i

Implementing

Financial Governance

The Municipal Finance Management Act No. 56 of 2003 as basis for creating a service delivery culture

Learner Guide & Reference Source for the MFMA Induction Programme National Treasury

iii

Table of contents

List of tables ... xi

List of figures ... xii

List of legislature ... xiii

List of abbreviations ... xiv

Introduction to the Municipal Finance Management Act (MFMA) induction programme ... 1

Learning outcomes ... 1

Key concepts ... 1

Scene-setting questions ... 1

Introduction ... 2

The what and the how of service delivery ... 2

How the MFMA promotes enhanced levels of service delivery ... 4

The need for financial management capacity development ... 5

The MFMA Induction Programme as part of a comprehensive PFMCDS ... 5

Target audience for this MFMA Induction Programme ... 8

Goal, objectives and outcomes of the Induction Programme ... 8

Summary ... 9

PART ONE VISION AND UNDERLYING PRINCIPLES ... 10

Chapter 1: Roles of national and provincial government ... 11

1.1. Learning outcomes ... 11

1.2. Key concepts ... 11

1.3. Scene-setting questions ... 11

1.4. Introduction ... 12

1.5. Where the individual municipal official fits into the picture ... 12

1.6. National government ... 12

1.7. Provincial government ... 13

1.8. Summary ... 14

Chapter 2: Legislation and governance frameworks ... 15

2.1. Learning outcomes ... 15

2.2. Key concepts ... 15

2.3. Scene-setting questions ... 15

2.4. Introduction ... 15

iv

2.6. The framework of legislation ... 16

2.7. Provisions concerning municipal service delivery present in the Constitution ... 25

2.8. The MFMA and the Municipal Systems Act as interrelated legislation ... 25

2.9. Summary ... 29

Chapter 3: Vision of a modernised financial system ... 30

3.1. Learning outcomes ... 30

3.2. Key concepts ... 30

3.3. Scene-setting questions ... 30

3.4. Introduction ... 30

3.5. Where the individual municipal official fits into the picture ... 30

3.6. Legislative and policy reforms ... 31

3.7. Approach taken in modernising financial management ... 31

3.8. Summary ... 33

Chapter 4: Underlying principles supporting sound financial governance ... 34

4.1. Learning outcomes ... 34

4.2. Key concepts ... 34

4.3. Scene-setting questions ... 34

4.4. Introduction ... 35

4.5. Where the individual municipal official fits into the picture ... 35

4.6. Promoting sound financial governance by means of clarifying roles ... 36

4.7. A more strategic approach to budgeting ... 38

4.8. Enhancing revenue management and revenue collection ... 39

4.9. Modernisation of financial management ... 41

4.10. Promoting cooperative government ... 42

4.11. Promoting sustainability ... 44

4.12. Summary ... 47

PART TWO ROLES AND RESPONSIBILITIES IN MUNICIPAL FINANCE ... 48

Chapter 5: Clarifying roles and responsibilities of the council, the executive and the accounting officer ... 49

5.1. Learning outcomes ... 49

5.2. Key concepts ... 49

5.3. Scene-setting questions ... 50

v

5.5. Where the individual municipal official fits into the picture ... 51

5.6. Role of the council ... 52

5.7. Role of the non-executive councillor ... 53

5.8. Role of the executive mayor or committee ... 54

5.9. Role of the municipal manager (the accounting officer) ... 54

5.10. Oversight on performance: agreements, monitoring, evaluation and reporting 56 5.11. Combating misconduct, incapacity and unethical conduct ... 57

5.12. Summary ... 60

Chapter 6: Top management and the delegation of accounting officer responsibilities ... 61

