TO START OR NOT TO START? AN EMPIRICAL EXAMINATION OF THE DECISION TO START A BUSINESS

Justin Kelly Kent

A dissertation submitted to the faculty at the University of North Carolina at Chapel Hill in partial fulfillment of the requirements of the degree of Doctor of Philosophy in Business Administration from the Kenan-Flagler Business School in the Strategy and Entrepreneurship

area.

Chapel Hill 2020

Approved by: Atul Nerkar

Christopher Bingham Isin Guler

ABSTRACT

Justin Kelly Kent: To Start or Not to Start? An Empirical Examination of the Decision to Start a Business

(Under the direction of Atul Nerkar)

The decision to start a business is a fundamental issue in entrepreneurship research and has significant economic implications for policymakers and individuals. In this dissertation, I build on the entrepreneurial decision-making literature by exploring certain contextual and cognitive factors associated with the decision to start a business.

Using data collected from potential entrepreneurs over four years (2015–2019), I analyze how work experience, motivation, and cognitive style influence decisions to engage in

entrepreneurial action in two situations: (a) entrepreneurship through acquisition decision context and (b) forming a new business. I find that experience length, experience type, implicit

motivations of status, and cognitive style are associated with the decision to proceed with an entrepreneurial opportunity.

Dedicated to my wife, Jami,

ACKNOWLEDGEMENTS

This dissertation is the culmination of many years of effort spent on my behalf by family, faculty, and fellow PhD students. It is an honor to express my gratitude to those who have helped me along my doctoral journey.

First and foremost, I want to thank my wife, Jami. With her encouragement, I left a stable but unfulfilling career to pursue my dream of becoming a professor. She has supported me from the beginning as I struggled to adjust to the rigors of academia including preparation for

comprehensive exams, the job market, and dissertation defense. She was always ready with words of encouragement and love whenever I was nervous or discouraged. Without complaint, she took on a larger portion of the parenting responsibilities while I worked late and on

weekends. Certainly, I could not have done this without her.

I also want to thank my wonderful girls, Emma, Macie, Annie, and Livvy. So many times they were patient when I had to work on Saturday or teach in the evenings. The prospect of spending time with them also motivated me to be efficient at the office. We made a point to spend time together as a family, however infrequently, during my time as a doctoral student. It meant lunches in the McColl cafeteria, and no screen weekend trips and Sunday family time. I always felt energized for work after spending time with these wonderful little people.

ultimately sparked my interest in research. Not only did Atul teach me how to be an effective instructor, he also suggested we work together after he learned of my frustration with research. There‘s a good chance I would not have finished my PhD without Atul‘s help. I cannot thank him enough for his time, including the Saturdays and Sundays he spent helping me prepare for the job market and dissertation defense, and his patience as I learned the art of research. I consider Atul a lifelong friend and mentor and look forward to working with him on future projects.

I would also like to thank the other members of my dissertation committee, Chris

Bingham, Isin Guler, Hugh O‘Neill, and Elad Sherf, for their input and support. Their input and

timely feedback have been of significant help throughout the dissertation phase and my

development as a scholar. Chris and Hugh, in particular, met with me early and often during my time as a doctoral student and have had a profound effect on research interests and how I

approach research in general.

Finally, I thank my parents, Kelly and Connie Kent. As I was growing up, they fostered an environment at home that valued education, self-improvement, and hard work. I‘m sure neither could have predicted my pursuit of a doctorate given my apathetic attitude and proclivity to cut class in high school. I credit my father for my interest in entrepreneurship. As a young college student, I approached him for help in starting my first venture. He was highly willing to help me get started and was always ready to help if needed. Without his support I would not have experienced entrepreneurship and probably would have chosen a different career path.

TABLE OF CONTENTS

LIST OF TABLES ...x

CHAPTER 1: INTRODUCTION ...1

CHAPTER 2: LITERATURE REVIEW AND RESEARCH QUESTIONS ...4

Organic Form of Entrepreneurship ...6

Inorganic Form of Entrepreneurship ...6

CHAPTER 3: THEORY AND HYPOTHESIS DEVELOPMENT ...19

CHAPTER 4: DATA AND METHODOLOGY ...30

Measurement of Dependent Variable-Organic Entrepreneurship...30

Measurement of Dependent Variable-Inorganic Entrepreneurship ...31

Measurement of Independent Variables ...36

Control Variables ...39

Model Specification ...40

CHAPTER 5: RESULTS ...42

CHAPTER 6: DISCUSSION AND CONCLUSION ...46

Contributions...46

Limitations and Future Research ...50

Implications...52

LIST OF TABLES

Table 1: ETA, LBO, and Franchise Comparison ...53

Table 2: Study 1 Descriptive Statistics and Correlation Table ...54

Table 3: Study 1 Main Results ...55

Table 4: Course Outline and Questions used to Evaluate Cognitive Factors ...56

Table 5: Study 2 Descriptive Statistics and Correlation Table ...57

CHAPTER 1: INTRODUCTION

Why do some individuals and not others become entrepreneurs? This fundamental question in entrepreneurship research motivated early scholars from a wide range of disciplines including economics, sociology, and psychology to investigate the differences between

entrepreneurs and non-entrepreneurs (McClelland (1961; Collins and Moore (1964; Brockhaus (1975; Wilken (1979; Baumol (1993; Stinchcombe (1965). These avenues of research have yet to find a strong unifying explanation that would predict the likelihood of an individual‘s becoming an entrepreneur (Gartner (1988).

Given the absence of a unifying explanation, an associative rather than causal approach can help us understand the decision to become an entrepreneur. For example, medical

researchers found that the incidence of cholera was higher in communities that collected water from polluted sources than communities that collected water from wells (Cameron and Jones (1983). This initial finding by John Snow was based on associations that eventually led to the development of the field of epidemiology. In this dissertation, similar to epidemiological researchers, I examine the relationship between factors that may influence, though not cause, individuals to become entrepreneurs (MacMillan and Katz (1992).

and Jemison (1991), entrepreneurship scholars have focused attention on organic new venture creation while neglecting the inorganic mode of entrepreneurship (Hunt and Fund (2012).

In this dissertation, I explore both organic entrepreneurship and inorganic

entrepreneurship and how several contextual and cognitive factors are associated with a decision to take entrepreneurial action. Through two studies, I explore how an individual‘s previous experience and cognitive characteristics are associated with taking entrepreneurial action. For both studies, I create a unique dataset of aspiring entrepreneurs whom I follow over time. Because almost anyone can become an entrepreneur, finding a suitable risk set from which to study entrepreneurship can be challenging (Shaver, Gartner, Crosby, Bakarlarova, and Gatewood (2001). This approach mitigates these challenges by identifying individuals who have

demonstrated their interest in entrepreneurship before the study was initiated.

In both studies, I use a non-experimental field survey research design that does not manipulate independent variables but measures these variables and tests their associations using statistical methods. In study one, I use a longitudinal approach to study how an individual‘s experience, cognitive style, and confidence are associated with actual new business formation. The second study builds on the first but uses a cross-sectional field survey to examine how work experience—both type and duration—and motivation are associated with the decision to proceed with an ETA opportunity. ETA is an understudied phenomenon, and this study provides some needed insight into the characteristics of individuals who would proceed with this alternative approach to entrepreneurship.

information on my sample, data, and methodology in chapter four and explain my results in chapter five. Finally, I provide a discussion on my findings, identify limitations, and identify future research opportunities in chapter six.

