Supply Chain Resilience 2012. Copyright © 2012 The Business Con nuity Ins tute. All Rights Reserved. 1

Supply

Chain

Resilience

2012

4th Annual Survey

Published November 2012

Supported by:

Supported by: An international survey of more than 530 organisations from Supported by:

over 65 countries, which considers the origin, causes and

consequences of supply chain disruption, along with proven

Contents

03

Execu ve

summary

04

Introduc on

05

Experience

of

disrup on

09

Supply

chain

con nuity

14

Business

con nuity

in

tendering

and

contrac ng

19

Review

and

conclusions

21

About

the

survey

22

About

the

BCI,

CIPS,

Zurich

&

DHL

Supply

Chain

26

Annex

1:

Wri en

comments

by

survey

respondents

15

Geographical

and

sector

perspec ves

18

Lesson

learned

and

key

challenges

32

Annex

2:

Full

sector

and

geographical

data

Introduc on

This survey is the fourth in a series, star ng

back in 2009, that sets out to consider the

challenge of developing resilient supply

chains.

Key

Findings

73% of survey respondents experienced at

least one disrup on with an average of

five. This high level is consistent with the

trend‐line over the past four years

39% of analysed disrup ons originated

below the immediate er one supplier,

underscoring for the second consecu ve

year the deep‐rooted nature of disrup on

Unplanned IT or telecom outages jumped

to the top of sources of disrup on with

52% affected to some or a high degree.

The level was 41% in 2011

Adverse weather maintained its prominent

posi on with 48% ci ng it as a cause of

disrup on, but rela vely unchanged from

51% in 2011

Failure of service provision by outsourcing

suppliers has doubled from 17% to 35% of

disrup on and joins the top three causes

21% suffered more than €1M in costs for a

single incident; higher than 2011 and in

spite of lower overall levels of disrup on

59% cited loss of produc vity as the

primary impact of the disrup on

experienced, up from 49% in 2011. Across

all indicators there was a deepening on

impact experienced with an average of

three dis nc ve consequences per incident

25% of respondents have s ll to consider

supply chain disrup on in their business

con nuity programmes, and 44% of

respondents have weak supply chains,

while major sector differences persist

especially in manufacturing and retail and

between countries such as the UK and USA

While 47% now look for evidence of a

business con nuity programme over a

simple plan and 23% run joint exercises—

all improvements on 2011—15% s ll do

not collect any informa on from key

suppliers, and 41% do not validate that key

supplier plans might work in prac ce

42% stated the biggest on‐going challenge

is to secure buy‐in to implement supply

chain con nuity prac ces in their firm

Review

&

Conclusions

Since 2009 consistently high levels of supply

chain disrup ons have been experienced and

events are becoming more consequen al

even with absolute levels dipping a er 2011,

a year, which saw the Great East Japan

Earthquake and extensive flooding in

Thailand.

Business con nuity is widely seen as effec ve

in resis ng the impact of disrup on, alongside

its core benefits of enabling con nuity and

faster recovery from incidents.

The drama c rise in disrup on through

outsourcer service failures requires further

study into service chains and the specific

challenges inherent in them.

Given the dominance of supply chain

disrup on through unplanned IT or telecom

outages, there is now a need to evaluate the

contribu on of “the cloud” to resilience.

The challenge of securing execu ve buy‐in

requires an understanding of the broader

trends driving supply chain vulnerability and

its disrup on. In this way it will become

possible to demonstrate that high levels of

disrup on are not going to go away, however

fragile corporate memory may be.

Introduc on:

73%

experienced

at

least

one

disrup ve

supply

chain

incident

with

an

average

of

fi

ve

This report is the fourth in a series that,

star ng in 2009, set out to consider the

challenge of developing resilient supply chains.

While we have con nued to track trends in

supply chain disrup on, mi ga on and

assurance methods employed, the 2012 survey

is re‐focused on events that cause at least

some if not high levels of disrup on, rather

than disrup on in general, much of which can

be dealt with as part of business as usual.

When reviewing the results it is naturally

important to consider the profile of the

respondents: In this case 82% of respondents

work “in‐house” i.e. they are employed to run

business con nuity, supply chain or risk

programmes with 18% providing consul ng

services in these domains. The organisa ons

responding are typically large ones—42%

employ between one thousand and fi y

thousand staff and 12% employ more than fi y

thousand people.

The 2012 survey has also achieved a stronger

balance of views from across risk, business

con nuity and supply chain professionals.

Finally, we asked respondents to ar culate the

tough challenges where they are s ll to find an

answer, insights which inform the Business

Con nuity Ins tute’s thinking on next steps.

So, what do we mean by supply chain? Here is

a reprise of the defini on that we first used in

2011 (Christopher 2005):

The network of organisa ons that are involved,

through upstream and downstream rela

on-ships, in the different processes and ac vi es

that produce value in the form of products and

services in the hands of the ul mate consumer.

The headline figure for disrup on in the 2012

survey is that 73% of responding organisa ons

experienced at least one disrup on in the

previous 12 months, with an average level of

five incidents. In 2011, supply chains were

widely disrupted by the Great East Japan

Earthquake and flooding in Thailand causing a

jump to 85% in the deadline disrup on figure

and peaking above the established trend‐line,

to which we have now returned.

