Master Thesis

Moving from Conservatism to

Neutrality: Is this Reflected in

Accounting for R&D Expenditures?

The case of AkzoNobel and Royal DSM

Student name: N.S. de Koning Student number: 5755018

Date of submission: 24th of June, 2013 Version being submitted: First

Word count: 18,422

Qualification: MSc Accountancy & Control Specialization: Accountancy

Name of the institution: Amsterdam Business School

Faculty of Economics and Business, University of Amsterdam Name of UvA supervisor: Prof dr. D.M. Swagerman

Name of Second UvA reader: dr. ir. S.P. van Triest Name of Deloitte supervisor: J.S. Visch MSc RA

2

Abstract

Both the IASB as well as the FASB state that conservatism should no longer be part of the conceptual framework for financial reporting. The fundamental argument they provide for this change is that conservatism is believed to be inconsistent with the qualitative characteristic of neutrality. This move from conservatism to neutrality has led accounting standard setters to make changes to the current accounting standards to make them less conservative. One of the standards that have been revised is RJ210 (Dutch GAAP). This standard deals with the recognition of research and development (R&D) expenditures. Prior to the amendment of RJ210 in 2001 the standard prescribed to expense the R&D costs completely (in the income statement). The revised RJ210 standard states that the research expense component has to be expensed completely, while the development expenses must be capitalized when certain criteria have been met. According to IAS 38 (IFRS), which was established already in 1978, development cost must also be capitalized when certain criteria have been met. Conservatism refers to companies tending to disclose bad news (losses) earlier than good news (profits). Completely expensing R&D costs is a form of bad news, since the reported net income will be lower compared to a situation where some of these costs may be capitalized and expensed in later years instead. When this brake of expensing development costs is removed to let managers capitalize development costs and in this way show the investors what they are doing, one would expect that management will engage in more R&D, expense less and reflect more development costs in the balance sheet. This removal of the brake will be explored by examining two Dutch, R&D intensive chemical companies. This way, the impact of the revised standards concerning R&D expenditure is investigated. Has the revised IAS 38 standard and RJ210 led to increased neutrality in financial reporting?

Keywords

3

Preface

This report is my master thesis for the completion of my Master program Accountancy & Control at the University of Amsterdam. Moreover, it is also a completion of my internship at the Consumer Business, Core Audit department of Deloitte. I really appreciate the help I have received from many people while writing this thesis.

I would first like to thank my supervisor from the University of Amsterdam, Prof dr. D.M. Swagerman. He gave me much guidance in how to structure the thesis. Moreover, brainstorming about the subject was very helpful to me.

I would like to extend my gratitude to J.S. Visch MSc RA, my supervisor at Deloitte, Senior Manager at the Consumer Business, Core Audit department. He was very helpful in getting me into contact with some experts from the field.

Last but not least, I would like to thank the experts from the field, who I have interviewed. The interviewees were Karim Safar and Ivar Smits from AkzoNobel; Peter Sampers and Jan van den Bossche from Royal DSM, as well as an expert of one of the big four accounting firms, who wished to remain anonymous. I am very grateful for the time and effort of all the mentioned people. The open interviews provided me with a good understanding of the issues regarding R&D accounting, which has been applied throughout this thesis.

This thesis provides new insights in the accountancy science, especially regarding R&D accounting and the possible contribution of the standards regarding R&D accounting towards neutral accounting.

4

Table of Contents

1. Introduction……… 6

2. Background and State of the Art of the Literature………....….... 10

2.1. Trade-off between Relevance and Reliability………10

2.2. Conservatism……….….... 11

2.3. Explanations of Conservatism………... 13

2.3.1. Contracting Explanation……… 13

2.3.2. Income Tax Explanation……… 13

2.3.3. Litigation Explanation………... 13

2.3.4. Accounting Regulation Explanation…….………. 14

2.3.5. Non-conservatism Explanations……… 14

2.4. Criticism of Conservatism………. 14

2.5. Move to Neutrality………. 15

2.6. Criticism of Neutrality………...………… 15

2.7. IAS 38 Intangible Assets: R&D………...……. 16

2.8.Dutch GAAP: RJ210………..…… 17

2.9. Other Amendments Made to Move to Neutrality..…………18

2.10. Managerial Problem of locating R&D costs……… 19

3. Research Question……….… 22 4. Research Methodology……….……… 23 5. Context Analysis……… 28 5.1.AkzoNobel ……….… 28 5.2. Royal DSM……… 29 6.Content Analysis……… 30 6.1. AkzoNobel ……… 30

6.2. AkzoNobel and the R&D Accounting Standards……….… 39

6.3. Royal DSM……… 41

6.4. Royal DSM and the R&D Accounting Standards……….… 47

7. Comparison AkzoNobel and Royal DSM………. 51

8. Investors and R&D……… 54

9. Conclusion………..………... 56

9.1. Concluding Remarks………... 57

9.2. Limitations and Future Research………..… 59

9.3. Final Conclusion……… 59

Literature References……… 61

5

List of Tables and Illustrations

Figure 1 Book values of a fixed asset under conservative accounting……… 12

Figure 2 Reported net income under conservative accounting……….. 12

Figure 3 Research Model: Step 2 ………..……….. 22

Figure 4 Research Model: Step 3……… 23

Figure 5 Research Methodology Model………. 24

Figure 6 Research Methodology Model: Context Analysis……… 28

Figure 7 Research Methodology Model: Content Analysis……… 30

Figure 8 R&D Accounting Treatment AkzoNobel collected from DataStream…………. 32

Figure 9 R&D Accounting Treatment AkzoNobel hand collected from the annual financial statements……….……….…….. 32

Figure 10 Relationship R&D Expenses and Capitalized Development Costs AkzoNobel (DataStream)………..….. 33

Figure 11 Relationship R&D Expenses and Capitalized Development Costs AkzoNobel (Hand collected) ………..… 33

Figure 12 Extract from the Financial Economic Manual (FEM) of AkzoNobel ……….. 36

Figure 13 KPIs related to R&D of AkzoNobel: R&D Major Projects as % of R&D expenses ……….………….. 40

Figure 14 R&D Accounting Treatment Royal DSM collected by DataStream …….…… 42

Figure 15 R&D Accounting Treatment Royal DSM hand collected………... 42

Figure 16 R&D Expenses and Capitalized Development Costs Royal DSM (DataStream) ………. 43

Figure 17 PMP Process at Royal DSM ………. 45

Figure 18 KPI related to R&D of Royal DSM: Innovation Sales ……….… 49

Figure 19 KPI related to R&D of Royal DSM: Total R&D Expenditure as % of Net Sales ……… 49

Figure 20 Move from Tangible Assets to Intangible Assets……… 50

Figure 21 Comparison Capitalized Development Costs (in millions of Euros)………..… 53

Figure 22 EBITDA minus capitalized development cost on sales (Barco) ……… 55

Figure 23 Research Methodology Model: Results ………. 57

6

1.

Introduction

Despite criticism, conservatism in accounting has survived for many centuries (Watts, 2003, p.1.). Accountants traditionally express conservatism by the adage: “anticipate no profit, but anticipate alllosses (Bliss, 1924)”. Basu (1997, p.7) explains this adage by the tendency of accountants to require a higher degree of verification to recognize good news, such as gains, than the degree of verification required to recognize bad news, such as losses.

