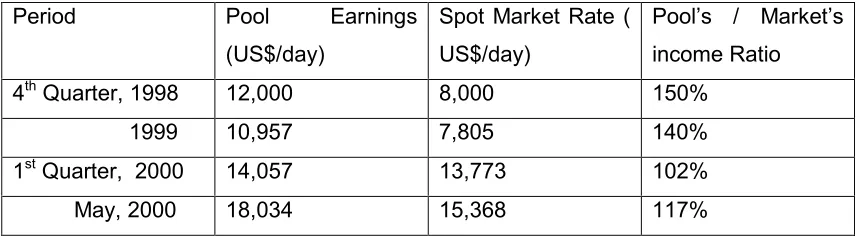

Privatisation of the shipping industry in Vietnam : the benefit, problems and proposals

Full text

Figure

Related documents

The intensity and frequency of stutter peaks in the n-8 and n+4 positions were not reported in the user manual for standard amplification with Identifiler [13]; however, the n+4

Figure 3: Light microscopic photomicrograph of left testis from adult rats in high dose ( Persea americana ) showing abnormal testicular architecture with focal

Fig 1: Showing the effects of alcohol on the level of gastric acid secretion in experimental rats expressed as Mean±SEM Ω : Omega-3, ALC : Alcohol, (a) Significant increase

Evaluation of Antidiabetic Activity of Polyherbal Formulation in Streptozotocin- Induced Diabetic Rats.. Arijit Chaudhuri,

Four genes ( oculocutaneous albinism II ( OCA2 ) , tyrosinase-related protein 1 ( TYRP1 ) , dopachrome tautomerase ( DCT ), and KIT ligand ( KITLG )) implicated in human

found in local anesthetics can be replaced by amide nitrogen, having chloro methyl group attached to the carbonyl carbon of amide.. In this type of arrangement,

FACTORS AFFECTING FOOD INTAKE: COMMITTEE ON

Karmaka et al evaluated neuropharmacological activity like analgesic, Locomotor, Anticonvulsant property and muscle relaxant effect of Curcuma caesia rhizome in