It is also worth no ng that only one in four

firms have the full picture on supply chain

disrup on, which would be achieved by record‐

ing, measuring and repor ng on performance‐

affec ng supply chain disrup ons across the

whole enterprise. For 75% of respondents, this

is therefore not the case, so the level of

disrup on recorded here is likely to be an

underes mate of actual levels, albeit major

disrup ons are likely to be picked up across

company boundaries.

We hope this year’s survey provides some new

insights and would welcome your feedback.

Chart 1: How many supply chain incidents would you es mate your organisa on experienced in the past 12 months that caused disrup on to your organisa on?

Origin of disrup on

Following on from providing informa on on

the number of disrup ve incidents

experienced in the last 12 months, those who

had experienced disrup on were asked

whether they had analysed the original source

of the disrup on within their supply chain. The

ques on specifically asked whether the disrup‐

on occurred with the immediate supplier ( er

one) or their supplier ( er two), or much lower

down in the supply chain ( er three or four

etc). 87% of respondents to this ques on were

able to provide an analysis of the source of dis‐

rup on as seen in Chart 2.

61% of disrup on originated with the

immediate supplier according to this year’s

survey meaning that 39% originated in the

extended supply chain ( er two, three, etc).

This level of disrup on is consistent with levels

reported in 2011, and confirms the deep‐

rooted nature of disrup on. The

comments suggest that buying

organisa ons take it upon them‐

selves to scru nise their extended

supply chain rather than rely on

their immediate supplier to audit

their suppliers in turn, which would

be an alterna ve method of

addressing a difficult challenge.

“We reach to the original source of

the supply chain to minimize

contamina on to produce high

purity products. When suppliers of

original source are hired, we have

excep onal confidence they are not

contamina ng”

“While we don’t rou nely analyse

the full supply chain, I was able to review three

of the disrup ons that I was made aware of

and found one to be an immediate supplier

failure and two to be er two”

Causes of disrup on

When considering causes of disrup on in the

2012 survey, we refined the main ques on to

dis nguish between disrup on that caused

some impact from disrup on that had high

impact in order to qualify the severity of the

disrup on. The results in Chart 3 show the

totals of each threat type experienced over the

previous 12 months.

Overall some 1,200 causes of disrup on were

reported with 301 of them designated as high

impact. The top five causes by high impact

represent 42% of severe events.

Unplanned IT or telecom outages are the most

commonly experienced source of some or high

levels of disrup on with 52% of responding

organisa ons selec ng this op on. Adverse

weather drops from first place in the 2011

survey to second place in 2012 at 48%.

Failure in service provision by an outsourcer

reaches the top three with 35% sta ng they

experienced some impact or high impact from

Experience

of

Disrup on

such an event. This is a significant increase

from the 17% level recorded in 2011.

In 2011, we wrote that intellectual property

viola ons was one to watch and this has

proved to be the case in jumping to 16th place

above cyber a ack, industrial dispute

and act of terrorism with 11% and 26

responses compared with 25th place

in 2011 with just five responses.

Other significant climbers included

energy scarcity in sixth place (14th in

2011) and new laws/regula ons in

seventh place (17th in 2011).

Cyber threats tend to score highly in

horizon scanning and the media, so it

is interes ng to note the low levels of

disrup on actually experienced: only

16% of respondents recorded severe

or some supply chain disrup on as a

result of a cyber threat, ranking it 18th

on the list of threats experienced by

severity out of 25, and 14th by

number of incidents registered. What

is notable is the concentra on of this

disrup on in the financial services

sector, which claimed 41% of incidents

recorded. The finding suggests that this threat

has a strong sector bias rather than one for all ‐

data from 2009, 2010, and 2011 support this

conclusion as well.

The prominence of earthquake/tsunami in the

list underscores the extended recovery mes

faced by some organisa ons following the

2011 disaster.

Loss of talent/skills has slipped in 2012 from

sixth posi on down to tenth. The London 2012

Chart 3: How severely has your supply chain been aff

ect-ed by any of the following sources of disrup on over the past 12 months? Severity levels can be considered in terms of ini al impact, ability to con nue to deliver key products and services and recovery me, as well as the consequences on brand and reputa on. Base: 227

Olympics registered as a source of disrup on at

the UK level but not in the overall interna onal

survey.

Consequences of disrup on

When comparing 2012 with 2011 data on the

consequences arising from disrup ons, the first

observa on is an increased level of responses

across all 14 poten al areas of impact. As can

be seen from Chart 4, loss of produc vity is s ll

the primary consequence, with 59% checking

this in 2012 compared with 49% in 2011.

Increased cost of working, loss of revenues,

customer complaints all increased over 2011

levels. Product release delay jumped from 17%

in 2011 to 26% in 2012. Further down the list,

the jump in payment of service credits (from

1% to 9%) mirrors the prominence of

outsourcer failures among the top three

sources of disrup on. Incidents forcing a

product recall or withdrawal also increased

from just 5% in 2011 to 11% in 2012. As

iden fied in 2011, longer term impacts are be‐

ing experienced more frequently with damage

to brand reputa on increasing from 17% to

24% in this year’s survey.

