Issues

ISSN: 2146-4138

available at http: www.econjournals.com

International Journal of Economics and Financial Issues, 2016, 6(S4) 26-35.

Special Issue for "International Conference of Accounting Studies (ICAS 2015), 17-20 August 2015, Institute for Strategic and Sustainable

Accounting Development (ISSAD), Tunku Puteri Intan Safinaz School of Accountancy, College of Business, Universiti Utara Malaysia, Malaysia"

Management Control System and Performance: Accountability

Attributes in Local Authorities

Norazlina Ilias

1*, Nik Kamaruzaman Abdulatiff

2, Nafsiah Mohamed

31Centre for Fundamental and Liberal Education, Universiti Malaysia Terengganu, 21030 Kuala Terengganu, Terengganu, Malaysia, 2Faculty of Accountancy, Universiti Teknologi Mara Kelantan, Bukit Ilmu, 18500 Machang, Kelantan, Malaysia, 3Accounting Research Institute & Faculty of Accountancy, Universiti Teknologi Mara, 40450 Shah Alam, Selangor, Malaysia.

*Email: [email protected]

ABSTRACT

This study used the structural equation modeling tool to examine the impact of management control system on performance in Malaysian local authorities. This study applies a questionnaire-based survey to look for responses from 899 heads of departments attached to the local authorities within Peninsular Malaysia. Out of the 899 questionnaires distributed, 372 were returned, which resulted in 335 usable responses that were used for further analysis. Statistical results showed that the external control and formal internal control were significantly associated with all three performance dimensions - financial, service quality, and procedural, as expected. However, the internal informal control only had a significant relationship with the service quality performance. This study also revealed that the external control, through the presence of the formal internal control, had a stronger relationship with all the three performance dimensions, as compared to the direct relationship between the external control and performance.

Keywords: Management Control System, Performance, Accountability, Local Authorities, Structural Equation Modeling

JEL Classifications: M410, M490

1. INTRODUCTION

Recently the topic of performance of Malaysian local authorities has attracted the attention of both the government and the public. The demands of the public and other stakeholders and continuous complaints concerning the dissatisfaction with the public

services have contributed to the urgent need for accountability

and transparency in delivering public services (Ibrahim and Karim, 2004). This is because local authorities are devices for delivering public services to the local community through the efficient use of resources. The local authorities need to create value for all resource providers to satisfy them, especially the public as they are part of the resource providers through their tax payments. Indeed, the public is becoming more aware that failure in the value creation will be reflected in the value that they can receive from the service providers, for example, the

services from the local authorities. As a result, the role of local governments as service providers are now becoming more and more important as its functions are seen as an essential system to govern the community.

2. LITERATURE REVIEW

Kloot (1999) and Chan (2004) claimed that local authorities should have a good performance measurement system (PMS) to ensure that the public services could be delivered successfully to the community. Therefore, the MCS, as part of the PMS, should be implemented systematically to increase the performance of the local authorities. Through the implementation of an MCS, the service delivery to the public could be evaluated to identify whether its objectives and targets are achieved. Greiling (2005; 2006) believed that the use of an MCS in the public sector will increase the effectiveness and efficiency of the services. Moreover, the MCS can also be used to highlight the strengths of the programs offered to the public.

In this sense, Malaysian local authorities are no exception. Khalid (2010) claimed that Malaysian local authorities have implemented control systems that are used to measure the performance of the process of service delivery, human resources, financial productivity, and customers’ satisfaction with the services received. While Khalid (2010) found that the key performance indicators (KPIs) were implemented in Malaysian local authorities to enhance the effectiveness and efficiency of the public services, Muhammad et al. (2015) suggested that the involvement of local communities in plans or programme provided by local authorities and their point of views might help in improving the services delivery. This recent study by Muhammad et al. (2015) yet reported that the local authorities are more likely to choose only some of the information given by the local communities. Thus, this will cause a conflict between local authorities and local communities.

Furthermore, Ilias (2016) conducted observations and interviews with two head of departments at one of the district councils in the East Coast Region of Peninsular Malaysia and found that KPIs had been developed in that council to evaluate the performance of the organization. Unfortunately, there were no specific internal control systems to ensure how far the KPIs were being implemented. According to the interviewees, this was due to the lack of awareness among the employees about the system, which, in turn, has led to poor performance.

One of the possible reasons for the poor performance is the absence of external evaluation and control. This was supported by Khalid (2010) who noted that even though Malaysian local authorities have KPIs as one of the tools to improve their performance, no rewards or punishments are applied when the local authorities meet or fail to meet their KPIs targets. This is because no external evaluation is made concerning the implementation of KPIs, and, further, it is used for internal purposes only. This was also supported by Agbejule and Jokipii (2009) who found that high degrees of internal control activity and low levels of monitoring would have the greater effectiveness of the internal control system. However, a high degree of internal control activity and high degrees of monitoring would lead to a very efficient internal control system. Additionally, the latest study by Berahim et al. (2015) verified that weak surveillance and enforcement by the local authorities, as well as the poor documentation and recording

systems, were among seven problems that have led to poor performance of Malaysian local authorities.

One of the ways for the local authorities to resolve these problems is by improving the MCS, as suggested by some researchers, such as Verbeeten (2008), Davila (2000), Durden (2008) and Langfield-Smith (1997). The key forces that demand the need for an MCS in an organization include undesirable behavior among people in the organization; motivational problems; and inadequate control that lead to organizational failure (Merchant, 1982).

