Please cite this article in press as: Cullen, J., et al., Reverse logistics in the UK retail sector: A case ContentslistsavailableatSciVerseScienceDirect

Management

Accounting

Research

j our na l h o me p a g e:ww w . e l s e v i e r . c o m / l o c a t e / m a r

Reverse

logistics

in

the

UK

retail

sector:

A

case

study

of

the

role

of

management

accounting

in

driving

organisational

change

John

Cullen

a,∗,

Mathew

Tsamenyi

b,

Mike

Bernon

c,

Jonathan

Gorst

daManagementSchool,UniversityofSheffield,9MappinStreet,SheffieldS14DT,UnitedKingdom

bBirminghamBusinessSchool,UniversityofBirmingham,UniversityHouse,EdgbastonParkRoad,BirminghamB152TY,UnitedKingdom cCentreforLogisticsandSupplyChainManagement,CranfieldSchoolofManagement,BedfordshireMK430AL,UnitedKingdom dSheffieldBusinessSchool,SheffieldHallamUniversity,CityCampus,HowardStreet,SheffieldS11WB,UnitedKingdom

a

r

t

i

c

l

e

i

n

f

o

Keywords:Managementaccountingpractice Reverselogistics

Interventionistresearch Manageriallyrelevantsolutions Strategicandcommercialadvantage Change

a

b

s

t

r

a

c

t

Thispaperillustrateshowinterventionistresearchcanbehelpfulinprovidingmanagerially relevantsolutionsandfurthersthedebateabouttherelationshipbetweensocialscience researchandpractice.Throughthisuseofinterventionistmethods,thepapercontributes toknowledgebyillustratingthewayinwhichmanagementaccountingwasusedalongside othermanagerialdisciplinesinaUKretailorganisationtopromotechangeandinfluence outcomes.Specifically,thepaperfocusesonchangestothereverselogisticsprocessesofthe organisationandtheimportantrolethatmanagementaccountingplayed.Italsoillustrates theuseofmanagementaccountinginthepursuitofstrategicandcommercialadvantage. Asresearchers,ourworkwasgroundedinactionratherthanbeingjustobservers.

© 2013 Elsevier Ltd. All rights reserved.

1. Introduction

Thispaper explorestheengagementofmanagement accountinginorganisationalchange(AhrensandChapman,

2007;BurnsandScapens,2000)andtheroleof

account-inginthepursuitofstrategicandcommercialadvantage

(AhrensandChapman,2007).InlinewithJørgensenand

Messner’s (2010) call to examine accounting in terms

of howit relatesto,and intersectswith, othertypes of activities,ourpaperfocusesontherelationshipwiththe managementofreverselogisticsprocesses.Reverse logis-ticsconcernsthemanagementofaproductorserviceafter thepointofsaleandparticularlyfocusesonthe manage-mentofreturns.Weexplorethisthroughacasestudyofone organisation,Halfordsplc,withintheUKretailsector. Hal-fordsplcisaUKbasedcompanythatisintheFTSE250and hadamarketcapitalisationofapproximately

£

894million atthetimeoftheempiricalresearch.∗ Correspondingauthor.Tel.:+4401142223429; fax:+4401142223348.

E-mailaddress:john.cullen@sheffield.ac.uk(J.Cullen).

Intermsoftheliterature,AhrensandChapman(2007)

suggestthat,whilstcontemporarydiscussionof manage-mentcontrol(e.g.KaplanandNorton,1996;Simons,1995) frequently seeks to address strategic concerns, the lit-eraturedoesnot tendtoelaborateon specificactivities throughwhich these concernsmaybe addressed. Simi-larly,JørgensenandMessner(2010)callformoreresearch ontherelationshipbetweenaccountingandstrategising. This paper seeks to provide an illustration of manage-ment accounting practiceand its interconnectionswith otherorganisationalpracticesin thepursuit ofstrategic andcommercialadvantage.Engagingwiththis manage-ment accounting practice theme, Malmi (2010) reflects onapaperhewrotewithcolleagues(Malmietal.,2004) onthe application of quality costing. He highlights the factthatthe2004paperhasfewcitationsand thatthis mayreflecttheviewthat“ithasnotbeenacceptedthat researchers can innovate something and lead the way forpractitioners”(p. 2).Taking a management account-ingpracticeperspective,ourpaperseekstodisprovethis assumptionandarguestheimportanceofsuchresearch in terms of both theoretical contribution and practical relevance.

1044-5005/$–seefrontmatter© 2013 Elsevier Ltd. All rights reserved.

Please cite this article in press as: Cullen, J., et al., Reverse logistics in the UK retail sector: A case In methodological terms, we use interventionist

researchwhich hasbeenthesubjectof somedebatein recentmanagementaccountingliterature(Baldvinsdottir etal.,2010).Thepolyphonicdebate(Ahrensetal.,2008) engagedanumberofacademicsintryingtoidentifyways forwardwithregardtothefutureofinterpretive account-ingresearch.Ofrelevancetothispaperisthedebateabout thenatureofengagementwithpractitioners.Granlund,in

Ahrenset al.(2008),suggeststhat thereis spacein the

interpretiveaccountingresearchagendafor intervention-istresearchapproaches. In thesamearticle, Mennicken arguesthatpractice shouldinformourresearchagenda whilstMikessuggeststhatagrowingnumberof practition-ersareshowinganinterestinthefindingsofinterpretive accounting research.Chua (2011) reflects that research shouldmakestronganddeepconnectionswithpractice. Further,Parker(2008) insists that weshould reflect on whatcouldorshouldbeandnottoworrytoomuchabout beinglabelledundertheunfashionablebrandof norma-tivism.Ourcontentionhereisthatbyusinginterventionist researchmethods,wewereabletoengagepractitioners inaresearchprocessthatwasofinteresttothem.Inthis paper,weengagewithboththeoryandcraftknowledgeof accountants(Scapens,2008)andothermanagersengaged inthereverselogisticsprocesses.Weseethisengagement

likeWoutersandRoijmans(2011)asajourneyofjoint

dis-coverybetweenourselvesasacademicsandpractitioners engagedwithinthecaseorganisation.Whilstthisjourney ofdiscoveryneedstoincorporatea“betterunderstanding oftheprocessesbywhichmanagementaccounting knowl-edgeisproduced,disseminatedandoperationalised”(Seal, 2010,p.2),wewouldargue,incontrasttoWoutersand

Roijmans(2011),thatourworktakesknowledgefurther

forwardbyprovidingsomemoreconvincingevidenceof theimpactofthisjointdiscovery.

In summary, theresearchpuzzle in this paperis an explorationofthewayinwhichmanagementaccounting becameembeddedinthereverselogisticsprocessesat Hal-fordsand,inordertoengagewiththispuzzle,weaddress thefollowingtworesearchquestions:

(1)Howismanagementaccountingengagedinchanging thereverselogisticsprocessesinthecasestudy com-pany?

(2)What is the role of interventionist research in contributing to our understanding of management accountingpractice?

Thepaperstartswithabriefreviewofsomerelevant literatureandthenintroducestheconceptofreverse logis-tics.Thisisfollowedbyanoverviewoftheresearchmethod adoptedandanexplanationoftheinterventionistnature oftheresearch.TheHalfordscasestudyisthenintroduced andthisisfollowedbyadiscussionrelatedtotheresearch questions.Finally,concludingthoughtsarepresented.

2. Briefliteratureoverview

Jørgensen and Messner (2010) have called for more

research on the relationship between accounting and strategising. Strategising reflects the activities that are

undertaken inpursuit ofsomesharedstrategicideasor objectives.JørgensenandMessner(2010)detailtheway in which management accounting information shaped continuous strategising efforts by providing a general understandingoftheimportanceofprofitabilityaswellas throughspecificrulesthatwereenactedatcriticalpoints intime.Importantly,JørgensenandMessner(2010) con-clude that“the influenceof accountinginformation can onlybeunderstoodwhenconsideredininteractionwith othertypesofaccountsorrationalities,suchasstrategic objectives” (p. 202). The emphasis hereis on the posi-tionof accountingalongsideotheractivitiesrather than thepositionofaccountinginisolationtherebysupporting theargumentthataccountingdoesnotoperateina

vac-uum(Chua,1986;Alcouffeetal.,2008).Inourresearch,

engagementbetweenresearchersfromdifferentacademic disciplineswashelpfulinfacilitatingamorefruitfulroute tonewideas(Chua,2011)andenabledawiderperspective tobetakenonthepracticestakingplaceandtheireventual outcomes.