Overall the survey recorded 741 impacts from

215 respondents. Of the 195 survey

respondents who experienced ‘1‐5’ disrup ve

events, 18 stated they endured six or more

consequences (9%), i.e. evidence that there is

more than one consequence from a single

event. Events which lend themselves to this

cascading effect are unplanned telecom/IT

outages, outsourcer failure, loss of talent/skills

and currency vola lity.

Economic consequences

One in five responding organisa ons had

suffered a single loss event of more than €1M

in the past 12 months up from 2011, when 17%

registered a similar magnitude of loss. This

increase is noteworthy given the overall lower

level of disrup on experienced in this year’s

survey, sugges ng an increase in the

Chart 4: Which of the following impacts or consequences arose from the incidents/ disrup ons experienced in the last 12 months? Base 215.

consequen al nature of supply chain

disrup on.

The aggregate annual figure could clearly be

higher given that the average level of incidents

experienced was five.

It is worth comparing the single loss event

against the annual revenues of organisa ons to

understand the significance of the event.

Considering the 29 cases where this

comparison can be made the average (mean)

minimum loss is €8M but there is significant

varia on. For example, three firms experienced

a single event loss between €1M and €10M on

annual revenues of €1M to €10M indica ng a

significant bo om line hit. While another

suffered a loss of between €51M and €100M

on annual revenues greater

than €50BN. The economic

consequences will therefore

be subject to further study.

One ques on that arises is

around the profile of those

organisa ons suffering a

single event loss of more

than €1M. Are these firms

simply laggards in terms of

business con nuity?

The answer is, in fact, quite

the opposite.

Firstly, the affected organi‐

sa ons were much larger

ones than the survey

average with 58%

employing more than

10,000 employees and 49% had revenues in

excess of €1BN (compared with 23% and 22%

respec vely in the overall sample). Larger

organisa ons tend to have business con nuity

programmes, even if they are not labelled as

such.

These organisa ons do have more key

suppliers than the average with 43% recording

more than 100 key suppliers compared with

the survey average of 23%, indica ng increased

complexity and higher need for assurance

resources.

What is also clear is that those affected had

stronger business con nuity programmes with

63% having BC in place for supply chain

disrup on, and a more rigorous approach was

taken across all assurance methods (more on

the criteria will follow in the following sec on

of the report).

Most noteworthy is that in spite of the

economic hit over the past 12 months, this

group is convinced that business con nuity has

helped them resist the impact of disrup on

(63%) and helped with con nuity and recovery

(96%).

Chart 5: Considering the single most significant incident in the last 12 months what was the approximate

financial cost (loss of revenue and/ or increased cost of working)? Please give your response in EUROs. Base:182

Does your business con nuity programme

consider supply chain disrup on?

When asked whether the responding

organisa on had business con nuity (BC)

arrangements in place to deal with supply

chain disrup on only 58% stated that this was

the case with 25% sta ng they definitely did

not and a further 17% not knowing.

For those with BC in place for their supply

chain (237) a series of follow up ques ons

were asked. The first was to consider three

business con nuity benefit statements and

rate their strength of agreement with each

one based on a scale from strongly agree

through to strongly disagree (refer to Chart 6)

The conclusion is that BC is an essen al

component of supply chain resilience, as more

than 90% agree it delivers the capability of

faster recovery and the capability to con nue

to deliver key products and services. There is

less agreement about BC allowing survey

respondents to resist any impact of

disrup on, but even so, s ll more than 60%

agree with the statement.

As the supplier base for larger organisa ons

can number hundreds if not thousands of

companies, the next logical step is to seek to

understand supplier BC arrangements. This

can be a daun ng task, even assuming

resources are available to do so. The BCI

Partnership has published separate guidance

on how to perform the task of iden fying key

supply chain partners from among the wider

supply base in a separate paper available to

download from the BCI website. In the case

of this survey, 77% of responding

organisa ons had less than 100 key suppliers,

a level which is felt to be a manageable one.

The survey found that 77% of survey

respondents who have BC themselves took

the step of asking their key suppliers whether

they had business con nuity arrangements in

place for their own needs. 16% did not ask

this ques on.

The response to this ques on provides an

insight into the state of supply chain resilience

across a wide range of sectors (and beyond

Supply

Chain

Con nuity—

25%

of

in

‐

house

BC

programmes

do not

consider

supply

chain

disrup on

Chart 6: If you have BCM arrangements in place for your supply chain, how strongly would you agree with the following statements? Base: 237 (only those with BCM could respond to this ques on).

the BCI’s membership). This can be viewed in

Chart 7 below.

In 2012 we can see that 55% of survey

respondents have key supply chains where at

least half of the companies that comprise these

supply chains do have business con nuity in

place for their own needs. However, 44%

have much weaker supply chains, where less

than half have BC arrangements in place. In

the sector and country analysis that follows

later in this report, the strength of supply

chains is one of the key indicators for

comparison. Nevertheless, we can report that

their has been a modest strengthening of

supply chains compared with 2011.

Another new dimension in the 2012 survey was

to consider not just upstream supply chain but

also the presence of BC arrangements

downstream among channels, distributors,

franchisees etc. Here 17% ensured that all

have BC in place, while 50% focus on the key

channel partners. 19% do not take this step,

leaving a major vulnerability in the end‐to‐end

business con nuity picture.

