Chapter

29

Mergers and

Acquisitions

P

AR

T

EIGHT

___

The 2009 consolidation of two British banks, Halifax Bank of Scotland (HBOS) plc and Lloyds TSB plc, was just one of many corporate restructurings that took place as a result of the major downturn in developed economies. To understand the importance of the HBOS–Lloyds TSB consolidation it is neces-sary to consider both banks in the context of the larger British banking sector. HBOS was Britain’s largest mortgage lender, with a market share of 20 per cent. Lloyds TSB was in a similar position, but slightly smaller, having a market share of 9 per cent. Combining both companies resulted in the largest bank in the UK.

The consolidation also led to the British government owning 43.4 per cent of the shares of the new entity, Lloyds Banking Group plc. This was later increased to 65 per cent because of the disastrous state of HBOS’s bad debts. So why did Lloyds TSB merge with HBOS? HBOS was in serious difficulty resulting from significant exposures to short-term funding requirements and bad loan portfolios. Hindsight has shown that Lloyds would have been far better off without the ‘toxic assets’ they inherited from the consolidation.

The main reason given by both firms for the merger was cost savings, which were estimated to be £1.5 billion per annum. Of course, the cost savings were only an estimate, and often these estimates are incorrect. Unfortunately for the new Lloyds Banking Group, the markets did not respond well, and in the first week of trading the share price collapsed. How do companies like Lloyds and HBOS determine whether an acquisition or merger is a good idea? This chapter explores the reasons why corporate restructurings, such as mergers, should take place – and, just as important, the reasons why they should not.

29.1 The Basic Forms of Acquisition

Acquisitions follow one of three basic forms: (a) merger or consolidation; (b) acquisition of shares; and (c) acquisition of assets.

Merger or Consolidation

A merger refers to the absorption of one firm by another. The acquiring firm retains its name and identity, and it acquires all of the assets and liabilities of the acquired firm. After a merger, the acquired firm ceases to exist as a separate business entity.

A consolidation is the same as a merger except that an entirely new firm is created. In a consolidation both the acquiring firm and the acquired firm terminate their previous legal existence and become part of the new firm.

The Basic Forms of Acquisition

785

___

___

EXAMPLE29.1

Merger Basics

Suppose firm A acquires firm B in a merger. Further, suppose firm B’s shareholders are given one share of firm A’s equity in exchange for two shares of firm B’s equity. From a legal standpoint, firm A’s shareholders are not directly affected by the merger. However, firm B’s shares cease to exist. In a consolidation, the shareholders of firm A and firm B exchange their shares for shares of a new firm (e.g., firm C).

Because of the similarities between mergers and consolidations, we shall refer to both types of reorganization as mergers. Here are two important points about mergers and consolidations:

A merger is legally straightforward, and does not cost as much as other forms of acquisition.

1

It avoids the necessity of transferring title of each individual asset of the acquired firm to the acquiring firm.

The shareholders of each firm must approve a merger.

2 1 Typically, votes of the owners of

two-thirds of the shares are required for approval. In addition, shareholders of the acquired firm have appraisal rights. This means that they can demand that the acquiring firm purchase their shares at a fair value. Often the acquiring firm and the dissenting shareholders of the acquired firm cannot agree on a fair value, which results in expensive legal proceedings.

Acquisition of Shares

A second way to acquire another firm is to purchase the firm’s voting shares in exchange for cash, or shares of equity and other securities. This process may start as a private offer from the management of one firm to another. At some point the offer is taken directly to the selling firm’s shareholders, often by a tender offer. A tender offer is a public offer to buy shares of a target firm. It is made by one firm directly to the shareholders of another firm. The offer is communicated to the target firm’s shareholders by public announcements such as newspaper advertisements. Sometimes a general mailing is used in a tender offer. However, a general mailing is difficult, because the names and addresses of the shareholders of record are not usually available.

The following factors are involved in choosing between an acquisition of shares and a merger:

In an acquisition of shares, shareholder meetings need not be held and a vote is not

1

required. If the shareholders of the target firm do not like the offer, they are not required to accept it and need not tender their shares.

In an acquisition of shares, the bidding firm can deal directly with the shareholders of a target

2

firm via a tender offer. The target firm’s management and board of directors are bypassed. Target managers often resist acquisition. In such cases, acquisition of shares circumvents

3

the target firm’s management. Resistance by the target firm’s management often makes the cost of acquisition by shares higher than the cost by merger.

Frequently a minority of shareholders will hold out in a tender offer, and thus the target

4

firm cannot be completely absorbed.

Complete absorption of one firm by another requires a merger. Many acquisitions of shares

5

end with a formal merger.

Acquisition of Assets

One firm can acquire another by buying all of its assets. The selling firm does not necessarily vanish, because its ‘shell’ can be retained. A formal vote of the target shareholders is required in an acquisition of assets. An advantage here is that although the acquirer is often left with minority shareholders in an acquisition of shares, this does not happen in an acquisition of Finanza aziendale

___

assets. Minority shareholders often present problems, such as holdouts. However, asset acquisition involves transferring title to individual assets, which can be costly.

A Classification Scheme

Financial analysts have typically classified acquisitions into three types: Horizontal acquisition

1 : Here, both the acquirer and acquired are in the same industry. Lloyds TSB’s merger with HBOS in 2009 is an example of a horizontal merger in the banking industry.

Vertical acquisition

2 : A vertical acquisition involves firms at different steps of the production process. The acquisition by an airline company of a travel agency would be a vertical acquisition.

Conglomerate acquisition

3 : The acquiring firm and the acquired firm are not related to each other. The acquisition of a food products firm by a computer firm would be considered a conglomerate acquisition.

A Note about Takeovers

Takeover is a general and imprecise term referring to the transfer of control of a firm from one group of shareholders to another.2 A firm that has decided to take over another firm is usually referred to as the bidder. The bidder offers to pay cash or securities to obtain the equity or assets of another company. If the offer is accepted, the target firm will give up control over its equity or assets to the bidder in exchange for consideration (i.e., its equity, its debt, or cash).

Takeovers can occur by acquisition, proxy contests, and going-private transactions. Thus takeovers encompass a broader set of activities than acquisitions, as depicted in Fig. 29.1.

If a takeover is achieved by acquisition, it will be by merger, tender offer for shares of equity, or purchase of assets. In mergers and tender offers the acquiring firm buys the voting ordinary shares of the acquired firm.

Proxy contests can result in takeovers as well. Proxy contests occur when a group of share-holders attempts to gain seats on the board of directors. A proxy is written authorization for one shareholder to vote for another shareholder. In a proxy contest an insurgent group of shareholders solicits proxies from other shareholders.

In going-private transactions a small group of investors purchases all the equity shares of a public firm. The group usually includes members of incumbent management and some outside investors. The shares of the firm are delisted from the stock exchange, and can no longer be purchased in the open market.

