I N F O R M AT I O N F O R A DV I SE R S O N LY

Group Insurance for Employer Super

Reference Guide

Introduction

The intention of this booklet is to provide advisers with:

■ general information on Automatic

Acceptance Limits (AALs), underwriting, Forward Underwriting Limits (FULs) and benefit design for group insurance

■ assistance on providing group insurance

arrangements for their clients The booklet is not intended to be a comprehensive guide to group insurance.

1300 128 482 mlc.com.au Employer Super GPO Box 2567W Melbourne Victoria 3001 Facsimile (03) 9869 1595

About MLC

Founded as a life insurance business for miners during the gold rush of 1887, MLC has become one of Australia’s iconic brands.

As the wealth management division of the National Australia Bank we provide investment, super, insurance and private wealth solutions to over 1.5 million people.

We’re also proud to have been voted Australia’s Life Insurance Company of the year in 2009 for the fourth time in six years* and Australia’s

number one major financial advice group** for

the past two years running.

Looking after our customers’ interests and delivering value in the communities in which we operate has always been at the heart of what we do.

* Australian and New Zealand Institute of Insurance ** CoreData, awarded to MLC/Garvan financial planning network

Contents

Section one Automatic acceptance 4

What is automatic acceptance? 4 Automatic acceptance rules (ie. eligibility) 4 Automatic Acceptance Limits (AALs) 4

Section two Insurance benefit types 5 and cover options

Section three Category design 6 Section four Underwriting and Forward 7

underwriting

When will members need to be underwritten? 7 Death and TPD underwriting requirements 8 Examples of Death and TPD underwriting 8 requirements

Income Protection underwriting requirements 9 Examples of Income Protection underwriting 9 requirements

Section five Helpful hints 10 Section six Premium example (annually) 11

Section one

Automatic acceptance

This guide is only applicable to ‘Group’ insurance arrangements and operates quite differently to individual insurance arrangements whereby, and with some exceptions, any increase in cover other than CPI increases are usually subject to underwriting.

What is automatic acceptance?

Automatic acceptance enables eligible employee members of an employer superannuation plan to receive insurance cover, up to certain dollar limits, without the need for the members to complete a personal statement, or provide other health or financial information. The level of automatic cover applying to each employer plan will depend on the number of insured members in the plan and is subject to the plan meeting certain eligibility rules, as set out under the next heading.

Automatic acceptance rules

(ie. eligibility)

You can help the employer choose the insurance arrangements that will apply to employees. However, for automatic acceptance to apply, you must keep the following requirements in mind:

■ there is a minimum of five insured

members for Death and Total and Permanent Disablement (TPD) cover

■ there is a minimum of ten insured members

for Income Protection (IP) cover

■ newly insured members must be under age 65 ■ ‘at work’ requirements must be satisfied and

‘at work’ certification must be provided

■ there must be pre-determined and acceptable

benefit formulae applying to members seeking cover under automatic acceptance

■ new members must join the plan and take

up insurance within 120 days of joining the employer

Automatic Acceptance Limits

(AALs)

#The following table shows the maximum AALs that apply according to the benefit type and number of insured members within an employer plan.

Number of insured members Death or Death & TPD AAL Income Protection AAL 1-4 Nil Nil 5-9 up to $200,000 Nil 10-19 up to $300,000 up to $4,000 20-49 up to $400,000 up to $5,000 50-99 up to $600,000 up to $7,000 100-199 up to $750,000 up to $8,000 200-499 up to $850,000 up to $9,000 500-999 up to $900,000 up to $10,000 1000+ Refer to BDM up to $12,000

# Automatic Acceptance Limits do not apply to Employer

Super Spouse Account insurance. Such members’ applications for any insurance are subject to underwriting. However, they will benefit from the relevant employer plan’s group discounts on insurance premiums. MLC Limited reserves the right to decline to offer AALs or

to offer AALs at levels lower than those shown in the table above. MLC Limited assesses the overall risk of the plan (including occupation profile) before offering an AAL.