Building confidence

In order to understand what the presence of

BC arrangements among the key supplier base

may mean in prac ce, the survey looked at the

informa on requested from key supply chain

partners, how this informa on was collected

and subsequently validated and reviewed.

These steps are clearly essen al in developing

a sense of confidence in the resilience of

supply chains. Naturally the picture that is then

developed may require one or more subse‐

quent ac ons. Within the survey, we asked

about the measures taken to deal with any

uncertainty generated from feedback from key

supply chains.

Informa on sought by survey respondents

As set out in Chart 8 (overleaf) the most

popular ques ons to ask relate to the existence

Chart 7: Considering your key suppliers, what percentage of them would you say have business con nuity arrangements in place to address their own needs?

of a business con nuity programme (47%),

whether its scope is appropriate (44%) and rel‐

evant to the product or service being pur‐

chased (44%). This may seem obvious but in

earlier surveys the focus was on the business

con nuity plan rather than the overall

programme. In 2011 only 28% of respondents

were looking for the BC programme.

Standards and codes of prac ce play an

important role in assessing the resilience of key

suppliers with 37% and 36% respec vely

looking for alignment or compliance.

Cer fica on lags behind on 28%.

One area with a significant increase from 2011,

is asking where responsibility for BC is held in

the organisa on and the involvement of senior

management. This clearly provides evidence of

the level of commitment behind the BC

programme. In 2011 the figure was just 23%

but has jumped to 36% in this year’s survey.

The least likely ques on to ask is around the

creden als of those who run the BC

programme, such as statutory membership of

the BCI, which would seem to be a cri cal one

given the programme can only be as effec ve

as the people assigned to deliver it. Only 18%

asked this ques on, albeit this level has

doubled from 2011.

How is the informa on collected?

51% of survey respondents required copies of

supplier documenta on, up frac onally from

48% in 2011. The self‐assessment ques on‐

naire retains its popularity in second place with

45% of respondents selec ng this op on, while

there has been a rise from 37% to 42% of those

who will retrieve informa on through audit.

Reques ng an independent audit is s ll the

least popular op on among those who collect

informa on at 9%, down from 12% in 2011.

15% s ll do not collect any informa on,

implying it is good enough for the supplier to

just state they have business con nuity in

place.

“We do not ask to see their BCP but rather we

ask that they state whether they have a BCP

and will only award the contract to those who

have a BCP for key contracts”

There were a significant number of comments

to illustrate approaches taken, which are listed

in Annex 1, but four are quoted here to reflect

the range of approaches undertaken:

“Ini al ques onnaire followed up with further

ques ons, mee ngs and site visits as

appropriate to nature of the service being

supplied”

“We would ask them to set out their BCM plans

in response to par cular scenarios”

Chart 8: What informa on do you seek in order to be er understand the business con nuity management (BCM) arrangements of key suppliers? Base 200.

“We personally visit each key supplier each

year and if they have presented any significant

problems then have moved to audit them”

“Ac vi es may be performed by various

disciplines , for example, internal audit,

depart-ment-level vendor managers and procurement”

Valida ng that plans may work in prac ce

The crucial step of valida ng whether plans

and inten ons might be effec ve in prac ce is

s ll one that 41% do not take. The good news

is that this level has fallen from the 49% figure

registered in 2011.

A number of op ons were offered to respond‐

ents and naturally most would use a variety of

techniques depending on the assigned

cri cality of the supply chain partner. The

most popular selec on was to request

documented outcome reports and ac ons

plans following recent exercises conducted by

the supplier. 40% chose this op on, up from

34% in 2011. Another angle on the same

technique is to approve the scope of tests in

advance and sign‐off all post‐test reports, this

was used by 11% of respondents. Holding a

workshop with a key supplier or running a desk

‐top exercise were techniques used by 16% of

respondents, unchanged from 2011. One area

that has grown in popularity is the running of

joint exercises based around likely scenarios,

which was selected by 23% of respondents

compared with just 17% in 2011.

One respondent summarises the challenge and

benefit of valida ng supplier planning:

“The extent we get involved does depend on

risk, coopera on and rela onships. Most key

suppliers are open to close engagement and

see the opportunity of shared learning and

improved longer term rela onships and

resilience”

Reviewing requirements

One of the biggest changes in the 2012 survey

comes in the sec on on reviewing require‐

ments. Given the frequency of change within

organisa ons, it seems highly likely that

priori es, scope and resources around business

con nuity programmes may change more

frequently than key supplier contracts.

Likewise new threats or opportuni es may

arise that need to be considered within an

organisa on and through its supply chain.

In the 2012 survey, 44% of respondents s ll

wait un l contract renewal before reviewing

their business con nuity requirements with

key suppliers and their ability to meet them.

This has increased from 37% in 2011.

Having said this, only 8% never review,

significantly down from 18% in the 2011

survey. Likewise ad hoc mee ngs have dipped

from 24% in 2011 to 21% in 2012. Scheduled

review mee ngs with key suppliers at

appropriate me intervals as part of an exis ng

governance process has jumped to 40% from

31% in 2011, providing a good example of

embedding BC in the organisa on.

