BANK BETTER HAVE MY MONEY: CRISES, DEMOCRATIC INSTITUTIONS, AND GOVERNMENT BANK ACQUISITIONS

Devin Case-Ruchala

A thesis submitted to the faculty of the University of North Carolina at Chapel Hill in partial fulfillment of the requirements for the degree of Master of Arts in the Department of Political Science.

Chapel Hill 2019

Approved by:

Layna Mosley

Cameron Ballard-Rosa

ABSTRACT

Devin Case-Ruchala: Bank Better Have My Money: Crises, Democratic Institutions, and Government Bank Acquisitions

(Under the direction of Layna Mosley)

ACKNOWLEDGEMENTS

TABLE OF CONTENTS

LIST OF TABLES . . . vii

LIST OF FIGURES . . . viii

1. INTRODUCTION . . . 1

2. POLITICAL ECONOMY OF GOVERNMENT BANK OWNERSHIP & ITS LIMITS . . . 6

3. CRISES, RESPONSES TO CRISES & DEMOCRATIC INSTITUTIONS . . . 9

4. RESEARCH DESIGN . . . 15

4.1 Empirical Models . . . 15

4.2 Data . . . 16

5. RESULTS . . . 21

5.1 Aggregate Effect of Regime Type . . . 21

5.2 Mechanisms: Political Competition & Freedom of Expression . . . 24

5.3 Mechanisms: Other Correlates of Democracy . . . 25

6. ROBUSTNESS CHECK: ACCOUNTING FOR FINANCIAL INTEGRATION . . . 30

6.1 Why Financial Integration? . . . 30

6.2 Approach, Empirical Models, & Data . . . 32

6.3 Results . . . 35

7. CONCLUSION . . . 43

Summary Statistics . . . 47

Additional Tables . . . 50

Additional Figures . . . 57

LIST OF TABLES

1 Model results with crisis dummy . . . 22

2 Model results with neighbor crisis weight interaction . . . 35

3 Model results with centrality control . . . 42

4 Summary statistics (all variables) . . . 47

5 Model results with executive constraints interaction . . . 51

6 Model results with political competition interaction . . . 52

7 Model results with freedom of expression interaction . . . 53

8 Model results with central bank independence interaction . . . 54

9 Model results with property rights interaction . . . 55

LIST OF FIGURES

1 Distribution of percent of bank assets acquired (with U.S.) . . . 17

2 Distribution of percent of bank assets acquired (without U.S.) . . . 18

3 Marginal effect of crisis by polity . . . 23

4 Marginal effect of crisis by political competition . . . 24

5 Marginal effect of domestic crisis by freedom of expression . . . 25

6 Marginal effect of crisis by executive constraints . . . 26

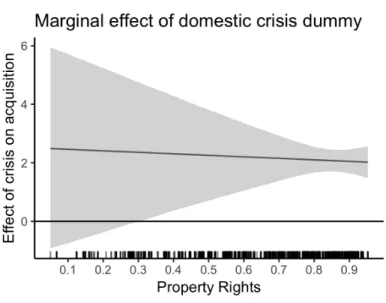

7 Marginal effect of crisis by property rights . . . 27

8 Marginal effect of crisis by political corruption . . . 28

9 Marginal effect of crisis by central bank independence . . . 28

10 Marginal effect of neighbor crisis weight by polity . . . 36

11 Marginal effect of neighbor crisis weight by political competition & freedom of expression . . . 37

12 Network plot of global financial system colored by regime type (2006) . . . 39

13 Results of AME network model . . . 40

14 Conditional effect of crisis by polity (with centrality control) . . . 41

15 Correlation matrices . . . 48

16 Distribution of outcome variable (vs. logged outcome). . . 49

17 Outcome variable ordered by country-year (& logged outcome) . . . 50

18 Acquisitions as % of GDP (all sectors) . . . 57

19 Sector breakdown of total volume of acquisitions . . . 57

20 Marginal effect of crisis by other mechanisms. . . 58

21 Network plot by regime type (2001; 2003; 2009; 2012) . . . 59

1. INTRODUCTION

The degree of government involvement in the management of private market activity is subject to significant historical variation and debate. The decades leading up to the twenty-first century can be characterized as entailing a parallel worldwide trend towards increasing democratization along with economic integration and financial liberalization (Bernhard and Leblang, 1999; Milner and Kubota, 2005; Pandya, 2014). The era preceding that, meanwhile, was characterized by what Karl Polanyi described as a re-embedding of the state in the market among Western industrialized nations after the Great Depression revealed the limits of laissez faire economics, and in particular, unregulated financial markets (Polanyi and MacIver, 1944; Blyth et al., 2002). Subsequent decades saw the construction of robust welfare states in the developed world (Esping-Andersen, 1990). Outside of the developed world, the Cold War saw the maintenance and spread of state-led communist regimes while other developing countries on the global periphery turned to import-substitution industrialization strategies to grow their developmental states (Lange and Rueschemeyer, 2005). This trajectory of government-mediated economic growth continued up through the 1970s, when the collapse of the Bretton Woods monetary system and stagflation challenged the dominance of Keynesian economic theory that had partly informed the re-embedding of the state in governing market activities in the post-WWII era, turning the global trajectory of government-market relations back towards laissez faire fundamentals and a process of government disembedding (Blyth et al., 2002).

that government ownership and management within the financial industry will be reserved for those countries still struggling to compete in global markets (requiring more state-led development) or less democratic countries governed by leaders with corrupt political interests (La Porta et al., 2002; Megginson, 2005).

However, I argue that these assumptions and prior accounts of what motivates greater government involvement in the form of direct ownership within the financial industry do not adquately explain historical waves of increased government ownership, and in particular the most recent wave of increased government ownership through acquisitions occuring in the beginning of the twenty-first century after this long period of dis-emebedding and financial liberalization.1 One main limitation of these prior analyses is their reliance on the use of levels of government ownership as a percent of the banking sector, which can change by various means, such as: the privatization of current state-owned banks, acquisitions of private banks, establishment of new state-owned banks (for which there is no publicly available data), or simply a growth in the relative size of the private or public banking sector (such as via opening up financial markets). All of these mechanisms arguably entail distinct causal pathways, and collapsing them into one measure obscures the role of important overlooked explanatory factors, such as banking crises.

Moreover, these analyses lack consistent cross-sectional data on changes in levels of government ownership over time.2 Collectively, the data is sufficient enough to indicate that there is interesting variation in the levels of government ownership across time and within and among different regime types and development statuses (Cull et al., 2018). However, given that the data is based on a relative indicator (percent of government owned banks in the banking sector) and given the lack of consistent data, the theoretical leverage that can be employed with it is fairly limited. As a result,

1

See Voszka (2017) for a contextualization of historical waves of nationalizations and privatizations, and see Figure 18 in the Additional Figures section of the Appendix for an accompanying time series graph of the most recent waves of nationalization and privatization. Figure 19 in the Appendix shows that the vast majority of these acquisitions occurred in the finance sector.

2

there remains a rather scant body of literature on the topic of government ownership within the financial industry.

