Global Themes that Shape the Future

Spot

light

April 2013

The ING Global Opportunities strategy uses

a thematic approach to identify attractive

investment opportunities. The sub-theme

‘Big Data’ helps identify companies that will

benefit from a growing global requirement

to collect, organise, mine and analyse large

and diverse datasets.

t

Experienced management teamt

Dynamically playinto real world developments

t

Outstanding performance track recordt

Thematic approach uncovers best opportunitiesWhat is Big Data?

The benefits to a business of using its own data are frequently higher when addressing the variety of the data it collects as opposed to the volume. Unfortunately traditional data warehouses are not well-equipped to do this and certainly cannot handle modern unstructured data such as videos, images, texts and music. Fortunately, there is a new and on-going form of innovation within the IT sector that is permitting many organizations to deploy large amounts of complex data at a much faster rate and sophistication than previously was possible. This is what we call Big Data.

In practice Big Data has two main definitions. It usually refers to a special type of data: high volume, high speed and complex; or to a set of new technologies used to collect, organise, mine and analyse large and diverse datasets.

Background

Big Data opportunities emerged when several advances in four different information techno-logy categories aligned in a short period from mid-2008 through to the latter part of 2009, creating a dramatic increase in computing technology capacity.

The technological advances included the following:

t

Memory usage doubledt

Decreasing pricing of high speed networkt

Storage technology advancementt

Enhanced computing power.These cycles of improvement are normally occur-ring events — but each has a different cycle length. By mid-2009, all four of these forces

ING Global Opportunities

Big Data: The Corporate

Search for Digital Treasure

Data growth is exploding. Before 2003 mankind created 5 exabytes of data, now we

generate 5 exabytes of data every 3 days. Decoding the human genome took 10

years before 2003 but now it can be achieved in one week. Wal-Mart handles more

than 1 million customer transactions every hour with the equivalent amount of data

as 167 times the books in America’s Library of Congress. Large amounts of data offer

opportunities but putting it all together requires new IT solutions. Enter Big Data!

Dirk-Jan Verzuu is Senior Portfolio Manager & Client Portfolio Manager of the ING Global Opportunities strategy.

Zhikai Xu is an Investment Analyst within the ING Global Equity Research Team focusing on Global Software and IT.

combined almost simultaneously and formed a massive new capacity for information management environments, serving as a Big Data trigger.

In 2012, business operations discovered that new capacity, combined with latent demands for analysis of social network data and operational technology (or machine data), created an environment highly conducive to rapid innovation.

MapReduce and Hadoop

Google is one of the pioneers of the type of technology frequently used to build Big Data solutions. It designed MapReduce and Google File System (GFS) to cope with its expanding data challenges. The concepts behind Google’s designs were shared with the IT community.

Apache Hadoop is the derived open-source software frame-work used by the IT community to build Big Data architectures. It is already used by many well-known organisations such as Google, Amazon, Facebook, Twitter, Yahoo and eBay.

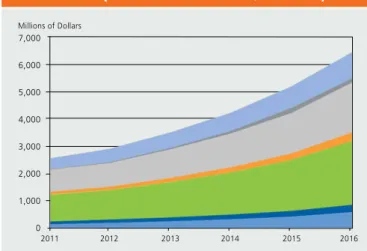

Figure 1: IT Spending Driven by Big Data Issues,

2011 to 2016, Enterprise Software-Specified

Sub Markets (Rounded to Nearest $1 Million)

7,000 6,000 5,000 4,000 3,000 2,000 1,000 0 2011 Millions of Dollars 2012 2013 2014 2015 2016

Ŷ

Storage Management (percentage is averaged from others provided)Ŷ

Big Data Social and Content AnalyticsŶ

Database Management SystemsŶ

Data Integration Tools and Data Quality ToolsŶ

Application Infrastructure and MiddlewareŶ

Business IntelligenceSource: Gartner (October 2012)

What is driving Big Data?

The list of companies mentioned above already hints to the forces driving the demand for Big Data innovation. Indeed we already described how Google’s business model helped to pioneer advancements in this area. Notwithstanding Google’s enormous capacity requirements, it is fair to say that the need to collect data and store it is very widespread across most industries. In the case of Facebook, the company is home to more than 200 billion photos and more than 200 million are

uploaded every day. However, the real commercial treasure is considered to be the ability to analyse the large volumes of social content and related behaviour. Of course, in order to do this you would need to have the right kind of software and also a certain level of speed to ensure timely application of any business opportunities.

The benefits of combining large volumes of complex data with analytics and velocity are still yet to be discovered in some industries while in others they are already being implemented. For example, regular air travellers may have noticed that some operators are now able to offer real time prices based not only on seat availability but also on luggage, leg room, meal, car hire and hotel requirements. The efficiency in which airlines can also factor in movements in the oil price and forecasted fuel costs can also be linked to Big Data solutions.

In retail, predictive big data analytics based on shopping habits have been around for a while. In the United States, the large discount store company Target famously knew that a teenage school girl was pregnant before her father did. The retailer had sent baby clothes vouchers to the girl’s home address having used her shopping data to conclude she was pregnant. The father initially complained to the local store manager, only to later apologise.