Three more dynamic op ons are less popular,

namely reviewing business con nuity

whenever there is a major change event at the

buyer (21%) or supplier end (20%), and

whenever a new significant external threat is

iden fied (20%).

Again comments received provide some clues

into how prac oners approach this issue:

“We plan to develop a schedule, but have not

at this me. We have inadequate staffing to

“Contracts are usually for three years, we audit

at the start of the contract and mid term”

“Our concerns tend to be greater on companies

that are smaller with less public informa on

available”

“On an annual basis we select four cri cal

suppliers for capability assessment”.

Seeking alignment and adap ng

The next logical step is to check whether the

BC plans of the supplier would help you. In the

survey we termed this alignment. As BC

programmes are organised around the

objec ves and priori es of the supplying firm,

it is important for the buying firm to

understand where it fits in the picture should

an event occur. It is quite common for

organisa ons to priori se between services

and hence customers in terms of con nuing

and restoring impaired ac vi es. In prac cal

terms being able to respond that you have

been largely successful, i.e. most key suppliers

are aligned, would seem to be a good result. In

2012, 23% could state this while a further 6%

stated all of their key suppliers were aligned.

The number who had not tried alignment was

14%, down from 24% in 2011, which again is a

posi ve trend.

When key suppliers do not, cannot or will not

meet alignment needs, then respondents will

typically take a number of ac ons as set out in

Chart 9. 48% of respondents are keen to work

with the supplier where there is a will on the

other side to improve. Fewer in 2012 just

accept the risk at 26%, down from 39% in 2011.

Bringing an addi onal supplier on board has

become more popular at 38% (2011: 31%).

Insurance or risk transfer is consistently one of

the least chosen op ons at 5%.

Comments from respondents illustrate the

choices available:

“A er iden fying vulnerabili es, we implement

mi ga on programs, generally around mul

-sourcing”

“Un l we find a more cost effec ve solu on, we

are using inventory to decouple our supply

capability from our supplier”

End of sec on.

Being asked about BC in tendering

Results show that more organisa ons are being

requested to provide evidence of their business

con nuity arrangements when tendering for

new business. The figure for those receiving

this request for the majority if not all tenders

has increased from 28% to 33%. Mirroring this

increase, the number who stated they are

rarely, if at all asked to provide such evidence

has fallen from 24% to 19%. Comments from

respondents suggested the trend was driven by

major global customers, the banking and

financial sector, the healthcare sector and large

automo ve manufacturers.

Among those not seeing a customer pull are

retailers and local authori es, the emergency

services and regulated monopoly service

providers, who either do not seek to win

business or whose customers don’t have the

buyer power to ask for evidence of BC

programmes (i.e. consumers).

BC involvement in procurement processes

When considering the involvement of business

con nuity prac oners in the procurement

process, there is s ll a long way to go. 51%

stated that business con nuity featured as an

integral part of the procurement process from

the start, a modest improvement on 47% in

2011, but a significant minority either ignore

business con nuity or make it a post‐purchase

ac vity. However, the comments from

respondents are more encouraging, sugges ng

that this is one area of intense ac vity, so we

should see future improvements on this

indicator. Here’s one example:

“Increasingly BCM is becoming an integral part

of the procurement process and in some cases

a key upfront objec ve. There are s ll

occasions where parts of the business make

purchasing decisions before engaging on BCM,

though the frequency is fast reducing”

Business

Con nuity

in

Tendering

and

Contrac ng

Processes

Chart 10: When tendering for new business

clients over the past 12 months, how o en have

you had to provide assurance to clients that your

own business con nuity arrangements are

sufficient? Base: 207

Chart 11: Does business con nuity feature

as part of your supplier contractual

Geographical

and

Sector

Perspec ves

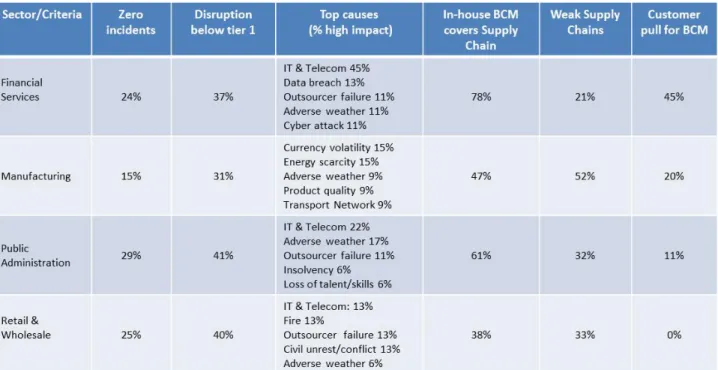

Sector comparisons

Table 1 provides a comparison of selected

industry sectors to highlight the significant

varia on in terms of disrup on, preparedness

and customer pull. A full sector lis ng is

available in Annex 2.

The criteria for comparison are as follows:

The level of incidents reported with a focus

on those repor ng “zero”

The origin of the disrup on in terms of ers,

with a focus below er one

The top five causes of disrup on by levels of

high impact

The number who state their internal BCM

programme considers supply chain

disrup on

And two further measures:

The strength of supply chains, where the

percentage against “weak supply chains”

refers to how many respondents have key

suppliers where less than half have BC

programmes in place for their own needs

Customer pull, where this means the

frequency with which evidence of BC is

requested in tendering for new business, and

the percentage relates to those who do so

every me or the majority of mes

The financial services sector is more advanced

than other sectors in terms of extending BC

programmes to consider their supply chain at

78% and their key supply chains are stronger

than other sectors, confirming a head‐start in

the introduc on of supply chain con nuity.