I therefore refine the scope of the theory and analysis of this paper to unpacking just one of these pathways through which variation in government ownership is produced: government acquisitions of banks. In particular, I am interested in explaining the most recent wave of acquisitions occuring since the begining of the twenty-first century using data available through the SDC Mergers & Acquisitions database, which provides transactional data on government acquisitions of private bank assets. Refining the focus to acquisitions elucidates an under-theorized pathway through which increases in government bank ownership occur. Namely, I argue that the weakening of the private financial system through systemic banking crises is a significant explanatory factor in what drives increased government ownership, specifically via government bank acquisitions. Moreover, I argue that this crisis effect is more pronounced among more democratic countries given that democratic leaders face short term electoral incentives to pursue policy responses to crisis that will allow for swift economic recovery and avoid the costs associated with a prolonged recessionary period (such as extensive bailout or nationalization programs). That is, while the public may not necessarily be supportive of extensive bailout policies given that they use taxpayer funding and reinforce moral hazard, I argue that democratic leaders will be more concerned about the electoral costs associated with an economic contraction and will pursue policies that maximize economic recovery despite being costly for voters in the short run.

In examining this increase in government acquisitions and focusing on the role of systemic banking crises and patterns of financial integration, this analysis also builds on international political economy literature on responses to financial crisis, as well as a growing body of literature that emphasizes a departure from the traditional “open political economy” approach by centering the role of structural features of the international financial system in influencing domestic political economic outcomes (Oatley, 2011; Pepinsky, 2014). In particular, by demonstrating that financial integration among democracies is an important structural feature of both democracies and the global financial system that may increase crisis susceptibility, it suggests even greater attention is needed at the system level to understand how de facto financial connections are formed, how crises diffuse, and in turn how certain policy outcomes at the domestic level may be generated.

Ultimately, in providing an account of government bank acquisitions that suggests more demo-cratic and financially integrated countries tend to acquire more, this analysis yields a novel substantive conclusion with implications for future academic and policy consideration. Namely, it suggests a certain paradoxical conclusion that increasing democratization and liberalization may actually be resulting in more government intervention and involvement through a form of re-embedding, albeit a reactionary and incidental one. While many of the bailout programs were intended to be short term, and in some places the process of re-privatization has already begun in the last several years, some significant financial institutions remain nationalized (Mercille and Murphy, 2016).

2. POLITICAL ECONOMY OF GOVERNMENT BANK OWNERSHIP & ITS LIMITS

The rather brief body of literature that could be considered part of the subject of the political economy of government bank ownership has been dominated by the argument that government ownership leads to inefficiencies (Andrews, 2005). Exceptions to this claim exist with respect to the natural resources and utilities industries, given that historically the natural monopoly and “public service” nature of utilities (and to some extent natural resources) have been considered by economic theory to be more amenable to public ownership for the purpose of avoiding monopoly pricing (Plaiss, 2016; Jones, 1979). However, particularly with the breakdown in relative consensus around Keynesian economic theory, susbsequent economic theory has emphasized the notion that government intervention, particularly in the form of ownership, is not welfare maximizing. The banking industry in particular is perceived as such given that it historically has not been considered a utility or “public service”, and subsequent financialization has only reinforced this argument, increasingly placing the (private) financial system at the center of the global economic system (Ho, 2009; Van der Zwan, 2014; Maxfield et al., 2017). Thus government ownership of banks is more consistently viewed as inefficient in the long term and that, per the extant “political” and “development” views of government ownership of banks, it primarily exists to serve political and economic interests of state actors—either corrupt political interests and weak protection of private property in less politically open regimes or the economic interests of less developed states (Gerschenkron, 1962; La Porta et al., 2002; Megginson, 2005).

financial sector as a way to catch up with international competition. Subsequent studies brought the argument back to the domestic level in arguing, against Gerschenkron, that the types of banking that took center in industrializing countries depended not so much on international economic or military competition, but as a result of the domestic financial regulatory framework and the constraints or incentives facing private bankers (Verdier, 2000; Forsyth and Verdier, 2003).

One uniting limitation of each of these accounts is that the the role of political actors in the expansion or contraction of state-owned banks—arguably a distinctly political process—is not clear. Yet changes in government ownership of banks arguably result from a combination of economic and political processes and the incentives therein for taking as significant of an action as involving the government directly in the banking industry. Specifically, Verdier’s (2000) unique historical account acknowledges this and provides evidence to suggest that state-owned banking predominates where private banking is weaker, and that GOBs originated through a process of economic demand and political supply (Verdier, 2000). On the economic demand side, sectors harmed by industrialization and the centralization of private banks (namely, agriculture and small business) generated demand outside of private finance. Further, this demand emerged when the nonprofit and local banking sectors were not strong, which occurred when private for-profit banks were competing for deposits and/or when regulation did not shelter local banks and nonprofit banks. On the political supply side, politicians needed support to establish state-owned (public) banks, which was stronger when state banks faced no concentrated opposition, such as when large private banks were weakened after the crises and regulatory changes in the 1920s and 1930s. Accordingly, following the 1930s, the level of GOBs declined once again, as private banks strengthened once again with subsequent financial deregulation and internationalization.

processes that weaken private banking is significant, and the fact that this occurred around the time of the crises of the 1920s and 1930s indicates that systemic banking crises may be an important direct way that private banking is weakened such that government intervention through increased ownership is required.

3. CRISES, RESPONSES TO CRISES, & DEMOCRATIC INSTITUTIONS

The above discussion of the extant literature on the political economy of government bank ownership, including both its limitations and insights, indicates that banking crises are an important factor in explaining increases in government bank ownership occuring through acquisitions. Crises matter to the extent that they weaken the private banking system and thus generate the economic demand for government intervention, which can take the form of acquisitions via bailouts and nationalizations. As a baseline hypothesis, I therefore expect that systemic banking crises will have a positive effect on government bank acquisitions (Hypothesis 1).

Now, the claim that increased government ownership of banks may predominate when private banking is weakened, and that systemic banking crises may drive increases in government ownership through acquisitions, is perhaps an obvious statement, particularly for the period of interest in the present analysis. However, just as historical changes in government ownership were not just motivated exclusively through economic but also political processes, the effect of banking crisis will also be mediated by political institutions. That is, while crises occur quite frequently, they are varied in origin and governments’ inherently political responses to such crises are multifarious, particularly given that the political institutions of more democratic versus autocratic regimes create differening incentives that structure their response (Reinhart and Rogoff, 2009; Pepinsky, 2014). Accordingly, the answer to the question of “how do domestic political institutions mediate the effect of banking crisis on acquisitions?” remains less obvious than the effect of crisis alone.

will arguably be more concerned about the costs of not swiftly and adequately acting during crisis despite that there may be public resistance to the particular form that policy response takes—i.e bailouts or nationalizations.

Notably, this argument stands in contrast to previous work on responses to banking crises, which has focused on explaining the propensity of governments to choose extensive bailout programs as compared with other policy options. Specifically, Rosas (2009) argues that governments’ responses to crisis exist on a policy continuum that ranges from ‘Market’ to ‘Bailout’. Market governments pursue the “radical strategy” of simply letting banks fail during crisis, while on the other end of the scale, Bailout governments focus on providing the support needed to avoid financial meltdown and thus “support banks liberally with no strings attached” (p.6). The argument here is that “the political regime within which governments operate has a discernible impact on policy responses to banking crises” (p.4) and that autocratic regimes are “more prone to bail out banks” (p.4) given that democratic governments are more constrained by electoral accountability as voters are more wary of policies that rely on taxpayer funding (such as bailouts). This does not necessarily mean that democratic governments pursue the Market response, but that on the continuum of Market to Bailout, autocracies will be more prone to the bailout approach, and the results of the analysis are consistent with Rosas’ argument.

to crisis that maximize short term gains in economic growth, which entails extensive bailouts or nationalizations, either of which would increase government bank acquisitions.3

In a prior analysis, Rosas (2006) did test the hypothesis that democratic leaders may be more likely to pursue the Bailout approach given the potential for greater economic costs of crisis in instances where the magnitude of the crisis is greater (operationalized as higher deposit share of banks as a percent of GDP), but the results did not support this hypothesis. However, one immediate issue here is that the outcome of this analysis was a binary policy choice across seven policy options (ranging from Market to Bailout) with the intent of capturing bailout propensity as a matter of policy choice as opposed to directly explaining the extensiveness of the bailouts, which is more so the focus of this analysis. Given that I am interested in explaining the degree to which governments pursue acquisitions in response to crisis, and given that I expect more extensive bailouts to be pursued as a result of electoral pressures to maximize short term recovery, I therefore re-center the role of these electoral incentives facing democratic leaders as being relevant to explaining increases in acquisitions occuring in the context of crisis (in the form of bailouts or nationalizations).