Recently the International Accounting Standards Board (IASB) as well as the

Financial Accounting Standards Board (FASB) argue that conservatism should no longer be part of the conceptual framework for financial reporting. The fundamental argument they provide for this is that conservatism is incongruent with the qualitative characteristic of neutrality, which encompasses freedom of bias (Conceptual Framework, 2008, pp.48-49). The IASB states that:

“Conservatism in financial reporting should no longer connote deliberate, consistent

understatement of net assets and profits. The Board emphasizes that point because

conservatism has long been identified with the idea that deliberate understatement is a virtue

(Conceptual Framework, 2008, p.49)”.

Some familiar terms like substance over form, reliability and prudence are therefore no longer mentioned in the framework. The move from conservatism to neutrality has led accounting standard setters to make changes to the current accounting standards to make them less conservative. This in turn would lead to a positive effect on value, which is relevant to the financial statement users.

One of the standards that has been changed relates to the recognition and accounting for research and development (R&D) expenditures. In the Netherlands, the standard related to R&D is RJ210: Immateriële Vaste Activa (Intangible Assets) and the international standard related to R&D is IAS38: Intangible Assets. We will take a closer look at both standards since the sample, as explained later, consists of Dutch companies that complied with the Dutch GAAP till 2005, and have switched to applying International Financial Reporting Standards (IFRS) from that year on. However, from 2005 till 2012 they both applied Dutch GAAP as well, as far as applicable. RJ210 was amended in 1999, with effective date first of January 2001. According to this new accounting standard development costs are to be capitalized when certain criteria are met. Prior to this change, development costs were

7 expensed when incurred (RJ210, 1999, p.25-26).

When considering a more global scope, for instance, take a look at IAS 9: Research and Development Costs which was established on the first of July 1978. IAS 38 superseded IAS 9 on the first of July, 1998. Under the now-superseded IAS 9, the research costs had to be expensed and the development costs had to be capitalized and expensed over the periods of expected benefit. IAS 38 regarding to R&D is similar to IAS 9; the research cost component should be expensed completely according to IAS 38 paragraph 54; and according to

paragraph 57, the development expenses must be capitalized as an intangible asset when certain criteria have been met (IAS 38, 2012; History of IAS 38, 2013). As we can see, under IFRS capitalization of development costs was allowed many years before it was allowed in the Netherlands.

The question that arises is whether this change in standards has indeed reduced conservatism and thereby increased neutrality in accounting. As such, the research question of this thesis is: Is the IFRS’s move from conservatism to neutrality reflected in actual reporting of R&D?

By examining two Dutch, R&D intensive chemical companies, the impact of the revised standard concerning R&D expenditure is investigated.By conducting case studies of the two sample firms, one can determine whether these two firms treat the IAS 38 and RJ210 standards concerning R&D in a similar way. It will become clear whether these companies indeed started to capitalize their R&D after the first of April 2001, which is the effective date of the amended RJ210 standard and whether they complied with IAS38 when they started to apply the IFRS standards back in 2005 (History of IAS 38, 2013; RJ210, 1999, p.25-26). In Chapter 4 Research Methodology, the choice for AkzoNobel and Royal DSM will be further explained.

Since accounting exists, conservatism, also known as prudence, has been one of the most fundamental accounting principles. Therefore, the IASB and FASB’s move away from conservatism, which became more explicit with the introduction of IFRS in 2005 and the 2008 Exposure Draft release from the common Conceptual Framework of the IASB/FASB, is of great interest. To my knowledge there is no prior research about whether the standards that the IASB has changed, aimed at decreasing conservatism, has indeed led to less

conservatism. The motivation for this study is consequently derived from the literature gap of the effects of the change of the IAS 38 and RJ210 standards on financial reporting.

Conservatism actually means that bad news (losses) will be disclosed earlier than good news (profits). Completely expensing R&D costs is a form of bad news, since the

8

reported net income will be lower than when some of these costs had been capitalized. When this brake of expensing development costs is removed, to let managers capitalize

development costs and in this way show the investors what they are doing, one would expect that management will engage in more R&D, expense less and reflect more development costs in the balance sheet. This removal of the brake will be analysed by looking at two R&D intensive companies.

The research result shows that both firms indeed started to capitalize development costs when it became allowed. AkzoNobel started capitalizing as early as 2001 and Royal DSM started capitalizing in 2009 due to applying the IFRS more strict than before and due to some difficulties they faced regarding the implementation of the new standard in their

accounting systems and processes. However, both firms still take a conservative approach towards the new standard, which hampers the move towards neutrality. The firms both recognize a different explanation for conservatism; AkzoNobel recognizes the income tax explanation for conservatism and Royal DSM recognizes the contracting explanation for conservatism. Moreover, they both believe that the amendment did not have any, positive nor negative, effect on them. Other stakeholders do not seem to benefit from the amendment either; therefore the IASB and the FASB might reconsider accounting standards regarding R&D, as well as the move to neutrality itself.

This thesis investigates the amended accounting standards concerning R&D expenditures since information related to the treatment of R&D expenditures is publicly available in the financial statements and therefore the information disclosure about R&D may have an effect on the decision-making process of investors. Investors are demanding market values to assist them in their decision making process. Financial reporting is trying to assist the investors; one of the objectives of financial reporting is to provide information that is

decision-useful for current and future investors as well as other stakeholders (IFRS Conceptual Framework 2011). As such, this research can potentially be of great social relevance and offer a valuable contribution to the existent literature. This research will contribute to the controversial discussion about the accounting of R&D expenditures. Accounting policy makers, managers, the tax authorities as well as other stakeholders, all have different views of how one should treat R&D expenditures, whether they should be capitalized or be expensed. The main scientific contribution of this research is that it will become clear whether the amended RJ210 and IAS 38 regarding R&D has the desired effect, this effect being that accounting for R&D expenses has indeed become less conservative, as was intended.

9

However, a limitation of this thesis might be the small sample size as it consists of only two companies. Nevertheless, it can be argued that this will not be a problem since they both are R&D intensive and IFRS applicants. Therefore it can be assumed that focusing on different companies that are specialized for example in High Tech R&D or Automotive R&D will not lead to different conclusions, since the definition of R&D remains the same and they are all subject to the same R&D standards.

Chapter 2 describes the background and the current state of the literature on this topic. The remainder of this paper is organized as follows: Chapter 3 contains the research question; Chapter 4 describes the research methodology chosen for this thesis; Chapter 5 contains the Context Analysis which provides a short introduction to AkzoNobel and Royal DSM; Chapter 6 consist of the Content Analysis, in this section the accounting treatment regarding R&D of the selected companies will be investigated and several interviews with employees with accounting and/or controlling expertise will provide insight in the problems related to R&D accounting; Chapter 7 contains the comparison of the results of the case studies; Chapter 8 describes to what extend investors are interested in capitalized development costs; and Chapter 9 provides the conclusion of the research.

10

2.

Background and the State of the Art of the Literature

2.1. Trade-off between Relevance and Reliability

Some accountants believe that historical cost accounting best predicts firm performance; others believe that current values will predict firm performance better. Historical cost will lead to more reliable financial statements and current values will lead to more relevant financial statements (Scott, 2012, pp.66-67). Two qualitative characteristics of financial accounting information are relevance and reliability. These qualitative characteristics are both critical for the quality of information, however an emphasis on one will hurt the other, and the other way around. When accounting information is provided in time it is relevant,

however at early stages the information is uncertain and therefore not reliable. When we wait till the information gains reliability, the relevance is lost. Consequently, we have to make a trade-off between relevance and reliability (Accounting Explained, 2012).