6.1. Learning outcomes ... 61

6.2. Key concepts ... 61

6.3. Scene-setting questions ... 61

6.4. Introduction ... 61

6.5. Where the individual municipal official fits into the picture ... 62

6.6. Delegations and accountability ... 63

6.7. Delegation risks and risk controls ... 65

6.8. Summary ... 66

Chapter 7: The budget and treasury office (BTO) as a governance structure ... 67

7.1. Learning outcomes ... 67

7.2. Key concepts ... 67

7.3. Introduction ... 67

7.4. Scene-setting questions ... 67

7.5. Where the individual municipal official fits into the picture ... 67

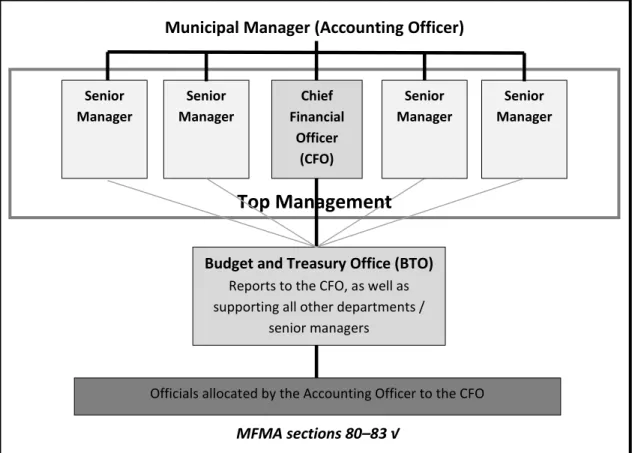

7.6. Areas of responsibility and the organisation of the BTO ... 68

7.7. The chief financial officer (CFO) ... 70

7.8. The governance responsibilities of the CFO and the BTO ... 72

7.9. Summary ... 74

PART THREE MUNICIPAL SERVICE DELIVERY PLANNING AND IMPLEMENTATION ... 76

Chapter 8: Three-year budgeting and planning ... 77

8.1. Learning outcomes ... 77

8.2. Key concepts ... 77

8.3. Scene-setting questions ... 78

vi

8.5. Where the individual municipal official fits into the picture ... 78

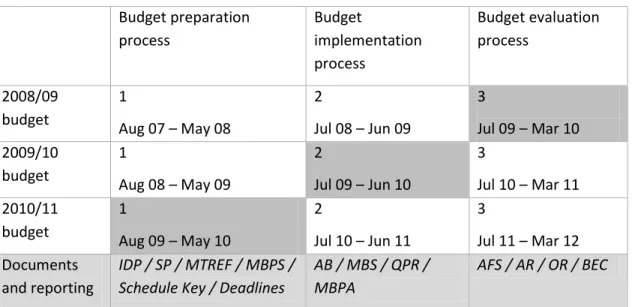

8.6. The budget preparation process ... 79

8.7. Role of the budget steering committee ... 81

8.8. Funding the budget ... 82

8.9. Adoption of the annual budget ... 83

8.10. Budgets of municipal entities ... 84

8.11. Budget implementation ... 85

8.12. Variation from budget estimates ... 86

8.13. Revision of budget estimates ... 87

8.14. Unauthorised, irregular, and fruitless and wasteful expenditure ... 87

8.15. Contemporary Issues in municipal budgeting ... 89

8.16. Summary ... 89

Chapter 9: Costing and capital planning ... 91

9.1. Learning outcomes ... 91

9.2. Key concepts ... 91

9.3. Scene-setting questions ... 91

9.4. Introduction ... 91

9.5. Where the individual municipal official fits into the picture ... 92

9.6. Project management as an indispensable way of working ... 94

9.7. Costing ... 94

9.8. Capital planning ... 97

9.9. Summary ... 98

Chapter 10: Asset management ... 100

10.1. Learning outcomes ... 100

10.2. Key concepts ... 100

10.3. Scene-setting questions ... 100

10.4. Introduction ... 101

10.5. Where the individual municipal official fits into the picture ... 101

10.6. Management of assets and the asset register ... 102

10.7. Legislative mandates ... 106

10.8. Financing of assets ... 106

10.9. Utilisation performance of assets ... 107

vii

10.11. Accounting for assets ... 107

10.12. Disposals and transfers of assets ... 108

10.13. Summary ... 109

PART FOUR SUPPLY CHAIN MANAGEMENT, ALTERNATIVE SERVICE DELIVERY MECHANISMS, AND CONTRACT MANAGEMENT ... 111

Chapter 11: Supply chain management ... 112

11.1. Learning outcomes ... 112

11.2. Key concepts ... 112

11.3. Scene-setting questions ... 112

11.4. Introduction ... 112

11.5. Where the individual municipal official fits into the picture ... 113

11.6. Institutional arrangements and policy provisions for SCM ... 114

11.7. Governance of municipal SCM ... 116

11.8. Legislation and government policies that impact on SCM processes ... 116

11.9. Municipal SCM processes ... 118

11.10. Competitive bids ... 119

11.11. Contemporary issues in municipal SCM ... 121

11.12. Summary ... 122

Chapter 12: Alternative service delivery mechanisms ... 123

12.1. Learning outcomes ... 123

12.2. Key concepts ... 123

12.3. Scene-setting questions ... 123

12.4. Introduction ... 123

12.5. Where the individual municipal official fits into the picture ... 124

12.6. Municipal entities as service delivery mechanism ... 125

12.7. Principles underlying PPPs in municipal service delivery ... 127

12.8. Pros and cons of a PPP ... 129

12.9. Matters to consider when using PPPs ... 129

12.10. Summary ... 130

Chapter 13: Contract management ... 131

13.1. Learning outcomes ... 131

13.2. Key concepts ... 131

viii

13.4. Introduction ... 131

13.5. Where the individual municipal official fits into the picture ... 131

13.6. Contract management in the municipal context ... 132

13.7. Contemporary issues in contract management ... 136

13.8. Summary ... 137

PART FIVE REPORTING AND CONTROL ... 139

Chapter 14: In-year reporting ... 140

14.1. Learning outcomes ... 140

14.2. Key concepts ... 140

14.3. Scene-setting questions ... 140

14.4. Introduction ... 140

14.5. Where the individual municipal official fits into the picture ... 141

14.6. Reporting in the municipal context ... 141

14.7. The AGSA and other contemporary issues in mid-year reporting ... 147

14.8. Summary ... 147

Chapter 15: MFMA performance monitoring ... 148

15.1. Learning outcomes ... 148

15.2. Key concepts ... 148

15.3. Scene-setting questions ... 148

15.4. Introduction ... 148

15.5. Where the individual municipal official fits into the picture ... 149

15.6. Purpose and structure of the MFMA performance monitoring instrument ... 150

15.7. Reporting ... 151

15.8. Contemporary issues in financial performance management ... 151

15.9. Summary ... 152

Chapter 16: Annual reports ... 153

16.1. Learning outcomes ... 153

16.2. Key concepts ... 153

16.3. Scene-setting questions ... 153

16.4. Introduction ... 153

16.5. Where the individual municipal official fits into the picture ... 154

16.6. Purpose and preparation of the annual report ... 154

ix

16.8. Approval and use of completed annual reports ... 156

16.9. Contemporary issues in the production and utilisation of annual reports ... 158

16.10. Summary ... 158

Chapter 17: Risk management ... 159

17.1. Learning outcomes ... 159

17.2. Key concepts ... 159

17.3. Scene-setting questions ... 159

17.4. Introduction ... 160

17.5. Where the individual municipal official fits into the picture ... 160

17.6. Risk and the need for risk management in a municipality ... 161

17.7. Legislation and regulations providing for risk management in municipalities .. 161

17.8. Institutional arrangements for risk management in a municipality ... 162

17.9. The risk management process ... 162

17.10. Contemporary issues in risk management ... 163

17.11. Summary ... 164

Chapter 18: Internal control processes, audits and audit committees... 165

18.1. Learning outcomes ... 165

18.2. Key concepts ... 165

18.3. Scene-setting questions ... 166

18.4. Introduction ... 166

18.5. Where the individual municipal official fits into the picture ... 166

18.6. Internal control... 167

18.7. Internal audit ... 169

18.8. Audit committees ... 171

18.9. Executive oversight ... 172

18.10. Contemporary issues relating to internal control, audits and audit committees172 18.11. Summary ... 174

Chapter 19: External audit as consolidated and independent finding on performance ... 175

19.1. Learning outcomes ... 175

19.2. Key concepts ... 175

19.3. Scene-setting questions ... 175

19.4. Introduction ... 175

x

19.6. The difference between an external and an internal audit ... 176

19.7. The role and responsibilities of AGSA ... 176

19.8. Summary ... 177

Annexure A: MFMA Delegations Framework ... 178

Annexure B: Relationship between the strategic areas, the outcomes, and the indicators, as well as the source documents to be used in connection therewith ... 218

Annexure C: Checklist of internal control matters included in the MFMA ... 222

Annexure D: Information to be included in the audit file ... 230

List of resources ... 233

xi

List of tables

Table 1: Legislation providing a framework for a modernised financial system ... 16

Table 2: The linkages and alignment between the Municipal Systems Act and the MFMA .... 26

Table 3: The financial governance framework ... 38

Table 4: Simultaneous focus on three different budgets (using the 2007–2012 period as an example) ... 39

Table 5: Roles and responsibilities of the municipal manager in cooperative governance... 43

Table 6: Summary of the framework for cooperative government ... 44

Table 7: Competencies of the CFO ... 71

Table 8: Typical governance positioning of the Budget and Treasury office ... 104

Table 9: Key with which to interpret Table 8 ... 105

Table 10: SCM systems ... 115

Table 11: Legislation, policies and regulations to be considered in SCM ... 117

Table 12: SCM requirements for specialised services ... 121

Table 13: Overview of financial reports ... 142

Table 14: Summary of the budget and reporting cycle ... 144

Table 15: MFMA provisions for internal control ... 167

xii

List of figures

Figure 1: MFMA Induction Programme as part of the national Capacity Development Strategy

... 7

Figure 2: Vision and underlying principles of the MFMA ... 10

Figure 3: Municipal finance roles and responsibilities emanating from the MFMA ... 48

Figure 4: Governance and accountability: oversight, and clear lines of reporting ... 51

Figure 5: Example of a written delegation ... 63

Figure 6: Structure of the BTO of a small municipality ... 70

Figure 7: Structure of the BTO of a medium and large municipality ... 70

Figure 8: Typical structure of the BTO ... 73

Figure 9: Municipal service delivery planning and implementation ... 76

Figure 10: Local government fiscal framework ... 79

Figure 11: Annual budget preparation cycle ... 80

Figure 12: Municipal service delivery system ... 92

Figure 13: The sustainability challenge for municipalities ... 96

Figure 14: The concepts and functioning of municipal SCM, alternative service delivery mechanisms and contract management ... 111

Figure 15: SCM model ... 119

Figure 16: The contract life cycle (Source: CFO’s Handbook) ... 134

Figure 17: Municipal reporting and control ... 139

Figure 18: Municipal reporting flow chart (National Treasury MFMA Circular No. 63, 2012:4) ... 155

xiii

List of legislature

Basic Conditions of Employment Act No. 75 of 1997

Broad-Based Black Economic Empowerment Act No. 53 of 2003 Competition Act No. 89 of 1998

