1

Many economic activities in an economy require transactions with other countries. We drive in buses that were manufactured in and imported from Europe or Japan; sell agricultural produce and minerals to the United States; eat at fast-food outlets that are franchises of American companies; maintain bank accounts in foreign countries; and receive remittances from family or friends living abroad.All of these activities are not, in principle, different from those which occur between regions of the same country. City dwellers consume produce grown in the country; rural folk may buy life insurance from a financial institution headquartered in the capital city. When the transaction has to cross a national border, however, there often has to be an exchange of currencies as well. French vintners don’t usually accept Myanmar kyat in exchange for their wine. We refer to the foreign currency that people need to carry out international transactions as foreign exchange.

I

NTERNATIONAL

T

RANSACTIONS

All the types of economic activities in which we normally engage in our local economies can cross international borders: the purchase and sale of goods and services, cash transfers, and the acquisition and disposal of fixed and financial assets. We can organize these transactions into convenient categories.

The most visible form of international economic transaction is the trade in tangible goods. Manufactures, agricultural produce, and mineral ores originate in one country and are used in others. While rice is grown on a large scale in only a handful of countries (Guyana, Japan, China, Thailand, India, The Philippines, amongst a few others), it is consumed worldwide. Again, perhaps a dozen countries manufacture automobiles on a large scale, but they are used in every country. Goods produced abroad and used at home are called imports; those produced locally and shipped abroad are exports.

Countries also trade services. Local insurance companies may buy re-insurance policies from larger insurers in the United States or the European Union, while local hotels provide the service of accommodation to tourists and business travelers from other countries. One type of trade in services that has become increasing popular (and, in some quarters, contentious) is the trade in business processes, such as customer service, accounting, database maintenance, and data entry, so-called “outsourcing”, that is carried out in the Caribbean, Africa, and India for customers in the United States and Britain. Other traded services include shipping, entertainment, and education.

Prepared for Principles of Economics, University of the West Indies, Mona. © Damien King, November 2012.

An increasing amount of economic activity crosses international boundaries.

Foreign Exchange

Foreign currency needed to carry out international transactions.

2

Another source of international transactions is current transfers – payments that are not in exchange for goods, services or assets. For many countries, the most visible and largest transfer is remittances. Remittances, often sent through Western Union or a similar money transfer service from the United States, the United Kingdom, and Saudi Arabia is the largest or nearly the largest source of foreign exchange earnings in many countries. Guatemala, Poland, Morocco, and Vietnam are all large recipients. Remittances originate mostly from family members who have migrated eitherpermanently or on temporary work programmes. Other current transfers include profits earned by investments abroad and remitted to home

countries and foreign aid donated by wealthy countries to governments and organizations in poorer ones.

Foreign direct investment (FDI) describes the acquisition of fixed,

productive assets in one country by a resident of another. Total of France owns petrol stations throughout Latin America; Sandals of Jamaica owns hotels in the rest of the Caribbean; Lenovo of China owns administrative offices and R&D facilities in North America; Intel of the United States manufactures in Costa Rica, Malaysia, and Vietnam. The country selling the asset the asset or is the recipient of the investment refers to it as inward FDI; the purchasing country classifies it as outward FDI. Foreign direct investment flows are massive, amounting to nearly US$1½ trillion

worldwide in 2012 and the evidence of it can be seen in the signage all over the world for the likes of McDonald’s, Holiday Inn and Santander.

Residents of one country also buy and sell financial assets, such as stocks and bonds. For one example, pension and mutual funds based in North America, the United Kingdom, and Europe often buy shares of companies in emerging markets and developing countries as part of their portfolio of investments. It is also common for investors in one country to purchase bonds issued by foreign governments, called sovereign bonds. Local residents who maintain bank accounts abroad are yet another example of an international financial asset transaction. All such acquisitions are referred to as portfolio investments.

The final category of international transactions is the acquisition and sale of official reserves by a country’s central bank. The net international reserves are usually held in United States dollars, but some is also held in euros, British pounds, and Japanese yen. In 2012, for example, the Brazilian central bank was holding the equivalent of some US$380 billion in official reserves. Whenever central banks acquire or dispose of reserves, there is an international currency transaction.

T

HE

B

ALANCE OF

P

AYMENTS

All of a country’s external dealings, such as the ones outlined above, are accounted for in its balance of payments – the official record of a country’s international transactions. If the transaction generates an inflow of foreign exchange to the country, it is deemed a credit; if it results in an outflow of foreign exchange, it is recorded as a debit.