29.2 Synergy

The previous section discussed the basic forms of acquisition. We now examine why firms are acquired. (Although the previous section pointed out that acquisitions and mergers

Figure 29.1 Varieties of takeover

F I G U R E29.1

Acquisition Proxy contest Takeovers Going private Merger or consolidation Acquisition of shares Acquisition of assets Finanza aziendaleSynergy

787

___

___

have different definitions, these differences will be unimportant in this, and many of thefollowing, sections. Thus, unless otherwise stated, we shall refer to acquisitions and mergers synonymously.)

Much of our thinking here can be organized around the following four questions: Is there a rational reason for mergers? Yes – in a word,

1 synergy.

Suppose firm A is contemplating acquiring firm B. The value of firm A is VA and the value of firm B is VB. (It is reasonable to assume that, for public companies, VA and VB can be determined by observing the market prices of the outstanding securities.) The difference between the value of the combined firm (VAB) and the sum of the values of the firms as separate entities is the synergy from the acquisition:

Synergy = VAB – (VA + VB)

In words, synergy occurs if the value of the combined firm after the merger is greater than the sum of the value of the acquiring firm and the value of the acquired firm before the merger.

Where does this magic force, synergy, come from?

2

Increases in cash flow create value. We define ΔCFtas the difference between the cash flows at date t of the combined firm and the sum of the cash flows of the two separate firms. From the chapters about capital budgeting, we know that the cash flow in any period t can be written as

ΔCFt = ΔRevt – ΔCostst – ΔTaxest – ΔCapital Requirementst

where ΔRevtis the incremental revenue of the acquisition, ΔCoststis the incremental costs of the acquisition, ΔTaxestis the incremental acquisition taxes, and ΔCapital Requirementst is the incremental new investment required in working capital and fixed assets.

It follows from our classification of incremental cash flows that the possible sources of synergy fall into four basic categories: revenue enhancement, cost reduction, lower taxes, and lower capital requirements. Improvements in at least one of these four categories create synergy. Each of these categories will be discussed in detail in the next section.

In addition, reasons are often provided for mergers where improvements are not expected in any of these four categories. These ‘bad’ reasons for mergers will be discussed in Sec. 29.4.

How are these synergistic gains shared? In general, the acquiring firm pays a premium for

3

the acquired, or target, firm. For example, if the equity of the target is selling for $50, the acquirer might need to pay $60 a share, implying a premium of $10 or 20 per cent. The gain to the target in this example is $10. Suppose that the synergy from the merger is $30. The gain to the acquiring firm, or bidder, would be $20 (= $30 − $10). The bidder would actually lose if the synergy were less than the premium of $10. A more detailed treatment of these gains or losses will be provided in Sec. 29.6.

Are there other motives for a merger besides synergy? Yes.

4

As we have said, synergy is a source of benefit to shareholders. However, the managers are likely to view a potential merger differently. Even if the synergy from the merger is less than the premium paid to the target, the managers of the acquiring firm may still benefit. For example, the revenues of the combined firm after the merger will almost certainly be greater than the revenues of the bidder before the merger. The managers may receive higher compensation once they are managing a larger firm. Even beyond the increase in compensation, managers generally experience greater prestige and power when managing a larger firm. Conversely, the managers of the target could lose their jobs after the acquisition, and they might very well oppose the takeover even if their share-holders would benefit from the premium. These issues will be discussed in more detail in Sec. 29.9.

___

29.3 Sources of Synergy

In this section, we discuss sources of synergy.

Revenue Enhancement

A combined firm may generate greater revenues than two separate firms. Increased revenues can come from marketing gains, strategic benefits, or market power.

Marketing Gains It is frequently claimed that, because of improved marketing, mergers and acquisitions can increase operating revenues. Improvements can be made in the following areas:

Previously ineffective media programming and advertising efforts

1

A weak existing distribution network

2

An unbalanced product mix

3

Strategic Benefits Some acquisitions promise a strategic benefit, which is more like an option than a standard investment opportunity. For example, imagine that a sewing machine company acquires a computer company. The firm will be well positioned if technological advances allow computer-driven sewing machines in the future.

Michael Porter has used the word beachhead to denote the strategic benefits from entering a new industry.3 He uses the example of Procter & Gamble’s acquisition of the Charmin Paper Company as a beachhead that allowed Procter & Gamble to develop a highly interrelated cluster of paper products – disposable nappies, paper towels, feminine hygiene products, and bathroom tissue.

Market or Monopoly Power One firm may acquire another to reduce competition. If so, prices can be increased, generating monopoly profits. However, mergers that reduce competition do not benefit society, and the government regulators may challenge them.

Cost Reduction

A combined firm may operate more efficiently than two separate firms. This was one the primary reason for the Lloyds TSB–HBOS merger. A merger can increase operating efficiency in the following ways.

Economies of Scale An economy of scale means that the average cost of production falls as the level of production increases. Fig. 29.2 illustrates the relation between cost per unit and size for a typical firm. As can be seen, average cost first falls and then rises. In other words, the firm experiences economies of scale until optimal firm size is reached. Diseconomies of scale arise after that.

Though the precise nature of economies of scale is not known, it is one obvious benefit of horizontal mergers. The phrase spreading overhead is frequently used in connection with economies of scale. This refers to sharing central facilities such as corporate headquarters, top management, and computer systems.

Economies of Vertical Integration Operating economies can be gained from vertical com-binations as well as from horizontal comcom-binations. The main purpose of vertical acquisitions is to make co-ordination of closely related operating activities easier. This is probably why most forest product firms that cut timber also own sawmills and hauling equipment. Because petroleum is used to make plastics and other chemical products, the DuPont–Conoco merger was motivated by DuPont’s need for a steady supply of oil. Economies from vertical integration probably explain why most airline companies own airplanes. They may also explain why some airline companies have purchased hotels and car rental companies.

Technology Transfer Technology transfer is another reason for merger. An automobile manufacturer might well acquire an aircraft company if aerospace technology can improve Finanza aziendale

Sources of Synergy

789

___

___

automotive quality. This technology transfer was the motivation behind the merger of GeneralMotors and Hughes Aircraft.

Complementary Resources Some firms acquire others to improve usage of existing resources. A ski equipment store merging with a tennis equipment store will smooth sales over both the winter and summer seasons, thereby making better use of store capacity.

Elimination of Inefficient Management A change in management can often increase firm value. Some managers overspend on perquisites and pet projects, making them ripe for take- over. Alternatively, incumbent managers may not understand changing market conditions or new technology, making it difficult for them to abandon old strategies. Although the board of directors should replace these managers, the board is often unable to act independently. Thus a merger may be needed to make the necessary replacements.

Mergers and acquisitions can be viewed as part of the labour market for top management. Michael Jensen and Richard Ruback have used the phrase ‘market for corporate control’, in which alternative management teams compete for the rights to manage corporate activities.4

Tax Gains

Tax reduction may be a powerful incentive for some acquisitions. This reduction can come from: The use of tax losses

1

The use of unused debt capacity

2

The use of surplus funds

3

Net Operating Losses A firm with a profitable division and an unprofitable one will have a low tax bill, because the loss in one division offsets the income in the other. However, if the two divisions are actually separate companies, the profitable firm will not be able to use the losses of the unprofitable one to offset its income. Thus, in the right circumstances, a merger can lower taxes.

