How much you know matters: A note on the exchange rate disconnect puzzle

Full text

Figure

Related documents

The field of study called information systems encompasses a variety of topics including systems analysis and design, computer networking, information security, database management

BRRI is a research based organization but many infrastructure development works are procured under building and contractions division. Purchasing division procure many

Dairy farming is practiced in the highland areas of the country – mainly Central, South Rift, North Rift, parts of Eastern (Meru and Embu counties) and Western Kenya.. The

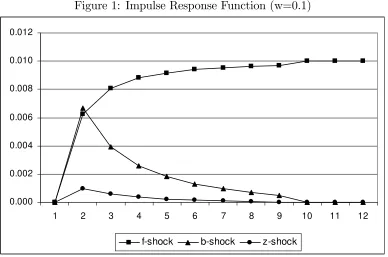

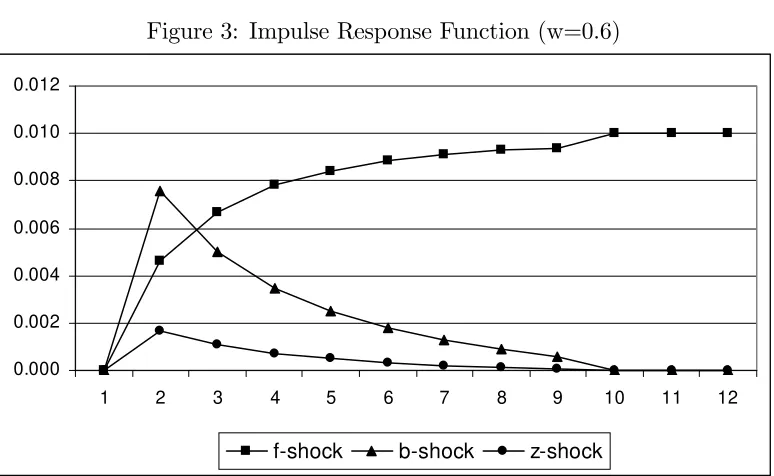

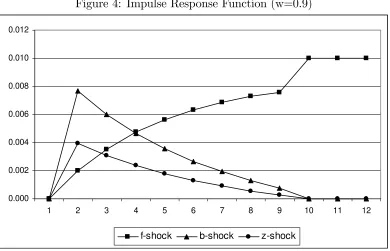

Money growth and trade balance explain only up to 0.48% and 3.47% of forecast error variance in inflation respectively, suggesting that movements in inflation can neither be

In this study, SLM with a pulsed laser mode is used to produce 316L stainless steel samples for an investigation on chemical distribution from mac- roscopic level down to

Overall, four different treatments were performed: (i) inoc- ulation of cells with AcEGFP-PH ⫺ , followed 24 h later by inoculation with SfMNPV; (ii) a simultaneous infection in

Uniform Standards of Professional Appraisal Practice (USPAP) 1994 Update Course, American Society of Appraisers, July 1994. Residential Contents, American Society of