PERFORMANCE PERSISTENCE IN INDIAN MUTUAL FUNDS USING

DATA ENVELOPMENT ANALYSIS

Dr Vipul Sharma

Associate Professor, University of Petroleum & Energy Studies, Dehradun

&

Dr Geetika Sharma

Research Scholar, Mahrishi Dayanand University, Rohtak

ABSTRACT

The paper aims at observing improvements and stability in the efficiencies/ performance of

mutual funds of India over successive time periods. It proposes a methodology to test the

dependence of future performance of mutual funds on their past performance of the selected

mutual funds. The paper utilizes a time series analysis technique known as Window analysis

based on the technical efficiency scores obtained by employing the Data envelopment technique

(DEA) on our dataset. The results obtained were further subjected to Regression analysis to

investigate the performance persistence of the mutual funds.

Keywords: Performance Persistence, Mutual Funds, Data Envelopment Analysis

Introduction

Performance persistence refers to a tendency of an organization to obtain similar results in consecutive periods and the ability of a fund to maintain its relative performance ranking against a specified benchmark over time. The finance literature specifies two types of this tendency: winning persistence which occurs when organizations repeat good results, while it’s opposite – losing persistence – means achieving bad results in subsequent periods. Performance reversal is a

International Research Journal of Management and Commerce

ISSN: (2348-9766) Impact Factor- 5.564, Volume 4, Issue 10, October 2017

Website- www.aarf.asia, Email : [email protected] , [email protected]

specific type of return dependence and it consists in being a winner after losing or a loser after winning in performance distribution.

The issue of whether persistence in performance exists, is important for several reasons: the financial media devotes considerable space to the publication of performance tables and the identification of funds with superior ‘track records’; fund managers’ reputations and remuneration are heavily influenced by their ability to achieve consistently ‘superior performance’(Fierman(1994)); much of the marketing of funds is based on their performance

track record (Hartman and Smith (1990)); and, from the perspective of the investors, historical performance is an important criterion in the choice of a fund (Capon et al(1996)).

From an academic perspective the existence of persistence is of interest because of its implications for market efficiency. Early tests of the weak-form of the efficient market hypothesis indicated that the history of past share prices contained no information which could be used to predict future price movement. Persistence in performance is synonymous with predictability. If past performance is a reliable guide to future performance, this means that there is information in the past performance which can be used to predict future performance. Whilst performance predictability by itself is far from conclusive evidence of market inefficiency, it nevertheless provides an impetus for further research in this area.

The empirical research on the issue of performance persistence of mutual funds is important to the managers of collective investment companies as well as investors for several reasons. First of all, the investors may treat performance persistence as a key factor for investment decisions. Secondly, the research on performance persistence helps to evaluate the efficiency of organizational solutions and human resources policy applied by the mutual funds. Thirdly, the analysis of mutual funds performance could reveal the causes leading to the occurrence of performance persistence or non-persistence, which in turn may be explained by market tendencies or valuable and diverse skills of fund managers.

Review of Literature

persistence in the mutual funds for a longer duration. Elton, Gruber & Blake (1996) and Drooms and Walker (2001) found the evidence of positive persistence up to three years.According to Chen, Jegadeesh and Wermers (2000); Jan and Hung (2004); Rao (2006), Kaur A (2011) performance persistence exists in the mutual funds. Their results confirmed that the investors can gain by selecting mutual funds on the basis of their past performance. James and Douglas (1998) found no relationship between past performance and future returns as far as bond mutual funds are concerned. And thus they did not support the existence of performance persistence in the mutual funds. In another study by Jan and Hung (2003), the authors did not support the performance persistence in the mutual funds..

Banerjee and Chakrabarti(2008),used a regression approach and a contingency table approach to test persistence, and the results were further substantiated with a Spearman Rank Correlation Coefficient test. Their analysis shows moderate evidence of persistence. With shorter time horizons like three months or six months, many cases of reversal are observed but if the time horizon is one year, the persistence exhibited is quite prominent, particularly for growth funds. Literature gives a little evidence of using Window analysis as a tool to test persistence in the performance of mutual funds, which motivates us to take up this methodology.