Consider Table 29.1, which shows pre-tax income, taxes and after-tax income for firms A and B. Firm A earns $200 in state 1 but loses money in state 2. The firm pays taxes in state 1 but is not entitled to a tax rebate in state 2. Conversely, firm B turns a profit in state 2 but

Figure 29.2 Economies of scale and the

optimal size of the firm

F I G U R E

29.2

Cost per unit

Minimum cost

Economies of

scale Diseconomiesof scale

Optimal size Size

___

not in state 1. This firm pays taxes only in state 2. The table shows that the combined tax bill of the two separate firms is always $68, regardless of which state occurs.

However, the last two columns of the table show that, after a merger, the combined firm will pay taxes of only $34. Taxes drop after the merger, because a loss in one division offsets the gain in the other.

The message of this example is that firms need taxable profits to take advantage of potential losses. These losses are often referred to as net operating losses or NOL for short. Mergers can sometimes bring losses and profits together. However, there are two qualifications to the pre- vious example:

Many countries’ tax laws permit firms that experience alternating periods of profits and

1

losses to equalize their taxes by carry-back and carry-forward provisions. For example, a firm that has been profitable but has a loss in the current year may be able to get refunds of income taxes paid in three previous years and can carry the loss forward for 15 years. Thus a merger to exploit unused tax shields must offer tax savings over and above what can be accomplished by firms via carry-overs.5

Tax authorities in many countries are likely to disallow an acquisition if its principal

2

purpose is to avoid the payment of taxes.

Debt Capacity There are at least two cases where mergers allow for increased debt and a larger tax shield. In the first case the target has too little debt, and the acquirer can infuse the target with the missing debt. In the second case both target and acquirer have optimal debt levels. A merger leads to risk reduction, generating greater debt capacity and a larger tax shield. We treat each case in turn.

Case 1: Unused Debt Capacity In Chapter 16 we pointed out that every firm has a certain amount of debt capacity. This debt capacity is beneficial, because greater debt leads to a greater tax shield. More formally, every firm can borrow a certain amount before the marginal costs of financial distress equal the marginal tax shield. This debt capacity is a function of many factors, perhaps the most important being the risk of the firm. Firms with high risk generally cannot borrow as much as firms with low risk. For example, a utility or a supermarket – both firms with low risk – can have a higher debt-to-value ratio than can a technology firm.

Some firms, for whatever reason, have less debt than is optimal. Perhaps the managers are risk-averse, or perhaps they simply don’t know how to assess debt capacity properly. Is it bad for a firm to have too little debt? The answer is yes. As we have said, the optimal level of debt occurs when the marginal cost of financial distress equals the marginal tax shield. Too little debt reduces firm value.

This is where mergers come in. A firm with little or no debt is an inviting target. An acquirer could raise the target’s debt level after the merger to create a bigger tax shield.

TA B L E

29.1

Table 29.1 Tax effect of merger of firms A and B

Before merger After merger

Firm A Firm B Firm AB

If state 1 If state 2 If state 1 If state 2 If state 1 If state 2 Taxable income (C) 200 −100 −100 200 100 100 Taxes (C) 68 0 0 68 34 34 Net income (C) 132 −100 −100 132 66 66

Neither firm will be able to deduct its losses prior to the merger. The merger allows the losses from A to offset the taxable profits from B – and vice versa.

Two ‘Bad’ Reasons for Mergers

791

___

___

Case 2: Increased Debt Capacity Let us move back to the principles of modern portfolio theory, as presented in Chapter 10. Consider two equities in different industries, where both equities have the same risk or standard deviation. A portfolio of these two equities has lower risk than that of either equity separately. In other words, the two-equity portfolio is somewhat diversified, whereas each equity by itself is completely undiversified.6

Now, rather than considering an individual buying both equities, consider a merger between the two underlying firms. Because the risk of the combined firm is less than that of either one separately, banks should be willing to lend more money to the combined firm than the total of what they would lend to the two firms separately. In other words, the risk reduction that the merger generates leads to greater debt capacity.

For example, imagine that each firm can borrow £100 on its own before the merger. Perhaps the combined firm after the merger will be able to borrow £250. Debt capacity has increased by £50 (= £250 − £200).

Remember that debt generates a tax shield. If debt rises after the merger, taxes will fall. That is, simply because of the greater interest payments after the merger, the tax bill of the combined firm should be less than the sum of the tax bills of the two separate firms before the merger. In other words, the increased debt capacity from a merger can reduce taxes.

To summarize, we first considered the case where the target had too little leverage. The acquirer could infuse the target with more debt, generating a greater tax shield. Next, we considered the case where both target and acquirer began with optimal debt levels. A merger leads to more debt even here. That is, the risk reduction from the merger creates greater debt capacity and thus a greater tax shield.

Surplus Funds Another quirk in the tax laws involves surplus funds. Consider a firm that has free cash flow. That is, it has cash flow available after payment of all taxes, and after all positive net present value projects have been funded. In this situation, aside from purchasing securities, the firm can either pay dividends or buy back shares.

We have already seen in our previous discussion of dividend policy that an extra dividend will increase the income tax paid by some investors. Investors pay lower taxes in a share repurchase.7 However, a share repurchase is not normally a legal option if the sole purpose is to avoid taxes on dividends.

Instead, the firm might make acquisitions with its excess funds. Here, the shareholders of the acquiring firm avoid the taxes they would have paid on a dividend.8

Reduced Capital Requirements

Earlier in this chapter we stated that, owing to economies of scale, mergers can reduce operat-ing costs. It follows that mergers can reduce capital requirements as well. Accountants typically divide capital into two components: fixed capital and working capital.

When two firms merge, the managers will probably find duplicate facilities. For example, if both firms had their own headquarters, all executives in the merged firm could be moved to one headquarters building, allowing the other headquarters to be sold. Some plants might be redundant as well. Or two merging firms in the same industry might consolidate their research and development, permitting some R&D facilities to be sold.

The same goes for working capital. The inventory-to-sales ratio and the cash-to-sales ratio often decrease as firm size increases. A merger permits these economies of scale to be realized, allowing a reduction in working capital.

29.4 Two ‘Bad’ Reasons for Mergers

Earnings Growth

An acquisition can create the appearance of earnings growth, perhaps fooling investors into thinking that the firm is worth more than it really is. Let’s consider two companies, Global Resources and Regional Enterprises, as depicted in the first two columns of Table 29.2. As can Finanza aziendale

___

be seen, earnings per share are $1 for both companies. However, Global sells for $25 per share, implying a price–earnings (P/E) ratio of 25 (= 25/1). By contrast, Regional sells for $10, imply-ing a P/E ratio of 10. This means that an investor in Global pays $25 to get $1 in earnings, whereas an investor in Regional receives the same $1 in earnings on only a $10 investment. Are investors getting a better deal with Regional? Not necessarily. Perhaps Global’s earnings are expected to grow faster than Regional’s earnings. If this is the case, an investor in Global will expect to receive high earnings in later years, making up for low earnings in the short term. In fact, Chapter 5 argues that the primary determinant of a firm’s P/E ratio is the market’s expectation of the firm’s growth rate in earnings.