Exports of goods earn foreign exchange and so are a credit in the balance of payments while imports use foreign exchange and are a debit. The

difference between exports and imports of goods is referred to as the merchandise trade balance or more simply as the trade balance (and sometimes as net exports). Popular references to a country’s trade deficit

Balance of Payments

The official record of a country’s international transactions.

3

are referring to this balance. If credits exceed debits, a balance is said to be in surplus; otherwise, there is a deficit.When credits and debits that arise from trade in services are added to those for trade in goods, the resulting figure is the balance on goods and services. See the structure of the balance of payments in Figure 1 for a schematic view. If we include current transfers into and out of a country to the previous balance, we get the current account balance. This balance reflects the net balance of all current transactions, that is, transactions that do not give rise to a future claim by the residents of one country against another. When people make reference to the state of the balance of payments, they are often referring only to the current account.

Changes in the ownership of existing assets fall into the capital account,1 which consists of all the flows of foreign direct investment, cross-border portfolio and other investment, and changes in official foreign reserves. The residual after the debits are subtracted from the debits is the capital account balance. A typical example of a balance of payments account, that for Costa Rica, is presented in Table 1.

B

ALANCING THE

P

AYMENTS

The balance of payments account is a budget statement for a country vis-à-vis the rest of the world. It records all the payments between the residents of the country and those outside of its geographic borders. Thus, from a purely accounting perspective, debits have to match credits. Any

discrepancy between desired inflows and outflows will be matched by an undesired but recorded change in some financial assets, even only cash savings, thus ensuring that the accounts are balanced.

This budget for the whole country imposes a binding constraint on foreign exchange flows just as how your household budget imposes a limit on the spending of the household. Without depleting its savings or borrowing money, a household’s monthly spending cannot for long exceed the total of its earnings and asset sales. Similarly, in the absence of depleting its reserves or international borrowing, the foreign exchange spent by a country is limited by its foreign exchange earnings and FDI and portfolio inflows.

Since the sum of all the debits and credits in the overall balance of payments must be zero, it follows that, having dichotomized the accounts into current and capital accounts, then the balance on any one of those two must be matched by an equal but opposite balance on the other. In other words, if there is deficit on the current account, there must be a surplus of equal size on the capital account. The foreign exchange to finance a current account deficit, for example, must be coming from somewhere.

Alternatively, if the country has experienced a capital account surplus, then the surplus money must have gone somewhere, and that somewhere is necessarily to fund the excess of outflows over inflows in the current account.

Notwithstanding the ex ante equality of inflows and outflows, since the decisions to import, export, send remittances, keep a foreign bank account, and invest abroad are all made independently by different people, there is no a priori reason why, at any particular exchange rate, desired inflows have to match desired outflows.

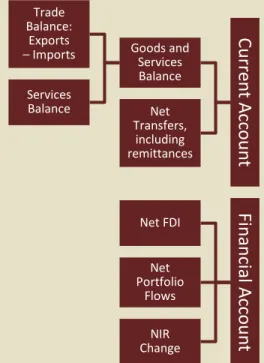

C

ur

ren

t

A

cc

ou

n

t

Goods and Services Balance Trade Balance: Exports –Imports Services Balance Net Transfers, including remittancesFin

an

ci

al

A

cc

ou

n

t

Net FDI Net Portfolio Flows NIR ChangeFigure 1: The Structure of the Balance of Payments

Goods, Credit (Exports) 4,932

Goods, Debit (Imports) 11,868

Trade Balance -6,935

Services, Credit 6,644

Services, Debit 1,624

Services Balance 5,021

Goods & Services Balance -1,914

Transfers, Credit 1,023

Transfers, Debit 1,907

Net Transfers -885

Other (net) 604

Current Account

-2,195

Direct Inv., asset acquisition 58

Direct Inv., liability incurrence 2,176

Net Foreign Direct Invest. 2,118

Portfolio, Net asset acquisition -259

Portfolio, Net liability incurrence 5

Net Portfolio Investment 263

Other Investment Net -203

Reserve Assets 132

Errors and Omissions -279

Other 185

Other (including Reserves) -165

Financial Account

2,217Capital Account, Net -22

Table 1: Balance of Payments Accounts, 2011, Costa Rica, US$m.

4

A country’s policy-makers can choose to peg their exchange rate to a major currency, say, the U.S. dollar or the Euro, fixing the exchange rate at a particular level. In such a case, the central bank has to be prepared to either provide any excess foreign exchange needed or alternatively, accumulate all excess foreign exchange inflows.If the central bank is not prepared to provide or absorb any imbalances, then the exchange rate will have to float, rising and falling to bring desired inflows and outflows into approximate balance. In order to gain an understanding of how that works, we need to first understand the difference between the nominal and real exchange rate.