Objectives of the Study

The main aim of this section is to examine the performance persistence of Indian equity mutual funds (represented by 33 Open ended Equity (Diversified /Large Cap) over time in the light of Data envelopment analysis(DEA).So, the changes in performance over time can be studied with respect to

The improvements in the technical efficiency scores in successive time periods. The stability in the technical efficiency scores and ranks over different time horizons. The dependence of future performance of mutual funds on their past performance.

The Data and the Methodology

The data have been collected from the website of Association of Mutual funds in India and Personnel FN .Out of 46 companies listed under open-ended equity(Diversified/Large Cap Growth fund(Regular plan)) fund selected, a total of 7 such mutual fund schemes were dropped out which were operating with asset under management of less than Rs.100 crores. Moreover, the required data was missing for 6 schemes. So, 33 open ended equity (diversified /Large Cap) funds were selected to represent the mutual fund industry of India. The data was collected for the period starting from financial year 2008-09 to 2012-13.Here, financial year refers to the time period starting from 1st April of a year to 31st March of next year.

Specification of Inputs and Outputs

The selection of inputs and outputs for the performance evaluation of a process with the help of DEA needs a careful consideration as only the right selection of inputs and outputs will able to bring out the special characteristics of the process. In the conventional application of DEA, it is assumed that one can, given a collection of available measures, clearly specify which will constitute inputs and which will constitute outputs (Cook and Zhu,2006). But in some cases, the performance model is not well defined, so it is critical to select the appropriate inputs and outputs by other means. When we have many potential variables for evaluation, it is difficult to select inputs and outputs from a large number of possible combinations. The objectives of the analysis crucially rely upon the choice of inputs and outputs. The context of assessment is a key issue in selecting the inputs and outputs.

minimization analysis are fund returns (i.e. annualized daily arithmetic returns). Fund returns are net of expenses but gross of any sales charges.

The input variable standard deviation of returns (the dispersion of return) represents the fund’s total risk which may be important for the not-well-diversified small funds. The beta coefficient a measure of fund volatility relative to the SENSEX (Index of Bombay stock exchange) is estimated using the following formula

Cov(RM ,RF ) Var(RM)

Where Cov(RM , RF ) is covariance of market returns (RM ) and Fund returns( RF ). Var(RM)is the variance of market returns (RM)

Beta measures the systematic risk that cannot be further reduced through diversification but it is a statistical measure that can be quite useful for diversification and advanced risk/volatility measurement purposes. Fund returns are monetary gains on the investment made by investors. The returns may be of two types:

1. Capital Gain 2. Dividend

In the present study, growth option of diversified equity mutual funds have been selected with which is associated only the capital gains.

Window Analysis

A DEA window analysis works on the principle of moving averages (Charnes et al(1994),Yue (1992)) and is useful to detect the performance trends of a decision making unit(DMU) over time. Each DMU in a different period is treated as if it were a 'different' unit. In doing so, the performance of a DMU in a particular period is contrasted with its performance in other periods in addition to the performance of other units. This results in an increase in the number of data points in the analysis, which can be useful when dealing with small sample sizes.

To formalize, consider 𝑛𝐷𝑀𝑈𝑠 (𝑚 = 1, … , 𝑛) which are observed in 𝑃periods (𝑡 = 1, … , 𝑃) and which all use 𝑟inputs to produce 𝑠outputs. The sample thus has 𝑛𝑥𝑃observations,and an

observation 𝑚in period 𝑡, 𝐷𝑀𝑈𝑡𝑚has an 𝑟 −dimensional input vectorxtm(x1mt,x2mt,...,xrtm)T

The window starting at time k, 1kPand with the width 𝑤 ,1wPk, is denoted by kw

and has 𝑛𝑥𝑤observations.