This dissertation contributes to the entrepreneurship literature in several ways. First, I address one of the primary questions in entrepreneurship: Why do some individuals pursue entrepreneurial opportunities while others do not? I show that both cognitive factors, such as motivations and cognitive style, and contextual factors, such as prior work experience and age, influence the decision to take entrepreneurial action.

Second, I shed light on ETA as an alternative path to entrepreneurship. Despite the large role it plays in economies, ETA has thus far been understudied by researchers. To my

knowledge, this study represents the first empirical analysis on ETA and provides a starting point for future research.

Finally, I demonstrate how linguistic measures based on computer-aided text analysis (CATA) can be used to measure cognitive factors. Psychometric measures of cognitive constructs can be biased by question-wording, order of questions, and respondents‘

CHAPTER 2: THEORY AND RESEARCH QUESTIONS

For many years, scholars have debated the definition of ―entrepreneurship‖ (Brockhaus and Horowitz (1985; Carsrud, Olm, and Edy (1985; Gartner (1990). For example, economists have described entrepreneurs as risk-takers (Mill, 1848), uncertainty bearers (Knight (1921), innovators (Schumpeter (1934), and arbitrageurs (Kirzner (1973). Other research has explored the effects of entrepreneurship on economies (Acs and Szerb (2007; Wennekers and Thurik (1999) and communities (Barth (1963; Austin, Stevenson, and Wei-Skillern (2006), and still many others have explored discovery, evaluation, and exploitation processes (Bhave (1994; Shah and Tripsas (2007; Ajuha and Lampert (2001). More recently, Venkatraman (1997) has

integrated these perspectives into a definition that has found some consensus in the

entrepreneurship community, stating, ―How, by whom, and with what effects opportunities to create future goods and services are discovered, evaluated, and exploited (pg. 120).‖ However, the underlying assumption regarding how opportunities to create future goods and services come to fruition is grounded in de novo entrepreneurship. Except for corporate entrepreneurship, the vast majority of entrepreneurship research has focused on new venture creation as the primary mode of entrepreneurial entry while under-exploring alternative paths to entrepreneurship such as through the acquisition of an existing business (Cooper and Dunkelberg (1986; Parker and Van Praag (2012).

discovering, evaluating, and exploiting an opportunity that begins with an idea and grows from inception into an organization. Similar to inorganic growth strategies in the mergers and

acquisitions literature, inorganic entrepreneurship involves entering entrepreneurship through the acquisition of an existing organization (Haspelagh and Jemison (1991). The process of

discovery, evaluation, and exploitation are present in inorganic entrepreneurship because the entrepreneur must discover a suitable business to acquire, evaluate both the terms of a purchase agreement and their ability to successfully manage the business, and exploit the potential acquisition by creating new value from existing business systems and underutilized assets

(Stevenson, Sharpe, Roberts (2012). For example, opportunities positioned in new industries that are surrounded by a high degree of uncertainty regarding demand and design might be more attractive to organic entrepreneurs. Entrepreneurs who are comfortable with uncertainty and prefer to experiment with different business models or product innovations stand to reap substantial financial returns if they are able to establish the dominant design and become the market leader (Murmann and Tushman, 2001). They also risk failure if their assumptions about the market are wrong (Aldrich and Fiol (1994). This high-risk high-reward approach to

entrepreneurship is not for everyone. Many individuals would prefer to create future goods or services in a context where business processes have been established and uncertainty has been reduced. ETA is an alternative mode of entrepreneurship that allows individuals to exploit their human, social, and financial capital to become business owners (Parker and Praag, 2012).

clarifying ETA, or inorganic entrepreneurship, and identifying characteristics associated with a decision to proceed with an ETA transaction.

Organic Form of Entrepreneurship

Organic entrepreneurship is the act of creating a new organization to facilitate the production of future goods or services. The act of creating an organization requires the entrepreneur to recognize and correctly evaluate potentially valuable opportunities (Baron (2006), acquire financial and human resources (Shane (2003), and respond effectively to

environmental change (Brown and Eisenhardt (1997). Recognizing valuable opportunities relies on the entrepreneur‘s ability to identify situations where new goods, services, raw materials,

markets, and organizing methods can be introduced through the formation of new means, ends, or means-ends relationships (Eckhert and Shane (2003). After the decision to exploit an

opportunity has been made, the entrepreneur organizes the financial and human resources needed to develop the product or service. Financial resources most often come from the entrepreneur‘s savings (Aldrich and Ruef (2006), but external debt and equity funds can also be secured from banks and investors. If the entrepreneur does not possess the human capital needed to

successfully exploit the opportunity, they can recruit cofounders, or if sufficient financial capital is available, employees to supply the needed expertise. Finally, entrepreneurs are more likely to successfully create a business if they remain flexible with their business model and are willing to change if environmental conditions change (Eisenmann, Ries, and Dillard (2012).

Inorganic Form of Entrepreneurship

venture.1 ETA is an important part of the entrepreneurial ecosystem because it involves the revitalization of existing systems of wealth and contributes to the well-documented interplay between entrepreneurship and economic growth (Hunt & Fund (2012). Using InfoUSA reports, the Dunn and Bradstreet database, and interviews with 15 business brokers, Hunt and Fund (2012) conservatively estimate that out of 700,000 total ownership transfers in the United States (20,000–30,000 ETA transactions are completed each year representing $25–40 billion in total value. ETA‘s economic impact is likely far greater than these statistics show given Hunt and Fund‘s restricted definition of ETA.

ETA as a model of entrepreneurship is also growing in acceptance in MBA programs. Harvard, Stanford, Northwestern, University of Chicago, and other top universities offer courses in ETA for MBA students, and an annual conference has been established through a joint

partnership between the Booth-Kellogg schools of business to help facilitate best practices and connect nascent entrepreneurs with potential investors.

ETA is also important for policymakers. There is an increasing demand for capable entrepreneurs to take over existing businesses. Populations are aging in both the United States and Europe, and many small business owners do not have children who want to take over the family business (Levesque and Minniti (2011). A significant value is at risk if business owners are unable to find successors for their businesses including the loss of jobs, potential experience, and economic output. ETA provides a vehicle for succession and provides a way to preserve and renew the economic, intellectual, and cultural value contained in these aging businesses.

1

Notwithstanding the growing interest in ETA and its impact on the economy, little is known about the characteristics of potential entrepreneurs attracted to ETA opportunities. Some scholars have explored the factors that influence entrepreneurial entry mode decisions by comparing entrepreneurs who take over a business, either a family business they are associated with or an external takeover, with entrepreneurs who founded their venture (Cooper and

Dunkelberg (1986; Parker and Van Praag (2012). While these comparisons help understand the differences between start-up entrepreneurs and take-over entrepreneurs, it is difficult to study these preferences after the decision to exploit has already been made. This project complements the research on entry mode preferences by using a risk set of potential entrepreneurs to explore the factors that influence their decision to proceed or not proceed with an ETA opportunity. A Pluralistic Approach to Entrepreneurship

In their seminal work, March and Simon (1958) question the assumptions of neoclassical economics and identify individuals as boundedly rational who satisfice to cope with incomplete information, which led to the emergence of behavioral theory. I use the underlying assumptions of behavioral theory as a starting point in developing a non-causal pluralistic approach of entrepreneurship (Ripsas (1998; Fisher (2012).