Whatever view taken, all accountants feel that financial statements should be useful (Scott, 2012, pp.66-67). According to the IFRS Conceptual Framework of 2011, as issued on January 2012 the general purpose of financial accounting is to provide

“ financial information about the reporting entity that is useful to existing and potential investors, lenders and other creditors in making decisions about providing resources to the entity. Those decisions involve buying, selling or holding equity and debt instruments, and providing or settling loans and other forms of credit. Many existing and potential investors, lenders and other creditors cannot require reporting entities to provide information directly to them and must rely on general purpose financial reports for much of the financial

information they need. Consequently, they are the primary users to whom general purpose financial reports are directed (IFRS Conceptual Framework 2011, emphasis added)”.

Concisely, the aim of financial accounting is to provide financial information that is decision useful for existing and potential stakeholders.

There are two perspectives of decision usefulness; the information perspective and the measurement perspective. The information perspective states that information is useful if it leads investors to change their beliefs and actions. The degree of usefulness can be measured by the extent of volume or price change following the release of the information. It also acknowledges that investors are individually responsible for predicting future firm performance, instead of having accountants do it for them (Scott, 2012, Chapter 5). The

11

measurement perspective, on the other hand, states that accountants undertake a

responsibility to incorporate fair values in financial statements to assist investors to predict fundamental firm value. The measurement approach to decision usefulness suggests a greater usage of current value in the financial statements to assist investors. This approach likewise acknowledges that investors are individually responsible for predicting future firm

performance. However, this approach wants to enable better predictions by providing more useful information (Scott, 2012, Chapter 6). This last approach is fundamental in the discussion about the IASB’s move away from conservatism to neutrality.

2.2. Conservatism

As discussed in paragraph 2.1. the accounting standard setters have to choose between either making financial reporting more reliable or making financial reporting more relevant. It is not possible to make financial reporting both reliable and relevant. Only during the past decade the focus shifted to relevance as opposed to reliability which was previously prevalent in contemporary accounting practice. Reliability is mostly reflected by historical cost accounting. Conservatism comes into play when considering reliability.

The concept conservatism is clearly depicted by the following quote:

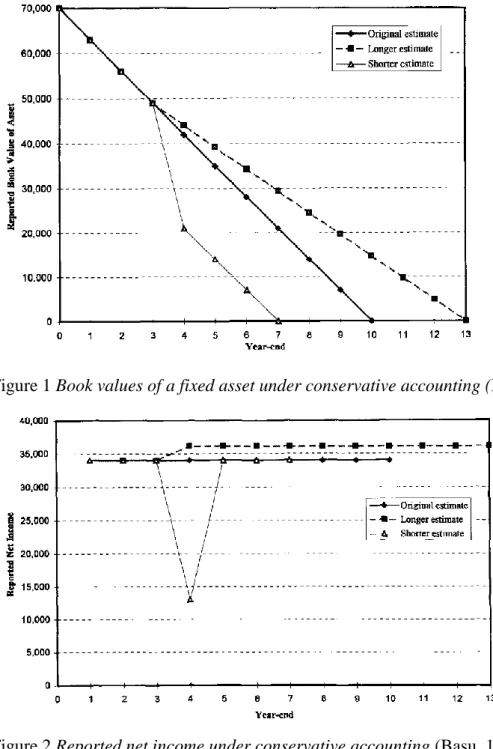

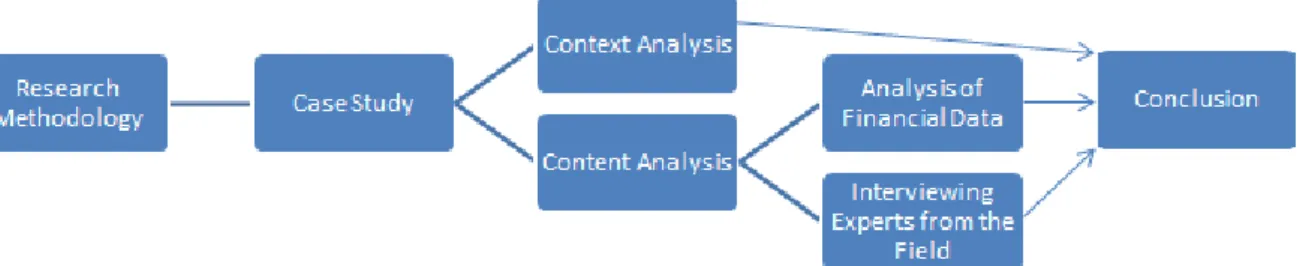

“Assets are often, by reason of prudence, estimated and stated to be estimated, at less than their probable real value. The purpose of the balance sheet is primarily to show that the financial position of the company is at least as good as there stated, not to show that it is not or may not be better (Basu, 2009, p. 3)”.

Basu (1997, p. 4) explains that conservatism is the concept that earnings are reflecting bad news more timely than good news, and therefore accounting information is biased towards negative events. Basu (1997, p.4-6) also states that bad news earnings is not only more timely but less persistent as well. This is known as conservatism bias, which is clearly depicted by Figure 1 and 2 below. Consider a company that receives news which forces the company to reconsider the remaining useful life of an asset. When the new estimate is longer, the

depreciation charges that would have been taken in the current and future years are smoothed out over the new remaining useful life, which result in lower depreciation charges (Figure 1) and subsequently an increase in the reported net income (Figure 2). However, when the expected new remaining useful life is shorter, the company will have to impair the asset. Consequently there will be an increase in depreciation charges as the total depreciation will

12

have to be divided over a smaller number of years compared to before the change (Figure 1) and leads to a sharp reduction in the reported net income in the year of the impairment but will have no effect on future reported net income (Figure 2). The latter finding is clear evidence that the reporting of bad news is less persistent compared to the reporting of good news.

Figure 1 Book values of a fixed asset under conservative accounting (Basu, 1997, p.5)

Figure 2 Reported net income under conservative accounting (Basu, 1997, p.5)

13 2.3. Explanations of Conservatism

There are several explanations for conservatism. Watts (2003) claims that there are four conservative explanations, namely Contracting, Taxation, Litigation and Accounting Regulation, and two non-conservative explanations, namely Earnings Management and the Abandonment Option Effect, which will be described in the next paragraphs.

2.3.1. Contracting Explanation

One explanation of conservatism is the contracting explanation. Due to moral hazard that arises because parties of the firm have asymmetric information, asymmetric payoffs, limited liability and limited horizons, various parties of the firm draft contracts to constrain managers to engage in activities that will harm the parties related to the firm. For example, a bank can draft a debt covenant contract before lending an amount of money to the company. When the company is in breach of a debt covenant, the bank has the legal right to withdraw the loan. As a result, the company should behave more conservative in order to retain the loan. In other words, conservatism mitigates the opportunistic behaviour exhibited by management. Another contract one can think of that leads to conservatism is the compensation contract. Due to the fact that the manager often has more information than other parties within the firm, a compensation contract can refrain the manager from exhibiting opportunistic behaviour. Moreover, the limited tenure and limited liability of the manager increases the need for contracting, to make sure the manager acts in the best interest of the shareholders. Phrased differently, contracting is simply another way of directing the manager’s actions (Watts, 2003, p. 1-15).

2.3.2. Income Tax Explanation

Another explanation for conservatism is that of the income tax. The amount of tax that has to be paid by the company depends on its reported earnings. The higher the reported earnings, the higher the taxable income and consequently, the higher the tax to be paid. The link between reported earnings and taxable income creates an incentive for managers to defer or understate their income to reduce the amount of tax payable. Just like the contracting explanation, this incentive leads to the understatement of net assets and hence can be considered a form of conservatism (Watts, 2003, p. 20).

