Voting in general elections on single day

and in single phase

Varma, Vijaya Krushna Varma

10 February 2014

Online at

https://mpra.ub.uni-muenchen.de/60944/

* This expanded banking syst em w ill help t he Elect ion Commission conduct General

elect ions on single day and in single phase.

* All elect ions from panchayat s t o Parliament can be conduct ed w it h t he help of expanded

banking syst em w it h minimum cost and w it hout rigging and impersonat e vot ing.

* As st at ed earlier t he t here w ill be a bank branch in every village or colony having a

populat ion of 2,500.

* Every cit izen above t he age of 15 years w ill have one compulsory M ain Savings Account

in t he banks. Each individual w ill have only one M ain Savings Account . There w ill be no

possibilit y of generat ing duplicat e M ain Savings Account s for t he same person. Individual

can have any number of Sub Savings Account s if he w ishes. There is no limit for having Sub

Savings Account s for each individual but t here w ill be only one M ain Savings Account for

each individual above t he age of 15 years.

* Each bank branch w ill handle approximat ely 2000 M ain Savings Account s.

* All cit izens above t he age of 18 years as recorded in t heir M ain Savings Account w ill have

vot ing right s aut omat ically.

* All banks are connect ed t o cent ral servers maint ained by Cent ral bank. All cit izens’ finger

print s’ dat a w ill be st ored in Cent ral Bank servers.

* Cit izens need not enrol t heir names in vot er list s as in t he present syst em. All cit izens w ill

get int o vot er list s once t hey get t he age of 18.

* No government machinery is needed t o enrol cit izens in voter list s.

* There w ill be no possibilit y of complaint s from vot ers for non inclusion of t heir names in

vot er list s

* The banks w ill submit t he list of all individuals above t he age of 18 years according t o t he

M ain Savings Account s handled by each bank branch t o t he Elect ion Commission as and

w hen t he Elect ion Commission asks for it .

* As it is st at ed earlier t here w ill be a bank branch in every colony or village having

populat ion of 2500.

* Each bank branch premises should have t w o huge rooms/ part it ions/ floors/ blocks

* The one room/ part it ion/ floor/ block w ill be used for daily banking operat ions and t he

second room/ part it ion/ block/ floor in t he same bank premises w ill be used as polling boot h

for all elect ions from panchayat s t o Parliament , from general elect ions t o bye-elect ions

* In t his second room/ part it ion/ block/ floor of every bank branch t w o vot ing machines are

placed permanent ly and in w orking condition

w ill be st ored in t he Cent ral Elect ion Commission servers

* The vot ing machines w ill have t w o part s. The upper part w ill have screen out side as in

t he ATM s. The low er part w ill be empt y

* On t he screen of t he upper part of t he vot ing machine t here w ill be elect ions symbols of

t he cont est ing candidates. These symbols w ill be in single row .

* The elect ion symbols are same in all vot ing machines of all branches t hat are sit uat ed in

same const it uency.

* The symbols in t he vot ing machines may vary according t o t he cont est ing candidat es in

different const it uencies.

* These are designed t o regist er vot es bot h digit al recording and symbol print ing on roll of

paper

* Every machine w ill have separat e spools for all symbols. The roll of t he paper spool

should be 50 met res long and w idt h of t he roll should be 2 cm. The paper slip t hickness

t hat is being used in t he present ATM s is enough t o t his vot ing paper also.

* The ent ire roll of paper w hich is 50 met res long should be divided int o 2500 square part s.

Each part on t he roll of paper is 2 cm w idt h and 2 cm height .

* Inside t he vot ing machines t hese 8 spools are fixed in alignment of t he symbols on t he

front screen of t he vot ing machine

* One square part of each spool paper can be seen empt y from out side.

* One square part of each spool paper can be visible side by side in a single row t hrough

glass below each symbol of cont est ing candidat es.

* On t he back side of each part of t his spool paper t here w ill be serial numbers from 1 t o

2500. These numbers w ill not be visible t o t he vot er.

* If t here are more t han 8 candidat es cont est ing in const it uency t hen t here w ould be t w o

vot ing machines. To reduce t he number of cont est ant s and eliminat e t he non serious

cont est ant s elect oral reforms are required. See t he w eb sit e -

w w w .elect oralreforms.net

* When a vot er w ant s t o cast his vot e he has t o put his left hand on t he symbol he w ant s

t o vot e.

* The vot ing machine w ill scan t he fingers image, t ally w it h t he dat a at cent ral servers and

regist er his choice of vote digit ally inside t he vot ing machine. The count ing number of each

symbol w ill not be visible t o t he vot er. But t he cumulat ive number of all vot es on all

symbols w ill be displayed on t he vot ing machine [It can be seen on t he vot ing machine by

t he vot er] Every t ime a vot e is regist ered by t he vot ing machine t he t ot al number increase

by one number.

* At t he same t he vot ing machine w ill print a small symbol of t he vot er’s select ed symbol

on square part on t he symbol’s spool paper and t he spool rolls 2 cm dow nw ards.

spool rolls 2 cm dow n in t o low er part of t he vot ing machine. Now t he next empt y square

part on t he roll paper is seen.

* When t he next vot er arrives he w ill see only empt y square part on all spool papers. He

w ill cast his vot e and comes out . All t his happens in a few seconds for each vot er.

* The vot ing machine w ill not regist er t he vot e if t he vot er t ries t o put his hand on t he

machine second t ime. It inst ant ly sends out a w arning siren. The securit y guards w ill t ake

him out side.

* There w ill be a screening machine at t he ent rance of t his polling room. This is not vot ing

machine. This is vot e slip producing machine. Every vot er before ent ering t he room w ill

have t o put his left hand on t he screen of t his machine. The machine w ill scan t he finger

images, t ally and check w it h t he st ored dat a and produce small vot e slip if t he vot er has

an account in t hat branch and if he did not vot e already. The machine w ould not produce a

vot er slip for second t ime for t he same person. The vot er slip cont ains his name and

account number.

* Then t he vot er w ill be allow ed int o t he vot ing room and should hand over t he slip t o t he

polling official.

* The polling room should be divided int o t hree part s. In t he first part t he vot ing machines

w ill be placed. In t he second part t he polling officials w ill sit and in t he t hird part t he

polling agent s of t he cont est ing candidates w ill sit

* There w ill be screen board in t he polling room connect ed t o t he vot ing machines.

* The screen board w ill show t he t ot al vot er number at each vot e cast . The t ot al number

w ill increase by one number aft er each vot e is registered

* When t he voter cast his vot e, his name and vot er number w ill be displayed on t he board.

* The boot h agent s w ill mark t he vot ers’ names in t heir list s

* All t he vot ing machines w ill be connect ed t o t he cent ral servers in t he Cent ral Elect ion

Commission.

* In t his w ay t he t ot al number of vot es polled can be known according t o boot h w ise,

const it uency w ise, stat e w ise and count ry w ide at every second.