In consideringtherelationshipsbetweenlogistics(in theirparticularcase,forwardlogistics)andmanagement accounting,WoutersandRoijmans(2011)engagedin lon-gitudinalactionresearchinordertoexploretheprocessby whichenablingperformancemeasurementsystems(PMS) werecreatedatanoperationallevelinthetransportation departmentofamediumsizedcompanyinthebeverage manufacturing industry. Enabling PMS are described as informationwhichisperceivedbyemployeesas facilitat-ingtheirresponsibilitiesratherthanprimarilybeingused forcontrolpurposes.Suchsystemsareoftendiverseand informalalthoughtheyarenotcompletelydetachedfrom formalsystems. Knowledgeexchange occurredbetween the researchers, accountants and operational managers engaged in the organisation. The authors argued that, whilst there has been supportfor user participation in developing accountinginformation, therehasbeenlittle in the literature about how users are engaged in the experimentation process (i.e. experimenting with new informationsystems)inordertocreateenablingPMS.Akey componentofenablingPMSisanunderstandingofwhat action managers taketoinfluence costsand how these actionscanbesupportedbyaccountingandothertypesof information.Centraltothisdebateisthewayinwhichthe partiesinvolvedinteractinordertocreateenablingPMS. WhatisnotevidentintheworkofWoutersandRoijmans

(2011)istheorganisationaloutcomesresultingfromthese

enablingPMS.Whilsttheirarticledescribesindetailthe processesofquestioninganddevelopingnewaccounting information through interdisciplinarydialogue,it is rel-ativelysilentontheresultingoutcomes.Therearesome brief comments about thefact that the system was in useoneyearaftertheresearchperiodandthatthenew systemshadhelpedtomonitorandcontroltransportation costsaswellasbetterinformingthecompanyaboutthe factorswhichdetermineactualcosts.Thereisalsomention of some efficiency impacts as well as some limitations in the new systems around unintended consequences of changes in packaging design. However, despite this better understandingof theprocess of interdisciplinary relationshipsinthislogisticscontextandthedetailofnew

Please cite this article in press as: Cullen, J., et al., Reverse logistics in the UK retail sector: A case accountinginformation,therewaslittleevidenceprovided

withregardtooutcomesarisingoutofthenewenabling PMS.Wewouldarguethatthisisaweaknessintermsof thepresentedwork.IndeedWoutersandRoijmans(2011)

themselvesraise theprospectat theend oftheirpaper aboutfutureresearchworkonthepossibleconsequences in terms of performance. Therefore, as well as looking atthepracticesandactivitiesbywhichinteractionstake placeamongstinter-disciplinarymanagers,itisimportant toexploreoutcomesarisingfromthesepracticeswithin thecontextofdevelopingstrategicobjectives.

The linkbetween managerialaction, strategic objec-tivesandorganisationalperformancehasbeendiscussedin themanagerialistliterature(PetersandWaterman,1982;

Reed, 2007; O’Reilly and Reed, 2010). The

managerial-istdoctrinewhichinformsouranalysis,presupposesthe importance andefficacy ofmanagement as a systemof organisational co-ordination (O’Reilly and Reed, 2010). Thefundamentalpremiseofmanagerialismis“the dom-inanceofmanagementpracticesandideas”(Kreutzerand

Jäger,2011,p.635)withemphasisonrationalityin

orga-nisationalprocesses.Managerialismassumesthatallthe activitiesthattakeplaceinanorganisationcanbe man-agedaccordingtorationalstructuresandproceduresinline withthegoalsofseniormanagementandthoseinauthority

(WallaceandPocklington,2002;MaierandMeyer,2011).

Ineffect,managerialismfocusesontheeconomic conse-quencesoroutcomesofmanagerialdecisions(Henriand

Journeault,2010),whichfitswithourinterestinexploring

theoutcomeofchangesinreverselogisticsprocessesand managementaccounting.

Mueller and Carter (2007) discuss the diffusions of

innovationssuchas“activitybasedcosting,totalquality management,businessprocessre-engineering,enterprise resourceplanningandknowledgemanagement”asdriven bymanagerialism.Theauthorsarguethat“managerialism embracesnotions of‘excellence’,‘customersatisfaction’, ‘leadership’and‘addingvalue”’(p.182).Webelievethat recognisingtheexistenceofthismanagerialistperspective hasenabledustoappreciateandunderstandhow manage-ment accounting and management accountants became implicatedintheday-to-daymanagementofthereverse logistics.Theemphasis in theorganisationwasonhow management accounting can contribute to the reverse logisticsprocessthroughqualitycostingandperformance measurementinordertoimprovethebottom-line.Whilst therehavebeennumerouscritiquesofmanagerialist per-spectives in the literature (for example, Alvesson and

Sveningsson,2011),itisalsorecognisedthatforlarge

num-bers of peopleworking inorganisations, managerialism or newmanagerialismis predominant inorganisational life.AlvessonandSveningsson(2011)indeedfoundthatin thefirmstudied,“strengtheningofmanagementandthe positionofmanagersdoingleadership(andotherthings) is the solution suggested and embraced by most peo-ple in thefirm studied” (p. 359). Therefore, we would arguethatitisimportanttoexplorewaysinwhichusing interventionistresearchinmanagementaccounting prac-tices,incollaborationwithotherdisciplinaryplayers,can leadtomanageriallyrelevantsolutionstoissuesfacingan organisation.

Inthenextsection,wegoontointroducetheconceptof reverselogisticsinordertoensurethatthereader under-standsthecontextinwhichweareexploringtheresearch instudyingmanagementaccountingpractices.

3. Reverselogisticscontext

Reverse logistics is currently generating interest acrossa number of academicdisciplines (Prahinskiand

Kocabasoglu,2006)andisgraduallybecomingrecognised

as an integral discipline within supply chain manage-ment. Pokharel and Mutha (2009) suggest that reverse logistics involves a paradigm shift in terms of product froma“cradle-to-grave”approachtoa“cradle-to-cradle” approach.Reverselogisticshasbeendescribedasaprocess thatgoesthewrongwaydownaone-waystreetas sup-plychainsareoptimisedaroundforwardlogistics(Lambert

andStock,1981).Liberalreturnspolicies,buyer’sremorse

and productrecalls areamong thereasons thatlead to productsbeingreturnedbackupthroughthesupplychain

(Rogersetal.,2002).Thescopeofreverselogistics

through-outthe1980swasbasicallylimitedtothemovementof material against the primary flow. Through time how-ever,moresophisticateddefinitionsbegantoemergeand

RogersandTibben-Lembke(1998)definedreverselogistics

as“theprocessofplanning,implementingandcontrolling theefficient,costeffectiveflowofrawmaterials,in-process inventory,finishedgoodsandrelatedinformationfromthe pointofconsumptiontothepointoforiginforthepurpose ofrecapturingvalue,orproperdisposal”(p.2).However, thisdefinitionislimitedsincemanyproductsarereturned toapointofrecoveryandnottheirorigin(De Britoand

Dekker,2002).Inrecentyears,anumberofdefinitionshave

emergedandthispaperreferstoreverselogistics“asall activityassociatedwithaproduct/serviceafterthepointof sale,theultimategoaltooptimiseormakemoreefficient aftermarketactivity,thussavingmoneyandenvironmental resources”(ReverseLogisticsAssociation,2009).

Thescale oftheproblemcanbesignificantwiththe retailsectorinparticularbeingthemostaffected. Over-allreturnratesforUKhighstreetretailingarebetween5%

and6%(Raimer,1997).However,differencesbetween

sec-torsvarydramaticallywithmailordercompanieshaving levelsofupto60% forladies apparel(Wheatley,2002). ThetotalvalueofretailreturnsintheUKhasbeen esti-mated at

£

5.75bn (Bernon and Cullen, 2004) whilst a surveyofUScataloguecompaniesreportedtheoperational coststobe10%oftotallogisticsexpenditure(Daughertyet al., 2001). Blanchard (2007) estimated that product

returns cost retailers and manufacturers in the United States around$100bn.It is ourexperiencethat returns arenotmanagedwiththesamesophisticationasforward logistics and hence the total costs for all the activities involved,suchas,writeoff’s,managementtimeand inven-torymanagement,arerarelyknownorreported.

Earlier literature provides support for committing management resources to thedevelopment and imple-mentationof reverse logistics processes. Understanding thewayinwhichtheseresourcescanbeutilisedsuggests potential support from management accounting tech-niquessuchasactivitybasedcosting(GoldsbyandCloss,

Please cite this article in press as: Cullen, J., et al., Reverse logistics in the UK retail sector: A case

2000)andqualitycosting(DaleandWan,2002).Thelatter couldprovideabetterunderstandingoftherelationship betweenplanninganddesignfeaturesandsubsequent fail-uresinthesystem.Technologyhasaparttoplayinthe reverselogisticsprocess (Bernonand Cullen, 2007)and therehavebeenseveralpaperslookingattheroleof enter-prise resource planning (ERP) systems in management accountingchange(ScapensandJazayeri,2003;Dechow

andMouritsen,2005;SpathisandAnaniadis,2005).Caglio

(2003)observedthattheadoptionofanERPsystemhas

implicationsforthedefinitionoftheexpertiseandroles ofaccountantswithinorganisations.Nevertheless,whilst

DechowandMouritsen(2005)haveobservedhow

man-agementcontrols,technologyandcontextareinterwoven making it impossible to study one without the others, there hasbeenlimited mentionof therole of manage-mentaccountinginthereverselogisticsprocess(Bernon

andCullen,2007;Bernonetal.,2011).Theaimofthispaper

istocontributetoourunderstandingofhowmanagement accountingisembeddedinthereverselogisticsprocess. Inparticular,weexplorethecross-disciplinaryaspectof accountantsandreverselogisticsmanagersengagedinthis activity.

