International Journal Advances in Social Science and Humanities

Available online at: www.ijassh.comRESEARCH ARTICLE

Assessment of Factors that affect Customer Retention in Punjab National

Bank: Amroha Branch

Sarfaraz Karim*, V.P.S. Arora

Department of Management, Shri Venkateshwara University, Amroha, U.P., India.

Abstract

The purpose of this study is to assess the factors that affect customer retention and how customers evaluate banking services based on their important level that affect their relationship with the branch and also assess employees’ perception of customer retention. To achieve the objectives of this study, both quantitative and qualitative methodology were employed and data were collected through questionnaire and interview from sample of 352 bank customer and 8 employees of the branch. These respondents were selected using a non-probability purposive sampling method. Secondary data were collected through surveying documents of the bank, magazines, bulletins and reports. The data collected were descriptive analyzed. Findings from this study reveal that, customers were most dissatisfied with the issues dealing with factors that affect customer retention such as, services provided by the branch, speedy service of the branch, customer service of PNBs comparing with private banks, and loan policy of PNBs comparing with private Banks. And also customers were commented that complaint handling of the branch not satisfactory and suggest some additional improvements in the branch banking services other than the services currently offer. Finding of the study also indicates that employees’ of the branch were agreed that, all service provided by the branch have different problem that affect customer retention significantly loan and local transfer services. Based on the findings of the study the researcher forwards some recommendation to the branch management to widening service quality and providing good customer services to customers and to be considered seriously by PNB Amroha branch in designing its marketing strategies.

Keywords: Customer retention, Customer satisfaction, Marketing strategies, and Relationship marketing.

Introduction

The banking industry is highly competitive, with banks not only competing among each other, but also with non-banks and other financial institutions. Most banks product developments are easy to increase and when banks provide nearly similar services, they can only distinguish themselves based on price and quality as by Holstius and Kaynak [1]. Customer retention is an effective and important tool that banks can use to gain a strategic advantage and survive in today’s ever increasing banking competitive environment, suggested by Kaynak and Kucukemiroglu [2]. The Subject of customer retention is relatively global issue. It is more rational and economical to keep customers instead of looking for new ones. According to Kotler [3], The costs of acquiring customers to replace those who have been lost are high,

the major factor for its continuing existence and profitability. As it is said a bird in the hand is worth two in the bush, different studies have also indicated that customer retention delivers to an organization a lot of benefits, suggested by Colgate et al.[5]. According to Almossawi [6], the longer a customer stays with an organization or a company the more utility the customer generates. In addition to this, different researchers similarly argue that besides the benefit customers’ longevity- creates, the costs of customer retention activity are less than the costs of acquiring new ones. For instance, Kotler [3] stated that “the cost of attracting new customers may be five times as costly as keeping existing customer.” On the other hand, maintaining high levels of customer satisfaction may not ensure customers’ loyalty. Retaining customers is also dependent on a number of factors which are customers’ choices, conveniences, prices, incomes, approval of the employee and compliant mechanism. Although such studies have contributed substantially to the literature on customer retention, their findings may not be applicable to other countries like India, due to differences. The establishment of new private banks in the country gives customers free choice of banks to work with. Therefore, it is observed that PNB has lost its well treated and seemed satisfied customers who felt that they would get better services in other private banks. The bank’s confinement and focus only on these limited sectors could restrict the bank’s loan product provisions to other sectors. This less attention to finance domestic trade service individuals who need additional working capital, forced them to shift other private banks to solve their financial problems. Therefore, this issue triggered the researcher to assess the factors that affects customers’ retention and loyalty in PNB Amroha branch.

The general objective of the study is to assess the factors that affect customer retention in Punjab National Bank (PNB) Amroha Branch. Specific Objectives are to examine bank image towards retaining customers, to evaluate factors that customer consider important in selecting their choice of Bank, to identify the affect of financial benefits to customers, towards retaining

customers, to analyze the customers’ perceived value of bank services, to investigate the complaint handling and perception of the employees in the effort to retain customer.