2.1. Formal Control Systems and Informal Control Systems

Horngren et al. (2011) considered MCS to be a system consisting of both formal and informal control. The formal MCS of an organization include explicit rules, procedures, performance measures, and incentive plans that guide the behavior of its managers and other employees. The formal control system comprises several systems, such as the management accounting system, which provides information regarding costs, revenue, and income; the human resources system, which contains information on recruiting, training, absenteeism, and accidents; and the quality system, which provides information concerning yield, defective products, and late deliveries to customers. On the other hand, informal MCS include shared values, loyalties, and commitment among members of the organization, organizational culture, and the unwritten norms of acceptable behavior of the people in the organization (Anthony and Govindarajan, 2007).

In another review paper, Macintosh and Daft (1987) classified MCS as a formal control and defined them as a package of

control that includes accounting reports, budgeting, formal hierarchy and supervision, job descriptions, rules and standard operating procedures, statistics for measuring performance, organizational structure, and employees and performance appraisal systems. In addition, Simons (1990) defined MCS as a precise control that involves the formal procedures and systems to maintain or to alter patterns in organizational activities. The

definitions of MCS by Macintosh and Daft (1987) and Simons (1990) appear similar to the study of Otley and Berry (1994) in which MCS are termed as being a set of procedures and processes that manager and other organizational participants

use in order to ensure the achievement of their goals and the

goals of their organizations.

2007), Batac and Carassus (2009), Otley (1980), Ouchi (1977). Also, Chenhall (2003) classified informal control into personal control and social control. Personal control involves centralized decision-making in which individuals see themselves as having more interaction on formal-related-matters (for example budget), and being required to explain the variances in the budget. Therefore, they are satisfied with their superior-subordinate relationships. Whereas, social control relates to how the management controls the behavior of people in the organization to achieve its desired objectives, such as through the hierarchical order, institutional structure, and communication structure (Lebas and Weigenstein, 1986).

Anthony and Govindarajan (2007) also considered the process of MCS, which is much more involved with the informal interactions between one manager and another, or between a manager and their subordinates. The informal interactions normally occur

through informal communications using memoranda, meetings,

conversations, or even by facial expressions. Furthermore, they further acknowledge that both formal systems and informal processes influence human behavior in organizations, and, consequently, they affect the degree to which goal congruence can be achieved. The formal control systems normally involve strategic plans, budgets, and reports, while the informal processes take into account the work ethics, management style, and culture that exists in the organization.

A more comprehensive review of the MCS component was reported by Batac and Carassus (2009). They examined and identified budgeting, accounting and management controls as formal control, which is accompanied by informal control. They claimed that the behavior of the organizational members, which is considered as informal control, could influence the success of the formal control system, or, in other words, the informal control might affect the formal control. For example, if the organizational members readily (informal control) follow the set of policies and procedures (formal control) designed in the organization, then the MCS could be successfully implemented. In the current literature, Cuguero-Escofet and Rosanas (2013) treated the definition of MCS similar to Batac and Carasssus (2009) who referred to formal MCS as a set of objectives and rule-based control system, while the informal MCS is needed to influence the formal control process. Further, Cuguero-Escofet and Rosanas (2013) revealed that both the formal and informal control systems are crucial in improving the performance of organizations.

Based on the above discussion, it is recognized that MCS comprise

both a formal and informal system that is used by the management

to control the activities within the organization to achieve their goals and objectives. Instead of the formal and informal type of control, Batac and Carasssus (2009) also differentiated MCS into two different aspects, namely, internal and external control. Similar to other scholars on internal control who typically focus on accounting control, which is of particular interest in auditing research (see, for example, Adeyemi and Adenugba, 2011; Fadzil et al., 2005; Suyono and Hariyanto, 2012), so did Batac and Carasssus (2009). They claimed that such internal control is designed to ensure that the operational activities of the organization

are going according to plan, while, the external control, such as legal laws and external auditing practice, is used to ensure compliance with rules and regulations that govern the organization.

2.2. MCS and Performance

In the MCS literature, some studies suggested a positive relationship between MCS and performance (Herath, 2007; Ittner and Larcker, 1997; 2003; Merchant, 1982). MCS is used by

management to achieve the desired goals and to ensure that the

activities or organization are functioning by the organizational policies. It is also a process by which managers influence other members of the organization to implement the organization’s strategies to achieve the goals and objectives (Anthony and Govindarajan, 2007) by encompassing both financial and non-financial performance measures, which, in turn, might affect the organizational performance. Also, Chenhall (2003) characterized MCS as a broader term that covers management

accounting systems in achieving goals, and as a tool that

provides external and internal information to assist managerial decision-making.

All of these descriptions imply that MCS is a tool that is used in decision-making and managerial action processes. For many researchers and scholars, MCS is a part of the performance management process (Anthony and Govindarajan, 2007; Chenhall, 2003; Chenhall and Euske, 2007; Rashid, 1999) that readily lends itself to real-world applications of the management process as it leads to achieving the goals and objectives of the organization. This applied control process incorporates performance management techniques to describe and predict outcomes based on management experience.

Thus, it was proven that performance management would affect the performance of both private and public sector organizations (Chenhall and Euske, 2007; Ittner and Larcker, 1997; Verbeeten, 2008). This is consistent with Otley (1999) and Heinrich (2002) who state that the organization must organize its performance management properly to ensure the MCS could be developed successfully in the process of defining goals, selecting strategies, allocating resources, and measuring and rewarding performance to obtain better organizational results.

2.3. The Relationship between External Control and Performance

External control is one of the important components that should be considered in MCS (Gottardo and Moisello, 2011). The example of an external control that is discussed in previous research was external audit (Batac and Carassus, 2009; Coombs and Edwards, 1990; Ibrahim et al. 2004), and public regulatory authorities (Batac and Carassus, 2009; Boyne, 2000; Gottardo and Moisello, 2011).