Now let’s imagine that Global acquires Regional, with the merger creating no value. If the market is smart, it will realize that the combined firm is worth the sum of the values of the separate firms. In this case, the market value of the combined firm will be $3,500, which is equal to the sum of the values of the separate firms before the merger.

At these values Global will acquire Regional by exchanging 40 of its shares for 100 shares of Regional, so that Global will have 140 shares outstanding after the merger.9 Global’s share price remains at $25 (= $3,500/140). With 140 shares outstanding and $200 of earnings after the merger, Global earns $1.43 (= $200/140) per share after the merger. Its P/E ratio becomes 17.5 (= 25/1.43), a drop from 25 before the merger. This scenario is represented by the third column of Table 29.2. Why has the P/E dropped? The combined firm’s P/E will be an average of Global’s high P/E and Regional’s low P/E before the merger. This is common sense once you think about it. Global’s P/E should drop when it takes on a new division with low growth.

Let us now consider the possibility that the market is fooled. As we just said, the acquisi-tion enables Global to increase its earnings per share from $1 to $1.43. If the market is fooled, it might mistake the 43 per cent increase in earnings per share for true growth. In this case, the price–earnings ratio of Global may not fall after the merger. Suppose the price–earnings ratio of Global remains at 25. The total value of the combined firm will increase to $5,000 (= 25 × $200), and the share price of Global will increase to $35.71 (= $5,000/140). This is reflected in the last column of the table.

This is earnings growth magic. Can we expect this magic to work in the real world? Managers of a previous generation certainly thought so, with firms such as LTV Industries, ITT and Litton Industries all trying to play the P/E-multiple game in the 1960s. However, in hindsight it looks as if they played the game without much success. These operators have all dropped out, with few, if any, replacements. It appears that the market is too smart to be fooled this easily.

TA B L E

29.2

Table 29.2 Financial positions of Global Resources and Regional Enterprises

Global Resources before merger Regional Enterprises before merger Global Resources after merger The market is ‘smart’ The market is ‘fooled’

Earnings per share (C) 1.00 1.00 1.43 1.43

Price per share (C) 25.00 10.00 25.00 35.71

Price–earnings ratio 25 10 17.5 25

Number of shares 100 100 140 140

Total earnings (C) 100 100 200 200

Total value (C) 2,500 1,000 3,500 5,000

Exchange ratio: 1 share in Global for 2.5 shares in Regional.

A Cost to Shareholders from Reduction in Risk

793

___

___

Diversification

Diversification is often mentioned as a benefit of one firm acquiring another. However, we argue that diversification, by itself, cannot produce increases in value. To see this, recall that a business’s variability of return can be separated into two parts: (a) what is specific to the business, and called unsystematic; and (2) what is systematic, because it is common to all businesses.

Systematic variability cannot be eliminated by diversification, so mergers will not eliminate this risk at all. By contrast, unsystematic risk can be diversified away through mergers. However, the investor does not need widely diversified companies such as Unilever to eliminate unsys-tematic risk. Shareholders can diversify more easily than corporations by simply purchasing equity in different corporations. For example, instead of Air France and KLM merging to form Air France-KLM, the shareholders of Air France could have purchased shares in KLM if they believed there would be diversification gains in doing so. Thus diversification through merger may not benefit shareholders.10

Diversification can produce gains to the acquiring firm only if one of two things is true: Diversification decreases the unsystematic variability at a lower cost than by investors’

1

adjustments to personal portfolios. This seems very unlikely.

Diversification reduces risk and thereby increases debt capacity. This possibility was

2

mentioned earlier in the chapter.

29.5 A Cost to Shareholders from Reduction in Risk

In Chapter 22 we used option pricing theory to show that pure financial mergers are bad for shareholders. In this section we shall revisit this idea from an alternative perspective and show that the diversification effects of mergers can benefit bondholders at the expense of shareholders.

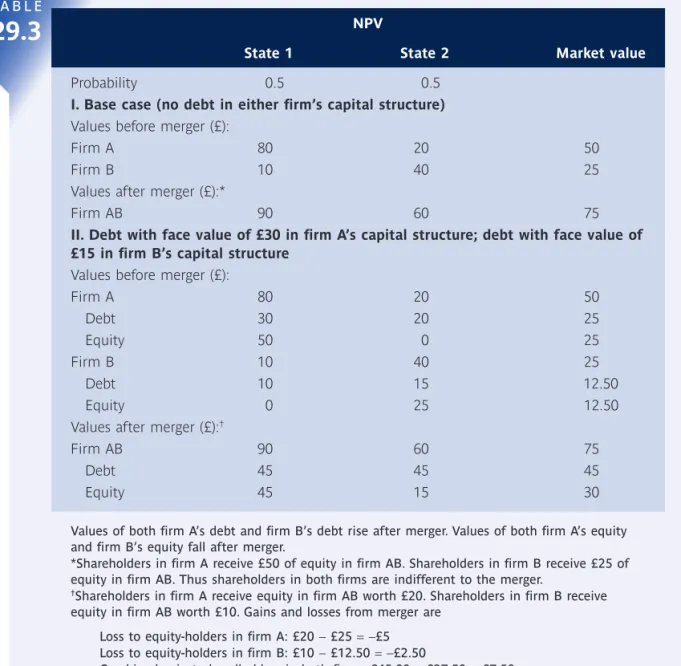

The Base Case

Consider an example where firm A acquires firm B. Panel I of Table 29.3 shows the net present values of firm A and firm B prior to the merger in the two possible states of the economy. Because the probability of each state is 0.50, the market value of each firm is the average of its values in the two states. For example, the market value of firm A is

0.5 × £80 + 0.5 × £20 = £50

Now imagine that the merger of the two firms generates no synergy. The combined firm AB will have a market value of £75 (= £50 + £25), the sum of the values of firm A and firm B. Further imagine that the shareholders of firm B receive equity in AB equal to firm B’s stand-alone market value of £25. In other words, firm B receives no premium. Because the value of AB is £75, the shareholders of firm A have a value of £50 (= £75 − £25) after the merger – just what they had before the merger. Thus the shareholders of both firms A and B are indifferent to the merger.

Both Firms Have Debt

Alternatively, imagine that firm A has debt with a face value of £30 in its capital structure, as shown in Panel II of Table 29.3. Without a merger, firm A will default on its debt in state 2, because the value of firm A in this state is £20, less than the face value of the debt of £30. As a consequence, firm A cannot pay the full value of the debt claim: the bondholders receive only £20 in this state. The creditors take the possibility of default into account, valuing the debt at £25 (= 0.5 × £30 + 0.5 × £20).

Firm B’s debt has a face value of £15. Firm B will default in state 1 because the value of the firm in this state is £10, less than the face value of the debt of £15. The value of firm B’s debt is £12.50 (= 0.5 × £10 + 0.5 × £15). It follows that the sum of the value of firm A’s debt and the value of firm B’s debt is £37.50 (= £25 + £12.50).