Businesses are increasingly seeing the power of putting their large volumes of “sleeping” data to work. In figure 1, we can see how IT expenditure levels related to Big Data are set to con-siderably grow over the coming years. With this extraordinary level of investment we can only conclude that industries will be revolutionised going forward as Big Data will help them to:

t

Signal Customer Behaviour and Demandt

Support Management and Decision Makingt

Enhance Product Innovationt

Increase R&D Speed and Capacityt

Reduce Costst

Create Entirely New BusinessesThe main drivers of Big Data are ultimately these eventual benefits. From a data perspective, it can also be seen as simply the need for speed, volume, complexity and analytics.

How will Big Data change the IT world?

We know that Big Data initiatives and needs will increase corporate and public sector spending and investment in tech-nology. However, it is not sharply reshaping the IT architecture. It is rather an evolving process. Sometimes organizations just have to do the traditional thing of “catching up”. Most Big Data technologies are offering niche functionality on top of the legacy solutions currently, as the majority of workload is still handled in traditional enterprise IT architecture. As Big Data evolves, niche offerings may merge and new standards will emerge, typically in the open source world. There will probably be lower cost and far more flexible solutions in the future and that will challenge legacy constructions.

Looking at IT vendors, it can be anticipated that the majority of new participants that offer services on how to address Big Data issues will be consolidated in a wave of acquisitions. This trend has actually already begun and will continue through to 2018. A small minority of new vendors, focused on identification, auditing, organization and enablement of semantic consis-tency of Big Data assets will mature and survive as information services providers, specializing in accessing and delivering data from widely disparate information systems.

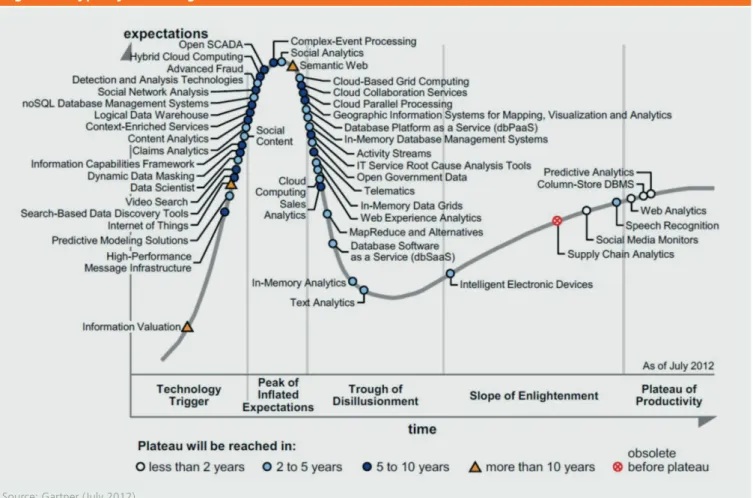

Which areas of Big Data are growing?

Despite Big Data being in its early growth stage, some areas of Big Data are nearing the end of the “additive” phase of a composite market and entering into the “competitive” phase, while others are still in the additive phase. Gartner’s hype cycle (figure 2 above) illustrates the depth and diversity of emerging sub-segments within Big Data. Some descriptions refer to enabling technologies, some reflect the uses of Big Data, while others represent new information types. The far left of the diagram is where current innovation can be found while to the right we are looking at areas that have demonstrated their commercial benefits and are being adopted by industry on a significant scale.

Within Big Data it is still necessary to apply normal data management practices such as data security and data protec-tion. Technologies directed at supporting these functions for

Big Data are only now beginning to emerge and significantly lag Big Data processing technologies. If we try to size the opportu-nity, a total of $5.5 billion in software sales in 2012 was driven directly by demands for new Big Data functionality. A significant amount of Big Data-driven IT spending will be in IT services to support Big Data use. The cost of IT services to support Big Data initiatives is very high relative to software purchases (20 times that of software). Skills are rare and in high demand.

Data analyst – the new profession

While Big Data technology can help companies gain a com-petitive advantage on their rivals, the ability to interpret and filter Big Data and translate it into viable corporate strategic initiatives will become a science in itself. Data analysis has not typically been considered as an attractive career path for young and ambitious university students. However, this will change as businesses will need to attract talent to make their Big Data ambitions work. This may mean forming partnerships with universities and implementing graduate training programmes. In Gartner’s hype cycle, they identify the role of the “data scientist” as one of the emerging areas, with an expected 5-10 years before being widely adopted. A shortage of skills is therefore expected in the short run. The mismatch between increased demand for data analysts and supply of qualified individuals may turn companies in the direction of staff retraining in order to bridge a gap.