3

Section two

Insurance benefit types and cover options

The type of cover available within the employer plan is very flexible. A combination of options is available and you can nominate any of the following:

■ Death only ■ TPD only ■ Death and TPD

■ Death and Income Protection ■ Death, TPD and Income Protection ■ Income Protection only*

- up to 75% of pre-disability income (plus an option of up to 10% of pre-disability income paid directly into super while on claim) - choice of 30, 60, 90 or 120 day waiting periods - benefit payment period of two years, five

years, to age 60 or to age 65

The level of benefit available for an employer plan can also be chosen to reflect the profile of the plan membership and it may be reasonable to select different levels of cover for specific categories within the same plan.

* Income Protection benefits in excess of two years cannot be offered on a stand alone basis and must combine Death and/or TPD cover.

Cover options include:

■ Future Service Multiple

(% of salary for each year to age 65) eg. 35yr old earning $50,000 15% x 50,000 x (65 – 35) = $225,000 Considerations:

- premiums kept reasonably stable as cover reduces with age

- insured amount decreases with age, however is offset if salary increases

■ Fixed Multiple of salary

eg. 4 x $50,000 = $200,000 Considerations:

- simple to determine the amount of cover each year

- cover increases as salary increases - premium rates generally increase with age

so the premium cost rises each year due to age and level of cover

- rising cover may not necessarily match the member’s needs

■ Fixed dollar amount

(minimum cover of $50,000) eg. $200,000

Considerations:

- members know exactly how much cover they have

- premium rates generally increase with age so the premium cost rises each year due to age - while rising levels of cover may not necessarily

match the member’s insurance needs, likewise a fixed level of cover may not match the member’s needs

■ Fixed premium amount ($) per week

Premium can range from $1 to $5 per week and the amount of cover will vary depending on age, sex and occupation.

Considerations:

- know exactly what the premium will be each week/year

- level of cover reduces each year even though the premium remains fixed

- cost relative to salary reduces each year - members may need more, rather than less,

cover as time progresses

Note that any of the above options (apart from the $1 per week type cover) can be either:

- inclusive of account balance; or

- additional to account balance (will default to this option if nothing selected).

Income Protection Cover

Benefit payment period: two years, five years, to age 60 and to age 65.

Waiting period: 30, 60, 90 or 120 days. Benefit Level: generally, 75% of pre-disability income is insured and there is also the option to insure an additional 10% of income** (which would be paid directly into the member’s superannuation account) in the event of the member being on claim.

** On claim, the superannuation component must be paid

directly into a superannuation fund, and is not available as a cash benefit directly to the claimant.

Section three

Category design

Certain types of cover may not be available, or may only be offered on a modified basis in respect to certain occupational categories.

If you are uncertain whether cover will be available for some employees, or you would like to check the occupational rating, you can email your query to the Employer Super administration team at [email protected] or alternatively you can access the occupational ratings guide by logging onto mlc.com.au

Example 1:

An employer group consists of 55 white collar workers, including four executives and 10 casual staff.

AAL: $600,000 for Death & TPD and $7,000 for Income Protection cover.

Category A

Executives

$600,000 Death & TPD with IP (a 30 day waiting period and benefit period to age 65).

Category B

Staff

15% x salary for each year to age 65 Death & TPD with IP (a 90 day waiting period and two year benefit period).

Category C

Casuals

$2 per week Death only

Example 2:

An employer group consists of 14 blue collar workers (plumbers) and two directors.

AAL: $300,000 for Death & TPD and $4,000 for Income Protection cover.

Category A

Directors

17.5% x salary for each year to age 65 Death & TPD with IP (a 30 day waiting period and benefit period to age 65).

Category B

Blue Collar Workers $200,000 Death & TPD

Example 3:

An employer group consists of 10 linked companies (common ownership of all companies). This group consists of four executives,

20 management, 50 administration staff and 40 process workers.