N

OMINAL AND

R

EAL

E

XCHANGE

R

ATES

One of the factors that differentiates cross border transactions from those within a country is that cross border economic activity usually requires a change of currency. In order for most consumers in the world to drive a Japanese car, the person or firm responsible for the importation has to get their hands on the foreign exchange with which to pay for the car. The Japanese seller is unlikely to accept Angolan Kwanzas, Icelandic Kronas, or Philippine Pesos in exchange for the car. And even if he does, he will promptly offer it up in exchange for a currency that is more useful to him, such as his own country’s Yen or an international currency such as the Euro. Either way, someone involved in the trade has to conduct a currency transaction.

For this reason, changes in the exchange rate are of critical importance to many economies, and it is therefore important to understand the factors that influence such changes. Before we can do so, though, we need to understand the difference between the nominal exchange rate and the real exchange rate.

The nominal exchange rate is the price of one currency in terms of another. It therefore provides a relative price at which to exchange money in one currency into its equivalent amount in another. It is conventional to define exchange rates as the cost in domestic currency of buying one United States dollar. So, for example, the exchange rate between Chilean Pesos and the U.S. dollar is expressed as 480 Pesos to the dollar.

When the domestic currency depreciates, it loses value relative to other currencies. It will therefore require more of the now depreciated domestic currency to purchase a U.S. dollar. For example, a depreciation of the Chilean Peso would have occurred if, instead an exchange rate of 480 Pesos to the dollar, it required 500 Pesos to buy a U.S. dollar.

The real exchange rate measures the price of one country’s products in relation to another – not how many Malaysian Ringgits are required to purchase a U.S. dollar, but how many Malaysian Tiger beers it would take to buy a bottle of American Budweiser. Suppose a Budweiser in the U.S. sells for US$2; the exchange rate for Malaysian Ringgits is RM3 to the dollar; and a bottle of Tiger beer in Malaysia is worth RM6. Then we can work out that, since the cost of the Budweiser in Ringgits is RM6 and one bottle of Tiger can fetch RM6, then one Tiger is the equivalent of one Budweiser. Exchange Rates are usually defined in

terms of a currency’s equivalence to one U.S. dollar.

Nominal Exchange Rate

The price of one currency in terms of another.

Real Exchange Rate

The price of one country’s products in relation to that of another.

5

If the American price of a Budweiser rises, or the number of Ringgits per dollar rises (a nominal depreciation), or the price of a Tiger in Malaysia falls, it will then require more Tigers to be the equivalent of a Budweiser. The Tiger will have depreciated in value. That is, relative to Budweisers, Tigers have become cheaper. Similarly, there will have been anappreciation, Tigers will be more valuable in terms of Budweisers, if any of the following happens: the price of a Budweiser falls, the exchange rate falls, or the Ringgit price of a Tiger rises.

While we have used a single product to illustrate the concept of the real exchange rate – the amount of Tiger required to buy a Budweiser – the concept applies to the broad range of products produced by one country in relation to the equally broad range (but likely consisting of different products) produced by the other country. Thus, a country experiencing a real depreciation will observe its own products are generally becoming cheaper relative those of its trading partners.

A

R

EAL

E

XCHANGE

R

ATE

F

ORMULA

The idea behind the real exchange rate can be captured by a simple formula. 𝑟𝑒𝑎𝑙 𝑒𝑥𝑐ℎ𝑎𝑛𝑔𝑒 𝑟𝑎𝑡𝑒 =𝑛𝑜𝑚𝑖𝑛𝑎𝑙 𝑒𝑥𝑐ℎ𝑎𝑛𝑔𝑒 𝑟𝑎𝑡𝑒 × 𝑓𝑜𝑟𝑒𝑖𝑔𝑛 𝑝𝑟𝑖𝑐𝑒 𝑙𝑒𝑣𝑒𝑙

𝑑𝑜𝑚𝑒𝑠𝑡𝑖𝑐 𝑝𝑟𝑖𝑐𝑒 𝑙𝑒𝑣𝑒𝑙

Let’s see how this expression can help us to understand how the real exchange rate can change. Suppose the nominal exchange rate and the foreign country’s price level both remain unchanged, so the numerator of the fraction on the right side does not change in value. If at the same time, however, the home economy experiences inflation, then the domestic price level in the denominator will take on a larger value. With a larger

denominator, the entire ratio will be smaller, so the real exchange rate will have a lower value, reflecting that it will now require fewer domestic goods to procure a given amount of foreign goods. There will have been an appreciation of the domestic currency, but in real terms only.