Entrepreneurs must take on multiple roles to exploit an opportunity, whether organic or inorganic. First, the entrepreneur must find a suitable opportunity to pursue. Next, the

The entrepreneur as arbitrageur has roots in the Austrian tradition of economics. As opposed to the steady equilibrium world of neoclassical economics, the Kirznerian entrepreneur operates in a dynamic market where prices fluctuate in response to constantly changing supply and demand. Shortages, surpluses, and misallocated resources create opportunities for

entrepreneurs to buy when prices are too low and sell when prices are high, thus moving the market in the equilibrating direction (Kirzner (1997). Individuals can create an organization to buy undervalued assets at a low price with the intent to resell them in the future at a higher price as shown by many wealth management organizations. Alternatively, the individual can view the firm itself as an undervalued asset that can increase in value under the direction of the

entrepreneur. The act of searching for a company to purchase with the intent to sell in the future for a profit is an act of arbitrage. As a result of incomplete information, ETA entrepreneurs believe they are more aware of the market value of the target business than others, including the owners (Kirzner (1973). Put differently, ETA involves the purchase of a set of tangible and intangible assets that, as a whole, are undervalued from the entrepreneur‘s point of view. The

entrepreneur expects, in the context of uncertainty, that the value of the bundle of assets will appreciate in value over time. Purchasing an undervalued business with the expectation of reselling it in the future for a profit is the first step in value creation in an ETA opportunity. Entrepreneur as Organizer of Resources

After an arbitrage opportunity has been discovered by the entrepreneur, acquiring the business requires the entrepreneur to act as an organizer of resources (Herbert and Link (1989). The entrepreneur acquires and organizes capital from institutions and investors by raising debt and equity financing to exploit the opportunity. The entrepreneur typically believes and

use of capital than alternatives given its comparable risk profile. Variation exists within the potential future capital structures of the business. A more levered structure increases the risk to the entrepreneur and the associated cost of capital but multiplies the equity holder‘s return on investment. To efficiently organize resources, the entrepreneur must take into account the risks associated with the creation or acquisition of the business. Because of information asymmetry, the entrepreneur knows more about the quality of the acquisition and their abilities to

successfully manage the business in the future than the resource providers. Therefore, debtors and investors will require terms that reduce their risk such as collateralization of assets or flexible investment instruments. Through negotiation, the entrepreneur can create value by structuring the transaction in a way that positions them for the best chance of success. Entrepreneur as Recombinor

In contrast to the Kirznerian entrepreneur, the Schumpeterian entrepreneur recombines resources in new ways to create new opportunities that lead to market disequilibrium. The entrepreneur enacts their vision in a process of creative destruction by introducing new

products/services, entering new geographical markets, using new raw materials, implementing new methods of production, and/or organizing in new ways (Schumpeter (1934). Recombination can also occur in inorganic entrepreneurship where the innovations introduced by the

value as a Kirznerian entrepreneur through arbitrage by procuring undervalued assets with the intent to sell in the future at a profit. These undervalued assets could include the acquisition of an undervalued company and selling it in the future at a profit. They also create value as a resource organizer by assembling the debt and equity financing needed to develop or acquire the business and structuring the transaction. Finally, they create value as a Schumpeterian entrepreneur by enacting their vision for the business through recombination. Each of these mechanisms affects the motivation and choice to become an entrepreneur.

The earlier description paints a picture of the entrepreneur as an individual who is boundedly rational with incomplete information and who satisfices while engaging in arbitrage, organization, and re-combination. However, how individuals generally and entrepreneurs specifically process information and arrive at conclusions is relevant in understanding the decision to start or not to start a business (Mitchell et al. (2002; Mitchell et al. (2004; Smith, Mitchell, Mitchell (2009).

Cognitive Style

Research in entrepreneurial cognition often paints a rather unflattering picture of the aspiring entrepreneur as a brash, overconfident maverick who relies on ―gut feel‖ or intuition to decide to start a business (Anderson and Warren (2011). However, the decision to enter

entrepreneurship is non-trivial and will likely result in significant life changes for the aspiring entrepreneur which should encourage planning, analysis, and forethought. If entrepreneurs generally rely on intuition to make decisions, including the decision to start or acquire a business, how does an analytic mindset influence entrepreneurial entry?

decision-making (Hayes and Allinson (1998; Streufert and Nogami (1989). Brigham and De Castro (2003) described cognitive style as a consistent approach toward understanding and solving problems, implying that cognitive style is an enduring dimension of personality (Hayes & Allinson (1994). Cognitive style influences both individual and organizational behavior (Sadler-Smith and Badger (1998). Cognitive styles are unique and distinct from cognitive ability, suggesting that one style is not preferred over another (Witkin et al. (1977). Cognitive ability refers to general mental capability comprised of reasoning, problem-solving, planning, abstract thinking, complex idea comprehension, and learning from experience (Gottfredson (1997). In contrast, ―cognitive style reflects ‗how,‘ rather than ‗how well‘ we perceive and judge

information. It emphasizes individual traits rather than cognitive ability, focusing on ‗preferred styles‘ as opposed to ‗more is better‘ psychometric measures such as IQ‖ (Hough & Ogilvie (2005: 421).

Cognitive style has been viewed through many lenses beginning with Witkin‘s theory of field dependence-independence (FDI) (Witkin, Moore, Goodenough, and Cox (1977). FDI is grounded in education theory and measures how individuals experience their environment. Building on Witkin, industrial organizational psychology and management scholars have

explored how cognitive style influences business and management practices (Hayes and Allinson (1994). Much of the cognitive style research in industrial-organizational psychology relies on the theory of psychological types operationalized by the Myers-Briggs Type Indicator (MBTI) (Carey, Fleming, and Roberts (1989). Within MBTI, cognitive style has typically been measured by comparing and contrasting how individuals perceive and process information which is

cognitive style (Kirton (1976). KAI was developed specifically for bureaucrats and managers to measure how they approach problem-solving and decision-making. Similar to FDI and MBTI, KAI measures cognitive style on a continuum ranging from adaptive to innovative. Other conceptualizations of cognitive style include the cognitive style index (Allinson and Hayes (1996), the cognitive style indicator (Cools and Van den Broeck (2007), and the linear-non-linear thinking style profile (Vance, Groves, Paik, and Kindler (2007).

In summary, there are many similarities among the different conceptualizations of the cognitive style. Each has an analytic dimension that in some way refers to judgment based on mental reasoning and a focus on detail and an intuitive dimension that describes non-conformity, open approaches to problem-solving, and exploration (Allinson & Hayes (1996). These

contrasting styles have foundations in cognitive systems theory but differ in important ways. Cognitive systems theory identifies two methods used to process information. The first, often identified as System 1 (Kahneman (2011; Stanovich and West (2000) or Type 1 (Evans and Stanovich (2013), is intuitive (Hammond (1996), experiential (Epstein (1994), impulsive (Strack and Deustch (2004), holistic (Nisbett, Peng, Choi, and Norenzayan (2001), and automatic

Consistent with other studies of cognitive style in management and entrepreneurship (Mittenness, DeJordy, Ahuja, and Sudek (2014; Brigham, DeCastro, and Shepherd (2007; Kickul, Gundry, Barbosa, and Whitcanack (2007), I conceptualize the cognitive style as a mode of processing information that ranges on a continuum between intuitive and analytic.

Analytic Style and Related Constructs Effectuation

trends, forecasts, or competitor analysis (Porter (1980). The causal logic is similar to the analytic cognitive style with seeking to gather external information to optimize decisions. This approach is consistent with rational decision-making that assumes information is available that allows preferred future states to be identified and ordered according to preference. Conversely, effectual logic will favor control based strategies that will focus on the resources available to the

entrepreneur, including potential relationships with key stakeholders who are willing to engage with the new venture. Control based strategies are internally focused where strategic actions are based on who the individual is, what they know, and whom they know (Sarasvathy (2001). Human, social, and financial capital are seen as opportunities rather than constraints that allow for creative problems-solving, consistent with an intuitive cognitive style.