2.3.3. Litigation Explanation

Prior research finds that litigation risk under the Securities Act is more likely to materialise when a firm is overstating its assets than when a firm is understating its assets. Therefore

14

litigation risk is another explanation for a firm to engage in conservatism. Managers and auditors will be encouraged to understate assets in order to reduce the risk of litigation (Watts, 2003, p. 19-20).

2.3.4. Accounting Regulation Explanation

If firms overstate their assets, accounting standard setters and regulators are more likely to get negative criticism compared to when firms understate their assets. Therefore, accounting standard setters and regulators favour conservatism because this will lead to a reduction of the political costs that they will face in case of the discovery of an overstatement of assets (Watts, 2003, pp. 5, 21-22). An event that clearly depicts the extent to which the accounting regulators and standard-setters favour conservatism is shown by the fact that the Securities and Exchange Commission (SEC) during its first 30 years prohibited upward valuations of assets (Zeff, 1972, pp. 156-160). Another example of how conservatism is compelled is the enforced GAAP rules concerning revenue recognition. The revenue recognition rules require that there is a greater degree of verification needed to recognize revenues than for losses, which again is congruent with the core principle of conservatism (Watts, 2003, p. 22).

2.3.5. Non-Conservatism Explanations

Earnings management and the abandonment options are also explanations for conservatism; however they cannot be the fundamental explanation. Earnings management can be used by managers in a good way, to signal important information; however managers can also manage earnings in a bad way, to obtain personal gains. An example of bad earnings management is big bath accounting, which is when a manager understates earnings in one year in order to overstate earnings in future years. The understatement of earnings, as well as assets, is part of conservatism. However, the manager’s intention is not based on prudence; the manager only understates earnings in an earlier year in order to overstate earnings in later years. The abandonment options is another conservatism explanation. Managers can abandon operations that are not profitable and this will lead to an understatement of assets. Again, the understatement of assets is part of conservatism. However, the manager’s intention is not based on prudence (Watts, 2003, p. 6).

2.4. Criticism of Conservatism

There is a lot of criticism on conservatism in accounting. The main criticism is that

conservatism is not very helpful for investors in their investment decision making since the conservatism depicts a lower firm value than the actual firm value. Conservatism therefore

15

leads to a gap between the firm value and the market value. By for example using historical cost accounting and by strict revenue recognition criteria, the firm’s financial statements may cause the firm to be undervalued by investors.

2.5. Move to Neutrality

Since accounting exists, conservatism, also known as prudence, has been one of the most fundamental accounting principles. Nowadays, the IASB as well as the FASB claim that conservatism should no longer be part of the conceptual framework for financial reporting. The fundamental argument they provide for this is that conservatism is inconsistent with the qualitative characteristic of neutrality. In their view more neutral accounting, hence moving to mark-to-market accounting, will lead to more useful information to investors. Fair value leads to an increase in relevance and a decrease in reliability. Relevance and reliability need to be treaded off. Nowadays, the accounting policy setters clearly try to move to more relevant financial information.

Next to the views of opponents for moving away from conservatism described above, there are proponents as well. Some views of proponents are provided in the next paragraph.

2.6. Criticism of Neutrality

Proponents for moving away from conservatism believe that moving to fair value accounting is risky because this form of accounting lacks verifiability. Moreover, it is argued that more neutral accounting will increase the opportunity for earnings management, since a lower degree of verification is asked for in contrast to historical cost accounting. Moving to neutral accounting may do more harm than good. For instance, Watts states that:

“successful elimination of conservatism will change managerial behaviour and impose significant costs on investors and the economy in general (2003, Synopsis)”.

He argues that the FASB cannot afford more Enron scandals; the accounting standards setters should reconsider their move towards accounting neutrality (Watts, 2002, p. 31). Likewise, Commissioner Barnier commented on the proposals by the European Commission to reform the audit sector that the financial crisis was a reminder of how much reliable information is needed (Barnier, 2011).

Conservatism has been an important principle in accounting for a long time. Therefore, one can question whether the move away from conservatism towards neutrality

16

will be an appropriate basis for the framework of financial reporting. For example, the only accepted change regarding derivatives is to decrease the book value. However, when moving to neutrality, are accounting standard setters going to allow companies to increase the book value of derivatives as well? This issue will be dealt with further on in this thesis.

Another criticism of neutrality might be that, since financial reporting will move towards relevance, this will reduce the reliability. Reliability is hampered due to the introduction of the extensive use of judgement and estimations.

The last criticism one might think of is that neutrality may release competitor sensitive information, e.g. proprietary information of a company. This might be the case when companies capitalize intangible assets at market value, the competitor can then observe the company’s view of what investments are profitable. This can lead to more entrants to the market (see Chapter 6.4.).

2.7. IAS 38 Intangible Assets: R&D

Since February 1977 accounting standards setters are establishing and constantly changing accounting standards concerning the treatment of intangible assets. The objective of the IAS 38 is to provide guidance for the accounting treatment for intangible assets that are not specifically discussed in other IFRS. When certain criteria are met, IAS 38 requires an entity to recognize an intangible asset. The two criteria which have to be met are the following:

“1) it is probable that the future economic benefits that are attributable to the asset will flow to the entity and 2) the cost of the asset can be measured reliably (History of IAS 38, 2013)”.

The requirement applies both to intangible assets obtained externally and to those generated internally. The IAS 38 prescribes additional recognition criteria for intangible assets that are

generated internally:

“1)The probability of future economic benefits must be based on reasonable and

supportable assumptions about conditions that will exist over the life of the asset and 2) The probability recognition criterion is always considered to be satisfied for intangible assets that are acquired separately or in a business combination (History of IAS 38, 2013)”.

17 (History of IAS 38, 2013).

In this thesis the focus will be on the standards concerning the accounting treatment of R&D costs. One should start to look at IAS 9: Research and Development Costs which was established on the first of July 1978. IAS 38 superseded IAS 9 on the first of July, 1998. Under the now-superseded IAS 9, the research costs had to be expensed and the development costs had to be capitalized and expensed over the periods of expected benefit. IAS 38

regarding R&D is similar to IAS 9; the research cost component should be expensed completely according to IAS 38 paragraph 54; and according to paragraph 57, the

development expenses must be capitalized as an intangible asset when certain criteria have been met (IAS 38, 2012; History of IAS 38, 2013). According to IAS 38 development costs

“are to be capitalized only after technical and commercial feasibility of the asset for sale or use have been established. This means that the entity must intent and be able to complete the intangible asset and either use it or sell it and be able to demonstrate how the asset will generate future economic benefits [IAS 38.57]. If an entity cannot distinguish the research phase of an initial project to create an intangible asset from the development phase, the entity treats the expenditure for that project as if it were incurred in the research phase only

(History of IAS 38, 2013).”

Initial recognition of an on-going R&D project acquired through a business combination is treated as follows:

“a research and development project acquired in a business combination is recognized as an asset at cost, even if a component is research. Subsequent expenditure on that project is accounted for as any other research and development cost [IAS 38.34] (History of IAS 38, 2013)”.