Alternatively if the domestic price level remains unchanged but either the nominal exchange rate or the foreign price level in the numerator rises, then the real exchange rate will have risen – a real depreciation of the currency. It will then require more domestic output to buy a given amount of foreign products.

Note that if the nominal rate is stuck at any particular value, then figuring out what is happening to the real exchange rate is simply a matter of comparing the changes in the two price levels. If, for example, both countries are experiencing inflation but the local inflation rate is higher than the foreign one, then the denominator is expanding faster than the numerator so the real exchange rate is falling – a real appreciation.

R

EAL

E

XCHANGE

R

ATES AND

T

RADE

Like any consumption choice, a person’s choice between consuming a domestically produced product and one that is produced abroad will be influenced by a large number of factors, including tastes, culture, and the level of the consumer’s income. And as we have already seen in our discussion of demand, in addition to those considerations, the price of any particular good or service relative to others will also be a key determinant.

Real Exchange Rate: How much Malaysian beer does it take to buy an American beer?

6

When such a comparison is made between a domestically produced product and one that originates in another country, it is the real exchange rate, and not the nominal rate, that reflects the relative price of the two products. To see the role of the real exchange rate in practice, consider a typical resident of the Tuaran district in Malaysia as he contemplates his beer purchasing decision. In choosing between the local Tiger brand and an imported Budweiser from the United States, his preference for the sweeter taste in the imported lager could be a consideration, as perhaps will his cultural affinity for the local brew. In addition, the relative price of the two products when measured in local currency, the real exchange rate that is, will also be a factor.Suppose our Tuaran beer consumer currently splits his purchases between the two brands. Now suppose there is a change in the relative price of the two products. While the U.S. dollar price of a Budweiser rises by 3 percent, say, the Malaysian Ringgit price of a Tiger may have risen by 10 percent. Meanwhile, the nominal exchange rate remains unchanged. The combined effect of all the above will be to make Tigers more expensive relative to Budsweisers and Budweisers relatively cheaper compared to Tigers. In other words, there has been a real appreciation of the Malaysian currency. The typical consumer is likely to respond to this relative price change by reducing his consumption of the now relatively more expensive Tiger and substituting for it the now relatively cheaper Budweiser. Since many consumers will do the same, imports of Budweiser into Malaysia will rise. And since consumers will be carrying out a similar comparison over a range of products, we conclude that a real appreciation of the Ringgit leads to a rise in imports. Correspondingly, a real depreciation of the local currency, which raises the relative cost of imports, will lead to an decrease in imports. Consumers outside of Malaysia will also notice the change in relative costs. Beer drinkers in Bangladesh, for example, are also likely to respond to the higher cost of a Tiger relative to a Budweiser by shifting consumption from the Malaysian brand to the American one. Since Tiger is not brewed locally in Bangladesh, the reduced consumption of the brand in favour of

Budweiser will represent a reduction in export demand for the Malaysian-produced product. So the real appreciation of the Malaysian currency also promotes a fall in Malaysian exports.

These changes in imports and exports that result from consumption

decisions are reinforced by decisions on the production side of the economy as well. After a real appreciation, a Malaysian brewer will get more revenue for beer sold at home compared to beer exported to, say, the United States. He will therefore want to shift his production capacity from producing for the export market towards producing for the local market. As he does so, exports will fall. Similarly, American brewers will now be more inclined to send product to Malaysia where beer is fetching a relative higher price than at home. So Malaysian imports rise.

The comparison of the cost of beer in the two countries is only illustrative since the influence of the real exchange rate on exports and imports does not depend on a comparison of a particular product such as beer or even of products similar to each other. The real exchange rate reflects the cost of the broad collection of goods and services produced in an economy relative those produced in other countries. And as those relative costs change,

7

consumers and producers at home and abroad will shift their consumption and sales pattern between the two economies even if the goods and services produced by the two economies are not similar.To summarize, the real value of the currency, as distinct from the nominal value, includes consideration of relative price levels in order to arrive at the relative cost of domestic goods versus foreign goods. And changes in that relative cost influences the amounts of imports and exports of a country. In particular, a real appreciation reduces net exports (that is, reduces exports while stimulating imports) while a real depreciation will have the opposite effect, increasing exports and reducing imports. The real exchange rate signals consumers and producers about how to allocate their purchases and sales between the domestic economy and the rest of the world.

T

HE

F

OREIGN

E

XCHANGE

M

ARKET

We have established that the real exchange rate is important because it affects a country’s levels of imports and exports. It also affects the volume of many other international transactions. The real exchange rate is an especially important variable in more open economies – those in which international transactions are large relative to the amount of domestic economic activity. So how the real exchange rate is determined is important.