* At t he end of t he day t he t ot al number vot es cast w ill be not ed by t he polling officials and

polling agent s. The rooms w ill be sealed and cc video cameras w ill be act ive monit oring

t he vot ing machines and w hole inside of t he vot ing room.

* The polling boot h official should hand over t he collect ed vot er slips t o his higher

aut horit ies.

* The count ing can be done t he next morning. There w ill be no need t o move vot ing

machines t o count ing cent res.

* The polling officials w ill open t he vot ing machine in t he presence of polling agent s and

w it h full coverage of cc video cameras. This ent ire process of count ing should be made

public and put on t he int ernet .

recorded and also t he last print ed number on back side of t he roll of spool paper in t he

presence of polling agent s. The digit al recording of t he symbol and print ing number of t he

symbol should be same and w ould be t he same. The t ot al number of vot e’s regist ered and

t ot al individual votes of all symbols should be same.

* The digit al recording of all vot es w ill be connect ed t o t he const it uency server and Cent ral

elect ion commission servers.

* This process can be complet ed w it hin half an hour.

* The final result s can be declared by t he Cent ral Elect ion Commission w it hin one hour on

t he count ing dat e.

* There is absolut ely no possibilit y for bogus vot ing, impersonat e vot ing and rigging

* There w ill be no need for boot h officials t o put a mark on vot er’s finger and verify t he

vot er list s.

* Vot ing w ill t ake less t ime. There w ill be no long queues out side polling boot hs. Each

vot er ent ers t he polling boot h, put his left hand on t he symbol of his choice on t he screen,

see his symbol print ed on t he roll paper and rolls dow n and ret urns back. Vot ing is as

simple as t hat .

* Elect ions can be conduct ed on single day in single phase.

* The vot ing should be conduct ed on bank holidays and st aff of bank branches should be

int erchanged for polling dut y.

* The polling officials should be paid double amount for w orking on t his day.

* To oversee t he polling ot her government employees can be deput ed as poll observers at

each polling boot h [bank branch] one poll observer at each polling boot h is necessary for

smoot h conduct of elect ions.

To achieve 100% free and fair elect ions t he government should implement elect oral and

polit ical reforms

See t he w ebsit e -

w w w .elect oralreforms.net

w w w .polit icalreforms.net

Tradit ional Copy Right – All Right s Reserved

The w orking modules for expanded banking syst em

Are

available

t o

dow nload

on

w ebsit es

--

M ulti dimentional M ain Savings Account

- It is the main keel of this restructured banking.Purpose of this multi dimensional account

1. This savings account can be used for receiving, storing and spending of money.

2. It can be used for buying, selling and holding property rights of immovable properties like lands, plots, flats and commercial establishments.

3. It can used for buying, selling and holding properties rights of movable properties like vehicles, gold etc.

4. It can used for buying, selling and holding shares

5. It can be used for getting driving license, passport, birth certificate, voter ID card, ration card, pension, relief funds, subsidies, and compensation.

Application of this new restructured banking system:- Banking is expanded so that taxation, tax collections, tax enforcement, tax compliance, registration departments, pass port offices, land registration departments, vehicle registration departments, share transactions, Public distribution system, census department, revenue department can be unified and integrated in this new banking system.

Salient features

Fully liberalised and self regulating banking sector

1. Automatic adjustment of money supply in banking system w ithout any external regulators 2. No external regulators needed to control inflation and deflation.

3. Portable savings account. Customers can shift their accounts w ith same account number from one bank to another bank at any time w ithout need for closing their accounts in the past bank and opening in the new bank.

4. Portable savings account number. It is valid, active, permanent and portable during his/ her entire life period from the time it w as given and up to his/ her death.

5. No non-performing assets [NPA]

6. Loans can be sanctioned w ithin 5 minutes w ithout need for documents, encumbrance certificates, legal opinions, mortgages.

7. Easily distinguishable real money and loan money

8. No common financial year for all accounts. Financial year of an account begins on the day it opened. There w ill be no need to submit annual tax returns. All accounts are involuntary taxpaying accounts.

9. Banks w ill only handle citizens’ savings accounts. The banks are handlers of savings accounts and they do not ow n them.

10. M oney, in this restructured banking, does not have storage value. It w ill have only transaction value. That means there w ill be no interest rates on demand deposits and fixed deposits. M oney w ill have no depreciating value. In fact Rupee’s value is more or less constant. Expansion and contraction of money supply according to the demand is automatic in this new banking system.

11. Total values of money supply, physical money, digital money, loans/ advances, Real money Banks’ capital money in the entire banking system can be know n at any point of time.

13. By using this restructured banking system, single phase election on single day can be held throughout the country w ith help of banking sector. No rigging, no impersonation of voting and no electoral mal practices can be possible in this new banking structure.

14. Electoral rolls/ voter listed can be prepared and supplied to Election Commission by banks w ithin one hour. These voter lists get updated at every second.

15. 100% accountable and transparent governance 16. No bankruptcy of banks

17. No third party or agencies required to deposit cash in the ATM s.

18. Economy can be run on limited paper currency. 99.4% of total money supply w ill be in digital form and only 0.6% of total money supply w ill be in physical form in Rs 30, Rs. 20, and Rs. 10 notes apart from Rs. 5 Rs. 2 and Rs. 1 coins.

19. Fixed CRR at 10%. It is permanent and there is no need change from time to time. 20. Fixed PLR at 3%@ per annum up 10 lakhs and at 4% per annum on loans above 10 lakhs.

21. M ain savings account in this new restructured banking system is an involuntary taxpaying account just like respiratory system in human body. No tax returns, accounting and auditing required.

22.Banks’ profits can be know n at every day, every hour or even at every minute.

23. There w ill be no vacancy for cheating chit fund companies in this restructured banking system. 24. Easier and quicker liquidity of all assets that belong to a person or organisation into cash w ithin minutes.

Advantages of

M ain Savings Account

Every bank branch w ill become an E-Seva centre.

1. Vehicle registrations and the transfer of ow nership rights of vehicles can be made at any bank branch w ithin 5 minutes. No regional transport offices are required.

2. Registration of properties like lands, flats, plot s and all immovable assets can be made at any bank branch. Registration for selling/ buying of properties can be made w ithin 5 minutes. No registration departments are required.

3. There w ill be no tax collection expenditure for the Governments and no tax compliance cost for the people.

4. Citizens need not maintain separate account books and submit tax returns annually for paying either Direct taxes on personal incomes or Indirect taxes w hile running business or industry.

5. There w ill be no check posts, w ay bills, accounting, auditing, tax laws, tax raids, etc

6. Electoral rolls can be available at banks at any time as and w hen required by Election commission. The electoral rolls w ill get updated constantly at every second in banks.

7. Exact population figures can be available at every second.

8. Birth certificates, death certificates, rations cards, can be got at any branch w ithin five minutes 9. People can get passports at any bank branch w ithin five minutes.

10. Selling/ buying of shares can be done at any bank branch.

11

.

