FINANCIAL PERFORMANCE OF INDIAN BANKING SECTOR: A CASE STUDY OF SBI AND ICICI BANK

Full text

Figure

Related documents

We highlight the potential of selective inhibitors of endocannabinoid metabolism, directed at fatty acid amide hydrolase and monoacylglycerol lipase, to reduce anxiety and

For NAGase, all three plots had significantly different enzyme activities, with the highest activity at prescribed burn plot highest and lowest at the wildfire plot (critical p

Hence, this paper estimated the carbon stocks in shaded and unshaded cocoa sys- tems at different age categories; the fields were selected from the Eastern region (E) and

[r]

Berdasarkan nilai T Statistik dari penelitian yang dilakukan menyatakan bahwa Customer Experience memiliki hubungan yang signifikan dan positif terhadap Customer

While progress in reducing under-five and neonatal mortality rates in urban areas appears to be levelling off, polices targeting rural populations and scheduled caste and tribe

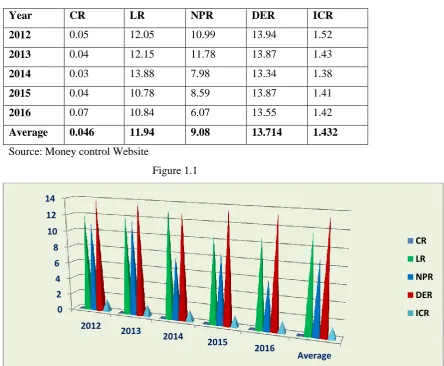

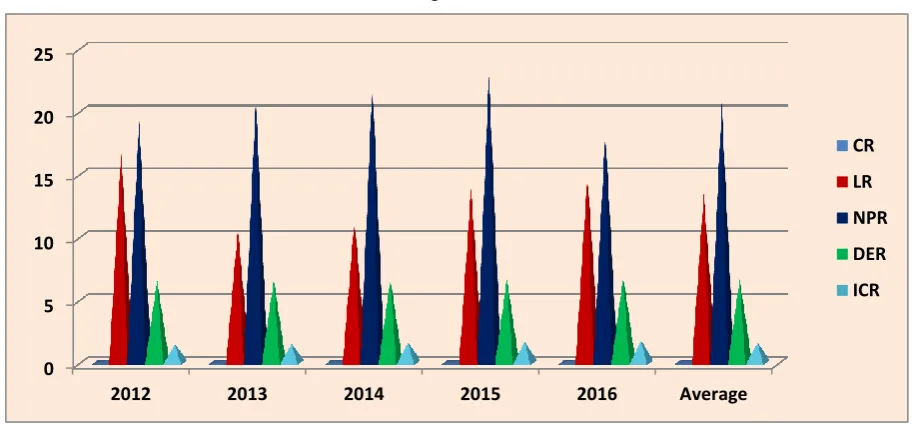

In the present study, an attempt has been made to measure, evaluate and compare the financial performance of SBI and ICICI Bank which one related to the public sector and