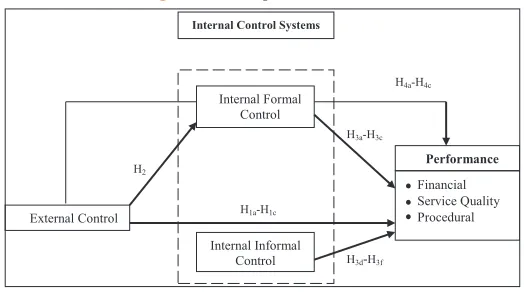

hypotheses related to external control and performance are proposed for testing:

H1a: There is a relationship between external control and financial performance.

H1b: There is a relationship between external control and service quality performance.

H1c: There is a relationship between external control and procedural performance.

2.4. The Relationship between External Control and Internal Formal Controls

It is found that the auditing by the auditor-general can help local authorities to control their internal procedures and control systems (Barret, 1996; Batac and Carassus, 2009). The auditor-general provides an opinion concerning whether the local authorities comply with the regulations in respect of accounts handling, public funds spending, financial reports, assets management and other related controls (Local Government Act 1976 [Act 171] & Subsidiary Legislation, 2010). Indeed, from the interviews that were conducted with some heads of department, Ilias (2016) found that starting in 2007, an accountability index for financial management was implemented to assess how far the rules and financial procedures were complied with by Malaysian local authorities.

Accordingly, Malaysian local authorities are also bound by other

rules and regulations, which include the Local Government Act 1976 (Act 171), Town and Country Planning Act 1976 (Act 172), Street, Drainage and Building Act 1974 (Act 133), Road Transport Act 1987 (Act 333), and Building and Common Property (Maintenance and Management) Act 2007 (Act 663). All these regulations provide guidelines that should be followed by local authorities in providing services to the public. The external control is likely to directly improve the internal control of the organization because of the higher control from outside parties (Anthony and Govindarajan, 2004; Batac and Carassus, 2009).

Moreover, Ibrahim et al. (2004) studied the audit certificate issued by the auditor-general in the local authorities of the North Coast Region of Peninsular Malaysia for the period 1997 to 2001. They found that 75.72% of the audit certificates issued to the local authorities in their study was qualified. Hence, it can be concluded that the existence of the auditor-general auditing the local authorities improved their reliability of internal control and thus led to a reduction in financial statement error.

Therefore, it is believed that the more the local authorities comply with the external control, the higher the increase in their internal control systems, both formal and informal. Based on the above arguments, it can be theorized that the existence of external control could increase internal control systems. Thus, the following hypothesis is tested:

H2: There is a relationship between external control and formal internal control.

2.5. The Relationship between Internal Control and Performance

Internal control system has been seen as a tool to enhance the

monitoring and reporting processes in the organization, and to

ensure the compliance with laws and regulations (Jokipii, 2010). Indeed, Ittner and Larcker (1997) and Herath (2007) agreed that the internal control will lead to the higher performance. In fact, Khalid (2010) found that the internal control systems such as the use of KPIs has led the improvement in local authorities’ performance.

As documented by these researchers, the ultimate goal of internal

control is to assure the achievement of predetermined objectives of the organization. In order to perform well, internal control plays the function of monitoring, communicating, measuring, reviewing and analyzing the progress of organizational strategies in achieving the targeted goals. As empirically proven in previous studies, the positive relationship between internal control and performance has been reported (Simons, 1990; Triantafylli and Ballas, 2010; Tsamenyi et al., 2011; Yahya et al., 2008). Therefore, these arguments lead to the following hypotheses:

H3a: There is a relationship between formal internal control and financial performance.

H3b: There is a relationship between internal formal control and service quality performance.

H3c: There is a relationship between formal internal control and procedural performance.

H3d: There is a relationship between internal informal control and financial performance.

H3e: There is a relationship between internal informal control and service quality performance.

H3f: There is a relationship between internal informal control and procedural performance.

2.6. Internal Control System as a Mediator

Ittner and Larcker (1997), Herath (2007) and Jokipii (2010) found evidence that the internal control system mediated the relationship between contingency factors and performance. Ittner and Larcker (1997), for instance, provided a model of how to link the quality strategy to the organizational performance while the strategic control is used as a mediator. The strategic control of Ittner and Larcker’s includes external monitoring, internal monitoring, and implementation of the strategic control system. Ittner and Larcker (1997), however, noted that formal plans that are too rigid could obstruct the performance of the organization.

Herath (2007), on the other hand, assumed that the core control package is surrounded by organizational structure and strategy, corporate culture, and management information systems. The control system package is used as a mediator in the relationship of contingent factors and the organizational performance. All these components of control system interact with each other to support the success of the controlling system, which, in turn, leads to the achievement of organizational goals and objectives.

H4a: The relationship between external control and financial performance is mediated by formal internal control. H4b: The relationship between external control and service quality

performance is mediated by formal internal control. H4c: The relationship between external control and procedural

performance is mediated by formal internal control.

The literature also supports the formulation of the conceptual framework for examining the relationship between external control, internal control systems, and performance of Malaysian local authorities (Figure 1).

3. METHODOLOGY

The unit of analysis of the study is all the departments of city councils, municipal councils, and district councils in Peninsular Malaysia. The respondents are heads of department attached to the local authorities. Currently, there are 149 local authorities in Malaysia, including in the state of Sabah and Sarawak. Out of the 149 local authorities, 99 are located in Peninsular Malaysia consisting of eight city councils, 34 municipal councils, and 57 district councils that are governed by the Local Government Act 1976. From the 99 local authorities in Peninsular Malaysia, there are 899 departments as summarized in Table 1.