There w ill be no multiple selling of the same property to different people and unauthorised selling/ purchase and illegal occupation of other person’s property w ithout his/ her know ing/ consent w ill not be possible.12

.

Total elimination of black money, fake currency, corruption and money laundering13

.

Out of total money supply 99.4% w ill be in digital form and only 0.6% of total money supply w ill be in physical form.* The government should build t he basic infrast ruct ure [building premises and int ernet connect ions] for providing banking service for every village/ suburb/ t ow n or colony having a populat ion of around 2500 w it h t he help of privat e sect or banks and inst it ut ions. India need 5,00,000 fully fledged bank branches. Each bank shall handle approximat ely 2000 account s on average.

* Banking licence should be fully liberalised.

* Banking licence should be given t o any promot er or inst it ut ion t hat has capit al invest ment of minimum one t housand crore rupees. The qualificat ion t o st art banking business should be a minimum capit al invest ment of 1000 crore rupees. Even individuals or a set of people w it h capit al of 1000 crores shall be allow ed t o operat e banking business.

* Banks should be allow ed t o handle bank account s w hose cumulat ive t ot al money should not exceed 18 t imes t he bank’s ow n capit al money.

* Banks should be allow ed t o generat e money and sanct ion loans up t o 9 t imes t he value of it s capit al money but not more t han t he 47.37% of t he value of [t ot al digit al money in all account s it handles + it s ow n capit al money in digit al and physical form]. Read more on money supply [real money and loan money] on page 16.

* [For example if a bank has 1000 crore has it s capit al money, t he t ot al money it w ill be allow ed t o handle from all it s account s is 18,000 crore rupees. So w it h t he capit al of 1000, t he t ot al money supply t he bank can handle is 1000+18000= 19000. Wit h t his t ot al money supply t his bank handles, t he loans sanct ioned by t his bank should not exceed t he value of 47.37% of 19000crores] = 9000. Wit h t he 1000 as it capit al money, t he maximum level of t his bank’s money handling capacit y of 19000 crores = 9,000crore loan money [maximum level] + 10,000 crore real money]. As t he bank’s capit al money increases it s money handling and loan generat ion capacit y w ill increase correspondingly.

*

A bank’s money supply handling capacit y w it h 100 as it s capit al w ill be at t he level of 100 w hen t he bank has zero account s at t he launching t ime and it can reach up t o at t he maximum level of 1900.*

A bank’s loan money generat ion capacit y w it h 100 as it s capit al w ill be at t he minimum level of 47 and at t he maximum level of 900 w hen t he bank reaches t he maximum level of t ot al money it handles reaches 1900. On t he first day w it h 100 as it s capit al t he bank, w it hout any account s, can generat e and sanct ion loans up t o 47 only. If t heir account s increase, t he money it handles also increases and correspondingly t he money generat ion capacit y also increases up t o t he maximum level of 900 w hen t ot al money it handles in all it s account s reached t he maximum level of 1900.* Banks should not be allow ed t o use or w it hdraw it s capit al money by its promot ers for any purpose ot her t han paying salaries, st at ionery or ot her running or operat ing cost s of t he bank. That means t he init ial capit al money cannot be used for any ot her purpose or w it hdraw n by it s promot ers.

* There should be one bank branch for every 2500 people. That means t here should be a bank branch in every village or colony w it h a populat ion of 2500 people. India need 5,00,000 bank branches and minimum of 15 lakh bank employees. See Bank’s operat ing cost and profit s on page 57 onw ards. * The government should bear ent ire cost of t he rent al charges, int ernet charges and current charges of bank branches sit uat ed in rural areas t o promot e est ablishing bank branches at t he rat io of one branch for every populat ion 2500 t o 3000 people.

In t his new banking syst em t here w ill be t hree t ypes of account s. The t hree t ypes of

bank account s are called

1

M ain Savings Account

2 Sub Savings Account [SSA]

and

3

Corporate Account Number.

generat ed at t he servers maint ained by t he Cent ral Bank. If t he user t ries t o provide t he same biomet ric t o open anot her account in t he same branch or anot her branch anyw here in t he count ry, t he main server should be able t o ident ify and reject t he new account generat ion for t he same individual. There should not be mult iple generat ions of account numbers w it h an individual’s same biomet ric dat a [finger print s and iris]

*

It should be made mandat ory for every cit izen above t he age of 15 years t o t ake a M ain Savings Account in any bank branch.* The servers should have t he capacit y t o handle 150 crore individuals’ dat a and be able t o handle 1500 crore t ransact ions every day.

*

Aft er est ablishing sufficient number of banks/ service cent res by t he Government (for example, India) w it h t he help of privat e sect or banks and financial inst it ut ions, all t he cit izens above age of 15 years should be asked t o open M ain Savings Account s at any bank w it hin 30 days w it hout need for any init ial deposit s. It can be opened w it h zero balance. Indians, w ho reside out side India, should be given six mont hs t ime t o open M ain Savings Account at any branch in India. All t hese bank branches are connect ed t o cent ral servers. No second generat ion of M ain Savings Account number of any person w ould be possible w it h t he same dat a of his/ her finger and iris images. There aft er no new M ain Savings Account should be given t o any individual. From here aft er anyone w ho does not have M ain Savings Account should be deemed as illegal migrant . All new babies born are t o be are recorded in t heir mot hers’ personal account in her M ain Savings Account w it hin t hree mont hs of t heir birt h. In case of orphans t hey should be recorded in Government ’s social w elfare minist ry account . Once t hey get t he age of 12 years t he banks generat e t heir M ain Savings Account w it h t he digit al recording of t heir finger print images and iris dat a. Aft er t he init ial launch of t his syst em t here should be no generat ion of M ain Savings Account s for individual w ho are not recorded at t he t ime of t heir birt h eit her in t heir mot hers M ain Savings Account or Government ’s social w elfare minist ries’ account .*

A person’s M ain Savings Account number w ill remain same for his/ her ent ire life t ime. He/ she can change t he bank at any t ime but t he account number w ill remain same. That means t he M ain Savings Account number is port able, act ive and permanent during his/ her ent ire lif e period. These permanent M ain Savings Account numbers cannot be changed. These account numbers w ill become ceased or closed only upon deat h of t he account holder.Usage of M ain Savings Account

Unlike savings account in t he present banking syst em, t his M ain Savings Account consist s of 5 sub account s. It is a combinat ion of 1] M oney Account 2] Land Savings Account [LSA] 3] movable property account (M PA) 4] Shares Account (SA) 5] Personal Account (PA).