___

Now let’s see what happens after the merger. Firm AB is worth £90 in state 1 and £60 in state 2, implying a market value of £75 (= 0.5 × £90 + 0.5 × £60). The face value of the debt in the combined firm is £45 (= £30 + £15). Because the value of the firm is greater than £45 in either state, the bondholders always get paid in full. Thus the value of the debt is its face value of £45. This value is £7.50 greater than the sum of the values of the two debts before the merger, which we just found to be £37.50. Therefore the merger benefits the bondholders.

What about the shareholders? Because the equity of firm A was worth £25 and the equity of firm B was worth £12.50 before the merger, let’s assume that firm AB issues two shares to firm A’s shareholders for every share issued to firm B’s shareholders. Firm AB’s equity is £30, so firm A’s shareholders get shares worth £20 and firm B’s shareholders get shares worth £10. Firm A’s shareholders lose £5 (= £20 − £25) from the merger. Similarly, firm B’s shareholders lose £2.50 (= £10 − £12.50). The total loss to the shareholders of both firms is £7.50, exactly the gain to the bondholders from the merger.

There are a lot of numbers in this example. The point is that the bondholders gain £7.50 and the shareholders lose £7.50 from the merger. Why does this transfer of value occur? To TA B L E

29.3

Table 29.3 Equity-swap mergers

NPV

State 1 State 2 Market value

Probability 0.5 0.5

I. Base case (no debt in either firm’s capital structure) Values before merger (£):

Firm A 80 20 50

Firm B 10 40 25

Values after merger (£):*

Firm AB 90 60 75

II. Debt with face value of £30 in firm A’s capital structure; debt with face value of £15 in firm B’s capital structure

Values before merger (£):

Firm A 80 20 50 Debt 30 20 25 Equity 50 0 25 Firm B 10 40 25 Debt 10 15 12.50 Equity 0 25 12.50

Values after merger (£):†

Firm AB 90 60 75

Debt 45 45 45

Equity 45 15 30

Values of both firm A’s debt and firm B’s debt rise after merger. Values of both firm A’s equity and firm B’s equity fall after merger.

*Shareholders in firm A receive £50 of equity in firm AB. Shareholders in firm B receive £25 of equity in firm AB. Thus shareholders in both firms are indifferent to the merger.

†Shareholders in firm A receive equity in firm AB worth £20. Shareholders in firm B receive equity in firm AB worth £10. Gains and losses from merger are

Loss to equity-holders in firm A: £20 − £25 =−£5 Loss to equity-holders in firm B: £10 − £12.50 =−£2.50

Combined gain to bondholders in both firms: £45.00 − £37.50 = £7.50

The NPV of a Merger

795

___

___

see what is going on, notice that when the two firms are separate, firm B does not guaranteefirm A’s debt. That is, if firm A defaults on its debt, firm B does not help the bondholders of firm A. However, after the merger the bondholders can draw on the cash flows from both A and B. When one of the divisions of the combined firm fails, creditors can be paid from the profits of the other division. This mutual guarantee, which is called the co-insurance effect, makes the debt less risky and more valuable than before.

There is no net benefit to the firm as a whole. The bondholders gain the co-insurance effect, and the shareholders lose the co-insurance effect. Some general conclusions emerge from the preceding analysis:

Mergers usually help bondholders. The size of the gain to bondholders depends on the

1

reduction in the probability of bankruptcy after the combination. That is, the less risky the combined firm is, the greater are the gains to bondholders.

Shareholders of the acquiring firm are hurt by the amount that bondholders gain.

2

Conclusion 2 applies to mergers without synergy. In practice, much depends on the size

3

of the synergy.

How Can Shareholders Reduce Their Losses from

the Co-insurance Effect?

The co-insurance effect raises bondholder values and lowers shareholder values. However, there are at least two ways in which shareholders can reduce or eliminate the co-insurance effect. First, the shareholders in firm A could retire its debt before the merger announcement date and reissue an equal amount of debt after the merger. Because debt is retired at the low pre-merger price, this type of refinancing transaction can neutralize the co-insurance effect to the bondholders.

Also, note that the debt capacity of the combined firm is likely to increase, because the acquisition reduces the probability of financial distress. Thus the shareholders’ second alter- native is simply to issue more debt after the merger. An increase in debt following the merger will have two effects, even without the prior action of debt retirement. The interest tax shield from new corporate debt raises firm value, as discussed in an earlier section of this chapter. In addition, an increase in debt after the merger raises the probability of financial distress, thereby reducing or eliminating the bondholders’ gain from the co-insurance effect.

29.6 The NPV of a Merger

Firms typically use NPV analysis when making acquisitions. The analysis is relatively straight-forward when the consideration is cash. The analysis becomes more complex when the consideration is equity.

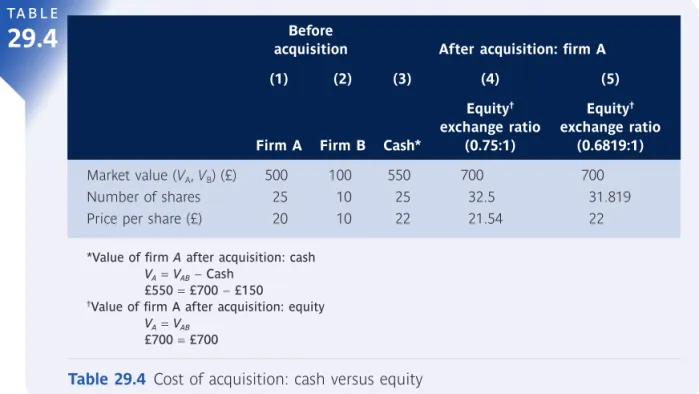

Cash

Suppose firm A and firm B have values as separate entities of £500 and £100, respectively. They are both all-equity firms. If firm A acquires firm B, the merged firm AB will have a combined value of £700 due to synergies of £100. The board of firm B has indicated that it will sell firm B if it is offered £150 in cash.

Should firm A acquire firm B? Assuming that firm A finances the acquisition out of its own retained earnings, its value after the acquisition is11

Value of firm A after the acquisition = Value of combined firm − Cash paid = £700 − £150

= £550

Because firm A was worth £500 prior to the acquisition, the NPV to firm A’s equity-holders is

£50 = £550 − £500 (29.1)

___

Assuming that there are 25 shares in firm A, each share of the firm is worth £20 (= £500/25) prior to the merger and £22 (= £550/25) after the merger. These calculations are displayed in the first and third columns of Table 29.4. Looking at the rise in equity price, we conclude that firm A should make the acquisition.

We spoke earlier of both the synergy and the premium of a merger. We can also value the NPV of a merger to the acquirer:

NPV of a merger to acquirer = Synergy − Premium

Because the value of the combined firm is £700 and the pre-merger values of A and B were £500 and £100, respectively, the synergy is £100 [= £700 − (£500 + £100)]. The premium is £50 (= £150 − £100). Thus the NPV of the merger to the acquirer is

NPV of merger to firm A = £100 − £50 = £50

One caveat is in order. This textbook has consistently argued that the market value of a firm is the best estimate of its true value. However, we must adjust our analysis when discuss-ing mergers. If the true price of firm A without the merger is £500, the market value of firm A may actually be above £500 when merger negotiations take place. This happens because the market price reflects the possibility that the merger will occur. For example, if the probability is 60 per cent that the merger will take place, the market price of firm A will be

£530 = £550 × Market value of firm A with merger Probabbility of merger Market value of firm A withou 0 60. + tt merger Probability of no merger £500 × 0 40.