The causal and effectuation logics are situational approaches to problem-solving under uncertainty that have roots in an individual‘s cognitive style. Effectuation principles are

prescriptive actions entrepreneurs can take to improve the likelihood of a new venture‘s success (Sarasvathy (2009), whereas cognitive style is an enduring attribute that is relatively stable over time (Kirton (1984). Entrepreneurs who have more analytic cognitive styles are likely to favor rational approaches to problem-solving consistent with the causal logic. Entrepreneurs with an intuitive cognitive style are likely to favor creative problem-solving approaches that take into account multiple possible solutions that are in line with the effectuation logic.

Biases and Heuristics

Most entrepreneurs face tremendous odds when they start a business, and many

entrepreneurship is irrational, yet thousands of businesses are started each year (Wilmoth (2019). The biases and heuristics literature help explain why some individuals decide to start businesses despite the high likelihood of failure (Hayward, Shepherd, and Griffin (2006). Heuristics are simplifying strategies to reduce complex decisions to more simple cognitive operations to deal with uncertainty and complexity (Kahneman, Slovic, Slovic, and Tversky (1982; Tversky and Kahneman (1974; Holcomb, Ireland, Holmes, and Hitt (2009). However, these ―rules of thumb‖ often result in suboptimal decisions. Entrepreneurs are often overconfident in their abilities to successfully exploit an opportunity (Forbes (2005; Lowe & Ziedonis (2006; Simon et al. (2000) while overly relying on small samples of information to make important decisions (Busenitz (1999; Busenitz & Barney (1997). The foundations of these heuristics and biases are rooted in the cognition of the entrepreneur (Kruger 2003). Individuals with an analytic cognitive style will more likely gather more information when evaluating opportunities, reducing the chance of representative bias. Those with an intuitive cognitive style are more likely to be overconfident in their gut feel and move forward with a decision they are convinced is correct.

Nascent entrepreneurs often rely on heuristics to manage the uncertainty and complexity inherent in starting a business yet some fall victim to biases that contribute to failure while others do not. The research on biases and heuristics in entrepreneurship helps explain why

entrepreneurs may make irrational decisions at certain times but does not provide a complete picture of how entrepreneurs gather, process, and evaluate information. The entrepreneur‘s use of heuristics may result in biased episodic decisions, but these decisions are nested within the stable cognitive style of the entrepreneur.

The entrepreneurial mindset has been described as the ability to rapidly sense, act, and mobilize, even under uncertain conditions (McGrath and MacMillan (2000). Other scholars have defined the entrepreneurial mindset as ―a growth-oriented perspective through which individuals promote flexibility, creativity, continuous innovation, and renewal (Ireland, Hitt, and Sirmon 2003 pg.968).‖ Entrepreneurially minded individuals are able to identify and exploit new opportunities because they possess the cognitive abilities that allow them to make sense of ambiguous and fragmented situations in the context of uncertainty (Alvarez and Barney (2017). From a cognitive perspective, entrepreneurs can be seen as motivated tacticians who have multiple cognitive strategies from which to choose when confronted with a decision (Fiske and Taylor (1991). Some of these cognitive strategies include thinking in pictures, employing analogies, and synthesizing information relative to a particular goal of the entrepreneur (Haynie, Shepherd, Mosakowski, and Earley (2010). Altogether, the entrepreneurial mindset can be viewed as a state of mind that is ready and able to process complex information that encourages opportunity recognition, evaluation, and possible exploitation.

CHAPTER 3: THEORY AND HYPOTHESIS DEVELOPMENT

A potential entrepreneur‘s accumulated experience plays a major role in the decision to take entrepreneurial action. Experience increases the chances of finding a suitable opportunity to exploit, both organically and inorganically, and provides a foundation of knowledge from which to evaluate the opportunity. Entrepreneurial alertness, or the ability to notice overlooked

opportunities (Kirzner (1979), is an attribute that builds on prior knowledge (Ardichvili, Cardozo, and Ray (2003) and is developed over time (Baron and Ensley (2006). More

experienced potential entrepreneurs have had more time to build a stock of prior knowledge that can help them recognize opportunities that others do not see and accurately evaluate an

opportunity‘s chances of success (Clouse (1990; Kautonen (2008; Kautonen, Down, and Minniti (2014; Lévesque and Minniti (2006). This prior knowledge could include relevant industry trends or available technology that could be deployed in a new or acquired business.

Besides entrepreneurial alertness, increased experience is an advantage in financial capital acquisition. Funds to create or acquire a business can come from personal savings built up over time or through fund-raising efforts from external sources. The vast majority of start-up entrepreneurs finance their venture with their savings (Aldrich and Ruef (2006) and more experienced individuals have had more time to save the funds necessary to get their venture off the ground.

strength of their network ties. Acquiring external funding in any setting is challenging because of information asymmetries and uncertainty. Resource seekers have more and better information about the opportunity than potential investors and can use that information to their advantage (Amit, Glosten, and Muller (1990). Only the entrepreneur knows the depth of their commitment and ability to exploit an opportunity, and savvy investors are aware that the potential

entrepreneur can use this information to negotiate a better deal than is otherwise warranted (Shane and Cable (2002). To mitigate information asymmetries, investors often use social ties when making investment decisions (Granovetter (1985; Venkataraman (1997). Social ties reduce an individual‘s motivation to act in self-interest by introducing the logic of social obligation, generosity, trust, and fairness to the relationship (Gulati (1995; Uzzi (1996). Investors who share social ties with potential entrepreneurs are more likely to invest (Shane & Cable (2002; Shane & Stuart (2002), and potential entrepreneurs with more developed social networks are more likely to share social ties with prospective investors. Individuals with more experience have a higher likelihood of securing external financing because they will have a greater number of social ties from which to solicit investment (Burton, Sorenson, and Beckman (2002; Shane and Stuart (2002; Shane and Cable (2002).

manage the venture from inception to exit and therefore is more worthy of investment (Feeney, Haines, and Riding (1999; Casson (1982; Mason and Harrison (1996).2

More experience positively influences the likelihood of taking entrepreneurial action for multiple reasons. Potential entrepreneurs with more experience are more likely to recognize and correctly evaluate opportunities. More experienced potential entrepreneurs are more likely to secure needed resources either from their accumulated savings or from investors.

Hypothesis 1a: Potential entrepreneurs with more experience will be more likely to start a business.

Hypothesis 1b: Potential entrepreneurs with more experience will be more likely to proceed with an ETA opportunity.

Besides work experience tenure, experience type also plays a role in entrepreneurial decision-making (Dobrev & Barnett (2005). Characteristics of previous employers, such as age, size, and reputation, have been shown to affect rates of entrepreneurial entry (Buenstorf & Klepper (2009; Gompers, Lerner, & Scharfstein (2005; Stuart, Ding, & Stuart (2006). The hierarchy of large and established organizations promotes efficiency and control, which makes decision-making under uncertainty rare (Burns and Stalker (1961). Individuals with work experience in hierarchical organizations are less likely to take entrepreneurial action for many reasons. First, hierarchies have rigidly defined roles and emphasize rules and routines in a way that can lead employees to focus on strict adherence to regulations which induces timidity and conservatism (Merton (1968). Other studies have found that individuals who work in hierarchical

2

organizations have less intellectual flexibility and greater social conformity than those who work in non-hierarchical organizations (Kohn, & Schooler (1982). Hierarchy‘s effect on employee attitudes and cognitive frames may increase timidity, conservativism, rigidity, and conformity, which stands in stark contrast to attributes typically found in entrepreneurship such as boldness, risk-taking, flexibility, and going against social norms (Sorensen (2007).

