Introduction to

Microeconomics

1 of 33

THE PRODUCTION PROCESS: THE BEHAVIOR

OF PROFIT-MAXIMIZING FIRMS

production The process by which inputs

3 of 33

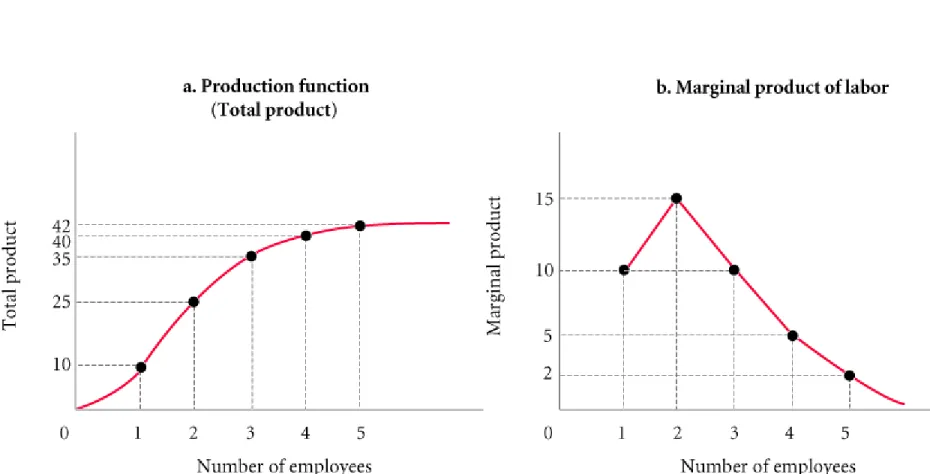

THE PRODUCTION PROCESS

production function or total product

function A numerical or mathematical

expression of a relationship between inputs and outputs. It shows units of total product as a function of units of inputs.

TABLE 7.2 Production Function (1) LABOR UNITS EMPLOYEES (2) TOTAL PRODUCT (SANDWICHES PER HOUR) (3) MARGINAL PRODUCT OF LABOR (4) AVERAGE PRODUCT OF LABOR (TOTAL PRODUCT LABOR UNITS) 0 1 2 3 4 5 6 0 10 25 35 40 42 42 10 15 10 5 2 0 10.0 12.5 11.7 10.0 8.4 7.0

5 of 33

THE PRODUCTION PROCESS

6 of 33

THE PRODUCTION PROCESS

Marginal Product and the Law of Diminishing Returns

marginal product The additional output

that can be produced by adding one more unit of a specific input, ceteris paribus.

law of diminishing returns When additional

units of a variable input are added to fixed inputs after a certain point, the marginal product of the variable input declines.

7 of 33

THE PRODUCTION PROCESS

Marginal Product versus Average Product

average product The average amount

produced by each unit of a variable factor of production.

labor of

units total

product total

labor of

product

THE PRODUCTION PROCESS

9 of 33

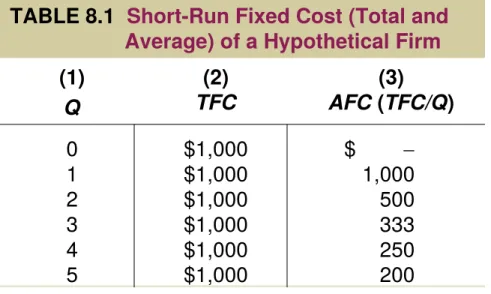

TABLE 8.1 Short-Run Fixed Cost (Total and Average) of a Hypothetical Firm (1)

Q

(2)

TFC AFC ((3)TFC/Q)

0 1 2 3 4 5 $1,000 $1,000 $1,000 $1,000 $1,000 $1,000 $ 1,000 500 333 250 200

COSTS IN THE SHORT RUN

total fixed costs (TFC) or overhead The

total of all costs that do not change with output, even if output is zero.

Total Fixed Cost (TFC)

FIXED COSTS

10 of 33

COSTS IN THE SHORT RUN

spreading overhead The process of dividing

total fixed costs by more units of output.

Average fixed cost declines as quantity rises.