This sector also stands out for having to

provide evidence of their BC programme in

tendering, with 45% having had this experience

in the past 12 months.

Given the high reliance on technology it is not

surprising to see IT and telecom outages as the

leading source of disrup on in financial

services coupled with informa on and cyber

security threats.

Manufacturing serves as a good contrast,

experiencing high levels of disrup on rela ve

to others (85% experienced at least one

disrup on) and a different range of disrup ve

events consistent with the sector. At 47%

fewer in‐house BC programmes consider

supply chain partners than in financial services

and those that have addressed this issue face a

major challenge with their supply base—52%

of respondents in manufacturing concede that

less than half of their key supply chains have

business con nuity for their own needs (let

alone any a empt at alignment). It is also

evident that to date there has been a low level

of customer pull to change this situa on at

20%.

With public administra on, we would not

expect to see a high level of customer pull but

there are o en statutory requirements that

drive BC programmes. The range of sources of

disrup on provides some contrast with

outsourcer failure, insolvency and loss of talent

or skills causing disrup on. Policy changes for

public administra ons to move to shared

service models and private sector providers

may well be exposing organisa ons in this

sector to these threats.

The retail and wholesale sector does not have

their customers reques ng evidence of BC

arrangements before making a purchase, and

it’s good that the survey confirms this long

standing assump on. It’s also consistent with

the nature of the sector that their supply chain

may be affected by riots or civil disturbances as

these tend to occur in city centres. The sector

does stand out from others for the lack of

in‐house BC programmes considering supply

chain disrup on at just 38%.

Geographical comparisons

There is significant varia on in maturity with

respect to considering supply chain disrup on

within in‐house BC programmes when viewed

on a geographical basis. Respondents from the

UK and USA form a substan al part of the

survey response and therefore lend themselves

to comparison (Annex 2 provides a fuller

geographical breakdown of responses).

The UK sample is drawn from 14 different

sectors with 28% from financial services, 16%

from public administra on, 11% from

professional services and IT/communica ons

and transport/storage each sharing 7%. 80%

experienced at least one disrup on and 33%

found the disrup on originated in the

extended supply chain. The London 2012

Olympics registered as one of the top five

causes of some or high impact disrup on and

was ahead of industrial ac on but some way

behind IT and telecom outages and adverse

weather. The UK stands out from other

countries in considering supply chain

disrup on within BC programmes with 75%

confirming this compared with just 44% of US

respondents and similar levels in Australia,

New Zealand and Canada. The UK also differs

from other countries in respect of customer

pull for the provision of informa on around

business con nuity in tendering processes,

where 34% stated that they typically have to

do this compared with 23% in the US. The US

sample in this survey was also drawn from 14

sectors, however manufacturing was the lead

sector in terms of response at 18% with retail/

wholesale at 13% and financial services at 13%.

The US respondents reported lower levels of

disrup on and the top threat profile reflects

the different mix in sectors with product

quality incident and lack of credit featuring

prominently.

Although the US respondents may lag on

considering supply chain business con nuity,

those that do are slightly ahead of the UK and

other countries in terms of having stronger

supply chains, i.e. more than 50% of key supply

chain partners have BC arrangements, and they

are less likely to wait for contract renewal

before reviewing their business con nuity

requirements with their key suppliers.

Looking beyond these two countries to a

broader regional picture, we see that the

region which experienced most disrup on was

the Middle East & Africa where 78%

experienced at least one disrup on. 70% of

respondents from con nental Europe and

Central & La n America experienced at least

one disrup on, while respondents in Asia

experienced a quieter year with 43%

registering “zero incidents”. There is a

significant difference in threats when viewed

on a regional basis with energy scarcity and

exchange rate vola lity domina ng in Middle

East & Africa, while IT and telecom was the

primary source of disrup on in con nental

Europe.

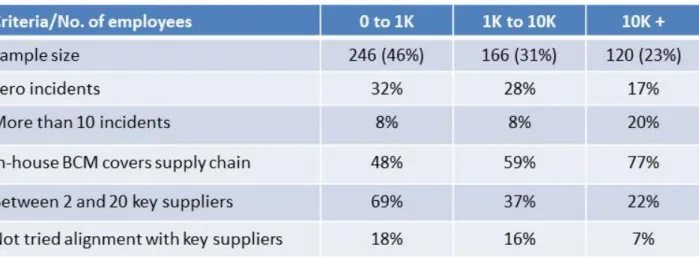

Comparison by organisa onal size

The size of an organisa on also has an impact

on the experience of disrup on and business

con nuity approach as Table 3 shows. The

results are consistent with expecta ons— the

larger the organisa on, the greater the

likelihood of experiencing disrup on. 20% of

firms with more than ten thousand staff

experienced more than ten incidents compared

with 8% in smaller sized en es. Larger

organisa ons are also more developed in

considering business con nuity for the supply

chain and more likely to have tried to align

their requirements with their key supply chain

partners.