For this study, it was necessary to ensure that the sample was as representative as possible of the population from which it was drawn. Additionally, because the researcher was interested in the MCS implementation in local authorities within Peninsular Malaysia, not just those in city councils or municipal councils, it was essential that the sample include all the departments from each type of local authority. In line with the above discussions and also by taking into consideration the probability of non-response, the main concerns of the researcher was to achieve a minimum of 300 usable responses. Therefore, the sample size of 899 was determined for this study by using the total number of

departments in the local authorities within Peninsular Malaysia. A questionnaire-based survey was carried out to look for responses from the 899 heads of department. Out of the 899 questionnaires distributed, 372 were returned, which resulted in 335 usable responses that were used for further analysis.

4. RESULTS AND DISCUSSIONS

This section of the study presents and discusses the empirical

results of the study based on the feedback from the questionnaire

survey. The findings are reported as follows - assessment of goodness of measures which includes the reliability and validity of the instruments used in the study, and the hypotheses testing results.

4.1. Assessment of Goodness of Measures

It is important to validate the measures used in this study as it builds trust in providing correct results. The validation of measures can be divided into two main aspects: Reliability and validity assessment. Reliability is a measure of the internal consistency of a set of scale items, whereas validity is used to determine whether the constructs of the study measure the intended concept (Sekaran and Bougie, 2011).

4.1.1. Reliability

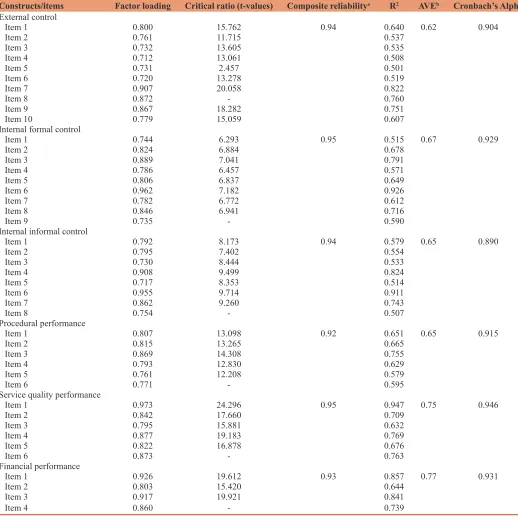

As this study used the structural equation modeling (SEM) technique to analyze the data, Bagozzi, and Yi (1988) suggest three types of reliability that could be examined: Individual item reliability, composite reliability, and average variance extracted (AVE).

4.1.1.1. Individual item reliability

Individual item reliability is computed directly by the AMOS program and is listed as squared multiple correlations (SMC) in the output, which is represented by R2. In this study, the R2 values of the measurement model in the observed variables were used as estimations for a particularly observed variable. Following Bollen (1989), R2 values of above 0.50 provide evidence of acceptable reliability.

4.1.1.2. Composite reliability

Composite reliability is used to assess measurement model reliability, which means that a set of latent construct indicators are consistent in their measurement. Items for measuring a construct with highly intercorrelated among others show that they measure the same latent construct. However, there is no definite acceptable

threshold. Fornell and Larcker (1981) suggest that values >0.50 are considered adequate, while Bagozzi and Yi (1988) suggest that values >0.60 are desirable.

4.1.1.3. Average variance extracted (AVE)

The AVE reflects the overall amount of variance captured by the latent construct. It has been suggested that the AVE value for a construct should exceed 0.50 (Bagozzi and Yi, 1988; Fornell and Larcker, 1981). Inevitably, Cronbach’s Alpha is also measured in this study for each confirmed scale. The Cronbach’s Alpha is calculated after demonstrating the uni-dimensionality of a measure as suggested by Anderson and Gerbing (1988).

Table 1: Sample

Location Type of local

authority Number of local authorities departmentsNumber of

Peninsular

Malaysia City councilMunicipal council 348 33697

District council 57 466

Total 99 899

The acceptable value of Cronbach’s Alpha in social science research is 0.70 (Hair et al., 2010; Sekaran and Bougie, 2011). All these reliabilities are shown in Table 2. It can be seen that the Cronbach’s Alpha coefficients for all the variables exceeded the 0.70 cut-off level (Hair et al., 2010; Sekaran and Bougie, 2011), thereby indicating that there was a good level of internal

consistency among the constructs, and thus indicates strong

reliability.

4.1.2. Validity

In this paper, construct validity was employed to determine the validity of the survey instruments used.

4.1.2.1. Construct validity

Construct validity is a validity test that is important when discussing the validity of instruments used in a study. Although construct validity is claimed to be the most difficult type of validity to establish, it is also the most “powerful” when it comes to measuring how well the correlations between variables can fit with the theories around which the test is designed (Sekaran and Bougie, 2011).

This can be assessed through the determination of both convergent

validity and discriminant validity (Hair et al., 2010).

According to Hair et al. (2010), three methods can be used to determine convergent validity - the analysis of factor loadings, the

Table 2: Results of confirmatory factor analysis of measurement model

Constructs/items Factor loading Critical ratio (t-values) Composite reliabilitya R2 AVEb Cronbach’s Alpha External control

