likely to make extensive use of ‘customer survey data’ (12 versus 23%) and ‘call centre data’ (10% versus 18%).

Companies

Figure 21: To what extent are the following sources of data used for improving the

customer experience?

Agencies

Figure 22: To what extent are the following sources of data used for improving

the customer experience?

4.6.

Ownership and budget

4.6.1.

Ownership of integrated customer experience

As the perception of the customer experience continues to change, it is encouraging that many organisations are taking ownership of its integration. Having said that, there are still 12% of companies reporting that ‘no-one’ owns the integrated customer experience.

Almost half the respondents (48%) say their customer experience is owned by ‘a mixture of different departments’, demonstrating the interconnected nature of an integrated customer experience.

Ownership by different departments can be seen as a good or a bad thing. On the plus side, inter-departmental co-operation is very positive, though the lack of a single champion to own this may mean that it can fall between stalls.

Organisations that work with agencies are now more likely to follow suit, with 47% having a shared ownership of customer experience, which is a 15% increase from 2011. Just over a quarter of agencies (27%) say customer experience within client organisations is owned by ‘marketing and/or sales department.’

Companies

Figure 23: Who, if anyone, within your organisation owns the integrated

customer experience?

IT Department was not given as an option in the 2011 survey Leadership Team/CEO was not given as an option in the 2013 survey

Response 2011: 263 Response 2013: 291

Agencies

Figure 24: Within client companies, who typically owns the integrated customer

experience?

IT Department was not given as an option in the 2011 survey Leadership Team/CEO was not given as an option in the 2013 survey

Response 2011: 183 Response 2013: 289

4.6.2.

Dedicated budget for improving customer experience

The likelihood of companies having budget dedicated to improving the customer experience is largely unchanged from 2011. One in 10 companies say that they have a ‘single dedicated budget,’

though 6% fewer companies than in 2011 say ‘there is no budget at all’ (21%, down from 27%). There has also been minimal change from the perspective of agencies. The biggest change is that 6% more clients have ‘no budget at all’ from two years ago, exactly the reverse of what company respondents are reporting.

Companies

Figure 25: Does your organisation have a dedicated budget for improving

customer experience?

Response 2011: 265 Response 2013: 271

Agencies

Figure 26: Do clients typically have a dedicated budget for improving customer

experience?

Response 2011: 183 Response 2013: 271

4.6.3.

Budget plans for improving customer experience

Figure 27 illustrates the financial intentions of companies with regards to improving customer experience.

It appears that many companies will be using their budget to address some of the deficiencies highlighted earlier in the report. The areas that will see an increase in budget from the highest proportion of companies (‘data and insight’ and ‘systems and skills’) are the areas with the biggest discrepancy between perceived importance and ability. This is a positive indication that companies are indeed committed to improving the customer experience.

Agency clients also intend to increase budgets, particularly for ‘data and insight’ (57%). It is also encouraging that no more than 4% of agency clients intend to decrease budget across any areas needed to improve customer experience.

What is less encouraging from both the client-side and agency perspective is that only a third of companies (34%) and 29% of agencies say there will be an increase in spending for training and skills. The importance of people for maintaining and improving the customer experience has already been noted, so it is disappointing that relatively few companies are increasing budgets in this area.

Figure 27: In the context of improving customer experience, what are your plans

for budgets over the next year?

Agencies

Figure 28: In the context of improving customer experience, what are your

clients’ budget plans over the next year?

4.7.

Improving customer experience

4.7.1.

Most significant factor for improving customer experience

Respondents were asked an open-ended question about what critical single thing needs to happen to enable a more integrated customer experience.

Many company respondents stated that buy-in is required from management and staff in order to improve. Other respondents felt that a dedicated team specifically for customer experience needs to be put together to enable a more integrated customer experience. Other themes cited by company respondents revolved around a management strategy, improving the systems that are in place and making better use of data.

Companies

Figure 29: What single thing needs to happen within your organisation to enable

a more integrated customer experience?

Company respondents

What single thing needs to happen within your organisation to enable a more

integrated customer experience?

“Top down buy-in and a the creation of a dedicated digital team”

“Company needs to add/revamp a few systems to enable a more automated and integrated customer experience.” “Our data needs to be joined up. At the moment our users have different relationships with different

departments but these are not yet tied together.”

“Management need to create a culture and identify a team charged with developing and implementing systems to help deliver this.”

“A willingness and focus from staff to be able to work together towards the same goal, which will be hard as we have historically worked in silos.”

In comparison, agencies are calling on their clients to have a more long-term approach to customer experience. Many comments from agencies talk about clients needing a strategic or

cultural change, with a high level of commitment. Buy-in is also needed from top-level management in order to enable a more integrated customer experience.

Agencies

Figure 30: What single thing needs to happen within your clients’ organisation to

enable a more integrated customer experience?

Agency respondents

What single thing needs to happen within your clients’ organisation to enable a

more integrated customer experience?

“Have an overarching strategy and someone/a team responsible for overseeing the full customer journey.” “Realise that revenue is important on a short-term basis. But for long term benefit, they should take into account customers' feedback.”

“Better understanding of integrated marketing and the ability to think long term by investing in tools, technologies and training.”

"A cross functional team that is dedicated to understanding and developing integrated processes and customer journeys.”

“Long term commitment to customer experience strategy and programme of change.” “Top management buy-in and budget allocation.”

4.7.2.

Information and advice

Respondents were also asked where they get their information and advice from pertaining to customer experience. Most companies that were surveyed tend to go online to find information, through blog articles, industry websites and, flatteringly, Econsultancy.’ Respondents also said they sought the advice of agencies and consultants, as well as searching internally for answers through marketing departments.

Agency respondents stated that their clients tend to go to their own or other agencies for additional information and advice.

Companies

Figure 31: Where do you turn to for information and advice about integrating the

customer experience?

Agencies

Figure 32: Where do your clients turn to for information and advice about

integrating the customer experience?

5.

Appendix

5.1.

Respondent profiles

The total number of respondents to the survey was 890, including 474 who described themselves as working in-house (company) and 416 who stated they worked for agency, vendor or as a consultant.

Of the 474 company respondents, 59 were exclusively B2B, 154 were exclusively B2C and 261 were a mixture of B2B and B2C [Figure 34].

Figure 33:

Companies

Figure 34: Is your organisation focused on B2B or B2C?

5.1.1.

Size of company revenue

More than four in 10 of the client-side respondents (44%) stated that their annual turnover was over £150m. Most agencies that took part in the survey work for companies earning £10m or less (73%).

Companies

Figure 35: What is your annual company turnover?

Agencies

Figure 36: What is your annual company turnover?

5.1.2.

Business Sector

The industries that were the most strongly represented were ‘retail/mail order’ (20%), ‘consumer products and services’ (16%) and financial services (12%).

Figure 37: In which business sector is your organisation?

5.1.3.

Type of Agency

Almost a third of supply-side respondents (30%) came from ’digital agencies’, with 18% coming from an ‘integrated agency’, while11% stated they were an ‘independent consultant.’

Figure 38: Which type of agency do you work for?

5.1.4.

Geography

Half of the respondents were based in the UK, with an additional 18% coming from elsewhere in Europe and 14% coming from Asia Pacific.