Total insured membership = 114 members AAL: $750,000 for Death & TPD and $8,000 for Income Protection

Category A

Executive and Management

5 x salary for Death & TPD with IP (a 30 day waiting period and benefit period to age 65).

Category B

Administration staff

12.5% x salary for each year to age 65 Death & TPD with IP (a 90 day waiting period and two year benefit period).

Category C

Process workers $150,000 Death only

5

Section four

Underwriting and Forward underwriting

When will members need to

be underwritten?

Employer specified (default) cover

Where a member’s employer specified insurance (default) cover is based on his or her salary, each time the member’s salary increases then so too would the level of insurance cover. This is most likely to occur when cover is based on a fixed multiple of salary eg. for Death & TPD, 5 x salary or for IP, 75% of income.

Once a member’s level of cover exceeds the plan’s AAL, or increases by over 25% or more over the past 12 months, the member will be underwritten to a Forward Underwriting Limit (FUL).

So that underwriting is not required each time the insurance cover increases purely because the salary has increased, the member is underwritten only once whilst the level of cover is within a FUL. Once the member’s cover exceeds either the AAL or exceeds the specific FUL, he or she will then need to be underwritten to a higher level (ie. the next FUL).

Where a member’s default insurance cover first exceeds either the employer plan AAL category levels, or the limits as per the underwriting limits (as specified in the relevant Table A or B over the page), then the member will need to be underwritten and accepted for insurance before being eligible to be covered for that amount which exceeds the AAL or FUL.

Voluntary cover

Voluntary increases in insurance cover are always underwritten. Where a member chooses voluntary insurance (eg. a fixed $500,000) on top of their employer specified insurance (or default) cover, it

is the combined amount of these covers which determines what degree of underwriting is required and, hence, what the FUL will be. The FUL is, therefore, determined according to the combined cover that has been underwritten, but keeping in mind that any further voluntary

increases will again be underwritten.

Summary

A member needs to be underwritten:

■ once his or her cover first exceeds the AAL ■ once his or her cover first exceeds a FUL ■ where there is a default insurance formula

applying but there is no AAL

■ where any voluntary cover is sought

■ where default cover increases by 25%, or more,

over the previous 12 months

■ where a Spouse Account member applies

for insurance

Where cover either exceeds the AAL or enters into another forward underwriting limit band, and underwriting is required, it is only the default cover in excess of the AAL or FUL which is subject to any applicable premium loadings or cover exclusions. Voluntary cover, in its entirety, may be subject to loadings or exclusions depending on the underwriting assessment of that cover. Where a member had opted to reduce or cancel existing cover, he or she is generally only able to increase the cover again subject to underwriting and acceptance by MLC Limited – regardless of whether or not the employer plan still has an AAL in place.

■ Limits apply once the AAL is exceeded or where

the insured cover increases by more than 25%

over the previous 12 months.

■ Where a member’s cover increases from a level

below the AAL to a level above the AAL, then the revised cover will be underwritten. This is within the requirements of the band that the cover level is in (unless within $50,000 of the next band, in which case the underwriting requirements of the next band will apply).

■ Where cover of a member increases within

$50,000 of the next band, and underwriting is required to be undertaken, then cover must be underwritten to the limit of the next band.

Tip: Where a member has applied for both Death/TPD cover and Income Protection concurrently, and where both a medical exam by a general practitioner and a Rapidcheck

are required, then only the general practitioner medical exam should be obtained.

Examples of Death and TPD

underwriting requirements

(see Table A):

1. There is an AAL of $500,000 and default cover increases from $430,000 to $560,000 in which case the insured member is underwritten within the requirements of Underwriting Band #1 to a level of $750,000.

2. There is an AAL of $680,000 and default cover increases from $650,000 to $700,000. In this case the insured member is underwritten within the requirements of Underwriting Band #2 to a level of $1,000,000 (since the new cover is within $50,000 of the start of Underwriting Band #2).