The exchange rate is just a price – the price of consuming foreign goods (or, for foreigners, the price of consuming our goods). Prices are usually determined in markets, and in countries with flexible, market-determined exchange rate regimes, the exchange rate is determined in the market for foreign exchange.2

The foreign exchange market consists of buyers and sellers of currency all over the world trading currencies through a wide variety of institutions and media. Trading is done through commercial banks, central banks, cambios, online brokers and in some countries, informal street traders. Most of the currency trading in the world, however, is done through approximately a hundred large banks.

Only a handful of currencies are widely traded across dispersed foreign exchange markets worldwide – United States dollar, European euro, British pound, and Japanese yen. For most currencies, the vast majority of the trading in them is localized, taking place in the banks and cambios located in the home country of the currency. If a merchant in Myanmar wanted to import wine from France, he would not have much luck trying to unload his kyat with a Parisian bank in order to get the Euros he needs to pay for transaction. That currency transaction would most likely take place with a bank in Myanmar.

To represent the foreign exchange market, on the horizontal axis in the market diagram shown in Figure 2, we measure the amount of foreign currency that can be bought or sold during some time period. On the vertical axis, we show different values of the real exchange rate. The demand for foreign exchange, in exchange for the local currency, derives from the outflows in the balance of payments discussed above. If you are a resident of Papua New Guinea, for example, it derives from the

8

desire to buy Korean cars, invest in Japanese stock, service European creditors, and remit profits to Australian business owners. All the activities in the balance of payments that potentially generate an outflow of foreign exchange is a part of the demand side of the foreign exchange market. The demand for foreign exchange, being in part a derived demand of that for imports, will be affected by the real exchange rate. Since a rise in the real exchange rate (a currency depreciation) reduces the demand for imports, it therefore reduces the demand for foreign exchange. For this reason, on the diagram of the foreign exchange market in Figure 2, we show the demand curve for foreign exchange as downward-sloping. Thedownward slope captures the idea that, as the real exchange rate rises, the quantity of foreign exchange demanded falls.

The supply of foreign exchange is made up of the inflows in the balance of payments – from the desire of the rest of the world to buy local crops and manufactures, send remittances, take a stake in the local stock market, and lend money to the government. We have already shown that as a rise in the real exchange rate raises the price of foreign goods and services relative to domestic ones, exports will rise. Since exports are paid for by foreigners who pay in foreign exchange to the exporting country, the quantity of foreign exchange supplied will be greater. So a rise in the real exchange rate ultimately results in a greater amount of foreign exchange being supplied, Consequently, the supply of foreign exchange curve shown in Figure 2 slopes upward, reflecting the positive relationship between the real exchange rate and quantity of foreign exchange supplied.

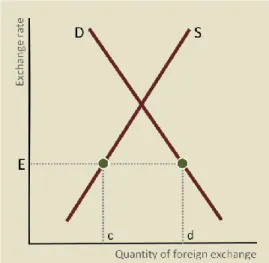

If the current level of the real exchange happens to be such that the inflows of foreign exchange from exports, remittances, and inward foreign direct investment (quantity supplied) exceed the outflows for imports, debt servicing, and the like (quantity demanded), then foreign exchange traders, rather than accumulate unsold foreign exchange, will lower the nominal exchange rate so as to attract purchasers of foreign exchange. This is illustrated by exchange rate E1 in Figure 3 at which the quantity of foreign exchange supplied, “b”, exceeds the quantity demanded, “a”. This is no different from when shopkeepers reduce prices to attract more customers. The reduction in the nominal rate would have to be sufficient to

compensate for any changes in the two countries’ price levels to ensure that the real exchange rate falls. (Review the real exchange rate formula above if the previous sentence is not sufficiently clear.)

Conversely, if the current real exchange rate is such that outflows (quantity of foreign exchange demanded) exceeds inflows (quantity supplied), then forex traders will want to raise their nominal exchange rate rather than wait until their foreign exchange float runs out and they have no more foreign exchange to sell. Exchange rate E2 in Figure 3 represents this possibility where the quantity supplied is only “c” and the quantity demanded is the larger amount “d”. Upping the nominal rate, other things remaining unchanged, will raise the real rate.

Since excess supply of foreign exchange induces the real exchange rate to fall and excess demand induces it to rise, the real exchange rate will generally drift towards the market-clearing equilibrium – exchange rate E0 in Figure 3 – at which inflows and outflows are equal.