Methodology

Target GroupsThe target groups of this study were the PNB Amroha Branch, employees who are currently working in different sections of this branch, current customers (existing customers) who are using different services of the branch and former loan customers of this particular branch but who left the branch and shifted to other private Banks found in Amroha town.

Data Source and Type

Concerning data sources, both primary and secondary data were used. For the primary source observation, personal interview and questionnaire were used. The secondary data were collected from reading of literatures related to the problem investigated and from documents of the Bank. To have enough information as much as possible and address all the research questions, both qualitative and quantitative data types were employed. Qualitative data are designed to understand the perception of respondents, and to create space for researchers to analyse complex and often non quantifiable cause and effect relationships and the meaning that owners impute to these relationships, as pointed by Holland and Campbell [7].

Sampling Techniques and Sample Size

The target population of the study was included employees and customers of the branch. Hence it is inevitable to go for selecting sample from the whole population. Given the nature of the study (due to the unavailability of sampling frame of the branch customers’ or infinite population), a non-probability purposive sampling is chosen. Determine sampling size for above 10,000 populations, standard statistical approach equation was used.

Therefore, n= Z2 pq/d2

population is greater than 10,000

Z = The standard number variable at a required level of confidence

p= The proportion of in the target population estimated to have characteristic being measure q=1-p

d=The level of statistical significance test

(0.05)

n =Z2 p(1-p)/d2 =(1.96)2(.5×.5)/(.05)2 =384.2 ≈ 385

In this way, the researcher distributed 385 questionnaires to customers who are using this branch: to transfer money to other branches, for forex and for saving and current account services purposely. In this study, eight employees of the branch selected based on experiences in their current job, their direct contact with customer and interviews were conducted by purposive method.

Data Analysis Method

More of qualitative method of analysis was employed in addition to quantitative method so as to address the aforementioned problems of customer retention of the branch. Both methods of analysis were used on the data collected through the well-structured questionnaire, interview and secondary sources. Findings, which reflect a high magnitude of the problem, were selected from interview and questionnaires, the raw data were analyzed, presented, and interpreted to give solutions for the research problem. Moreover, most of the data were summarized and presented in tables, graphs, and different types of charts. Percentages for these data were calculated in order to facilitate the analysis and to make it presentable for the readers.

Result

Major results are shown below in the form of descriptive and factor analysis

Table 1: Results of profile data of the respondents

Variable Categories Frequency Percent

Sex Male 271 77

Female 81 23

Age Below 27 Years 186 52.7

27 - 35 years 100 28.4

36 -45 Years 56 15.9

Above 45 years 11 3

Level of Below Preparatory 16 4.5

Education School Completed 35 10

Diploma 30 8.5

Bachelor Degree 207 58.7

Master and Above 64 18.3

Level of Lower than Rs. 8,000 74 20.9

Income Rs. 8001 to 12,000 208 59.2

Rs. 12,001 to 25,000 58 16.4

More than 25,000 12 3.5

Table 2: Distribution of respondents’ Age by occupation

Occupation Sex Number Percentage

Student Male 131 87%

Female 19 13%

Employee Male 84 66.70%

Female 42 33.30%

Businessman Male 58 75%

Female 18 25%

Total 352 100%

Table 3: Respondents degree of satisfaction with the bank services

Question Response Number Percent

Are you satisfied with the banking services offered by PNB

Yes 215 61.2

Factor Analysis

All analysis is conducted using SPSS statistical software version 20 for Windows. The evaluative criteria items were factor

analyzed to reduce the variables to a

manageable number of components.