Second, hierarchies may hamper or prevent employees from developing skills that might be helpful in entrepreneurial settings. Employees in hierarchical organizations are more likely to be responsible for a narrow set of tasks while missing out on opportunities to develop a broader skill-set that might be useful in entrepreneurial contexts. Lazear (2005) argued that entrepreneurs should be jacks of all trades or have some knowledge of a large number of business areas to bring together many different resources to create a firm. Entrepreneurs need to be able to come up with the initial product or service and create a plan to bring the product or service to market. They also must build their management team and outsource responsibilities to capable service providers or perform the responsibilities themselves. Successful completion of these tasks requires a varied set of skills unlikely to be developed in hierarchical settings.

Finally, employment in hierarchical organizations is often seen as preferable to smaller, less formalized organizations. Larger organizations provide more stability and career progression potential than smaller organizations where slack resources might be insufficient to weather a period of poor performance or where career advancement might be tied to the subjectivity of personal relationships. For many, the opportunity cost of leaving stable employment with career advancement to enter entrepreneurship is just too high.

that stymie experimentation and creativity. Potential entrepreneurs with hierarchical work

experience are less likely to have opportunities to develop a broad scope of knowledge and skills that would aid in taking entrepreneurial action. Finally, some individuals might self-select into hierarchical organizations because of preferences for stability and career advancement

opportunities that are not available in entrepreneurial settings thus decreasing the likelihood of even considering taking entrepreneurial action.

Hypothesis 2a: Potential entrepreneurs with hierarchical work experience will be less likely to start a business.

Hypothesis 2b: Potential entrepreneurs with hierarchical work experience will be less likely to proceed with an ETA opportunity.

Individuals are motivated to enter entrepreneurship for a variety of reasons (Carsrud & Brannback (2011; Yitshaki & Kropp (2016;York, O‘Neil, & Sarasvathy (2016). Early

entrepreneurship theory identifies financial rewards as the primary motivation behind entrepreneurship (Knight (1921; Cantillon (1931; Schumpeter (1934), and more recent conceptual and empirical work has built on this premise (Benzing, Chu, & Kara (2009; Naffziger, Hornsby, & Kuratko (1994). However, other empirical studies have found that financial motivations are often less important than non-pecuniary motivations (Amit,

individuals understand the need to make enough money to support themselves and therefore must take into account the financial prospects of a potential opportunity.

Contextual factors influence the economic drivers for aspiring entrepreneurs. Individuals are more likely to exploit an opportunity when the difference between the expected utility of entrepreneurship is larger than the alternative. Individuals with high opportunity costs such as a comfortable, high-paying job are less likely to leave reliable, steady employment to start a business (Johansson (2000). In contrast, those with low opportunity costs, such as those who are unemployed or unhappy at work, will view almost any opportunity as better than the status quo (Ritsilä & Tervo (2002; Taylor (2001).

an entrepreneur are motivations for some aspiring entrepreneurs to exploit an opportunity (Akehurst, Simarro, & Mas-Tur (2012; Edelman et al. (2010).

Taken together, the motivations behind entrepreneurial entry are multifaceted and depend on the individual and the opportunity. Specifically, implicit motivations of status are associated with the decision to enter entrepreneurship. From inception, entrepreneurs are often seen as larger-than-life heroes because they forge their own path and help solve society‘s problems through their creative genius (Anderson & Warren (2011). As the organization grows, the entrepreneur‘s status increases as employees are hired and the social standing of the business in the community builds. The non-financial benefit from status is similar to the socioemotional wealth construct in family business research which has been shown to impact decision-making (Gomez-Mejia et al. (2007).

Hypothesis 3a: Potential entrepreneurs who have implicit motivations of status and recognition will be more likely to start a business.

Hypothesis 3b: Potential entrepreneurs who have implicit motivations of status and recognition will be more likely to proceed with an ETA opportunity.

The recognition of entrepreneurial opportunities is determined, in part, by an individual‘s search behavior (Shepherd and Levesque (2002) and attention allocation (Shepherd, McMullen, and Jennings (2007). Individuals with an analytical style are more likely to search for

decreases the likelihood of discovering a novel solution to a market demand. Therefore, analytic individuals will recognize fewer potential opportunities and consider less novel ways to exploit them, thus decreasing the likelihood of starting a business (Olson (1985).

Cognitive style also influences how opportunities are evaluated once a suitable

opportunity has been discovered. Research has shown that entrepreneurs see opportunities where others see risks (Ziestma (1999; Sarasvathy, Simon, and Lave (1998). Those with an analytic cognitive style are more likely to become aware of risks associated with discovered opportunities because of their thorough approach to information search and analysis. This analysis will

increase the number of perceived risks and challenges associated with potential opportunities and discourage new venture creation. Besides formal analysis, analytic individuals will spend

time required for a thorough evaluation of the opportunity, and rigid decision rules that provide ample opportunity for the aspiring entrepreneur to abandon the opportunity. Therefore:

Hypothesis 4a: Potential entrepreneurs who are more analytic will be less likely to start a business.

Hypothesis 4b: Potential entrepreneurs who are more analytic will be less likely to proceed with an ETA opportunity

Experience can help more analytic individuals overcome the challenges they face in starting a venture in several ways. As previously stated, analytic individuals search for

opportunities within an existing paradigm, yet search and evaluation activities within existing paradigms likely differ between more experienced and less experienced individuals. Experienced potential entrepreneurs who are more analytic are more likely to know where to search for and how to exploit external information that is necessary for opportunity discovery and evaluation. This targeted search decreases the time needed to find a suitable opportunity to exploit and allows them to see more and better opportunities from within the existing paradigm, thus

search for opportunities within their existing paradigm and will take longer to analyze the information they gather because they have not had the life experience necessary to develop their entrepreneurial absorptive capacity. Therefore:

Hypothesis 5a: The negative relationship between analytic cognitive style and the likelihood to start a venture is attenuated as experience increases.

Hypothesis 5b: The negative relationship between analytic cognitive style and the likelihood to proceed with an ETA opportunity is attenuated as experience increases.

Expertise is related to experience, but they are not the same thing. Expertise requires

extensive, deliberate practice over time, whereas experience suggests a regular pattern of

engagement or participation but does not require a prolonged and focused effort (Baron & Henry (2010). Analytic individuals who have had prior entrepreneurship experience have overcome the struggle to ―pull the trigger‖ of engaging in entrepreneurial action despite their proclivity to

gather more information and conduct more analysis. The individual‘s prior entrepreneurship

experience has resolved much of the personal uncertainty that surrounds entrepreneurial entry,

and they are likely to move forward with an opportunity because they have an idea of what to

expect. Analytic individuals with prior entrepreneurship experience will also know the right

questions to ask when evaluating opportunities and arrive at a decision sooner than someone

without experience, which allows them to evaluate opportunities more efficiently thus leading to

an ability to evaluate more opportunities. Finally, individuals with prior entrepreneurship

experience will be ―in the flow,‖ meaning they will know where to look for the opportunities that

will have the greatest chance of success. Entrepreneurship experience provides unique

understand the value chain as well as customers, and operating a business helps with this

understanding much more than doing market research and reaching out to suppliers with

hypothetical scenarios. This understanding is enhanced when the individual has a more analytic

style because their approach to problem-solving is more effective than the intuitive style when

operating within a known paradigm. Therefore:

Hypothesis 6a: The negative relationship between analytic cognitive style and the likelihood to start a business is attenuated by prior entrepreneurship experience.