The M SAshall be used t o deposit , w it hdraw , receive or pay salaries, professional fees, service fees, remunerat ions, donat ions, loans et c The M ain Savings Account (M SA) should also be used for buying of shares, land for agricult ure or indust rial purpose, plot s, flat s, gold, jew ellery, vehicles, commercial est ablishment s or any ot her movable or immovable propert y.M ain Savings Accountis also needed t o get driving licence, passport , vot ing right , subsidies, funds, mont hly rat ion, pensions, remit t ances and loans (personal, agricult ure, business, educat ional and indust rial) and for get t ing compensat ion/ exgrat ia/ relief funds in t he event of nat ural calamit ies like cyclones, eart hquakes, floods, famines, accident s, et c,

From here onw ards t his rest ruct ured banking syst em is called “ TOP TAX SYSTEM ”

years t o have M ain Saving Account . Children below t he age of 12 years w ill be regist ered in t heir mot her’s or fat her’s or guardian’s or social w elfare minist ries’ or NGO’s account . From t here aft er every child w ill get M ain Savings Account once he/ she reaches 12 years of age. Alt hough t his account number is given and regist ered in t he mot her’s M ain Savings Account w it hin one mont h of child’s birt h, it w ill be act ivat ed and come int o live account only w hen t he child reaches 12 years of age as decided by t he Government . A person’s M ain Savings Account w ill become operat ional and st art funct ioning from t he age of 12 years as decided in t he part icular count ry. In case of orphans t he account numbers w ill be regist ered in t he social w elfare minist ries’ account s and it should be made mandat ory for St at e Governments t o look aft er every orphan’s w ell-being and care t ill he/ she reaches t he age of 20 years and he/ she get s employment .

The 15 digit M ain Savings Account number w ill act as money savings account, movable property account, immovable properties account, shares account, citizenship card, taxpaying account, ration card, Pass port and voter identity card.

An example of M ain Savings Account number –

210801101456789

The first t w o digit s from left side 21 indicat e t he day, t he next t w o digit s 08 indicat e t he mont h and t he next t hree digit s 011 indicat e t he year w hen t he M ain Savings Account is issued t o t he person or his/ her birt h year. Alt hough t his account number is given and regist ered in t he mot her’s M ain Savings Account w it hin t hree mont hs of t he child’s birt h, it w ill be act ivat ed and become int o live account at t he age of 12 or 15 years as decided by t he Government. A person’s M ain Savings Account w ill become operat ional and st art funct ioning from t he age of 12 or 15 years. In t he case of orphans t he account numbers w ill be regist ered in t he social w elfare minist ry’s account and it should be made mandat ory for St at e Government t o look aft er every orphan’s care t ill he reaches 20 years and unt il he/ she get s employment . That means t here w ill be no st reet children and child labour.

The eight h and nint h digit s from t he left side [01] denot e t he main savings account . It is comm on for all M ain Savings Account s. The last six digit s 456789 are serial numbers of t he M ain Savings Account s. That means on each day t he nine digit s from t he lef t side w ill remain same. The last six digit s from right side w ill be from 000001 t o 999999. The person can choose his/ her M ain Savings Account number from t he available numbers. Wit h t he change of dat e, mont h and year t he last six digit serial numbers w ill repeat . For every 999 years t he 15 digit M ain Savings Account numbers w ill repeat once again.

M ain Savings Account

Land Savings Account

[lands, plot s, flat s, commercial

est ablishment s, buildings, houses et c., ]

Vehicles Account

[vehicles, gold]

Shares Account

[SA]

Once t aken/ given, t he M ain Savings Account number is permanent for his/ her ent ire life. From t hen he/ she can choose any bank t o maint ain and operat e his/ her M SA. As said earlier M SA is port able bank account . The M SA w ill cont ain 5 sect ions/ sub account s. A person’s money, immovable propert ies, movable propert ies, shares and family det ails w ill be maint ained in different sect ions/ sub account s of a person’s M ain Savings Account . The 5 sub account numbers of M ain Savings account are same except

t he nint h digit . If t he nint h digit is 1, it is money account

.

210801101456789

This number implies that21-08-011-01-456789

[Dat e-mont h-year-M SA-serial number]

If t he nint h digit is 2, it is immovable propert y account. If t he nint h digit is 3, it is movable propert ies account . If t he nint h digit is 4, it is shares account .

If t he nint h digit is 5, it is family account .

The overview of a

M ain Savings Account

click here t o dow nload

M ain Savings Account 210801101456789

210801101456789 M ain Savings Account / M SA

210801102456789 Immovable propert ies/ Land Savings Account 210801103456789 Vehicles Account

[M PA] movable propert ies 210801104456789 Shares Account (SA)

210801105456789 Personal Account (FA)

The user name, profile pass w ord, logs in passw ord and t ransact ion passw ord are same for all t hese sub account s of a person’s M ain Savings Account . Thus t he M ain Savings Account is a mult i dimensional and mult i funct ional single savings account for st oring/ using money, for buying/ selling of shares, movable and immovable propert ies, for direct receiving of subsidies, pensions, relief funds, rat ions, scholarships et c., from t he Government . The main funct ions of M ain Savings Account are

*

M oney account is just like t he present savings account w here money w ill be st ored and used. M oney in flow s (credit s) and money out flow s (debit s) w ill be recorded in t his account . M oney can be used or spent t hrough cheques, debit cards, credit cards, demand draft s and online t ransfers only. There w ill be no pay orders and ot her means of conveyance for money. M oney flow s w ill be only in five forms.*

Buying, selling or mort gaging of immovable propert ies like lands, plot s, flat s, house, commercial est ablishment s et c., w ill be recorded in land savings account (LSA) of his/ her M SA, w hich is managed by banks. Purchases and selling of immovable propert ies w ill be done t hrough t his account by banks.*

Buying, selling and mort gaging of movable propert ies like vehicles and gold w ill be recorded in t he movable propert ies account (M PA) of his/ her M SA.*

Buying or selling of shares w ill be recorded in t he shares account (SA).*

A person’s personal account is used as a rat ion card, cit izenship card, vot er card, passport , driving license, hall t icket for all exams, CV and insurance policy.[B] Sub Savings Account (SSA)

Every cit izen w ould be allow ed t o open any number of Sub Savings Accounts (SSA) by using t he same

open Sub Savings Account s t o run t hese indust ries or business cent res in mult iple places in t he count ry. These Sub Savings Account numbers are also port able. People can change t he banks t o operat e t heir Sub Savings Account s at any t ime. Usually people, w ho run business or indust ry, w ill need Sub Savings Account s. Generally 10% (approximat ely) of t ot al populat ion of any count ry, w ho run business or indust ries w ill need Sub Savings Account s. Even individuals w ho do not run business or indust ry shall be allow ed t o open Sub Savings Account s. In Sub Savings Account s only money w ill be managed by banks.