According to their character seven factors are identified:

Table 4: Customer retention factors

Factors labeled Factors

Factor 1: Financial benefits/technology Low interest rate on loans High interest rate on saving

Attractive interest within short period of time Phone banking facility

Internet banking facility Low service Charge

Factor 2: Service provision Good customer services

Bank has speedy services Reception at the bank Variety of services are offered

Factor 3: Employer's & Friends influences My employer used the same bank Recommendation from friends Extended operation hours Availability of ATM services

Factor 4: Reputation Establishment time of the bank (oldest)

Bank's reputation

Being a government owned bank

Factor 5: Promotion strategy Advertising Via mass media

Availability of Several Branches Availability of parking space nearby

Factor 6: Convenience/Security Proximity to home and /or work place

Security arrangement of the bank

Factor 7: Bank image Pleasant bank environment

External appearance of the bank

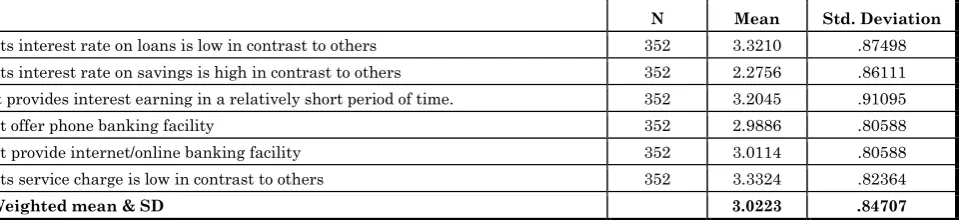

Table 5: Descriptive results of factor “financial benefit/ technology” for customer relationship with the bank

N Mean Std. Deviation

Its interest rate on loans is low in contrast to others 352 3.3210 .87498

Its interest rate on savings is high in contrast to others 352 2.2756 .86111

It provides interest earning in a relatively short period of time. 352 3.2045 .91095

It offer phone banking facility 352 2.9886 .80588

It provide internet/online banking facility 352 3.0114 .80588

Its service charge is low in contrast to others 352 3.3324 .82364

Weighted mean & SD 3.0223 .84707

The First factor financial benefit/technology in Table 5 delineates a retention factor based on low interest rate on loans, high interest rate on savings, attractive interest within short period of time and the e-banking facilities. This factor may be labeled a financial benefits/ technology factor. Here, it can be noticed that low service charge mean = 3.3324 (SD=0.82), low interest rate on loans mean = 2.0896 (SD=0.91095), attractive interest within short period of time mean = 3.2045 (SD=0.91095) and providing internet banking facility have the highest means in this factor, indicating the vast importance of service charges and

interest rate on in determining customers’ relationship with the bank. In addition interest rate on saving mean 2.2756 (SD=0.86111) has the lowest mean in this factor indicating the least important in this factor.

Table 6: Descriptive results of factor “Service provision” for customer relationship with the bank

N Mean Std. Deviation

It provide good service to customers 352 3.2727 .89922

Its service provision is fast & efficient 352 3.3295 .76567

The reception at the bank 352 3.2557 .84562

It offered variety of services to customers 352 2.9602 .88906

Weighted mean & SD 3.2045 0.8499

mean = 3.3295 (SD=0.76567), good customer service mean = 3.2189 (SD=0.89922), and customer reception at the bank mean = 3.2557 (SD=0.84562) while the least

important item is variety of service offered mean = 2.9602 (SD=0.88906).

Table 6: Descriptive results of factor “Employer's, family and friends influences” for customer relationship with the bank

N Mean Std. Deviation

My employer uses the same bank. 352 3.2472 .91443

Its extended operation hours (i.e Saturday, evening etc ) 352 3.1960 .97179

The facilities of ATM services 352 1.4830 .73166

Recommendation from my family and/or my friends 352 1.5909 .76066

Weighted mean & SD 2.3792 0.8446

The third factor employer's, family and friends influences, containing items related to my employer uses the same bank and services offered by banks including extended operation hours, availability ATM services,

and recommendation from relatives

influence. Within this factor, in relation to

PNB is paying governmental and

nongovernmental employees’ salary,

employer uses the same bank is the most

important determinate mean 3.2472

(SD=0.91443), in customer retention process. Next to the aforementioned item the branch extended operation hours is also the important determinant item mean = 3.1960 (SD= 0.97179). On the other hand, the least important item in this respect is facilities’ of ATM service mean = 1.4830 (SD=0.73166).