Now, this is not to say that the public will be universally in favor of the use of bailouts or nationalizations as a policy solution given that such policy responses may entail the use of public funds, and particularly with bailouts, they may signal a reward to banks’ risky behavior and failure (reinforcing the moral hazard problem). Indeed, the Occupy Wall Street movement evidenced a significant degree of public disastisfaction towards the use of bailouts. Rather, the main argument I advance is that government leaders will also weigh the costs of a prolonged economic contraction that may result from pursuing policies that might induce better market discipline in the long term but would be highly costly—economically and politically—in the short term. Democratic leaders arguably face greater electoral costs and public pressure of not pursuing policies that will maximize

3

short term economic recovery. I therefore expect the effect of crisis on acquisitions to be positively mediated by democracies; that is, I expect democracies to pursue acquisitions to a greater extent in the context of crisis (Hypothesis 2).

To test this hypothesis I begin by looking at aggregate regime types, namely the range of democracies to non-democracies provided by the Polity IV data. However, to better test the relevant mechanism I propose, I further test this more directly by examining not just the effect of aggregate democracy scores but also examining subcomponent measures including political competition and freedom of expression. This allows me to better assess the effect of the degree to which politicians need to be concerned with electoral and public backlash. I thus further expect that the domestic institutional mechanisms of political competition and freedom of expression will positively mediate the effect of crisis (Hypotheses 2a and 2b, respectively)

Finally, I further compare these mechanisms to the role of lower executive constraints, lower property rights protection, and higher political corruption that Rosas and prior literature on government ownership of banks suggest ought to be associated with more extensive acquisitions. Testing these latter three institutional features of regimes allows me to not only test my theory in opposition to theory presented in prior literature, but to also disaggregate the institutional features of democracies to more precisely identify the those that are driving the differences in acquistions among the aggregate measures of regime type. In all three tests of prior theory, I expect these proposed features of regimes with bank acquistions to negatively mediate the effect of crisis; that is, I expect that lower executive constraints, lower property rights protection, and higher political corruption will be associated withless extensive acquisitions in the context of crisis (Hypotheses 2c, 2d and 2e).

accords with the broader argument that leaders’ short term concern for returned economic growth following a crisis is what drives acquisitions.

Meanwhile with respect to corruption, more attention has been devoted to the variation in policy formation and responses to crisis among autocratic regimes given varied legislative structures and coalitional and sectoral politics (Pepinsky, 2008; Jensen et al., 2014). This literature suggests that autocratic leaders are respondent to at least some forms of domestic audiences and serve complex “informal networks of patronage and exchange” (Pepinksy 2008, p. 473) that may not necessitate or may even run against forms of theft or the overt expropriation of private assets, which prior theory presumes would be intended to generally serve regime interests. Compared to democracies, in that sense, there is a less coherent policy preference among autocratic leaders than might be expected by the corruption argument and compared to that of democratic leaders, who are more consistently respondent to median voter interests. Finally, executive constraints may be positively associated with greater acquisition given that while there may be more legislative checks on executive action among more democratic countries, the legislators themselves may face incentives to advocate for more extensive acquisitions (per the broader theory outlined above).

One final domestic institutional mechanism worth considering is the role of independent central banks. Here it could be argued that greater independence of the central bank is associated with either increased or decreased degree of acquisitions. On the one hand, an independent central bank may per its intended purpose serve as a form of a constraint on the degree to which democratic leaders can act on the electoral incentives to pursue liberal bailouts (Rosas, 2006). On the other hand, central bankers in independent central banks can still be motivated by political pressures from the legislature or by private interests given that some start out working in the private financial industry and some central bankers also serve as the bank regulators (Singer, 2007; Winecoff, 2014); all of which would arguably create adverse incentives to push for a more liberal bailout strategy. Sufficient literature exists to support the latter possibility such that I expect increased central bank independence to be associated with a greater degree of acquisitions (Hypothesis 2f).

4. RESEARCH DESIGN

4.1 Empirical Models

The primary goal of the present analysis is to test the hypothesis that systemic banking crises drive government bank acquisitions, but that this crisis effect varies by regime type given that certain features of democracies make them more likely pursue government acquisitions of banks in the context of crisis. Given the discussion above, for the purpose of this analysis, the features of democracy that I consider most relevant to include are political competition, freedom of expression, executive constraints, property rights, political corruption, and central bank independence.

Accordingly, I use a series of models to test the unique effects of domestic banking crisis and regime type, as well as the conditional effect of crisis by polity, and the conditional effect of crisis by each of the mechanisms just identified. Each model is a multilevel linear regression with country-level random intercepts to account for within-country variation. In all models the independent variables are lagged one year to avoid post-treatment effects (in particular, of acquisitions inducing crisis). The first of the main three models includes a domestic crisis binary variable and aggregate regime type (uninteracted), with the second model adding an interaction term to test the moderating effect of crisis by regime type (Polity), and the third adding in specific mechanisms in place of aggregate regime type:

yi =β0,j[i]+β1P olityi−1+β2Crisisi−1+xi−1β+ (1) yi =β0,j[i]+β1Crisisi−1∗P olityi−1+β2P olityi−1+β3Crisisi−1+xi−1β+ (2) yi=β0,j[i]+β1Crisisi−1∗dcorrelatei−1+β2dcorrelatei−1+β3Crisisi−1+xi−1β+ (3)

where yi is a country-year continuous Government Acquisitions Indicator (described further in the

political corruption, and central bank independence);4 andxi is a vector of predictors including: log

GDP, central bank independence, and log of the size of the banking industry as percent of GDP.5

4.2 Data

Dependent Variable

Using SDC Mergers & Acquisitions data, which collects transactional data on purchases and sales of assets by private and public institutions, I construct a continuous measure of government bank acquisitions using the same formula as the Herfindahl-Hirschman Index (HHI) measure of market concentration, which takes the sum of squared market shares of firms. This measure, or the Government Acquisition Indicator (GAI) thus captures the degree and concentration of government bank acquisitions by taking the sum of squared acquisition shares:

GAI =a21+a22+a23+. . . +a2n

where ais the percent of bank assets acquired by the government (multiplied by 100). Unlike the HHI, the range of this outcome variable is thus not constrained by a maximum given that the number of transactions could theoretically be infinite (versus a select number of firms existing in a finite market). This does not present practical issues for the present analysis, but rather helps provide a more dynamic measure that captures both degree and concentration of acquisitions (for example capturing differences between a country that fully nationalizes three banks, versus another that, say, nationalizes one bank but acquires small shares of assets of many more banks).