Hypothesis 6b: The negative relationship between analytic cognitive style and the likelihood to proceed with an ETA opportunity is attenuated by prior entrepreneurship

CHAPTER 4: DATA AND METHODS

In this dissertation, I explore the associations between experience, cognition, and the likelihood of taking entrepreneurial action, the latter of which I analyze in two contexts: starting a business and exploiting a case-based ETA opportunity. I will consider each in turn.

Measurement of Dependent Variable—Organic Entrepreneurship

Organic entrepreneurship is the act of creating a new organization to facilitate the production of future goods or services. The creation of an entity that did not exist previously requires individuals with expertise to seek out resources and organize them in a way that competitors view them as a new market entrant and potential customers view them as a new source of supply (Gartner (1985). For example, the foundation of Uber involved the recruitment of individuals capable of developing the platform, business development experts to build the business, and other employees in supporting roles. Uber was able to hire these employees because the entrepreneurs were successful in their solicitation of financial resources from investors. Through the organization of human and financial resources, Uber is viewed as a competitor to taxi companies and a means of transportation to customers. A new restaurant also organizes human and financial resources to create the business but does so on a much smaller scale than does Uber. Both small and big companies represent organic entrepreneurship.

I used LinkedIn data to identify individuals who started a business after their enrollment in an Introduction to Entrepreneurship class had ended. LinkedIn is the largest professional networking site on the internet with over 610 million profiles. LinkedIn is used by 92% of Fortune 500 companies, and many MBA programs require students to have a LinkedIn profile. LinkedIn profiles in management research have been used to study entrepreneurship in

developing economies (Avnimelech, Zelekha, and Sharabi (2014), business model evolution (Snihur and Zott (2019 and diffusion (Dokko and Gaba (2012). These individuals voluntarily enrolled in this elective course offered in their MBA curriculum, and the majority of individuals expressed interest in participating in entrepreneurship in some capacity in the future.Any student with a job in their work history that was titled founder/cofounder, owner, CEO, president,

principal, or proprietor in the work experience was identified as a possible entrepreneur. From this subset, I independently verified actual entrepreneur status through the company website or social media sources. Within my sample of 996 MBA enrollees, 39 people started a business after completion of the course.

Measurement of Dependent Variable—Inorganic Entrepreneurship

As previously stated, inorganic entrepreneurship is the acquisition of an existing business by an individual (or group of individuals) with the intent to enact their vision and actively

ETA and LBOs both seek to identify and acquire undervalued assets, but ETA differs from LBOs in several ways. First, the goal of an LBO is to improve efficiency and reduce costs to generate free cash flows sufficient to service the debt used to acquire the assets. Over time, value is created by paying down the debt and incrementally improving performance. Equity holders in an LBO will typically pursue an exit within three-to-five years through a sale to a strategic buyer, IPO, or recapitalization (Olsen (2003). In contrast, ETAs use free cash flows to fund growth initiatives such as new products, services, and/or markets to increase value. Entrepreneurs who acquire an existing business have a longer time horizon than LBO funds to allow initiatives to come to fruition. LBOs and ETAs also differ in their governance. LBOs maintain a principle-agent structure with fund managers (agents) overseeing management. An ETA is free from the monitoring and incentive alignment issues associated with principal-agent governance because the entrepreneur who acquires the business is both the principal and the agent (Jensen and Meckling (1976).

The act of franchising could be considered a type of ETA, but I argue that franchising is fundamentally distinct from ETA. Franchising is a contractual arrangement between two independent entities whereby the franchisee pays the franchisor for the right to sell the

key component of ETA. Franchising is also contractually limited in duration while ETA continues in perpetuity or when the entrepreneur decides to sell or close the business.

ETA and franchising also differ in their governance and strategy. Franchisees purchase a residual claim but do not have full decision rights and must operate within the boundaries outlined by the franchisor to maintain trademark value. Some decision rights (e.g., menu

selection, building design) are maintained by the central company. The central company has the authority to monitor the franchisee for product quality and to terminate the contract if the quality is not maintained (Brickley and Dark (1987). Consequently, strategies of efficiency and cost control are preferred while long term growth is accomplished through geographic expansion. In contrast, participants in ETA have full decision rights including the freedom to implement any changes they believe will enhance the future prospects of the business without oversight from an outside entity. They have the freedom to pursue a variety of strategies including introducing new products or services, entering new markets, or reconfiguring the value chain.

In summary, ETA, LBOs, and franchising all involve the purchase of assets but are dissimilar in their purpose, governance, strategy, and time horizon. The key difference is that ETA entrepreneurs have the freedom to operate the business, including the autonomy to pursue organizational changes, to grow the business over a long term time horizon.

In the entrepreneurship literature, ETA represents an alternative path to business ownership because many of the challenges facing potential entrepreneurs in de novo

opportunities are absent in ETA opportunities. For example, nascent entrepreneurs must first have an idea for a business, develop a business model, and conduct activities to reduce uncertainty and mitigate risk. Start-up entrepreneurs increase their chances of success by

contrast, an ETA entrepreneur‘s early success depends on their ability to forecast the future performance of the business and negotiate acquisition terms with current owners. Once a decision to exploit an opportunity has been made, start-up entrepreneurs identify and seek to acquire the necessary financial, social, and human capital needed to support the new venture. Activities are focused on growing the business and developing legitimacy (Aldrich and Ruef (2006). ETA entrepreneurs, meanwhile, become managers of established businesses that own a specific stock of human, social, and financial capital as well as a certain level of legitimacy. Activities for ETA entrepreneurs, post-acquisition, are focused on implementing their vision for the business and executing the strategy they believe will lead to success.

Research on ETA has been hampered by data access and identification. Despite the significant number of ETA deals completed each year, most details surrounding the transactions remain private. Additionally, it is difficult to identify ex ante entrepreneurial intent in business acquisitions. Not all acquisitions are entrepreneurial in nature, and growth is not necessarily an indicator of entrepreneurship (Davidsson, Delmar, & Wiklund (2006). Many acquisitions are completed to secure patents or human capital or as a competitive response to a perceived threat. My research design addresses some of these concerns. My sample consists of potential

entrepreneurs who all evaluate the same ETA opportunity.

explanations that could be attributed to the heterogeneity of opportunity and creates a risk set of potential entrepreneurs, a challenge to research on entrepreneurial entry (Kim, Aldrich, Keister 2006).

I use the HBS Case ―Jim Southern‖ (5-389-073) as the setting for ETA. This case

features Jim Southern as the protagonist, a recent MBA graduate, and his experience as the first search fund entrepreneur. Search funds are a subset of ETA where aspiring entrepreneurs raise capital to search for and acquire undermanaged businesses that have the potential to increase in value through an infusion of capital and entrepreneurial strategic intent (Grousebeck (2010). The case begins with Jim‘s search for investors who are interested in helping him acquire and a low

tech company which he will subsequently manage. Following his search, Jim negotiates a purchase with the owner of a printing company while raising both debt and equity financing. Once the financing is secured, Jim must decide whether to continue with the purchase despite a last-minute ultimatum from the seller to personally guarantee a set of accounts payable or abandon the printing company and begin a new search. Jim acts as an arbitrageur by searching for an undervalued company to acquire. As an organizer of resources, Jim secures debt and equity financing to purchase the company. Finally, Jim plans to enact changes within the company to improve profitability should he decide to proceed with the acquisition. I ask each student to respond to the questions, ―As Jim Southern, would you proceed with the purchase of American Printing? Why or Why not?‖

and responses ranged from very short sentences to long paragraphs to explain their reasoning. Students who indicated they would proceed with the deal were coded as 1; those who voted to abandon the deal were coded as 0. Consistent with past research on decision-making (Dearborn & Simon (1958; Houghton & Goldberg (2000; Simon et al. (2000), I use student responses to surveys based on several case studies to test my hypotheses.