An example of Sub Savings Account number

210801110456789 -

The Sub Savings Account number of a person is same as of his/ her M ain Savings Account except t he eight h and t he nint h digit s from left side. He/ she can choose Sub Savings Account numbers from 10 t o 99. The remaining 13 digit s w ill remain t he same as of his/ her M ain Savings Account number. That m eans t he Sub Savings Account s of a person are offshoot s from his/ her M ain Savings Account . He/ she can open up t o 89 Sub Savings Account s t o run mult iple indust ries or business act ivit ies locat ed at different locat ions. If he/ she needs more t han 89 account s t hen he/ she w ill have t o t ake Corporat e Account numbers. These Sub Savings Account s w ill be used t o maint ain money only.The Sub Savings Account s (SSA) and also t he M ain Savings Account s (M SA) can be used for running business, indust ry, schools, colleges, hospit als, hot els, rest aurant s, const ruct ion, st udios, services, or any ot her t ype of business. Just like M SA, t he SSA can also be used t o receive or pay salaries, professional fees, service fees, remunerat ions, donat ions loans et c,

210801110456789 –This number implies t hat 21-08-011-10-456789 [dat e-mont

h-year-SSA-serial number]

[C] Corporat e Account Numbers (CAN)

Corporat e account is a seven layer account – it is seven layer account s for 1] money operat ion, 2] immovable propert y account 3] movable propert y account 4] shares account 5] man pow er account 6] raw mat erials account 7] finished product s account

Corporat e account number - Finance account

Immovable propert y account-

1

00801101001345

M ovable property account -

2

00801101001345

Shares account -

3

00801101001345

M an pow er account [employees] -

4

00801101001345

Raw mat erials account -

5

00801101001345

Under proposed TOP Tax syst em t he account ing and audit ing of t he corporat e or public companies w ill be mandat ory and compulsory as in t he present syst em for prot ect ing t he int erest s of t he invest ors. Corporat e or public companies, w hich issued share t o public, w ill be given Corporat e Account Numbers (CAN).

An example of Corporat e Account number

000801101001345

The f irst t hree digit s from lef t side are zeroes in all Corporat e Account Numbers. The next t w o digit s 08 indicat e mont h and t he next t hree digit s 011 indicat e t he year of t he account number t aken. The eight h and t he nint h digit s 01 indicat e t he indust ry or sect or codes. The next t hree digit s 001 indicat e t he product code and last t hree digit s 345 are serial numbers of indust ries regist ered in t he same mont h. In t he same mont h, t he last t hree digit s w ill repeat many t imes [possible 99,999 t imes if need] for different sect ors/ indust ries and for different product s. 0008011101001345 This number implies t hat 00-08-011-01-001-345 [00-mont h-year-indust ry code-product code-serial number]

Corporat e Account

number

0008011010013

45

000801101001345

M oney Account

100801101001345

Immovable propert ies/

Land savings account (LSA)

200801101001345

M ovable properties account

300801101001345

Shares account (SA)

400801101001345

M an pow er account

500801101001345

Raw mat erials account

600801101001345

Finished product s account

The corporat e or public companies w ill have t o operat e all cash t ransact ions t hrough t he Corporat e Account Number (CAN) only.

An example of Cent ral Government account number

222222010013456

In all Cent ral Government account s t he first six digit s 222222 from left side are t w os. The next t w o digit s 01 indicat e minist ry code. The next t hree digit s 001 indicat e depart ment or inst it ut ion code and t he last four digit s 3456 indicat e serial numbers.

An example of St at e Government account number

333301010013456

minist ry codes. The next t hree digit s 001 indicate depart ment or inst it ut ion codes and t he last four digit s 3456 indicat e serial numbers

.

An example of Bank [Financial inst it ut ion] account number

999000001456789

456789 is t he bank

[Financial inst it ut ion]

account number and 000001 is one of it s

branch code numbers.

For all bank account s t he first t hree digit s are 999. The last five digit s 456789 are bank account numbers. The banks can choose t heir account numbers available at t he t ime of regist rat ion from 000001 t o 999999. The middle six digit s 000001 are t hat part icular banks’ branch code numbers. The bank can allot any code numbers from 000001 t o 999999 t o each of it s branches.

Banks [financial inst itut ions] operat e M SAs, SSAs and CANs as long as t he account holders w ant . But t hey w ould not ow n t hese account s. These account s are port able and can be shift ed from any bank t o any bank at any t ime.

Non Government organisat ion account numbers st art w it h four 4’s 444400000000000 Educat ional inst it ut ions numbers st art w it h four 5’s 555500000000000

Healt h care service inst it ut ions’ account number st art w it h four 6’s 666600000000000 Trust s’ account numbers st art w it h four 7’s 777700000000000

Usage of M SAs, SSAs and CANs:-

In t he present economic syst em a person’s or a company’s money, movable or immovable propert ies(like vehicles, plot s, flat s, houses, fact ories, commercial est ablishment s, lands et c.,) shares, family t ree, insurance policies and all ot her asset s are recorded, managed and handled by different depart ment s, agencies or inst it ut ions.

But in t he suggest ed TOP Tax syst em each individual above t he age of 12 years w ill have one M ain Savings Account consist ing of five folders. M oney, movable or immovable propert ies (like vehicles, plot s, flat s, houses, commercial est ablishment s, lands et c.,) shares, family t ree, insurance policies et c., are recorded, managed and handled in a single account called M ain Savings Account (M SA) w ith five folders in case of individuals and in Corporate Account Numbers (CAN) w ith seven folders in case of companies w hich issued shares for public. These accounts namely, M SAs, SSAs and CANs w ill be maintained and operated by banks replacing different departments, tax collection and tax enforcement boards, agencies or institutions of the present economic system.

Thus people’s money, shares, all movable and imm ovable propert ies w ill be in only one account (M SA)

w it h different folders operat ed by banks.

1.

M ain Savings Account

(M SA)

- There w ill be only one compulsory and mandat ory M SA for each person given by t he Government . This M SA w ill have five sub account s for each specific purpose of an individual.The first sub account (M oney account) w ill be used for st orage and usage of money got t hrough savings/ earnings/ incomes/ donat ions. This M SA can also be used t o run or operat e any business or indust ry ow ned w holly by an individual.

est ablishment s, and et cet era. The ow nership right s of t hese asset s w ill be t ransferred from one person’s LSA t o anot her person’s LSA w hile purchasing/ selling/ donat ing of t hese immovable propert ies.