Figure 3: Determining the equilibrium real exchange rate

9

D

ISTURBANCES IN THE

M

ARKET

The demand for and supply of foreign exchange is affected by much else besides the exchange rate. As income levels change in a country, for example, consumption will rise or fall along with it. Since a typical household’s consumption will include some foreign goods, and even domestically produced goods and services will use some inputs produced abroad, any change in the level of income will induce a corresponding change in the amount of imports. The increased demand for foreign exchange necessitated by a higher level of imports is represented on the market diagram as an outward (or rightward) shift of the foreign exchange demand curve.

In a similar manner, rising income abroad, in the economies of a country’s trading partners, will induce higher consumption there, which consumption will include some commodities and inputs that are produced here, raising exports and therefore the supply of foreign exchange. In the this way, higher incomes abroad mean an outward shift of the supply of foreign exchange curve.

One way in which the rapidly rising incomes in China is being spent is on holidays abroad. So nearby countries will experience an increase in visits by Chinese tourists, boosting the supply of foreign exchange in the countries being visited. In Figure 4, this situation, applicable to the countries receiving Chinese tourists such as the Pacific Islands, is shown as a rightward shift of their foreign exchange supply curve. As illustrated, the additional inflows will create an excess supply that will propel the real exchange rate downwards in order to encourage potential foreign exchange users to purchase the newly earned foreign exchange.

Interest rates also influence the demand for and supply of currencies. The rate of interest in a country indicates the returns to be had from holding financial investments in that country, such as lending money to the

government. So if domestic interest rates were to fall, say, the return on the loans may not compensate some lenders for the perceived risk of lending to the government. These investors would therefore want to shift their financial investments to other countries whose interest rates may not have fallen and who therefore now offer a comparatively better deal. As the financial capital shifts, it requires increasing the demand for foreign exchange. As a consequence, then, of lower domestic interest rates, the demand for foreign exchange will rise and consequently so will the exchange rate, depreciating the currency.

Anything, therefore, that causes a change in the demand for or supply of foreign exchange will have a consequence for the level of the real exchange rate. A bumper harvest of a major export crop will boost foreign exchange earnings, an outward shift of the supply curve, and cause the exchange rate to fall. An increase in external borrowing by the government will also have the same effect, as the government has to sell the borrowed foreign

exchange in order meet its domestic spending obligations in local currency. In a non-oil producing country, a rise in the world oil price will raise the bill for importing oil and so increase the demand for foreign exchange, driving up the exchange rate.

Figure 4: An Increase in the Supply of Foreign Exchange

10

P

URCHASING

P

OWER

P

ARITY

The demand and supply model of the foreign exchange market, which is based on foreign exchange earnings and outflows, helps us to understand how the real exchange rate responds to changes in inflows and outflows of foreign exchange in the short run. But what about the factors that

determine those flows? If we have that information, we will understand what factors drive the real exchange in the long run.

The discussion will also provide an explanation for the long run secular depreciation of the nominal exchange rate observed in many developing countries. To procure one U.S. dollar took only eight Jamaican dollars in 1990 but by 2013 required more than 13 times as much Jamaican currency to buy the same dollar? It is certainly not because the real exchange rate has changed by that multiple over the period. Indeed, the real exchange has hardly changed from the value it had nearly a quarter century earlier. To explain movements in the nominal exchange rate, even when there is no corresponding change in the real rate, we turn to the theory of purchasing power parity.

A

RBITRAGE AND THE

L

AW OF

O

NE

P

RICE

Arbitrage is the profitable exploitation of different prices for the same commodity in different markets. Fruit vendors do this when they purchase fruit cheaply in the countryside and then bring it to the city where it can be sold at a higher price. Currency traders also exploit opportunities for arbitrage. If the pound is selling for $1.50 in New York and $1.45 in London, an arbitrageur can profit by simultaneously purchasing pounds in London and selling them in New York. Arbitraging mangoes is no different from doing so with currencies.

Because they are always persons willing to take advantage of arbitrage opportunities, such opportunities do not persist. The arbitrageurs increase the demand for the commodity in the market where the price is lower, pushing the price up, and increase the supply in the market in which the price is higher, driving the price down. These forces should continue until the two prices are unified, or at least until the difference between them is sufficiently small such that the cost of transportation between the markets will absorb any profit remaining to be had from arbitraging further. Arbitraging underlies the law of one price, which states that a commodity cannot have different prices persisting in different markets if trade can take place between those two markets. In practice, of course, a price difference can persist as long as the difference is less than the cost of transportation between the two markets. Persistent price differences for the same commodity may also persist if the difference reflects other conditions that differentiate the two markets, such the convenience or security of shopping in one place versus another. But arbitrage will always eliminate any price differences that are greater than those considerations can justify.