4. Researchmethod

In order to engage with practitioners and to fully understand the role of management accounting in the reverse logistics process, we adopted interventionist research methods (Labro and Tuomela, 2003; Wouters

andWilderom,2008;Dumay,2010;WestinandRoberts,

2010;Jönsson,2010;SuomalaandLyly-Yrjänäinen,2009;

Suomalaetal.,2010;Baard,2010;TerBogtandvanHelden,

2011).Thepaperisdrawnfromalargemulti-disciplinary researchproject focusing onreverse logisticsprocesses thatranforaround21monthsfromSeptember2005to May2007(mainlyfundedbytheDepartmentforTransport [DfT] with some additional funding from the Char-teredInstituteofManagementAccountants[CIMA]).The researcherscamefromthedifferentacademicdisciplines of accounting, supply chain management and logistics management.

Around40companieswereengagedintheprojectand 13 workshops/industrialforums were held. Each work-shop/industrial forum was attended by on average 20 managers and lasted around 5h. The participants rep-resenteda rangeof retailsectors includinggrocery and supermarkets,generalmerchandisers,homeandpersonal care,homefurnishing,catalogueretailing,car entertain-mentandaccessories,electronictoys,mobilephonesand cosmetics. In additiontoretailers, specialist third party logisticsprovidersandmanufacturersintheretailsupply chainwerealsopresent.Wehavealsoundertakenintensive casestudiesaspartoftheprojectandthispaperisfocussed aroundHalfords,whowereengagedintheprojectfromthe beginning.

EdenandHuxham(1996,p.75)defineinterventionist

(action)researchaswherethereis“aninvolvementwith membersofanorganisationoveramatterwhichisof gen-uineconcerntothem”.Interventionistresearchhasbeen recommendedfor thestudyof managementaccounting

practice(Kaplan,1998;AhrensandChapman,2006)and

Jönsson and Lukka (2007) suggest that interventionist

research provides opportunities for new insights given thattheresearcherwantstoachievesolutionsthatwork inthefieldandcomebackwithevidenceoftheoretical sig-nificance.Inessence,undertakinginterventionistresearch allowedustoengageinachangeprocesswhichresulted inaconstructionofnewreality(JönssonandLukka,2007) focussedaroundthemanagementofthereverselogistics process. Therefore, in our case study, interventionist research was perceived as an appropriate approach to examinetheroleofmanagementaccountinginthereverse logistics process. The engagement with practitioners provideduswithrichinsight(Whyte,1990)ofthereverse logisticsprocessasindicatedbythefollowingquotefrom ChrisHall(Halfords):

The reverse logistics project had a major influence ontheintroductionofnewreverselogisticsprocesses within Halfords. It helped to increase awareness of theissuesandthelargepotentialforimprovementto both bottom line performance and customer service throughtheintroductionof improvedprocesses.The identificationofnewtoolsandthesupportprovidedby discussionsattheworkshopsplayedavitalpartinthe implementationofchangeatHalfords(ChrisHall,Head ofQuality&CostReduction,Halfords)

The aim of the overall reverse logistics projectwas to develop a set of diagnostic tools to assist organisa-tionsimplementeffectivereverselogisticsoperations.To this end, this case studywasundertakenas partofthe wider project and it was completed with the full co-operationof Halfords.The data for this case studywas collectedthroughHalfordsparticipationinthestructured workshops/industrialforums.Thesewereorganised and facilitatedbytheresearchteamandnotesofthese work-shopswerecollected,collatedandusedduringthewriting of this case study. Two membersof theresearch team hadsignificantresearchexperienceinreverselogisticsand theyfacilitatedtheworkshops/industrialforums.Alldata wasrecordedbya thirdresearcher throughnote-taking and thesenotes werewrittenupimmediatelyfollowing themeetings.Inaddition,datarecordedonA1flipcharts andotherdocumentswerealsocollated.Where discuss-ionswerefacilitated throughworkingideasupon white boards, these were photographed. Companies involved in the workshops/industrialforumsmade presentations andHalfordspersonnelmadepresentationsatthe work-shops/industrialforums onfourseparateoccasions.The data was analysed using themes and codes as part of the development of the reverse logistics toolkit which wasthemainpractitioneroutputfromthewiderresearch project. The toolkit was developed around nine key themes(costandperformancemeasurement,avoidanceof productreturns,processmanagement,physicalnetwork, inventorymanagement,informationandcommunication technology,materialhandlingcontainers,sustainable dis-tributionandcompliancewithlegislation).Withinthenine key themes,there were207self-assessmentstatements which were derived fromthe dataarising out thedata collection.

Please cite this article in press as: Cullen, J., et al., Reverse logistics in the UK retail sector: A case Inadditiontoengagementintheworkshops,visitsby

the researchteam weremade onfouroccasions tothe Halfords HeadOffice to discussin detail thework that hasbeencarriedoutontheHalfordsreverselogistics pro-cesses.Eachofthesevisitslastedforonedayandinvolved formal and informal meetings as well as informal dis-cussionsoverlunch.AsindicatedinthequotefromChris Hall,thesewereinteractivediscussionsthatalsoinfluenced thechangestakingplaceatHalfords.Theresearch ques-tionsbeingaddressedinthispaperareanexplorationand engagementin theevolvingchangesbeingmadetothe managementofreverselogisticsprocessesatHalfordsand theroleofmanagementaccountingchangeinfacilitating andinitiatingsuchchanges.Wewouldarguethattherich insightsfromourinterventionistresearchapproachmeet the two requirementsfor validity in interpretive man-agement accounting research, namely authenticity and plausibility(LukkaandModell,2010).

Site visits,documentationandinterviews(both indi-vidual and group interviews) at Halfords Head Office and National Distribution Centre have been used to develop the case material and also to make presen-tations at the workshops. The documentation that we lookedatincludedaccountingreports,logisticsand ware-housereports,reportsonreturns,lostintransitreports, definitive guides on faulty goods processes, scripts for stores staffand processflowcharts.Thechangesin both managementaccountingsystemsandreverselogistics pro-cesseshavebeenongoingthroughouttheresearchprocess andoutcomesfromtheresearchprocesshaveinfluenced changeswithintheorganisation.Interviewswereheldwith employeesatdifferentlevelswithinaccounting,quality, supplychainandlogistics.Thecontinuousdialogue main-tainedthroughouttheresearchprojectmeantthatthecase materialwasconstantlyverifiedandcheckedforaccuracy

(AhrensandChapman,2006).Aroundoneyearafter

com-pletingtheinterventionistresearch,theresearchersvisited sixstores(March,2008)tointerviewstoresmanagersand other stores employees.Each of the stores visits lasted between3and4h.Thesevisitswereundertakeninorderto getadifferentperspective(triangulation)oftheimpactof thechangesinmanagementaccountingandreverse logis-ticsprocessesthathadtakenplaceduringtheperiodofthe project.Thesixstoreswereintwogeographicalregions, representingarangeofstoreformatsandmanagerswith differentlevelsofexperience.Aswellasinterviewingstaff, observationsofnoticeboardsinstaffrestroomsand prac-ticeswithinthestoreswereundertaken.Throughoutthe researchprocess,thedatawasanalysedusingthethemes and codes that we had developed as partof thewider researchproject.Aftervisitingthestores,wehadafurther meetingwithChrisHallandPeterCobden(Returns Man-ager)toreflectonourobservationsatthestoresandthis mayhaveinfluencedfurtherchangesatHalfordsbutthisis outsidethetimelinerepresentedbythispaper.

5. Case

Asalreadymentioned,HalfordsisaUKbasedcompany thatisintheFTSE250andhadamarketcapitalisationof approximately

£

894millionatthetime oftheempiricalresearch.Itaimstodelivertravelandleisuresolutionsto peopleonthemovethroughmarketleadingknowledge, choiceandservice.HalfordsistheUK’sleadingretailer,on thebasisofturnover,ineachofthekeyproductmarketsin whichitoperates,thesebeing(Halfordswebsite): •carmaintenance (includingcar parts,servicing

consu-mables(such as oil),workshop tools and body repair equipment);

•car enhancement(including in-carentertainment sys-tems,cleaningproducts,accessories,interiorandexterior car styling products, navigation systems and alloy wheels);

•leisure(includingcyclesandcycleaccessoriesandroof boxes,cyclecarriers,childcarseatsandoutdoorleisure equipment).