Thus, this indicator helps to capture some degree of magnitude of government bank acquisitions while also avoiding a statistical problem presented by using a simple count of transactions per year, given that the U.S. is an outlier in the number of transactions in which it acquired small shares of assets (presumably as part of the Troubled Assets Relief Program and quantitative easing program).

4

In the model that examines the conditional effect of central bank independence in crisis, I also include political competition as a control to control for the general effect of countries with more democratic electoral institutions.

5I include minimal controls in part to avoid overfitting resulting from the fact that of the 1,872 country-years

As shown in Figures 1 and 2, the distribution of transactions by percent of share acquired changes dramatically once the U.S. is excluded from the sample. The distribution of GAI for each country year also exhibits a long tail, however, so I take thelog(GAI + 1) to normalize the distribution and further control for the influence of outliers.6

Figure 1: Distribution of percent of bank assets acquired (with U.S.)

6

Figure 2: Distribution of percent of bank assets acquired (without U.S.)

The type of financial institutions included in the sample of government acquisitions includes “all financial institutions” and therefore includes both commercial banks as well as investment banks, mortgage companies (such as Fannie Mae and Freddie Mac) and other financial companies. I subset the data to include purchases only by national government agencies to capture behavior at the national and not regional or local level.

Independent Variables

highly correlated with the outcome variable of interest). The domestic crisis binary variable is thus coded 1 if a crisis was recorded for that country-year and zero otherwise.

For aggregate regime type, I use the Polity scores presented in Polity Project’s Polity IV database. The Polity scores are a combined score that set a country’s measure of democracy on a range of -10 to 10 to “facilitate the use of the POLITY regime measure in time-series analyses” (Marshall et al., 2017). Higher values translate to more democratic countries. Countries with a value

of 6 or greater are typically considered democracies (Marshall et al., 2013). Polity is a composite, weighted measure of indicators of democracy and autocracy; here it simply serves the purpose of capturing the aggregate degree to which regimes can be considered autocratic or democratic.

I further use other correlates of democracy to test particular aspects of democracies that may not be captured by the gross measure. These include the Polity IV executive constraints and political competition measures used to construct the aggregate Polity scores.7 The executive constraints measure is a range from 1 to 7 that captures the “extent of institutionalized constraints on the decision-making powers of chief executives” (Marshall et al., 2017, p.24). It ranges from 1, or “unlimited authority”, to 7, or “executive parity or subordination”. Political competition is a composite measure of both regulation of participation (PARREG), which refers to free and non-coercive participation of all political groups, and competitiveness of participation (PARCOMP), which refers to the “extent to which alternative preferences for policy and leadership can be pursued in the political arena” (Ibid, p.26). This variable thus ranges from 1, or “suppressed”, to 10, or “institutionalized electoral”.

The other correlates of democracy, including freedom of expression, property rights protection, and political corruption, are taken from the Varieties of Democracy (VDEM) dataset. The freedom of expression indicator is on a scale of 0 to 1, and captures the degree to which the government respects free press and the ability for citizens to discuss political matters at home and in the public sphere. The property rights indicator is also on a scale of 0 to 1 and captures the ability for citizens to acquire and sell private property. More limited property rights include legal limitations or failure to enforce private property rights. The political corruption indicator again ranges from 0 to 1 and captures the pervasiveness of political corruption such as in the form of bribery, theft, and

7

embezzlement occuring in the executive, legislative, and judicial realm. Lower scores indicate lower levels of corruption.

My remaining independent variable of interest is central bank independence (CBI), for which I use Garringa’s (2016) measure. In addition to including CBI as a variable of interest, I also control for CBI in each model to control for the possible mediating effect of the autonomy granted to regulators in the form of CBI on government acquisition of bank assets. Garringa’s measure of CBI is a weighted measure of central bank independence based on a coding of 16 different policy indicators and is available through the year 2012 (Garriga, 2016). Higher values (on a continuous scale of 0 to 1) indicate a greater degree of CBI.

5. RESULTS

5.1 Aggregate Effect of Regime Type

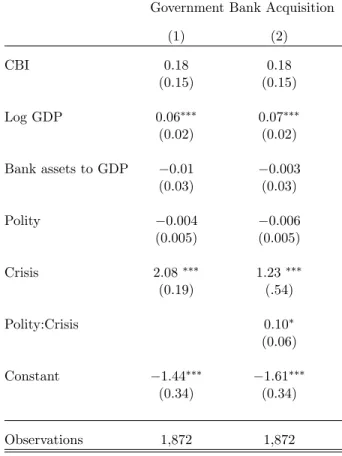

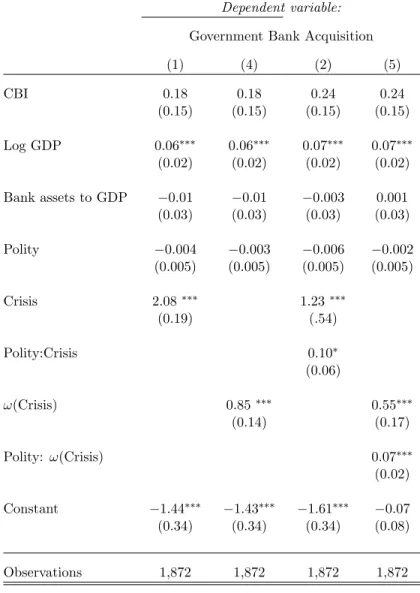

The results of the models including the aggregate polity score and domestic crisis (models 1 & 2 above) are presented in Table 1. The results of model 1 confirm my first hypothesis that systemic domestic banking crises has a significant and positive effect on government bank acquisitions in a given country-year.8 Notably, contrary to both the “corruption” and “development” theories of government bank ownership, the coefficient on GDP is positive and significant, indicating that more developed countries are associated with acquisitions. Meanwhile, the effect of polity is not by itself significant.

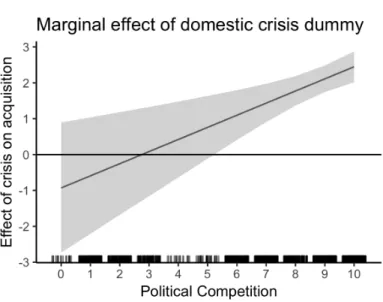

The conditional (marginal) effects plots in Figure 3 facilitate depicting the interactive terms of model 2, and show how the effect of domestic crisis increases over the values of polity.9 These results confirm my second hypothesis that democracies will have a positive mediating effect of crisis on acquisitions. That is, in the context of domestic crisis, democracies pursue acquisitions to a greater degree than less democratic countries

8

The results presented in all tables are the pooled estimates from the five repeated complete analyses using the imputed data. The pooled estimates are averaged estimates of the complete data model, and the standard errors are computed as the total variance over the repeated analyses according to Rubin’s rules: Tm=Um+ (1 +m−1)Bm

(Rubin, 1987, p.76)

9Marginal effects are computed at the 90% significance level. The plots portray the marginal effects of only one of

Table 1: Model results with crisis dummy

Dependent variable:

Government Bank Acquisition

(1) (2)

CBI 0.18 0.18

(0.15) (0.15)

Log GDP 0.06∗∗∗ 0.07∗∗∗ (0.02) (0.02)

Bank assets to GDP −0.01 −0.003 (0.03) (0.03)

Polity −0.004 −0.006

(0.005) (0.005)

Crisis 2.08∗∗∗ 1.23∗∗∗

(0.19) (.54)

Polity:Crisis 0.10∗

(0.06)

Constant −1.44∗∗∗ −1.61∗∗∗ (0.34) (0.34)

Observations 1,872 1,872

5.2 Mechanisms: Political Competition & Freedom of Expression

To better isolate that this positive aggregate democracy effect is resulting from the heightened concern of democratic leaders of the consequences of not pursuing extensive acquisitions in response to crisis, I test the conditional effect of political competition and freedom of expression. The conditional effects of domestic crisis by political competition are presented in Figure 4.10 Here the results show that the interactive effect of political competition and domestic crisis is in fact positive and significant in the context of domestic crisis, supporting Hypothesis 2a.