The matrix of inputs for this window analysis is given by

) ,..., , , ,... , ,..., ,

( 1k k2 kn k1 1 kn1 1k w k2 w kn w

k x x x x x x x x

X

w

and the matrix of outputs is

) ,..., , , ,... , ,..., ,

( 1k k2 kn k1 1 kn 1 1k w k2 w kn w

k y y y y y y y y

Y

w

The input oriented DEA window problem for 𝐷𝑀𝑈𝑡′ under a variable Returns to Scale(VRS) assumption, is given by

w n m y Y x X t s m m t k t k t k w w w

1, 1,..., 0 0 . min ' ' , ' … (1)Results And Discussions

The formulae adapted from D. B. Sun (1988) can be used to study the properties of this window analysis. We already denote number of DMUs by 𝑛.We introduce the following symbols

𝑘 = 𝑛𝑢𝑚𝑏𝑒𝑟𝑜𝑓𝑝𝑒𝑟𝑖𝑜𝑑𝑠

𝑝 = 𝑙𝑒𝑛𝑔𝑡ℎ𝑜𝑓𝑤𝑖𝑛𝑑𝑜𝑤(𝑝 ≤ 𝑘)

𝑤 = 𝑛𝑜. 𝑜𝑓𝑤𝑖𝑛𝑑𝑜𝑤𝑠

We give following numerical illustrations The length is calculated as below

𝑝 =

𝑘 + 1

2 𝑤ℎ𝑒𝑛𝑘𝑖𝑠𝑜𝑑𝑑 𝑘 + 1

2 ±

1

2𝑤ℎ𝑒𝑛𝑘𝑖𝑠𝑒𝑣𝑒𝑛

So, 𝑓𝑜𝑟𝑘 = 5, 𝑤𝑒𝑔𝑒𝑡𝑝 = 3

window

no. of "different" DMUs Npw 33×3×3=297 Δ no. of DMUs n(n-1)(k-p) 33×2×2=132

Here ∆ represents an increase compared to 33× 5 = 165 DMUs that would have been available if the evaluation had been separately effected for each of the 33 DMUs in each year.

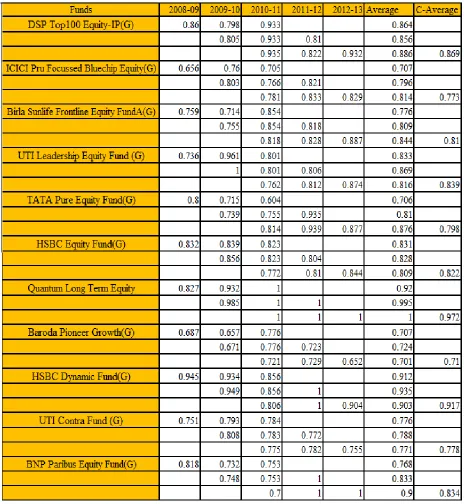

The basic idea of window analysis is to regard each DMU as if it were a different DMU in each of the reporting year 2009,2010 and 2011.The result in row 1 for DSP Top 100in table 1 represent three value obtained by using its results in 2009, 2010 and 2011 by bringing this fund into the objective for each of these years. Because 33 funds are regarded as different DMUs in each year, these evaluations are conducted by reference to the entire set of 3× 33 = 99 DMUs that are used to form the data matrix Thus the values 𝜃∗ = 0.860,0.798 𝑎𝑛𝑑 0.933 in row 1 for

DSP Top 100 represent its performance in first three years of study as obtained from this matrix. Similarly, first row results for other funds are obtained for each of the 10 mutual funds in the table 1,which we have extracted from a larger tabulation of 33 mutual funds to obtain compactness. After first row, values have been similarly obtained, a new 3-year period window is obtained by dropping the data for 2009 and adding the data for 2010 and implementing the same procedure as before produces the efficiency scores in row two for each mutual .The process is then continued until no further year are added as in the row three with its three entries. In this manner, the window analysis enables us to identify the best and the worst banks in a relative sense, as well as the most stable and variable funds in DEA scores.