Vivid explanation:

-

Land Savings Account/ LSA

In t his suggest ed TOP Tax syst em t he Land Savings Account of each person shall be ut ilised as t he de-mat account of t hat person’s ow nership right s of immovable propert ies like lands, plot s, flat s, asset s, fact ories and ot her est ablishment s in t he ent ire count ry. While purchasing or selling, t he t ransfer of ow nership right s of t hese asset s/ propert ies from one person t o anot her person shall be made from one person’s LSA t o anot her person’s LSA t hrough banks/ service cent res. So t he t ransfer of asset s like lands, plot s, flat s, st ruct ures and ot her est ablishment s w ill t ake place in physical form upon t he t ransfer of ow nership right of t hat asset in digit al form from one LSA (seller) t o anot her LSA (buyer). TOP Tax syst em suggest s t hat t ot al land record of t he count ry should be demat erialised according t o ext ent , locat ion, mapping and ow nership. The land belongs t o people w ill be recorded in t heir respect ive LSAs. Similarly t he land t hat belongs t o Government , Government organisat ions, companies should be recorded in t heir respect ive account s.Repeat;- Under the TOP tax system the purchase of lands, plots, flats or other properties should be made through Land Savings Account (LCA), the sub account of M ain Savings Account (M SA) operated by banks. If any person buys land, plot, flat or any ot her property anyw here in India the extent and nature of the property w ill be credited in his Land Savings Account and the same property w ill be debited from the seller’ Land Savings Account (LSA). W henever he/ she sells any property that is credited in his LSA, the same w ill be debited from his/ her Land Savings Account and the same property w ill be credited in the buyer’s Land Savings Account (LSA). The credit in the LSA means purchase of immovable property and debit means selling of immovable property. The immovable properties w ill be in dematerialised form and the ow nership rights can be transferred from one account to another account just like money transfers and shares. Just like shares there w ill be no paper documents for properties. Unlike cash transfers the buyer’s presence and signature/ authentication shall also be needed for any property transaction. A bank statement of the second folder (LSA) of any person’s M ain Savings Account w ill hold the entire ow nership rights of that person’s all immovable properties in the entire country. The People can get these bank statements of their properties at any time at banks in addition to w eekly, monthly or yearly statements by post or e-mails or both. They w ill get phone messages and email statements immediately after each property transfer.

There w ill be no multiple selling of the same property to different people and unauthorised selling/ purchase and illegal occupation of other person’s property w ithout his/ her know ing/ consent w ill not be possible.

Advantages of

Land Savings Account/ LSA

:-1. Land ceiling act

In the present system rich people are having huge tracts of agriculture lands in different districts and States making mockery of the land ceiling act. The registrations of lands, flats, plots and other properties are being made by the registration departments and land records are maintained by revenue departments.

district, state, extent and date of selling/ buying of each property of each person w ill be recorded and maintained in Land Savings Account (LCA).

The Land Savings Account w ill be operated and maintained by banks just like money savings accounts. Debits and Credits of all properties w ill be made in the Land Savings Account w hile a person buys or sells his property. The total extent of land recorded in all Land Savings Accounts belonging to people, Governments, departments, organisations, companies, institutions etc., w ill remain exactly the same even after countless number of debits and credits each day. The Land Savings Account w ill show an individual’s exact ow nership rights of his/ her all immovable properties. The total land extent in each Land Savings Account w ill never cross the upper limit of 20 acres (as envisaged in TOP Tax system) strictly adhering to land ceiling act. There can be absolutely no multiple selling of same property t o different people. It w ill become impossible for any individual to ow n huge extent of lands (beyond land ceiling act) under different names in different locations of the country. TOP Tax system ensures that the land ceiling act can be implemented in totality to perfection making Government’s task easier in pushing forw ard land reforms and allocating land to landless poor.

There w ill be no paper documents for all movable and immovable properties. Hence no separate registration and revenues departments are needed in the suggested TOP Tax system. Only land survey department w ould suffice to mark and clear boundary disputes.

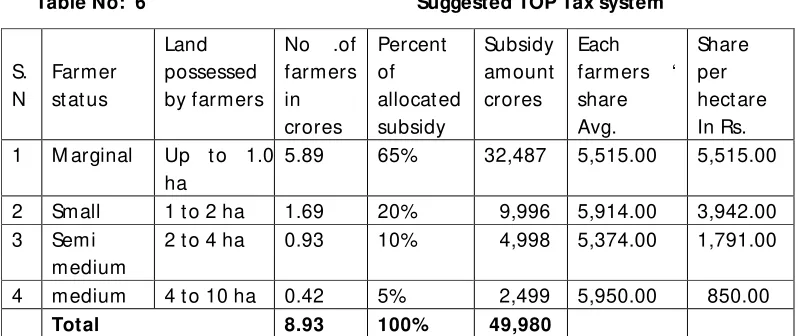

2. Farm subsidies; -

In present system 90% of total farm subsidies are being gobbled up by rich farmers (10%), w hile the small and marginal farmers (90%) are getting only 10% of total farm subsidies. This anomaly can be totally checked in TOP Tax system w here Land Savings Account is a sub account of M ain Savings Account operated by banks. According to records in Land Savings Accounts, the t otal farm subsidies (100%) w ould reach the small and marginal farmers w hile keeping aw ay rich farmers from all subsidies. Here rich farmers means industrialists, contractors, professionals, celebrities, individuals, politicians, business class, salaried class (govt or private) etc., w hose annual incomes are more than 2,00, 000 (other than agriculture income).3. Farm loans; -

In the present system getting farm loans by farmers is cumbersome, laborious, time consuming and bribery ridden exercise. Farmers need to go from one department to another department to get land documents, evaluation and encumbrance certificates, revenue certificates etc., after paying heavy bribes. Farmers are being forced to take loans from private lenders w ho charge high interest rates.But Land Savings Account w ill make money borrow ing by farmers from banks so much easy, instant, smooth, timely and time saving exercise. By using Land Savings Accounts the branch managers can sanction farm loans instantly based on land records in the LCAs.

4. Interest rates on farm loans

In the suggested TOP Tax system the interest rates on farm loans, up to Rs.10, 000, 00, w ill be only 3% per annum and 4% per annum beyond Rs. 10,000,00.

5. Land acquisition and compensation

;- If an individual or company acquires land of more than 20 acres of land for industry, studios, real estate or any other purpose, land tax of 10,000 per acre per annum needs to be levied. If land is acquired for SEZs the farmers should be paid not only the market price of the land but also Rs 1,000 per acre per month for rest of his/ her life and thereaft er to his/ her legal heir. It is easier for local panchayats, municipalities, corporation to collect house tax, vacant plot/ land tax and properties tax as all the details of a person’s properties are recorded in his/ her Land Savings Account (LSA).land, plot, flat, house or other commercial establishments w ill be same and equal all over India irrespective of the place and market value of property. The registration charges w ould be only Rs. 1,000 per acre, Rs. 1,000 per 300 square yards of plot or Rs 1,000 per 1000 square feet of flat and multiples thereof. These registrations of land transfers can be made in any bank and anyw here in India. It is needless to say that the loss of stamp duties w ould be compensated by the “TOP Tax” w hich is compulsory on any money transfers. If a person buys a property (land, plot, flat, house, commercial establishment) for Rs. 10 lakhs, a TOP tax of Rs. 40,000 w ill be deducted from his M SA or SSA w hile transferring the cash to the sellers account. If he/ she buys the same property for Rs. 1 crore the deducted TOP tax w ill be Rs. 4 lakhs. In the case a person transfers a property as a gift to his/ her son/ daughter or any other person, trust or organisation the TOP tax deducted w ill be nil as there is no cash transfer made. That means there w ill be no need for separate registration and revenue departments for registrations and handling of all immovable properties.