Companies Act No. 71 of 2008

The Constitution of the Republic of South Africa, 1996 Consumer Protection Act No. 68 of 2008

Division of Revenue Act (annual) Electricity Regulation Act No. 4 of 2006 Employment Equity Act No. 55 of 1998 Housing Act No. 107 of 1997

Intergovernmental Fiscal Relations Act No. 97 of 1997 Intergovernmental Relations Framework Act No. 13 of 2005 Labour Relations Act No. 66 of 1995

Local Government: Municipal Demarcation Act No. 27 of 1998 (Demarcation Act) Local Government: Municipal Electoral Act No. 27 of 2000

Local Government: Municipal Finance Management Act No. 56 of 2003 (MFMA)

Local Government: Municipal Structures Act No. 117 of 1998 (Municipal Structures Act) Local Government: Municipal Systems Act No. 32 of 2000 (Municipal Systems Act) Local Government: Municipal Systems Amendment Act No. 7 of 2011

Local Government: Property Rates Act No. 6 of 2004 (Property Rates Act) Municipal Fiscal Powers and Functions Act No. 12 of 2007

National Land Transport Act No. 5 of 2009 National Small Business Act No. 102 of 1996 National Water Act No. 36 of 1998

Preferential Procurement Policy Framework Act (PPPFA) No. 5 of 2000 Prevention and Combating of Corrupt Activities Act No. 12 of 2004 Promotion of Access to Information Act No. 2 of 2000 (PAIA) Promotion of Administrative Justice Act No. 3 of 2000 (PAJA)

Promotion of Equality and Prevention of Unfair Discrimination Act No. 4 of 2000 Public Finance Management Act No. 1 of 1999 (PFMA)

Public Finance Management Amendment Act No. 29 of 1999 Public Office-Bearers Act No. 20 of 1998

Remuneration of Public Office Bearers Act No. 20 of 1998 Rental Housing Act No. 50 of 1999

Skills Development Act No. 97 of 1998

South African Qualifications Authority Act No. 58 of 1995 State Information Technology Agency (SITA) Act No. 88 of 1998 Local Government Transition Act No. 209 of 1993

xiv

List of abbreviations

ABC activity-based costing AFS annual financial statementAGSA Auditor-General of the Republic of South Africa BTO budget and treasury office

CEO chief executive officer CFO chief financial officer

CIDB Construction Industry Development Board CMFM Certificate in Municipal Financial Management FMIP Financial Management Improvement Programme GRAP Generally Recognised Accounting Practice HDI Human Development Index

IAS International Audit Standards

ICT information and communications technology IDP Integrated Development Plan

ILO International Labour Organization IT information technology

LGSETA Local Government Sector Education and Training Authority MB&RR Municipal Budget and Reporting Regulations

MEC Member of the Executive Council

MFIP Municipal Finance Improvement Programme MFMA Municipal Finance Management Act

MPAC Municipal Public Accounts Committee

MTREF Medium-term Revenue and Expenditure Framework NDP National Development Plan

NEPAD New Partnership for Africa’s Development NERSA National Energy Regulator of South Africa NSBC National Small Business Council

Ntsika Ntsika Enterprise Promotion Agency

PAIA Promotion of Access to Information Act No. 2 of 2000 PAJA Promotion of Administrative Justice Act No. 3 of 2000 PFMA Public Finance Management Act

PFMAA Public Finance Management Amendment Act

PFMCDS Public Financial Management Capacity Development Strategy PMBOK project management body of knowledge

PMS performance management system PPP public–private partnership

PPPFA Preferential Procurement Policy Framework Act RDP Reconstruction and Development Programme SCM supply chain management

SDBIP Service Delivery and Budget Implementation Plan

SOC state-owned company

1

Introduction to the Municipal Finance

Management Act (MFMA) induction

programme

Learning outcomes

Although this introduction to the programme is not part of the content, it serves to set out how public financial capacity supports better service delivery, and how the MFMA, together with other pieces of legislation and regulations, serves to focus attention on what financial capacity is required. After completing this introduction, you should be able to explain the relevance of the MFMA Induction Programme for all new managers of municipalities.

Key concepts

Public service delivery – The services and the products that the government has undertaken to provide, or that communities rightfully expect to be provided with, as well as the

protection of individuals and of the public, and what they value, where it is the duty of the government to provide such protection.

Ethos – An institutional culture, and the attitude of the members of the institution concerned.

Ethics – The conduct and character of people, as well as their principles and methods of distinguishing right from wrong, and good from bad (see Chapter 5 of this guide as well). Batho Pele – The expression means ‘people first’, and is the title of the White Paper on Transforming Public Service Delivery (Republic of South Africa, 1997).

Public financial management (PFM) – PFM refers to financial accounting; management accounting; supply chain management (SCM); asset management; risk management; internal audit; internal control; governance; and transversal information management systems in the national, provincial and local spheres of government.

Public Financial Management Capacity Development Strategy (PFMCDS) – The National Treasury’s comprehensive strategy for addressing PFM capacity constraints.

Financial Management Improvement Programmes (FMIP I, II & III) – Programmes with particular key result areas geared towards the implementation of the PFMCDS.

Scene-setting questions

In the interest of setting the scene for the course, please reflect on and discuss the following: 1. Is, in your opinion, your municipality delivering services in line with its constitutional

mandate? If not, why not, and what should be done to correct the situation? 2. What is your understanding of a ‘good’ public service ethos and ethics? 3. What does a good public service ethos and ethics mean in your specific work

2

4. Given the most recent Auditor-General of South Africa’s (AGSA’s) findings and

newspaper reports, how would you describe the current general ethos and ethics in the local government sphere in South Africa?

5. How can sound financial management promote the handling of such issues as gender inequality and HIV/AIDS?

Introduction

As well as being a learner guide for a course about making a positive difference to service delivery, this is also a learner guide and a course for all managers and other officials of municipalities exercising financial management responsibilities. Such individuals must, in terms of section 78 of the Local Government: Municipal Finance Management Act No. 56 of 2003, hereinafter referred to as the MFMA, “take all reasonable steps within their respective areas of responsibility to ensure” that the machinery of service delivery is functioning as productively as is possible.

Although the title of this learner guide and induction programme refers specifically to the MFMA, the point of departure is, in the first place, the consideration of service delivery in a South African context. By ‘service delivery’, we mean those services and products that the government undertakes to provide to communities, or with which communities rightfully expect to be provided. Such delivery also refers to the protection of that which is valued by individuals and the public, where it is the duty of the government to provide protection. However, service delivery not only refers to what is provided, but also refers to how those providing the delivery generally act and interact with the recipients and beneficiaries of the services and products involved.

In a course unpacking a piece of legislation we have then, secondly, to clarify how the framework of compliance, as defined by various laws and regulations, supports service delivery. In this programme, we, therefore, wish to show how, in particular, the MFMA, together with other laws, regulations and guidelines, promotes the what and the how of service delivery by municipalities and municipal officials.

With the above in mind, our approach in this programme is to start with a relatively

comprehensive explanation of the what and the how of service delivery. We then clarify how the objective of the MFMA, together with that of other laws and regulations, is the

promotion of service delivery. We also explain why public financial capacity development among all officials, and not only among financial specialists, is important for service delivery. Each chapter of this guide specifically shows how the various financial functions under discussion impact on the work of all officials involved with service delivery.