Table 7: Descriptive results of factor “Reputation” for customer relationship with the bank

N Mean Std. Deviation

It was established early ( it is the oldest bank) 352 2.5000 1.11197

By its reputation/brand name 352 3.2642 .92516

Being a governmental bank 352 3.4233 .77704

Weighted mean & SD 3.0625 0.9381

The forth factor, has been labeled as “Reputation factor”. Items related to this factor are establishment period of the bank (being established before others), PNB’s reputation and being a government owned bank. Among the items in this factor, being a governmental bank mean = 3.4233

(SD=0.77704) and reputation mean = 3.2642 (SD=0.92516) are the highest ranked. An implication of this is that customers consider being a governmental bank and reputation to be an important measurement in their long term relationship with the branch.

Table 8: Descriptive results of factor “Promotion strategy” for customer relationship with the bank

N Mean Std. Deviation

It advertises it’s services in mass medias 352 2.6790 .89431

It have several branches 352 3.3920 .80578

It give parking facilities 352 1.5227 .74692

Weighted mean & SD 2.5312 0.81567

The fifth factor comprises items related to

promotion strategy including advertising

services via mass-media, availability of

branches is the most significant attribute within this factor mean = 3.3920 (SD=0.80578) whereas accessibility of

parking space nearby is the least important with mean of 1.5227 (SD=0.74692).

Table 9: Descriptive results of factor “Convenience/Security” for customer relationship with the bank

N Mean Std. Deviation

The security arrangement at the bank 352 3.2642 .87124

The closeness/nearness to home and workplace 352 3.4091 .78644

Weighted mean & SD 3.3366 0.8288

The six factor, Convenience/Security:

encompasses proximity to home and/ or workplace and security arrangement in which proximity is the most important item

with a mean score of 3.4091 (SD=0.78644) this factor may be considered as convenience.

Table 10: Descriptive results of factor “Bank image” for customer relationship with the bank

N Mean Std. Deviation

The convenient location of the bank 352 3.2812 .83914

The exterior and/or interior appearance of bank 352 3.1023 .90946

Weighted mean & SD 3.1918 0.8743

Finally, the seventh factor includes items associated to bank image like pleasant bank atmosphere and external appearance of the bank. Pleasant bank atmosphere is the most important item with a mean score of 3.2812 (SD=0.83914).

It is worth mentioning that among the seven factors reported above, the sixth and the second two factors are characterized by much higher mean importance ratings than the other characteristics, emphasizing the importance of convenience and service provision for long time relationship decisions of customers by this market segment.

However, facilities of ATM services, giving parking facilities and recommendation from family and/ or friends have the lowest mean of importance rating in above mentioned components (factors). This implies that these characteristics are not important at all to customers for their long time relationship with the PNB Amroha branch.

Ranking Importance of Customer Retention Factors

In order to analyze differences in the importance of customer retention effect criteria employed, a ranking table was produced showing the weighted mean score of each factor.

Table 11: Ranking importance of customer retention factors

Factors Mean Rank

Convenience/Security 3.3366 1

Service provision 3.2045 2

Bank image 3.1917 3

Reputation 3.0625 4

Financial benefits/ technology 3.0222 5

Promotion strategy 2.5312 6

Employers and relatives influence 2.3792 7

In terms of overall factor weighted means indicated according to their importance in customer retention: the sixth factor, the second factor, the seventh factor, the forth factor and the first factor have above 3 weighted mean. And the fifth and the third factors have less than 3 weighted mean. Table 11: presents findings with respect to

interesting that the determinants of the customer retention related to the reputation are not that highly ranked as expected by PNB management. The “convenience” is the only determinant that is highly ranked by most of the respondents that also leads to the conclusion that the respondents consider the proximity to their home and/ or workplace criterion to customers remain loyal. Financial benefit/technology, promotion strategy and Employer’s influence related items are considered as the least important criteria by the customers to selecting and to be loyal to the branch. Based on the above results, we are able to attain a conclusion that the more advanced technologies are not influential by customers to facilitate reduction of the visits to the banks or reduction of personal contacts with the employees of the bank.

