Cisco Internet Business Solutions Group (IBSG)

SMB Public Cloud Adoption

$51 Billion of Enterprise Disruption

By Douglas P. Handler, Joel Barbier, and Paul Schottmiller,

Cisco

®Internet Business Solutions Group (IBSG)

Introduction

The cloud services U.S. market size is estimated to grow to $16 billion by 2015 for micro-SMBs—the “very small business” segment comprising firms with fewer than five employees, but also a vast “non-employer” segment. This market opportunity for cloud adoption is very large precisely because cloud services address more than just current IT hardware,

software, and services spending. Cloud services can help automate non-IT functions, and therefore could be attractive to a wide customer base of companies eager to spend from non-IT budgets, or even to make greenfield expenditures where time or labor costs—often uncompensated—could be saved.

An earlier paper from the Cisco® Internet Business Solutions Group (IBSG), “SMB Public

Cloud Adoption: The Opening of a Hidden Market,” identified a large cloud services market opportunity with micro-SMBs. This follow-up paper sizes the overall market for U.S. SMB cloud services. It considers firms with 100 or fewer employees, including micro-SMBs and non-employer firms. We estimate the SMB cloud services market opportunity at $51 billion by 2015.

2 Ways To Segment the Opportunity:

SMB Employment Size and Service Types

Two principal segmentations of the SMB cloud services market exist. The first involves an employee size split and occurs at around 50 employees. SMBs with fewer than 50 employ-ees generally have no dedicated IT professional on staff, whereas larger SMBs often have at least one “IT guy.” For these smaller SMBs, IT assets most often include PCs, broadband connectivity, an email distribution list, and perhaps a central server—owned or outsourced. Firms with fewer than 50 employees spend more on website hosting services than any other service. The absence of an IT professional on staff most often connotes the absence of an IT infrastructure. Most new services, therefore, will very likely be hostable on a public cloud. For firms with more than 50 employees, dedicated IT professionals provide many of the needed IT services, although the presence of a dedicated IT employee usually bolsters rather than precludes the purchase of a public cloud service.

A “sweet spot” for cloud spending occurs in the 20- to 49-employee range, where the number of firms is large and services spending per firm is also significant (see Figure 1).

Figure 1. Among Firms with Employees, the Cloud Spending “Sweet Spot” Can Be Found in the 20- to

49-Employee Size Category.

The second segmentation involves the type of cloud services being purchased: either one service unit per firm (often a software as a service, or SaaS, contract), or one service unit (or seat) per employee or per a certain amount of revenue (email, storage, or network services).

Cloud Research Findings Help Size Cloud Adoption over Next 5 Years

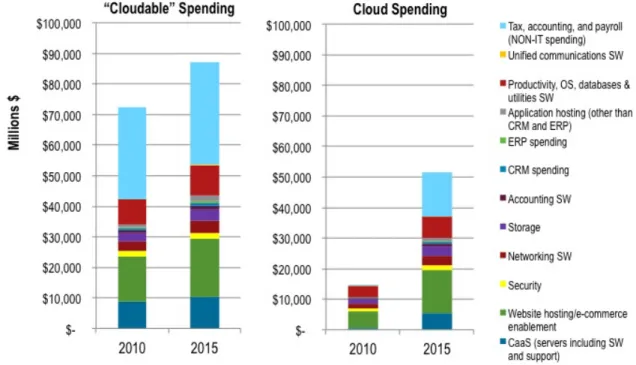

To identify the cloud opportunity for SMBs (other than non-employer firms), spending data from AMI Partners was multiplied by a cloud services penetration rate obtained from Cisco IBSG’s primary research for all the IT hardware, software, and services that were deemed “cloudable” (the “cloudable” list can be seen in the legend of Figure 2). Two other compo-nents were added to this total: (1) spending for the non-employer firms, and (2) non-IT spending on tax, accounting, and payroll services (as described in the previous paper). The in-scope spending (total addressable market, or TAM) is shown on the left side of Figure 21; cloud services spending emanating from the TAM is shown on the right-hand

side of Figure 2.

1 While some of the employee-size and cloud-spending categories were not quite consistent between the two sources, it was possible to make intelligent estimates of the penetration rates.

Figure 2. The Total Addressable Market for Cloud Spending (left) and the Portion that Will Drive Cloud Spending (right).

In 2010, about 20 percent of all SMB cloudable spending used public clouds. This is expected to rise to 59 percent by 2015. By the end of the decade, this penetration will be nearly 100 percent as the cost and capabilities benefits of cloud-based applications and services outweigh the advantages SMBs can garner through maintaining a dedicated, customized data center.

The Importance of Non-IT Cloudable Expenses

To reiterate, one of the principal drivers of this growth is the migration of non-IT spending in the tax, accounting, and payroll areas of cloud services. This spending category is large because of its ubiquity—every company needs to supply these services either internally or externally. However, there are other potential areas of spending migration that are just as ubiquitous, but are not included in Figure 2 because of their difficulty to measure.

For example, firms with less than $250 million of annual revenue (mapping into an employee size of 500-1,0002) spend between $500 and $3,000 per employee annually on human

resources (HR) processes.3 This includes the hiring, retention, recruiting, and counseling of

employees, as well as the administration of their compensation, but does not include the cost of salaries or benefits. Many of these processes are increasingly provided through cloud-based services. For example, SMBs can maintain employee data on the cloud, streamline the employee hiring and evaluation processes, and give employees control of

2 Based on U.S. Census Bureau data, 2010.

3 APQC benchmarking data, 2011.

their personal data and benefits selection. If the cloud services cost less than this spending benchmark and the quality of service is maintained, business migration to clouds in the HR area should at least match, if not exceed, the migration rates for other cloudable services. As 42 million U.S. workers are employed by firms with fewer than 100 employees (non-employ-er firms are excluded),4 at $500 per employee, a possible market of up to $21 billion exists.

In much the same manner that HR can be put on the cloud, CRM, supply chain, and many other SG&A processes are certainly cloudable, with medium and large enterprises already doing this.

Conclusion

An executive at a large incumbent software leader recently told an interviewer that “due to a ‘generational’ mentality in enterprises, it could be decades before enterprises shake off their security concerns and adopt [public] cloud computing beyond testing and development. . . .”5

Moreover, during several engagements, Cisco IBSG has learned that enterprise customers may not have a sufficient handle on their data center costs or their potential companywide data-center-driven benefits. It is probable that these enterprise adoption barriers have been cemented by decades of dealing with early versions of applications that overpromised capabilities and cost savings.

SMBs, unhindered by both this generational legacy and lack of existing IT infrastructure, can adopt technologies that will enable them to disrupt their market. The greatest benefit of any SMB cloud service is its riskless nature; if it doesn’t work, there is minimal additional expense from any sunk costs.

The two major sources of private cloud demand (see Figure 2) will be (1) tax, accounting, and payroll applications, and (2) website hosting and e-commerce enablement. The first source will involve primarily cost cutting and internal process improvements, and will be relevant across all vertical industries. This latter source has the greatest potential to disrupt the retail and distribution sectors. But it is naïve to think that these two industry areas will be the only ones that are affected. Cloud services can consolidate price and quality information; improve the ability to buy “on-demand” key inputs of production and to better manage inventories; and accelerate the product development process through better collaboration tools and greater dissemination of new ideas and collaboration tools.

As long as large enterprises maintain their innate aversion to adopting cloud services, preferring large investments to innovate, reshape markets, and educate customers, SMBs can be disruptors capable of competing effectively using these cloud-based best-of-breed services.

4 U.S. Census of Businesses, 2010.

5