The

what and the how

of service delivery

The national, provincial and local spheres of government in South Africa are mandated individually and jointly to deliver public services, or to ensure the delivery of public services. The Constitution of the Republic of South Africa, 1996, hereinafter referred to as ‘the Constitution’, sets out the following mandate:

Chapter 2, “Bill of Rights”, explains the rights of all people in the country. These rights reflect that which individuals have a right to value, and which the

3

Chapter 3, “Co-operative Governance”, sets out the principles underpinning the joint responsibility of all spheres of government for service delivery.

Chapter 4, “Parliament”, and Chapter 5, “The President and National Executive”, as well as Schedule 4, explain the functioning of the national legislature and executive in terms of service delivery.

Chapter 6, “Provinces”, and Schedules 4 and 5 explain the functioning of the provincial governments in terms of service delivery.

Chapter 7, “Local Government”, and Schedules 4 and 5 explain the municipal service delivery mandate.

A constitutional democracy requires checks and balances, and therefore the Constitution provides for courts and for the administration of justice, as well as for state institutions supporting constitutional democracy in Chapters 8 and 9. The functions of AGSA, as provided for in section 188, are of particular relevance in this programme.

Chapter 10, “Public Administration”, specifically directs what and how service delivery should take place in terms of section 195, “Basic values and principles governing public administration”.

Given that the right to protection is regarded as part of service delivery, the Constitution makes specific provision for security services in Chapter 11. Chapter 12, “Traditional Leaders”, contributes to institutionalising the South

African context in which service delivery must be provided in a culturally sensitive way.

Finally, Chapter 13, “Finance”, is again of particular interest, because the chapter, among others, provides for: equitable shares and allocations of revenue (section 214); budgets for all spheres of government (section 215); treasury control (section 216); and procurement by all spheres of government (section 217).

In the light of South African citizens being very much aware of how their rights are protected by the Constitution, they have come publicly to demonstrate their expectations and to protest against poor service delivery performance in no uncertain terms. The pressure for service delivery is, consequently, great, especially as it is heightened even further by a very high expectation of development. Section 195 (1) (c) of the Constitution specifically instructs that public administration must be development-oriented, which means that the lives of those who live under unfavourable conditions must be improved as part of service delivery. The requirement for such delivery exerts an extreme demand for a high level of performance on the service delivery mechanisms of the government, and on the shoulders of all

government officials. In order to maximise the provision of public services and products utilising the available resources, abiding by the three principles of efficiency, economy and effectiveness in resource application is essential. The Constitution, accordingly, provides for the promotion of the “efficient, economic and effective use of resources” (section 195 (1) (b)).

However, the maximisation of service delivery through a high level of performance requires the creation of an ethos or culture of service delivery that will enable the public to benefit from each official performing at their utmost best. The cultivation of a favourable ethos is dependent on all officials who deal with the public exhibiting a positive attitude. For this reason, The White Paper on Transforming Public Service Delivery (Republic of South Africa,

4

1997), titled “Batho Pele” (a Sesotho word meaning ‘people first’), was launched with a view to impacting on the skills and attitudes of the officials who are required to develop such a culture. The Batho Pele slogan ‘We belong, we care, we serve’, and its eight principles of (1) consultation; (2) known service standards; (3) redress, where these first two principles are not met; (4) equal access; (5) courtesy; (6) information; (7) openness and transparency; and (8) value for money, stipulate how the public should be served (see Chapter 3 of this guide). Specific to local government, Schedules 1 and 2 of the Local Government: Municipal Systems Act No. 32 of 2000, hereinafter referred to as the Municipal Systems Act, provide codes of conduct for municipal councillors and officials, respectively. Apart from contributing to the service delivery ethos or culture mentioned above, said codes of conduct also promote the notion of ethics. A service delivery ethos is based on the conduct and character of people, and on their principles and methods of distinguishing right from wrong, and good from bad. Regardless of differences in social background, culture, religious beliefs, or any other deeply embedded frame of reference of individual officials, ethical norms provide a common universal framework for the practice of acceptable behaviour. If there is a perception among the public that public office-bearers and officials are not adhering to this common universal framework for acceptable behaviour, for example due to their use of public resources for self-enrichment, and/or their due to their abuse of their positions for personal gain, and/or them acting with prejudice (i.e. being corrupt, or allowing corruption to take place, rather than acting with total integrity), the service delivery concerned is likely to be viewed with suspicion.

How the MFMA promotes enhanced levels of service delivery

The MFMA should certainly not be seen as legislation that was written for such municipal finance specialists as accountants and auditors. The Act should also not be seen as so restrictive that it enforces such an extent of compliance that there is no room for discretion and innovation among managers at any level of a municipality. In the paragraphs above, we alluded to the fact that the recipients and the beneficiaries of public services, especially given the developmental context, expect more services for comparatively less cost. Such

expectations can only be met if efficiency, economy and effectiveness in delivery is

maximised, and the relevant office-bearers’ and officials’ actions bear witness to a service- oriented ethos and to the highest standards of ethics.

The object of the MFMA is to ensure that this expectation is realised, by means of all officials concerned adhering to the set prescripts. In addition, the norms and standards involved should create room for discretion, and, therefore, for innovation, in such a manner that all financial risks are kept under control. In the words of section 2 of the MFMA, “[t]he object of this Act is to secure sound and sustainable management of the fiscal and financial affairs of municipalities and municipal entities by establishing norms and standards and other requirements” for all financial actions, transactions and other financial matters of

municipalities and municipal entities, as well as national and provincial organs of state, to the extent of their financial dealings with municipalities (MFMA, section 3).

Chapter 8 of the MFMA deals with the responsibilities of municipal officials. Section 78, in particular, makes better service delivery than was delivered in the past the business of each official who exercises financial responsibilities. It is impossible to separate any form of

5

management discretion from the exercising of financial responsibilities, and section 78 will, therefore, be a recurring premise in unpacking the financial functions of all officials who are involved in this programme. It is worthwhile, therefore, to quote section 78 in its entirety:

“78 Senior managers and other officials of municipalities

(1) Each senior manager of a municipality and each official of a municipality exercising financial management responsibilities must take all reasonable steps within their respective areas of responsibility to ensure –

(a) that the system of financial management and internal control established for the municipality is carried out diligently;

(b) that the financial and other resources of the municipality are utilised effectively, efficiently, economically and transparently;

(c) that any unauthorised, irregular or fruitless and wasteful expenditure and any other losses are prevented;

(d) that all revenue due to the municipality is collected;

(e) that the assets and liabilities of the municipality are managed effectively and that assets are safeguarded and maintained to the extent necessary;

(f) that all information required by the accounting officer for compliance with the provisions of this Act is timeously submitted to the accounting officer; and

(g) that the provisions of this Act, to the extent applicable to that senior manager or official, including any delegations in terms of section 79, are complied with.”

The provisions of the MFMA in general, and of section 78 in particular, promote improved service delivery by seeing to the focused and well-controlled application of resources for service delivery, and, for such purpose, seeing that the business of each official concerned should be the exercising of the appropriate form of discretion.

The need for financial management capacity development

Section 216 of the Constitution and section 5 of the MFMA have assigned the function of supervision, including promoting the objects of the MFMA and taking any appropriate steps to do so, over local government financial matters to the National Treasury. Financial

management capacity development is indispensable as one such appropriate step. In this introduction to the programme, the relevance of the MFMA Induction Programme as part of the comprehensive PFMCDS is explained, the target audience identified, and the overarching goal, objectives and outcomes defined.