The column views for this fund, at the same time shows stability. The C-average, which actually is the average of averages of row views, for Quantum Equity fund is 0.972 which suggests its good performance over this five year period of study.

Table 1 Showing Results of Window Analysis

thus showing improvement over time. Similarly ,if look through the windows of Baroda Pioneer Growth(G)and UTI Contra Fund (G),their row views do not show any reasonable improvements ant their column views marks for their consistent underperformance with a C-average of only 0.71 for Baroda Pioneer Growth(G)and 0.778 for UTI Contra Fund (G).

In the similar manner , results of window analysis can be interpreted for other funds. The knowledge of stability and improvement of the performance of funds ,if utilized carefully and cautiously, can be beneficial for not only mutual fund managers but also to the investors while choosing a robust portfolio and making a long term investment . The C-average gives a reasonably good measure of performance of a fund over a given time period .

As quoted earlier that persistence in performance is synonymous with predictability. Predictability refers to the prediction of future performance based on past performance. In our present context of DEA and window analysis, predictability will hold a relevance if the performance of the mutual funds in different windows of the analysis show a close association and dependence.

To investigate the persistence of mutual fund performance, we use the the results of window analysis carried out for 33 mutual funds of Indian mutual fund industry. We investigate persistence of performance using regression analysis by regressing average performance of window 3 of the mutual fund against average performance of window 1 and 2. Here performance refers to technical efficiency scores as obtained by employing BCC-DEA model on the data set. Therefore, the regression equation can be written as

i window i

window i

window a b TE c TE

TE 3 1 2

(2)

Where TEwindow3denotes the average technical efficiency of window 3 of ith mutual fund.

1 window

TE denotes the average technical efficiency of window 1 of ith mutual fund.

2 window

TE denotes the average technical efficiency of window 2 of ith mutual fund.

The regression equation is

Window3 = 0.190 - 0.259 Window1 + 1.03 Window2

Predictor Coefficient Standard Error Coefficient

T P

Constant 0.19001 0.07633 2.49 0.019

Window1 -0.2589 0.1269 -2.04 0.039

Window2 1.0350 0.1428 7.25 0.000

S = 0.0345878 R-Sq = 73.4% R-Sq(adj) = 71.7%

Analysis of Variance Source Degree of

Freedom

Sum of Squares

Mean Square F P

Regression 2 0.099196 0.049598 41.46 0.000

Residual Error 30 0.035889 0.001196 - -

Total 32 0.135085 - - -

Regression analysis tests the null hypothesis that constant=0. TEwindow1andTEwindow2 =0.The

results reveal that estimates of coefficients TEwindow1and TEwindow2in the regression equation 2 are

-0.2589 and 1.030 respectively. The corresponding t-statistics are 0.039 and 0.00 which is

significant at 5% level of significance .Therefore it can be concluded TEwindow1and TEwindow2 play

a significant role in the regression model. The regression analysis suggests a strong association between the past and future performance of mutual funds. The value 𝑅2 𝑎𝑑𝑗 = 71.7%

indicates that when ever we observe a variation in the value of TEwindow3, 71.7%% of it is due to

the model (or due to change in TEwindow1and TEwindow2 ) and the rest is due error or some

unexplained factor.

Here, ANOVA tests the hypothesis that TEwindow1and TEwindow2are equal to zero.In fact F is

nothing but T-square. A low p-value suggest that TEwindow1and TEwindow2plays a significant role in

Conclusions and Findings

The investigation of the improvements and stability in the performance of33 open ended equity (Diversified /Large Cap) funds of the mutual fund industry of India has been carried out using the tools DEA and window analysis for a five year(financial year) period of study 2008-09 to 2012-13in a purview of guiding investors and fund manager while choosing a portfolio and planning a long term investment.

Persistence and predictability in the performance has also been observed using the aforementioned tools along with regression analysis.