End of sec on.

“Assurance from suppliers can only go so far. A

plan for dealing with the effects of a disrup on

is needed, even if the supplier’s business

con nuity arrangements are extremely robust”

Survey respondents felt the main lesson to be

taken away from the disrup on they

experienced was to improve their approach to

business con nuity in terms of risk assessment,

mi ga on efforts, planning and exercising.

“The plans we have in place and work we’ve

done with suppliers have helped an cipate

incidents, proac vely plan our response,

communicate to stakeholders and minimise

impact. Several years ago this would not have

been the case”

Specific ac ons taken over the past 12 months

can be divided into three broad areas of

ac vity: More analysis, securing new policies

or introducing new processes, and taking the

extra step of running joint workshops or

exercises with partners, the la er generated

some very posi ve outcomes:

“Joint exercises with key suppliers and

observing their exercises. These really focus

the minds and the general improvement in

exercising is reassuring”

Some changes in procurement policy were also

required including moving away from single

source (where possible), making provision for

alterna ve suppliers, transport routes and

payment methods, and introducing buffer

stocks.

“We have amended tender packs to request

details of suppliers’ BCM. We have introduced

a consistent ra ng methodology to assess

supplier cri cality in line with our own BIA

process”

The top 10 challenges (see Table 4) are led by

two related subjects in the sense that resource

and budget availability in larger organisa ons,

where most respondents are, is really a ma er

of priority and buy‐in and not a lack of people

or funds. Beyond these leading factors, there

is a wide range of issues to be addressed, in

some cases it would warrant a re‐evalua on of

the strategy. For more comments, please

refer to Annex 1.

Table 4: Base: 167 respondents provided free-form responses

Since 2009 consistently high levels of supply

chain disrup on have been experienced and

events are becoming more consequen al even

with absolute levels dipping a er 2011, a year

which saw the Great East Japan Earthquake

and extensive flooding in Thailand.

One area for further work is a be er

understanding of the cascading nature of risks

and their consequences in supply chain

con nuity. The research in 2012 has iden fied

that there are mul ple consequences from the

same event.

A number of non‐tradi onal business

con nuity risks have registered in this year’s

survey, most notably disrup on caused by

exchange rate vola lity. Applying business

con nuity exper se specifically around

con ngency planning presents an excellent

opportunity for prac oners to provide a more

valuable service to their organisa ons. One

other risk type also became more visible,

namely disrup on caused by intellectual

property viola ons, and this deserves further

analysis.

The drama c rise in disrup on through

outsourcer service failures requires further

study into service chains and the specific

challenges inherent in them.

Given the dominance of supply chain

disrup on through unplanned IT and telecom

outages, there is now a need to evaluate the

contribu on of “the cloud” to resilience.

The challenge of securing execu ve buy‐in

requires an understanding of the broader

trends driving supply chain vulnerability and its

disrup on. In this way it will become possible

to demonstrate the trend is not going to go

away, however fragile corporate memory may

be.

More work is also required to understand the

economic impact of supply chain disrup on

including the value of investment in raising the

level of resilience in key supply chains.

This la er work will help support the challenge

of unlocking resources through execu ve

commitment. In addi on, the broader trends

that are driving supply chain vulnerability and

hence disrup on need to be be er

understood.

One useful next step from this research would

be to develop an assurance model that would

allow a calibrated response to the ques on

“how confident are you in the resilience of our

key supply chains?”

Another business con nuity specific

perspec ve to track is whether the new

interna onal business con nuity standard ISO

22301 will make efforts to seek alignment

easier and thereby contribute to improved

resilience.

The good news for business con nuity

professionals is that the BC methodology is

widely seen as effec ve in resis ng the impact

of disrup on, alongside its core benefits of

enabling con nuity and faster recovery from

incidents. Good prac ce is documented in

abundance in the survey and there is li le

excuse for not trying out some of the ideas.

The value of moving from a documenta on

centric approach for evalua ng supply chain

resilience to one based on ac ve engagement

and joint exercises is also clear. In closing, let’s

not find ourselves in the situa on that one

person did:

“A major failure that impacted our customers

drew management a en on to the issue. It

took a $4million (US) loss to get any a en on.”

Respondent

Profile—base

532

Chart 14: Geographical loca on

Chart 13: Primary ac vity of the organisa on

Chart 16: Size of organisa on by revenues

or budget (public sector): 460 respondents

Chart 12: Func onal role

Chart 15: Size of organisa on by number of

Fieldwork for the 4th Annual Supply Chain Resilience Survey commenced on 22nd June and closed on 31st August 2012 with

532 responses validated. All members of the Business Con nuity Ins tute received an individual email invita on to complete

the online survey. This was complemented by the Chartered Ins tute of Purchasing and Supply invi ng its members to

contribute through their exis ng communica on methods. In addi on, support is acknowledged from the following people

and organisa ons:

Chartered Ins tute of Logis cs & Transport

AIRMIC

Colin Ive MBCI and the BRiSC community

Buyers Mee ng Point

Kuniyuki Tashiro MBCI for transla ng the survey into Japanese.

We would like to thank Zurich Insurance Group for sponsoring this research for the fourth successive year and DHL Supply

Chain for joining them for a second year.