The MFMA Induction Programme as part of a comprehensive PFMCDS

The National Treasury has developed a comprehensive PFMCDS in partnership with the relevant stakeholders (National Treasury, 2012). This strategy contains an integrated capacity development framework that is structured to ensure that all capacity development efforts serve a common strategic purpose. The strategy also provides direction for capacitydevelopment in the environmental, institutional, organisational, individual and stakeholder dimensions to be interrelated, so as to ensure sustainability. The capacity development initiatives must, therefore, be part of a holistic and integrated strategy, with clarity regarding the interdependence of the key elements concerned.

6

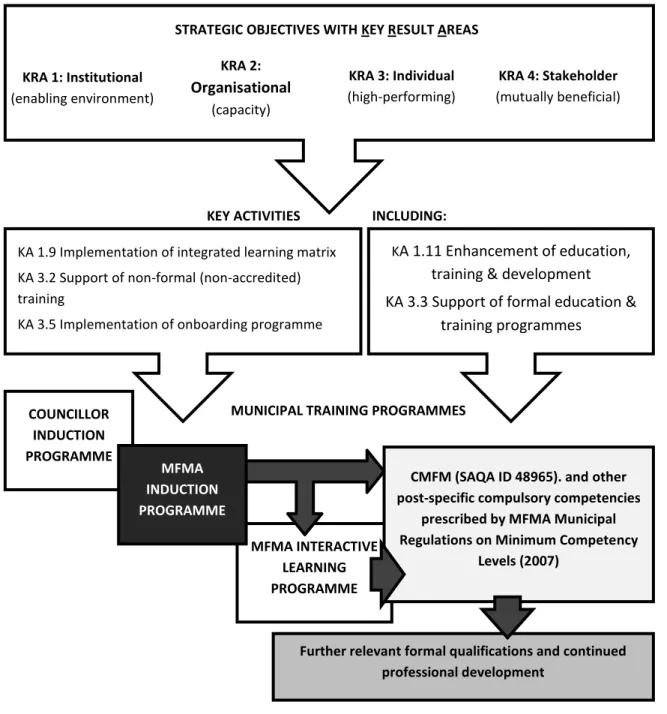

Four capacity development pillars, namely institutional, organisational, individual and stakeholder pillars, support the strategy. The strategy, in turn, has four strategic objectives, each with a set of key activities to support them. Although these are not fully explained in this learner guide, Figure 1 depicts the link between the national CDS and the MFMA Induction Programme, as well as other relevant MFMA programmes, and further relevant formal qualifications and continued professional development. The diagram depicts the MFMA Induction Programme as a non-accredited onboarding programme that forms part of the integrated learning matrix.

The MFMA Interactive Learning Programme, in turn, is shown on the diagram to be concomitant with the MFMA Induction Programme. The former programme provides the opportunity for municipal officials to enhance their MFMA knowledge, either as groups or individuals, at a pace that is convenient to the group or individual. It is a fully computerised, interactive learning programme, including assessment and certification.

7

Figure 1: MFMA Induction Programme as part of the national Capacity Development Strategy

The Councillor Induction Programme, which is also depicted as being concomitant with the MFMA Interactive Learning Programme, was designed to help executive mayors or

committees and non-executive councillors, working together with municipal officials, to implement legislation that would bring about the reform of municipal financial management practices across South Africa. The programme explains how the municipal finance system, and the councillors’ role within it, works (National Treasury, 2006).

The comprehensive Certificate in Municipal Financial Management (CMFM, SAQA ID 48965), supplemented with other compulsory unit standards, is a programme that is intended for municipal accounting officers, chief financial officers (CFOs), senior managers, other financial officials; heads of SCM and SCM officials, in adherence to the prescriptions of sections 83,

KRA 1: Institutional (enabling environment) KRA 2: Organisational (capacity) KRA 3: Individual (high-performing) KRA 4: Stakeholder (mutually beneficial)

STRATEGIC OBJECTIVES WITH KEY RESULT AREAS

KA 1.9 Implementation of integrated learning matrix KA 3.2 Support of non-formal (non-accredited) training

KA 3.5 Implementation of onboarding programme

KA 1.11 Enhancement of education, training & development KA 3.3 Support of formal education &

training programmes

KEY ACTIVITIES INCLUDING:

MFMA INTERACTIVE LEARNING PROGRAMME

MUNICIPAL TRAINING PROGRAMMES COUNCILLOR

INDUCTION PROGRAMME

CMFM (SAQA ID 48965). and other post-specific compulsory competencies

prescribed by MFMA Municipal Regulations on Minimum Competency

Levels (2007)

Further relevant formal qualifications and continued professional development

MFMA INDUCTION PROGRAMME

8

107 and 119 of the MFMA and of the Municipal Regulations on Minimum Competency Levels (Republic of South Africa, 2007). As the CMFM and other compulsory unit standards are accredited and quality controlled by the Local Government Sector Education and Training Authority (LGSETA), an opportunity for accessing further relevant formal education programmes and continued professional development is provided. Given the time and financial constraints experienced, prospective participants must carefully consider for which unit standards they should enrol, by first prioritising the unit standards that they should obtain in order to attain competence in their particular posts.

Target audience for this MFMA Induction Programme

The MFMA Induction Programme targets all new managers in the local government sector. The course is aimed at overcoming the existing disjuncture between the understanding and the practices of new entrants in the municipal finance environment, and the ethics and the ethos that is required in public finance. Limited understanding of the roles and

responsibilities in terms of, and non-compliance with, the MFMA is exacerbating the problem as it is currently being experienced. The National Treasury wishes the intended course to be compulsory, so that it can follow on within three months of an individual entering the municipal environment and signing the necessary performance agreements.

Goal, objectives and outcomes of the Induction Programme

The overarching goal of this non-accredited five-day MFMA Induction Course is to provide local government managers with a broad overview and understanding of the public sector ethos and ethics, including the municipal service delivery mandate, as well as the municipal finance environment and MFMA reforms. This understanding should serve as a stepping stone to be crossed in order to gain increased in-depth learning and professionalisation by means of following further accredited training and education programmes. The following five objectives are set, namely for the participants to understand and relate their own position to:

the vision and underlying principles of the MFMA;

the roles and responsibilities in municipal finance emanating from the MFMA; municipal service delivery planning and implementation;

supply-chain management, alternative service delivery mechanisms and contract management; and

reporting and control.

In the above-mentioned five objectives, the emphasis is placed on the provisions in the MFMA. However, it must be kept in mind that the MFMA forms part of a much more comprehensive framework of legislation, all contributing to ensure enabled,

well-capacitated, high-performing, well-integrated, and sustainable municipal service delivery. Given said five objectives, the following outcomes stand to be achieved:

Objective 1 is to show understanding of the vision and the underlying principles of the MFMA, in proof of the attainment of which the participants must be able to explain the concepts of:

the roles of national and provincial government in municipal financial management;

9

the legislation and governance framework of municipal finance; the vision of a modernised municipal financial system; and

the underlying principles of a modernised municipal financial system. Objective 2 is to show understanding of the municipal finance roles and the

responsibilities emanating from the MFMA, in proof of the attainment of which the participants must be able to explain the concepts of:

the distinctive roles and responsibilities of the council, the executive and the officials;

the responsibilities of top management and delegation for the accounting officer; and

the governance structure for the budget and the treasury.

Objective 3 is to show understanding of municipal service delivery planning and implementation, in proof of the attainment of which the participants must be able to explain the concepts of:

three-year budgeting and planning; costing and capital planning; and asset management.