Data Collected from PNB Personnel

The semi-structured interview was prepared for the branch Manager, a customer service manager (CSM), the customer relation officer (CRO) and for five customer service officers (CSOs). These respondents were selected on the basis of a criterion which demands at least two years of experiences in their current job. And researcher considered also managerial respondents as key informants, because managers are most of the time responsible for all operations or activities taking place in the bank. The first part of the interview consists of the demographic information of the respondents and the second, part of the interview consists of the perception of managers and customer officers about customer retention. In the first part of the interview requested limited amount of information related to personal and professional demographic characteristics of the respondent. These variables include number of years the employee worked in the bank, job title, sex and educational qualification of the respondent.

The general comments given by the respondents’

Almost all respondents agreed that all services have different problem that affect customer retention, significantly loan

section, local transfer and cash sections are affected by the problem

Lack of skilled and well trained employees to give efficient and quality service

Length of service delivery time

Repetitive network filler

Mal functionality of cash counting machines

Length of integration between the management body and subordinates

Lack of having motivated employees to give quality services.

Actions are or will be taken to reduce the rate of defection by the bank are:

All the respondents argued that the works of the bank is to satisfy its customers in a better way because the bank can’t maximize its market if its customers are not satisfied.

The respondents are emphasizing on providing quality services to its customers.

Collaborating of staffs in reducing the work load of local transfer messages.

To handle complaints the bank organized the complaints handling committee and tried to discuss on the suggestion given by customers through suggestion box.

To reactivate dissatisfied customers the branch manager stated that branch gives more attention for the key customers of the branch to avoid customer turn over to other banks by giving loans and accepting their money to deposit in the branch. But to retain existing customers most marketing and promotion activities including advertising services via mass-media are exercised at corporate level. Some strategies designed and practiced as aggressively opening new branches, which significantly increase the availability several branches throughout the country. Enhancing the quality of the newly implemented core banking system, this is helpful in improvement of services and customer satisfaction. That is done through an intensive manpower training to implement totally performance standards through all touch points. Now a day, PNB is in a process of transformation based on

Financial Sector Growth and

Transformation Program based on this concept the bank, has put in its vision and mission statement “to be one of the world class bank” that have efficiency, good governance, and also it has described its corporate values, objectives and strategies. The next step will be creating awareness of the transformation process to all stakeholders and implementing the well-studied and far sighted process of transformation that moves the bank towards best international banking practices [9-16].

Conclusion

Looking at the specific banking services, customers are widely noticed using a saving account, money transfer services and current account. The respective numbers of beneficiaries are about 71 percent, 42 percent and 29 percent respectively. Apart from the current services, clients highlighted some further improvements in the banking industry. Among others, introduction of internet banking, phone banking, and access to ATM over all branches and inter-branch networking were identified as a key future requirements that the bank should fulfill. The factor analysis results revealed that convenience, service provision and bank image as fundamental determinants of customer retention, among others. To reveal all facts about the retention problem of the branch, interview and observation data were collected. The results showed as the major courses are summarized under the following paragraphs. The finding of the study also indicates that employees’ of the branch were agreed that, all service provided by the branch have different problem that affect customer retention significantly loan and local transfer services. Most customers who want to borrow from the branch are not only dependent on agricultural, industrial or foreign trade business but also domestic trade, transportation, hotel and etc businesses. But according PNB loan policy loan requisition for the business rather than priority sector (Agricultural, Industrial and Foreign trade) will automatically rejected. Obviously, the major source of profit is interest collected from granted loans and those customers are profitable customers. And having them retain will ensure the future of the bank profitability.

Due to the bank (PNB) is government owned bank, most de-motivated employees of the branch believed that “nothing will hurt their life” whether they perform their duties effectively or not and whether they give diligent service or not. Services given by such employees are full of complaints and results customer defection. To walk along with advanced technology and information system it is essential to offer customer oriented trainings and other advanced coursed to the workers. But training in PNB s not enough from the data obtained. Some employees in the branch are de-motivated and will not ready for the needed banking transformation. Due to lack of appreciation from their supervisors and managers for their or work mate better and exemplary performances and due to allowances payment differentiation for similar job title.