The managers would underestimate the NPV from the merger in Eq. (29.1) if the market price of firm A is used. Thus managers face the difficult task of valuing their own firm without the acquisition.

TA B L E

29.4

Table 29.4 Cost of acquisition: cash versus equity

Before

acquisition After acquisition: firm A

(1) (2) (3) (4) (5)

Firm A Firm B Cash*

Equity† exchange ratio (0.75:1) Equity† exchange ratio (0.6819:1) Market value (VA, VB) (£) 500 100 550 700 700 Number of shares 25 10 25 32.5 31.819

Price per share (£) 20 10 22 21.54 22

*Value of firm A after acquisition: cash VA=VAB− Cash

£550 = £700 − £150

†Value of firm A after acquisition: equity VA=VAB

£700 = £700

The NPV of a Merger

797

___

___

Equity

Of course, firm A could purchase firm B with equity instead of cash. Unfortunately, the analysis is not as straightforward here. To handle this scenario we need to know how many shares are outstanding in firm B. We assume that there are 10 shares outstanding, as indicated in column 2 of Table 29.4.

Suppose firm A exchanges 7.5 of its shares for the entire 10 shares of firm B. We call this an exchange ratio of 0.75:1. The value of each share of firm A’s equity before the acquisition is £20. Because 7.5 × £20 = £150, this exchange appears to be the equivalent of purchasing firm B in cash for £150.

This is incorrect: the true cost to firm A is greater than £150. To see this, note that firm A has 32.5 (= 25 + 7.5) shares outstanding after the merger. Firm B shareholders own 23 per cent (= 7.5/32.5) of the combined firm. Their holdings are valued at £161 (= 23% × £700). Because these shareholders receive equity in firm A worth £161, the cost of the merger to firm A’s shareholders must be £161, not £150.

This result is shown in column 4 of Table 29.4. The value of each share of firm A’s equity after an equity-for-equity transaction is only £21.54 (= £700/32.5). We found out earlier that the value of each share is £22 after a cash-for-equity transaction. The difference is that the cost of the equity-for-equity transaction to firm A is higher.

This non-intuitive result occurs because the exchange ratio of 7.5 shares of firm A for 10 shares of firm B was based on the pre-merger prices of the two firms. However, because the equity of firm A rises after the merger, firm B equity-holders receive more than £150 in firm A equity.

What should the exchange ratio be so that firm B equity-holders receive only £150 of firm A’s equity? We begin by defining a, the proportion of the shares in the combined firm that firm B’s shareholders own. Because the combined firm’s value is £700, the value of firm B shareholders after the merger is

Value of firm Bshareholders after merger:

a × £700

Setting a × £700 = £150, we find that a = 21.43%. In other words, firm B’s shareholders will receive equity worth £150 if they receive 21.43 per cent of the firm after merger.

Now we determine the number of shares issued to firm B’s shareholders. The proportion, a, that firm B’s shareholders have in the combined firm can be expressed as follows:

α = New shares issued Old shares New shares issued+ ==

+

New shares issued 25 New shares issued Plugging our value of a into the equation yields

0.2143 New shares issued 25 New shares issued =

+ Solving for the unknown, we have

New shares = 819 shares

Total shares outstanding after the merger are 31.819 (=+ 6.819). Because 6.819 shares of firm A are exchanged for 10 shares of firm B, the exchange ratio is 0.6819:1.

Results at the exchange ratio of 0.6819:1 are displayed in column 5 of Table 29.4. Because there are now 31.819 shares, each share of equity is worth £22 (= 00/31.819), exactly what it is worth in the equity-for-cash transaction. Thus, given that the board of firm B Finanza aziendale

___

will sell its firm for £150, this is the fair exchange ratio, not the ratio of 0.75:1 mentioned earlier.

Cash versus Equity

In this section we have examined both cash deals and equity-for-equity deals. Our analysis leads to the following question: When do bidders want to pay with cash and when do they want to pay with equity? There is no easy formula: the decision hinges on a few variables, with perhaps the most important being the price of the bidder’s equity.

In the example of Table 29.4, firm A’s market price per share prior to the merger was £20. Let’s now assume that at the time firm A’s managers believed the ‘true’ price was £15. In other words, the managers believed that their equity was overvalued. Is it likely for managers to have a different view than that of the market? Yes – managers often have more information than the market does. After all, managers deal with customers, suppliers and employees daily, and are likely to obtain private information.

Now imagine that firm A’s managers are considering acquiring firm B with either cash or equity. The overvaluation would have no impact on the merger terms in a cash deal; firm B would still receive £150 in cash. However, the overvaluation would have a big impact on a share-for-share deal. Although firm B receives £150 worth of A’s equity as calculated at market prices, firm A’s managers know that the true value of the equity is less than £150.

How should firm A pay for the acquisition? Clearly, firm A has an incentive to pay with equity, because it would end up giving away less than £150 of value. This conclusion might seem rather cynical, because firm A is, in some sense, trying to cheat firm B’s shareholders. However, both theory and empirical evidence suggest that firms are more likely to acquire with equity when their own equities are overvalued.12

The story is not quite this simple. Just as the managers of firm A think strategically, firm B’s managers are likely to think this way as well. Suppose that in the merger negotiations firm A’s managers push for a share-for-share deal. This might tip off firm B’s managers that firm A is overpriced. Perhaps firm B’s managers will ask for better terms than firm A is currently offering. Alternatively, firm B may resolve to accept cash or not to sell at all. And just as firm B learns from the negotiations, the market learns also. Empirical evidence shows that the acquirer’s equity price generally falls upon the announcement of a equity-for-equity deal.13

29.7 Valuation of Mergers in Practice

The previous section provided the tools of merger valuation. However, in practice the approach to valuation is significantly more complex and subjective. Mergers and acquisitions have two distinct differences from the typical investment project that a firm will undertake. First, the size of a merger will be significantly larger, which means that the risks of mis-evaluation are substantially higher. If an acquiring firm arrives at the wrong value of a target it may destroy both companies. A good example of this is the Royal Bank of Scotland acquisition of the Dutch bank ABN AMRO in 2007, when the Royal Bank of Scotland (with Fortis Bank and Banco Santander) bought ABN AMRO for £49 billion. The acquisition took place just before the collapse in bank valuations because of the global credit crunch. Two years later, in 2009, the Royal Bank of Scotland revalued the acquisition and reported a resultant £28 billion loss. The bank was subsequently bailed out by the British government, and most of the directors lost their jobs.

The second difference is that if the target company is listed on a stock exchange, the share price can be used as an indicator of the value of the target’s equity. While this makes things intuitively easier, because of the run-up in target valuations when takeover bids are rumoured, share price valuations may be too high if the current share price is used. As the previous section shows, this may lead to the wrong bid price being tabled.