2.8. Dutch GAAP: RJ210

Following the appearance of IAS38 Intangible Assets, the existing RJ210 was thoroughly revised. The amendment closely relates to IAS38, only provisions that are inconsistent with Dutch law were not adopted. Some of these provisions, which are inconsistent with Dutch law, relate to the valuation of intangible assets at fair value and the amortization of all intangible assets based on the estimated economic life. According to the amendment of RJ210 in 2001; research costs may not be capitalized anymore but must be expensed when

18

incurred (RJ210, 1999, p. 25-26) However, development costs must be capitalized when all

the following criteria have been met:

“(a) the technical feasibility of completing the intangible asset so that it will be available for use or sale;

(b) its intention to complete the intangible asset and use or sell it; (c) its ability to use or sell the intangible asset;

(d) how the intangible asset will generate probable future economic benefits. Among other things, the enterprise should demonstrate the existence of a market for the output of the intangible asset or the intangible asset itself or, if it is to be used internally, the usefulness of the intangible asset;

(e) the availability of adequate technical, financial and other resources to complete the development and to use or sell the intangible asset; and

(f) its ability to measure the expenditure attributable to the intangible asset during its development reliably (IAS 38, 2003, p. 22)”

These criteria of RJ210 are exactly the same criteria according to IAS38 (IAS 38, 2003, p.22.; RJ210, 1999, pp. 270-271)(see Chapter 2.7.).

2.9. Other Amendments Made to Move to Neutrality

Some other accounting standards that have been amended in order to make financial reporting more neutral are IAS 38 relating to intangibles assets acquired from business combinations and useful life accounting; and IFRS 3, relating to business combinations (IAS 38, 2012). The most important change regarding IFRS 3, in accordance with IAS 38

Intangible Assets, is that intangible assets that are obtained from a business combination must be recorded separately from goodwill (IFRS 3, 2012; IAS 38, 2012). The amended standard states that in-process R&D that is acquired in a business combination is recognized as an asset at cost, even if a component of the project relates to research (History of IAS 38, 2013). This amendment makes accounting less conservative, since even research costs can be translated into assets, which IAS38 does not allow for internally generated intangible assets. Therefore a lower degree of verification is needed to record the assets, which makes

accounting less conservative. The other change of IAS 38 next to the changes in internally generated R&D and externally acquired R&D from a business combination is that intangible assets are allowed to have an indefinite life and therefore should not be amortized; they

19

should undergo a yearly impairment test. The useful life has moved from maximum 20 years to indefinite (IAS 38, 2012). Previously under the old standard, a company would have to amortize its assets while the useful life in reality might be longer than 20 years, this in turn would lead to an undervaluation of assets. This clearly indicates conservative accounting. When one would give the assets an infinite useful life, one has to periodically perform impairment testing, which leads to a book value on the balance sheet that better reflects the underlying value of the asset. These two standards are effective for Business Combinations since the first of April 2004.

2.10. Managerial problem of locating R&D costs

Dukes et al. (1980, p.3) state that there is a connection between decisions related to R&D and the reporting of the associated costs. When R&D must be expensed completely, reported net income will be lower. If spending on R&D will lower a company’s reported net income, managers may be inclined to reduce R&D expenditures. This reduction in reported net

income will have an effect on the market valuation as well as on the compensation and tenure of managers. The agency theory explains why changes in reported net income may affect the decisions taken by managers. For example, it seems as if the bond and debt covenants are part of the compensation, both are tied to reported net income, which emphasizes the importance of the reported net income for management. These two components may lead to earnings manipulation in order to obtain the adequate level of reported net income. To confirm Dukes’ (1980) assertions, Baber, et al (1991, p.818) find that if spending jeopardizes the ability of reporting a positive net income figure, R&D expenditure is significantly less.

When development costs, which meet the specific recognition criteria, can be

identified as an asset instead of an expense, the manager will be less inclined to spend less on R&D, since it does not affect the reported net income directly. Another advantage of

capitalizing development costs is that this will provide more inside information to

stakeholders, regarding the success that is expected of a development project to stakeholders. However, the problem which remains is that the capitalization of development costs provides a greater opportunity for earnings management (Healy, et al., 2002, p.678).

The financial crisis of 2008 has raised questions about the value of audits, the independence of auditors and the quality of audit work (Sika, 2009, p.2). The Autoriteit Financiële Markten (AFM), the supervisor of the Dutch financial markets regarding savings, insurance, loans and investments (AFM, 2013) , has increased pressure on the Big Four accounting firms to improve the quality of their work (Druk AFM, 2012).

20

To provide insight in how auditors deal with complex judgmental issues regarding R&D accounting by a client, an expert who is working for one of the big four accounting firms and deals with consultations of auditors every day, has been interviewed. He wished to remain anonymous and therefore his name, and the audit firm he is working for, will not be

mentioned throughout this thesis. The remainder of this chapter consists of the results of the interview. Audit quality is the ‘license to operate’ of each big four accounting firm. There is a tendency observable of auditors who are searching for assurance when it comes to complex accounting issues and to achieve this they can consult the Consultation Desk (this is a fictitious name, to ensure the anonymity of the big four office). The interviewee observes an increase in the number of consultations submitted by professionals in recent years. This has not yet been investigated; however it may have to do with the firms’ ambition to become ‘the standard of excellence’.

The Consultation Desk can be consulted by submitting an accounting position paper to the Consultation Portal of the Consultation Desk. The issue will be laid out by the auditor, and the view of the audit team as well as that of the client is described. Next, the Consultation Desk will give their advice, which is always signed off by two employees. Auditors can request guidance when they are dealing with complex, material auditing issues. One can think for example about the issue of determining at what specific moment it is allowed to start capitalizing development costs. Specific statistics were not available at the time of the interview, however in the last few years the Consultation Desk has not been consulted often when it comes to issues regarding capitalization of development costs. This may be due to the fact that this issue is possibly not considered as material to a company. Another reason might be that the financial reporting framework for this issue already exists for many years and therefore has become common practice which may reduce the need to consult the

Consultation Desk.

In the years 2001 to 2004 accounting for R&D was more a hot topic than it is today. As said before, it has become common practice. In the chemical and pharmaceutical industry R&D accounting is still of great interest. When pharmaceutical companies like Pfizer,

Johnson & Johnson and Roche develop an improved recipe for an existing medicine, there are often different project phases spread over several years. Only from the moment when a company receives Food and Drug Administration (FDA) approval, the product can be

brought on the market. However, since there often is a significant period of time between the start of the research phase and ultimate FDA approval, the question arises at what specific moment development costs meet the criteria to be capitalized. In this period of time a lot of

21

development will have been done, which will meet almost all of the criteria but may not be capitalized since it is not 100% clear whether the product will actually be sold or not. Due to this legislation, many development costs are assigned to the research component and

expensed through the profit and loss statement. The current accounting standards regarding the treatment of development expenses, RJ210 and IAS38, state that when a company meets the recognition criteria to capitalize, they shall capitalize the expenses and when they do not meet all the recognition criteria they shall not capitalize the costs and expense these to the profit and loss statement. It is not only important not to capitalize when recognition criteria has been met, it is also important to capitalize development costs when a company does meet all of the recognition criteria. However, a cautious auditor might focus more on whether or not the account development costs may be on the balance sheet. The auditor should also consider the research costs in the profit and loss statement and determine if these costs meet the recognition criteria and whether these expenses should be recognized as development costs on the balance sheet instead. If an audit team detects a misstatement in the draft of the financial statements of a company, for example when development costs are capitalized when the costs do not meet all the recognition criteria, a qualitative and quantitative evaluation of the error will provide insight into the impact of the error on the balance sheet. When the misstatement is material, e.g. when it can influence the decision-making process of financial statement users, the misstatement must be corrected. If the misstatement occurred in prior year(s), it must be corrected retrospectively in equity when the misstatement is fundamental, i.e. when the misstatement substantially affects the decision-making process of financial statement users. However when the misstatement is material (but not fundamental) the error will be corrected prospectively in the profit and loss statement (RJ210, 1999).