Figure 4: Marginal effect of crisis by political competition

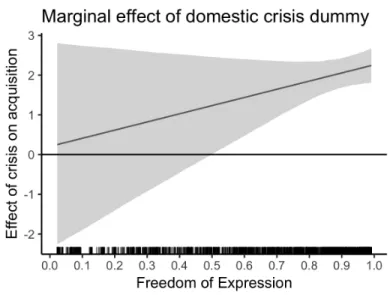

The results of the interactive model including the VDEM freedom of expression variable shows similar results. While the interaction term on freedom of expression and domestic crisis is not significant, Figure 5 shows that the effect of crisis increases over the range of freedom of expression, indicating countries with higher levels of free expression are positively associated with acquisitions. This reflects the expectation (Hypothesis 2b) that greater freedom of expression will be associated

10

with greater acquisitions in the context of crisis given the need to avoid a potentially more costly and unpopoular economic depression.

Figure 5: Marginal effect of domestic crisis by freedom of expression

Collectively these results provide initial support for the argument that acquisitions in this period are driven by banking crises, and that domestic institutional features of democracies create short term electoral incentives for leaders to respond to crisis through more extensive acquisitions. However, to rule out other possible domestic insitutional explanations identified in prior theory, the next section examines the effects of the four other correlates of democracy (executive constraints, property rights, political corruption, and central bank independence).

5.3 Mechanisms: Other Correlates of Democracy

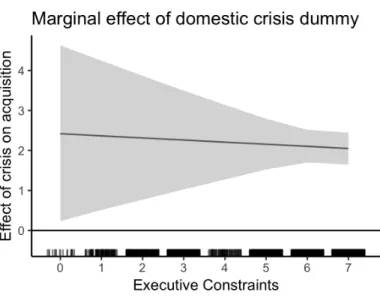

One interpretation of these results may be that while concern about public backlash may motivate a greater degree of acquisitions as the prior analysis indicates, greater executive constrains may have a tempering effect.

Figure 6: Marginal effect of crisis by executive constraints

Figure 7: Marginal effect of crisis by property rights

Figure 8: Marginal effect of crisis by political corruption

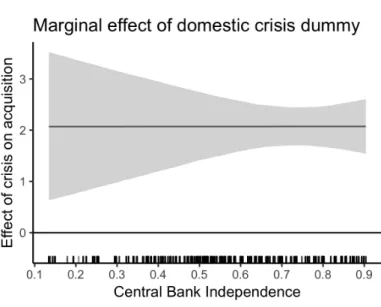

Finally, looking at the results of the model including central bank independence as a variable of interest (with political competition as a control) demonstrates that there is no strong moderating effect of central bank independence on acquisitions during domestic crisis (though the interaction term is significant). That is, as depicted in Figure 9, a higher degree of central bank independence is only very weakly associated as increasing the conditional effect of domestic crisis on acquisitions. This then provides only very weak, if any, support for Hypothesis f.

Figure 9: Marginal effect of crisis by central bank independence

increase the effect of crisis. Namely, regime type does not have a significant effect on acquisitions outside of crisis, while crisis alone does increase acquisitions. In the context of crisis, however, more democratic countries, and specifically countries with higher levels of political competition and freedom of expression positively mediate the effect of crisis on acquistions, which I argue reflects that democratic leaders face electoral incentives to pursue policies that maximize short term economic recovery during crisis. I do not find support for the argument that corruption has a positive mediating affect on crises, while the support for the alternate mechansims of executive constraints and property rights suggest some interesting variation in the effect of certain features of regimes, though the effects are not significant enough to make a strong claim about their effects.

6. ROBUSTNESS CHECK: ACCOUNTING FOR FINANCIAL INTEGRATION

6.1 Why Financial Integration?

The significance of testing the role of financial integration as one main potential threat to inference is twofold. First, there is historical evidence to suggest that in the last 200 years, democracies on average are more crisis-prone. Specifically, Lipscy (2018) establishes this empirical regularity (outside of the decades of the 1980s and 1990s) and outlines several features of democracies that may make them more likely to experience crisis, one of which is financial liberalization. The other factors identified include constraints on democratic leaders to curtail speculation and take actions to stop a crisis before it starts as well as higher turnover of leaders that may disincentivize pursuing more costly but more prudent financial policies.

general importance of crisis selection and in particular the role of financial integration in increasing crisis susceptibility is important for not only accounting for possible endogeneity concerns, but also capturing another feature of democracies (financial integration) that may be relevant to driving bank acquisitions.

Second, considering not just openness in the sense of capital account openness, but financial integration in particular, is important given that the global financial system is not composed of evenly financially connected states. Rather, it exhibits a hierarchical structure in which a select few countries constitute a highly integrated core, with a multitude on the periphery (Oatley et al., 2013). The main implication of this is that domestic crises in a highly integrated, hierarchical financial system—particularly crises among the core of the financial system—are global in nature, such that the global financial system has been characterized as “an oscillating system that generatesboom and bust capital flow cycles” (Bauerle Danzman et al., 2017). Specifically, crises occuring in the periphery are not likely to affect the core, however crises in the core threaten the system as a whole. Thus countries’ susceptibility to crisis is determined not just by the fact they are more financially open and may have lowered capital controls, but also by their position within this network and the strength of their financial relationships with other countries in the network.

Incorporating these findings in this analysis are thus important to the extent that the degree of acquisitions may be affected by the level of crisis susceptibility via financial integration, which I expect from Lipscy’s assessment to be more so a feature of democracies than autocracies. While Rosas’s (2006) analysis did include a control for financial openness in an effort to control for the effect of crisis susceptibility, traditional measures of financial openness primarily capture a country’s policy position with respect to capital controls as opposed to the more dynamic measure of degree of financial integration. Consequently, variation in capital account openness among democracies tends to be fairly uniform and static, at least relative to financial relationships in volume terms.

test the assumption that crisis susceptiblity may be greater among democracies as a result of the predominance of heightened financial integration primarily among democratic countries. In doing so I identify a novel empirical finding that democracies financially trade more with one another on average, which provides some evidence to suggest that financial integration is a structural feature of democracies that may increase crisis susceptibility. However, I then control for degree of financial integration in my original model to re-examine the conditional effect of polity and my main mechanisms of interest, and still find a positive and signficant effect of democracy in crisis.