When considering a potential target for acquisition or merger, both firms should evaluate a variety of scenarios and consider the various embedded options that exist in most firms (see Chapter 8). We suggest that acquiring firms take the following steps to evaluate prospec-tive targets.

Valuation of Mergers in Practice

799

___

___

Stage 1: Value the Target as a Stand-Alone Firm

The first stage in the valuation process is to consider the target as a stand-alone entity. This is the base-case valuation upon which the merger can be assessed. To value a company requires estimates of future cash flows and the appropriate rates for discounting the cash flows. The initial valuation should then be compared with the current share price of the target to form an initial opinion of the merger.

Stage 2: Calibrate the Valuation

It is very unlikely that your initial valuation of the target firm will be equal to its share price, and any differential in valuations needs to be explained. As mentioned in the previous section, share prices may also reflect takeover probabilities and potential takeover premiums. In addi-tion, the share price may not incorporate private information that has been gained as a result of your in-depth analysis. For example, private information could be provided by the manage-ment of the target firm if the merger is friendly and fully supported by the target’s board. Alternatively, new information may have been discovered in the course of your investigations. Because the effort in this phase is so great, and the analysis so extensive, it is possible that your valuation may be better than the share price of the market. This is especially true if the target firm is listed on a small exchange or emerging market, where valuations may not be so accurate.

If you do not have more information than the market, and there is still a difference between your valuation and the share price, it is highly probable that your valuation is incorrect. In other words, your estimate of future cash flows and discount rates will be different from that of the market. At this point it is strongly recommended that you revisit your assumptions to see whether anything can be improved. It is imperative that you get your assumptions right, because they are the building blocks for the rest of your analysis.

Stage 3: Value the Synergies

Whereas stages 1 and 2 focus on your initial valuation of the target, stage 3 concerns your assessment of the benefits of a possible merger or acquisition. To do this, you must value the synergies associated with combining the target and the acquirer. In the same way as you initially valued the target firm, you value synergies by estimating the cash flows generated by the synergies along with the appropriate discount rates. Some synergies are easier to predict, but others are considerably more difficult. For example, synergies that come from tax savings or reductions in fixed costs are easier to predict than increased sales or reductions in variable costs.

The future cash flows and the discount rates used in the base-case valuation are likely to be used in valuing risky synergies. For example, you may believe that the proposed merger will lead to a 10 per cent increase in the target’s cash flows in the five years after the merger. Valuing this synergy will require both the pre-acquisition discount rate and the cash flows of the target. In addition, valuing synergies may also require an estimate of the acquiring firm’s cost of capital and expected cash flows. Hence the acquiring firm will want to use the procedures outlined in stages 1 and 2 to value its own equity and calibrate its cost of capital and cash flows.

When synergies are valued, it is important to discount cash flows arising from the synergy using the weighted average of both firms’ cost of capital. For example, as a result of the disastrous conditions in the automobile market in 2009, Fiat entered into merger talks with Chrysler. The reason for the merger was that Fiat would have access to the North American car market and Chrysler would be able to increase its presence in Europe. Assume that, as a result of the merger, both companies would increase their pre-tax profits by 10 per cent per year. Given that the gain in each year is proportional to the pre-acquisition cash flows of both firms, the appropriate discount rate would be an equally weighted average of the two firm’s costs of capital.

The Fiat–Chrysler example illustrates a case where synergies affect both parties to the merger equally. However, this will not always be the case. If the merger was expected to result in a proportional increase in Fiat’s profits, but not Chrysler’s, then you would use Fiat’s cost of capital to value the synergy.

___

Because the major gain from the merger is Fiat’s penetration of the North American market, there will be many strategic options open to the company once it starts operations. Consequently, it might be better to consider valuing the synergy as a strategic option, using the real options methodology in Chapters 8 and 22, instead of the risk-adjusted discount rate method. When a firm expands into a new market, it has the option to expand further if prospects turn out to be more favourable than originally anticipated, and to exit if the situation turns out to be unfavourable. In these situations an investment may be substantially undervalued when such options are ignored.

Stage 4: Value the Merger

The final part of the analysis is to add the base-case valuation of the target to the value of the synergies from the merger or acquisition. The rule of thumb is that the merger or acquisi-tion should go ahead if the costs of the merger, which include the bid premium as well as all transaction costs, are lower than the combined value of the merger.

29.8 Friendly versus Hostile Takeovers

Mergers are generally initiated by the acquiring, not the acquired, firm. Thus the acquirer must decide to purchase another firm, select the tactics to effect the merger, determine the highest price it is willing to pay, set an initial bid price, and make contact with the target firm. Often the CEO of the acquiring firm simply calls on the CEO of the target and proposes a merger. Should the target be receptive, a merger eventually occurs. Of course, there may be many meetings, with negotiations over price, terms of payment, and other parameters. The target’s board of directors generally has to approve the acquisition. Sometimes the bidder’s board must also give its approval. Finally, an affirmative vote by the shareholders is needed. But when all is said and done, an acquisition that proceeds in this way is viewed as friendly.

Of course, not all acquisitions are friendly. The target’s management may resist the merger, in which case the acquirer must decide whether to pursue the merger and, if so, what tactics to use. Facing resistance, the acquirer may begin by purchasing some of the target’s equity in secret. This position is often called a toehold. Regulation in almost every country requires that an institution or individual disclose their holding in a company once a specific percentage ownership threshold is passed. For example, in the UK, an acquiring company must disclose any holdings above 3 per cent and provide detailed information, including its intentions and its position in the target. Secrecy ends at this point, because the acquirer must state that it plans to acquire the target. The price of the target’s shares will probably rise after the disclosure, with the new equity price reflecting the possibility that the target will be bought out at a premium.

Although the acquirer may continue to purchase shares in the open market, an acquisition is unlikely to be effected in this manner. Rather, the acquirer is more likely at some point to make a tender offer (an offer made directly to the shareholders to buy shares at a premium above the current market price). The tender offer may specify that the acquirer will purchase all shares that are tendered – that is, turned in to the acquirer. Alternatively, the offer may state that the acquirer will purchase all shares up to, say, 50 per cent of the number of shares outstanding. If more shares are tendered, pro-rating will occur. For example, if, in the extreme case, all of the shares are tendered, each shareholder will be allowed to sell one share for every two shares tendered. The acquirer may also say that it will accept the tendered shares only if a minimum number of shares have been tendered.

National regulators normally require that tender offers be held open for a minimum period. This delay gives the target time to respond. For example, the target may want to notify its shareholders not to tender their shares. It may release statements to the press criticizing the offer. The target may also encourage other firms to enter the bidding process.