Measurement of Independent Variables

Independent variables were collected from individual LinkedIn profiles, the university provided demographic information, and case surveys. The construct of ―Experience‖ is measured by the age of each student (Mincer (1974). I also capture the construct ―Hierarchy‖ from

LinkedIn as employment in the military at some point in the individual‘s career. From class rosters I identify gender and cohort.

The construct ―Prefounder‖ was measured as any prior entrepreneurship experience included on the LinkedIn profile for each student. I began by tracking each student‘s employment history. Any student with a job in their work history that was titled

founder/cofounder, owner, CEO, president, principal, or proprietor in the work experience was identified as a possible entrepreneur. From this subset, I independently verified actual

entrepreneur status through the company website or social media sources.

opportunities and a measure of their cognitive style. Students are required to evaluate a case study each week. Weeks 1–4 required the students to decide whether they would proceed or not proceed with an opportunity and explain the rationale behind their decision. Data from week five were omitted because the case did not ask about opportunity evaluation. Table 5 provides an overview of the instrument and survey questions.

To measure the construct of ―Implicit motivations of status and recognition,‖ I use computer-aided text analysis (CATA) to examine student responses to surveys on the two cases before the ―Jim Southern‖ case. Traditional methods of measuring implicit motivations use semantic coding of imaginative stories that require a significant contribution from subjects and highly trained coders (Schultheiss, and Pang (2007). CATA provides a more efficient and reliable alternative to implicit motivation measurement by eliminating the human element (Neuendorf (2002). Using CATA to measure implicit motivation, Schultheiss (2013) found that both traditional and CATA methods capture the implicit motives for power, achievement, and affiliation for both US and German University students and did not overlap with measures of self-attributed motivational needs thus demonstrating discriminate validity from self-reported motivations.

previous two cases provides a more robust estimate of the individual‘s true implicit motivations and reduces any bias idiosyncratic to a single case.Implicit motivations of status and recognition was determined using the LIWC ―Power‖ dictionary. The ―Power‖ dictionary is a subcategory of the ―Drives‖ dictionary and consists of 518 words associated with power such as superior and

bully. The drives category within LIWC was assembled to measure needs and motivation

(Pennebaker et al. (2015). Other ―Drive‖ categories include affiliation, achievement, reward, and risk. One advantage of using LIWC as opposed to other CATA programs is that it produces results as a percentage of overall content which normalizes answers and eliminates variance that could result from the overall length of an individual response (Wolfe & Shepherd (2015a). LIWC has been used to study entrepreneurial orientation (Moss, Neubaum, & Meyskens (2015; Wolfe & Shepherd (2015b), customer service (Olekalns & Smith (2006), and negotiations (Olekalns & Smith (2009).

The construct of analytic cognitive style was also measured using CATA. I used the rationale provided by students for each of the four weeks to measure cognitive style using the LIWC content analysis software. CATA methods provide a more efficient and reliable

alternative to cognitive style measurement by eliminating the human element (Neuendorf (2002). Traditional measures of cognitive style such as the cognitive style index (Allinson and Hayes (1996), Kirton‘s (1976) adaption-innovation inventory, and the cognitive style indicator (Cools and Van den Broeck (2007) rely on self-reported data, which is often susceptible to bias

information each week and asked to make a decision, the only variation in this construct comes from their interpretation of the data which provides a clean measure of cognitive style.

Cognitive style is provided by LIWC‘s algorithm analytic as the degree of analytical, logical, and consistent thinking, as opposed to more intuitive, narrative writing (Pennebaker, Boyd, Jordan, & Blackburn (2015). This category is derived from prior studies linking the use of articles, prepositions, and conjunctions to logical and analytical thinking (Pennebaker, Chung, Frazee, Lavergne, & Beaver (2014). One advantage of using LIWC other than CATA programs is that it produces results as a percentage of overall content that normalizes answers and

eliminates variance that could result from the overall length of an individual response (Wolfe & Shepherd (2015a). LIWC has been used to study entrepreneurial orientation (Moss, Neubaum, & Meyskens (2015; Wolfe & Shepherd (2015b), customer service (Olekalns & Smith (2006), and negotiations (Olekalns & Smith (2009).

Control Variables

I control for gender, word count, student responses to case scenarios (to proceed or not proceed), and cohort in my models. There‘s reason to suspect that gender could be related to the decision to start a business in my model. Research has shown that men and women differ in their propensity to start a business so it is appropriate to control for gender (Fischer, Reuber, and Dyke (1993; Elam (2014). I control for word count to ensure that response length is not a factor in the results. I also control for each student‘s decisions to proceed or not proceed with hypothetical

entrepreneurial decision across 996 students was 1.9, with 58 students having a value of 0 (voted against all four opportunities) and 25 students having a value of 4 (voted for all four

opportunities). Finally, data collection took place over five years, and world events, as well as instruction, differed between cohorts which could be related to the dependent variables. Model Specification

I run two separate analyses to test my hypotheses. First, I test the association between my independent variables and the decision to start a business. In the second set, I examine the

linkage between my independent variables on the decision to proceed with an ETA opportunity. I run my analysis using the STATA statistical package.

In the first analysis I use a Cox proportional hazard model (Cox (1972) to test hypotheses 1a, 2a, 3a, 4a, 5a, and 6a.

where Xi=(Xi1,Xi2,⋯,Xip) is the predictor variable for the ith subject, h(Xi,t) is the hazard rate at time t for Xi, and

h

0(t) is the baseline hazard rate function. Cox proportional hazard models are appropriate when the final state of some observations is unknown at the end of the studyIn the second analysis I use a logit model to test hypotheses 1b, 2b, 3b, 4b, 5b, and 6b. Logit models are appropriate when the dependent variable of the regression model is binary such as the decision to proceed with an ETA opportunity.

,

CHAPTER 5: RESULTS

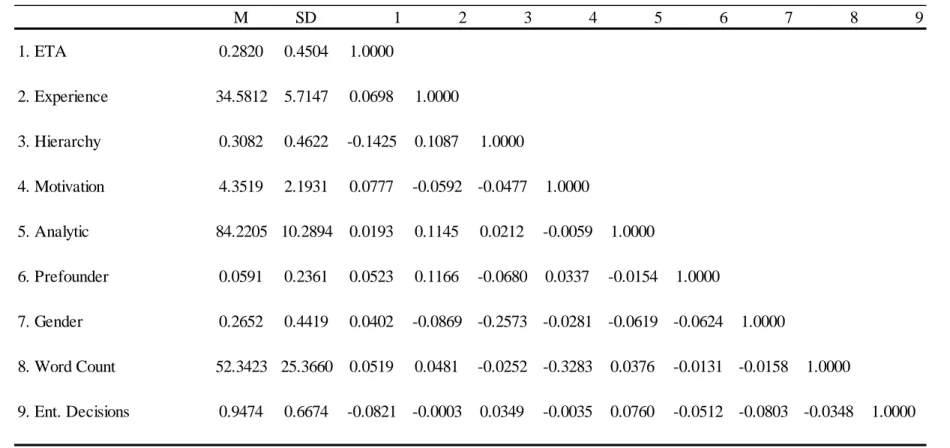

Table 2 presents the descriptive statistics and correlation coefficients for the study

variables related to study 1. The correlation coefficient between Veteran Status and Gender is the highest (-0.2573) but less than 0.04. I conducted a variation inflation factor analysis and found that all variables have a VIF of less than two. Consistent with previous research, a VIF of less than 10 is indicative of inconsequential collinearity (Hair, Black, Babin, and Anderson (1998).