6.2 Approach, Empirical Models, & Data

I approach testing the possible effect of financial integration in elevating crisis susceptibility by first constructing a new measure of crisis susceptibility via financial integration. Using my prior three models, I thus replace the domestic banking crisis dummy with this “neighbor crisis weight”,

ω(Crisis):

yi =β0,j[i]+β1P olityi−1+β2ω(Crisis)i−1+xi−1β+ (4) yi=β0,j[i]+β1ω(Crisis)i−1∗P olityi−1+β2P olityi−1+β3ω(Crisis)i−1+xi−1β+ (5) yi=β0,j[i]+β1ω(Crisis)i−1∗dcorrelatei−1+β2dcorrelatei−1+β3ω(Crisis)i−1+xi−1β+ (6)

wherexi anddcorrelateis the same vector of predictors as in first model, andω(crisis) is calculated

as the product of the systemic banking crisis dummy variable for countryiand a weight matrix that captures the strength of financial connectedness between countries by taking the portfolio share of financial sector assets invested in country iby countryj over the total value of financial assets invested in countryi:

ω(Crisis) =X

j

Wi,j,t∗ Crisisj,t−1

Wi,j,t=

investmenti,j,t

P

jtotalinvestmentsi,j,t

Investment Survey database, to construct a measure of internationally mediated crisis. The data take the form of a sociomatrix and capture the debt and equity investments between countries on an annual basis. I code missing values and values coded as “C” for confidential as zero for the purpose of this analysis both to facilitate imputation and with the assumption that this would likely serve to understate any effects. The resulting “neighbor crisis weight” variable is a continuous measure on a scale of 0 to 1 that captures the extent to which the countries that collectively invest in a given country experienced a crisis in a given country year.

The primary purpose of this variable is to directly capture international financial connectedness among countries, and allows me to test the effect of democracy and my mechanisms of interest among countries that are more crisis exposed. While openness may be a common feature of democracies, the degree of financial integration may vary. So I opt to not use other common, general indicators of economic openness such as Karcher and Steinberg’s (2013)ckaopen, which builds on Chinn and Ito’s (2008)kaopen measure to ensure I am not conflating economic openness and political openness within the same model (as these more flat indicators may not provide sufficient variation). Rather this approach allows me to capture the degree of financial integration more directly by providing a more precise indicator for the effect of crisis occurring in part of the international system a country is connected with versus openness generally. In doing so I follow Karcher and Steinberg’s (2013) admonition that when attempting to capture financial openness, “researchers must take greater care when selecting measures of capital account openness and other key concepts” (p. 136).

However, the goal of the test here is not just that any particular country may be more crisis susceptible as a result of being more financially integrated, but that this may be particularly true of democracies in particular. That is, I aim to test the possibility that the “neighbor crisis weight” variable in the models above is capturing yet another feature of democracies (financial integration) that is contributing to crisis and thus acquisitions. While again it is not within the scope of this paper to directly model and test the selection into crisis among democracies or crisis diffusion among democracies, I provide an initial test of the role of financial integration among democracies in three parts.

my original analysis (2001-2012), again using this IMF CPIS data. This model allows me to measure the effect of regime type on the strength of financial connectedness by examining the sender, receiver, and dyadic effects of being a democracy—that is, the effect of democracy on the amount invested in a country (receiver, or in this case, row effects), amount invested in other countries (sender, or in this case, column effects), and co-investments (dyadic effect). The model is constructed as follows:

yi,j =β0+βrTpolityr,i+βcTpolityc,j+βTdpolitydyadd,i,j+ai+bj +uTi vj+i,j

where yi,j is a sociomatrix capturing a logged continuous measure of financial assets (in millions)

invested from countryito countryj; polity is a binary variable for 1 if democracy and 0 if autocracy; “politydyad” is 1 only if the two countries are democracies; ai and bj are additive components

controlling for row and column variance; and uTi vj is the multiplicative component to control for

triadic dependence, which in this case is of rank 4 (Hoff, 2015).11

Finally, given that it is evident from this network information that democracies are more central to the global financial system (much more highly integrated), I test the extent to which network centrality is what’s driving the results by adding a control for network centrality with domestic crisis into my original baseline models for polity and each of the correlates of democracy of interest in my argument (political competition and freedom of expression). From this I re-check the conditional effect of crisis by polity and examine the significance of the interaction terms for each of the models:

yi=β0,j[i]+β1Crisisi−1∗P olityi−1+β2Centralityi−1+β3P olityi−1+β4Crisisi−1+xi−1β+ yi =β0,j[i]+β1Crisisi−1∗dcorrelatei−1+β2Centralityi−1+β3dcorrelatei−1+β4Crisisi−1+xi−1β+

where xi is a vector of predictors including the same controls as before.

11

6.3 Results

The results of the uninteracted and interacted models including the “neighbor crisis weight” variable (models 4 & 5) are presented in Table 2 along with the results of the original models including domestic banking crisis (presented in Table 1 above). The results of model 4 provide support for the notion that crises occurring in a country’s financial neighbors have a positive and significant effect on government bank acquisitions. This suggest that openness, or more specifically, greater financial connectedness with other countries experiencing crisis, has a positive effect on government bank acquisitions.

Table 2: Model results with neighbor crisis weight interaction

Dependent variable:

Government Bank Acquisition

(1) (4) (2) (5)

CBI 0.18 0.18 0.24 0.24

(0.15) (0.15) (0.15) (0.15)

Log GDP 0.06∗∗∗ 0.06∗∗∗ 0.07∗∗∗ 0.07∗∗∗ (0.02) (0.02) (0.02) (0.02)

Bank assets to GDP −0.01 −0.01 −0.003 0.001 (0.03) (0.03) (0.03) (0.03)

Polity −0.004 −0.003 −0.006 −0.002 (0.005) (0.005) (0.005) (0.005)

Crisis 2.08∗∗∗ 1.23∗∗∗

(0.19) (.54)

Polity:Crisis 0.10∗

(0.06)

ω(Crisis) 0.85∗∗∗ 0.55∗∗∗

(0.14) (0.17)

Polity: ω(Crisis) 0.07∗∗∗

(0.02)

Constant −1.44∗∗∗ −1.43∗∗∗ −1.61∗∗∗ −0.07 (0.34) (0.34) (0.34) (0.08)

Observations 1,872 1,872 1,872 1,872

Models 2 and 5 highlight the importance of the moderating effect of democratic institutions in addition to financial integration when looking at the conditional effect of crisis as moderated by regime type. As was found in the analysis above, Model 2 indicates that the interaction between polity and a domestic banking crisis is positive and significant, though only at the 90% level. The interaction term in model 5 meanwhile indicates that the effect of “neighbor crisis weight” is positive and significant for higher values of polity at the 99% confidence level. This suggests that when looking at the aggregate measure of polity, more democratic countries that are also more financially integrated with other countries in crisis are associated with more government acquisition of banks. The conditional effects plot of the effect of neighbor crisis as mediated by polity depicted in Figure 10 alongside the original results for domestic crisis shows this much stronger positive mediating effect.

Figure 10: Marginal effect of neighbor crisis weight by polity

The results of the models that include my mechanisms of interest—political competition and freedom of expression—show similar effects, as depicted in Figure 11.12 The interactive effect between the “neighbor crisis weight” is significant for both, and both demonstrate a stronger positive conditional effect of the “neighbor crisis weight” than that of domestic crisis. This indicates that

12

while these domestic institutional features are relevant in the context of domestic crisis in driving acquistitions, financial integration may in part be what is contributing to susceptibility for domestic crisis, in turn driving acquisitions.

Figure 11: Marginal effect of neighbor crisis weight by political competition & freedom of expression

Similarly, the results of the models including each of the other domestic institutional mechanisms further point to the potential importance of financial integration.13 Namely, while the conditional effect of political corruption remains essentially the same (lower levels of corruption is associated with more acquisitions during crisis), the conditional effect of executive constraints and private property rights flip in the models accounting for financial integration.