Objective 4 is to show understanding of supply-chain management, alternative service delivery mechanisms and contract management, participants must be able to explain:

o Supply-chain management;

o Alternative service delivery mechanisms; o Contract management.

Objective 5 is to show understanding of municipal reporting and control, in proof of the attainment of which the participants must be able to explain the functioning of: in-year reporting;

MFMA performance monitoring; annual reports;

risk management;

internal control processes, audits and audit committees; and

external audit as consolidated and independent finding on performance.

Summary

This introduction has served to explain:

the what and the how of service delivery;

how the MFMA promotes better service delivery;

the need for financial management capacity development;

how the MFMA Induction Programme fits into the comprehensive PFMCDS; who the target audience is; and

10

PART ONE

VISION AND UNDERLYING PRINCIPLES

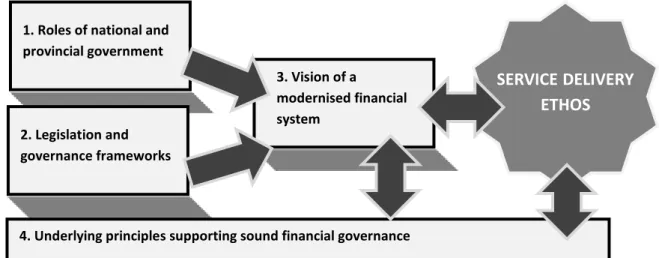

In order to show understanding of the vision and the underlying principles of the MFMA as the first objective of this programme, the participants must be able to explain: the roles of national and provincial government in municipal financial management; the legislation and governance framework of municipal finance; the vision of a modernised municipal financial system; and the underlying principles supporting sound financial governance (see Figure 2 below).Figure 2: Vision and underlying principles of the MFMA

1. Roles of national and provincial government 2. Legislation and governance frameworks 3. Vision of a modernised financial system

4. Underlying principles supporting sound financial governance

SERVICE DELIVERY

ETHOS

11

Chapter 1: Roles of national and provincial

government

1.1.

Learning outcomes

After completing this chapter, you should be able to explain:

how your own position and responsibilities may be informed and affected by the roles of national and provincial government in PFM; and

how your municipality’s mandate may be informed and affected by the roles of national and provincial government in financial management.

1.2.

Key concepts

Cooperative relationship – Section 154 of the Constitution determines that national and provincial governments, by legislative and other measures, must support and strengthen the capacity of municipalities.

Spheres of government – Section 40 of the Constitution determines that the government is constituted as national, provincial and local spheres of government that are distinctive (with each having a specific constitutional and legislative mandate), interdependent (with each sphere depending on the others to fulfil its specific mandate), and interrelated (with the fulfilment of public value outcomes only being able to be achieved by the combined effort of the three spheres).

National Treasury – Said Treasury was established in terms of section 216 of the Constitution to ensure both transparency and expenditure control in each sphere of the government. Provincial Treasuries – Said Treasuries were established in terms of section 17 of the Public Finance Management Act No. 1 of 1999, hereinafter referred to as the PFMA, as amended by the Public Finance Management Amendment Act No. 29 of 1999.

Division of Revenue Act – The Act is an annual Act of Parliament that was promulgated to provide for the equitable division of nationally generated revenue among all spheres of the government, in terms of section 214 of the Constitution.

National Treasury Regulations – The Regulations are promulgated in terms of section 76 of the PFMA, or in terms of section 168 of the MFMA, which are considered to be part of the two above-mentioned Acts.

National Treasury Circulars – Guidelines for municipalities, issued from time to time in terms of section 168 of the MFMA.

1.3.

Scene-setting questions

1. How does the involvement of national and provincial government in municipal finance affect your own work responsibilities?

2. How do the oversight and support roles of national and provincial government, and related state-owned companies, affect your area of responsibility, with specific

12

focus on: planning alignment; funding; service delivery; service standards; and financial reporting?

3. What are the possible challenges in the cooperation actions taken between your municipality and the national and provincial governments regarding financial matters, and how can these be mitigated?

1.4.

Introduction

The MFMA and the Municipal Systems Act require the maintenance of a close, cooperative relationship within, and between, the different spheres of government, especially in terms of planning, budgeting and financial management, as well as in areas of service delivery. The MFMA provides a role for national and provincial government to support, to build capacity and to monitor municipalities, while providing mechanisms in which such sector-specific regulators as the National Energy Regulator of South Africa (NERSA) and such parastatals as ESKOM, the Land Bank and other public entities are required to engage with municipalities. The roles of national and provincial government in a modernised municipal financial system are highlighted in this chapter.

1.5.

Where the individual municipal official fits into the picture

As a manager with an area of responsibility somewhere within the line or support services of your municipality, your actions are determined by your own particular field of professional expertise. Said field must inform what and how you directly, or indirectly, contribute to service delivery in the most effective, efficient and economic manner, but subject to the directives of your delegation, or assigned area of responsibility, and within the provisions of the Integrated Development Plan (IDP), as the strategic plan of the municipality. In addition, you must also be aware of the roles that the national and provincial departments and other regulatory authorities and parastatals play with regard to the sector in which you work, and the financial actions that you take.

1.6.

National government

The National Treasury and various national departments play a role in municipal service delivery in general, and in financial matters in particular. Said Treasury is responsible for prescribing all regulations, frameworks, budget formats, inflation limits, and other information required by the MFMA to ensure uniform norms and standards for implementation.

The monitoring and reporting obligations of municipalities allow for providing early warning and efficient responses in the case of municipalities experiencing financial distress, with appropriate interventions being instituted to ensure that the municipalities concerned recover. Formal or informal interventions by the National Treasury are necessary only where all other options have failed.

The informal process can take the form of technical support by the National Treasury through the Municipal Finance Improvement Programme (MFIP), and, on request, by the municipality. Said Treasury can also provide support to municipalities that request assistance in developing financial recovery plans, in line with Chapter 13 of the MFMA.

13

Formal intervention occurs when municipalities are in material breach of National Treasury-prescribed measures, including section 216 of the Constitution, and section 38 and Chapter 13 of the MFMA, among others.

Other national government departments also have a key role to play in policy development and in the execution of programmes in provinces and municipalities. Such national

departments as the Department of Cooperative Governance have an overarching

responsibility for strengthening cooperative governance, while such departments as those of Water Affairs, Mineral Resources, Energy, Transport and Human Settlements have a direct role to play in monitoring sector-specific outcomes and service delivery. Therefore, the production of relevant documentation addressing the needs of the various sectors progressively serves to make the monitoring of responsibilities less onerous for the municipalities and the departments concerned. In this regard, it is imperative that the municipalities should prepare their capital and operating budgets, in-year reporting, and annual reports with the above factor in mind, and that they should provide information in support of decision-making.

A uniform set of data and budget formats is, therefore, required in the MFMA, resulting in the National Treasury issuing regulations to ensure the adequacy of information reported. Municipalities must also be aware of the provisions that are made in the annual Division of Revenue Act, and of the guidance provided in the various National Treasury MFMA circulars.

1.7.

Provincial government

Section 154 of the Constitution determines that the national and provincial governments, by legislative and other measures, must support and strengthen the capacity of municipalities to manage their own affairs, to exercise their powers, and to perform their functions. Section 155 (6) (a) and (b) provide for the monitoring and support of local government in the

provinces and promote the development of local government capacity. Section 139 of the Constitution further determines that a provincial executive may intervene if a municipality fails to fulfil an obligation to which they are bound. Such intervention is possible if a

municipality fails to approve a budget, or if it fails to approve any revenue-raising measures that are necessary to give effect to the budget. However, such intervention is temporary, and it is aimed at correcting the municipality, and enabling it to exercise its powers and to

perform its duties.