11 of 33

COSTS IN THE SHORT RUN

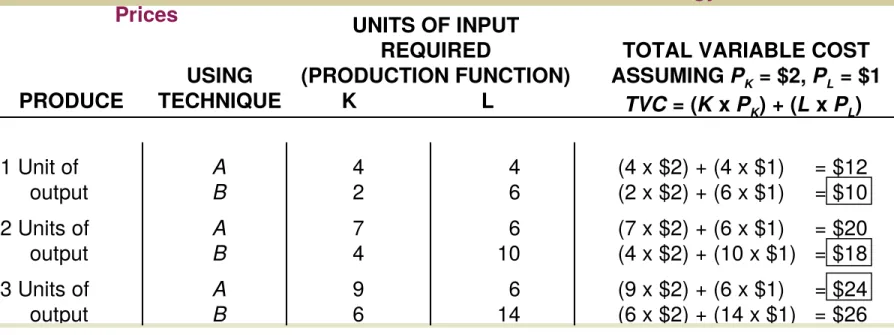

(9 x $2) + (6 x $1) = $24 (6 x $2) + (14 x $1) = $26 6 14 9 6 A B

3 Units of output

(7 x $2) + (6 x $1) = $20 (4 x $2) + (10 x $1) = $18 6 10 7 4 A B

2 Units of output

4

6 (4 x $2) + (4 x $1) = $12(2 x $2) + (6 x $1) = $10 4

2

A B

1 Unit of output

TOTAL VARIABLE COST ASSUMING PK = $2, PL = $1

TVC = (K x PK) + (L x PL) USING

TECHNIQUE

UNITS OF INPUT REQUIRED

(PRODUCTION FUNCTION) K L PRODUCE

TABLE 8.2 Derivation of Total Variable Cost Schedule from Technology and Factor Prices

12 of 33

COSTS IN THE SHORT RUN

The total variable cost curve embodies information about both factor, or input, prices and technology. It shows the cost of production using the best available technique at each output level given current factor prices.

13 of 33

TABLE 8.3 Derivation of Marginal Cost from Total Variable Cost

UNITS OF OUTPUT TOTAL VARIABLE COSTS ($) MARGINAL COSTS ($)

0 1 2 3

0 10 18 24

0 10 8 6

COSTS IN THE SHORT RUN

Although the easiest way to derive marginal cost is to look at total variable cost and

subtract, do not lose sight of the fact that when a firm increases its output level, it hires or demands more inputs. Marginal cost measures the additional cost of inputs required to produce each successive unit of output.

marginal cost (MC) The increase in total cost that

14 of 33

COSTS IN THE SHORT RUN

The Shape of the Marginal Cost Curve in the Short Run

15 of 33

COSTS IN THE SHORT RUN

Graphing Total Variable Costs and Marginal Costs

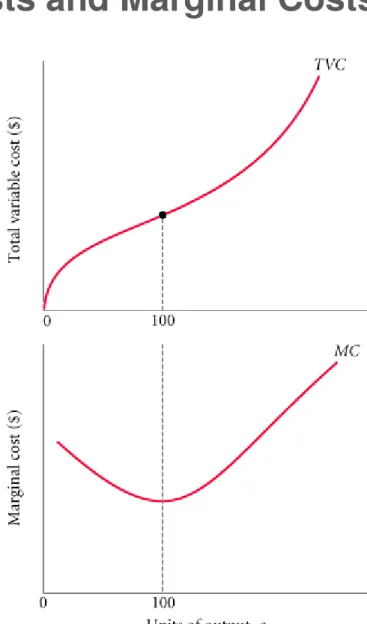

FIGURE 8.5 Total Variable Cost and Marginal Cost for a Typical Firm

MC TVC

TVC q

TVC

TVC

1 Δ

of slope

Average Variable Cost

(AVC)

q

TVC

16 of 33

COSTS IN THE SHORT RUN

Marginal cost intersects average variable cost at the lowest, or minimum, point of AVC.

Graphing Average Variable Costs and Marginal Costs

17 of 33

COSTS IN THE SHORT RUN

18 of 33

COSTS IN THE SHORT RUN

FIGURE 8.8 Average Total Cost = Average Variable Cost + Average Fixed Cost

The relationship between average total cost and marginal cost is

exactly the same as the

COSTS IN THE SHORT RUN

SHORT-RUN COSTS: A REVIEW

TABLE 8.5 A Summary of Cost Concepts

TERM DEFINITION EQUATION

Accounting costs Out-of-pocket costs or costs as an accountant would

define them. Sometimes referred to as explicit costs. Economic costs Costs that include the full opportunity costs of all inputs.