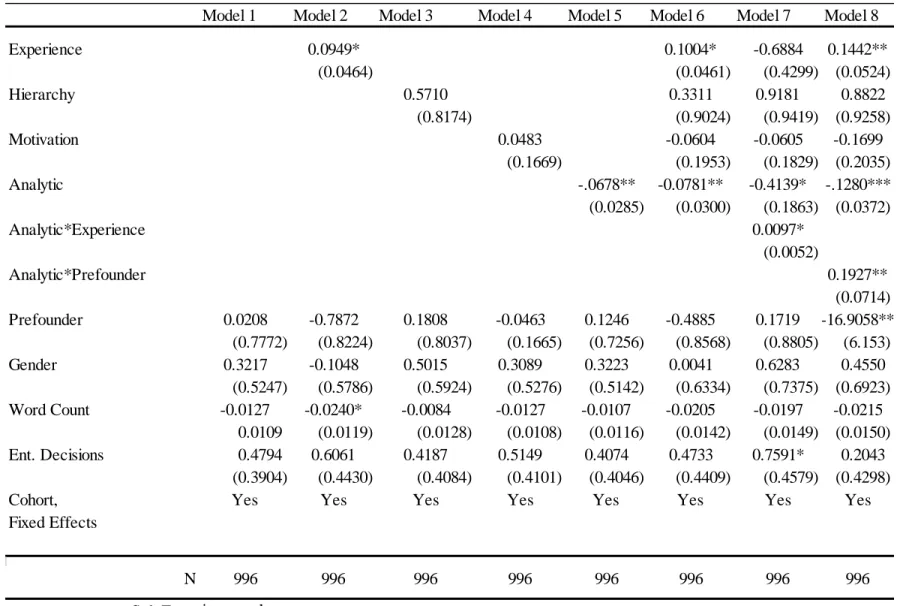

organization is not associated with the likelihood of starting a business. Thus, hypothesis 2a is not supported. Model 4 tests the relationship between implicit motivations of status and recognition and the likelihood of starting a business. Results show no statistically significant relationship and leave hypothesis 3a unsupported. Model 5 shows the coefficient for analytic cognitive style is negative and significant at the .01 level, suggesting that a more analytic cognitive style reduces the likelihood that a potential entrepreneur will start a business, thus supporting hypothesis 4a. When exponentiating the coefficient of -0.0781, a hazard ratio of .9248 is given indicating a one-unit increase in analytic cognitive style is associated with a decrease in the likelihood of starting a business by 7.5%.

Model 7 introduces the interaction term between experience length and an analytic cognitive style. The coefficient for this interaction term is positive and statistically significant at the 0.05 level, indicating that age attenuates the negative effect an analytic cognitive style has on starting a business. Thus, hypothesis 5a is supported. Model 8 shows the interaction term

between prior entrepreneurship experience and analytic cognitive style. The coefficient on the interaction term is positive and statistically significant at the .01 level, thus demonstrating support for hypothesis 6a. Like experience length, prior entrepreneurship experience attenuates the negative relationship between an analytic cognitive style and the decision to start a business.

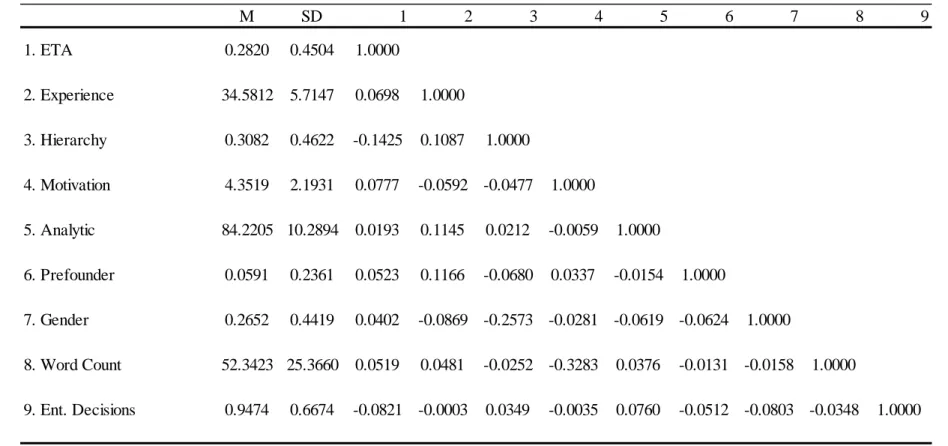

Table 5 presents the descriptive statistics and correlations for the variables related to Study 2. The correlation between hierarchy and gender is higher than all others, and the

correlation between ETA and hierarchy is also high. To address the concern of multicollinearity, I ran a variation inflation factor analysis and found that all variables have a VIF of less than two. Consistent with previous research, a VIF of less than 10 is indicative of inconsequential

Table 6 presents the logistic regression estimates of the effect work experience length, hierarchical work experience, implicit motivation, and analytic cognitive style have on the likelihood of proceeding with an ETA opportunity. Similar to Study 1, all hypotheses are one-directional, and statistical tests are therefore one-tailed for independent variables and two-tailed for control variables. It is important to note that each hypothesis is tested using a one-tailed test because I hypothesize the direction of the relationship between the independent variable and the dependent variable. Model 1 includes all the control variables. Model 2 tested the main effect of experience length. The coefficient is positive and significant (p<.10), showing weak support for hypothesis 1b. Potential entrepreneurs with more experience are more likely to proceed with an ETA opportunity. Model 3 tested the association between hierarchical work experience and the likelihood to proceed with an ETA opportunity. The coefficient is negative and significant (p<.001), showing support for hypothesis 2b. Potential entrepreneurs with hierarchical work experience are less likely to proceed with an ETA opportunity. Model 4 tested the association between implicit motivations of status and recognition and the likelihood to proceed with an ETA opportunity. The coefficient is positive and significant (p<.05), showing support for hypothesis 3b. Potential entrepreneurs with implicit motivations of status and power are more likely to proceed with an ETA opportunity. Next, I tested the association that an analytic cognitive style has on the decision to proceed with an ETA opportunity. Results show that an analytic cognitive style is not associated with the decision to proceed with an ETA opportunity in a statistically significant way. Thus, hypothesis 4b is unsupported. Finally, I tested the

CHAPTER 6: DISCUSSION AND CONCLUSION Contributions

This dissertation investigates the associations between work experience, motivation, and cognitive style and what these have on taking entrepreneurial action. In summary, experience length, experience type, and implicit motivations influence the likelihood that potential entrepreneurs will proceed with a hypothetical ETA opportunity. Potential entrepreneurs with more experience are more likely to proceed with an ETA opportunity, whereas those with experience working in hierarchical organizations are less likely to proceed with an ETA opportunity. Motivation also influences opportunity evaluation. Potential entrepreneurs who have stronger implicit motivations of status and recognition are also more likely to proceed with an ETA opportunity.

This research also supports earlier work on the negative effect working in hierarchical work environments can have on entrepreneurship as well as the positive effect experience has in opportunity exploitation. These findings open the door for future research on other variables that might affect the decision to proceed with an ETA opportunity as well as shed light on alternative modes of entrepreneurial entry.

Building on the hypothetical case study used to explore ETA, the findings of this