The law of one price operates only weakly between different countries. Governments erect artificial barriers to trading commodities, such as import tariffs and quality regulations. Additionally, it is inconvenient and costly to transport some commodities, such as carbonated sodas across far distances. And many products are not tradable at all, such as housing and

Law of One Price

A commodity can have only one price. Price variation in markets between which there is trade will be arbitraged away.

Arbitrage

The exploitation of price differences between difference markets in the same commodity.

11

haircuts. For these reasons, the forces of arbitrage exhibit only a weak influence across international borders, and for particular commodities large price differences can and do persist between countries.T

HE

R

EAL

E

XCHANGE

R

ATE IN THE

L

ONG

R

UN

However weak, international commodity arbitrage does exert some influence on relative prices in different countries, however slowly. This influence will be evident, not so much for individual items, but more so for the general price level and only over the long run. And it operates through changes in the nominal exchange rate.

If, at the current level of the nominal exchange rate, goods are generally substantially cheaper abroad than they are in the home country, an arbitrage opportunity will be present. Even if inflows and outflows of foreign exchange are roughly in balance to begin with, before long, consumers will seek to take advantage of cheaper imported goods. The growing demand for imports will simultaneously be a growing demand for foreign exchange, as illustrated by the outward shift of the demand curve for foreign exchange in Figure 5. At the same time, the relative costliness of domestic production will be recognized by consumers abroad as well who will therefore diminish their purchases of our exports, simultaneously reducing the supply of foreign exchange (not shown).

In this way, whenever there is a substantial divergence between the cost of goods at home and abroad, trade flows and the corresponding demand for and supply of foreign exchange will drive the real exchange rate towards the one that equates the purchasing power of a given amount of money in the two currency areas, that is, towards the exchange rate that achieves purchasing power parity, or PPP.

Suppose a shopping cart’s worth of supermarket items costs 300 Shekels in Tel Aviv while the same grocery list can be filled in New York for $75. The comparison implies that the exchange rate that would equate the

purchasing power of 300 Shekels in both countries is 4 Shekels to US$1. That is the PPP exchange rate.

But suppose further that the current exchange rate is actually 3.5 Shekels to US$1. The PPP theory suggests that, as consumers seek to take advantage of the lower prices of American goods, Israeli imports will rise and over time this will depreciate the Israeli Shekel towards 4 Shekels to US$1.

T

HE

N

OMINAL

E

XCHANGE

R

ATE IN THE

L

ONG

R

UN

For pairs of countries that both have low inflation rates, small changes in their rates of inflation, and therefore equally small changes in the PPP exchange rate, do not seem to have discernible effects on the nominal exchange rate between their currencies, especially in the short run. But for countries that allow their inflation rates to depart substantially from that of their trading partners, the foreign exchange market does not tolerate significant departures from PPP for very long. Before long, the difference between the two countries’ inflation rates is likely to result point in a compensating movement in the nominal exchange rate in order to restore purchasing power parity.

Figure 5: What happens when your country’s trading partner has a lower cost of goods?

PPP Exch. Rate =

𝑙𝑜𝑐𝑎𝑙 𝑐𝑜𝑠𝑡 𝑜𝑓 𝑔𝑜𝑜𝑑𝑠

𝑓𝑜𝑟𝑒𝑖𝑔𝑛 𝑐𝑜𝑠𝑡 𝑜𝑓 𝑔𝑜𝑜𝑑𝑠

= 300 𝑆ℎ𝑒𝑘𝑒𝑙𝑠

𝑈𝑆$75

12

Since the PPP exchange rate is the ratio of the cost of goods in the local market to that in the country of the other currency, then the PPP rate should, on average and in the long run, rise at a rate equal to the difference between the inflation rates at home and in the other country. A large inflation differential will produce a rapidly rising PPP exchange rate and therefore an equally rapidly rising actual exchange rate.As an example of purchasing power parity in action, Figure 6 shows the growth of the nominal exchange between Jamaican dollars and the U.S. dollar from 1990 to 2012 (the amber line) as it moved from eight Jamaican dollars for a U.S. dollar all the way up to 91. The darker-coloured line beneath shows what the exchange rate would have been if the difference between the American and Jamaican inflation rates (that is, PPP) had been the only influence on it. Since the two lines are closely aligned, it shows that the nominal exchange rate has not departed by much from what PPP alone would have dictated. We conclude that purchasing power parity has been the primary factor behind the substantial increase in the nominal exchange rate in Jamaica over the last two decades.

E

XCHANGE

R

ATE

R

EGIMES

Countries differ in the rules and policies that govern the behaviour of the foreign exchange market. At the extremes of the spectrum of exchange rate regimes are flexible exchange rates and pegged exchange rates.