Item 1 0.800 15.762 0.94 0.640 0.62 0.904

Item 2 0.761 11.715 0.537

Item 3 0.732 13.605 0.535

Item 4 0.712 13.061 0.508

Item 5 0.731 2.457 0.501

Item 6 0.720 13.278 0.519

Item 7 0.907 20.058 0.822

Item 8 0.872 - 0.760

Item 9 0.867 18.282 0.751

Item 10 0.779 15.059 0.607

Internal formal control

Item 1 0.744 6.293 0.95 0.515 0.67 0.929

Item 2 0.824 6.884 0.678

Item 3 0.889 7.041 0.791

Item 4 0.786 6.457 0.571

Item 5 0.806 6.837 0.649

Item 6 0.962 7.182 0.926

Item 7 0.782 6.772 0.612

Item 8 0.846 6.941 0.716

Item 9 0.735 - 0.590

Internal informal control

Item 1 0.792 8.173 0.94 0.579 0.65 0.890

Item 2 0.795 7.402 0.554

Item 3 0.730 8.444 0.533

Item 4 0.908 9.499 0.824

Item 5 0.717 8.353 0.514

Item 6 0.955 9.714 0.911

Item 7 0.862 9.260 0.743

Item 8 0.754 - 0.507

Procedural performance

Item 1 0.807 13.098 0.92 0.651 0.65 0.915

Item 2 0.815 13.265 0.665

Item 3 0.869 14.308 0.755

Item 4 0.793 12.830 0.629

Item 5 0.761 12.208 0.579

Item 6 0.771 - 0.595

Service quality performance

Item 1 0.973 24.296 0.95 0.947 0.75 0.946

Item 2 0.842 17.660 0.709

Item 3 0.795 15.881 0.632

Item 4 0.877 19.183 0.769

Item 5 0.822 16.878 0.676

Item 6 0.873 - 0.763

Financial performance

Item 1 0.926 19.612 0.93 0.857 0.77 0.931

Item 2 0.803 15.420 0.644

Item 3 0.917 19.921 0.841

Item 4 0.860 - 0.739

analysis of AVE, and the analysis of composite reliability. They suggested a standardized loading of 0.40 or higher for a sample size of more than 200, while Bagozzi and Yi (1988) recommended that factor loadings of each item ranging between 0.60 and 0.90 are satisfactory. In the SEM technique, using the AMOS program, Anderson, and Gerbing (1988) suggested that the accepted cut-off value for factor loadings is when t-values (which is reported as the critical ratio in AMOS output) are greater than ±1.96 or ±2.58 at 0.05 or 0.01 levels, respectively. In addition, the value of SMC or R2 is also inspected, which must be above the 0.3 cut-off value (Hair et al., 2010). The second method to determine the convergent validity is through the analysis of AVE. It is suggested that the satisfactory AVE values must exceed the 0.5 benchmark (Hair et al., 2010). While through the third method, Fornell and Larcker (1981) suggested that the values of composite reliability should exceed the 0.7 benchmark.

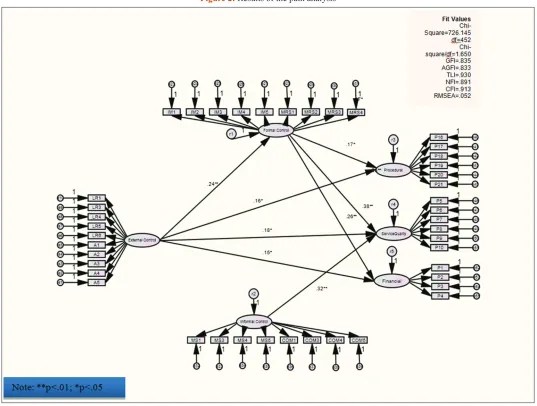

Table 2 presents the convergent validity results, which summarize the standardized loadings, critical ratio, SMC, composite reliability

and AVE of each item from the measurement model in Figure 2. As shown in Table 2, the value of the factor loadings for each item was above the cut-off value of 0.70 for the new measurement scales, as suggested by Hair et al. (2010), with all the critical ratios

being greater than ±1.96 at the 0.05 significance level (Anderson and Gerbing, 1988). Furthermore, the values for the SMC or

R2 were also above the suggested value of 0.30 (Hair et al., 2010). According to Hair et al. (2010), a composite reliability of 0.70 or above and AVE of more than 0.50 are considered to be acceptable.

As can be seen from Table 2, all the composite reliabilities were more than 0.90 and above the threshold values of 0.50 (Fornell and Larcker, 1981) and 0.60 (Bagozzi and Yi, 1988). Moreover, the AVE ranged from 0.62 to 0.77, which also exceeded the 0.50 rule of thumb (Bagozzi and Yi, 1988; Fornell and Larcker, 1981). Therefore, based on these results, it can be concluded that convergent validity has been established.

Discriminant validity refers to the degree to which measures of conceptually distinct constructs differ (Hair et al., 2010). It is established when the variance extracted from two constructs is greater than the square of the correlation between those two constructs (Fornell and Larcker, 1981). To identify the existence of discriminant validity, Fornell and Larcker (1981) suggested comparing the square root of AVE with the squared correlations between the latent constructs. If the square root of AVE value is

substantially greater than the squared correlations, then it indicates

that discriminant validity is attained (Table 3).

Investigation of the results in Table 3 shows that all the square roots of the AVE values were greater than the squared correlations, thereby indicating that the discriminant validity has been attained.

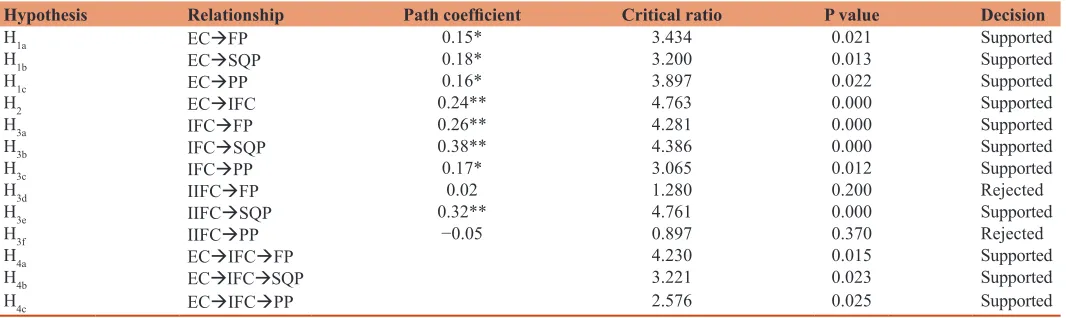

4.2. Hypotheses Testing Results

Figure 2 and Table 4 presents the results of 13 hypotheses generated in the study. Hypotheses 1a, 1b, and 1c examined the relationship between external control and financial performance, service quality performance, and procedural performance, respectively. The structural coefficient between external control and financial performance (H1a) was 0.16, while, between external control and service quality performance (H1b) it was 0.18. The structural coefficient of the path between external control and procedural performance (H1c) was 0.15. All three hypotheses (H1a,