Provincial treasuries must, among other duties, promote the object of the MFMA within the framework of cooperative government, and they must assist the National Treasury in enforcing compliance with the measures established in terms of section 216 (1) of the Constitution, as well as those that have been established in terms of the MFMA. The MFMA also requires provincial treasuries to monitor municipal compliance of the MFMA, and to assist in preparing the budget. A provincial treasury is required to work closely with other provincial departments, such as Local Government, Human Settlements, and Health, in order to implement the MFMA.

14

1.8.

Summary

The Constitution determines that the government is constituted as national, provincial and local spheres of government that are distinctive, interdependent and interrelated. The Constitution also determines that national and provincial governments, by legislative and other measures, must support and strengthen the capacity of municipalities to manage their own affairs, to exercise their powers, and to perform their functions

The National Treasury is responsible for prescribing all regulations, frameworks, budget formats, inflation limits, and other information to ensure uniform norms and standards for implementation, and to institute appropriate interventions where municipalities experience financial distress. Formal or informal interventions by the National Treasury are necessary only where all other options have failed.

A provincial executive may intervene if a municipality fails to fulfil an obligation, including where it fails to approve a budget or any revenue-raising measures that are necessary to give effect to the budget. Provincial treasuries must promote the object of the MFMA within the framework of cooperative government, and they must assist the National Treasury in enforcing compliance with the measures established in terms of section 216 (1) of the Constitution, as well as those that are established in terms of the MFMA.

15

Chapter 2: Legislation and governance

frameworks

2.1.

Learning outcomes

After completing this chapter, you should be able to explain:

how your own area of responsibility is affected by the framework of legislation; the enabling nature of the framework of legislation in municipal service delivery; the nature of provisions in the Constitution for municipal service delivery; and the specific relevance of interrelated matters between the MFMA and the

Municipal Systems Act directed at municipal service delivery.

2.2.

Key concepts

Enabling legislation – Legislation by which the legislature grants authority to take certain actions.

Integrated development planning – Municipal strategic planning, as prescribed in Chapter 5 of the Municipal Systems Act.

Corporate performance management system (PMS) – A system that is established and implemented as prescribed in Chapter 6 of the Municipal Systems Act.

2.3.

Scene-setting questions

1. Select three pieces of legislation that are relevant to your position from Table 1, and explain how each directly and/or indirectly impacts on your work.

2. What impact do the principles of cooperative government and intergovernmental relations, as provided for in the Constitution, make on your area of responsibility? 3. How do the MFMA and the Municipal Systems Act, as interrelated pieces of legislation,

facilitate and assist you in fulfilling your responsibilities in the workplace?

2.4.

Introduction

The municipal financial management system is framed, supported and enabled by a variety of laws and regulations that municipalities must consider in their day-to-day activities. This chapter provides a list of some of the applicable pieces of legislation, as well as an

explanation of the nature of provisions in the Constitution for municipal service delivery. It also explains and illustrates how the MFMA and the Municipal Systems Act are interrelated to enable municipal service delivery.

2.5.

Where the individual municipal official fits into the picture

As manager with an area of responsibility somewhere within the line or support services of your municipality, your actions are determined by means of legislation, regulations and professional codes relating to your own profession and/or field of professional expertise that must inform the manner in which you operate within your assigned area of responsibility. However, you also have to fulfil such obligations within the framework of legislation that is16

specific to local government, as well as being able to interpret the various pieces of legislation as interrelated parts of the same picture.

2.6.

The framework of legislation

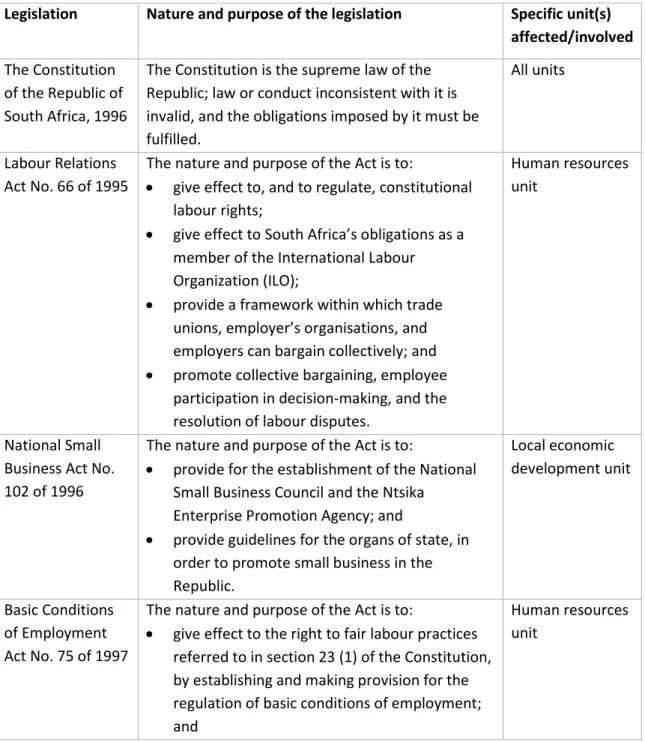

Table 1 below lists and explains the legislation and its nature and purpose relating to the provision of a framework for a modernised municipal financial system. The financial

implications of this framework can be derived from the nature and purpose of the legislation, which is explained in the second column of said table. The specific unit that is stated in the third column of the table serves to identify the unit that is primarily affected, or which is involved by way of input/output. The stipulated units are, however, not exclusively affected or involved. In fact, each position in a municipality is directly or indirectly affected by the legislation enumerated.

Table 1: Legislation providing a framework for a modernised financial system

Legislation Nature and purpose of the legislation Specific unit(s) affected/involved The Constitution

of the Republic of South Africa, 1996

The Constitution is the supreme law of the Republic; law or conduct inconsistent with it is invalid, and the obligations imposed by it must be fulfilled.

All units

Labour Relations Act No. 66 of 1995

The nature and purpose of the Act is to:

give effect to, and to regulate, constitutional labour rights;

give effect to South Africa’s obligations as a member of the International Labour Organization (ILO);

provide a framework within which trade unions, employer’s organisations, and employers can bargain collectively; and promote collective bargaining, employee

participation in decision-making, and the resolution of labour disputes.

Human resources unit

National Small Business Act No. 102 of 1996

The nature and purpose of the Act is to:

provide for the establishment of the National Small Business Council and the Ntsika

Enterprise Promotion Agency; and

provide guidelines for the organs of state, in order to promote small business in the Republic. Local economic development unit Basic Conditions of Employment Act No. 75 of 1997

The nature and purpose of the Act is to:

give effect to the right to fair labour practices referred to in section 23 (1) of the Constitution, by establishing and making provision for the regulation of basic conditions of employment; and

Human resources unit

17

ensure compliance with the obligations of the Republic as a member state of the International Labour Organisation.

Intergovernmental Fiscal Relations Act No. 97 of 1997

The nature and purpose of the Act is to:

promote cooperation between the national, provincial and local spheres of government on fiscal, budgetary and financial matters; and prescribe a process for the determination of an

equitable sharing and allocation of revenue raised nationally.