Thecompanydifferentiatesitselffromitscompetitors throughitsnationalstoreportfolio,itsbroadproductrange, competitivepricing(achievedthroughscaleofpurchasing power),customerserviceofferingsperformedin-storeby staff(e.g.fittingandrepairservices)anditsstrongbrands (Halfordswebsite).

ReturnsbecameincreasinglysignificanttoHalfordsas theyintroduced higher value products into their prod-uctoffering(e.g.satellitenavigationsystems).Therewas agrowingpercentageofno-faultfoundreturns1 andthis startedtoimpactontheirmargins.Upuntilthebeginning oftheresearchprocess,inlinewithmanyothercompanies asevidencedinourwiderresearchproject,Halfordshadno transparentperformanceevaluationofitsreverselogistics processes.However,changingmarketcircumstancesledto theareabeinggivenanincreasinglyimportantrolewithin the company from the Board down. The company had limitedknowledgeonthecostoftheirreturnspolicyand therewasasignificantlackofvisibilityandmanagement reportinginthisarea.Storesdidnotseethemanagementof returnsasasignificantdriverintermsoftheirperformance andreturnsavoidancestrategieswerenotfullyleveraged. Therewasasignificant“lostintransit”problem(i.e.delays intrackingthroughreturnsdocumentation)andtherewas alackof focussedfaulty goodscostmanagementin the organisation.

Following on from initial involvement in the wider reverselogisticsresearchproject(September,2005),Chris Hall(HeadofQuality&CostReduction,Halfords)prepared apresentationtotheBoard(October,2005)thatfocussed on“Avision forbest-practicereturnsprocess”.Financial informationwasusedaspartofthecaseforchangeand subsequentlyapproval wasgivenfor therecruitmentof aReturnsManager(PeterCobden)inacommercialrole. Intheinitialstages,Chrisworkedverycloselywith col-leaguesfromdifferentpartsoftheorganisation(product team,distribution,operationsteam,andfinance). Impor-tantly,whilstseniormembersoftheoperationsteamhad alwaysbeenveryprotectiveofcolleagueswithinthestores operationalteams,theywere persuadedofthevalueof

1 No-faultfoundreturnsarewhereproductsarereturnedbyacustomer

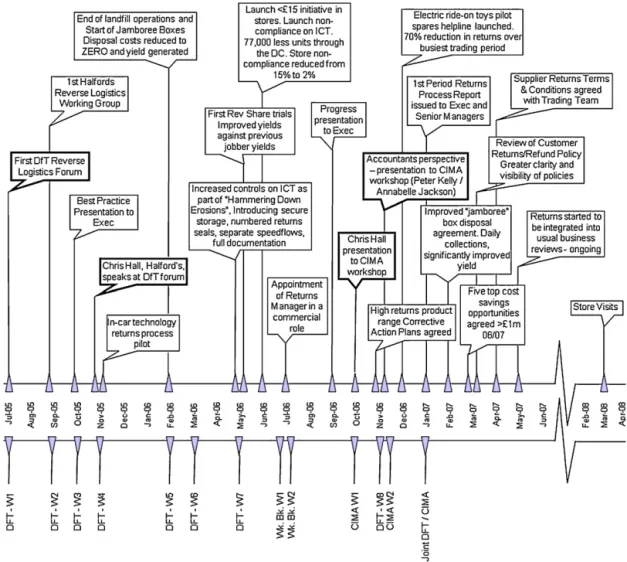

Please cite this article in press as: Cullen, J., et al., Reverse logistics in the UK retail sector: A case Fig.1. Timelineofkeyevents–abovethelineindicatesHalfordsactivities–belowthelineindicatesworkshops.Glossary:DFTW–Departmentfor Transportsponsoredworkshop;Wk.BK.W–Workbookworkshop;CIMAW–CharteredInstituteofManagementAccountantssponsoredworkshop.The boxesinboldindicateworkshopswhereHalfordsformallypresented.Theywereregularattendersattheotherworkshopstakingpartinthediscussions.

thechangesbeingsuggestedeventhoughthishad signifi-cantimpactsonstorespractices.Thetimelineforthenew returnsprocessaregiveninFig.1andthisfigurecanbe usedtotrackthesignificantchangesthattookplacewithin thereverselogisticsprocessesatHalfords.Atthesametime asthesechangesweretakingplace,aSAPR3systemwas introducedwithinHalfordsandthissystemwasusedto controlnearlyallofthefunctionswithinthecompany.

Duringtheresearchprocess,severaldiscussionstook placewithregardtothepotentialuseofqualitycosting andbalancedscorecardtypeperformancemeasuresforthe reverselogisticsprocess.Qualitycosting(DaleandWan, 2002)seemstohave particularvaluein thisareasince,

asBernonandCullen(2007)suggest,manyofthecauses

ofreturnsoccurupstreaminthesupplychain.The man-agementaccountantsandmanagersatHalfordsembraced theuseofprevention,appraisalandfailurecosts. Exam-plesof identifiedfailurecostsincludedstock write-offs, stafftimeinvolved,transportcostsassociatedwithreturns, warehousespace utilisedfor returns, triple handlingin theprocess,customerdissatisfactionandpotentiallossof

customers. Examples of expenditure on prevention includedtheissuingofclearerinstructionstobothstores andcustomers,increasedtrainingofstafftoprevent cus-tomerreturnsandincreasedtransparencythroughfurther monitoringandbehaviouralcontrols.Fig.2showsasimple

A simple example of the use of quality costing in the reverse logistics areaat Halfords:

Cost ofprevention–trainingemployees in stores inorder toreduce customer returns. Halfords trained members of their store staff to fit Satellite Navigation systems in customer's cars and show them how touse it. Thisreduced the returnrates of the products, most of which were deemed 'No Fault Found'.

Cost ofappraisal–following checklist of processes to ensure that returns are minimised. Halfords introduced processes, whereby customers were encouraged toring telephone helplines before returning particular types of product. Upon ringing a helpline a customer would betaken through a script of questions allowingthefault (perceived orreal) to be identified.

Cost ofinternal failure–costs ofwarehouse space allocated toreturns from stores that never reached the customer.

Cost ofexternal failure–costs of warehouse space allocated toreturnsfrom customers. Halfords introduced a policy of selling off unwanted products with a retail value of less than £15 in store as 'Managers Specials'. This had the effect of reducing the number of products returned to the Distribution Centre by about 40%

Please cite this article in press as: Cullen, J., et al., Reverse logistics in the UK retail sector: A case Script for stores – Key points to remember when selling Satellite Navigation Systems

Always offer free “Set-Up and Demo” service at hand over, to ensure operation of product in vehicle.

Please note that some products may need to be activated and/or fully charged by the customer before initial operation. This cannot be done in store. The customer should be offered the opportunity to return to store after they have done this for free set-up and demo if required.

Remember thatthe more comfortable the customer is with the productwhen they leave, the less likely you are to have to deal with the customer returning to the store with a problem.

The vast majority of customerreturns aredue to issues with the way that they are using the product and not dueto faulty units.

Managing the customer’s expectation of what the product can do is one of the most important parts of the sale. Do not tell the customer that the product does something that you are not sure it does as this could later form a legitimate reason for a return to store for which Halfords will receive no supplier credit. You will have to re-sell the product in store as second hand and take the loss.

Fig.3.Extractfromcustomerreturns:faultygoods:thedefinitiveguide. exampleoftheuseofqualitycostsinthereverselogistics area.

Aparticularlygoodillustrativeexampleoftheuseof qualitycostsrelatestothetreatmentofsatellitenavigation systems. The major satellite navigation system suppli-ers had previously dealt mainlywith militaryor major industrial customersand this moveintoretailwasnew tothem.Thisrequiredsignificantdiscussionsbetweenthe majorsatellitenavigationsuppliersandHalfordsaround understandingthenatureofthemarketandthenatureof theretailcustomersinterms oflackoftechnical know-how.Halfordsinitiallyuncoveredsignificantno-faultfound returns(leadingtosignificantfailure costs)becausethe customerssimplydidnotunderstandtheproduct.Aspart of the changes introduced,Halfordsincurred additional preventioncostsintheformofscripts(CoadandCullen, 2006)usedbystoresstaffand increasedexpenditurein terms oftimeinvolved intakingcustomersthroughthe installationprocess(seeFig.3).

Thesuccessof HalfordsWeFit servicefor customers, includingset-upanddemoforsatellitenavigation prod-ucts,hasalsohadapositiveeffectinreducingreturnsof manyproducts.Matt,storesmanagerintheNorth, empha-sisedthat“customersdovalueHalfordsserviceandthis helpscreate USPand maintenance andenhancement of marketshare”.Thisisinterestingbecauseanoperational changeinprocesshasledtotheintroductionofastrategic “uniquesellingpoint”whichhasbeenverysignificantin termsofthecompany’sbrandimage.Thechangesto pro-cessalsoextendedthroughthesupplychaintoencompass bothsuppliersandendcustomers.