H1b, and H1c) were supported at the 5% significant level, and thus, leading to the acceptance of these hypotheses. In addition, the relationship of external control and formal internal control (H2) was also examined and was found to be positively significant (P < 0.01) with the structural coefficient of the path being 0.24. Based on this result, hypothesis H2 was also supported.

The association between formal internal control and the performance of Malaysian local authorities - financial performance, service quality performance, and procedural performance - were tested in hypotheses 3a, 3b, and 3c, respectively. The results showed that two paths (H3a and H3b) were significant at the 0.01 level, while hypothesis 3c (H3c) was significant at the 0.05 level. Among these three relationships, formal internal control has the strongest effect

on service quality performance (path coefficient at 0.38). Thus, the results of the structural path established support for H3a, H3b, andH3c. Furthermore, a relationship between internal informal control and financial performance was also posited (H3d), as well as between internal informal control and service quality performance (H3e), and between internal informal control and procedural performance (H3f). Neither the structural path of H3d and H3f were significant as the critical ratios for the hypotheses were 1.280 and 0.897, respectively, which were below the cut-off value of 1.96 suggested by Hair et al. (2010). Accordingly, H3d and H3f were rejected. However, the relationship between internal informal control and service quality performance (H3e) was significantly supported at the 1% level, thus resulting in acceptance of the hypothesis.

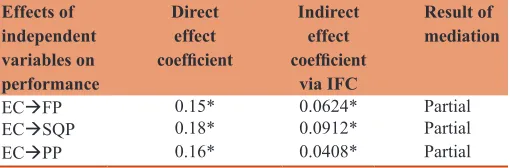

To test the mediation effects, Baron and Kenny’s (1986) principles of mediation were used. Table 5 presents the direct effects of external control and all three performance dimensions also significant (ECFP: 0.15, P < 0.05; ECSQP: 0.18, P < 0.05;

ECPP: 0.16, P < 0.05). Accordingly, these results conformed to the first step of Baron and Kenny in the mediation testing.

Looking at Table 4, the coefficients between external control on formal internal control was positively significant (ECIFC: 0.24, P < 0.01), thereby fitting the requirement of the second step of Baron and Kenny’s meditation testing procedure. Lastly, the third step of Baron and Kenny was investigated to identify

the existence of the mediation effects of formal internal control

in the relationship between external control and performance dimensions. Referring to Table 4, external control significantly influenced financial performance, service quality performance, and procedural performance via the internal formal control

(ECIFCFP: 0.0624, P < 0.05; ECIFCSQP: 0.0912,

P < 0.05; ECIFCPP: 0.0408, P < 0.05). In comparing the indirect effects and direct effects of external control and financial performance (0.0624 < 0.15), external control and service quality performance (0.0912 < 0.18), and external control and procedural performance (0.0408 < 0.16), it showed that although the indirect effects are still significant in the relationship, the coefficients were reduced. These results thus supported hypothesis 4a (H4a), Hypothesis 4b (H4b), and hypothesis 4c (H4c) - that formal internal control was the mediation variable in the relationship between external control and performance.

Table 3: Discriminant validity of constructs

Constructs (2) (3) (4) (5) (6) (7)

External control 0.787

Internal formal control 0.0012 0.819

Internal informal

control 0.0092 0.1246 0.806

Financial performance 0.0100 0.0196 0.0139 0.877

Service quality

performance 0.0035 0.0372 0.1129 0.0008 0.866

Procedural

performance 0.0035 0.0172 0.0169 0.0493 0.0029 0.806

Bold figures represent the square root values of AVE for each construct, while the other figures represent the squared correlations

Table 4: Hypotheses testing results

Hypothesis Relationship Path coefficient Critical ratio P value Decision

H1a ECFP 0.15* 3.434 0.021 Supported

H1b ECSQP 0.18* 3.200 0.013 Supported

H1c ECPP 0.16* 3.897 0.022 Supported

H2 ECIFC 0.24** 4.763 0.000 Supported

H3a IFCFP 0.26** 4.281 0.000 Supported

H3b IFCSQP 0.38** 4.386 0.000 Supported

H3c IFCPP 0.17* 3.065 0.012 Supported

H3d IIFCFP 0.02 1.280 0.200 Rejected

H3e IIFCSQP 0.32** 4.761 0.000 Supported

H3f IIFCPP −0.05 0.897 0.370 Rejected

H4a ECIFCFP 4.230 0.015 Supported

H4b ECIFCSQP 3.221 0.023 Supported

H4c ECIFCPP 2.576 0.025 Supported

5. CONCLUSION

This study contributes to the literature concerning the structural

linkage among external control, internal controls, and performance within Malaysian local authorities by developing and testing the hypothesized relationships using SEM analysis. This study also

tested the formal internal control as an intervening variable in

the relationship between external control and performance. The effects of the mediator variable on the performance were measured based on three different perspectives - financial performance, service quality performance, and procedural performance - which can provide new insight into the performance focus among the practitioners.