Office of the Municipal Manager

Housing Act No. 107 of 1997

The nature and purpose of the Act is to: provide for the facilitation of a sustainable

housing development process;

lay down general principles that are applicable to housing development in all spheres of government;

define the functions of national, provincial and local governments, in respect of housing development;

provide for the establishment of a South African Housing Development Board, for the continued existence of provincial boards under the name of provincial housing development boards, and for the financing of national housing programmes.

Housing unit

Water Services Act No. 108 of 1997

The nature and purpose of the Act is to:

provide a framework for the provision of water supply and sanitation services to households in South Africa;

set the standards for the local and provincial agencies, and establishes the norms and standards for tariffs; and

set out the rights and duties of the State and of water services providers in monitoring water services, and promotes effective water resource management.

Water unit

Remuneration of Public Office Bearers Act No. 20 of 1998

The nature and purpose of the Act is to:

provide for a framework for determining the salaries and allowances of the President, members of the National Assembly, permanent delegates to the National Council of Provinces, Deputy President, Ministers, Deputy Ministers, traditional leaders, members of provincial Houses of Traditional Leaders, and members of

Office of the Municipal Manager

18

the Council of Traditional Leaders;

provide for a framework for determining the upper limit of salaries and allowances of Premiers, members of Executive Councils, members of provincial legislatures and members of Municipal Councils; and provide for a framework for determining

pension and medical aid benefits of office-bearers. Local Government: Municipal Demarcation Act No. 27 of 1998 (Demarcation Act)

The nature and purpose of the Act is to provide for criteria and procedures for the determination of municipal boundaries by an independent authority.

Office of the Municipal Manager

National Water Act No. 36 of 1998

The nature and purpose of the Act is to provide for the fundamental reform of the law relating to water resources.

Water unit

Employment Equity Act No. 55 of 1998

The nature and purpose of the Act is to:

promote the constitutional right of equality and the exercise of true democracy;

eliminate unfair discrimination in employment; ensure the implementation of employment

equity to redress the effects of discrimination; achieve a diverse workforce that is broadly

representative of our people;

promote economic development and efficiency in the workforce; and

give effect to the obligations of the Republic as a member of the International Labour

Organisation.

Human resources unit

State Information Technology Agency (SITA) Act No. 88 of 1998

The nature and purpose of the Act is to establish a company that is responsible for the provision of information technology services to the public administration. Office of the Municipal Manager Local Government: Municipal

Structures Act No. 117 of 1998 (Municipal Structures Act)

The nature and purpose of the Act is to:

provide for the establishment of municipalities, in accordance with the requirements relating to the categories and types of municipality; establish criteria for determining the category

of municipality to be established in a specific area;

define the types of municipality that may be established within each category;

provide for an appropriate division of functions

Office of the Municipal Manager

19

and powers between categories of municipality;

regulate the internal systems, structures and office-bearers of municipalities; and

provide for appropriate electoral systems. Skills

Development Act No. 97 of 1998

The nature and purpose of the Act is to:

provide an institutional framework to devise and implement national, sector and workplace strategies to develop and improve the skills of the South African workforce;

integrate those strategies within the National Qualifications Framework contemplated in the South African Qualifications Authority Act No. 58 of 1995;

provide for learnerships that lead to recognised occupational qualifications;

provide for the financing of skills development by means of a levy-financing scheme and a National Skills Fund; and

provide for, and regulate, employment services.

Human resources unit

Rental Housing Act No. 50 of 1999

The nature and purpose of the Act is to:

define the responsibility of the government, in respect of rental housing property;

create mechanisms to promote the provision of rental housing property;

promote access to adequate housing, by means of creating mechanisms to ensure the proper functioning of the rental housing market; make provision for the establishment of rental

housing tribunals;

define the functions, powers and duties of such tribunals;

lay down general principles governing conflict resolution in the rental housing sector; and provide for the facilitation of sound relations

between tenants and landlords, and, for this purpose, to lay down general requirements relating to leases. Housing unit Local Government: Municipal Systems Act No. 32 of 2000 (Municipal Systems Act)

The nature and purpose of the Act is to:

provide for the core principles, mechanisms and processes that are necessary to enable municipalities to move progressively towards the social and economic upliftment of local communities, and to ensure universal access to essential services that are affordable to all;

Office of the Municipal Manager

20

define the legal nature of a municipality as including the local community within the municipal area, working in partnership with the municipality’s political and administrative structures;

provide for the manner in which municipal powers and functions are exercised and performed;

provide for community participation;

establish a simple and enabling framework for the core processes of planning, performance management, resource mobilisation, and organisational change that underpin the notion of developmental local government;

provide a framework for local public administration and human resource development;

empower the poor, and ensure that

municipalities put in place service tariffs and credit control policies that take their needs into account by providing a framework for the provision of services, service delivery agreements, and municipal service districts; provide for credit control and debt collection; establish a framework for support, monitoring

and standard setting by other spheres of government in order to progressively build local government into an efficient frontline

development agency that is capable of integrating the activities of all spheres of government for the overall social and economic upliftment of communities, in harmony with their local natural environment; and

provide for legal matters pertaining to local government. Promotion of Access to Information Act No. 2 of 2000 (PAIA)

The nature and purpose of the Act is to give effect to the constitutional right of access to any

information held by the State, and to any information that is held by another person, and that is required for the exercise or protection of any right(s). Office of the Municipal Manager Promotion of Administrative Justice Act No. 3 of 2000 (PAJA)

The nature and purpose of the Act is to give effect to the right to administrative action that is lawful, reasonable and procedurally fair, and to the right to written reasons for administrative action, as

Office of the Municipal Manager

21

contemplated in section 33 of the Constitution Promotion of Equality and Prevention of Unfair Discrimination Act No. 4 of 2000

The nature and purpose of the Act is to:

give effect to section 9, read with item 23 (1) of Schedule 6 of the Constitution, so as to prevent and prohibit unfair discrimination and

harassment;

promote equality and eliminate unfair discrimination; and

prevent and prohibit hate speech.

Human resources unit

Local

Government: Municipal Electoral Act No. 27 of 2000

The nature and purpose of the Act is to regulate all municipal elections held after the date determined in terms of section 93 (3) of the Municipal

Structures Act. Office of the Municipal Manager Municipal Performance Management Regulations, 2001

The purpose of the Regulations is to set out in detail the requirements for municipal PMSs. The regulations must entail a framework that describes and represents how the municipality’s cycle and process of performance management, including measurement, review, reporting and improvement, will be conducted. Office of the Municipal Manager Broad-Based Black Economic Empowerment Act, No. 53 of 2003

The nature and purpose of the Act is to:

establish a legislative framework for the promotion of black economic empowerment;

empower the Minister to issue codes of good practice and publish transformation charters; and

establish the Black Economic Empowerment Advisory Council. Finance unit Local Government: Municipal Finance Management Act No. 56 of 2003 (MFMA)

The nature and purpose of the Act is to:

secure sound and sustainable management of the financial affairs of municipalities and other institutions in the local sphere of government; and

establish treasury norms and standards for the local sphere of government.

Office of the Municipal Manager (as Accounting Office) Finance unit Division of Revenue Act (annual)

The nature and purpose of the Act is to provide for the equitable division of revenue raised nationally among the national, provincial and local spheres of government for the 20xx/xx financial year, and for the responsibilities of all three spheres pursuant to such division. Office of the Municipal Manager (as Accounting Office) Finance unit Local Government: Property Rates Act

The nature and purpose of the Act is to:

regulate the power of a municipality to impose rates on property;