ARTICLE INFO Ratikanta Barik

Master of Business Administration (MBA) , Asian Institute of Technology, Thailand.

Keywords: Canonical correlation, Option pricing, Horizon of risk, Financial indicators, Debt service ratio, Reserves over three months of imports. Corresponding author.

Email:

[email protected]

(R.Barik)

1. IntroductionExporting manufactured goods and agricultural goods into foreign markets exposes the exporter the risk of insolvency or delayed payment by foreign buyers. These risks are not only applicable to private buyer but also government buyers as well. It is very critical for an exporter to consider the available information about foreign markets and foreign importers. This helps the exporter to assess whether the foreign buyer will default on export credit payment or declare insolvency.

The indebtedness and creditworthiness of countries are major factors which determine the cost of financing and payment arrangements available to them and countries with adverse external financial situations such as in recession, war, and natural calamities have to shell out more to avail the financing and payment

ABSTRACT

The purpose of this dissertation is to compute and compare the export credit insurance premium by option valuation and OECD method. The tools from option pricing theory, Schich model and country risk assessment model for OECD method of premium were used to calculate the premiums. The comparison of premiums by both methods is carried out by canonical correlation analysis which is a multivariate statistical tool in SPSS. The canonical correlation coefficients provides evidence that the there is significant magnitude of relationship exists between the two premiums computed by two different methods.

Article history:

Received 31October 2015 Received in revised form 23 December 2015 Accepted 8 January 2016 Available online 10 March 2016

EXPORT CREDIT INSURANCE PREMIUM: OECD AND OPTION VALUATION

METHODS COMPARISON

credit agencies, the present study places particular emphasis on the identification of the determinants of these risk premiums that are specific to each debtor country, e.g. its liquidity and solvency indicators.

As per Posner (1997), the risks of foreign market are divided into three types namely commercial, political and economic. Commercial risk arises from the way each country conducts its business in areas such as tariffs, duties and freight structure. The commercial risks include buyer insolvency, default on payment, repudiation of goods, or contract termination (Posner, 1997). Wars, revolutions or civil disturbances in foreign countries are commonly recognized as political risks. This kind of risk often creates various problems for most exporters trying to conduct a profitable and stable business. Political risks also arise from foreign exchange conversion, transfer payment difficulties, insurrection, and cancellation of import or export permits and/or changes in policies or government regimes that impose new restrictions on or delay the execution of exporting contracts (Posner, 1997). Any form of political risk can either reduce the market share or slow down (or even stop) the exporters’ cash flow. According to Posner (1997), economic risks arise from the strengths and weaknesses of an importing country’s economic conditions.

In 1919, the British government established its Export Credit Guarantee Department (ECGD) with the main objective of assisting its domestic exporters to minimize risks and increase export sales in risky foreign markets. This establishment was a hallmark of the first government to provide export insurance and finance to its domestic exporters. Since then, many governments have followed the British government’s lead by establishing their own export credit programs and established Export credit agencies (ECAs) as public company or as private company.

The governments which used export credit insurance and/or guarantee programs considered these programs to be useful policy instruments and a means o f encouraging their producers to expand and diversify exports in manufactured goods. These programs were necessary to improve their trade balance and/or increase their foreign exchange reserves, instead of relying only on earnings from their primary export goods (UNCTAD,1976). In addition, the governments put great emphasis on promoting their exports through export credits as a strategy for

solving the balance of payments, unemployment, or other economic problems that resulted in mass poverty (Mutharika, 1976).

Export credit insurance is an important source of promoting trade financing for many countries. Due to the history of economic downturn worldwide at different point of time in different countries, exporters face a high risk of losses. Even if a company have never skipped payments, the company could become insolvent due to unforeseen circumstances. In these vibrant and dynamic world market conditions, export credit insurance would protect export businesses.

However, there is gap between premium charged by export credit agencies and actually what the premium would have been. This research will answer how macroeconomic indicators of a country and their change affect the rate of premium and comparison of export credit insurance premium by option valuation approach and Knaepen Package.

For this, theoretical models for valuation of export credit insurance of Option valuation approach and OECD method of calculation of premium is followed. As per Option method of valuation, export credit insurance is a derivative which behaves like put option. This option gives the buyer of the option to sell an asset to the writer of the option at a pre-decided price and expiry date. In the same way the exporter who has export credit insurance holds the right to sell his claim to the export credit insurance provider. Due to its similarity with put option, the analogy by Schich takes the option pricing theory to value the export credit insurance. Particularly the Black-Scholes portfolio arbitrage concept applied to value such insurance.