This suggets that when countries are more financially integrated with other countries in crisis, the tempering effect of executive constraints may play less of a role, perhaps as greater connection

13

with other countries in crisis may speak to the severity or extent of the systemic nature of the crisis that may necessitate more robust acquisitions as a response. It could also be that generally speaking, countries with higher exeuctive constraints (which also tend to be more democratic countries) are more financially integrated. Similarly, the flipped effect of property rights may suggest that the potential tempering effect of property rights protection is lowered when countries are more exposed to crises in their financial neighbors. Yet, again, it could also be the case that countries with higher protection of property rights (which tends to be higher among democracies) tend to also be more integrated with other countries in crisis.

Similarly, the effect of central bank independence is still significant, but much more clearly positive in the case of countries more integrated with other countries in crisis. gain, discerning to what extent this difference indicates an actual change in the unique effect of CBI versus captures the fact that more countries more exposed to crisis in this sample also tend to also have more independent central banks is difficult. It could be argued that when countries are more exposed to other countries in crisis, the need for central banker intervention and coordination becomes higher (Drezner, 2012). It could also be that CBI tends to play a more meaningful role among more democratic countries, which again I expect may more financially interconnected (Bodea and Hicks, 2015).

Figure 12: Network plot of global financial system colored by regime type (2006)

Note: nodes for democratic countries are colored blue; autocracies are colored red. Tie color corresponds to regime of sender. Node size corresponds to number of financial trading partners; edge size corresponds to amount of investments. Englarged plot included in Appendix.

the period, though perhaps the weight of the ties is only strong enough in the years 2005 and 2006 to be picked up as statistically significant in the model.

Figure 13: Results of AME network model

Therefore, to the extent that crises are an important driver of acquistiions, it appears that financial integration may be a source of crisis susceptibility that may in turn be driving acquistions. More importantly, to the extent that more integrated countries tend to be democracies, this crisis selection effect may be greater among democracies. Thus based on this analysis and novel empirical finding, I test the extent to which crisis susceptibility via financial integration is what is driving these results by extracting the measures of centrality from the network data for each of the years in my analysis and including them as a control in the original models with domestic crisis.

also positive, but this time not significant. Figure 14 plots the conditional effect of crisis by the aggregate polity score, which strongly resembles the original relationship indicated in Figure 3. This suggests that while centrality may matter as a structural feature of democracies that (at least for this period) may be elevating crisis susceptibility and in turn acquisitions, the positive effects of domestic democratic political institutions still hold.

Table 3: Model results with centrality control

Dependent variable:

Government Bank Acquisition

(1) (2) (3)

CBI 0.14 0.10 0.11

(0.14) (0.14) (0.14)

Log GDP 0.03 0.04∗∗ 0.04∗∗ (0.02) (0.02) (0.02)

Bank assets to GDP −0.04 −0.03 −0.03 (0.03) (0.04) (0.04)

Centrality 0.003∗∗∗ 0.002∗∗ 0.002∗∗ (0.001) (0.001) (0.001)

Crisis 1.22∗∗ −0.87 0.28

(0.54) (0.93) (1.33)

Polity −0.009∗

(0.005)

Polity:Crisis 0.01∗ (0.06)

Pol. Competition −0.01 (0.01)

Pol. Competition:Crisis 0.33∗∗∗ (0.10)

Free Expression −.16

(0.11)

Free Expression:Crisis 1.94

(1.45)

Observations 1,872 1,872 1,872

7. CONCLUSION

I examine the determinants of the most recent wave of acquisitions occurring since the beginning of the twenty-first century, focusing on the effect of crisis, domestic democratic political institutions, and financial integration. Contrary to the main prior theories of government bank ownership that argue increased ownership will occur among less developed and more corrupt regimes, I argue that these analyses overlook the role of systemic banking crises as an important and under-theorized factor that may increase government ownership partly as a result of the fact that these prior studies have focused on changes in the level of government ownership over time as opposed to looking at particular pathways by which government ownership may increase or decrease. I thus examine the effect of crises on acquisitions as one pathway through which government ownership increases, and the results of the analysis support the argument that systemic banking crises have a positive and significant effect on government bank acquistions.

Moreover, the results accord with my expectation that this effect of crisis is stronger among more democratic countries as a result of the need for democratic leaders to use extensive bailouts to avoid the political costs associated with economic contraction. This finding is robust even once testing for the effect of crisis susceptibility via financial integration with other countries in crisis and examining the patterns of financial integration among democracies. Once controlling for the effect of financial integration, indeed I find that higher centrality (greater degree of financial integration) within the financial system is positively associated with acquisitions, but the moderating effects of democratic political institutions still hold an additional positive effect in the context of domestic crisis.

network information on financial portfolio relationships among countries. This suggests that financial integration is a structural feature of democracies that may increase crisis susceptibility, which coupled with domestic institutional incentives, results in increased government bank acquisitions. While it was outside the scope of this analysis to test the role of crisis diffusion directly, this empirical finding suggests that future research devoted to further unpacking the structure of the global financial system by regime type and directly testing how crises diffuse among co-regime and non-co-regime financial neighbors could yield profound insights into the political economic nature of the global financial system.

Secondly, to the extent that greater financial liberalization and integration increases crisis susceptibility, this analysis suggests a paradoxical conclusion that pursuing economic liberalization and government dis-embedding to a considerable degree is in part what then actually drives greater government intervention in the form of increased ownership through bank acquisitions. Moreover, to the extent that economic openness is a feature of political openness, the results suggest this process is unique among more democratic countries despite that the global Occupy Wall Street movement demonstrated that the bailouts were not necessarily backed by universal appeal. In that sense, the systemic risk posed by intensive economic liberalization could be seen as increasing the susceptibility and costs of crisis to such a point that the presumed electoral backlash to bailouts is overshadowed by the need for democratic leaders to avoid the more costly impact of a severe economic contraction. Indeed, former US Federal Reserve Chairman, Ben Bernanke, expressly had the Great Depression of the 1930’s in mind as he and other regulators expressed their fear of “a decade of breadlines” resulting from a lack of extensive bailout intervention (Kai Ryssdal, 2018).

sustainable politically (Helleiner and Pagliari, 2011). To this latter point, recent work has indicated disillusionment and a short term drop in support for democratic instituions on the part of the public as a result of how bailouts were pursued in the case of the Eurozone irrespective of citizens’ vocalized lack of support (Schraff and Schimmelfennig, 2019).

Additionally, while I argue that the positive effect of political competition in mediating the effect of crisis should be read as democratic leaders’ need to be responsive to the electoral costs of not maximizing short term recovery during crisis, this positive effect of political competition could also be read as resulting not just from electoral incentives, but also from private interests (in this case, the banking industry, which may have an interest in receiving extensive bailouts). That is, democratic leaders maintain their political survival not just through the electorate but also through private interests (Grossman and Helpman, 1992). I do not test this possibility directly in this analysis as doing so would likely entail an entirely separate methodological approach given the types of data available to study interactions of private actors with elected leaders (e.g. lobbying reports and meeting transcripts). Moreover, it does not seem to be the case that the strength of the private banking sector (bank deposits as a percent of GDP) alone has an effect on acquisitions, nor does central bank independence (which, to the extent that even independent central bankers are in direct communication with or are regulators of banks, might lead to more acquisitions). Thus, to the extent that political competition may reflect any incentives—either electoral or private interest—on the part of leaders to maintain political survival, future research ought to also further unpack the role of political competition to study the electoral versus private influence motivations of leaders in pursuing acquisitions in the context of crisis.