At some point the tender offer ends, at which time the acquirer finds out how many shares have been tendered. The acquirer does not necessarily need 100 per cent of the shares to obtain control of the target. In some companies a holding of 20 per cent or so may be enough for control. In others the percentage needed for control is much higher. Control is a vague term, but you might think of it operationally as control over the board of directors. Shareholders Finanza aziendale

Defensive Tactics

801

___

___

elect members of the board, who, in turn, appoint managers. If the acquirer receives enoughequity to elect a majority of the board members, these members can appoint the managers whom the acquirer wants. And effective control can often be achieved with less than a majority. As long as some of the original board members vote with the acquirer, a few new board members can gain the acquirer a working majority.

Sometimes, once the acquirer gets working control, it proposes a merger to obtain the few remaining shares that it does not already own. The transaction is now friendly, because the board of directors will approve it. Mergers of this type are often called clean-up mergers.

A tender offer is not the only way to gain control of a hostile target. Alternatively, the acquirer may continue to buy more shares in the open market until control is achieved. This strategy, often called a street sweep, is infrequently used, perhaps because of the difficulty of buying enough shares to obtain control. Also, as mentioned, tender offers often allow the acquirer to return the tendered shares if fewer shares than the desired number are tendered. By contrast, shares purchased in the open market cannot be returned.

Another means to obtain control is a proxy fight – a procedure involving corporate voting. Elections for seats on the board of directors are generally held at the annual shareholders’ meeting, perhaps four to five months after the end of the firm’s fiscal year. After purchasing shares in the target company, the acquirer nominates a slate of candidates to run against the current directors. The acquirer generally hires a proxy solicitor, who contacts shareholders prior to the shareholders’ meeting, making a pitch for the insurgent slate. Should the acquirer’s candidates win a majority of seats on the board, the acquirer will control the firm. And as with tender offers, effective control can often be achieved with less than a majority. The acquirer may just want to change a few specific policies of the firm, such as the firm’s capital budgeting programme or its diversification plan. Or it may simply want to replace manage-ment. If some of the original board members are sympathetic to the acquirer’s plans, a few new board members can give the acquirer a working majority.

Whereas mergers end up with the acquirer owning all of the target’s equity, the victor in a proxy fight does not gain additional shares. The reward to the proxy victor is simply share price appreciation if the victor’s policies prove effective. In fact, just the threat of a proxy fight may raise share prices, because management may improve operations to head off the fight.

29.9 Defensive Tactics

Target firm managers frequently resist takeover attempts. Actions to defeat a takeover may benefit the target shareholders if the bidding firm raises its offer price or another firm makes a bid. Alternatively, resistance may simply reflect self-interest at the shareholders’ expense. That is, the target managers might fight a takeover to preserve their jobs. Sometimes manage-ment resists while simultaneously improving corporate policies. Shareholders can benefit in this case, even if the takeover fails.

In this section we describe various ways in which target managers resist takeovers. A company is said to be ‘in play’ if one or more suitors are currently interested in acquiring it. It is useful to separate defensive tactics before a company is in play from tactics after the company is in play.

Deterring Takeovers before Being in Play

Corporate Charters The corporate charter refers to the articles of incorporation and corporate by-laws governing a firm. Among other provisions, the charter establishes conditions allowing a takeover. Firms frequently amend charters to make acquisitions more difficult. As examples, consider the following two amendments:

Classified or staggered board

1 : In an unclassified board of directors, shareholders elect all of the directors each year. In a staggered board, only a fraction of the board is elected each year, with terms running for multiple years. For example, one-third of the board might stand for election each year, with terms running for three years. Staggered boards increase the time an acquirer needs to obtain a majority of seats on the board. In the previous example, the acquirer can gain control of only one-third of the seats in the first year after acquisition. Another year must pass before the acquirer is able to control two-thirds of the Finanza aziendale

___

seats. Therefore the acquirer may not be able to change management as quickly as it would like. However, some argue that staggered boards are not necessarily effective, because the old directors often choose to vote with the acquirer.

Supermajority provisions

2 : Corporate charters determine the percentage of voting shares needed to approve important transactions such as mergers. A supermajority provision in the charter means that this percentage is above 50 per cent. Two-thirds majorities are common, though the number can be much higher. A supermajority provision clearly increases the difficulty of acquisition in the face of hostile management. Many charters with supermajority provisions have what is known as a board out clause as well. Here supermajority does not apply if the board of directors approves the merger. This clause makes sure that the provision hinders only hostile takeovers.

Golden Parachutes This colourful term refers to generous severance packages provided to management in the event of a takeover. The argument is that golden parachutes will deter takeovers by raising the cost of acquisition. However, some authorities point out that the deterrence effect is likely to be unimportant, because a severance package, even a generous one, is probably a small part of the cost of acquiring a firm. In addition, some argue that golden parachutes actually increase the probability of a takeover. The reasoning here is that management has a natural tendency to resist any takeover because of the possibility of job loss. A large severance package softens the blow of takeover, reducing management’s inclination to resist.

Golden parachutes are very controversial in economic downturns, as there is nothing the media likes more than to splash an incredibly generous severance package all over the front pages when the company is in financial distress. This has been the case in recent years, when many outgoing executives bowed to public pressure and rescinded their golden parachutes. A good example concerns the chief executives of the Royal Bank of Scotland and HBOS, the big British banks that succumbed to the credit crisis in 2009. Fred Goodwin (RBS) and Andy Hornby (HBOS) gave up their golden parachutes of £1.2 million and £1 million respectively when they left their banks, after intense political and public criticism.

Poison Pills The poison pill is a sophisticated defensive tactic that is common in the US but illegal in Europe. In the event of a hostile bid, a poison pill allows the target firm to issue new shares at a deep discount to every shareholder except the bidder.

Perhaps the example of PeopleSoft (PS) will illustrate the general idea. At one point in 2005 PS’s poison pill provision stated that once a bidder acquired 20 per cent or more of PeopleSoft’s shares, all shareholders except the acquirer could buy new shares from the corporation at half price. At the time PS had about 400 million shares outstanding. Should some bidder acquire 20 per cent of the company (80 million shares), every shareholder except the bidder would be able to buy 16 new shares for every one previously held. If all shareholders exercised this option, PeopleSoft would have to issue 5.12 billion (= 0.8 × 400 million × 16) new shares, bringing its total to 5.52 billion. The share price would drop, because the company would be selling shares at half price. The bidder’s percentage of the firm would drop from 20 per cent to 1.45 per cent (= 80 million/5.52 billion). Dilution of this magnitude causes some critics to argue that poison pills are insurmountable.

Since poison pills are illegal in many countries, this has led to greater frequency of hostile take-overs, especially by hedge funds looking to take over a company quickly and sell it on at a profit. Outlawing poison pills has also led to some criticism, because acquiring firms can quickly take control of a target firm before other, possibly better, bids are being prepared by other firms.

Deterring a Takeover after the Company Is in Play

Greenmail and Standstill Agreements Managers may arrange a targeted repurchase to forestall a takeover attempt. In a targeted repurchase a firm buys back its own equity from a potential bidder, usually at a substantial premium, with the proviso that the seller promises not to acquire the company for a specified period. Critics of such payments label them greenmail.

A standstill agreement occurs when the acquirer, for a fee, agrees to limit its holdings in the target. As part of the agreement the acquirer often promises to offer the target a right of first Finanza aziendale