The Knaepen package was finalised on 20th Jun 1997 and integrated formally into the arrangement in December 1997. The aim of this package was to provide guidelines for setting premium fees for the export credit insurance by all the participating countries.

The key components of Knaepen package are: - A methodology for classification of countries into 7 risk categories as per their country credit risk profile.

- Formula to calculate minimum premium rates for each category of risk

extensively with the macro economic factors of a country. The premium rate computation methodology depends on a country’s risk score derived from external financial indicators and allocating rating based on the score.

So by obtaining premium rate by both methods, then compare whether both the premium rate for a particular country for a particular year converges or diverges significantly by canonical correlation analysis. 2.Option valuation and OECD valuation methodology

All the data are from secondary source from IMF International financial statistics (IFS) and World Bank. For application purpose there are 14 countries taken as samples from different parts of the world namely Argentina, Brazil, Chile, Columbia, India, Malaysia, Mexico, Nigeria, Pakistan, Peru, Romania, Thailand, Turkey and Venezuela. The period for which premium rates are computed are from 1990 to 2011 i.e. 21 years. Option valuation

Cost of export credit insurance by Schich model is done by putting the data in the option valuation equation for different countries for different historical years. The similarity between European put option and export credit insurance can be seen in payoffs.

Payoff from insurance = max {0; X - S}

Where X is the strike price which is value of the insured amount i.e. contractual debt service and S is the spot price i.e. the debt service that is actually made. If default occurs then the payoff is the difference between D and A and the payoff is zero for no default.

The equation for Premium rates for Export credit insurance as per option valuation approach is

Pt = r

e

- [²”(-s

s

)

2

µ

)

(

2-+

N

K

Ln

) -

e

^

µ

(K/N) ²” (-)]

Here ²”(.) is the cumulative normal probability for

a normal random variable having mean 0 and s = 1.

The cumulative normal probability is computed in EXCEL with the =NORMSDIST ( ) function.

The below assumptions are taken as representations of the right side of the equation:

K/N is approximated by debt service ratio

µ is approximated by the rate of change of debt service ratio

ó is approximated as the volatility of rate of change of debt service ratio

Another parameter is

K/N is approximated as the reserves over three months of imports

µ is approximated by the rate of change of reserves ó is approximated as the volatility of rate of change of reserves

Debt service ratio from World Bank and reserves over three months of imports from IFS are taken for above mentioned 14 countries. Average rate of change is calculated by using the below formula:

Where A(x) = Average rate of change of debt service ratio

F(b) = debt service ratio current year F(a) = Debt service ratio previous year b = current year

a = Previous year

The volatility determines the extent to which the underlying asset will move between now and expiration. Volatility per year is per the below formula

Where s = Standard deviation of change for last

three years

T = Three years

r = Rf = risk free rates for the country

OECD valuation

Application of Kneapen package will be step wise: 1. Country risk assessment model development 2. Minimum premium rate computation Step 1: Country risk assessment model development

Country risk can be defined as the degree of default may be arising from political, commercial and economic risks. Major element of country risks as per OECD are general moratorium, delay in transfer of funds, fluctuation in exchange rates, decision to prevent payment and force majeure.

The model uses 10 macroeconomic data as quantitative indicators and these are

a. Change of Per capita income GNI b. Change in GDP annually

c. Change in Inflation, consumer prices (annual %) d. Change in reserves

e. Change in Export of goods and services (% of GDP)

f. Change in Import of goods and services (% of GDP)

g. Total debt service (% of Export of goods , services and primary income)

h. Change in exchange rate

i. Central Government debt as (% if GDP) j. Standard & Poor Ratings

Then the weighting of all the indicators are done for a particular year and a score is computed for a particular country for a particular year. The score obtained is by quantitative factors. The bucketing of all the above 10 factors are given in Appendix 12.

By combining all the scores, a total score is calculated for a country for a particular year. As per scores, the countries are classified into 7 risk premium categories in appendix 13.

Step 2: Minimum premium rate computation The equation and values for coefficients are attached in the appendix 11

After getting premium rates then comparison of premium by both models can be done to investigate whether both data converge or deviate marginally or significantly. Statistically verify whether the premiums by both methods are related to each other or totally

independent. If related then the degree of association by canonical correlation analysis in SPSS.