3. Member is in Underwriting Band #3 and has been underwritten to $1,500,000 previously. The cover was $1,030,000 and has increased to $1,300,000 (i.e. >25%), so underwriting is again required within Underwriting Band #3, this being to $1,500,000 – even though this

Death and TPD underwriting requirements

The following is the Death and TPD table of forward underwriting requirements:

Table A (Death & TPD)

Underwriting

Band Forward underwriting limit (where above AAL)* Type of underwriting required

1 up to $750,000 ■ Personal statement

2 $750,001 to $1,000,000 ■ Personal statement, and ■ Rapidcheck

3 $1,000,001 to $1,500,000 ■ Personal statement

■ HIV, HEP B & C and MBA 20, and ■ Medical exam

Note: Rapidcheck if member is aged less than 45 next birthday in lieu of the Medical exam

4 $1,500,001 to $2,000,000 ■ Personal statement ■ HIV, HEP B & C and MBA 20 ■ Medical exam, and

■ ECG but only if member is older than age 45

next birthday

5 $2,000,000+ ■ At MLC Limited’s discretion – including a PMAR

7

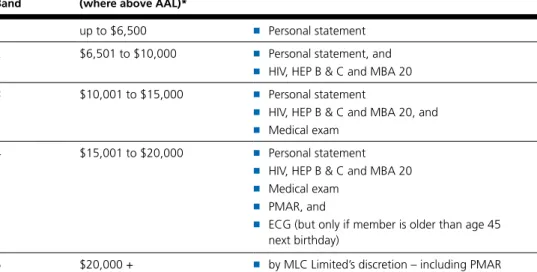

Income Protection underwriting requirements

The following is the Income Protection table of forward underwriting requirements:

Table B (Income Protection)

Underwriting

Band Forward underwriting limit (where above AAL)* Type of underwriting required

1 up to $6,500 ■ Personal statement

2 $6,501 to $10,000 ■ Personal statement, and ■ HIV, HEP B & C and MBA 20

3 $10,001 to $15,000 ■ Personal statement

■ HIV, HEP B & C and MBA 20, and ■ Medical exam

4 $15,001 to $20,000 ■ Personal statement ■ HIV, HEP B & C and MBA 20 ■ Medical exam

■ PMAR, and

■ ECG (but only if member is older than age 45

next birthday)

5 $20,000 + ■ by MLC Limited’s discretion – including PMAR

* The member’s cover either exceeds the AAL, or cover increases by 25% or more over the previous 12 months.

■ Limits apply once the AAL is exceeded or where

the insured cover increases by more than 25%

over the previous 12 months.

■ Where a member’s cover increases from a level

below to a level above the AAL, the revised cover above the AAL will be underwritten. The underwriting is within the requirements of the band that the cover amount lies in (unless this is within $1,000 of the next band, in which case the underwriting requirements of the next band applies).

■ Where the cover of an insured member

increases to within $1,000 of the next band and underwriting is required to be undertaken, then the cover must be underwritten within the requirements of next underwriting band.

Examples of Income Protection

underwriting requirements

(see Table B):

1. There is an AAL of $5,000 per month and default cover increases from $3,500 per month to $4,450 per month (ie. >25%), in which case

the insured member is underwritten within the requirements of, and to the limit of Forward Underwriting Band #1, this being $6,500. 2. There is an AAL of $6,000 per month and

default cover increases from $5,200 per month to $6,100 per month in which case the insured member is underwritten within the requirements of, and to the limit of Forward Underwriting Band #2 (since the new cover is within $1,000 of the start of Underwriting Band #2). 3. Member is in Forward Underwriting Band #3

and had been underwritten to a limit of $15,000 per month previously. The cover was $10,300 per month and increased, in this year alone, to $13,100 per month (ie. >25%), therefore underwriting is required within Forward Underwriting Band #3, this being to $15,000, even though this underwriting process had been done previously.