22

3

. Research Question

The theory regarding R&D provided in the prior chapter reveals that it is not certain that the current accounting standards related to R&D will contribute to the move towards neutrality. It seems that from the current accounting standards diversified incentives might emerge, which places an increase in decision-usefulness to financial statement users on an unstable ground. Therefore, these incentives might hamper the move towards neutrality. This has been the trigger to investigate in practice how and why the accounting standards related to R&D are used; and finally conclude whether the move to neutrality is reflected in actual reporting of R&D. Figure 3 consists of the Research Model which will guide us through the different research steps taken throughout this thesis. In the prior chapter the theory was described via desk research, which represents the first step of the research model. In this chapter the second step will be discussed. The second step consists of formulating a research question. The research question is formulated as follows:

Is the IFRS’s move from conservatism to neutrality reflected in actual reporting of R&D?

The research question will be answered by first obtaining an understanding of how and why firms report their R&D expenditures in a certain way.

There are two research approaches possible; the deductive approach and the inductive approach. The deductive approach reasons from general to more specific. It is also called the top-down approach since it starts off with a theory and moves its way down to the

confirmation. The inductive approach however, works the other way around. It is also called the bottom-up approach since it starts with an observation and works its way up to form a theory (Trochim, 2006). Clearly, the deductive approach is appropriate for this research since it starts off with a theory.

Figure 3 Research Model: Step 2

In the next chapter, the research methodology will be described more thoroughly. Theory Research Question Methodology Research Results

23

4.

Research Methodology

In the prior chapter’s the first and second step of the Research Model has been described. We now arrive at the third step which consists of the research methodology, see Figure 4 below.

Figure 4 Research Model: Step 3

The question that arises is what method to choose for the analysis in practice. Case study research has been chosen as method over other methods, since the case study method is preferred when

“(a) ‘how’ or ‘why’ questions are being imposed, (b) the investigators has little control

over events, and (c) the focus is on a contemporary phenomenon within a real-life context

(Yin, 2009, p.2)”

Accordingly, the research does meet all the criteria for case study research. The research question will be answered by first finding out “how” and “why” managers report their R&D expenditures in a certain way. Next, the investigator has no control over the event of the reporting of the R&D numbers and lastly, it focuses on a contemporary phenomenon within a real-life context. The use of case studies helps to understand real-life events like small group behaviour and managerial processes (Yin, 2009, p.4).

Figure 5 illustrates the details of the research methodology, which is the third step of Figure 4.The research methodology will consist of two case studies; AkzoNobel and Royal DSM. Case studies will be helpful in understanding a particular issue or situation in great detail and depth (Patton, 1987, p.19). Since this area has not been investigated before, case studies, e.g. qualitative research methods, will help in obtaining a deeper and more detailed understanding of the issues than only consulting qualitative research methods. The case study consists of two parts; a context analysis as well as a content analysis. The context analysis which is provided in the next chapter is in fact an introduction to the sample firms. The content analysis however, consists of two parts. First, financial statement data regarding R&D of the

24

sample firms will be analysed. Second, some experts from the field were interviewed to obtain a deeper understanding of the results of the financial data analysis.

Figure 5 Research Methodology Model

As mentioned before, to investigate the treatment of the Dutch and International standards regarding R&D two cases have been chosen. When deciding on what sample to take in order to analyze the hypotheses, it is useful to consider looking at two quite similar companies, within the same R&D intensive industry. This is because in this way almost all of the irregularities between the two companies should be filtered out; hence any differences in the treatment of IAS 38 and RJ210 should become clear. When searching for two quite similar companies that both are R&D intensive, listed and are both subject to reporting under IFRS on a mandatory basis, it seemed like a logical step to consider European companies, due to the fact that since 2005 all European listed companies must apply the IAS/IFRS standards (European Union, 2013).

Consequently, the two Dutch companies Royal DSM and AkzoNobel were the first two companies that were found who met the selection criteria, and for this reason these two were chosen to be used as the sample. The sample of this research therefore consists of these two Dutch chemical companies. Since January 2005, all European listed companies must apply the IAS/IFRS standards (European Union, 2013), therefore the Netherlands is an appropriate country for investigating the effects of the amended standards of IAS 38. The selection process of the sample will be described next.

A list of the top 30 R&D intensive companies of 2012 in the Netherlands, which consists of some worldwide known companies such as Phillips and Unilever and some companies which are less known such as RijkZwaan and Vanderlande Industries, was

consulted in order to identify two quite similar companies (Top 30, 2012). The list consists of companies from a wide range of differing industries; from a tire manufacturer to a blood bank organization. The type of industry in which the companies operated did not play a role in determining what companies to include in the sample, as long as they operated in the same

25

industry. The main consideration was the extent to which they were alike as well as being globally well-known companies. The chemical companies disclosed in the top 30 R&D intensive Dutch companies are Shell (number two), Royal DSM (number four) and

AkzoNobel (number eleven). Of these three companies Royal DSM and AkzoNobel are most alike since they are most similar in size; the total assets of these companies in the year 2011 are 11,157 million Euros and 19,869 million Euros respectively (Annual Report AkzoNobel, 2011; Annual Report Royal DSM, 2011, p.3). In contrast, Shell had total assets in 2012 of 345,257 million dollars, which was about 264,666 million Euros at 31st of December 2011 (Annual Report Shell, 2011; Wisselkoersen, 2013), which places Shell on a total different level. By comparing two quite similar R&D intensive companies, one could find out whether these two companies treat the amended RJ210 and IAS 38 standards concerning R&D in a similar way.

The consulted sources are as follows. The context analysis is done by consulting the website homepage of each firm, which is in fact desk research. The content analysis however, does not consist of only one consulted source. The first step of the content analysis consists of desk research as well; analysing financial data of the sample firms. The consulted sources for doing this are the database DataStream. DataStream has been chosen to collect the data from since this database has extensive financial information about European companies and the financial statements of AkzoNobel and Royal DSM for the years 2000 till 2012. RJ210 amended in 2001 and therefore, by looking at the years 2000 till 2012, one can see what the change has been since then till present time. The data has been hand collected via the websites of AkzoNobel and Royal DSM. Eventually, it should become clear whether these companies indeed started to capitalize development costs (more) after the first of July 2001, which is the effective date of the amended RJ210 standard (RJ210, 1999, p.25-26), and whether they, next to the RJ210 standard, applied the IAS 38 standard correct from the moment they started applying IFRS. The second step of the content analysis consists of interviewing experts from the field. Therefore, the last methodological approach of this thesis is the data collection from in- depth, open-ended interviews. There are three approaches of in-depth, open-ended interviews; “(1) the informal conversational interview; (2) the general interview guide, and (3) the standardized open-interview (Patton, 1987, p.109)”. The second

approach has been chosen for this research. An interview guide consists of a list of questions that are to be investigated in the interview, and it will help to make sure the same topics are covered in all the interviews. This approach has been chosen since the same topics are covered and at the same time, permits individual perspectives and experiences to evolve

26

(Patton, 1987, p.111). This seems appropriate because the topic has not been investigated before and therefore a thorough and detailed understanding is desired. After providing initial contact via email or phone with the managers and controllers and explaining them the aim of the interviews, the actual open interviews were conducted. All interviews lasted for

approximately one hour and minutes were handwritten. The interviews were then written down and sent back to the interviewees for their comments and suggestions, in order to confirm the interpretation and content of the interviews. After receiving feedback from the interviewees, any required changes were made and sent back for final approval of the interviewees.