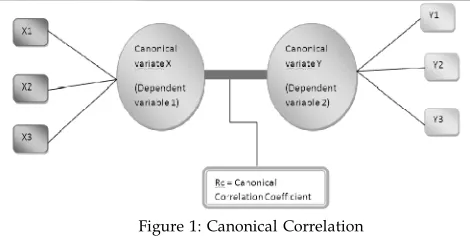

3. Canonical correlation analysis

It is a statistical multivariate tool that defines the relations between two sets of variables. It provides evidence that whether two dependent variables are related by any means and gives the strength of the relationship between the two variables.

Dependent variable 1 (X) = Premium by option valuation

Dependent variable 2 (Y) = Premium by OECD valuation method

X1, X2, X3... = Independent variables of option valuation such as debt service ratio and reserves over three months of imports etc.

Y1, Y2, Y3... = Independent variables of OECD valuation such as change in per capita income, change in GDP and change in CPI etc.

Rc = Canonical correlation co efficient which quantify the magnitude of relationships between two dependent variables.

4. Results and Discussions

There are 14 countries from different parts of the world are taken for study. Premium by both methods are calculated for all the 14 countries from 1990 to 2011. Export credit insurance premium by option valuation using debt service ratio (Appendix 1) and by reserves over 3 months of imports in (Appendix 2). Similarly export credit insurance premium by OECD method by taking horizon of risk 1.25 years is in (Appendix 3) and by taking horizon of risk 1.50 years is in Appendix 4.

The discussions part is divided into 6 subsections and those are:

A. Canonical correlation analysis of SPSS output B.Impact of volatility of debt service ratio on premium

C. Impact of volatility of reserves over three months of imports on premium D. Comparison of premiums by debt service ratio and reserves

E. Comparison of premiums by OECD method for different horizon of risk

F. Impact of risk ratings by country risk assessment model on premiums by OECD method A. Canonical Correlation analysis of SPSS output

When compared the option premium by both method, found interesting results from the canonical correlation analysis in SPSS.

Table 1 SPSS output for Thailand

Table 2 Multivariate tests of significance for Thailand

Statistical significance is done at 0.01 level and also test statistics such as Wilks’ lambda, Pillai’s criterion, Hotelling’s trace and Roy’s gcr and the Appendix 5 also contains the details of all tests, which all indicate that the canonical functions are statistically significant at the 0.01 level for Thailand.

Table 3 Canonical correlation coefficient for Thailand

With the canonical relationship deemed statistically significant and the magnitude of the canonical correlation coefficients is very high, we proceed to make substantive interpretations of the results by canonical loadings (structure correlations).

Table 4 Standardized canonical coefficients for Dependent variables

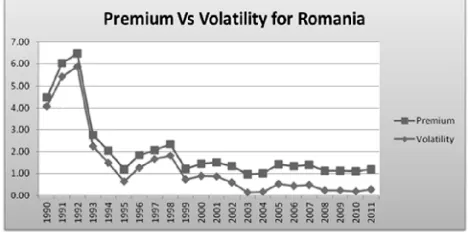

Statistical significance is done at 0.01 level and also test statistics such as Wilks’ lambda, Pillai’s criterion, Hotelling’s trace and Roy’s gcr and the Appendix 6 also contains the details of all tests, which all indicate that the canonical functions are statistically significant at the 0.01 level for Romania.

Table 6 Canonical correlations coefficients for Romania

The canonical correlation coefficient for Romania is 0.91347 which indicates that strong relationship exists between the premiums by two different methods.

Similarly for India the SPSS output for canonical correlation is in Appendix 7. The canonical correlation coefficient for India is 0.82642 which indicates that strong relationship exists between the premiums by two different methods.

So by taking premiums by option valuation and OECD method for Thailand, Romania and India as samples, it can be inferred that that two premiums are not totally different and there is strong relationship exists and the degree of relationship is given by the canonical correlation coefficients.

B.Impact of volatility of debt service ratio on premium

This is related to the macroeconomic indicators impact on the export credit insurance premium. The relationship between volatility of debt service ratio and premium by option valuation is analysed below by plotting graphs between volatility of debt service ratio and premium for different countries taken on sample basis.

Figure 2: The impact of volatility of debt service ratio on premium for Turkey

Figure 3: The impact of volatility of debt service ratio on premium for Romania

Figure 4: The impact of volatility of debt service ratio on premium for Peru

Figure 5: The impact of volatility of debt service ratio on premium for India

Figure 6: The impact of volatility of debt service ratio on premium for Nigeria

insurance premium. The increase in volatility increases the rate of premium and the decrease in volatility decreases the rate of premium.