Attentiononreturnshasbeenreinforcedsignificantly by the use of league tables of stores performance (see

Table1foranoutlineofgeneralheadingsofnewmonthly

returnsreport –introduced January2007).Chargeback to stores managersand league tables ofno-fault found returns have had a significant impact on behaviour at stores. Chargeback occurs when partsare missing from the returned products and where incorrect paperwork hasbeen completed.Previously, beforechargebackwas introduced,“storesmanagersweresendinggoodsbackas faultybecausetheyweregettingcredittoimprovetheir tradingposition”(ChrisHall).Fig.4illustratestheweekly reportthatwasintroducedandsenttostoresmanagers toemphasisethecorrect procedurestofollow and pro-videsillustrativeexamplesofthereasonwhychargeback hadbeenmadetostores.PeterCobdenemphasisedthat

Hammering Down Erosions: Weekly Update for Store Managers (Returns Procedure Update Week 19, August 2006)

You will be aware we launched phase 2, Hammering Down Erosions in week 11. In line with this, there are a weekly suite of reports being sent to Area Managers on Mondays highlighting all movements on code 80 (write off below £15), clearance of goods below £15 and code 58 (FAGO) within all stores.

Remember, it is your responsibility to make sure you clear returned or damaged stock if it’s value is below £15 and can be sold.

To help you identify the issues, a new report is now available on the store intranet (click on the information and sales information buttons and look for the report titled Product Written Off summary ) and this will allow you to check your written off stock. All Sat Nav and Audio “return errors” are being charged back to store now, so:

Check your Trading Account. The line is found under controllable erosions and is titled Sat Nav/Audio returns rejected.

To avoid you having stock charged back, ensure all relevant staff know the procedure (only Managers should be writing off).

It is also evident that some stores are not sealing cages, not separating the audio and Sat Nav and packing cages badly. FAGO is valuable stock; this is either returned to supplier or is being resold in many cases. You must seal all cages and speed flows; sealing covers all stores for any losses and will protect your store from chargeback through missing items. Sat Nav and Audio MUST be kept separate from otherreturns as they are received and stored in different locations. Drivers have been instructed to refuse cages unless they are sealed.

Don’t get caught out, ensure you and your staff earn maximum bonus by keeping erosions to a bare minimum. Some examples of return errors are shown below:

THIS STORE WAS CHARGED BACK £2,545 (COST) BECAUSE: The cage was not sealed

The stock was not in sealed speed flows Appropriate documentation was not presented

THIS STORE WAS CHARGED BACK £3700 (COST) BECAUSE: The cage was not sealed as per instruction

The stock was not in sealed speed flows

This stock was from a number of weeks, it should be sent back weekly.

Compliance is improving, but week 16 and 17 still saw £14,000 of charge backs, this will affect your Trading Account as part of the £95,000 applied in the last six weeks. During the last three weeks, 10% of the stock booked out on code 58 (FAGO) had a value of below £15, of this, 90% should have been dealt with at store.

Fig.4. Hammeringdownerosions.

“hammeringdownerosionsisanimportanttermin retail-ingaserosionsalwaysmeanalossofmoney”.

Thisimpactisinfluencedbythefactthatstores man-agersreceivedabonusbasedpartlyonstoresmarginsand attentiontothis matteris reflected in animprovement inmonthlyperformanceonrelevantfactors.Evena cou-pleoffairlyscepticalstoresmanagerswere“challenging chargebackfiguresbecauseoftheimpactonstores mar-gins”(PeterCobden).Sam,oneofthestoresmanagersin theMidlandsarea,verifiesthisbysayingthat“Iphoned through toHead Office tochallenge chargebackfigures becauseitreducedthebottomlineofthestoreand influ-encedtheleaguetables”.Matt,oneofthestoresmanagers intheNorth,saidthathisareamanagerwasparticularly keenonreducingchargebackand“askedstoresmanagers topresentreasonswhyparticularchargebackhadoccurred andhowthisissuewouldbeaddressedinthefuture”.Matt wasveryproudofhisperformance inthis areaand felt thattheintroductionofsuchcharges“focussedattention ongettingprocessessorted”.Attentiontodetailwith sup-plierswasparticularlyimportantherebecauseappropriate documentationhadtobecompletedinorderforthe com-panytogetrefundsfor faultygoodsfromthesuppliers. Non-complianceatstores withagreedreturnsprocesses fellfrom15%to2%(PeterCobden).Supplierperformance alsoformsanimportantpartofthemonthlyreturnsreport

(Table1),but theaccuracyofsuchreportsdependedon

appropriatedocumentationbeingrecordedatthestores level.

Please cite this article in press as: Cullen, J., et al., Reverse logistics in the UK retail sector: A case Table1

Newmonthlyreturnsreport.

Contents:

Page1 Contentspage

Pages2–4 CommentsontablesandgraphsincludedinP1returnsreport Page5 Faultygoods(FAGO)returnedtoDCvolumegraphYTD Page6 <£15FAGOwrittenofformarkeddowninstore Page7 Top40<£15FAGOwrittenoffinstore Page8 <£15FAGOwrittenoffinstorebysupplier

Page9 TotalFAGO2006verses2005

Page10 Supplierstop40FAGObyvalue

Page10 Travelsolutionstop10supplierswithFAGOrankedbyvalue Page12 Travelsolutionstop40FAGOarticlesrankedbyvalue Page13 Cyclingsupplierstop10withFAGOrankedbyvalue Page14 Cyclingtop40FAGOarticlesrankedbyvalue

Page15 Carenhancementtop10supplierswithFAGOrankedbyvalue Page16 Carenhancementtop40FAGOarticlesrankedbyvalue Page17 Carmaintenancetop10supplierswithFAGOrankedbyvalue Page18 Carmaintenancetop40FAGOarticlesrankedbyvalue Page19 StorereturnscomplianceinICTP5toP1

Page20 StoresreasonsforICTchargebacks

Page21 Storeschargebackonincartechnologyrankingas%ofcarenhancementsales Page22 Storestop20chargebacklocationsbyvalue

Page23 Storestop20“stocklostintransit”byvalue

Page24 Jobberandremarketeryields

Page25 RepairsturnaroundtimesbyABC(ABCcarryoutouraudiowarrantyrepairsandrefurbishmentprocesses) Page26 Incartechnologywarrantyrepairsanalysisbysupplier

Page27 YTDABCnofaultfoundanalysisbystore

Page28 ABCwarrantycarriagechargesabsorbedbyHalfords

Goodstockrecallprocesscurrentlybeingrevisedwithsupplyteam,distributionandstoreops,andareportwillbeissuedoncetheprocessisinoperation. Newbatterysupplierandcollectionprocessisimminent,andatrackingreportwillbeissuedoncetheprocessisinoperation.

Thestoresmanagerswhowereinterviewedinthe sec-ondstageoftheresearch(March,2008)wereclearlykeen todowellintheleaguetables(leaguetableinformation incorporatedintomonthlyreturnsreport–Table1).When walkingaroundthebackofficesofthestores,therewere flipchartsandnoticesonwallsshowingtheirpositionin leaguetables.Storesmanagersintwoofthestoresvisited werelesskeenonsomeofthechangessincetheprevious lackoftransparencyandlackofanychargebacktostores meantthattheyfeltlessexposed.However,despitethis lackofenthusiasm,thesemanagerswerejustasawareas theothersontheneedtoperformwellintheleaguetables sincecarryingoutthepracticemeantdoingthingsina par-ticularwayforthemanagersconcerned.Inourcasethough, comparisonsofpracticealsoreflectsupplychainpartners contributionsandtaketheconceptofplacebeyondtheone organisation.

From our observations at this later stage of the research, there was limited resistance to the changes being introduced. All of the managers involved in the secondstageoftheresearchfeltthat thechangein the reportingsystemhad significantlyinfluenced processes. Whywastheresuchlimitedresistancetochange?Chris Hall was a strong advocate of reverse logistics process changeand alsoa strongadvocate of engaging finance staffin thechangeprocess.Histotal engagementin the widerreverselogisticsproject,andtheengagementofthe accountantsfromHalfordsinthewiderreverselogistics projectworkshops/forums,meantthatthechangeswere givenlegitimacywithintheorganisation.Asalready men-tioned,thestoresmanagerswereverykeentodowellin termsofleaguetableperformance.Againlegitimacycame from engagement with the wider practice community

and recognitionby peers that the changes being made wereconsideredtobegoodpractice.Thetimelineshown inFig.1identifiesthetimesandstagesintheprocessof change where Halfords personnel made presentations tothewiderreverselogisticsworkshops/forums.Debate thatarosefromtheworkshops/industrialforumswasfed backintoprocessesatHalfordsandthisiterativeprocess was very influential in terms of changing practices at thecompany.ThequotefromChrisHall,intheresearch methodssectionabove,makesthispointveryclearlyand theappointmentofPeterCobden(July,2006),10months after the first Halfords reverse logistics working group met(seetimelineinFig.1)reinforcedtheimportanceof reverselogisticsprocesschange.