Recommendations

Based on the findings from the customer respondents’, researcher forwarded the following recommendations.

Customers place more emphasis on factors like convenience, service provision, bank image and reputation. Therefore, such factors should be considered seriously by the Punjab National Bank Amroha branch in designing its marketing strategies by widening its branches and providing good customers services to customers.

Customers suggest some additional improvements in the banking industry other than the services currently offered. Consequently, focusing on well-integrated application of technology and staff through operations that respond to customer needs encourage customers to use a whole range of banking services rather than just a few. It also helps to build loyalty by creating deeper and fuller customer relationships.

customers. In addition, the branch should try to find out some ways to better familiarize their customers with the borrowing products for customers.

Though about 50 percent of the customers report as satisfied, PNB should keep its customers more satisfied with the services provided. Based on the results of this study, customer satisfaction and loyalty would be increased by focusing on different, but related, factors: bank service processes, including well experienced bank personnel, inter-bank networking and service facilities required conditions for receiving the needed services, internet banking facilities and speed facilities.

Based on the findings from interview and observation, we forward the following recommendations.

PNB should provide training for its employees on customer oriented issues. Motivate employees who made great strides towards achieving PNBs ambition to become provider of excellent customer services. And motivate innovative

services, which utilize new technology to deliver quality, appreciate effective performance, punctually, diligent services and change initiatives.

The ground part of the PNB Amroha Branch is not enough for the existing work load therefore; the bank is strongly advised to expand its service delivery windows to the first vacant floor of the building.

Finally, the branch management should be aware that some of customer retention determinants factors differ from one segment to another in business firm market. These results would enable the bank managers to identify the factors that affect customer retention made by each segments in the business market. Since the results of this study are more dependent on customer

perception and investigating the

correspondence between customers’ and service providers’ is less prioritized by the researcher. This will help the bank to better understand whether both customers and banks have the same perceptions regarding factors that affect customer retention and could be an important research area among interested future researchers.

References

1. Holstius K, Kaynak E (1995) Retail banking in Nordic countries: The case of Finland. International Journal of Bank Marketing, 13(8):10-20.

2. Kaynak E, Kucukemiroglu O (1992) Bank and Product Selection: Hong Kong. International Journal of Bank Marketing, 10(1):3-16.

3. Kotler P (1999) Kotler on marketing: How to create, win, and dominate markets. New York: Free Press.

4. Abratt R, Russell J (2006) Relationship Marketing in Private Banking South Africa. The International Journal of Bank Marketing,

5. Colgate, M., Stewart, K and Kinsella, R. 2010. Customer Defection: A Study of the Student Market in Ireland. The International Journal of Bank Marketing

6. Almossawi M (2001) Bank selection criteria employed by college students in Bahrain: An empirical analysis. International Journal of Bank Marketing, 19(3):115-125.

7. Holland J, Campbell J (2005) Methods in development research: Combining qualitative and quantitative approaches. Rugby, Warwickshire, UK: ITDG.

8. Abduh M, Kassim SH, Dahari Z (2013) Factors Influence Switching Behavior of Islamic Bank Customers in Malaysia. JIF Journal of Islamic Finance, 2(1):12-19.

9. Beckett A, Hewer P, Howcroft B (2008) An Exposition of Consumer behavior in the financial services industry. The International Journal of Bank Marketing.

10. Bryman A (2008) Of methods and methodology. Qualitative Research in Organizations and Management: An International Journal Qual Research in Orgs & Mgmt, 3(2):430-439.

12. Fornell CA (2004) National customer satisfaction barometer: The Swedish experience. Journal of Marketing.

13. Ioanna, PD (2010) The Role of Employee Development in Customer Relations: The Case of UK Retail Banks. Corporate communication.

14. Lee J, Marlowe J (2003) How consumers choose a financial institution: Decision‐ making criteria and heuristics. International Journal of Bank Marketing, 21(2):53-71.

15. Maiyaki AA (2010) Factors determining bank’s selection and preference in Nigerian retail banking. International Journal of Business and Management, 6(1).