The third sub account of M SA

Vehicles Account

)

shall be ut ilised for ow nership right s of all movable propert ies like vehicles, gold, jew ellery, and et cet era. The ow nership right s of t hese propert ies w ill be t ransferred from one person’s M SA (manufact urer, dealer, and seller) t o anot her person’s M SA w hile purchase/ sale/ donat ion of t hese movable propert ies. The ow nership records w ill cont ain t he vehicle’s model, manufact uring dat e, engine number, chassis number, regist rat ion number, fit ness cert ificat e et c. The ow nership right s of all vehicles w ill be t ransferred from one M SA belonging t o manufact urer/ import er/ dealer/ ret ailer, or ot her cit izen t o t he buyer’s account t hroughonline just like money transfers in the present system.In t he TOP Tax syst em people w ill not need t o have separat e vehicle regist rat ion cert ificat es, fit ness cert ificat es, and insurance cert ificat es for each vehicle he/ she ow ns. The bank st at ement of t he t hird folder of his/ her M SA, w hich cont ains t he ow ning record of all his/ her vehicles, w ill suffice for all his/ her vehicles. That means the bank statement of the sub account (M PA) of any person’s M ain Savings Account w ill hold the entire ow nership rights of that person’s all movable properties. Furt hermore t here w ill be no need t o have separat e RTO depart ment s for regist rat ion and checking of vehicles in t he TOP Tax syst em. The t raffic police depart ment w ill suffice t o oversee all vehicles in prompt ly paying t he road t axes and insurance premiums regularly. The dat a on payment of road t axes collect ed from banks w ill ensure t hat t he checking aut horit ies can st op only t he non t ax- paying vehicles leaving t he t ax paid vehicles unst opped on t he highw ays.

st olen or bought from illegal means. People, w ho bring gold f rom abroad on ret urn, should record it in t heir M ain Savings Account at t he airport it self. The exact gold reserve ow ned eit her by people or Government s w ill be know n at any t ime. Every year t he import ed and locally produced gold w ill be added t o t hese reserves.

The fourth sub account

Shares Account

shall be ut ilised for st orage and usage of ow nership right s of shares/ st ocks, bonds, derivat ives et c. The ow nership right s of t hese securit ies w ill be t ransferred from one person’s M SA t o anot her person’s M SA w hile buying/ selling/ donat ion. The ow nership right s of shares can be t ransferred from one account t o anot her account by t he bank w hich handles t he account . The shares account is port able and t he cust omer can t ransfer his account from one bank t o anot her bank at any t ime for handling t he shares.The fifth sub account (personal account) shall be ut ilised for family det ails and called as personal account . M arriage regist rat ion and child birt h regist rat ions w ill be made bot h in husband and w ife’s family folders of M SAs. Based on t he det ails in t he family folders, mont hly rat ions w ill be comput ed and t ransferred every mont h, in t he form of cash, direct ly int o t he w ife’s M SAs. Every child w ill get his/ her ow n M SA account at t he age of 15 years. The bank st at ement of The fifth account (personal account) of M SA of any individual can be utilised as income certificate, voter list, ration card driving license and passport. It can be obtained w ithin minutes from any bank and from anyw here in the country. People need not pay bribes to get these certificates or documents from revenue department and passport offices. All funds allocated tow ards w elfare of SCs, STs and BCs can be transferred directly into the M SAs of these sections leaving no room for leakages, bribes and misappropriation of these funds.

Vivid explanation:- All t he det ails of a person’s occupat ion, educat ional qualificat ions, marriage, driving license, passport , his/ her life part ners name, children and t heir age et c, w ill be recorded in fift h sub account (personal account) of his/ her M ain Savings account. The parent s should regist er t heir child’s det ails in t he dat a record of t heir M ain Savings Account (M SA) w it hin t hree mont hs of t heir child’s birt h. Once t he child get s t he age of 15 years he/ she w ill aut omat ically get M SA. The t ot al care and w elfare of t he orphans should be t aken by t he St at e government s t ill t he child reaches t he age of 20 years. The pat het ic plight of st reet children and orphans w ill come t o an end once t he TOP Tax syst em becomes operat ional.

This syst em t ot ally and permanent ly checks t he ever increasing problem of illegal migrat ion from Pakist an and Bangladesh changing t he demographic proport ion of India t o an unimaginable level. Once all t he cit izens above t he age of 15 years are given t he mandat ory M ain Savings account (M SA) and t he TOP Tax syst em becomes fully operat ional, no adult w ill be given M ain Savings Account (M SA) t hereaft er. From hereafter every addit ional M ain Savings Account [M SA] w ill be an offshoot of an exist ing M SA belonging t o parent s or Government in case of orphans. There w ill be no quest ion of addit ional fresh M SA w it hout parent ’s exist ing M SA. Similarly exist ing M SAs w ill come t o cease upon t he deat h of individuals. All t he money, shares, movable and immovable propert ies recorded in t he five folders of M SA of t he deceased person w ill be t ransferred t o his/ her legal heirs or t o nominees regist ered in his/ her M SA account . The t ot al number of M SAs w ill increase every year depending upon t he grow t h rat e of populat ion of t hat count ry. TOP Tax syst em w ill record; maint ain every individual’s family record generat ion aft er generat ion. Therefore illegal migrant s from ot her count ries cannot ent er illegally int o India, get M ain Savings Account or Sub Savings Account s and assimilat e in Indian populat ion. It w ill be a lot easier for t he government t o det ect t errorist s and milit ant s w ho cross over from across t he border t o indulge in unlaw ful act ivit ies.

commission. According t o t he addresses recorded in t he M ain Savings Account t he area w ise vot er list s can be supplied by banks t o conduct polls t o panchayat s, cit ies, dist rict s, M LA, M P and all ot her polls. If by polls are t o be held, t he last vot er list s should be used in t hat part icular const it uency in order t o st op people from ot her areas t o change t heir addresses t o t hat by poll areas.

TOP tax system w ill be operated solely by banks to provide different services for the Government like taxation, tax collection, tax enforcement; for issuing caste certificates, income certificates, voter lists, monthly rations, subsidies, pensions, calamity relief funds, passports, licences, fees reimbursements, scholarships etc., at absolutely free of cost. TOP Tax system, operated by banks, w ill also help people in getting all the above mentioned services at single w indow through their M SAs w ith five different sub accounts. That means TOP Tax system w ill replace present system’s multiple departments like Income tax department, Central Excise department, CBDT, CBEC, Tax tribunals, passport department, census department, States’ commercial tax departments, civil supplies departments, registration departments, revenue departments etc., saving thousands of crores of Government’s non-plan expenditure.

2. Usage of Sub Savings Account (SSA)

:-

Every person can open and operat e as much number of SSAs as he/ she w ishes. The SSA is only a money account as in t he present syst em. This Sub Savings Account shall be used for receiving, st orage and usage of money t o operat e anybusiness or indust ry w holly ow ned by an individual.

3. Usage of Corporate Account Number (CAN)

: -

Corporat e companies, M NCs and Public limit ed companies w hich sold/ issued shares to the publicw ill be given CANs. Each Corporat e Account Number w ill have seven sub accounts for each specific operat ing/ running purpose of t he company.