Peter Cobden hasa clearvision of the linkbetween qualitycosts,customersatisfactionandlong-termcoststo thebusiness.Hedesignedawholerangeofnewreports and used the term “data driven decisions” to describe hismanagementstyle.Thesereportscontained informa-tionderivedfrommanagementaccountingdatapresented indifferentways.PeterCobdenheldastrongconviction for theimportantuseofqualitycostsin drivingcertain behavioursandqualitycostingwasmobilisedasameans ofpromotingreturnsavoidanceandthiswasseentobean importantkeydriverforreducingreverselogisticscosts, increasingcustomersatisfactionandreducingthe environ-mentalimpactofreturns.

There has been a significant increase in reporting through the introduction of the new returns report (January,2007–seeTable1).Aswellaslookingat inter-nalcomparisonsbetweenstores,thereportalsohighlights different supplier performance and is used to initiate new processes and supplieragreements with suppliers.

Please cite this article in press as: Cullen, J., et al., Reverse logistics in the UK retail sector: A case AnnabelleJackson,oneoftheaccountingstaffinthe

pro-cess,saidthattheintroductionofSAPhadfacilitatedthe speedy analysis of what was happening in stores with regard toreturns.Shecommentedthat storesmanagers were“nowsurprisedthatshecouldidentifymovements” virtuallyassoonastheyhappened.Performance measure-mentwasseenbyPeterKelly(thefinancialcontroller)as animportant driverof culturalchangewithinthe orga-nisation with respect to attitudes relating to returned products.Differentmanagersandsupervisorswithinthe reverselogisticsprocessallseemedconvincedaboutthe positive nature of thechanges being made, although it isimportanttorecognise,asmentioned previously,that somestoresmanagersfeltlesscomfortablebecauseofthe level oftransparency. Oneofthestores managers com-mentedthatthechanges“werebeneficialtothecompany butcreatedmoreofa challengeforstores managers”.A seriesofpotentialKPIs havebeenexploredwithaview tostreamliningthereverselogisticsprocess and speed-ing up cash flow payments from suppliers relating to faulty goods.Examples of thesemeasuresinclude cycle time–returnfromstores/moneybackfromsupplier;cycle time–returnfromstores/productsentbacktosupplier; % space taken up in warehouse by returned products; faileddebitnotes/successfuldebitnotes;returnsbystores relative to trained employees; store training cost rela-tivetobenchmarkedfigure;and %no-faultfound.Fig.5

providesnarrativerelatingtoeachoftheseperformance measures.

Thewayinwhichthelanguageofmanagement account-ingwasreflectedintheeverydaylifeofmanagersinvolved inthereverselogisticsprocessprovidesfurtherevidenceof themannerinwhichaccountingcanmakecontributionsto

Halfords Sample Key Performance Indicators

Cycle time –return from stores / money back from supplier- the time taken between a store returning a product back through the supply chain and Halfords receiving a credit from the suppler for the faulty product

Cycle time –return from stores / product sent back to supplier -the time taken from the store retuning a product back through the supply chain and the Halford's DC processing it and returning it to the supplier

% space taken up in warehouse by returned products - The amount of space that returned products are taking in the DC as a percentage of the total space available (for forward and returns)

failed debit notes / successful debit notes -level of success inreceiving payment from suppliers for returns.

returns by stores relative to trained employees - The numberof returns by stores with more 'product specialists' compared with other storeswho donot have the specialism, expressed as a proportion i.e. A store with 1 product specialist, might be experiencing 100 returns a week - proportion of 100 per specialist, whereas a store with 2 trainedproduct specialists might only be experiencing 50 returns a week -proportion of 25 per specialist

store training cost relative tobenchmarked figure - The level of trainingper employee. A measure to establish that ifa store spends moreon trainingits staff, theirreturnrate islower. Expressed asa proportion toallowcomparison across stores.

% No-Fault Found - The percentage of products returned as faulty, which on later inspection are found to have no fault

Fig.5. Halfordskeyperformanceindicators.

howorganisationalmotivationstakeshapeand organisa-tionscoordinateintentionalaction(AhrensandChapman, 2007).Whilstthisnewlanguagecreatedsomechallenges forthestoresmanagers,therewasnoescapingfromthe influencethattheseKPIswerehavingoneverydaylife.The evidencewasintheformofnarrativefromthemanagers engagedintheprocessaswellasthephysicalpresenceof performanceindicatorsclearlydisplayedonnoticeboards instoresbackofficeroomswherestoresstaffcongregated. Theperformancemeasurement systemsintroduced(e.g. newreturnsreport)wereusedtohelpmanagersdotheir

job(WoutersandRoijmans,2011)butincontrasttothe

narrativeusedbyWoutersandRoijmans(2011)interms ofenablingPMS,theywerealsousedtocontrolactivities fromthecentre(i.e.leaguetables).

Aspartofthenewreverselogisticsprocesses within Halfords,adecisionwastakentoselloffatstore(where appropriatetodoso–i.e.meetingallhealthandsafety requirements)itemsunderthevalueof

£

15retailthathad beenreturned(June,2006).Previously,anyoftheseitems thathad beenreturned, wouldgothrough theHalfords returnsprocessandbeeithersenttolandfillorjobbedoff. However,aspartofthemonitoringprocess,Halfords man-agementaccountantsidentifiedthatitcostsasignificant amounttoreturneachitem,thusinmanycasesmaking thecostofthereturnhigherthanthecostpriceofthe prod-uctinthefirstinstance.Thedecisionwasthereforetaken thatanyreturnedgoodsthat arein asaleablecondition witharetailvalueoflessthan£

15 aresoldoffinstore, savingHalfordsthecostofthereturn andgeneratingat minimumacontributiontowardsthecostpurchaseprice oftheproduct.Thisactionresultedina40%reductionin returnsandreducedsignificantlytheamountoflorrymiles devotedtoreturnedproducts.Onestoresmanagerinthe Midlandsarea,James,expressed“frustrationathavingto usestoresspaceforclearance”butrecognisedtherationale forthechange.Inaddition,attentionhasbeengivento cre-atingincreasedvaluefromgoodsthatarereturnedtothe distributioncentreeitherfordispositionthroughjobbers orremarketers.Transparencyofreverselogisticsprocesses hasledtochangesinrulesandroutinesregarding differ-entdispositionroutesandthepursuitofrevenuesharing opportunities(Autry,2005).PeterCobdencommentedthat theaccountspayablestaffhadstartedadialoguewithhim nowabout“paymentsbacktosuppliers”wheregoodswere returnedwithno-faultfound.Theaccountspayablestaff arenowsaying“Iamgladthatwecantellsomebodyabout thesethings”.Thiscreatedsomenewlinesofinvestigation withsuppliersandinitiationofrootcauseanalysisinorder toestablishwhythisishappeningandwhetheritcanbe tracedbacktoparticularstoresorprocesses.Process map-pingandSAPreportsfacilitatethepursuitofthesefurther reductionsinreturns.Extensivediscussionswithsuppliers eitherataregionallevel(e.g.FarEastsuppliersconference) oratanindividuallevelledtoinitiationofvisiblereturns allowancesforFarEastsuppliers(seeFig.6)andfurther transparencythroughroutinefeedbackreportstosuppliers onthemonthlylevelofreturns.Transparencyofthereturnsprocesseshasresultedin thematterbeingdiscussedmoreopenlywithinthe orga-nisation.For example,Fig.7 illustratesa reportusedto

Please cite this article in press as: Cullen, J., et al., Reverse logistics in the UK retail sector: A case

Far East products

With regards to Far East products, intervention strategies were implemented in order to reduce the costs of direct-sourced returns by 40% over a two year period and reduce the risk of exposure to the business. The fundamental issue was that Far East suppliers naturally built the cost of returns into the cost price, however this meant there was no visibility in terms of the actual cost of these returns. An intervention strategy was put in place and followed these steps:

Introduced an agreed visible returns allowance with key direct source suppliers in the Far East.

Encouraged suppliers to improve the quality of their products through the introduction of penalties where the visible returns allowance was exceeded.

Increased the level of information exchanged between Halfords and the suppliers in order to improve customer satisfaction.

In practical terms this meant:

90% of total value was covered by 17 suppliers. Initially Halfords targeted the top 12 suppliers.

Historical data on returns by product group, coupled with quality assurance manager’s knowledge and experience, was used to arrive at Halfords desired target for returns rates.

A mechanism was introduced to:

ο agree on an acceptable returns levels for suppliers within a trading year

ο monitor and feedback to suppliers on monthly returns rates

ο suspend charge back if at end of trading year, the rolling annual returns rate was below target. If the annual returns rate was above target, then a charge back would only be applied on the amount over target.

Feedback was provided to suppliers using transparent performance management techniques such as the use of a variety of monthly graphs and tables.