8. APPENDIX

8.1 Summary Statistics

Min. 1st Qu. Median Mean 3rd Qu. Max. GAI 0.00 0.00 0.00 0.13 0.00 11.40 Polity -10.00 -2.00 6.00 3.73 9.00 10.00 Domestic Crisis 0.00 0.00 0.00 0.02 0.00 1.00 Neighbor Crisis 0.00 0.00 0.00 0.05 0.00 1.00 Log GDP 19.11 22.60 23.90 24.15 25.73 30.40 Log Bank Assets (% GDP) -0.96 2.88 3.57 3.52 4.29 6.73 CBI 0.13 0.47 0.58 0.60 0.80 0.90 Executive Constraints 0.00 3.00 5.00 4.91 7.00 7.00 Political Competition 0.00 6.00 8.00 6.90 9.00 10.00 Free Expression 0.02 0.51 0.79 0.69 0.92 0.99 Property Rights 0.05 0.55 0.76 0.68 0.86 0.95

Figure 17: Outcome variable ordered by country-year (& logged outcome)

Table 5: Model results with executive constraints interaction

Dependent variable:

Government Bank Acquisition

(1) (2)

CBI 0.17 0.23

(0.14) (0.15)

Log GDP 0.06∗∗∗ 0.07∗∗∗

(0.02) (0.02)

Bank assets to GDP 0.003 0.01 (0.04) (0.04)

Exec. Constraints −0.02 −0.02 (0.02) (0.02)

Crisis 2.44∗∗∗

(1.13)

Exec. Constraints:Crisis −0.06 (0.17)

ω(Crisis) −.15 (0.37)

Exec. Constraints: ω(Crisis) 0.19∗∗∗ (0.07)

Observations 1,872 1,872

Table 6: Model results with political competition interaction

Dependent variable:

Government Bank Acquisition

(1) (2)

CBI 0.15 0.21

(0.14) (0.15)

Log GDP 0.06∗∗∗ 0.07∗∗∗

(0.02) (0.02)

Bank assets to GDP −0.005 0.006 (0.04) (0.07)

Pol. Competition −0.007 −0.01 (0.010) (0.01)

Crisis 0.91

(0.94)

Pol. Competition:Crisis 0.34∗∗∗ (0.10)

ω(Crisis) −.03 (0.36)

Pol. Competition: ω(Crisis) 0.12∗∗∗ (0.05)

Observations 1,872 1,872

Table 7: Model results with freedom of expression interaction

Dependent variable:

Government Bank Acquisition

(1) (2)

CBI 0.15 0.20

(0.14) (0.15)

Log GDP 0.06∗∗∗ 0.07∗∗∗

(0.02) (0.02)

Bank assets to GDP −0.004 0.003 (0.04) (0.04)

Free Expression −0.07 0.11 (0.11) (0.12)

Crisis 0.23

(1.34)

Free Expression:Crisis 2.02 1.45

ω(Crisis) −.25 (0.37)

Free Expression: ω(Crisis) 1.54∗∗∗ (0.48)

Observations 1,872 1,872

Table 8: Model results with central bank independence interaction

Dependent variable:

Government Bank Acquisition

(1) (2)

Pol. Competition −0.005 −0.004 (0.009) (0.010)

Log GDP 0.06∗∗∗ 0.07∗∗∗ (0.02) (0.02)

Bank assets to GDP 0.003 0.007 (0.04) (0.04)

CBI 0.15 0.13

(0.14) (0.15)

Crisis 2.08∗∗

(0.89)

CBI:Crisis −0.02 (1.19)

ω(Crisis) −.21 (0.46)

CBI:ω(Crisis) 1.68∗∗ (0.70)

Observations 1,872 1,872

Table 9: Model results with property rights interaction

Dependent variable:

Government Bank Acquisition

(1) (2)

CBI 0.12 0.18

(0.14) (0.15)

Log GDP 0.06∗∗∗ 0.07∗∗∗

(0.02) (0.02)

Bank assets to GDP −0.006 0.002 (0.04) (0.04)

Property Rights −0.01 −0.08 (0.15) (0.15)

Crisis 2.56

(1.87)

Property Rights :Crisis −0.57 (2.17)

ω(Crisis) −.79 (0.51)

Property Rights : ω(Crisis) 2.28∗∗∗ (0.69)

Observations 1,872 1,872

Table 10: Model results with political corruption interaction

Dependent variable:

Government Bank Acquisition

(1) (2)

CBI 0.11 0.17

(0.14) (0.14)

Log GDP 0.06∗∗∗ 0.06∗∗∗

(0.02) (0.02)

Bank assets to GDP −0.02 −0.01 (0.04) (0.04)

Pol. Corruption −0.07 0.03 (0.11) (0.12)

Crisis 2.31∗∗∗

(0.26)

Pol. Corruption:Crisis −0.78 (0.56)

ω(Crisis) 2.13∗∗∗ (0.26)

Pol. Corruption: ω(Crisis) −2.46∗∗∗ (0.43)

Observations 1,872 1,872

8.3 Additional Figures

Figure 18: Acquisitions as % of GDP (all sectors) Source: Voszka (2017)

REFERENCES

Andrews, M. M. (2005). State-Owned Banks, Stability, Privatization, and Growth: Practical Policy Decisions in a World Without Empirical Proof (EPub). Number 5-10. International Monetary Fund.

Barth, J. R., G. Caprio Jr, and R. Levine (2013). Bank regulation and supervision in 180 countries from 1999 to 2011. Journal of Financial Economic Policy 5(2), 111–219.

Bauerle Danzman, S., W. K. Winecoff, and T. Oatley (2017). All crises are global: Capital cycles in an imbalanced international political economy. International Studies Quarterly 61(4), 907–923. Bernhard, W. and D. Leblang (1999). Democratic institutions and exchange-rate commitments.

International Organization 53(1), 71–97.

Blyth, M., B. Mark, et al. (2002). Great transformations: Economic ideas and institutional change in the twentieth century. Cambridge University Press.

Bodea, C. and R. Hicks (2015). Price stability and central bank independence: Discipline, credibility, and democratic institutions. International Organization 69(1), 35–61.

Boehmer, E., R. C. Nash, and J. M. Netter (2005). Bank privatization in developing and developed countries: Cross-sectional evidence on the impact of economic and political factors. Journal of Banking & Finance 29(8-9), 1981–2013.

Chinn, M. D. and H. Ito (2008). A new measure of financial openness. Journal of comparative policy analysis 10(3), 309–322.

Chwieroth, J. (2007). Neoliberal economists and capital account liberalization in emerging markets. International organization 61(2), 443–463.

Cornett, M. M., G. Hovakimian, D. Palia, and H. Tehranian (2003). The impact of the manager– shareholder conflict on acquiring bank returns. Journal of Banking & Finance 27(1), 103–131. Cull, R., M. S. M. Peria, and J. Verrier (2018). Bank Ownership: Trends and Implications. The

World Bank.

Drezner, D. W. (2012). The irony of global economic governance: The system worked. Council on Foreign Relations International Institutions and Global Governance Program, Working Paper. Esping-Andersen, G. (1990). The three worlds of welfare capitalism. Princeton University Press. Forsyth, D. J. and D. Verdier (2003). The origins of national financial systems: Alexander

Gerschenkron Reconsidered, Volume 23. Routledge.