Table 2 Categorization of mutual funds based on persistence in performance.

References

Banerjee, A., & Chakrabarti, B. B. (2008). Persistence in performance of Indian equity mutual funds: An empirical investigation. IIMB Management review, 20(2).

Banker, R. D., Charnes, A., & Cooper, W. W. (1984). Some models for estimating

technical and scale inefficiencies in data envelopment analysis. Managment science, 30, 1078-1092.

Basso, A., & Funari, S. (2001). A Data Envelopment Analysis approach to measure the

mutual fund performance. European Journal of Operational Research, 135, 477-492.

Capon, N., Fitzsimong, G. J., & Prince , R. A. (1996). An individual level analysis of the

mutual fund investment decision. Journal of financial services research, 10, 59-82.

Carhart, M. M. (1997). On persistnence of mutual fund performance. Journal of finance,

52(1), 57-82.

Chen, H. L., Jagdeesh, N., & Wermers, R. (2000). The value of active mutual fund

management: An examination of the stockholdings and trades of fund managers. Journal of financial and quantitative analysis, 35(3), 343-368.

Choi, & Murthi. (2001). Relative performance evaluation of Mutual funds:A

non-parametric approach. Journal of Business Finance and Accounting, 23(7&8), 853-876.

Cook, W. D., & Zhu, J. (2006). Incorporating multi-process performance standards into the DEA framework. Operations Research, 54(4), 656-665.

Daraio, C., & Simar, L. (2006). A robust non-parametric approach to evaluate and explain

the performance of mutual funds. European Journal of Operational Research, 175, 516-542.

Drooms, & Walker. (2001). Persistence of mutual fund operating characterstics: returns,

turnover rates and expense ratios. Applied financial economics, 11(4), 457-466.

Elton, Gruber, & Blake. (1996). The persistnece of risk adjusted mutual fund performance.

Fierman, J. (1994, January 24). The contingency workforce. Fortune, pp. 30-36.

Grinblatt, M., & Titman, S. (1989). Mutual fund performance: an analysis of quarterly

portfolio holding. Journal of Business, 62(3), 393-416.

Grinblatt, M., & Titman, S. (1992). The persistence of mutual fund performance. Journal

of finance, 47(5), 1977-84.

Hartman, D. E., & Smith, D. K. (1990). Building a competitive advantage in mutual fund

sales. Journal of retail banking, 12, 43-49.

Jan, Y. C., & Hung, M. W. (2003). Mutual fund attributes and performance. Financial

services review, 12, 165-178.

Jan, Y., & Hung, M. W. (2004). Short-run and long-run persistence in mutual funds. Journal of investing, 13(1), 67-71.

Kaur, A. (2011). Persistence in performance of equity mutual funds in India-an empirical

investigation. International journal of management and computing sciences, 1(3), 77-86.

Morey, M. R., & Morey, R. C. (1999). Mutual fund performance appraisals: A

multi-horizon perceptive with endogenous benchmarking. Omega, 27, 241-258.

Rao, N. D. (2006). Investment style and performance of equity mutual funds in India.

Retrieved May 2012, from SSRN:

http://papers.ssrn.com/sol3/papers.cfm?abstract__id922595

Sedzro, K., & Sardano, D. (1999). Mutual fund performance evaluation using data

envelopment analysis. University of Quebec, School of Business, Montreal,Canada.

Sengupta , J., & Zohar, T. (2001). Non-parametric analysis of portfolio efficiency . Applied Economics Letters, 249-252.

Sun, D. B. (1988). Evaluation of managerial performance in large commercial banks by data envelopment analysis. Ph.D. Thesis, The university of texas, Graduate school of business, Texas.

Tulkens, H., & P., V. E. (1995). Non-parametric efficiency, progress and regress measures

for panel data:Methodological aspects. European journal of research, 80(3), 474-499.

Yue, P. (1992). Data envelopment analysis and commercial bank performance: A primer