An expert in the field on consultations of complex issues who is working for one of the big four accounting firms and deals with consultations of auditors every day, has been interviewed at the 26th of April, 2013. He wished to remain anonymous and therefore his name, and the audit firm he is working for, will not be mentioned throughout this thesis. The issues discussed were the policy of consultation, issues consulted most, judgment issues concerning R&D accounting and the rules regarding R&D itself. The knowledge gained by this interview has been implemented in Chapter 2.8. Moreover, two accounting and/or controlling experts of the two sample firms have been interviewed; Karim Safar, controller Research Development and Innovation (RD&I) Projects of AkzoNobel has been interviewed on the 13th of May, 2013; and Peter Sampers, Senior Accounting Officer at Royal DSM has been interviewed on the 15th of May, 2013. Some issues discussed with Karim Safar and Peter Sampers were the rules applied regarding R&D, any experiences with difficulties regarding allocating costs to research and development and whether management consults with the controller before deciding to invest in R&D projects. The knowledge gained by the latter two interviews has been embedded in Chapter 6 Content Analysis by providing quotes of the interviewees. All of the interview minutes are in hands of the author and available upon request.

To strengthen the generalisation of the results from the Content Analysis, additional information was obtained from the two sample firms. The additional information was

obtained to determine the extent to which investors and analysts are interested in the amount of capitalized development costs. This analysis is laid out in Chapter 8 Investors and R&D, in which the Investor Relations departments of AkzoNobel as well as of Royal DSM have been contacted. The contacted persons, Jan van den Bossche (Royal DSM) and Ivar Smits

(AkzoNobel), were approached by email on the 13th and 6th of June 2013 respectively. By comparing the AkzoNobel case with the Royal DSM case and a good comparison

27

can be made, one could assume that the results can be generalised. This is due to the fact that both companies apply to IFRS and are R&D intensive. Therefore it can be assumed that focusing on different companies that are specialized for example in High Tech R&D or Automotive R&D will not lead to different conclusions since the definition of R&D remains the same and they are all subject to the same R&D standards.

Eventually, by consulting these different sources, it should become clear whether the sample companies indeed started to capitalize development costs (more) after the first of July 2001, which is the effective date of the amended RJ210 standard (RJ210, 1999, p.25-26), and whether they, next to the RJ210 standard, applied the IAS 38 standard correct. It will be unravelled further on in this thesis whether managers and controllers who were interviewed believe the amendment has added value to financial accounting and whether it has made financial accounting more neutral.

28

5.

Context Analysis

As you can see in Figure 6 the context analysis will be provided in this chapter. This chapter will introduce AkzoNobel and Royal DSM briefly. These companies are operating globally and are known worldwide. They are two of the main players in the chemical industry and are both very innovative.

Figure 6 Research Methodology Model: Context Analysis

5.1. AkzoNobel

The roots of AkzoNobel can be traced back to as early as 1646. After many years of mergers and

acquisitions, in 1994, Akzo and Nobel Industries merged together to form AkzoNobel (History of AkzoNobel, 2013). AkzoNobel is one of the leading industrial companies in the world. The organization is divided into three branches; Decorative Paints, Performance Coatings and Specialty Chemicals. Decorative Paints are used in and on homes, buildings and infrastructure. Performance Coatings are coatings for, for example, cars, airplanes, boats, buildings, infrastructure, window frames, laptops, wood, pipelines and cosmetic packaging. Specialty Chemicals are crucial ingredients in everything from ice cream to asphalt, plastic to paper, and so on (Organization of AkzoNobel, 2013). The headquarter office is located in Amsterdam, the Netherlands, with 55,000 employees all over the world and it has operations in more than 80 countries. Furthermore, according to their website, they are one of the world leaders in sustainability. Some well-known brands that AkzoNobel created throughout the years are Dulux, Sikkens, Eka and International (About AkzoNobel, 2013). For more information, take a look at their website; www.akzonobel.com.

29 5.2. Royal DSM

In 1902 Royal DSM started as a small coal mining company in the Netherlands. Since then, they started setting up new businesses in different

areas and in 1973 the last coal mine was closed. Throughout the years, the company acquired many companies worldwide to expand its business. Royal DSM is a Dutch chemical

company which is active in three branches; Health, Nutrition and Materials. Products that Royal DSM develops are for example vitamins, antibiotics, pharmaceuticals, food, dietary supplements, personal care, medical devices, food security (anti-infective solutions), automotive, paints, renewable energy, fiber optic coatings and bio-based materials. Just as AkzoNobel, the core value of DSM is sustainability. The headquarter office is located in Heerlen, the Netherlands with 23,500 employees all over the world and has operations in almost 200 countries. Most of the brands that Royal DSM created throughout the years are not well-known since most brands represent ingredients. Some examples are Arnite,

CakeZyme, EcoPaXX and KhepriCoat (DSM, 2013). For further information, take a look at their website; www.dsm.com.

At this point both firms have been introduced shortly. The next step is the content analysis, which will be laid out in the following chapter.

30

6.

Content Analysis

In Figure 7 one can see that we have arrived at the second analysis of the case studies, the content analysis. This chapter contains of the analysis of financial data with regard to how Royal DSM and AkzoNobel are applying the RJ210 and IAS38 standards from the years 2000 till 2012. Moreover, the open interviews with experts from the field with a controlling and/or accounting function and who work for Royal DSM and AkzoNobel will be intertwined throughout this chapter. By examining these results, a conclusion can be drawn about

whether the amended RJ210 and IAS38 standards have made the accounting of these two companies less conservative.

Figure 7 Research Methodology Research:Content Analysis

6.1. AkzoNobel

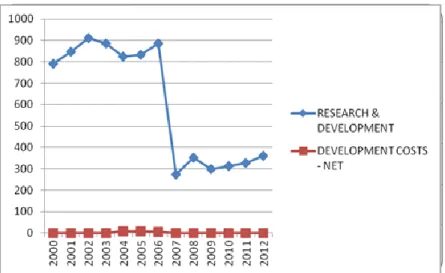

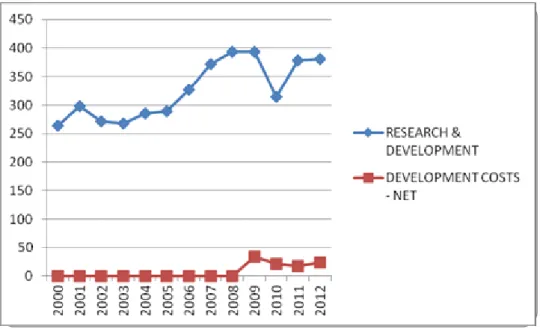

Figure 8 below consists of the treatment of AkzoNobel’s R&D costs in the years 2000 till 2012 (Annual Report AkzoNobel, 2000...2012) as collected from DataStream. The three accounts investigated in are R&D Expenses, which is an item on the income statement, Capitalized Research Costs and Capitalized Development Costs. The latter are both items on the balance sheet. Capitalized research costs and capitalized development costs are both part of intangible assets of a company. By looking at these three accounts one can find out how AkzoNobel treated research and development costs throughout the years. Since the account Capitalized Development Costs is of great importance for this research, the large amount of Not Applicable (NA) for this account in Figure 8 was the trigger to hand collect the data from the annual reports as well. The hand collected data is provided in Figure 9. When amounts differed between the hand collected and database data, they are displayed in bold. When hand collecting data from AkzoNobel, an interesting account was found on the balance sheet; Preparation and Start-up Expenses, as mentioned before. Since this account might possibly be capitalized research, it is included in Figure 9. This account, however, was not available in DataStream.

