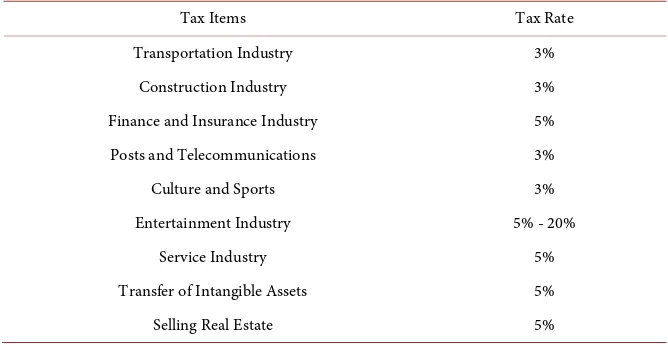

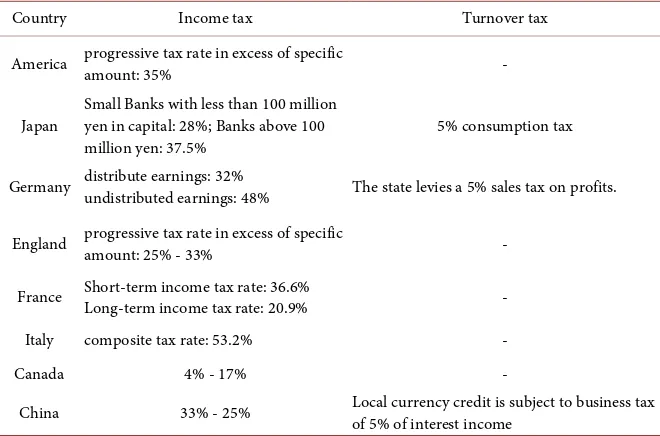

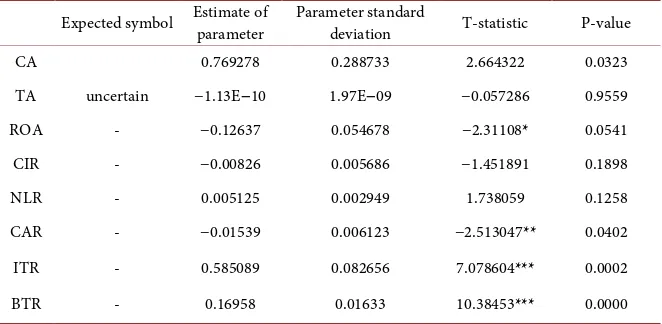

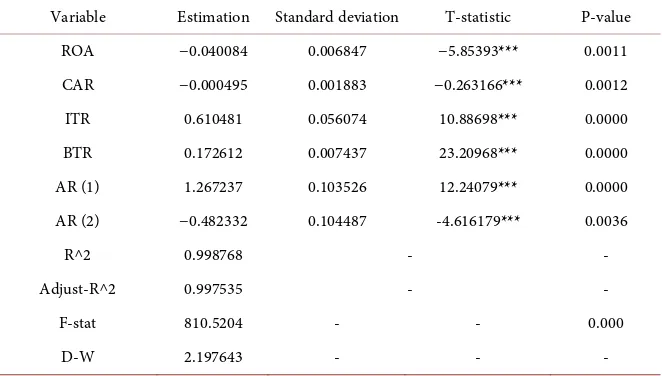

An Empirical Analysis of the Factors Affecting the Tax Burden of China’s Banking Industry

Full text

Figure

Related documents

considered to be a viable option for collecting the inventory information on guardrail and message boards since both assets are viewable from the travel lanes. The users identified

Currently, National Instruments leads the 5G Test & Measurement market, being “responsible for making the hardware and software for testing and measuring … 5G, … carrier

Carnegie Mellon University, Accounting Mini Conference, 2011, 2002 University of Missouri, Corporate Governance Conference, 2011 University of Fribourg, Accounting Research

The safety and efficacy of on-site paramedic and allied health treatment interventions targeting the reduction of emergency department visits by long-term care patients:

In this study, we aim to investigate the presence of fractal behaviour in the daily mean hourly ozone concentration time series observed at six air monitoring stations in

In Common Drain mode, if you short P3 and measure across an arbitrary DC and AC value for P2 with an given input signal and supply voltage, you can compare the AC variation of

This section examines the relation between firm- and loan-specific information asymmetry variables and the bid-ask spread. It then explores the impact of reporting

9000 YOU'VE GOT ANOTHER THING COMING JUDAS PRIEST 8699 YOU'VE GOT YOUR TROUBLES THE FORTUNES. 8700 YOU'VE LOST THAT LOVIN' FEELING THE