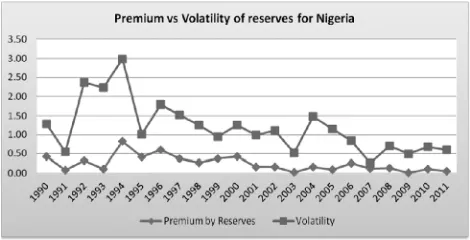

C. Impact of volatility of reserves on premium The below graphs are showing the relationship between premiums and volatility of reserves over three months imports.

Figure 7: The impact of volatility of reserves on premium for Pakistan

Figure 8: The impact of volatility of reserves on premium for Nigeria

From the above graphs for different countries, the inference is that the trends of all the graphs are same for all the countries. It is concluded that the volatility of reserves over 3 months of imports are one of the factor for determining the premium but less significant than debt service ratio. The premium rate does not move very closely to the volatility of reserves over three months of imports.

D. Comparisons of premiums by debt service ratio and ratio of reserves over three months of imports.

Figure 9: The comparison of premiums by debt service ratio and reserves for Pakistan

Figure 10: The comparison of premiums by debt service ratio and reserves for Nigeria

From the above graphs, the premium by debt service ratio is more than the premium by reserves over three month’s imports. Also the fluctuation of premium rate by reserves over three months of imports is more than the fluctuation of premiums by debt service ratio. This is due to the volatility of reserves over three months import is very high for the sample countries. So the premium by debt service ratio is more stable than the premium by reserves.

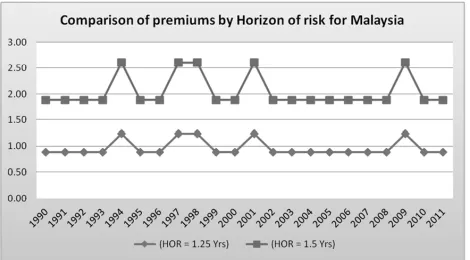

E. Comparisons of premiums by OECD method for different horizon of risk

Figure 11: The comparison of premiums by OECD as per horizon of risk for Thailand

Figure 13: The comparison of premiums by OECD as per horizon of risk for Malaysia

From the above graphs, the export credit insurance premium is higher for higher horizon of risk. So for the three countries taken as sample basis clearly demonstrates the impact of horizon of risk on the premium rates by OECD method.

F. Impact of risk ratings by country risk assessment model on premiums by OECD method

Figure 14: The comparison of premiums by OECD as per risk ratings for India

Figure 15: The comparison of premiums by OECD as per risk ratings for Mexico

The premium rate by OECD method depends primarily on the country risk category into which the country of the buyer/guarantor is classified. There are seven country risk categories of which seven (1 lowest risk to 7 highest risk) are used for the calculation of the premium. From the above graphs for India and Mexico, the premium rates are very closely related to the risk rating of the countries. If the risk rating downgrades, the premium increases and vice versa. It is so because the coefficients in the OECD method of premium calculation increase as the risk rating downgrades. Conclusion

The premiums by option valuation and OECD methods are not different from each other. There is strong degree of correlation exists between them as per the canonical correlation coefficients. The volatility of debt service ratio is very significant determinant of premium by option valuation method than volatility of reserves over three months of import. The countries traders with higher volatility in reserves over imports ratio which indicates the liquidity position and higher volatility in debt service ratio which describes the solvency situation of countries have to shell out more premiums for the export credit insurance protection. The premium by debt service ratio is more stable than the premium by reserves over three months of imports. The premiums by OECD method depend on the horizon of risk and risk ratings of countries. The premium rates for the export credit insurance increases for the rise in horizon of risk and vice versa. The premium increases if the risk rating downgrades and vice versa.

scoring is subjective. Also horizon of risk for each country is as per assumption made on length of disbursement period and length of repayment period due to unavailability of direct HOR. Political risk not covered in the OECD model. The current account is not included in the country risk assessment model.

The impact of government interventions (such as subsidies, quota and tariff etc) on the insurance premium charged by export credit agencies can be studied and further insights can be provided to this research. More variables can be incorporated as proxies for option valuation model.