As a result of these actions, the initial 12 suppliers signed up and a 40% reduction in direct -sourced returns was achieved.

Fig.6. FarEastsuppliers.

highlighttheleveloffaultygoodsonamonthlybasis(latest figuresidentifiedduringarecentfollow-upvisittoHalfords HeadOffice inNovember2011).Thereduction infaulty goodsovertheperiodfrom2007to2011isshowninthe samplefiguresandbythetrendlineinthegraph.

Also,ononeof ourvisitstothecompany,amember ofstaffapproachedChrisHallbythecoffeemachineand saidtohim,“youarecausingmea fewproblemsatthe moment”.Thiswasinrelationtothepolicyaroundreturns below

£

15 and Chris remarkedthat this wasindicative of thefact that peoplewere now openly talking about returnswhereaspreviouslyitwasnotsomethingwhich wasontheradar. Asubject thatwaspreviouslyhidden wasnowbeingtalkedaboutaroundthecoffeemachines. Bonuspaymentswerebeinginfluencedbynewreportsand exchangesoutsideoftheorganisationwereimpactedupon bynewaccountingreportsandtechniques(seeFig.6).Also, strategicandcommercialopportunitiesweremade trans-parentbynewpracticeswithintheorganisation.6. Discussion

Managerialismhasbeenidentifiedasthedrivingforce behind the diffusion of management accounting inno-vations(Muellerand Carter,2007).Quality costingfirst surfacedin1951whenJurancoveredcostofqualityinhis bookonqualitycontrol.Itthenbecamemorefashionable throughtheworkofCrosby(1979)andhassubsequently beenusedinpracticeandtalkedaboutinacademic jour-nals. It is also often referred to under the heading of strategicmanagementaccounting(Guildingetal.,2000) and,whilstlimiteduseseemstobemadeofthistechnique inpractice(Malmietal.,2004;Malmi,2010),itspotential

use was received positively by both Head Office man-agersandmanagementaccountantsatHalfords.Theuseof qualitycostingideas(i.e.identifyinglevelsoffailurecosts andthepotentiallevelofpreventioncosts)enabled man-agerstoinvestigatenewwaysofoperatingwhichimproved organisationalperformance(HenriandJourneault,2010). PresentationsbyHalford’sfinanceteamattheworkshops (seetimeline,Fig.1)highlightedpotentialpreventionand failure coststoa wider audience.This specificfocuson theconsequencesoffailure,areevidentinFig.3withthe emphasisbeingonthewaytoengagewiththecustomer inordertoreducethecostofno-faultfoundreturns.Better informedknowledgeregardingtheconsequencesof inade-quatesalespracticesintermsofcustomersatisfactionand ultimatebottomlineperformanceatbothstoresand orga-nisationallevelhasinfluencedemployeebehaviour.

New rules and routineswere developed (Burns and

Scapens,2000)aspartofthedesiretoreducethesignificant

costsassociatedwithno-faultfoundreturnsinmorehigh valueproductitems.Atthetimeoftheempirical interven-tion,itwouldseemthatthesepracticeshadbecomepart ofeverydaylifewithinHalfordsreverselogisticsprocesses (however,itisalsoimportanttorecognisetheapproachof “bitesizedchunks2”adoptedbyChrisHall).

Inthisrespect,inourcase,interventionsclearlyengaged supplychainpartnersandtooktheconceptofplacebeyond theone organisation.As illustratedinTable 1,focuson FAGO (faulty goods) incorporated comparative supplier performance and interventions with Far-East suppliers (Fig.6)formedakeypartinimprovingoutcomes. Inter-ventionstrategieswereimplementedinordertoreduce thecostofdirect-sourcedreturnsby40%overatwoyear period and reducetherisk ofexposuretothebusiness. Processimprovementstookplaceandthelongterm out-comesofsuchimprovementswereidentifiedwhichisin contrasttoWoutersandRoijmans(2011)whereimpacton performancewasnotfollowedthrough.

Theinteractionbetweenmanagementaccountingand reverselogistics,asevidencedbythepracticesinuse,was influencedbytheimplementationofSAP.Whilstthisstudy doesnotfocuspurelyoninformationtechnology,we cer-tainlyneedtoreflectonthechangingnatureofpractices inthisareaasaresultoftheimplementationofSAP.The introductionofSAPatHalfordshascertainly openedup newopportunitiesformanagementaccountants(Scapens

andJazayeri,2003)andtheirroleinthereverselogistics

processes hasbeena significantoneand a much wider onewithintheroutinesoforganisationallife(Scapensand

Jazayeri,2003).UnderstandingtheimpactoftheSAP

tech-nology and therole of themanagement accountants in organisationalchangehascertainlyrequiredtheauthorsto activelyunderstandthemanagementcontrols,technology andthecontext(DechowandMouritsen,2005).Withoutan understandingofthedevelopingrulesandroutines associ-atedwiththenewreturnsprocesses,asfacilitatedbyour interventionistresearchapproach,wewouldnothavefully

2Takinga“bitesizedchunks”approachrecognisesthat,whilst

demand-inganholisticapproachtochange,thechangeprocessneedstobedealt withinmanageablestages.

Please cite this article in press as: Cullen, J., et al., Reverse logistics in the UK retail sector: A case Fig.7. Monthlyvalueofreturns.Extractsfromamonthlyreporthighlightingreductioninvalueofreturns.FiguresobtainedduringvisittoHalfordsin November2011.Figuresareproducedonamonthly(period)basis.Thefiguresshownhighlightthesignificantreductioninreturnssincechangesintroduced. Informationonvolumesisalsoproducedbutnotshownhere.Figuresareproducedforeachperiod,butonlysampleadjustedfiguresareshownherein ordertopreserveconfidentialfigures.

appreciatedthefacilitatingrolethattheSAPsystemplayed

(BurnsandScapens,2000;SpathisandAnaniadis,2005).

TheimportantrolethatICTplayedinthechangesbeing madeareinlinewiththeimportanceplacedon informa-tiontechnologyinthereverselogisticsliterature(Bernon

andCullen,2007;Daughertyetal.,2005;Biehletal.,2007).

Thereforeinthecontextofeverydaylifeofreverse logis-ticsmanagementatHalfords,ICTplayedapartinenabling accountingtobecomeattachedtoneworthodoxies(Baxter

andChua,2008)inreverselogisticsmanagement.

The relationship between management accounting practiceandstrategising(JørgensenandMessner,2010)is evidentinthecasesincetheuseofmanagementaccounting datainfluencedbehaviourinsupportofstrategicobjectives whilstalsocreatinganewdifferentiationopportunityin terms oftheWeFitservice.Theconceptofquality cost-ing provided newnarratives (Hall,2010)for discussion that highlighted theimportance of preventionand cre-atednewprocessesforengagingwithcustomers.Ineffect, quality costing createdthe awareness tohave a better understandingandmanagement ofquality relatedcosts inthemanagementofreturns(MuellerandCarter,2007).

AssuggestedbyMalmi(2010),researcherscaninnovate somethingandleadthewayforpractitioners.Thequote fromChrisHallabouttheimportanceofthewiderreverse logisticsprojectemphasisesthewayinwhich the inter-activenatureoftheworkshops(seetimeline,Fig.1)and thecontinuousdialogueimpactedonchangeatHalfords. Equally,PeterCobdenoftenarticulatedhisstrong convic-tionfortheimportantuseofqualitycostsindrivingcertain behaviours.

In our particular case study, strategic objectives for reverselogisticsinterventionswereaimedatimproving processesandreducingcostandwearguethat practition-ers understoodtheseobjectives and wereable todraw onthemanagementaccountingsystemtoachievethese objectives.Ineffect,werecognisethecommercialand tech-nological roles of management accounting (Ahrens and

Chapman, 2007) aswellas theeconomic consequences

of adopting these management innovations (Henri and

Journeault,2010).Wewereabletodescribeand

under-standtheactivitiesthatthepractitionersperforminthe reverselogisticsprocessandhowtheydrewon manage-mentaccountingtoundertaketheseactivitiesthroughour

Please cite this article in press as: Cullen, J., et al., Reverse logistics in the UK retail sector: A case

Returns

Trading

Suppliers

Logistics

Store

Operations

Finance

Accounts Payable Commercial Finance Finance Director Financial Reporting Trading Director Buyers Quality Assurance Category Managers Accounts Customer Services Account Manager Operations Manager Supply Team DC Management Store Managers Store Colleagues Ops Director Customer Services Divisional Managers Area ManagersFig.8.Interdisciplinaryreverselogisticsmanagement.

engagementinthefielditselfratherthanjustobservingthe actionfromadistance.