In addition, the results of this study also clarify the role of external

control regarding external auditing and laws and regulations to improve the internal control of local authorities. This can explain how the external control influences the formal internal control of the organization, and, in turn, influences the performance. Therefore, to enhance the performance of the local authorities, top management should monitor and supervise the existing control systems, and, at the same time, improve the current systems by taking into account the needs and desires of all related stakeholders.

In fact, the mechanisms of MCS as accountability attributes in Malaysian local authorities that need to comply in a responsible manner with internal and external criteria defined by stakeholders, ensuring the implementation of appropriate actions, and therefore, explaining how those actions can be delivered to the public citizens properly.

REFERENCES

Adeyemi, B., Adenugba, A. (2011), Corporate Governance in the Nigerian Financial Sector: The Efficacy of Internal Control and External Audit. Paper Presented at the Global Conference on Business and Finance Proceedings, San Jose, Costa Rica.

Agbejule, A., Jokipii, A. (2009), Strategy, control activities, monitoring and effectiveness. Managerial Auditing Journal, 24(6), 500-522. Anderson, J.C., Gerbing, D.W. (1988), Structural equation modeling

in practice: A review and recommended a two-step approach. Psychological Bulletin, 103(3), 411-423.

Anthony, R.N., Govindarajan, V. (2007), Management Control Systems. Boston: McGraw-Hill.

Bagozzi, R.P., Yi, Y. (1988), On the evaluation of structural equation models. Journal of the Academy of Marketing Science, 16(1), 74-97. Baron, R.M., Kenny, D.A. (1986), The moderator-mediator variable

distinction in social psychological research: Conceptual, strategic, and statistical considerations. Journal of Personality and Social Psychology, 51(6), 1173-1182.

Barret, P. (1996), Some thoughts on the roles, responsibilities and future scope of auditors-general. Australian Journal of Public Administration, 55(4), 137-146.

Batac, J., Carassus, D. (2009), Interactions between control and organizational learning in the case of a municipality. A comparative study with Kloot (1997). Management Accounting Research, 20, 102-116.

Berahim, N., Jaafar, M.N., Zainudin, A.Z. (2015), An audit remarks on Malaysian local authorities immovable asset management. Journal of Management Research, 7(2), 218-228.

Bollen, K.A. (1989), Structural Equation with Latent Variables. New York: Wiley.

Boyne, G. (2000), Developments: External Regulation and Best Value in Local Government. Public Money and Management, 20(3), pp. 7-12. DOI:10.1111/1467-9302.00217.

Chan, Y.C.L. (2004), Performance measurement and adoption of balanced scorecards: A survey of municipal governments in the USA and Canada. The International Journal of Public Sector Management, 17(3), 204-221.

Chenhall, R.H. (2003), Management control systems design within its organizational context: Findings from contingency-based research and directions for the future. Accounting, Organizations, and Society, 28, 127-168.

Chenhall, R.H. (2007), Theorizing contingencies in management control systems research. Handbook of Management Accounting Research, 1, 163-205.

Chenhall, R.H., Euske, K.J. (2007), The role of management control systems in planned organizational change: An analysis of two organizations. Accounting, Organizations, and Society, 32, 601-637. Chenhall, R.H., Kallunki, J.P., Silvola, H. (2011), Exploring the

relationships between strategy, innovation, and management control systems: The roles of social networking, innovative organic culture, and formal controls. Journal of Management Accounting Research, 23, 99-128.

Coombs, H.M., Edwards, J.R. (1990), The evolution of the district audit. Financial Accountability and Management, 6(3), 153-176. Cuguero-Escofet, N., Rosanas, J.M. (2013), The just design and use of

management control systems as requirements for goal congruence. Management Accounting Research, 24(1), 23-40.

Davila, T. (2000), An empirical study on the drivers of management control systems’ design in new product development. Accounting, Organizations, and Society, 25, 383-409.

Durden, C. (2008), Towards a socially responsible management control system. Accounting, Auditing and Accountability Journal, 21(5), 671-694.

Fadzil, F.H., Haron, H., Jantan, M. (2005), Internal auditing practices and internal control system. Managerial Auditing Journal, 20(8), 844-866. Fornell, C., Larcker, D.F. (1981), Evaluating structural equation models

with unobservable variables and measurement error. Journal of Marketing Research, 18, 39-50.

Gottardo, P., Moisello, A.M. (2011), The fragmentation of entrepreneurial function and the role of external control on management behavior. iBusiness, 3(4), 339-344.

Greatbanks, R., Tapp, D. (2007), The impact of balanced scorecards in a public sector environment. Empirical evidence from Dunedin city council, New Zealand. International Journal of Operations and Production Management, 27(8), 846-873.

Greiling, D. (2005), Performance measurement in the public sector: The German experience. International Journal of Productivity and Performance Management, 54(7), 551-567.

Greiling, D. (2006), Performance measurement: A remedy for increasing Table 5: Analysis of direct and indirect effects of the

independent variables on performance

Effects of independent variables on performance

Direct effect

coefficient

Indirect effect

coefficient

via IFC

Result of mediation

ECFP 0.15* 0.0624* Partial

ECSQP 0.18* 0.0912* Partial

ECPP 0.16* 0.0408* Partial

the efficiency of public services? International Journal of Productivity and Performance Management, 55(6), 448-465.

Grubnic, S., Woods, M. (2009), Hierarchical control and performance regimes in local government. International Journal of Public Sector Management, 22(5), 445-455.

Hair, J.F., Black, W.C., Babin, B.J., Anderson, R.E. (2010), Multivariate Data Analysis. A Global Perspective. New Jersey: Pearson Prentice Hall.