Acknowledgements

I would also like to deeply extend my gratitude to Dr David Camino for being there in each step of this research completion and Dr. Juthathip Jongwanich and Dr. Supasith Chonglerttham for their invaluable inputs in conducting this research.

References

BLACK, F., and SCHOLES, M. [1973]: “The Pricing of Options and Corporate Liabilities,” Journal of Political Economy, 81, 637–654.

CLAESSENS, S., and VAN WIJNBERGEN, S. [1990]: “Secondary Market Prices Under Alternative Debt Reduction Strategies: An Option Pricing Approach with an Application to Mexico,” CEPR Discussion Paper, 415.

DOOLEY, M.P., FOLKERTS-LANDAU, D., SYMANSKY, S.A., and TYRON, R.W. [1990]: “Debt Reduction and Economic Activity,” IMF Occasional Paper, 68.

FEDER, G., and JUST, R. [1977]: “A Study of Debt-Servicing Capacity Applying Logit Analysis,” Journal of Development Economics, 4, 25–38.

GENOTTE, G., KHARAS, H., and SADEQ, S. [1987]: “A Valuation Model for Developing Country Debt,” World Bank Economic Review, 1(2), 169–176.

KLEIN, M. [1991]: “Bewertung von L¨anderrisiken durch Optionspreismethoden,” Kredit und Kapital, 24(4), 484–507.

KLEIN, M. [1994]: Bewertung von L¨anderrisiken. Berlin: Duncker & Humblot.

NOCERA, S. [1989]: “Pricing an Interest Payment Guarantee: A Contribution to Debt Reduction Techniques,” IMF Working Paper, WP/89/65.

SCHICH, SEBASTIAN T. [1994]: “Export Credits and the Cost of Trade Financing,” Ph.D. dissertation, London School of Economics.

SCOTT, L. [1990]: “Pricing Floating-Rate Debt and Related Interest Rate Options,” IMFWorking Paper, WP/90/7.

SILVERMAN, B.W. [1986]: Density Estimation for Statistics and Data Analysis. London: Chapman and Hall.

SOLBERG, R.L. [1988]: Sovereign Rescheduling: Risk and Portfolio Management. London: Unwin Hyman.

WHITE, H. [1980]: “A Heteroscedastic-Consistent Covariance Matrix Estimator and a Direct Test for Heteroscedasticity,” Econometrica, 48, 817–838.

Appendix :

S

P

S

S

O

ut

put

o

f

Ca

n

o

n

ic

al

c

or

re

la

ti

o

n

a

n

al

ys

is

f

o

r

T

h

ai

la

n

S

P

S

S

O

ut

put

of

Ca

n

o

n

ic

a

l

co

rr

el

a

ti

o

n

a

n

al

y

si

s

fo

r

In

di

Syntax for Canonical correlation analysis in SPSS MANOVA IAH SBS with MA MF PD K

/discrim stan corr alpha(1)

/print signif(mult univ eigen dimenr) /noprint param(estim)

/method=unique /error within+residual /design .

In statistics, latent variables (as opposed to observable variables), are variables that are not directly observed but are rather inferred (through a mathematical model) from other variables that are observed (directly measured).

Appendix 11

Calculation of the minimum premium rates by OECD methodology

MPR = ((a* HOR)+b)*(PC/.95)*QPF*PCF*(1-MEF)*BRF Where:

- a and b are coefficients associated with the applicable country risk category

- HOR is horizon of risk

- PC is the percentage of cover

- QPF is the quality of product factor

- PCF is the percentage of cover factor

- MEF is the country risk mitigation/ exclusion factor

- BRF is the buyer risk cover

Length of disbursement period 0.5 1

Length of repayment period 1 1

The Percentage of Cover (PC) expressed as a decimal value (i.e. 95 per cent is expressed as 0.95) The Percentage of Cover Factor (PCF) is determined as follows:

For PC <= 0.95, PCF = 1

For PC > 0.95, PCF = 1 + ( (PC - 0.95) / 0.05 ) * percentage of cover coefficient

Country risk category 1 2 3 4 5 6 7

Percentage cover coefficient 0 0.00337 0.00489 0.01639 0.03657 0.05878 0.08598

The Country Risk Mitigation/Exclusion Factor (MEF) is assumed as follows: For export credits with no country risk mitigation, MEF = 0

The Buyer Risk Cover Factor (BRF) is determined as follows: When cover for buyer risk is excluded completely, BRF = 0.90 When cover for buyer risk is not excluded, BRF = 1