These include what are often called implicit costs. Total fixed costs Costs that do not depend on the quantity of output

produced. These must be paid even if output is zero. TFC Total variable costs Costs that vary with the level of output. TVC

Total cost The total economic cost of all the inputs used by a

firm in production. TC = TFC + TVC Average fixed costs Fixed costs per unit of output. AFC = TFC/q

Average variable costs Variable costs per unit of output. AVC = TVC/q

Average total costs Total costs per unit of output. ATC = TC/q ATC = AFC + AVC

Marginal costs The increase in total cost that results from

COSTS IN THE SHORT RUN

Marginal cost is the cost of one additional unit. Average variable cost is the total variable cost divided by the total number of units produced.

TABLE 8.4 Short-Run Costs of a Hypothetical Firm

(1)

q TVC(2)

(3)

MC

( TVC)

(4)

AVC

(TVC/q) TFC(5)

(6)

TC

(TVC + TFC)

(7)

AFC

(TFC/q)

(8)

ATC

(TC/q or AFC + AVC)

0 $ 0 $ $ $1,000 $ 1,000 $ $

1 10 10 10 1,000 1,010 1,000 1,010

2 18 8 9 1,000 1,018 500 509

3 24 6 8 1,000 1,024 333 341

4 32 8 8 1,000 1,032 250 258

5 42 10 8.4 1,000 1,042 200 208.4

21 of 33

LONG-RUN COSTS: ECONOMIES

AND DISECONOMIES OF SCALE

increasing returns to scale, or economies of

scale An increase in a firm’s scale of production

leads to lower costs per unit produced.

constant returns to scale An increase in a

firm’s scale of production has no effect on costs per unit produced.

decreasing returns to scale, or diseconomies

of scale An increase in a firm’s scale of

22 of 33

LONG-RUN COSTS: ECONOMIES

AND DISECONOMIES OF SCALE

INCREASING RETURNS TO SCALE

The Sources of Economies of Scale

Most of the economies of scale that immediately come to mind are technological in nature.

23 of 33

LONG-RUN COSTS: ECONOMIES

AND DISECONOMIES OF SCALE

FIGURE 9.5 A Firm Exhibiting Economies of Scale

long-run average cost curve (LRAC) A graph that

24 of 33

LONG-RUN COSTS: ECONOMIES

AND DISECONOMIES OF SCALE

CONSTANT RETURNS TO SCALE

Technically, the term constant returns means that the quantitative relationship between input and output stays constant, or the same, when output is increased.

25 of 33

LONG-RUN COSTS: ECONOMIES

AND DISECONOMIES OF SCALE

DECREASING RETURNS TO SCALE

26 of 33

LONG-RUN COSTS: ECONOMIES

AND DISECONOMIES OF SCALE

optimal scale of plant The scale of plant

that minimizes average cost.

TABLE 7A.1 Alternative Combinations of Capital (K) and Labor (L) Required to Produce 50, 100, and 150 Units of Output

QX = 50 QX = 100 QX = 150

K L K L K L

A B C D E 1 2 3 5 8 8 5 3 2 1 2 3 4 6 10 10 6 4 3 2 3 4 5 7 10 10 7 5 4 3

27 of 33

ISOQUANTS AND ISOCOSTS

28 of 33

Isoquant A graph

that shows all the combinations of capital and labor that can be used to produce a given amount of output.

29 of 33

FIGURE 7A.2 The Slope of an Isoquant Is Equal to the Ratio of MPL to MPK

Slope of isoquant:

K L

MP

MP

L

K

marginal rate of

technical substitution

FIGURE 7A.3 Isocost Lines Showing the

Combinations of Capital and Labor Available for $5, $6, and $7

FACTOR PRICES AND INPUT

COMBINATIONS: ISOCOSTS

isocost line A

graph that shows all the combinations of capital and labor

31 of 33

FIGURE 7A.4 Isocost Line Showing All Combinations of Capital and Labor Available for $25

Slope of isocost line:

FIGURE 7A.5 Finding the Least-Cost Combination of Capital and Labor to Produce 50 Units of Output

FINDING THE LEAST-COST TECHNOLOGY WITH ISOQUANTS AND ISOCOSTS

The firm will choose the combination of inputs that is least costly. The least costly way to produce any given level of output is indicated by the point of tangency between an isocost line and the isoquant

33 of 33

FIGURE 7A.6 Minimizing Cost of Production for qX = 50,

qX = 100, and qX = 150

K L K L

P

P

MP

MP

slope

of

isocost

isoquant

of

slope

K L K LP

P

MP

MP

THE COST-MINIMIZING EQUILIBRIUM CONDITION

At the point where a line is just tangent to a curve, the two have the same slope. At each point of tangency, the

following must be true:

Thus,

Dividing both sides by PL and multiplying both sides by

MPK, we get