Heinrich, C.J. (2002), Outcomes-based performance management in the public sector: Implications for government accountability and effectiveness. Public Administration Review, 62(6), 712-725. Herath, S.K. (2007), A framework for management control research.

Journal of Management Development, 26(9), 895-915.

Ho, A.T.K. (2011), PBB in American local governments: It is more than a management tool. Public Administration Review, 71(3), 391-401. Horngren, C.T., Datar, S.M., Foster, G. (2011), Cost Accounting:

A Managerial Emphasis. New Jersey: Prentice Hall.

Ibrahim, F.W., Karim, M.Z.A. (2004), Efficiency of local governments in Malaysia and its correlates. International Journal of Management Studies, 11(1), 57-70.

Ibrahim, M.A., Ali, E.I.I., Ismail, S.S.S., Bidin, Z. (2004), Qualified audit reports of local authorities in the northern states of Malaysia. Malaysian Management Journal, 8(2), 77-86.

Ilias, N. (2016), Management Control Systems and Performance: Evidence from Malaysian Local Authorities. Unpublished Doctoral Dissertation. Malaysia: Universiti Teknologi MARA, Selangor. Ittner, C.D., Larcker, D.F. (1997), Quality strategy, strategic control

systems, and organizational performance. Accounting, Organizations and Society, 22(3/4), 293-314.

Ittner, C.D., Larcker, D.F. (2003), Coming up short on non-financial performance measurement. Harvard Business Review, 81, 88-95. Jokipii, A. (2010), Determinants and consequences of internal control in

firms: A theory-based contingency analysis. Journal of Management and Governance, 14, 115-144.

Khalid, S.A. (2010), Improving the service delivery: A case study of a local authority in Malaysia. Global Business Review, 11(1), 65-77. Kloot, L. (1999), Performance measurement and accountability in

Victorian local government. The International Journal of Public Sector Management, 12(7), 565-583.

Langfield-Smith, K. (1997), Management control system and strategy: A critical review. Accounting, Organizations and Society, 22(2), 207-232.

Lebas, M., Weigenstein, J. (1986), Management control: The roles of rules, markets and culture. Journal of Management Studies, 23(3), 259-272. Local Government Act 1976 (Act 171) & Subsidiary Legislation, (2010).

International Law Book Services. 15 June. ISBN: 9789678918268. Macintosh, N.B., Daft, R.L. (1987), Management control systems and

departmental interdependencies: An empirical study. Accounting, Organizations and Society, 12(1), 49-61.

Melkers, J., Willoughby, K. (2005), Models of performance-measurement use in local governments: Understanding budgeting, communication, and lasting effects. Public Administration Review, 65(2), 180-190. Merchant, K. (1982), The control function of management. Sloan

Management Review, 23, 43-55.

Midwinter, A. (1994), Developing performance indicators for local government: The Scottish experience. Public Money and Management, 14(2), 37-43.

Mimba, N.P.S.H., Helden, G.J.V., Tillema, S. (2013), The design and use of performance information in Indonesian local governments under diverging stakeholder pressures. Public Administration and Development, 33, 15-28.

Muhammad, Z., Masron, T., Abdul Majid, A. (2015), Local Government service efficiency: Public participation matters. International Journal of Social Science and Humanity, 5(10), 827-831.

Otley, D. (1999), Performance management: A framework for management control systems research. Management Accounting Research, 10, 363-382.

Otley, D.T. (1980), The contingency theory of management accounting: Achievement and prognosis. Accounting, Organizations and Society, 5(4), 413-428.

Otley, D.T., Berry, A. (1994), Case study research in management accounting and control. Management Accounting Research, 5, 45-65. Ouchi, W.G. (1977), The relationship between organizational structure

and organizational control. Administrative Science Quarterly, 22(1), 95-113.

Rashid, N. (1999), Managing Performance in Local Government. London: Kogan Page Limited.

Rosanas, J.M., Velilla, M. (2005), The ethics of management control systems: Developing technical and moral values. Journal of Business Ethics, 57, 83-96.

Sekaran, U., Bougie, R. (2011), Research Methods for Business: A Skill Building Approach, United Kingdom: John Wiley & Sons Ltd. Simons, R. (1987), Accounting control systems and business strategy:

An empirical analysis. Accounting, Organizations, and Society, 12, 357-374.

Simons, R. (1990), The role of management control systems in creating competitive advantage: New perspectives. Accounting, Organizations and Society, 15(1/2), 127-143.

Simons, R. (1991), Strategic orientation and top management attention to control systems. Strategic Management Journal, 12, 49-62. Steventon, A., Jackson, T.W., Hepworth, M., Curtis, S., Everitt, C. (2012),

Exploring and modeling elements of information management that contribute towards making positive impacts: An outcome-based approach for senior managers in a local government setting. International Journal of Information Management, 32(2), 158-163. Suyono, E., Hariyanto, E. (2012), Relationship between internal

control, internal audit, and organization commitment with good governance: Indonesian case. China-USA Business Review, 11(9), 1237-1245.

Torres, L., Pina, V., Marti, C. (2012), Using non-mandatory performance measures in local governments. Baltic Journal of Management, 7(4), 416-428.

Triantafylli, A.A., Ballas, A.A. (2010), Management control systems and performance: Evidence from the Greek shipping industry. Maritime Policy and Management, 37(6), 625-660.

Tsamenyi, M., Sahadev, S., Qiao, Z.S. (2011), The relationship between business strategy, management control systems and performance: Evidence from China. Advances in Accounting, 27(1), 193-203. Verbeeten, F.H.M. (2008), Performance management practices in public

sector organization. Impact on performance. Accounting, Auditing and Accountability Journal, 21(3), 427-454.