We would also like to thank the BCI Partnership Working Party on Supply Chain Con nuity under Steve Wicks MBCI, and the

wider BCI Partnership Steering Group for their support in the development of the survey.

Author: Lee Glendon CBCI, Head of Research & Advocacy, The Business Con nuity Ins tute

Reviewers: Lyndon Bird FBCI, Technical Director, The Business Con nuity Ins tute. Deborah Higgins MBCI, Technical &

Learning Manager, The Business Con nuity Ins tute

About

The

Business

Con nuity

Ins tute

Based in Caversham, United Kingdom, the Business Con nuity Ins tute

(BCI) was established in 1994 to “promote the art and science of business

con nuity management” and to assist organisa ons in preparing for and

surviving minor and large‐scale man‐made and natural disasters. The

Ins tute enables members to obtain guidance and support from their

fellow prac oners, as well as offers professional training and cer fica on

programmes to disseminate and validate the highest standards of

competence and ethics. It has over 7,000 members in more than 100

countries, ac ve in an es mated 2,500 organisa ons in private, public and

third sectors. For more informa on go to: www.thebci.org

The BCI Corporate Partnership, established in 2007, offers corporate

membership of the BCI with over 90 member organisa ons including: Aon

Risk Consul ng, BAE Systems, BP, BSI Management Systems, BT,

ClearView Con nuity, Con nuitySA, Con nuity Shop, DHL Supply Chain,

DNV Business Assurance, eBay, eBRP Solu ons, Hill Dickinson, iAgenci,

IBM, Itau‐Unibanco, KPN Corporate Market, LRQA, Link Associates, Milton

Keynes Council, Na onal Grid, Phoenix, Pruden al, PwC, Reed Elsevier,

Royal Mail, Savant, T‐Systems, VocaLink and Zurich Insurance Group.

To join as a corporate member, go to: www.bcipartnership.com

Business

Con nuity

Business Con nuity (BC) is the capability of the organisa on

to con nue delivery of products or services at acceptable

predefined levels following a disrup ve incident.

Business Con nuity Management (BCM) is a holis c

management process that iden fies poten al threats to an

organiza on and the impacts to business opera ons those

threats, if realized, might cause, and which provides a

framework for building organiza onal resilience with the

capability of an effec ve response that safeguards the

interests of its key stakeholders, reputa on, brand and

value‐crea ng ac vi es.

Source: ISO22301:2012

Contac ng

the

BCI

Lee Glendon CBCI, Head of Research & Advocacy

The Business Con nuity Ins tute

10‐11 Southview Park, Marsack Street

Caversham, RG4 5AF, UK.

Phone: +44 (0) 118 947 8215

About

The

Chartered

Ins tute

of

Purchasing

&

Supply

The Chartered Ins tute of Purchasing & Supply (CIPS) is the world’s largest procurement and supply

professional organisa on. It is the worldwide centre of excellence on purchasing and supply

management issues. CIPS has a global community of over 88,000 in 150 different countries,

including senior business people, high‐ranking civil servants and leading academics. The ac vi es of

purchasing and supply chain professionals have a major impact on the profitability and efficiency of

all types of organisa on and CIPS offers corporate solu ons packages to improve business

profitability.

Zurich

Zurich is a thought leader in supply chain risk management. It has developed supply chain risk

assessment tools and an innova ve and award winning supply chain insurance product. The company

has extensive experience of working with clients to help them make their supply chains more resilient.

Zurich Insurance Group (Zurich) is a leading mul ‐line insurance provider with a global network of

subsidiaries and offices in Europe, North America, La n America, Asia‐Pacific and the Middle East as

well as other markets. It offers a wide range of general insurance and life insurance products and

services for individuals, small businesses, mid‐sized and large companies as well as mul na onal

corpora ons. Zurich employs about 60,000 people serving customers in more than 170 countries.

Founded in 1872, the Group is headquartered in Zurich, Switzerland. Zurich Insurance Company Ltd

(ZURN) is listed on the SIX Swiss Exchange and has a level I American Depositary Receipt program

(ZFSVY) which is traded over‐the‐counter on OTCQX. Further informa on about Zurich is available at

www.zurich.com

Zurich

Contact

Details

Nick Wildgoose, Global Supply Chain Product Manager

Phone: +44 (0) 0787 588 6068

Email: [email protected]

About

DHL

DHL is the global market leader in the logis cs industry and “The Logis cs company for the world”. DHL

commits its exper se in interna onal express, air and ocean freight, road and rail transporta on, contract

logis cs and interna onal mail services to its customers. A global network composed of more than 220

countries and territories and about 275,000 employees worldwide offers customers superior service

quality and local knowledge to sa sfy their supply chain requirements. DHL accepts its social responsibility

by suppor ng climate protec on, disaster management and educa on.

DHL

Supply

Chain

Service

Capability

DHL Supply Chain provides solu ons for all industry sectors including retail and fashion. By understanding

your business needs, DHL delivers cost effec ve supply chain solu ons that improve efficiency. From

consul ng and design, sourcing and transporta on through to warehousing, order assembly, distribu on

and returns, we manage the full supply chain opera on. DHL is part of Deutsche Post DHL. The Group

generated revenue of 53 billion euros in 2011.