Section five

Helpful hints

■ For a plan to be eligible for an AAL for its

members, the plan must be the employer’s default superannuation arrangement.

■ New members are eligible for the AAL

provided they join the plan and take-up the insurance within 120 days of first being eligible to join the plan.

■ The AALs are based on the number of

insured members within the plan – reviewed on 1 July each year. As an example, you may have 110 members within the plan, however only 90 have insurance cover. The AAL would be based on the 90 insured members.

■ If there was a time when all 110 members

had cover, the AAL would have been based on the 110 members. Members at that time retain any cover that was attained under the higher AAL, even if the insured membership drops to 90 and the AAL reduces accordingly.

■ New members would get the AAL based on

the number of members insured at the time they joined (ie. if there were 90 insured members at the date they joined, the AAL would be based on 90 members).

Benefits of insurance within Employer Super account include:

■ AALs allow insurance cover without the need

for a personal health statement

■ generally cheaper premiums due to the

group discount

■ tax free premiums

If the insurance cover is related to salary (% x salary x yrs to 65), any benefit increase of 25% or more over the previous 12 months, will require the member to be underwritten. For insurance cover to remain in place, the premiums need to be paid. After 60 days, if there are insufficient funds to cover the premiums, the member will be sent a lapse notification warning letter. A further warning letter is again sent after 90 days and then after 120 days the cover will lapse and the member will receive a lapse letter. Casual staff are not eligible for Income Protection, however maybe eligible for Death & TPD cover under a ADL definition (activities of daily living).

11 Age next

birthday Future service multiple1 Fixed multiple of salary 2 Fixed dollar amount 3 $1 per week 4 Cover Death & TPD Premium Cover Death & TPD Premium Cover Death & TPD Premium Premium Death & TPD Cover 30 $262,500 $144.64 $200,000 $110.20 $300,000 $165.30 $52 $94,374.21 35 $225,000 $176.01 $200,000 $156.46 $300,000 $234.68 $52 $66,472.27 40 $187,500 $205.35 $200,000 $219.04 $300,000 $328.56 $52 $47,480.19 45 $150,000 $271.42 $200,000 $361.89 $300,000 $542.84 $52 $28,738.01 50 $112,500 $361.98 $200,000 $643.51 $300,000 $965.27 $52 $16,161.33 55 $75,000 $423.45 $200,000 $1,129.21 $300,000 $1,693.81 $52 $9,210.01 60 $37,500 $385.95 $200,000 $2,058.42 $300,000 $3,087.63 $52 $5,052.42 Cover is determined as follows:

1 15% of salary for each year to age 65 2 4 times salary

3 $300,000

4 Amount of cover that is purchased for $1 per week Assumptions:

a) Male, aggregate rates b) Salary: $50,000 c) Plan size: 55

d) Full commission (27.5% inc. GST) e) Occupation AA (white collar) f) TPD definition: Any Occupation g) Premium includes stamp duties

Section six

B_

10

10

Disclaimer

This document is issued by NULIS Nominees (Australia) Limited ABN 80 008 515 633, AFSL 236465 (NULIS).

This information is general in nature and does not take into account any particular persons situation or needs. Before deciding to acquire or dispose of the product your client should consider the Employer Super Product Disclosure Statement and whether it is appropriate for them. This product is issued by NULIS. A copy of the Product Disclosure Statement is available by visiting mlc.com.au. Applications to invest in a financial product issued by NULIS must be made by completing the application within the Product Disclosure Statement.

Further information

To find out more about Employer Super, simply contact a Business Development Manager in your state:

New South Wales and ACT

02 9259 8441

Northern Territory and South Australia

08 8179 2600 Queensland 07 3231 4777 Western Australia 08 9211 6400 Victoria 03 9829 8989 Tasmania 03 6244 9800

Alternatively you can contact Adviser Services on 1300 128 482 or visit mlc.com.au