Figure 2: Hype Cycle for Big Data, 2012

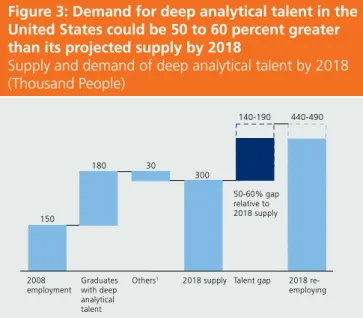

Figure 3: Demand for deep analytical talent in the

United States could be 50 to 60 percent greater

than its projected supply by 2018

Supply and demand of deep analytical talent by 2018

(Thousand People)

150

180

2008

employment Graduateswith deep analytical talent 2018 supply 2018 re-employing Talent gap 50-60% gap relative to 2018 supply Others1 30 300 140-190 440-490

1 Other supply drivers include attrition (-), immigration (+), and

re employing previously unemployed deep analytical talent (+). Source: US Bureau of Labor Statistics; US Census; Dun & Bradstreet, company interviews; McKinsey Global Institute analysis.

Sub-theme within the Global Opportunities

strategy

Leveraging Big Data will be a necessity for running the com-panies of the future. Adopting Big Data solutions could be like opening a treasure chest for many businesses. The ING Global Opportunities team seeks to identify the winners from this trend. Big Data is a sub-theme within the strategy’s ‘Digital Revolution’ investment theme, which is one of the seven main pillars of the team’s thematic approach to global investing. Fundamental analysis at stock level is supported by a large team of global equity research analysts, covering both develo-ped and emerging markets.

The 7 Global Investment Themes of ING (L) Invest Global Opportunities

1. Economic Growth – A number of countries in the world

is explicitly targeting economic growth and are structuring their governmental policies to support this goal.

2. Technological & Industrial Innovation – The factor

technology will have an equally decisive role in the future as labour and capital had in the past.

3. Changes in Consumer Behaviour – Driven by changes

in (the distribution of) wealth, demography and personal preferences, there are several significant changes in consumer behaviour around the globe.

4. Environmental Changes – Environmental awareness has

been put firmly on the global agenda, creating numerous investment opportunities in the area of clean energy, water management and ‘green’ production

processes.

5. Digital Revolution – While stock valuations in the late

1990s clearly got ahead of themselves, many predictions about information technology were in fact not far off the mark, measured by today’s numbers. Only now we are witnessing the far-reaching nature of information technology both in the lives of consumers as well as in the corporate world.

6. Social & Political Changes – Watching the phenomenon

of globalization closely, one can clearly see that both social and political changes influence the shape of economic deve-lopments in a meaningful way.

7. Shifts in Demography – The most striking global

phenomenon in the global demographic situation is the aging of the general population. The ratio between working and nonworking people will change dramatically and this will significantly change the allocation to labour, capital and technology.

Real world events

Investible Sub-themes

Stock opportunities

Themes

Disclaimer

The company and brand names mentioned in this document are given as an example and do not represent any recommendation to buy, hold or sell the stock. Securities may be/have been added and/or removed from the portfolio at any time without any pre-notice.

The elements contained in this document have been prepared solely for the purpose of information and do not constitute an offer, in particular a prospectus or any invitation to treat, buy or sell any security or to participate in any trading strategy. Invest-ments may be suitable for private investors only if they are recommended by an authorised self-employed or a professional employed adviser acting on behalf of the investor on the basis of a written agreement. While particular attention has been paid to the contents of this document, no guarantee, warranty or representation, express or implied, is given to the accuracy, correct-ness or completecorrect-ness thereof. Any information given in this document may be subject to change or update without notice. Neither ING Investment Management (Europe) B.V. nor any other company or unit belonging to the ING Group, nor any of its officers, directors or employees can be held direct or indirect liable or responsible with respect to the information and/or recom-mendations of any kind expressed herein. No direct or indirect liability is accepted for any loss sustained or incurred by readers as a result of using this publication or basing any decisions on it. Investment sustains risks. Please note that the value of your investment may rise or fall and also that past performance is not indicative of future results and shall in no event be deemed as such. This presentation and information contained herein is confidential and must not be copied, reproduced, distributed or passed to any person at any time without our prior written consent. Any claims arising out of or in connection with the terms and conditions of this disclaimer are governed by Dutch law.

ING (L) Invest Global Opportunities is a subfund of ING (L) Invest (SICAV), established in Luxembourg. ING (L) Invest is duly authorised by the Commission de Surveillance du Secteur Financier (CSSF) in Luxembourg. Both funds are registered with the CSSF. For more detailed information about the investment fund we refer to the prospectus and the corresponding supplements. In relation to the investment fund mentioned in this document a Financial Information Leaflet (simplified prospectus) has been published containing all necessary information about the product, the costs and the risks which may occur. Do not take unneces-sary risk. Read the Financial Information Leaflet (simplified prospectus). Investments are accompanied by risks. The value of your investments depends in part upon developments on the financial markets. In addition, each fund has its own specific risks. See the prospectus for fund-specific costs and risks. The prospectus, supplement and the Financial Information Leaflets (simplified prospectus) are available on the following website: www.ingim.com.

For more information please contact:

Dirk-Jan Verzuu (Client Portfolio Manager)Anthony de Silva (Portfolio Specialist)