F

LEXIBLE

E

XCHANGE

R

ATES

A flexible exchange rate regime is one in which the exchange rate is allowed to change based on market forces. Each commercial bank, cambio and trader adjusts its buying and selling rate for foreign currency to reflect the relative volumes of purchases and sales occurring on a given day.

From the perspective of the broader economy, this flexibility in the exchange rate ensures that inflows and outflows of foreign exchange are constantly being brought into alignment. Excess demand stimulates a depreciation which diminishes the excess demand; Excess supply results in an appreciation which similarly reduces the excess. In this way, the market ensures that inflows and outflows of foreign exchange are kept closely aligned.

As a result of this alignment, the central bank never needs to get involved in the market. It can choose to do so whenever it feels that it would like to increase its own reserves of foreign exchange, in which case it will purchase foreign exchange, or if it decides to reduce its holdings, in which case it would sell. But there would be no obligation for the central bank to enter the market if it were satisfied with its current level of international reserves.

Flexible exchange rate regimes have the advantage of providing a quick and automatic response to external shocks that affect a country. Suppose demand for a country’s exports were to decline. In the absence of an automatic response from the exchange rate, the country’s production would have to contract, likely resulting in unemployment and economic hardship. With a market-determined exchange rate, however, the reduction in exports will automatically instigate a currency depreciation, which in turn

1 5 25 125

1990

2000

2010

Figure 6: Nominal and PPP Exchange Rates, Jamaican Dollar to U.S. Dollar

Nominal Exchange

Rate

PPP Exchange

13

will stimulate higher demand for domestic goods by both foreigners and locals, automatically mitigating the fall off in exports. Flexible exchange rates acts as a “shock absorber” for events in the global economy. Most of the large, developed countries have flexible regimes. The United States dollar, the British pound, The Japanese Yen, and the Australian dollar are all so-called “floating” currencies whose exchange rates move up and down on a daily basis. Many developing and emerging countries also have flexible exchange rates for their currencies. Examples include the Georgia lari, the Papua New Guinean kina and the Zambia Kwacha.F

IXED

E

XCHANGE

R

ATES

An alternative to having market forces adjust the exchange rate every time there is a need for such is to fix, or “peg”, the exchange rate to another currency. Nepal’s rupee has been pegged at a value of 1.6 rupees to the United States dollar since 1993.

Under a fixed exchange rate regime, the central bank has to be willing to trade foreign exchange at that fixed rate. It is the central bank’s willingness and readiness to do so that actually fixes the rate. With the central bank standing by ready to trade, no buyer will pay anyone else a higher rate and no seller will accept a lower rate.

Since the central bank is obligated to trade foreign exchange at the pegged rate, any discrepancy between the amount the market wants to sell and what it would like to buy has to be made up by the central bank. At any point, therefore, unless the pegged rate just happens to be one that equates inflows and outflows, the central bank will find its foreign exchange reserves either accumulating or depleting. Figure 7 shows an exchange rate peg at which the quantity of foreign exchange demanded exceeds that supplied. The central bank would have to deplete its reserves by an amount equal to c-d each period to make up the difference. Neither situation, accumulation or depletion, can proceed indefinitely, so countries with fixed exchange rates occasionally have to adjust the peg to a different level. Fixed exchange rate regimes that can be maintained at the same peg over long periods, such as Panama’s balboa (unchanged since 1903) or Swaziland’s lilangeni (since 1974) have the advantage of minimizing exchange rate uncertainty that can be detrimental to investment planning in open economies. Thus, countries with successful pegged regimes tend to have higher rates of investment.

While much less popular than it used to be, fixed exchange rate regimes are sill the norm in many parts of the world. Hong Kong’s dollar, Lesotho’s loti, Latvia’s lats, and Saudi Arabia’s riyal are all pegged to one or another of the world’s major currencies.

One particularly stringent form of a fixed regime is the currency union, in which two or more independent sovereign nations will choose to share a single country. The euro of the European Union is one example; the Eastern Caribbean dollar amongst the Windward and Leeward islands in the Caribbean is another. Since there is a single currency, there is no option for the exchange rate to change between a country and its neighbours in the union short of the country exiting the currency union.

Figure 7: A pegged exchange rate that requires the central bank to supply foreign exchange to the market.

14

1 The IMF splits what the rest of the world calls the capital account into two parts: the financial account and the capital account, with most of the transactions falling into the financial account.

2 In some countries, the nominal exchange rate is “pegged” to the value of another currency and is not allowed to vary in order to allow for easy adjustment of the real exchange rate.