31

When looking at Figure 9, which contains the hand collected data, you can see that AkzoNobel started capitalizing development costs in 2001 and it kept increasing from then till present day, this treatment is consistent with the revised RJ210 of 2001. On the contrary, when collecting data via DataStream, AkzoNobel capitalized in the years 2004, 2005 and 2006. Other years are not applicable (NA). This makes the data from DataStream less useful than the hand collected data.

In Figures 10 and 11 the research and development costs (income statement) and the development costs (balance sheet) are depicted in a graph. Figure 10 shows the graph for the data collected from DataStream, and Figure 11 shows the data which was hand collected from AkzoNobel. In both graphs one can see an immense decline of the R&D expenses (income statement) from 2006 to 2007. There was a decline of 610 million Euros according to the DataStream data and a decline of 603 million Euros according to the hand collected data. What was the reason for this decline? We shall take a closer look at (the notes to) the financial statements to get a deeper understanding of the decline as well as to explain other changes in the three accounts.

Before we analyse these large variations in the selected accounts, we derived from the financial statements what AkzoNobel stated to use as accounting policy regarding R&D and in what years they comply with Dutch GAAP and/or IFRS. This might help us to get a base understanding of the variations observed in Figure 8-11.

From 2000 to 2004 it is stated in the notes to the financial statements of AkzoNobel that

“As the financial data of AkzoNobel N.V. are included in the consolidated financial statements, the statement of income of AkzoNobel N.V. is condensed in conformity with section 402 of Book 2 of the Netherlands Civil Code (Annual Report AkzoNobel, 2000..2004)”,

therefore AkzoNobel conformed to Dutch GAAP. In the financial statements from

AkzoNobel from 2005 onwards it is stated that the consolidated financial statements have been prepared in accordance with IFRS (Annual Report AkzoNobel, 2005..2012),which is in accordance with the mandatory adoption of IFRS by the European Union in 2005, as well as in accordance to Dutch GAAP as far as applicable. From 2005 to 2012 it is stated in the

32 In millions of Euros Year 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 R&D expenses 790 847 912 887 823 834 885 275 353 298 314 327 361 Capitalized Research Costs NA NA NA NA NA NA NA NA NA NA NA NA NA Capitalized Development Costs NA NA NA NA 8 8 5 NA NA NA NA NA NA IFRS Compliance √ √ √ √ √ √ √ √

Figure 8 R&D Accounting Treatment AkzoNobel collected from DataStream

In millions of Euros Year 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 R&D expenses 790 847 912 887 823 834 885 282 353 338 334 356 387 Capitalized Research Costs NA NA NA NA NA NA NA NA NA NA NA NA NA Preparation and start-up expenses 38 0 0 0 0 0 0 0 0 0 0 0 0 Capitalized Development Costs 0 6 5 8 8 16 17 12 32 39 46 141 166 IFRS Compliance √ √ √ √ √ √ √ √

Figure 9 R&D Accounting Treatment AkzoNobel hand collected from the annual financial statements

financial statements as follows:

“the consolidated financial statements have been prepared in accordance with IFRS as adopted by the European Union, and also comply with the financial reporting requirements

33

included in section 9 of Book 2 of the Netherlands Civil Code, as far as applicable (Annual Report AkzoNobel, 2005...2012, emphasis added)”.

Figure 10 Relationship R&D Expenses and Capitalized Development Costs AkzoNobel (DataStream)

Figure 11 Relationship R&D Expenses and Capitalized Development Costs AkzoNobel (Hand collected)

In the summary of significant accounting policies of the financial statements of 2001 of AkzoNobel it is stated that

“The Company used to expense development costs as incurred. In accordance with the new accounting standard development costs are to be capitalized, starting in 2001, if certain conditions are met. These conditions relate to the (technical) ability and intention to complete and use the intangible asset, and the probability of future economic benefits generated by this

RESEARCH & DEVELOPME NT; 2000; 790 RESEARCH & DEVELOPME NT; 2001; 847 RESEARCH & DEVELOPME NT; 2002; 912 RESEARCH & DEVELOPME NT; 2003; 887 RESEARCH & DEVELOPME NT; 2004; 823 RESEARCH & DEVELOPME NT; 2005; 834 RESEARCH & DEVELOPME NT; 2006; 885 RESEARCH & DEVELOPME NT; 2007; 275 RESEARCH & DEVELOPME NT; 2008; 353 RESEARCH & DEVELOPME NT; 2009; 298 RESEARCH & DEVELOPME NT; 2010; 314 RESEARCH & DEVELOPME NT; 2011; 327 RESEARCH & DEVELOPME NT; 2012; 361 DEVELOPME NT COSTS - NET; 2000; 0 DEVELOPME NT COSTS - NET; 2001; 0 DEVELOPME NT COSTS - NET; 2002; 0 DEVELOPME NT COSTS - NET; 2003; 0 DEVELOPME NT COSTS - NET; 2004; 8 DEVELOPME NT COSTS - NET; 2005; 8 DEVELOPME NT COSTS - NET; 2006; 5 DEVELOPME NT COSTS - NET; 2007; 0 DEVELOPME NT COSTS - NET; 2008; 0 DEVELOPME NT COSTS - NET; 2009; 0 DEVELOPME NT COSTS - NET; 2010; 0 DEVELOPME NT COSTS - NET; 2011; 0 DEVELOPME NT COSTS - NET; 2012; 0 RESEARCH & DEVELOPMENT DEVELOPMENT COSTS - NET RESEARCH & DEVELOPME NT; 2000; 790 RESEARCH & DEVELOPME NT; 2001; 847 RESEARCH & DEVELOPME NT; 2002; 912 RESEARCH & DEVELOPME NT; 2003; 887 RESEARCH & DEVELOPME NT; 2004; 823 RESEARCH & DEVELOPME NT; 2005; 834 RESEARCH & DEVELOPME NT; 2006; 885 RESEARCH & DEVELOPME NT; 2007; 282 RESEARCH & DEVELOPME NT; 2008; 353 RESEARCH & DEVELOPME NT; 2009; 338 RESEARCH & DEVELOPME NT; 2010; 334 RESEARCH & DEVELOPME NT; 2011; 356 RESEARCH & DEVELOPME NT; 2012; 387 DEVELOPME NT COSTS - NET; 2000; 0 DEVELOPME NT COSTS - NET; 2001; 6 DEVELOPME NT COSTS - NET; 2002; 5 DEVELOPME NT COSTS - NET; 2003; 8 DEVELOPME NT COSTS - NET; 2004; 8 DEVELOPME NT COSTS - NET; 2005; 16 DEVELOPME NT COSTS - NET; 2006; 17 DEVELOPME NT COSTS - NET; 2007; 12 DEVELOPME NT COSTS - NET; 2008; 32 DEVELOPME NT COSTS - NET; 2009; 39 DEVELOPME NT COSTS - NET; 2010; 46 DEVELOPME NT COSTS - NET; 2011; 141 DEVELOPME NT COSTS - NET; 2012; 166 RESEARCH & DEVELOPMENT DEVELOPMENT COSTS - NET