The first sub account shall be ut ilised for receiving, st orage and usage of money for running of t hat company.

The second sub account [LSA/ land savings account] shall be ut ilised for having all records of immovable propert ies like land, buildings, infrast ruct ure and et cet era of t hat project / plant / business.

The third sub account [Immovable Property Account/ M PA] shall be used for regist rat ion, st orage and usage of ow nership right s for all f leet of vehicles and ot her movable propert ies like machinery et cet era required for running of t hat company.

The fourth Sub account [Shares Account ] shall be used for st orage of all shares of t he promot ers and t he public of t hat company.

The fifth sub account w ill cont ain t he det ails and account s of all t he employed manpow er of t hat company.

The sixth sub account [ Raw materials account/ RM A] w ill cont ain t he det ailed account s of all raw mat erials and ot her required input s bought and used for running of t hat company.

The seventh sub account [Products Account/ PA] w ill cont ain t he det ails and account s of all product s manufact ured, sales and invent ory. TOP Tax syst em’s CAN w it h seven sub account s is a new procedure t o see t hat company’s financial books w ere clean, accurat e, open and t ransparent t o all share holders so t hat t here can be no room for fraudulent and decept ive financial st at ement s.

M oney w ill flow into the first sub account of Corporate Account Number (CAN) w hen products are sold and money w ill go out w hen payments are made tow ards salaries, purchase of raw materials, services, equipment etc,. The seventh sub account, w hich records the manufactured products, gets updated online at every stage of production and marketing just like money savings account. The depletion of stock in the seventh account (products account) means the increase of money in the money account (first sub account) on the selling of products. Similarly the decrease of raw materials in the sixth sub account means an increase of finished products in the seventh sub account. The increase of raw materials in the sixth sub account points to depletion of money in the money account (first sub account) on purchase of raw materials. All these seven accounts get updated online at every stage of construction, production and marketing show ing the exact details of debits and credits relating to money, raw materials, finished products, borrow ings, shares, etc., for the benefit of all investors w ho put their hard earned money into these companies. The total money, the value of raw materials, finished products, machinery, movable and immovable properties recorded in the seven sub accounts of any Corporate Account Number (CAN) minus the borrow ings is equal to the total strength of that company.

The TOP Tax syst em’s t ransparent account ing syst em in Corporat e Account Number (CAN) w it h seven sub account s for money, m ovable propert ies, immovable propert ies, manpow er, shares, raw mat erials and ot her input s, and manufact ured product s and invent ory w ill remove all frauds in account ing, securit ies, st ocks and invest ment . These CANs w it h seven sub account s ensure t hat t here w ill be no chance of fraudulent business pract ices of overst at ing profit s, concealing debt s, spreading t he expenses out over several years, under voicing or over voicing of raw mat erials, input s, and manufact ured product s, under or over st at ing of st ocks, padding up of project cost and divert ing of funds at grounding, const ruct ion, erect ion and all st ages of project implement at ion and publicat ion of falsified financial report s. The CANs of TOP Tax syst em can also check t he diversion of funds from one company t o anot her company w it hin t he group companies (same promot ers). The TOP t ax syst em gives a big boost t o st ock market s as people st art buying huge lot s of shares t o maint ain minimum balance in t heir account s in order t o avoid Profit tax. There w ill be no significant effect of TOP t ax syst em on int raday t rading and Fut ure opt ions t rading because t he looser looses ext ra 4% of t he loss amount only in t he int raday t rading. People w ill prefer t o buy shares on t he long t erm and annual yield basis. They invest in t he companies w hich give handsome dividends year aft er year.

Thus a country’s exact w orth of all its money, movable and immovable properties, shares, gold, ores and minerals w ill be know n exactly at any given point of time.

mineral w ill be made online from t he mining company’s CAN (sixt h sub account ) t o t he buyer’s CAN. At t he same t ime money w ill be t ransferred from buying company’s CAN t o mining company’s CAN. Aft er t he deplet ion of t he recorded bought st ocks in t he CAN, t he mining company w ill have t o buy fresh st ocks from t he Government s and replenish it s sixt h folder. That means t he buying and selling of nat ural resources w ill be made bot h in physical form and demat erialised form. TOP Tax syst em makes it impossible for any mining company t o illegally mine huge quant it ies of ore or minerals w it hout paying correct price. TOP Tax syst em makes it possible t o know t he exact quant it y of ores or minerals mined, export ed or used by domest ic companies.

TOP Tax system’s five main objectives are 1)The tax collections from people, 2) the distribution of revenues from governments to people in the form of subsidies, relief funds in the event of natural calamities like earth quakes, floods, famines, pensions, cash transfers tow ards monthly rations, hospital bills, education bills, et., 3) providing all basic services including registrations of movable and immovable properties, driving licences, air, bus, train tickets, permits, licences, payment of electricity, telephone bills, w ater cess, house taxes, issue of voter lists and voter slips, birth and death registrations, census figures at every day, every hour, every minute (unlike at every decade in the present system), 4) lending money to borrow ers at the low est PLR (average 3%per annum). All these objectives can be met and carried through banks/ service centres to all people at single w indow , situated nearest to their homes (5) implementation of w elfare schemes to BCs, SCs, STs, tow ards education, self employment and other areas, and monthly pensions to senior citizens (w ith no or paltry incomes) and physically challenged.

All t he earnings/ savings of an individual deposit ed in t heir respect ive account s (M SA/ SSA) in t he form of numerical/ digit al value can be ut ilised at any t ime for buying of movable or immovable propert y or for any ot her legally allow ed purpose. The unut ilised deposit s w ill be disbursed as loans t o t he borrow ers by t he banks at t he low est lending rat e (average 3% per annum as operat ing cost ). The t ot al profit s (an est imat ed 64,973crores) got by all t he banks/ service cent res w ill be more t han enough t o operat e t hem and t hey can meet all t he object ives of TOP Tax syst em i.e. providing all basic services t o people at absolut ely free of cost at single w indow .

.

3.

M oney Supply

(real money and loan money).

TOP Tax system suggests that total money supply (real money and debt money/ loan money) to be necessary for circulation in banks should be at the minimum level of 100% and at maximum level 110% of the value of GDP of the country. Out of this total money supply in the economic system, 99.4% of the money w ill be in dematerialised (non physical) form in the accounts of citizens, Governments and com panies. Only small portion of money, equalling just 0.6% of the total money in the economic system, w ill be in physical form i.e. currency notes Rs 30 Rs, 20, Rs. 10 and coins Rs 5, Rs 2 and Rs 1. All high valued paper currency notes Rs 1000, Rs, 500 Rs. 100 and Rs. 50 w ill be demonetised.

![Table – 1 Figures in rupees [example]](https://thumb-us.123doks.com/thumbv2/123dok_us/7754068.710676/31.612.70.527.489.628/table-figures-in-rupees-example.webp)