Insummary,increasedtransparencythroughthenew returnsreport (Table 1)and thechanging relationships withsuppliersthatresultedfromthisincreaseddataled toimprovedorganisationalperformance.Storesmanagers atHalfordswerereceivinginformationonaregularbasis about returns and this was impacting significantly on theirbehaviour.Theimpactontheirbonuswasan impor-tantfactorhere.Noticeboardsandothervisualdisplays were placed in prominent places in the staff areas of thestoresanddiscussionsatareaandregionalmeetings dealtwiththeleaguetableinformationonaregularbasis. Organisationalmembersdrewonmanagementaccounting informationinordertocommunicateandpromoteactions related to returns management (Ahrens and Chapman,

2007;Ahrens,2008)whichwereclearlyinlinewiththe

goalsof senior management (Wallace and Pocklington,

2002;MaierandMeyer,2011).Reflectingonthereverse

logisticsproject,PeterCobdendrewupadiagram(Fig.8) showingtheorganisationalmembersengagedinthenew processandtheimportantrolethatfinancewasplayingas partofthiscomplexnetworkofpeople.Inthecase orga-nisation, management accounting information certainly madesignificantcontributionstotheways inwhichthe returns processes were managed and changed (Ahrens

andChapman,2007).Intermsoforganisationaloutcomes,

improvementsinthereverselogisticsprocesseswereseen tohaveapositiveimpactontheorganisationandbeyond. Evidenceis providedby thereductionin returnsvalues (Fig.7)andtheresultingimprovementsinthebottomline

consistentwiththe managerialistnotions ofexcellence, addingvalueandachievingeconomicoutcomes(Mueller

and Carter, 2007;Henri andJourneault,2010).Personal

outcomes and organisationaloutcomeswere influenced by the new processes and strategising outcomes were evidencedthroughthecreationofanewUSPforHalfords. Thepracticalrelevanceofaccountingresearchisbeing increasinglychallengedbyanumberofresearchers(Reiter

andWilliams,2002;Hopwood,2007;CooperandMorgan,

2008).Theadoptionofinterpretivecasestudiesin partic-ularhasbeensuggested asa wayofmakingaccounting researchmorerelevanttopractice(Cooperand Morgan, 2008).Asalreadymentioned,Granlund(inAhrensetal., 2008)suggests that there is spacein the interpretative accounting researchagenda for interventionist research andMikes(alsoinAhrensetal.,2008)suggeststhata grow-ing numberof practitioners areshowinginterest inthe findingsofinterpretiveaccountingresearch.However,in ordertoconvincepractitioners ofthevalueofengaging withsuchresearch,weneedmoreexamplesofthe out-comesfromthistypeofresearch.Previouskeyresearch papersintheaccountingareawereeitherbasedon inter-viewsandobservation(AhrensandChapman,2007)oron revisitingsomemuchearlierempiricaldatathrougha dif-ferenttheoreticallens(BaxterandChua,2008).

Aswellasbeinginterventionistresearch,thisstudyalso constitutedlongitudinalresearchinlinewithcallsforsuch researchintoreverselogistics(Autry,2005).Undertaking research through this approach enabled information to be gained which was unlikely to have been observed through other forms of qualitative enquiry. Managers

Please cite this article in press as: Cullen, J., et al., Reverse logistics in the UK retail sector: A case and employees of Halfords, as well as other members

of the reverse logistics workshops, were fully engaged because theissues being investigated wereof strategic andoperationalimportancetothem.Aninterestingaspect ofthisresearchisthattheinterventiontookplacethrough interactionsattheworkshopsinvolvingmanycompanies and the application of these thought processes within the specific case organisation. Intervention at the case levelinvolvedexplicitdialoguewiththeresearchersthat influenced final processes that were introduced to the company.ItisimportanttonotethatHalfords represen-tativesmadeanumberofpresentationsattheworkshops andreactiontothepresentationsformedpartofthe mech-anisms for change(See timeline,Fig.1).These iterative processesallowedustoarriveatarichdescriptionofthe cross-disciplinary practices at Halfords and the way in which thenew practices reflected everyday life (Lukka

andModell,2010).Wemadesuggestionsregarding“lost

in transit”classificationsthat becameveryimportant in termsofchangingpractices(i.e.lostintransitdatarelated toStoresincludedinthenewmonthlyreturnsreport–see

Table1).Pureobservationmayhaveallowedustoreflect

andcritiquesuchissues,butitwouldnothaveallowedus toinfluencepracticesrelatingtothisissue.

The research process encouraged continuous reflec-tion between the empirics and the literature (Wouters

andWilderom,2008)overtheperiodofengagementwith

thewiderworkshopsandspecificcaseorganisation mem-bers.Theuseofinterventionistresearchenabledustotalk to participantsand case organisational membersin the context and language of theirown work (Wouters and

Wilderom,2008),notjustasobserversbutalsoaspeople

who weregenuinely interestedin addressing the prob-lemsofmanagingreverselogisticsprocesses.Asaresult, wefullyengagedinnewideascentredontheemergence ofnewways ofusingmanagementaccounting informa-tiontoinformstrategicandoperationaldecision-making. Suchengagementalsoenabledustoproducean authen-tic and plausible explanation (Lukka and Modell, 2010) ofwhatwashappeninginthefieldandaddressesissues aroundvalidation.Authenticityrelatestoarich descrip-tionoftheresearchobjectwhilstplausibilityrelatestothe credibilityoftheexplanationsbeingdeveloped. Undertak-inginterventionistresearchenabledustoprovidesucha richdescriptionofwhatwashappeningandreadersshould be convinced that the researchers were actually there

(Golden-BiddleandLocke,1993)sincewewereanintegral

partoftheprocess.Thecriteriaforplausibilityrelatesto whetherthefindingsmakesenseandtheuseof interven-tionistresearchensuresthat,becauseoftheengagement oforganisationalparticipants,theoutcomesmadesense in the context of organisational issues around reverse logistics.

Intermsofourresearch,whilstrecognisingsome lim-itations,wewouldarguethatundertakinginterventionist researchhasenabledustogetabetterfeelforactual ongo-ingpracticesincewewereinstrumentalinitsnatureand form. In many ways, our approach meant that as field researchers,wewerenotjuststumblingoveraninnovative practice that is merely documented to aid its dissemi-nationamongstpractitionersandacademics(Ahrensand

Chapman, 2007). We were, through engagement with

the craft knowledge of the practitioner, informing the developmentofpracticethroughacademicdiscourse.This approach has a resonance with Inanga and Schneider

(2005)whosuggestthat“research inaccountingshould

aimatimprovingaccountingpracticeinthesamewayas thegoalofmedicalresearchistoimprovemedicalpractice” (p.239).Thisisobviouslyacontroversialissuebutour con-tentionisthatinterventioniststudiesintopractice,such asours,willallowsocialscienceresearchtobeultimately appliedforthebenefitofmanagementaccountingpractice

(Baldvinsdottiretal.,2010).Wehavepresentedourworkto

multi-disciplinarypractitionersthroughoutEurope,often jointly withcolleaguesfromHalfords,and these practi-tionershavebeenveryreceptivetotheprocessesoutlined andtheoutcomesachieved.If weasan academic com-munityaretoencourage engagementwithpractitioners

(CooperandMorgan,2008)thenitmustbeveryimportant

thatsuchworkis publishedandsubsequently critiqued by other scholars. The research excellence framework (REF)3criteriademandsthatourworkshouldhaveimpact inthe widercommunity whilstat thesametime being academically robust. Our contention is that interven-tionist research such as evidenced in this paper that consists of a joint journey of discovery (Wouters and

Roijmans,2011),isapowerfultoolforboththe

advance-mentofknowledgeandtheimprovementof accounting practice.

Throughinterventionistresearchwehaveprovidednew insights on the way in which management accounting hasengagedwithotherdisciplinestocreatepositive out-comesforanorganisation.Thisisinlinewithmanagerialist perspectiveswhichpromoteeffectivenessand efficiency

(Peters and Waterman, 1982; Reed, 2007; O’Reilly and

Reed,2010).Our observationand engagementwiththe

field revealed that the reverse logistics is a purpose-fulactivity implementedbymanagement toaddress an important organisational problem. It was implemented inresponsetoinherentinefficienciesinthereturns pro-cess and as a result its rationales can be seen mainly as for the purposes of achieving effectiveness and effi-ciency.Theconceptofqualitycostingwasusedtoimprove customerserviceandreduceoverallcosts.Previous empir-ical evidence on quality costing is mainly limited to ratherdatedstudiesaroundmanufacturing.CreatingaUSP around“We-Fit”acknowledgesaroleforaccountingthat goesbeyondscorekeepingandintothestrategic manage-mentarea.Accountingbecameanintegralpartofframing strategy in the sense that accounting devices became strategicratherthanjustbeinglimitedtoimplementation

(SkærbækandTryggestad,2010).Performancemeasures

wentacrossorganisationalboundariesandwereusedto create newrelationships withsuppliersand customers. Newdialoguesopenedupbetweenaccountantsand man-agers from other disciplines. The range of disciplines engagedinthereverselogisticsprocessesarecapturedin

Fig.8.

3 TheREFisthesystemforassessingthequalityofresearchinUKhigher