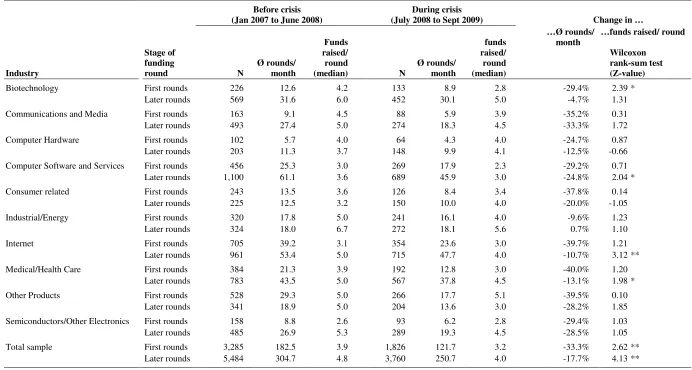

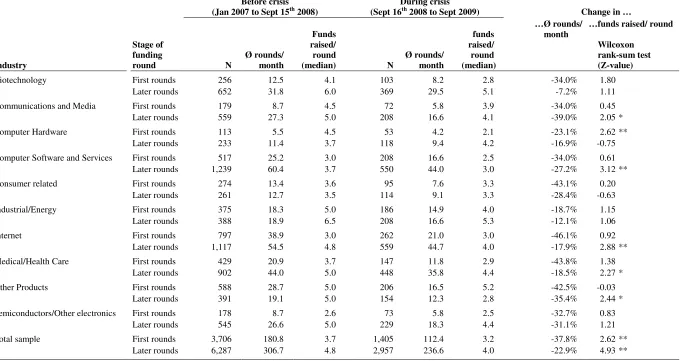

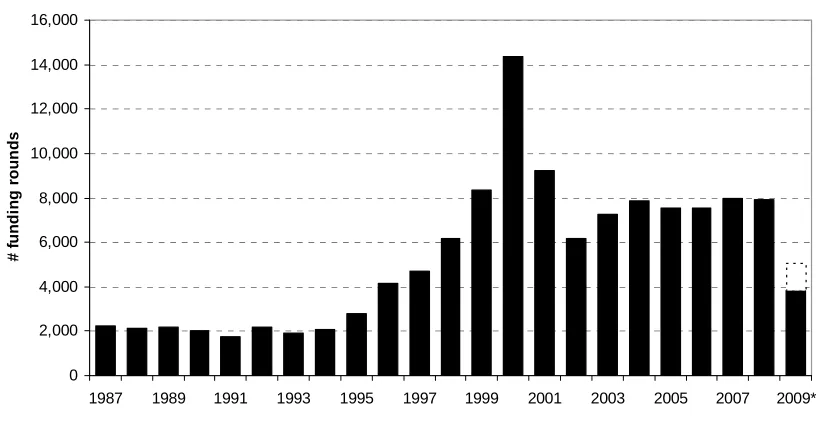

Venture capital and the financial crisis: an empirical study across industries and countries

Full text

Figure

Related documents

IU HEALTH NORTH HOSPITAL physicians/AHPs acting as Preceptors of an accredited school of medicine or an accredited Resident/Fellowship program shall provide documentation of

Since state guaranty associations ultimately pay off all liabilities by as- sessing the surviving companies, this expected loss represents an externality to the life insurers not

This scheme has now been revised to conform to the nationally recognised framework for Final Accuracy Checking of dispensed items (dispensary) and Pre and In-process checking

GDM: gestational diabetes mellitus; T1DM: Type 1 diabetes mellitus; T2DM: Type 2 diabetes mellitus; FPG: fasting plasma glucose; DBP: diastolic blood pressure; HbA1C: hemoglobin

It is essential to protecting what is left of the assets of the Alleged Debtor and its related entities that an interim trustee take immediate control of the books and records of

Difference spectra shows a symmetric broadening around peak maximum, consistent with the reduction of the core level intensity... C1s core

The upshot is a generalization of the Cournot outcome obtained by KS for a duopoly: when θ is su ffi ciently high, at the subgame perfect equilibrium solution of the capacity and

Impel is an integrated CRM solution from Ampersand that boasts of complete CRM functionality, encompassing market support, sales management and customer